Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

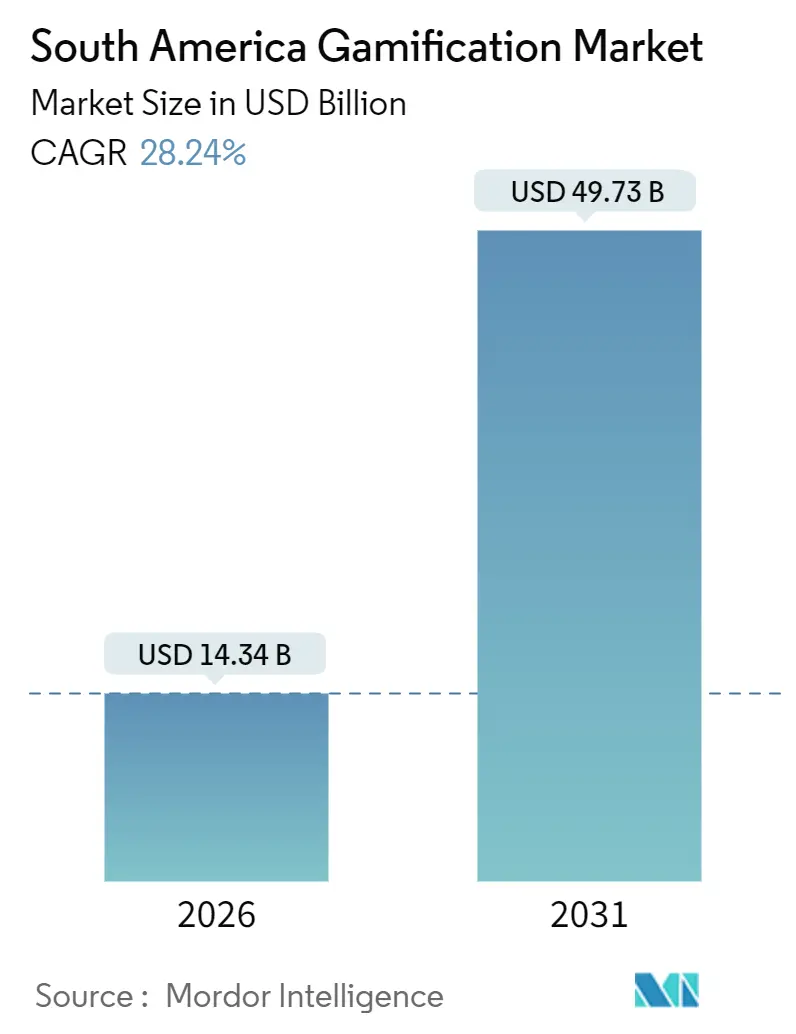

| Market Size (2026) | USD 14.34 Billion |

| Market Size (2031) | USD 49.73 Billion |

| Growth Rate (2026 - 2031) | 28.24% CAGR |

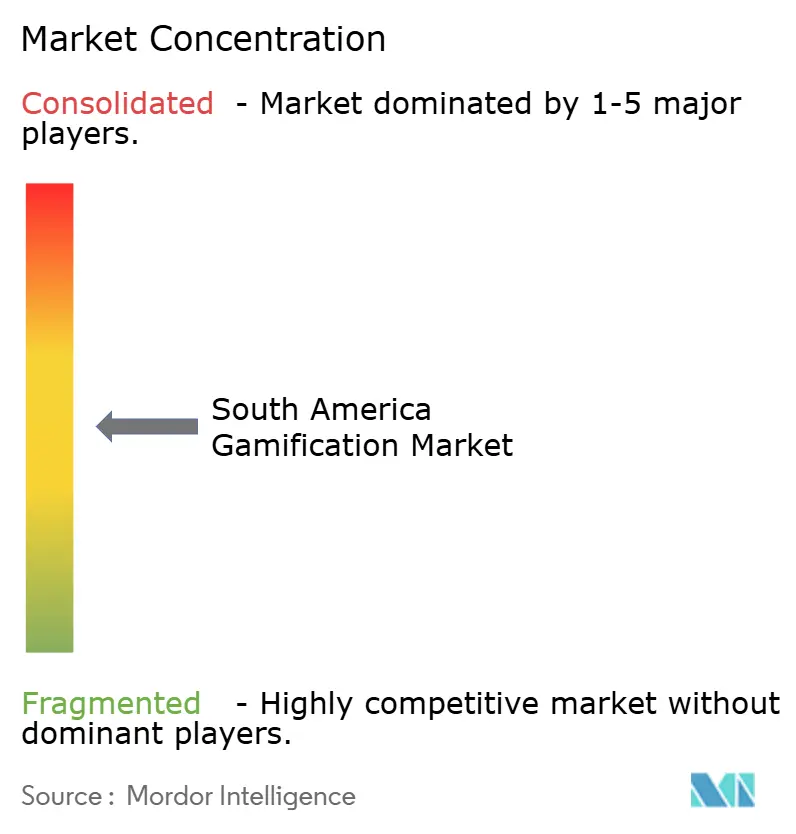

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Gamification Market Analysis by Mordor Intelligence

The South America gamification market size stood at USD 14.34 billion in 2026 and is projected to reach USD 49.73 billion by 2031, reflecting a robust 28.24% CAGR over the forecast period. Rapid cloud-native adoption, instant-payment rails that settle transactions in seconds, and rising enterprise budgets for interactive experiences are amplifying demand across consumer and workplace touchpoints. Hyperscalers have earmarked more than USD 10 billion for regional data center capacity to shrink latency for multiplayer and real-time reward mechanics. Instant-payment schemes such as Brazil’s Pix create new margin headroom for loyalty programs by reducing merchant costs, while low-code toolkits let non-technical teams build gamified screens in weeks rather than quarters. As data-residency barriers ease and mobile connectivity surpasses 5G thresholds, vendors can offer always-on leaderboards, surprise-and-delight cashback, and context-aware challenges that refresh engagement cycles.

Key Report Takeaways

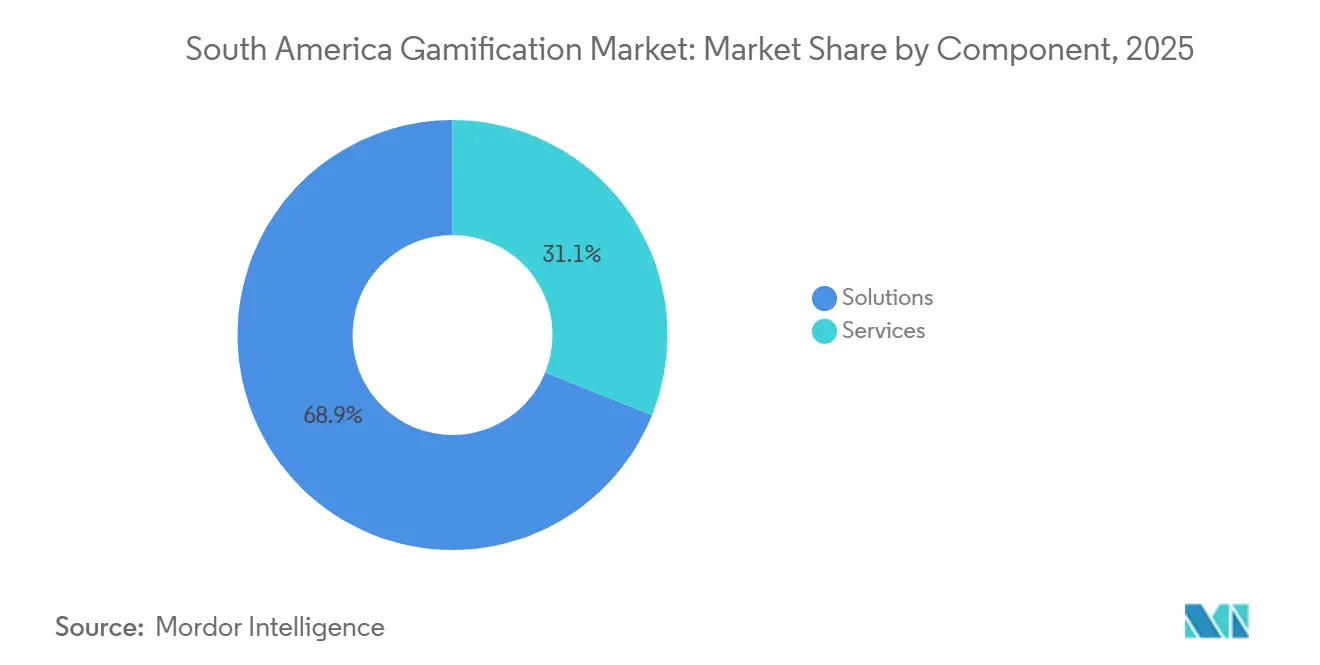

- By component, solutions held 68.91% revenue share in 2025, while services are projected to expand at a 28.43% CAGR through 2031.

- By gamification type, points and rewards accounted for 42.33% of the South America gamification market share in 2025, whereas leaderboards are forecast to grow at a 29.26% CAGR through 2031.

- By deployment mode, cloud deployments captured 73.42% of the South America gamification market share in 2025 and are advancing at a 28.47% CAGR over the forecast period.

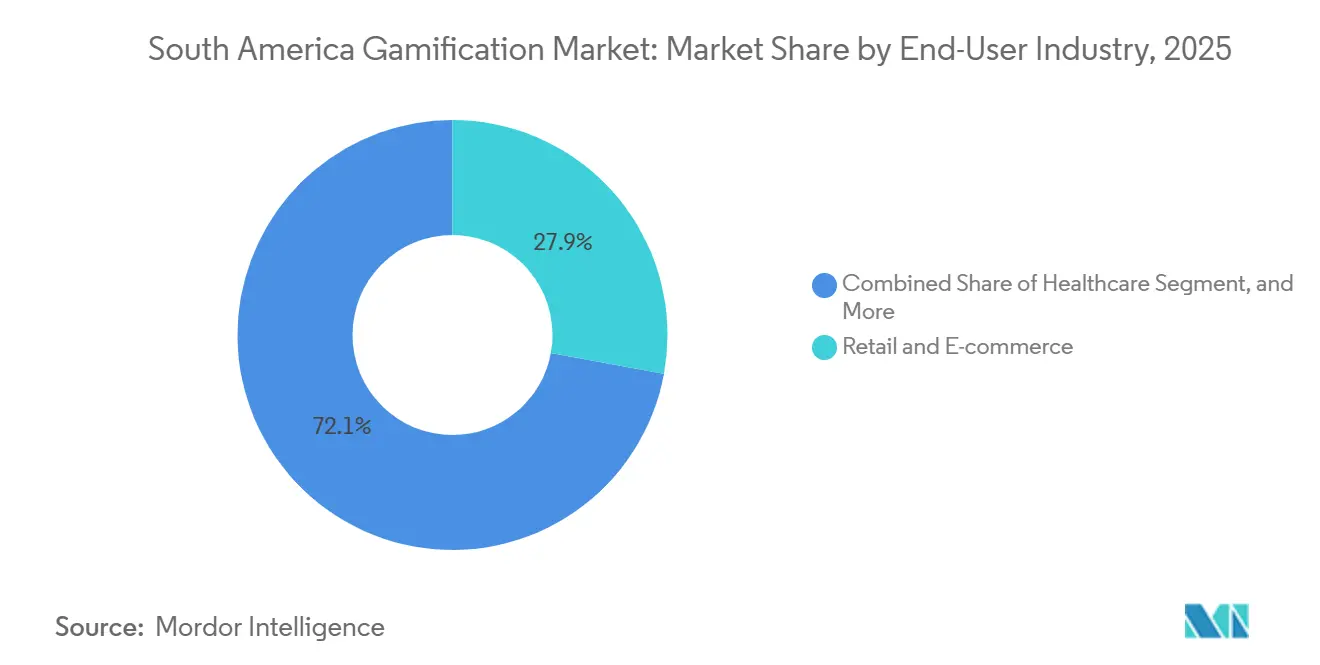

- By end-user industry, retail and e-commerce led with 27.89% revenue share in 2025, while healthcare is poised to grow at a 29.83% CAGR through 2031.

- By enterprise size, large enterprises accounted for 62.31% of the South America gamification market share in 2025, but small and medium enterprises are set to register a 28.51% CAGR to 2031.

- By geography, Brazil retained a 49.78% share in 2025, whereas Colombia is expected to record the fastest CAGR of 29.11% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Gamification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Smartphone Penetration and 5G Roll-outs | +4.8% | Brazil, Colombia, Chile; spillover to Argentina | Medium term (2–4 years) |

| Expansion of Digital Wallets and Embedded Payments | +5.2% | Brazil (Pix dominance), Colombia, Argentina | Short term (≤2 years) |

| Growing Corporate E-Learning Budgets Post-COVID-19 | +3.9% | Brazil, Mexico, Argentina; regional enterprises | Medium term (2–4 years) |

| Retail Loyalty Program Revamps Leveraging Gamification | +3.1% | Brazil, Colombia; urban centers across South America | Short term (≤2 years) |

| Esports Sponsorship Spill-Over into Brand Engagement | +2.7% | Brazil, Argentina, Chile | Medium term (2–4 years) |

| Rise of Low-Code Platforms Democratising Gamified Apps | +4.5% | Global; early gains in São Paulo, Santiago, Buenos Aires | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone Penetration and 5G Roll-outs

Brazil surpassed 188 million mobile internet users in 2025, and operators now deliver sub-50-millisecond latency in urban corridors. Similar roll-outs in Colombia and Chile unlock real-time leaderboards and augmented-reality hunts that previously stalled on congested 4G links. Vendors have seized the opportunity to offer mobile-first apps that gamify ride-hailing, grocery delivery, and rural agricultural advisory services. These experiences expand access beyond major cities, bringing interactive crop-management missions to farmers in interior states. As 5G coverage expands from population centers to secondary cities, daily active user counts are expected to compound, reinforcing the growth trajectory of the South America gamification market.[1]GSMA, “The Mobile Economy Latin America 2025,” gsma.com

Expansion of Digital Wallets and Embedded Payments

Pix processed 63 billion transactions in 2024 at an average merchant fee of 0.22%, a tenth of the legacy card rails' average merchant fee. Fintechs embed gamification directly into payment flows, delivering cashback chests or spin-to-win coupons immediately after checkout. Nubank’s in-app game reveals variable rewards when users pay bills, a frictionless mechanic now replicated by PicPay, Banco Económico, and Carrefour.[2]Flourish Fi, “Why Financial Health Is a Powerful Growth Engine for Banks and Fintechs,” flourishfi.com The model dismantles cumbersome point-tracking portals, elevating repeat purchase rates and driving wallet stickiness. As Colombia, Argentina, and Chile scale comparable instant-payment networks, embedded reward loops will propagate region-wide, lifting revenue intensity for platform owners.

Growing Corporate E-Learning Budgets Post COVID-19

Hybrid work norms sustained elevated training outlays, with Brazil’s enterprises channeling ever-larger shares to digital courses that replace seminar travel. Gamified modules shorten onboarding and improve knowledge retention by overlaying badges, level-ups, and peer challenges on conventional content. SENAC’s Orango platform issues verifiable credentials that sync with HR systems, enabling managers to link badge accrual to performance reviews.[3]SENAC, “Orango Gamified Learning Platform Launch,” senac.br Pharmaceutical and telecom firms extending Play2Sell’s scenario-based sales games reported double-digit productivity gains within one quarter. The success narrative is inspiring neighboring markets, pushing the South America gamification market deeper into corporate budgets.

Rise of Low-Code Platforms Democratising Gamified Apps

OutSystems and Microsoft Power Platform local partners enable non-coders to drag-and-drop reward mechanics, shrinking build times by 60% and development costs by 40%. Templates arrive pre-translated for Portuguese and Spanish, integrate with Pix and Mercado Pago, and include LGPD-compliant consent flows. Small retailers deploy cashier leaderboards that celebrate upsell wins, while logistics fleets gamify driver fuel efficiency through daily challenges. However, citizen-developer enthusiasm occasionally outpaces security rigor, prompting Brazil’s data-protection regulator to urge mandatory audits for low-code outputs that process personal data. The tension underlines why professional services remain pivotal even as tooling lowers the technical bar.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short-Term User Fatigue with Points-Based Mechanics | -2.3% | Urban Brazil, Argentina, Chile; early-adopter segments | Short term (≤2 years) |

| Scarcity of Localised Content in Spanish and Portuguese | -1.8% | Argentina, Colombia, Peru; non-Brazilian markets | Medium term (2–4 years) |

| Data-Privacy Compliance Costs (LGPD, Habeas Data) | -2.9% | Brazil (LGPD), Argentina (Habeas Data), regional cross-border | Long term (≥4 years) |

| Fragmented UX Standards Hindering Cross-Platform Plays | -1.4% | Regional; multi-country deployments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Short-Term User Fatigue with Points-Based Mechanics

Early retail and fintech programs spiked daily active users by up to 50% for 3 months, then saw a 40% decline as catalog variety stagnated. Gen Z cohorts, accustomed to instant gratification, disengage when points accrue slowly or expire quickly. Frictionless cashback and randomized chest-openers now replace linear accrual, sustaining curiosity through variable-reward psychology. Nubank’s chest mechanic illustrates the pivot, while Flourish Fi’s “Shake N Bank” bonus satisfies the craving for surprise. Regulators have noticed opaque redemption rules, signaling that transparency and renewal cadence will decide whether points-driven apps retain mindshare.

Data-Privacy Compliance Costs (LGPD, Habeas Data)

Brazil’s LGPD permits fines up to 2% of annual revenue or BRL 50 million (USD 8.9 million) per breach, forcing mid-sized vendors to budget heavily for audits, consent orchestration, and cross-border transfer safeguards. Gamification engines collect granular behavior logs that require explicit opt-ins and annual reviews. Multinational roll-outs multiply paperwork because Argentina and Colombia enforce distinct consent forms and storage mandates. Oracle and AWS offer in-country regions that keep personal data local, while vendors explore federated learning to personalize without centralizing raw logs. Yet these privacy-preserving architectures can blunt recommendation accuracy by up to 15%, tempering the engagement lift that gamification promises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Solutions as Integration Complexity Rises

Services outpaced solutions in terms of growth, even though ready-made platforms still accounted for 68.91% of 2025 revenue. Systems integrators now confront sprawling tech stacks that mix enterprise resource planning, payment hubs, and marketing clouds, compelling firms to hire specialists for customization, A/B testing, and security hardening. The South America gamification market size for the services segment is forecast to expand at a 28.43% CAGR through 2031, reflecting this rising integration intensity. Turnkey kits remain valuable for pilot proofs of concept, yet large-scale go-lives typically need bespoke reward logic, multilingual UX, and data-warehouse sync that off-the-shelf code rarely delivers.

Consulting engagements are expanding to include change management and behavioral economics coaching. Oracle teams supporting B3’s trading-floor dashboards embedded gamified badges that unlock once traders meet volume commitments within latency thresholds. SAP implementation partners layer level-ups onto supply-chain suites so warehouse crews gain real-time rank boosts for on-time picks. This professional-service heft reinforces why the South America gamification market continues to bifurcate between boxed software and high-touch advisory.

By Gamification Type: Leaderboards Gain as Sales Teams Demand Real-Time Visibility

Points-and-rewards accounted for 42.33% of 2025 value, yet leaderboards show the fastest 29.26% run rate as enterprises crave transparent competition. The South America gamification market share for leaderboards is widening because hourly rank refreshes spur immediate action, unlike delayed point tallies. Pharmaceutical firms broadcast territory scorecards on sales-floor screens, igniting peer rivalry that lifts call volume.

Adoption spills into call centers, where agents watch live dashboards that blend customer satisfaction scores with resolution speed. Simulation and serious games follow closely, especially in healthcare and mining, where risk-free practice scenarios cut error rates. Assessment modules embed quizzes into onboarding, so HR teams can automatically track certification milestones. Each mechanic taps different motivational levers, prompting many brands to mix modes within a single engagement funnel.

By Deployment Mode: Cloud Dominance Driven by Elastic Scaling and Hyperscaler Investments

In 2025, cloud deployments accounted for 73.42% of total spending and are projected to grow at a robust CAGR of 28.47% during the forecast period. It is projected to grow further as Amazon, Oracle, and Google add regions in São Paulo and Santiago. New zones slash round-trip latency, an essential when the South America gamification market for real-time multiplayer missions depends on sub-100-millisecond responses. Local hosting also satisfies LGPD controls by keeping personally identifiable information onshore, enabling banks and healthcare providers to offload non-core workloads.

On-premises still serves ministries and defense accounts, yet even those bodies test hybrid patterns that move low-risk learning games into managed Kubernetes clusters. Subscription pricing aligns spend with user peaks, shielding CFOs from the costs of lump-sum licenses. Elastic scaling also allows seasonal retailers to spin up Black Friday leaderboards overnight without capex. As multicloud interoperability matures, migration friction subsides, accelerating the flow of workloads into public infrastructure.

By End-User Industry: Healthcare Surges as Chronic-Disease Management Adopts Engagement Tools

In 2025, retail and e-commerce dominated with a 27.89% revenue share, while healthcare is set to surge at a 29.83% CAGR, continuing through 2031. Diabetes platforms map daily glucose logging to streak counters, while hypertension apps trigger animated celebrations when patients record seven consecutive readings. The South America gamification market size for healthcare modules is projected to triple as telemedicine reimbursement rules expand.

Banks sustain high adoption by weaving mini-quests into mobile apps that nudge users toward savings goals, credit-score milestones, or risk-profiling quizzes. Education, propelled by Kahoot! and Matific, keeps classrooms lively with timed quizzes and collaborative missions. Government agencies remain exploratory, piloting lottery-style tax incentives and citizen-service badges, but moving slowly due to procurement cycles.

By Enterprise Size: SMEs Accelerate Adoption via Low-Code Tools and Cloud Economics

Large enterprises still command 62.31% of 2025 spend, yet SMEs exhibit the sharper 28.51% CAGR thanks to pay-as-you-go subscriptions that bypass capex. Low-code catalogues let a 120-person logistics startup deploy driver scorecards in a month and cut late deliveries by double digits. The South America gamification market share held by SMEs will therefore tighten the gap with conglomerates over the forecast horizon.

Smaller firms benefit from faster decision loops, and store managers toggle reward logic daily without the delays of a steering committee. Data analytics maturity remains the chief hurdle, limiting their ability to personalize at scale. Vendors respond by offering plug-and-play segmentation based on behavioral heuristics rather than deep data science, enabling SMEs to still extract engagement lift.

Geography Analysis

Brazil accounted for 49.78% of 2025 revenue, buoyed by Pix instant payments, 188 million smartphone users, and in-country hyperscaler regions that guarantee low-latency gameplay. The South America gamification market in Brazil continues to grow as cloud providers add availability zones and LGPD sandboxes clarify consent orchestration. Enterprises from retail chains to telcos overlay cashback, badges, and leaderboards on daily customer interactions, fueling steady contract flow.

Colombia promises the fastest 29.11% CAGR to 2031. Government broadband subsidies pushed coverage to 70% by late 2025, and Bogotá’s public cloud region now hosts Oracle workloads for airlines and airport ground service firms. Fintech super-apps reward QR-code payments with instant cashback, while esports sponsorships translate into data-bundle perks, reinforcing consumer appetite for interactive rewards. This confluence propels the South America gamification market deeper into Colombian verticals from education to agriculture.

Argentina, Chile, Peru, and the broader Rest of South America segment complete the landscape. Argentina’s inflation challenges drive enterprises toward low-capex employee-engagement apps that bolster retention. Chile benefits from AWS’s USD 4 billion data-center plan, positioning Santiago as a latency-optimized hub for Southern Cone workloads. Peru pilots gamified math curricula that boost test scores, while Ecuadorian retailers test cashier-incentive dashboards tied to upsell conversion rates. Collectively, these markets illustrate the diverse yet converging adoption arc across the continent.

Competitive Landscape

Global software majors Oracle, SAP, and Microsoft embed gamification layers into cloud human-capital-management, customer-experience, and ERP suites, leveraging large installed bases to sidestep stand-alone sales cycles. Oracle’s multicloud pact with Google lets clients run Autonomous AI Database on Oracle Cloud Infrastructure inside Google data centers, simplifying procurement while ensuring LGPD compliance. SAP’s Business Data Cloud will reside in local AWS and Azure zones, bundling industry-specific reward mechanics that ride existing data models.

Regional specialists differentiate through language packs, local payment gateway connectors, and rapid localization services. Brazil’s Play2Sell tailors pharmaceutical and telecom sales games, while Argentina’s Scoring Gamification emphasizes Spanish-first UX and country-specific labor-law triggers. Chile’s MMD Games and Mexico’s BlueRabbit Edu capture education and mid-market corporate training deals. These players often partner with local systems integrators to offset brand-recognition gaps against global incumbents.

Artificial-intelligence personalization now separates leaders from laggards. Vendors blending reinforcement-learning algorithms with behavioral data predict churn, tailor challenge difficulty, and time reward drops, commanding premium pricing and multiyear renewals. Static rules engines face price erosion as clients demand adaptive engagement loops. White space persists in government projects, where budget cycles slow penetration, yet pilot successes in tax compliance hint at latent upside. Overall, rivalry is intensifying, but the South America gamification market remains moderately concentrated, with no single firm holding a dominant position.

South America Gamification Industry Leaders

Gamifier, Inc.

Oracle Corporation

SAP SE

Microsoft Corporation

Aon plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Oracle and Google Cloud made Oracle Database available on Google Cloud in São Paulo, enabling LGPD-compliant multicloud deployments that include gamified analytics dashboards for finance and retail clients.

- October 2025: Brazil’s National Data Protection Authority and Argentina’s Agency of Access to Public Information signed a memorandum of understanding to pilot an AI sandbox covering gamified decision engines, aiming to streamline cross-border data governance.

- September 2025: Oracle reported USD 7.2 billion in fiscal Q1 2026 cloud revenue, citing Latin American wins that bundled real-time performance dashboards for stock exchanges, insurers, and logistics groups.

- August 2025: SAP confirmed that Business Data Cloud will launch in Brazil within AWS and Azure zones, with partner-built gamification overlays for supply-chain visibility and sales-pipeline health.

South America Gamification Market Report Scope

The South America Gamification Market Report is Segmented by Component (Solutions, and Services), Gamification Type (Points and Rewards, Leaderboards, Simulation and Serious Games, Assessment and Training, Other Gamification Types), Deployment Mode (On-Premises, and Cloud), End-User Industry (Retail and E-commerce, Healthcare, Education, Banking Financial Services and Insurance, Telecommunications and IT, Media and Entertainment, Government, Other End-User Industries), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography (Brazil, Argentina, Colombia, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Component

| Solutions |

| Services |

By Gamification Type

| Points and Rewards |

| Leaderboards |

| Simulation and Serious Games |

| Assessment and Training |

| Other Gamification Types |

By Deployment Mode

| On-Premises |

| Cloud |

By End-User Industry

| Retail and E-commerce |

| Healthcare |

| Education |

| Banking, Financial Services and Insurance |

| Telecommunications and IT |

| Media and Entertainment |

| Government |

| Other End-User Industries |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Component | Solutions |

| Services | |

| By Gamification Type | Points and Rewards |

| Leaderboards | |

| Simulation and Serious Games | |

| Assessment and Training | |

| Other Gamification Types | |

| By Deployment Mode | On-Premises |

| Cloud | |

| By End-User Industry | Retail and E-commerce |

| Healthcare | |

| Education | |

| Banking, Financial Services and Insurance | |

| Telecommunications and IT | |

| Media and Entertainment | |

| Government | |

| Other End-User Industries | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the expected value of the South America gamification market in 2031?

It is projected to reach USD 49.73 billion, up from USD 14.34 billion in 2026.

Which deployment mode is growing fastest across the region?

Cloud deployments are forecast to advance at a 28.47% CAGR through 2031, driven by hyperscaler investments and lower data-residency hurdles.

Which industry will see the highest growth in gamification spending?

Healthcare is set to expand at a 29.83% CAGR as chronic-disease apps, telemedicine, and mental-health platforms embed engagement loops.

Why are leaderboards gaining traction inside enterprises?

Real-time rank visibility spurs instant competition, lifting sales and customer-support productivity while fitting naturally into performance-based incentive plans.

How do data-privacy laws affect gamification vendors?

Brazil’s LGPD, Argentina’s Habeas Data, and other statutes require explicit consent, in-country data storage, and periodic audits, driving up compliance costs and shaping architecture choices.

Page last updated on: