South America Fourth Party Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

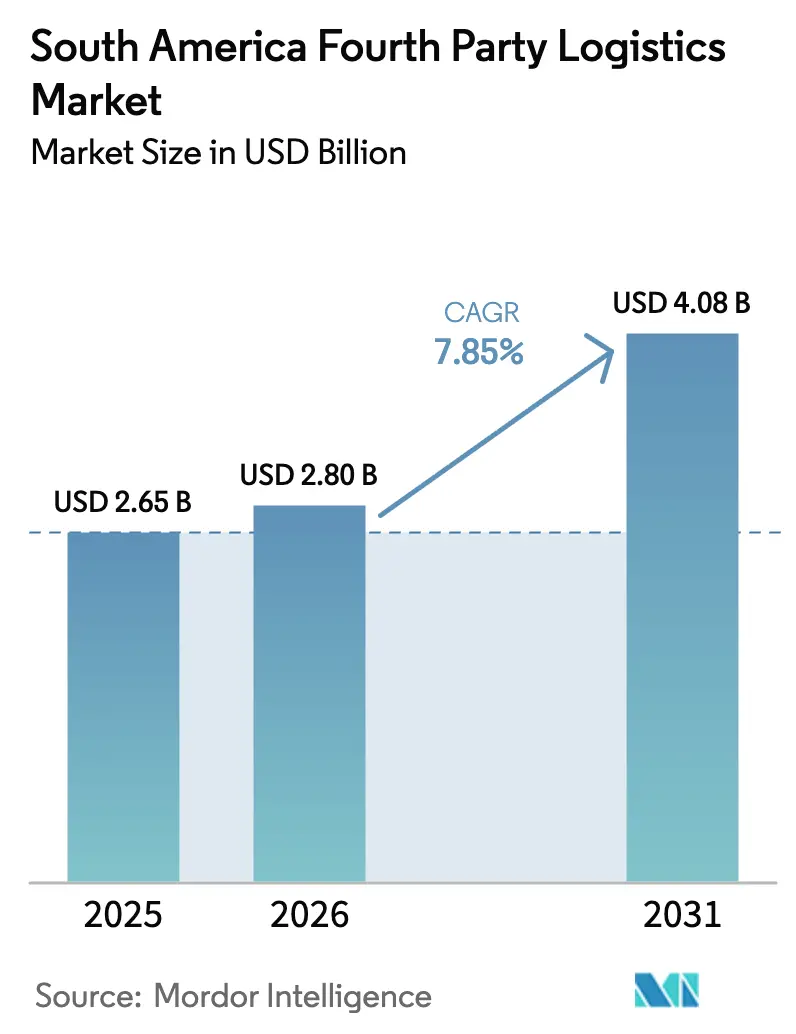

| Base Year Market Size (2025) | USD 2.65 Billion |

| Market Size (2026) | USD 2.80 Billion |

| Market Size (2031) | USD 4.08 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

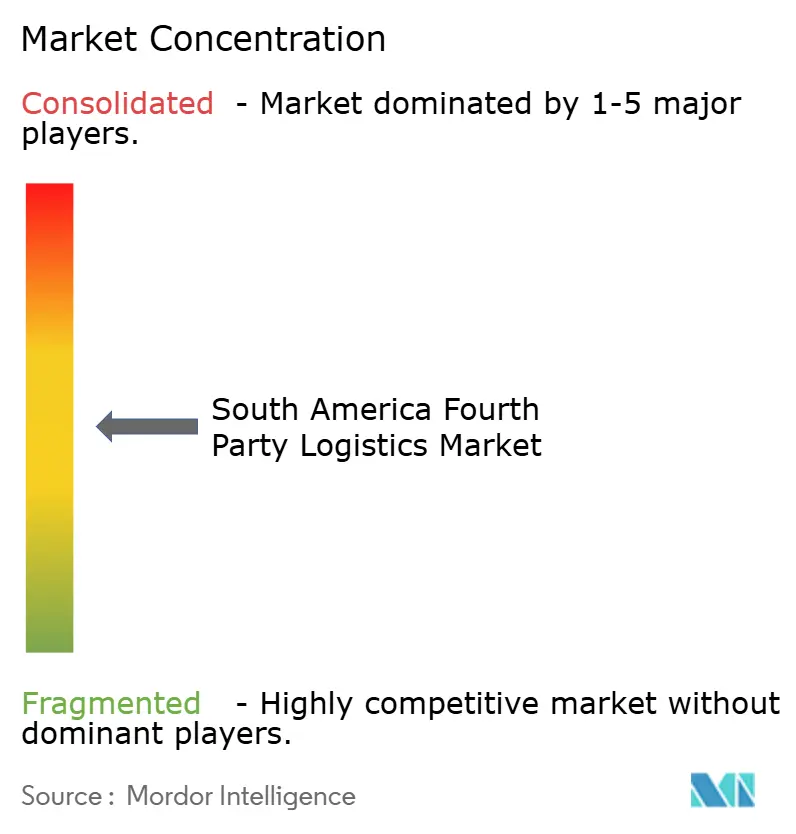

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Fourth Party Logistics Market Analysis by Mordor Intelligence

The South America Fourth Party Logistics Market size is expected to increase from USD 2.65 billion in 2025 to USD 2.80 billion in 2026 and reach USD 4.08 billion by 2031, growing at a CAGR of 7.85% over 2026-2031.

Demand is pivoting away from transactional freight brokerage toward single-contract orchestration platforms that layer customs brokerage, bonded warehousing, carrier procurement, and real-time visibility under unified service-level agreements. Brazil generated 52.75% of regional revenue in 2025 on the back of its Mercosur hub status and deep automotive and consumer-goods clusters, yet Colombia is expanding the fastest as nearshoring redirects electronics assembly and pharmaceutical cold-chain exports toward Pacific-facing gateways[1]A.P. Moller - Maersk, “Latin America Market Update,” MAERSK.COM . Retail and e-commerce shippers led 4PL adoption owing to MercadoLibre’s BRL 19 billion (USD 3.62 billion) fulfillment program, while infrastructure mega-projects such as the Bioceanic Corridor and Brazil’s National Logistics Plan are unlocking multimodal rail–short-sea options that 4PLs can blend with legacy trucking networks. Digitally enabled control towers, AI-assisted exception management, and ESG-compliant routing now influence bid outcomes, triggering accelerated platform rollouts by both global integrators and regional specialists.

Key Report Takeaways

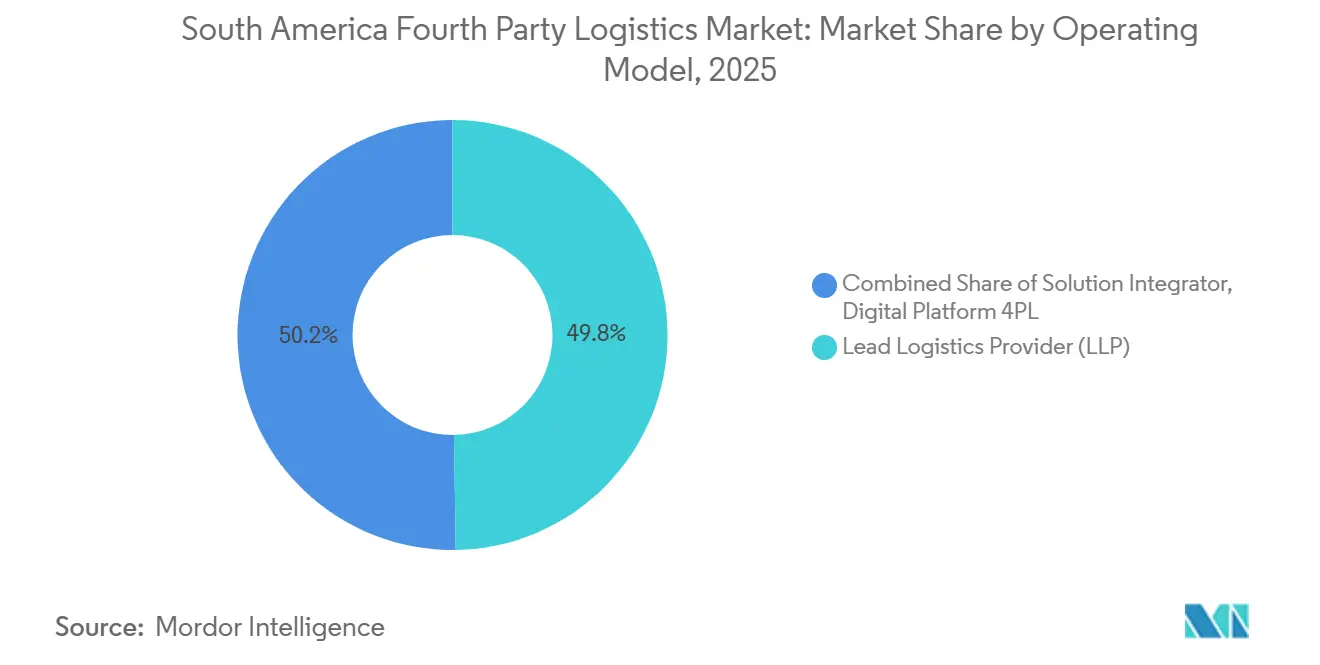

- By operating model, lead logistics provider contracts held 49.76% of the South America fourth-party logistics (4PL) market share in 2025, while Digital Platform 4PL architectures are forecast to expand at an 8.91% CAGR from 2026-2031.

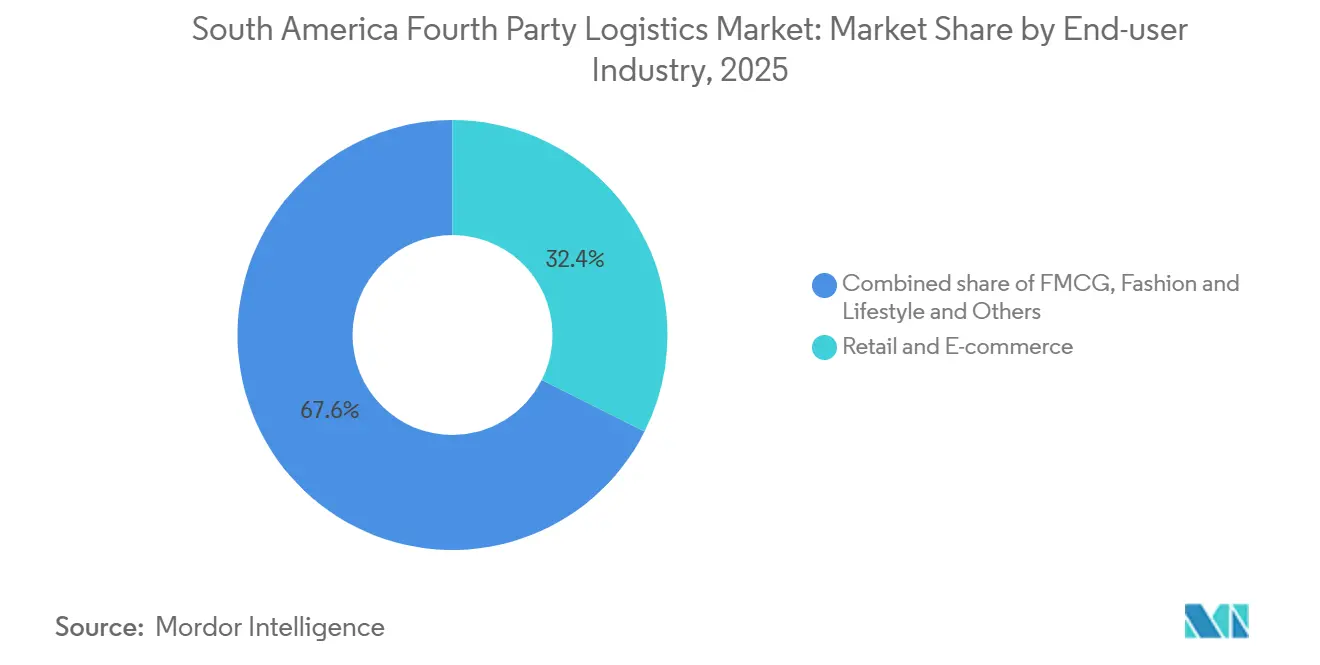

- By end-user industry, retail and e-commerce accounted for 32.41% of 2025 revenue in the South America fourth-party logistics (4PL) market size, while refrigerated and pharmaceutical corridors are projected to grow at a 9.36% CAGR through 2031.

- By geography, Brazil accounted for 52.75% of the 2025 value within the South America fourth-party logistics (4PL) market share, while Colombia is expected to post the quickest national expansion at a 9.85% CAGR over 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Fourth Party Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| The e-commerce boom is accelerating integrated logistics demand | +2.1% | Brazil, Argentina, Colombia; spill-over to Chile, Peru | Medium term (2-4 years) |

| Infrastructure mega-projects unlocking multimodal networks | +1.8% | Brazil, Colombia, Argentina, Chile | Long term (≥ 4 years) |

| Digitalization & real-time visibility platforms adoption | +1.5% | Brazil, Chile, Colombia | Short term (≤ 2 years) |

| ESG-driven low-carbon supply-chain optimization | +1.2% | Brazil, Chile, Argentina; EU-export corridors | Medium term (2-4 years) |

| Cold-chain corridor build-out for pharma & agrifood exports | +0.9% | Colombia, Chile, Peru, Brazil (Northeast) | Medium term (2-4 years) |

| Growth of bonded free-trade-zone ecosystems | +0.7% | Brazil (Manaus, Santos), Colombia (Cartagena, Bogotá), Chile (Iquique) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Accelerating Integrated Logistics Demand

MercadoLibre’s BRL 19 billion (USD 3.6 billion) Brazil build-out underscores the migration toward multi-client fulfillment nodes that 4PL orchestrators can consolidate across retailers. Argentina’s 30% e-commerce penetration is nudging merchants to adopt inventory-financing and dynamic pricing modules embedded in 4PL dashboards. Colombia’s flower-export peaks around Valentine’s Day require 4PLs to pre-book freighter lifts months in advance, using Panama as an overflow gateway to avert rate spikes.

Infrastructure Mega-Projects Unlocking Multimodal Networks

Brazil allocated BRL 140 billion (USD 26.7 billion) for railway upgrades and, together with IDB and CAF, secured USD 10 billion for the Bioceanic Corridor, a route that will cut ocean-rail transit between Sao Paulo and Antofagasta from 14 days to 7 by 2028. Colombia’s Pacific corridor shortened Bogota–Buenaventura hauls by 18% in 2025, though landslides and aging fleets oblige 4PLs to maintain redundant lanes[2]United Nations Development Programme, “Latin America Logistics and Transport Sustainability,” UNDP.ORG. Argentina’s Norte Grande program widens agricultural export access but still faces cargo-theft headwinds, driving demand for GPS-enabled tracking in 4PL SLAs. Congestion at Santos, where only two piers ran through mid-2025, pushed average waits beyond seven days; orchestrators that could reroute via Paranagua or Itapoa captured urgent volumes

Digitalization & Real-Time Visibility Platforms Adoption

Kuehne + Nagel’s cloud platform links over 40 technology partners across six regional control towers, trimming response cycles by 60% and safety stock by 10%[3]Kuehne + Nagel, “4PL Platform and Control Tower Capabilities,” KUEHNE-NAGEL.COM. FourKites processes 3.2 million shipments daily, but adoption in South America lags North America due to data-sovereignty rules. JSL’s proprietary WMS reduced warehouse errors by 25% across its 2 million m² footprint, signaling the ROI of self-built stacks. ISO 27001 is now a near-mandatory credential after ransomware attacks on logistics tripled between 2024-2025.

ESG-Driven Low-Carbon Supply-Chain Optimization

EU carbon border measures and deforestation rules are forcing South American exporters to document Scope 3 emissions, benefiting 4PLs that can report carbon data for each shipment leg. Maersk’s fully electrified Suape terminal, due online in 2026, and its renewed Santos concession enable orchestrators to market near-zero-carbon corridors. Kuehne + Nagel’s embedded emissions dashboard now carries up to 20% of the evaluation weight in tender scorecards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure gaps & high over-the-road dependency | –1.3% | Argentina, Peru, Paraguay, Bolivia, rural Brazil | Long term (≥ 4 years) |

| Complex cross-border customs/regulatory regimes | –0.9% | Argentina currency controls, Brazil import licensing, Mercosur lanes | Medium term (2-4 years) |

| Cybersecurity & data integration risk aversion | –0.6% | Brazil, Chile, Colombia; sectors handling sensitive data | Short term (≤ 2 years) |

| Cargo-theft-related insurance/risk premiums | –0.5% | Brazil 68% of incidents, Argentina: 12%, Mexico border corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Gaps & High Over-the-Road Dependency

Road freight’s 70% modal share, coupled with an average truck age of 15 years, caps reliability and raises emissions. IMF gravity-model analysis shows logistics infrastructure quality explains much of South America’s manufacturing under-trading. Currency volatility delays procurement of spare parts for Argentina’s Norte Grande road program, inflating carrier operating costs. Chile’s 2022 CIF/FOB margin reached 8.8%, almost double the global norm, reflecting the Andes barrier and limited multimodal choices[4]Organisation for Economic Co-operation and Development, “CIF/FOB Margins Dataset,” OECD.ORG. Port congestion at Santos compounds delays, raising expedite fees that 4PL contracts struggle to pass through.

Complex Cross-Border Customs/Regulatory Regimes

Mercosur, Pacific Alliance, and Andean Community rules diverge on valuation, licensing, and data exchange, driving compliance overhead for 4PLs. Paraguay posts an 82.8% UN/CEFACT score, but Brazil’s import bureaucracies and Argentina’s FX controls inject uncertainty into. WCO pilots on electronic Certificates of Origin remain uneven; manual interventions persist at land borders, prolonging cash-to-cash cycles. Volkswagen Puebla’s 2027 retool will raise overseas part numbers by 70%, exemplifying the coordination burden 4PLs must shoulder.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating Model: Digital Platforms Gain Share Despite LLP Dominance

Lead logistics provider agreements captured 49.76% of 2025 spending in the South America fourth-party logistics market share, reflecting long-term automotive and industrial outsourcing norms. Digital platform 4PL contracts, however, are set to register the highest CAGR at 8.91%, driven by demand for cloud-based control towers, predictive analytics, and modular pricing. Kuehne + Nagel’s network integrates forty technology vendors and reduces inventory buffers by 10%. FourKites’ AI-enabled control tower processes 3.2 million daily loads, underscoring scale benefits over asset-heavy LLP models.

Solution Integrators dwell in the advisory sweet spot, redesigning supply networks without taking execution risk. 4flow’s iTMS has delivered 5-15% freight savings with 12-16-week go-live cycles for OEMs, attracting mid-market nearshoring entrants. As convergence accelerates, Maersk and C.H. Robinson are layering SaaS TMS tools atop forwarding portfolios, blurring model boundaries across the South America fourth-party logistics market.

By End-User Industry: Retail–E-Commerce Leads, Cold-Chain Accelerates

In the South America Fourth-Party Logistics (4PL) Market size, the retail and e-commerce segment dominated with 32.41% of 2025 revenue and is set to grow at a 9.36% CAGR through 2031, the fastest among all sectors. MercadoLibre’s fulfillment network fuels multi-client warehousing where 4PLs consolidate last-mile capacity, while rising cold-chain volumes from Colombia’s flowers, Chile’s fruits, and regional vaccines highlight the need for sensor-equipped corridors as temperature losses reach 38% in Central America.

Automotive and mobility manufacturers rely on just-in-sequence inbound flows integrated with ERP systems; Nissan Brazil reduced truck dwell by 93% using visibility platforms. Tech shippers increasingly route China-origin parts through bonded zones to reduce tariff exposure, and fashion brands embed circular logistics and carbon metrics into 4PL scorecards to meet EU tender standards.

Geography Analysis

In the South America Fourth-Party Logistics (4PL) Market share, Brazil dominated with 52.75% of revenue in 2025, driven by Mercosur trade preferences, its dense automotive ecosystem, and MercadoLibre’s extensive warehouse network. Colombia, meanwhile, is projected to record the fastest growth at a 9.85% CAGR through 2031, supported by expanding export corridors and the rapid digitalization of logistics infrastructure. Brazil’s BRL 140 billion (USD 26.7 billion) National Logistics Plan and the Bioceanic Corridor, linking to Asia in just seven days, highlight significant potential for modal shift toward rail and multimodal solutions.

Regional 4PL orchestration is maturing, with JSL’s Intralog division managing 2 million m² of facilities and setting a model for local players aspiring to global integration standards. At the same time, Maersk’s electrified Suape terminal and its renewed Santos concession are establishing low‑carbon corridors increasingly attractive to ESG‑focused shippers seeking sustainable supply chain solutions.

Across other markets, Argentina’s Norte Grande road developments are opening new production zones, though progress is tempered by currency restrictions, freight theft (12% of incidents), and import licensing frictions. The IDB’s USD 3.91 billion nearshoring export forecast supports demand for bonded‑warehouse orchestration, while Chile maintains its Pacific‑gateway advantage demonstrated by FedEx doubling its Santiago DC to 14,000 m² (6,000 parcels/hour). Peru, Paraguay, Bolivia, Uruguay, and Ecuador represent white‑space opportunities where mid‑cap manufacturers still depend on fragmented brokerage networks.

Competitive Landscape

Global integrators such as DHL, Kuehne + Nagel, DSV, Maersk Logistics, GXO, CEVA, UPS SCS, FedEx Logistics, GEODIS, and C.H. Robinson compete head‑to‑head with regional leaders like JSL, SAAM, and Gafor in the South America Fourth‑Party Logistics (4PL) Market share. These players combine freight forwarding, contract logistics, transport management, and value‑added services such as customs clearance, data visibility, and sustainability tracking into a single orchestration layer. Technology adoption has become the key differentiator: Kuehne + Nagel’s cloud‑based control tower helps clients cut safety stocks by 10%, while JSL’s AI‑enabled warehouse management system (WMS) reduces errors by 25% and improves labor utilization across multiple facilities.

CEVA Logistics manages Iveco’s 20,000 m² parts hub in Minas Gerais, deploying wireless WMS tools that enable high‑frequency picking, paperless coordination, and real‑time updates for production lines. GEODIS’ partnership with Atlas Air secures freighter capacity into Brazil, Colombia, and Chile, offering stable peak‑season connectivity that mitigates the region’s volatile airfreight supply. These capabilities are increasingly decisive for winning integrated mandates from automotive, electronics, and pharmaceutical clients that prioritize reliability and full‑chain visibility.

Multinationals are scaling through mergers, acquisitions, and aviation alliances, allowing them to extend visibility platforms and temperature‑controlled lanes across continents. In contrast, regional firms are moving toward vertical integration, for instance, SAAM divested its port terminals to focus exclusively on high‑margin towage and logistics orchestration. With the digital ecosystem expanding, cybersecurity certifications such as ISO 27001 and TISAX have become non‑negotiable contract requirements, as ransomware and data breaches increasingly test the digital resilience that now underpins physical logistics networks.

South America Fourth Party Logistics Industry Leaders

DHL Supply Chain

Kuehne + Nagel

DSV

XPO Logistics

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: GEODIS signs an interline pact with Atlas Air to boost freighter capacity into Brazil, Colombia, Panama, Chile, and Costa Rica

- November 2025: JSL appoints a new CEO for 2026 and spins off Intralog, a BRL 2.4 billion revenue 4PL unit targeting >20% growth.

- November 2025: CEVA will operate a 20,000 m² parts DC for Iveco in Minas Gerais, supported by a BRL 93 million investment.

- October 2025: DHL’s Global Connectedness Tracker upgrades South & Central America trade forecasts after 5.4% y-t-d value growth.

South America Fourth Party Logistics Market Report Scope

| Lead Logistics Provider (LLP) |

| Solution Integrator |

| Digital Platform 4PL |

| FMCG |

| Retail and E-commerce |

| Fashion and Lifestyle |

| Technology and Electronics |

| Refrigerated and Pharma |

| Automotive and Mobility |

| Industrial Manufacturing |

| Others |

| Argentina |

| Brazil |

| Chile |

| Peru |

| Colombia |

| Rest of South America |

| By Operating Model | Lead Logistics Provider (LLP) |

| Solution Integrator | |

| Digital Platform 4PL | |

| By End-User Industry | FMCG |

| Retail and E-commerce | |

| Fashion and Lifestyle | |

| Technology and Electronics | |

| Refrigerated and Pharma | |

| Automotive and Mobility | |

| Industrial Manufacturing | |

| Others | |

| By Country | Argentina |

| Brazil | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

How large will the South American fourth-party logistics market be in 2026?

The market is projected to reach USD 2.80 billion in 2026.

Which operating model is expanding the quickest?

Digital Platform 4PL contracts are expected to grow at an 8.91% CAGR through 2031.

What factors make Colombia an attractive growth hotspot?

Upgraded Pacific corridors, 18% shorter Bogota-Buenaventura lead times, and nearshoring inflows underpin a 9.85% CAGR outlook.

How are ESG rules reshaping logistics contracts in the region?

EU carbon-border and deforestation regulations are pushing shippers to favor 4PLs that offer shipment-level emissions reporting.

Which infrastructure initiative will most alter regional routing patterns?

Brazil’s Bioceanic Corridor, set to halve Sao Paulo-Antofagasta transit to seven days by 2028, will materially shift modal choices.

What risk most significantly elevates insurance premiums?

Cargo theft valued at USD 5.5 billion annually and heavily concentrated in Brazil drives up insurance and necessitates GPS-based security.

Page last updated on: