South America Home Textiles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.09 Billion |

| Market Size (2026) | USD 7.54 Billion |

| Market Size (2031) | USD 9.87 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

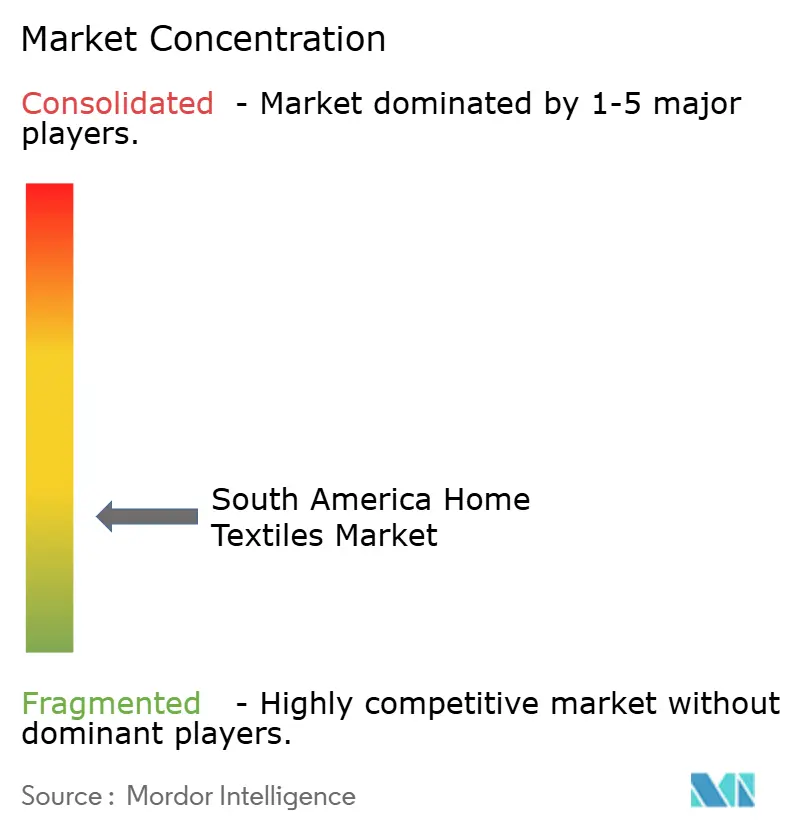

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Home Textiles Market Analysis by Mordor Intelligence

The South America Home Textiles Market size was valued at USD 7.09 billion in 2025 and is estimated to grow from USD 7.54 billion in 2026 to reach USD 9.87 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031). Market momentum reflects a dual-speed pattern in which Brazil anchors supply and scale while fast-modernizing neighbors capture gains in channels and midscale hospitality. Brazil accounts for 52.63% of regional demand, supported by a highly integrated cotton-to-retail system with traceability and Better Cotton protocols embedded at farm and mill levels, thereby reducing sourcing risk and compressing procurement lead times for institutional buyers [1]Better Cotton, “Better Cotton Renews Standard Recognition Agreement in Brazil,” Better Cotton, bettercotton.org. As traceability expands, retailers and hospitality operators can standardize quality specifications and audit supply chain lineage, favoring certified suppliers that meet cross-border compliance requirements, such as EU and U.S. entry requirements. Competitive tension persists as synthetic fibers broaden addressable price tiers for towels, bedding, and décor while e-commerce onboarding improves access to differentiated assortments and value-priced imports. The South America home textiles market continues to evolve around supply credibility, channel digitization, and procurement standardization as the core levers shaping both residential and institutional demand.

Key Report Takeaways

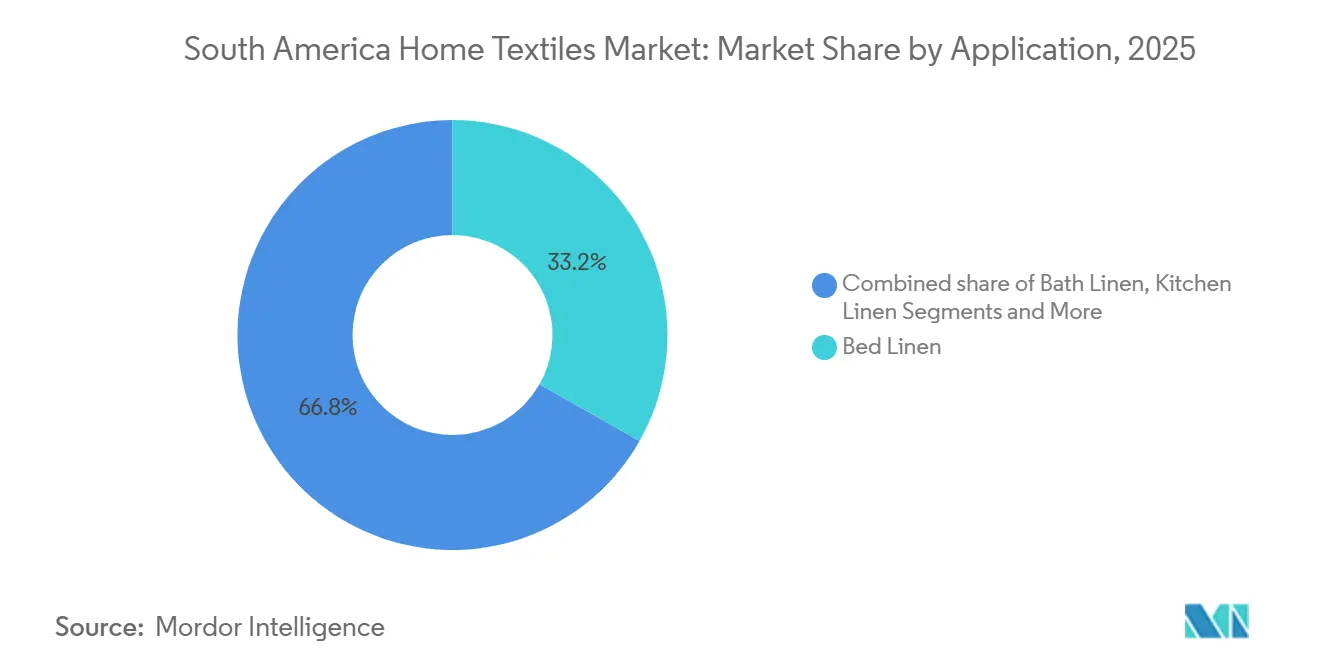

- By application, bed linen led with 33.28% of the South America home textiles market size in 2025, while bath linen is forecast to expand at a 7.21% CAGR through 2031.

- By material, cotton held 66.82% of the South America home textiles market share in 2025, and synthetic fibers are projected to grow at 5.89% annually during 2026–2031.

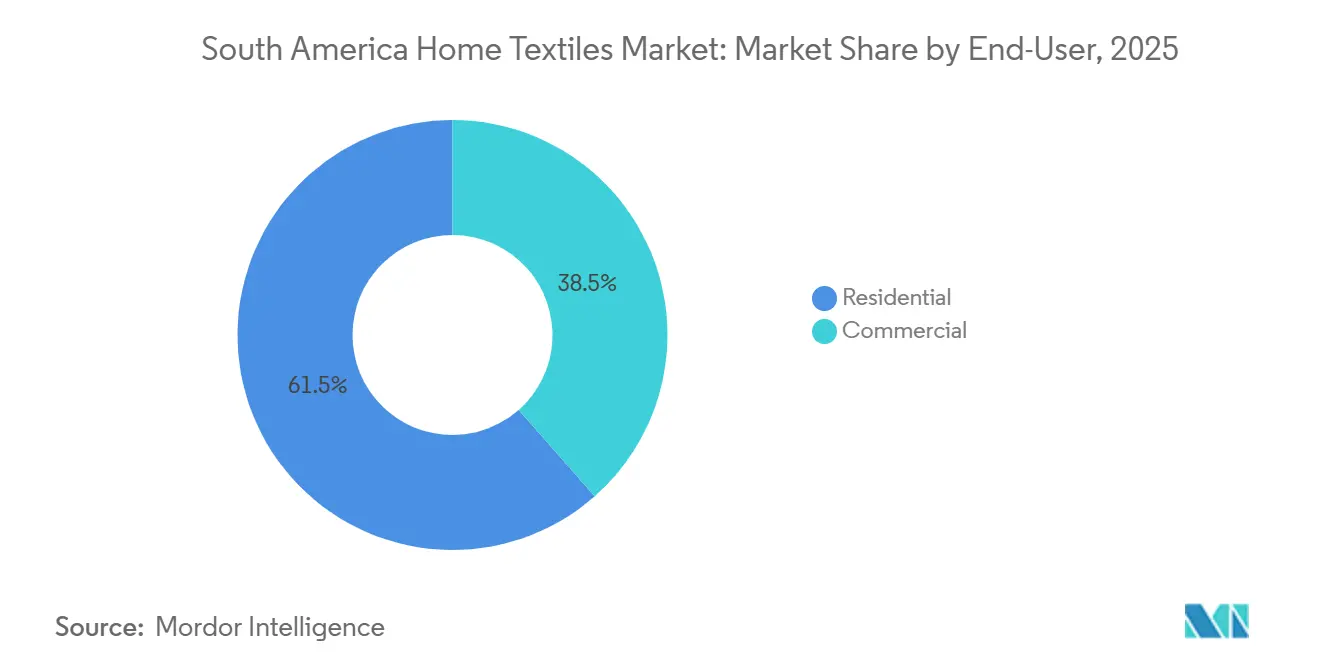

- By end-user, residential accounted for 61.45% of the South America home textiles market share in 2025, and commercial end-users are expected to advance at a 6.47% CAGR through 2031.

- By distribution channel, specialty stores commanded 46.17% of the South America home textiles market share in 2025, while online is projected to post a 10.08% CAGR to 2031.

- By geography, Brazil held 52.63% of the South America home textiles market share in 2025, and Chile is projected to record a 6.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Home Textiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer spending on renovation & home décor | +1.2% | Brazil, Chile, Peru (tourism-led income gains) | Medium term (2-4 years) |

| Hospitality construction pipeline driving institutional linen demand | +1.4% | Brazil core, spill-over to Andean corridor (Peru, Colombia) | Short term (≤ 2 years) |

| Rapid e-commerce and DTC adoption are increasing category penetration | +1.8% | Global, with Argentina/Brazil leading at 390% and 29% YoY e-commerce growth | Medium term (2-4 years) |

| Synthetic fibers' price-performance expanding addressable demand | +0.9% | National, with early gains in São Paulo, the Blumenau industrial clusters | Long term (≥ 4 years) |

| IKEA/Falabella omni-entry catalyzing premium merchandising and awareness | +0.6% | Chile, Peru, Colombia (metro cities) | Medium term (2-4 years) |

| Brazil's Better Cotton/ABR supply enables traceable, local sourcing | +0.4% | Brazil (83% of cotton certified), spillover to Mercosur retail | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Spending on Renovation & Home Décor

Spending on home upgrades and décor cycles is rising in key metros and tourism corridors, which supports steady volume lifts in core categories such as bedding, towels, and decorative items. In markets like Brazil and Chile, consumers funnel renovation budgets into materials that balance durability with comfort, which keeps higher thread counts and stable weave constructions at the center of the assortment. Demand is reinforced when mortgage costs ease and when tourism-driven economic growth improves local job creation, helping middle-income households refresh towels and bed sets more frequently. Retailers that link furniture and textiles within the same path-to-purchase increase attachment rates, and compact showroom formats paired with unified stock systems remove friction during discovery and fulfillment. As the South America home textiles market captures these upgrades, brands that focus on certified cotton and easy-care synthetics protect their share by aligning assortment depth and quality marks with how households are actually shopping across price bands.

Hospitality Construction Pipeline Driving Institutional Linen Demand

Institutional procurement is trending higher as hotel development, renovation, and brand conversions expand standardized linen packages in upper midscale and upscale tiers. Operators prioritize quick-dry towels and wrinkle-resistant bed runners to reduce laundry cycles and optimize turnaround, which adds momentum to polyester- and blended-construction products in back-of-house operations. Certified cotton and traceable inputs remain central to guest-facing items such as sheets and pillowcases, especially where brand standards reference OEKO-TEX or similar specifications linked to supplier audits. Domestic suppliers with proven hospitality lines and distribution coverage strengthen their bids by demonstrating product grammage consistency and lifecycle cost transparency, supported by in-house testing and quality documentation. The South America home textiles market benefits from this mix of durability and compliance as developers and operators institutionalize replenishment schedules across towels, bed linen, and tabletop textiles.

Rapid E-commerce and DTC Adoption Increasing Category Penetration

Digital channels are raising category penetration as shoppers embrace mobile-first discovery, targeted promotions, and simplified fulfillment options. Omnichannel leaders have expanded digital share through unified inventory, improved service levels, and last-mile partnerships that compress delivery windows while supporting options such as in-store pickup. Direct-to-consumer initiatives from legacy brands complement marketplace strategies by creating predictable flows of hero SKUs in bed and bath that fit envelope sizes for parcel-friendly shipping. As privacy and data rules mature, domestic players that invest in transparent user-consent frameworks and stable checkout experiences see higher retention in a category where replenishment is frequent. The South American home textiles market is leveraging these capabilities to curate higher-margin private-label and certification-backed ranges that travel well across digital shelves.

Synthetic Fibers' Price-Performance Expanding Addressable Demand

Polyester and smart polyamide solutions continue to expand the useful price-performance envelope for mainstream towels, bedding accessories, and decorative rounds. Suppliers are investing in domestic capacity upgrades and process innovation to improve energy efficiency and scale smart-yarn formulations that maintain performance in institutional wash cycles. Brand owners that integrate recycled polyester into pillow and accessory lines are also reinforcing sustainability credentials, which supports sell-through in retailers that have public targets for circular materials and traceable inputs. Over time, synthetics reduce housekeeping costs in hospitality due to faster drying and lower wrinkle rates, while high-thread-count cotton holds its role in premium sleep experiences. Yet volatility persists: Q2 2025 saw polyester filament yarn decline 10.9 percent in North America and 5.1 percent in China due to oversupply and subdued downstream demand, reminding stakeholders that input-cost advantages can reverse swiftly when feedstock dynamics shift [2]MSC, “Panama Canal Surcharge Trade from Asia to US East Coast and Gulf,” MSC, msc.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asian import penetration is compressing domestic margins | -1.6% | Brazil (30% volume surge), Argentina (70% import market share) | Short term (≤ 2 years) |

| Macroeconomic volatility in key markets (e.g., Argentina) is dampening demand | -1.3% | Argentina core, contagion risk to Uruguay, Paraguay | Medium term (2-4 years) |

| Panama Canal draft limits elevating logistics cost to Pacific SA | -0.5% | Peru, Ecuador, Chile (Pacific-facing economies) | Short term (≤ 2 years) |

| Financial distress among local champions is disrupting supply stability | -0.7% | Brazil (Springs Global, Karsten, under-going-concern review) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Asian Import Penetration Compressing Domestic Margins

Asian imports have raised competitive pressure on domestic suppliers, compressing gross margins and narrowing the window for price increases in a still price-sensitive category. The effect is concentrated in towels, mid-thread-count bed sheets, and basic decorative accessories, where landed prices are decisive. Retailers diversify vendor pools to maintain in-stock positions as local champions rebalance capacity and prioritize higher-margin SKUs. Judicial reorganizations among legacy players underscore the stress on balance sheets and operations as imported alternatives take share in value bands. The South America home textiles market shows that certification-backed ranges retain pricing power, while non-certified commodities are most exposed to import-driven price floors.

Macroeconomic Volatility in Key Markets (e.g., Argentina) Dampening Demand

Macroeconomic instability has weakened domestic consumption in some markets and delayed discretionary textile upgrades. Producers facing currency swings and changing tariff regimes have experienced higher uncertainty around plant utilization and procurement planning. Retailers recalibrate expansion plans and tilt investment to logistics and digital integration while monitoring household liquidity and inflation trends. Cross-border shopping options can siphon spend away from local shelves when trade rules shift, which fosters deflationary episodes in parts of the assortment. The South American home textiles market remains resilient, with hospitality and compliant private labels stabilizing baseline demand and reinforcing value communication at the point of sale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bath Linen Propels Growth Amid Institutional Refresh Cycles

Bed linen commands 33.28% of the category in 2025, while bath linen is set to expand at a 7.21% CAGR during 2026–2031 as operators and households replace towels more frequently to match hygiene and turnaround needs. Within hospitality, buyers prioritize quick-dry, high-absorption towels with consistent grammage that can withstand repeated wash cycles, thereby concentrating demand on proven constructions in cotton-rich and polyester-rich weaves. The South America home textiles market aligns to these specs through balanced assortments and SKUs that map to standard property counts for midscale and upper midscale hotels. Suppliers supporting this cadence with test reports and durability warranties can stabilize volumes across seasonal fluctuations. As the replacement cadence widens between bed sets and bath items, towels gain higher visibility in promotional calendars and specification documents.

Institutional procurement linked to tourism projects and property conversions reinforces volume on bath rounds, while residential shoppers maintain interest in elevated hand-feel and colorfastness in premium towels. The South American home textiles market uses certified cotton in guest-facing bath assortments and performance synthetics for back-of-house utility items to balance the guest experience with operating costs. Kitchen linen and upholstery grow more slowly due to longer replacement cycles and lower cross-border assortment variety in parcel-constrained shipping. Niche demand for carpets and area rugs persists in premium residential and hospitality interiors as part of a layered floor-covering approach. Vendors that align packaging, labeling, and compliance for hospitality audits maintain stronger tender outcomes.

By Material: Synthetic Fibers Gain Share Amid Cotton Cost Inflation

Cotton retains a 66.82% share in 2025, supported by Brazil’s scale and certification footprint, which stabilizes fiber availability and reinforces traceability credentials in bed and bath programs [3]USDA Foreign Agricultural Service, “Cotton and Products Annual - Brazil,” USDA FAS, apps.fas.usda.gov. Polyester and smart polyamide solutions continue to grow at a 5.89% CAGR as brands blend performance and cost efficiency in towels, pillows, and accessories. The South America home textiles market benefits from domestic fiber and yarn innovation agendas that pursue energy efficiency and material recycling without compromising lifecycle performance. Retailers that disclose sustainability criteria and expand recycled content in their private labels receive a favorable shopper response in curated online and in-store displays. Vendors that present clear fiber provenance and performance documentation win more placements at the shelf and in hospitality RFQs.

Linen holds a premium niche in duvet covers and decorative cushions due to its tactile and climatic properties, yet its share remains low due to cost and limited regional cultivation. Other natural fibers, including wool, hemp, silk, jute, and bamboo, remain concentrated in boutique channels and curated assortments that appeal to décor enthusiasts. The South America home textiles industry integrates these niche fibers selectively where price acceptance exists, while the volume core remains in certified cotton and synthetics that meet mainstream performance requirements. As certification and circularity targets tighten, blended constructions with recycled inputs will continue to scale, especially in non-guest-facing hospitality items. Suppliers continue to balance the fiber mix, hand-feel, and cost to maintain margin discipline without eroding the end-user experience.

By End-User: Commercial Segment Outpaces Residential Growth

Residential users held 61.45% in 2025, while commercial demand is projected to advance at a 6.47% CAGR, reflecting the steady institutional cadence of hotel openings, renovations, and standardized brand programs. Commercial procurement values compliance, lifecycle durability, and speed of replenishment, which sustain demand for standard SKUs in towels, bed linen, and tabletop textiles. The South American home textiles market positions certified cotton and durable synthetics to meet property-level specs that require repeatable performance across laundry cycles. Retailers and distributors that serve both channels hedge inventory across product families to reduce stockouts and to ride seasonal peaks. Residential demand continues to bifurcate, with premium households seeking certified cotton upgrades while value-seeking shoppers rely on promotional cycles and marketplace options.

In commercial settings, vendors with proven hospitality lines and national coverage secure long-term replenishment contracts, which smooth cash flows versus retail seasonality. The South American home textiles market for commercial applications is expected to grow with ongoing retail and tourism investments that lock in baseline offtake for bath and bed SKUs. Residential volumes remain stable when omnichannel tools improve availability and when curated planograms simplify choices within tight price bands. Digital capabilities such as click-and-collect and unified stock views support loyalty in a category where replenishment is frequent. Over time, a clearer split across commercial and residential needs allows suppliers to tailor fiber blends and weave density to different durability thresholds.

By Distribution Channel: Online Sprints Past Specialty Stores

Specialty stores accounted for 46.17% in 2025 as standalone brands and department stores used curated layouts and cross-category bundles to drive larger baskets. Online is the fastest-growing channel, projected to grow at a 10.08% CAGR to 2031, supported by mobile-first discovery, unified inventory, and improved last-mile fulfillment. The South American home textiles market sees incumbents defend their share by linking apps, stores, and distribution hubs to streamline pick, pack, and delivery operations at scale. Meanwhile, supermarkets and home centers hold a share in select missions such as impulse or convenience purchases that complement planned purchases. Certified assortments and sustainability storytelling also carry weight online, where filterable attributes and badges can surface premium picks more easily than on crowded shelves.

Omnichannel logistics has become central to conversion as retailers improve speed and predictability in delivery promises. The South America home textiles market share moving through digital channels will continue to expand, where convenient returns and reliable delivery build trust. For suppliers and marketplaces, clarity of product content and standardized size, color, and construction descriptors reduce return rates in soft goods. Specialty stores maintain their role in guided selling for high-touch categories such as premium bed linen, pillows, and coordinated sets. Over the forecast horizon, balanced investment across online tools and refined in-store experiences will shape the leading retail formats in this category.

Geography Analysis

Brazil leads with 52.63% of regional demand in 2025, underpinned by vertically integrated cotton-to-retail infrastructure, a high certification footprint, and national retail systems that scale omnichannel fulfillment. Better Cotton’s long-standing collaboration in Brazil and the ABR protocol deliver audited field practices and growing traceability coverage, which underpins premium and export-ready ranges across retailers and hospitality buyers. USDA confirms Brazil’s export scale and production strength, which enhances domestic conversion economics for cotton-rich bed-and-bath programs. Retailers with strong digital penetration continue to invest in distribution and data tools that lift attach rates and shorten lead times for replenishment. The South America home textiles market in Brazil gains resilience through this combination of certified inputs and omnichannel retail execution.

Chile is set to post one of the fastest growth rates through 2031 as local brands expand specialty formats and elevate décor merchandising. Department store operators are on multi-year investment cycles that refresh existing stores and add new openings in key corridors, which supports steady offtake in bed and bath. The South America home textiles market in Chile is also benefiting from curated private labels and higher visibility for premium construction details in displays and content that build category knowledge. Where imports are essential for synthetics and specific program needs, disciplined sourcing and standardized specs keep service levels intact. Over time, a broader multi-format retail base helps stabilize category volumes across seasonal peaks.

Peru and Colombia benefit from ongoing tourism and retail investments that anchor hotel development and store upgrades. The South America home textiles market in these countries reflects a healthy mix of institutional demand for standardized linens and residential demand for higher-quality cotton and blended towels and bed sets. Regional trade programs and industry promotion groups have expanded B2B outreach across the Andean corridor, supporting cross-border sourcing and supplier discovery [4]Texbrasil, “Brazil Stands Out at Colombiatex 2025,” Texbrasil, texbrasil.com.br. Ecuador and the Rest of South America maintain mid-single-digit contributions, where retail modernization and logistics improvements allow assortments to broaden. Across the region, compliance, logistics reliability, and balanced fiber mix remain the decisive factors behind steady growth.

Competitive Landscape

The category is highly fragmented and has a low concentration profile, reflected in the small shares held by individual leaders relative to the total addressable base. A set of domestic champions has undergone judicial reorganizations and asset optimization as part of a multi-year financial turnaround, reshaping vendor rosters and increasing the role of compliant imports in covering planograms. Retailers with robust digital and logistics platforms hold a competitive edge because they can plug certified suppliers into unified stock models, reducing out-of-stocks and boosting conversion rates. The South America home textiles market shows a clear divide between certified, traceable ranges that secure premium placements and compliance-heavy contracts, and price-led commodities that compete primarily on landed cost.

Strategic moves emphasize certification, traceability, and speed-to-shelf capabilities that support both retail and hospitality. Retailers deepen programs that validate supplier practices across environmental and social criteria and extend traceability pilots to a larger share of domestic partners. Industry promotion platforms report higher B2B deal activity in regional trade events, indicating that certified Brazilian fabric and home textile suppliers are expanding their reach into neighboring markets. Logistics costs, especially through the Panama Canal corridor, remain watch items as carriers keep surcharges in place, nudging some buyers to explore nearshore or alternative routings where quality and compliance align.

Operational discipline is now a key differentiator as brands and mills that maintain QA, testing, and audit readiness have better access to institutional tenders and premium retail slots. The South America home textiles market rewards manufacturers that balance certified cotton with performance synthetics to meet specific wash, dry, and lifecycle criteria for each end-use. Restructuring among legacy players opens space for nimble suppliers to win shelf space and long-term replenishment contracts as retailers diversify risk. Retailers continue to invest in digital tools and distribution capacity to sustain speed and accuracy in fulfillment, which remains central in this high-turnover category. Over time, scale, certification signaling, and omnichannel execution are set to define the leaders in both residential and commercial demand pools.

South America Home Textiles Industry Leaders

Springs Global Participações S.A.

Karsten S.A.

Döhler S.A.

Buddemeyer S.A.

Altenburg

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The Better Cotton Initiative's Brazil Cotton Multistakeholder Dialogue established a permanent governance structure (a Board of Directors with three representatives per segment: growers, traders, textile industry, retailers, and civil society) and announced a 2026 public webinar on traceability. The dialogue, launched in March 2025, aims to enhance collaboration and address challenges within Brazil's cotton sector.

- November 2025: Better Cotton Initiative surpassed 50% of BCI Cotton volumes traced in global fashion and textile supply chains, with over 23,000 metric tonnes traced from gins to retailers. Brazil and Australia were added to traceability coverage in 2025, expanding originating countries to 15.

South America Home Textiles Market Report Scope

This report aims to provide a detailed analysis of the home textile industry in South America. It focuses on market dynamics, technological trends, and insights into various materials, applications, and process types. It also analyzes the major players and the competitive landscape in the South American home textile industry. The South American home Textiles Market is segmented by Application (Bed Linen, Bath linen, Kitchen linen, Upholstery and Carpets & Area Rugs), By Material (Cotton, Linen, Synthetic Fibres, and Other Materials (Wool, Hemp, Silk, Jute, Bamboo)), By End-User (Residential and Commercial), By Distribution Channel (Offline and Online), and by Geography (Brazil, Argentina, Colombia, Chile, Peru, Ecuador, and Rest of South America). The report offers market size and forecast in value (USD million) for all the above segments.

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Carpets & Area Rugs |

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

| Residential |

| Commercial |

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Ecuador |

| Rest of South America |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Carpets & Area Rugs | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Offline Channels | ||

| Online | ||

| By Geography | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Ecuador | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the South America home textiles market in 2025, and how fast will it grow to 2031?

The South America home textiles market size is USD 7.09 billion in 2025, and it is projected to reach USD 9.87 billion by 2031 at a 6.11% CAGR.

Which country accounted for the largest share within South America in 2025?

Brazil holds 52.63% of regional demand, supported by a vertically integrated cotton-to-retail system and high certification penetration that improves supply reliability.

Which application category is growing fastest through 2031?

Bath linen is the fastest-growing application, forecast to expand at a 7.21% CAGR as replacement cycles accelerate in hospitality and wellness-oriented households.

How are materials shifting within the category?

Cotton retains a 66.82% share due to Brazil’s scale and traceability, while synthetic fibers are growing at a 5.89% CAGR on the strength of quick-dry and wrinkle-resistance attributes that cut operating costs for hospitality.

Which channels are set to outperform in the next five years?

Online is projected to grow at a 10.08% CAGR, outpacing specialty stores and other offline formats, with unified inventory and faster last-mile lift conversion.

What operational risks could pressure margins for suppliers?

Import penetration in value bands and higher logistics costs on Panama Canal routes are key risks, which suppliers mitigate with certification-backed assortments, diversified sourcing, and omnichannel replenishment models.

Page last updated on: