South America Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

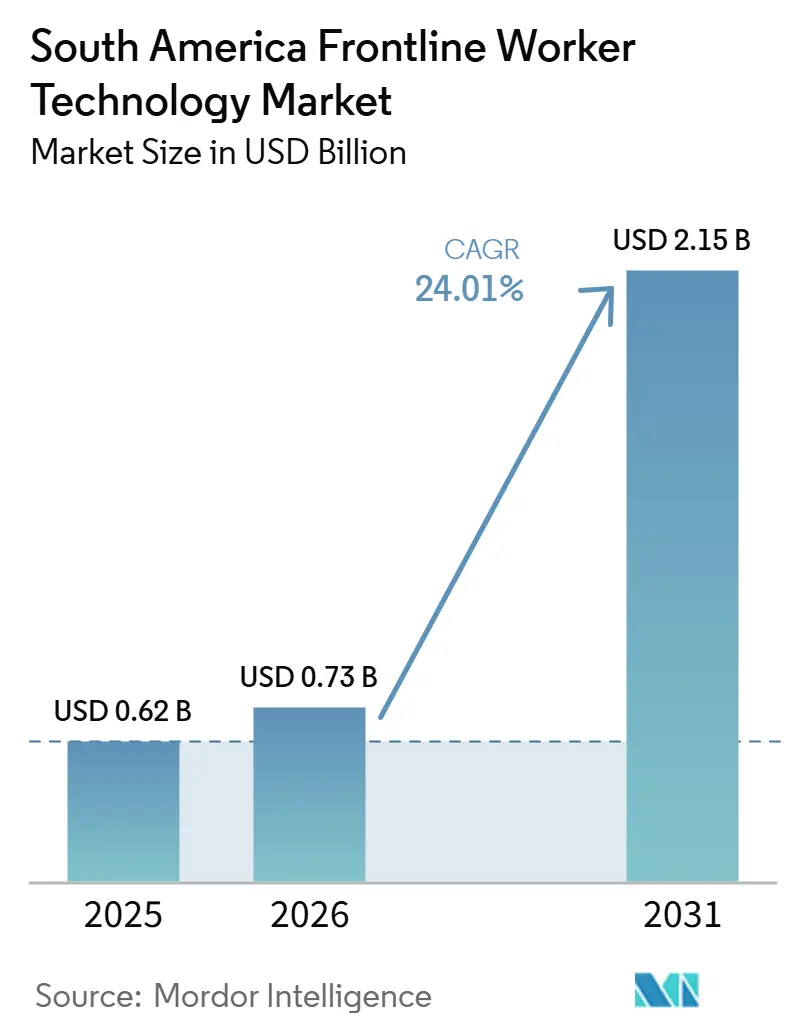

| Base Year Market Size (2025) | USD 0.62 Billion |

| Market Size (2026) | USD 0.73 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 24.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Frontline Worker Technology Market Analysis by Mordor Intelligence

The South America frontline worker technology market size was valued at USD 0.62 billion in 2025 and estimated to grow from USD 0.73 billion in 2026 to reach USD 2.15 billion by 2031, at a CAGR of 24.01% during the forecast period (2026-2031). The South America frontline worker technology market is expanding as employers move routine communication, task guidance, inspections, and reporting away from paper records and radio-only workflows into connected software environments that can be managed at scale. Demand is rising because industrial sites, ports, field operations, and large retail networks need reliable worker communication, stronger audit trails, and faster responses to safety events, making it harder to defer spending on frontline platforms than on many other software purchases. The South America frontline worker technology market is also benefiting from broader investment in site connectivity, including private networks, cloud infrastructure, and edge-enabled tools that keep frontline applications usable even in difficult field conditions. Competition is becoming more layered, with large global vendors holding an advantage in certified devices, enterprise integrations, and multi-country deployments, while regional firms compete with simpler rollout models, local language support, and pricing suited to smaller buyers. Over the forecast period, the South America frontline worker technology market is likely to see its addressable base expand as mobile-first and subscription models reduce entry barriers for smaller employers, even though device costs, battery limitations, and privacy concerns still restrain some of the demand.

Key Report Takeaways

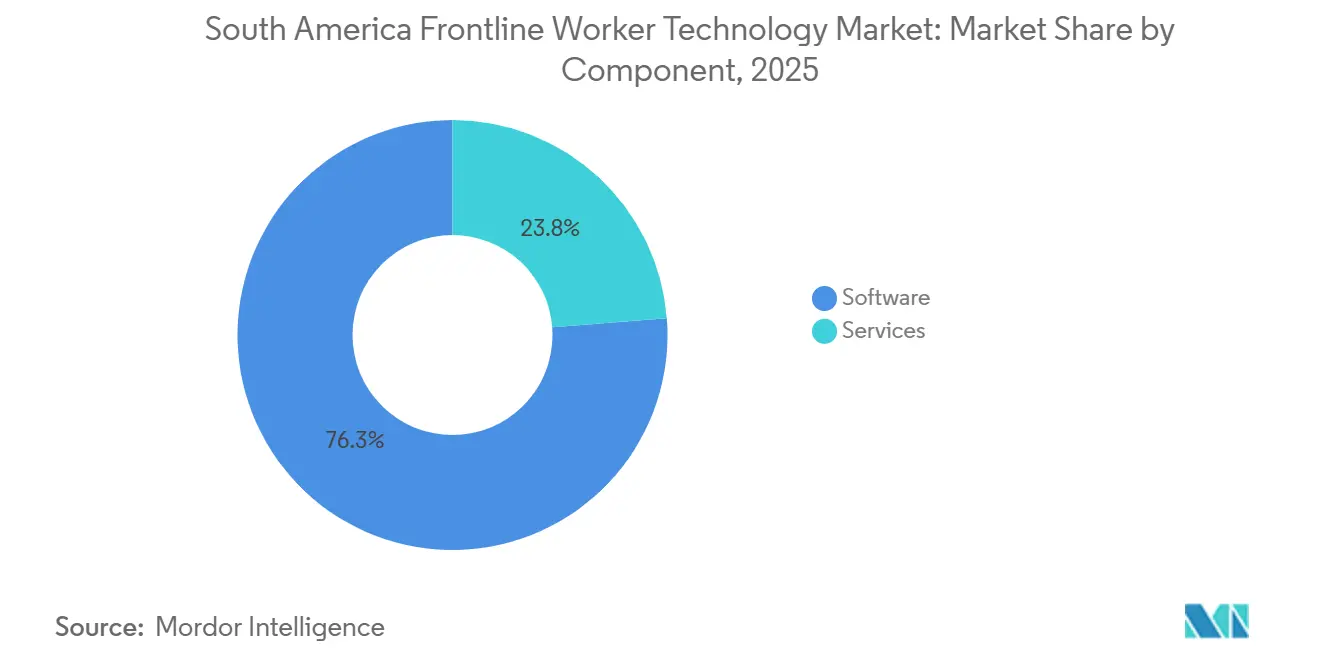

- By component, software held 76.25% of the South America frontline worker technology market share in 2025, while services are projected to expand at a 27.02% CAGR through 2031.

- By deployment, cloud-based deployment held 66.45% share of the South America frontline worker technology market size in 2025 and is projected to expand at a 26.34% CAGR through 2031.

- By organization size, large enterprises accounted for 68.33% of the South America frontline worker technology market share in 2025, while small and medium enterprises are projected to grow at a 26.77% CAGR through 2031.

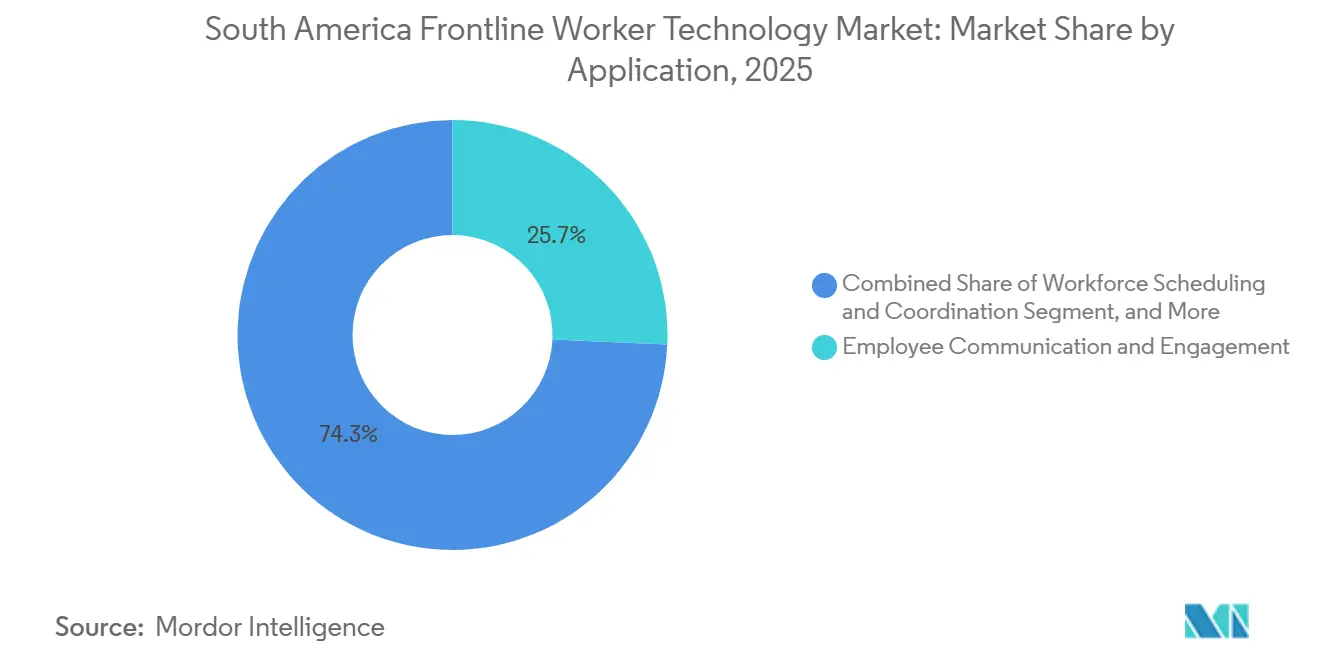

- By application, employee communication and engagement led with 25.71% of the South America frontline worker technology market share in 2025, while safety and compliance management is projected to expand at a 25.88% CAGR through 2031.

- By end-user industry, retail and e-commerce held 26.14% of the South America frontline worker technology market share in 2025, while transportation and logistics are projected to grow at a 25.49% CAGR through 2031.

- By geography, Brazil held 55.23% of the South America frontline worker technology market share in 2025, while Chile is projected to expand at a 26.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Hands-Free Task Guidance in Hazardous Operations | +5.2% | Brazil, Chile, Rest of South America | Short term (≤ 2 years) |

| Expansion of Private 5G and Wi-Fi 6 Networks in Industrial Sites | +4.3% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Increasing Adoption of Rugged Wearables for Worker Safety Compliance | +3.7% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Need for Real-Time Workforce Visibility and Traceability | +3.1% | Brazil-led, regional relevance across logistics and retail corridors | Short term (≤ 2 years) |

| Growth of Remote Expert Assistance in Mining and Oilfield Operations | +2.5% | Chile, Brazil | Medium term (2-4 years) |

| Digitalization of Maintenance, Inspection, and Training Workflows | +2.0% | Brazil, Chile, wider regional adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Hands-Free Task Guidance in Hazardous Operations

The South America frontline worker technology market is gaining support from employers that need workers to follow digital instructions without pausing manual tasks or removing protective equipment. This need is strongest in mining, metals, energy, and process industries, where a worker often must move, inspect, communicate, and confirm steps in the same operating cycle. Voice-controlled smart glasses and head-mounted tools reduce reliance on paper sheets, handheld devices, or repeated radio calls, making the workflow more practical in high-noise, high-risk settings. These deployments also create a continuous record of task completion, timestamps, and operating context, which gives safety, quality, and maintenance teams a data layer they could not consistently capture with analog methods. Once companies begin using this record for incident review and training, the same deployment starts supporting broader compliance and performance needs inside the South America frontline worker technology market. Product design is also becoming more localized for hazardous environments and privacy expectations, as shown by intrinsically safe smart glasses for noisy field use and smart badge systems aligned with Brazilian data privacy needs.

Expansion of Private 5G and Wi-Fi 6 Networks in Industrial Sites

The South America frontline worker technology market benefits when dedicated connectivity replaces shared and unstable communication layers in mines, plants, ports, and field assets. Frontline tools become far more useful when workers can receive live instructions, send video, confirm tasks, and share status data without the delays that often affect public networks in complex operating environments. This matters because many frontline use cases, including remote guidance, safety alerts, location tracking, and digital inspections, lose much of their value if coverage is inconsistent or latency varies during a shift. Better site connectivity also helps employers consolidate separate pilot tools into a single, broader operating platform, improving the economics of rollout and strengthening the case for long-term subscription spending. As networks become more dedicated and easier to govern, platform vendors can promise a more stable user experience and higher uptime across the South America frontline worker technology market. Brazil’s mission-critical communications rollout for federal agencies shows that dedicated broadband and unified communications infrastructure are moving into a long-term operational architecture, supporting the broader normalization of high-reliability workforce connectivity in the region.

Increasing Adoption of Rugged Wearables for Worker Safety Compliance

The South America frontline worker technology market is also being pushed by compliance needs that are less discretionary than pure productivity investments. Employers operating in hazardous environments need proof that workers received instructions, used equipment correctly, entered controlled areas under the proper conditions, and responded to safety checks in accordance with defined procedures. Digital wearables help create this record in real time, which makes them more reliable than paper logs that are often completed late or reconstructed after an event. Brazil’s Ministry of Labor and Employment updated its PPE certification framework in January 2025 through Portaria MTE nº 122, with the new conformity regime effective from February 2026, reinforcing the compliance environment for worker-worn equipment and related safety technologies.[1]Ministério do Trabalho e Emprego, “NR-06: Equipamento de Proteção Individual, Portaria MTE nº 122, 2025,” Governo Federal do Brasil, gov.br Once audit practices begin depending on device-generated records such as alerts, location logs, and equipment status checks, companies find it difficult to return to analog routines. Certified rugged devices and locally adapted wearable formats are therefore becoming more central to adoption across the South America frontline worker technology market.

Need for Real-Time Workforce Visibility and Traceability

The South America frontline worker technology market is growing because employers need to know where work is happening, who completed it, and whether handoffs were executed correctly across dispersed teams. This is especially important in logistics, retail, and manufacturing networks where managers must coordinate large workforces across stores, warehouses, transport nodes, and field locations in near real time. Visibility tools improve task assignment, exception handling, and incident response, but they also serve a second purpose by creating records that support labor accountability and operating discipline. As facilities add more automation and software-driven orchestration, frontline staff, machines, and data streams must be synchronized instead of managed through separate systems. That makes traceability part of routine operations rather than an added reporting layer, which strengthens recurring demand in the South America frontline worker technology market. Maersk’s April 2026 regional update described warehouse modernization through scanning, sensing, and software-driven orchestration, reflecting the operating environment that is elevating the value of connected frontline visibility tools across South American logistics networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Rugged Devices and Platform Integration | -3.8% | Regional, most acute among SMEs in Brazil and Argentina | Short term (≤ 2 years) |

| Limited Battery Life in Field-Deployed Wearables | -2.6% | Brazil, Chile | Medium term (2-4 years) |

| Data Privacy Concerns from Persistent Worker Monitoring | -1.9% | Brazil, Argentina | Medium term (2-4 years) |

| Weak Interoperability with Legacy OT and Enterprise Systems | -1.4% | Regional, strongest in legacy-heavy manufacturing and utilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Rugged Devices and Platform Integration

The South America frontline worker technology market still faces a clear adoption barrier because rugged devices cost far more than consumer hardware and usually require a separate investment case. This issue is most visible outside the large-enterprise tier, where a company may accept the value of frontline software but still delay purchases because the first deployment includes devices, accessories, configuration, training, and support. Integration adds another burden, since many buyers need the platform to connect with ERP, maintenance, workforce, or safety systems before it can become part of daily operations. Those integration projects are not simple, and they often consume months of specialist work before users see a full return. Smaller employers in the South America frontline worker technology market, therefore, tend to favor mobile-first or no-code options that can avoid part of the hardware and systems burden. Until financing models, device leasing, or lighter implementation methods become more common, cost will continue to keep a portion of demand in evaluation mode rather than full deployment.

Limited Battery Life in Field-Deployed Wearables

The South America frontline worker technology market also faces a practical limit when wearable battery life does not match the duration of long industrial shifts. Many field environments require a device to remain active through a full work cycle, yet continuous video, sensing, and data transmission can shorten usable battery life well before the shift is finished. This creates a weak point because workers may power down tools late in the day, when fatigue, risk, and communication failures are more likely. The problem is sharper in remote operations, where charging options are limited and device swaps interrupt work or require movement outside controlled zones. Battery constraints can therefore slow adoption in exactly the applications that need the strongest monitoring and guidance. Vendors are responding with swappable battery formats designed for hazardous settings, which helps, but the battery issue still shapes device choice and rollout pace across the South America frontline worker technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Drive the Orchestration Layer

Software held a 76.25% share of the South America frontline worker technology market in 2025, indicating that buyers are prioritizing the control layer that connects communication, tasks, analytics, and compliance records. The shift is important because employers no longer want separate tools for each frontline function when the real operational value lies in a single interface that links workers, devices, and enterprise systems. A platform-led architecture also supports hardware choice, since companies can add or change wearables, phones, tablets, or scanners without redesigning the core workflow logic each time. This makes software spending more durable because the platform becomes the execution framework rather than a single-use application. The South America frontline worker technology market, therefore, gives software vendors a stronger share of the budget when they can unify multiple workflows and support the local reporting and control needs of large employers.

The services segment is projected to expand at a 27.02% CAGR through 2031, indicating that software dominance is increasing service demand rather than reducing it. Once a frontline platform moves beyond basic messaging into workflow design, analytics, and compliance documentation, the buyer usually needs implementation support, integration work, process mapping, and user training. This is especially true when deployments must integrate with ERP, MES, CMMS, identity systems, or safety records that already reside within the enterprise stack. As the South America frontline worker technology market adds more AI-assisted features, the amount of specialist setup and ongoing optimization tends to rise further. TeamViewer’s June 2026 update to Assist AR, which added Microsoft Windows AI API support for clearer remote video under weak connectivity, shows how frontline platforms are becoming more advanced and, as a result, more dependent on skilled deployment and support services.

By Deployment: Cloud Infrastructure Anchors Market Architecture

Cloud-based deployment held 66.45% share in 2025, and this part of the South America frontline worker technology market benefits from the operating model that lets employers scale users, update workflows, and add features without repeated infrastructure purchases. Cloud delivery also suits organizations that run multiple sites because new users, locations, and process updates can be activated faster than they could through site-by-site local installations. For many employers, this model better aligns with budget planning because costs are spread across subscriptions rather than irregular capital projects. It also reduces dependence on scarce local IT talent, which is particularly useful in regions where advanced infrastructure support remains concentrated in a few urban centers. The South America frontline worker technology market has therefore treated cloud as the default architecture for many mainstream frontline applications, even where buyers still want local control over selected workloads.

Hybrid deployment remains relevant because some heavy industrial operations need local resilience, low latency, or continuity during network interruptions while still wanting cloud analytics and centralized administration. On-premises setups continue to matter in government and regulated utility environments where control, sovereignty, or legacy procurement structures still favor local infrastructure. Even so, cloud-based deployment is also the fastest-growing segment, with a 26.34% CAGR through 2031, indicating that the economics of centralized software management continue to improve. The direction of the South America frontline worker technology market suggests that the long-term structure will not be cloud-only, but cloud-led with edge capabilities layered in where field conditions require them. TeamViewer’s use of on-device AI for video enhancement in Assist AR supports this pattern by showing that cloud platforms are increasingly paired with local processing to preserve usability in low-bandwidth environments.

By Organization Size: Enterprise Scale Meets SME Leapfrogging

Large enterprises commanded a 68.33% share in 2025, reflecting the size of their deployments, the number of workers they manage, and the complexity of their operating environments. These buyers often run multi-site networks and need the same platform to support communication, safety, training, and task control across a much larger user base than smaller employers. They are also more likely to require formal audit trails, device certification, system integrations, and role-based access controls, which increases the total contract value and makes it harder for smaller vendors to contest the procurement. In the South America frontline worker technology market, large enterprise demand has therefore shaped product design around scale, reliability, and integration depth. The segment is likely to remain the main revenue anchor even as growth spreads further into smaller organizations.

Small and medium enterprises are projected to grow at a 26.77% CAGR through 2031, and this is one of the most important demand shifts within the South America frontline worker technology market. These buyers are entering through lighter deployment paths, including mobile-first applications, no-code setup, subscription pricing, and messaging-led workflows that avoid large infrastructure projects. This allows smaller firms to adopt frontline digitization without first building a complex device fleet or enterprise systems backbone. The model is especially attractive where workers already depend on smartphones and simple mobile communication habits in daily operations. IseTool’s stated reach of more than 115,000 frontline workers in Brazil through WhatsApp-delivered learning and task workflows shows how smaller employers can adopt practical frontline tools without the full hardware burden seen in larger enterprise deployments.

By Application: Communication Anchors the Base, Safety Compliance Leads Growth

Employee communication and engagement had the largest application share at 25.71% in 2025, making it the broadest entry point for the South America frontline worker technology market. Many organizations still face a basic communication gap between desk-based management and dispersed frontline staff, especially when work is spread across stores, production lines, transport networks, service teams, and field sites. A communication layer is often the first to be deployed because it can be rolled out quickly and used by many worker groups before deeper workflow automation begins. Once that communication base is in place, employers can add task management, learning modules, scheduling tools, and analytics on top of the same user environment. This is why communication keeps a large share of the South America frontline worker technology market, even as more specialized applications expand around it.

Safety and compliance management is projected to expand at a 25.88% CAGR through 2031, which shows that regulatory enforcement is becoming a stronger purchase trigger than discretionary experimentation. Employers value this segment because it turns inspections, acknowledgments, incident records, and worker checks into digital evidence that can be consistently retrieved and reviewed. That matters more when authorities and insurers begin recognizing technology-supported compliance pathways as valid operating practice. Argentina’s SRT Resolution 48/25 provided a clearer institutional framework for this trend by allowing employers and insurers to fulfill occupational risk obligations through certified technology providers. Over time, the South America frontline worker technology market is likely to see workforce analytics become a stronger complement to safety applications, as structured frontline data provides a basis for broader performance and risk analysis.

By End-User Industry: Retail and E-Commerce Leads, Logistics Grows Fastest

Retail and e-commerce accounted for 26.14% of revenue in 2025, making this vertical the largest revenue contributor in the South America frontline worker technology market. The segment requires rapid coordination among store staff, stockrooms, distribution centers, and omnichannel fulfillment points, making frontline communication and task management especially valuable. Retail operators also tend to operate at high worker volumes and experience frequent process changes, so digital instructions and structured execution tracking can improve consistency at scale. The buying case is therefore not only about labor visibility, but also about keeping customer-facing operations aligned with inventory, promotions, and service expectations. Within the South America frontline worker technology market, retail remains a strong anchor because it can justify deployment across both operational control and revenue protection needs.

Transportation and logistics are projected to grow at a 25.49% CAGR through 2031, reflecting the increasingly synchronized, data-led, and time-sensitive nature of supply chain operations. Facilities increasingly need workers, software systems, and automated assets to function together rather than as separate activity streams. That shift raises demand for task orchestration, exception alerts, safety monitoring, and instant communication, especially in large warehouses and networked logistics corridors. Maersk’s April 2026 regional update described this operating model as scanning, sensing, and software-driven orchestration across logistics environments, which closely aligns with the use cases driving growth in this segment.[2]A.P. Moller - Maersk, “Latin America Market Update, April 2026,” Maersk, maersk.com The South America frontline worker technology market is also seeing rising relevance in healthcare, construction, mining, and public administration, but logistics stands out because its operating pace makes coordination failures immediately visible and costly.

Geography Analysis

Brazil accounted for 55.23% of regional revenue in 2025, which gave it the largest position in the South America frontline worker technology market and the deepest installed base for enterprise-scale deployments. This lead reflects the country’s larger industrial and retail workforce, heavier compliance burden, and stronger history of investment in digital workforce management than most neighboring markets. Brazil also benefits from a broader communications and technology environment that supports frontline digitization, including mission-critical network investments and expanding software adoption across public and private operators. Motorola Solutions stated in June 2025 that its federal communications network project in Brazil would connect more than 6,500 government points across 27 state capitals, which underlines the scale of the country’s appetite for resilient worker communications infrastructure.[3]Motorola Solutions, “Motorola Solutions Unifies Communications Across Brazil's Defense and Public Safety Agencies,” Motorola Solutions, motorolasolutions.com Brazil’s regulatory setting around worker protection also keeps compliance-oriented spending relevant for the South America frontline worker technology market, especially as the updated PPE conformity regime takes effect from February 2026.

Chile is projected to expand at a 26.05% CAGR through 2031, which makes it the fastest-growing geography in the South America frontline worker technology market. The country’s mining base gives frontline technology a direct operating role because remote sites need reliable communication, guided procedures, digital inspection, and safety monitoring under difficult field conditions. These needs become stronger when companies automate more assets and retrain workers into technology-heavy operating roles. BHP reported that Escondida Norte in Chile became fully autonomous in January 2026 with 33 autonomous trucks and 11 autonomous drills, while more than 5,000 workers were retrained for new technology roles and women held 64% of autonomy-related roles. This kind of operating change supports demand across communication, training, remote assistance, and compliance layers, giving Chile an outsized growth profile in the South America frontline worker technology market.

Argentina and the Rest of South America remain earlier-stage areas of the South America frontline worker technology market, but their adoption path is becoming clearer. Argentina has a stronger case for safety-related deployments because the formal recognition of certified technology providers under SRT Resolution 48/25 gives employers and insurers a clearer route to digital occupational risk management. Across Peru, Colombia, Ecuador, and Bolivia, adoption is concentrated in mining and energy sites, where multinational operators bring connected worker practices from other regions into South American operations. This means diffusion may occur through cross-border operating models and standardized site practices rather than through a single local growth pattern, gradually widening the reach of the South America frontline worker technology market beyond its current core countries.

Competitive Landscape

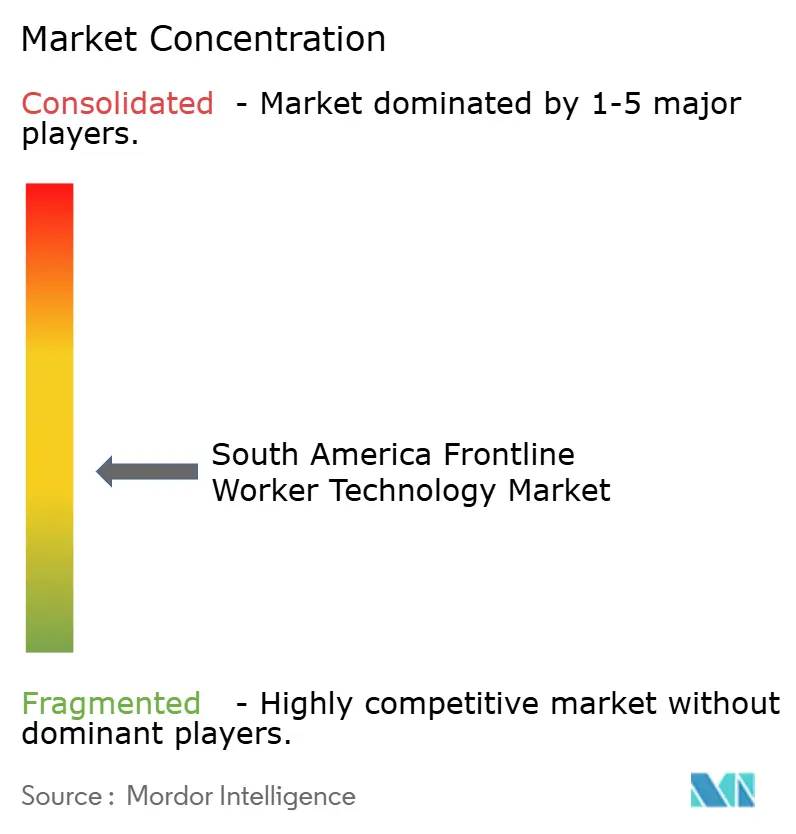

The South America frontline worker technology market is moderately concentrated at the platform level, but it remains fragmented across hardware, services, and vertical-specific solutions. Global vendors such as Zebra Technologies, TeamViewer, Microsoft, SAP, and Honeywell have an advantage in large-enterprise accounts because buyers value integration depth, device compatibility, and long-term product support. Hardware specialists such as RealWear, Vuzix, ProGlove, and Datalogic add another layer of competition by focusing on specific field conditions and worker use cases rather than trying to own the entire platform stack. In practice, the South America frontline worker technology market rewards vendors that can combine certified devices, software control, and implementation capacity rather than competing in a single product category. This structure gives large incumbents a durable edge in complex accounts, while still leaving room for smaller firms in narrower workflows and midmarket deployments.

Recent strategic moves show that competition in the South America frontline worker technology market is shifting from device ownership alone toward workflow intelligence and operating continuity. Zebra Technologies launched Zebra Nucleus, Workcloud Business Intelligence, and Workcloud Integration and Orchestration in June 2026, which widened its position from hardware management into platform oversight, analytics, and workflow connection. TeamViewer partnered with Microsoft in June 2026 to bring Windows AI API Video Super Resolution into Assist AR, which improved remote assistance performance under weak or unstable connectivity. RealWear continued to strengthen its hazardous-environment position with rugged intrinsically safe smart glasses and a swappable battery design that reduces field interruption in controlled zones.[4]RealWear, “RealWear Ships Most Advanced Rugged Enterprise Intrinsically Safe Smart Glasses,” RealWear, realwear.com Together, these moves show that leading vendors are competing on a broader set of promises: uptime, safety and readiness, analytics, and enterprise fit across the South America frontline worker technology market.

White space remains meaningful in the South America frontline worker technology market, especially among SMEs and in compliance-heavy deployments that need local templates, simpler pricing, and easier onboarding. Regional developers can still win when they build around familiar mobile behaviors, faster rollout, and practical workflow coverage for employers below the large-enterprise tier. Even so, global vendors hold a stronger position where buyers need certified hardware, broad partner ecosystems, and reliable operation under weak connectivity or hazardous conditions. The South America frontline worker technology market is therefore likely to maintain its mixed structure, with global firms occupying the upper tier and regional competitors remaining relevant in lower-tier, localized, and cost-sensitive use cases.

South America Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Microsoft Corporation

SAP SE

RealWear, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies launched Zebra Nucleus, a unified platform for total device fleet oversight and control, alongside Workcloud Business Intelligence and Workcloud Integration and Orchestration solutions at its annual ZONE 2026 conference in Nashville. The launch signals Zebra's strategic pivot from hardware-led to software-and-intelligence-led market positioning, directly competing with pure-play workforce software vendors in the retail, manufacturing, and logistics segments, where it has an established hardware installed base across South America.

- June 2026: TeamViewer partnered with Microsoft to integrate Windows AI API for Video Super Resolution into its Assist AR remote assistance solution for frontline workers and industrial environments, announced June 3, 2026. The integration uses on-device AI models running locally on Copilot+ PCs to reconstruct and sharpen incoming video in real time under weak or unstable mobile connections, a capability directly relevant to South America's remote mining and oilfield environments where network reliability is inconsistent.

- January 2026: BHP's Escondida Norte pit in Chile became fully autonomous, operating 33 autonomous trucks and 11 autonomous drills moving more than 350,000 tonnes of material daily and accounting for 30% of Escondida's production. More than 5,000 workers were retrained in new technology roles as part of the transition, with 64% of participants female, establishing the region's most advanced case study of technology-enabled frontline workforce transformation in mining.

- June 2025: Motorola Solutions was selected by EAF (ANATEL's Band Administration Entity) to implement Brazil's federal mission-critical communications network, integrating Land Mobile Radio systems across defense and public safety agencies with MCX broadband services. The contract covers a fixed network connecting more than 6,500 federal government points across 27 state capitals, as well as a mobile network for the Federal District.

South America Frontline Worker Technology Market Report Scope

The South America Frontline Worker Technology Market comprises software platforms, connected worker solutions, and digital productivity tools that support frontline employees across industries such as manufacturing, retail, healthcare, logistics, construction, and public services across South America. These technologies enable workforce communication, task execution, training, safety management, performance monitoring, and operational coordination. Increasing enterprise digitization, expanding adoption of the mobile workforce, and rising investments in workforce productivity and operational efficiency drive the market. The market focuses on improving frontline employee engagement, connectivity, and real-time decision-making across distributed work environments.

The South America Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other End-User Industries), and Geography (Brazil, Argentina, Chile, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other End-User Industries |

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

What is the size outlook for the South America frontline worker technology market?

The South America frontline worker technology market size was USD 0.62 billion in 2025, reaches USD 0.73 billion in 2026, and is forecast to reach USD 2.15 billion by 2031 at a 24.01% CAGR.

Which country leads regional demand for frontline worker technology in South America?

Brazil led regional demand with 55.23% revenue share in 2025, supported by its larger industrial base, broader compliance burden, and stronger communications infrastructure rollout.

Which application area is growing fastest in frontline worker technology across South America?

Safety and compliance management is the fastest-growing application, with a projected 25.88% CAGR through 2031, as employers need stronger digital evidence for audits, inspections, and worker protection.

Why is cloud deployment so important for frontline worker technology adoption?

Cloud-based deployment held 66.45% share in 2025 and is also the fastest-growing deployment model at 26.34% CAGR, because it supports easier scaling, faster updates, and lower infrastructure burden.

Which end-user group is creating the fastest demand growth?

Transportation and logistics is the fastest-growing end-user segment at a 25.49% CAGR through 2031, driven by the need to coordinate workers, systems, and automated assets in real time.

What is driving adoption among smaller employers in South America?

Small and medium enterprises are projected to grow at a 26.77% CAGR because mobile-first, subscription-based, and messaging-led tools reduce the cost and complexity of initial deployment.

Page last updated on: