South America Flat Glass Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

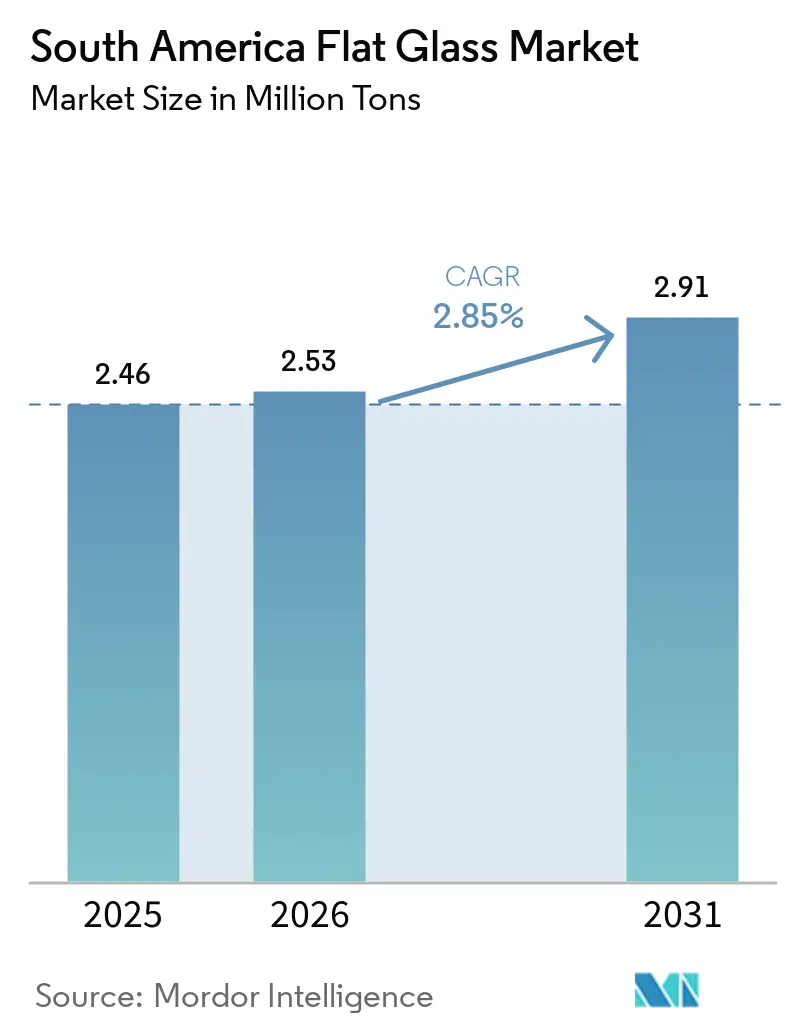

| Base Year Market Size (2025) | 2.46 Million tons |

| Market Volume (2026) | 2.53 Million tons |

| Market Volume (2031) | 2.91 Million tons |

| Growth Rate (2026 - 2031) | 2.85% CAGR |

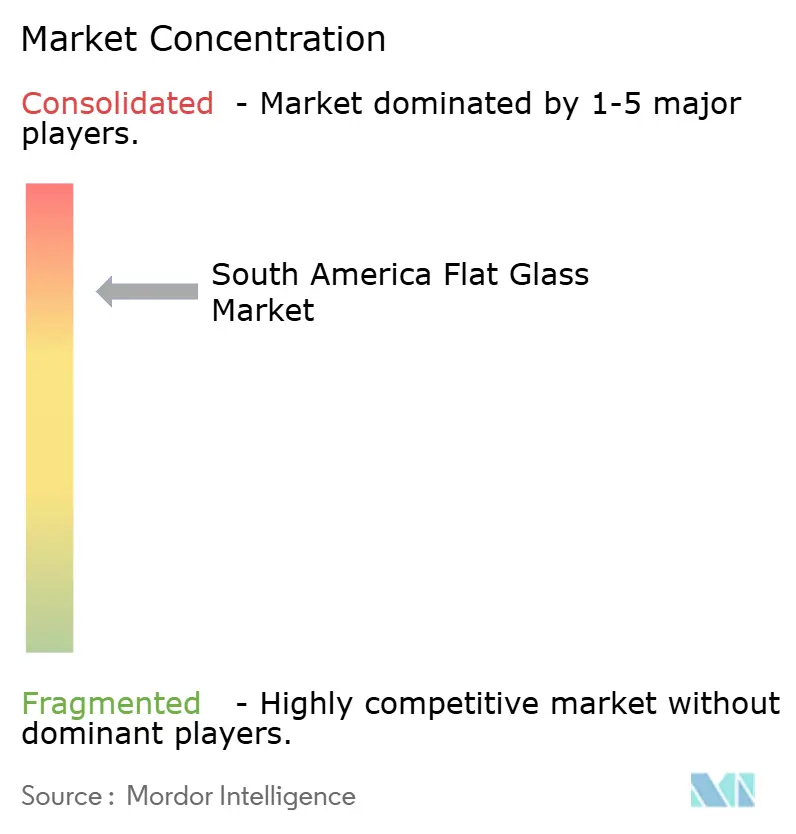

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Flat Glass Market Analysis by Mordor Intelligence

The South America Flat Glass Market size is expected to increase from 2.46 million tons in 2025 to 2.53 million tons in 2026 and reach 2.91 million tons by 2031, growing at a CAGR of 2.85% over 2026-2031. The growth trajectory indicates a transition from commodity annealed substrates to value-added products designed to comply with building-energy codes and solar-module requirements. Volume growth is influenced by Brazil’s green-building credit initiatives, the expansion of photovoltaic installations in the Northeast and Atacama regions, and the recovery of automotive production in Mercosur. Capacity decisions are more significantly impacted by import-substitution policies and anti-dumping duties than by raw demand trends. Additionally, smaller producers face margin pressures due to feedstock costs and emission-compliance expenses. Established players with access to hybrid melters and sputtering lines are positioned to capitalize on opportunities by promoting low-E, laminated, and low-iron glass, thereby increasing revenue per ton, even as overall tonnage grows at a moderate rate.

Key Report Takeaways

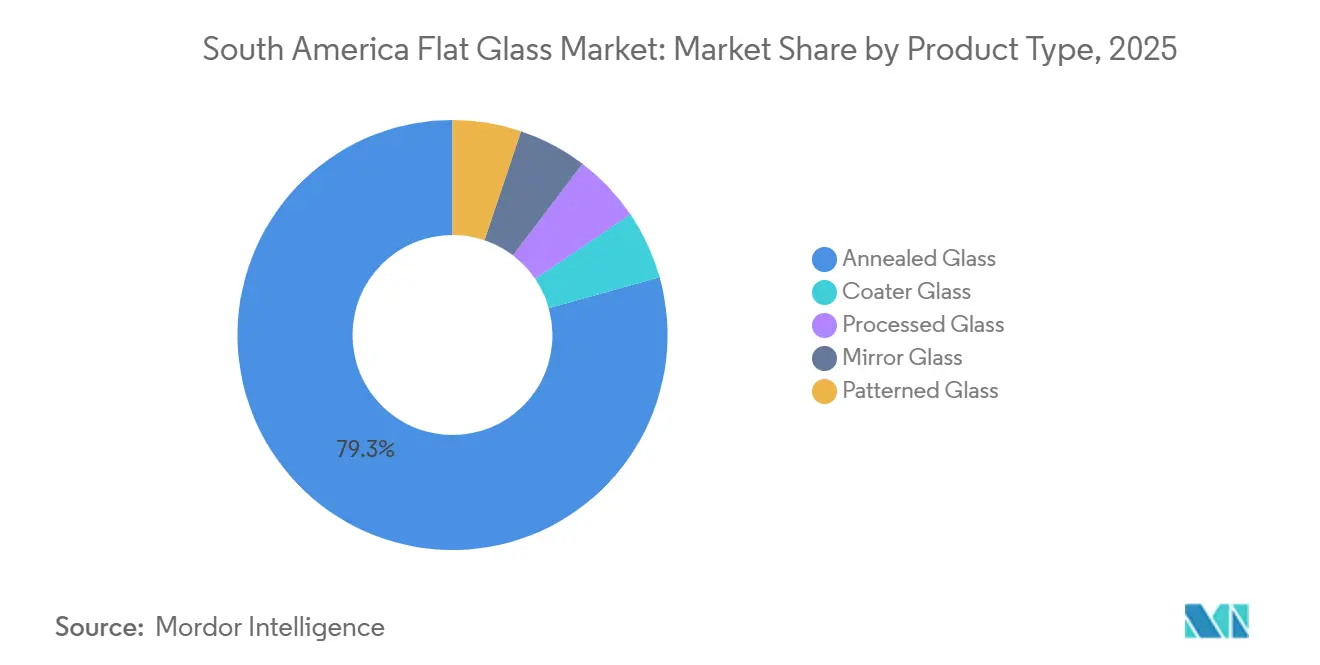

- By product type, annealed glass led with 79.32% of the South America flat glass market share in 2025, while processed glass is projected to advance at a 3.65% CAGR through 2031.

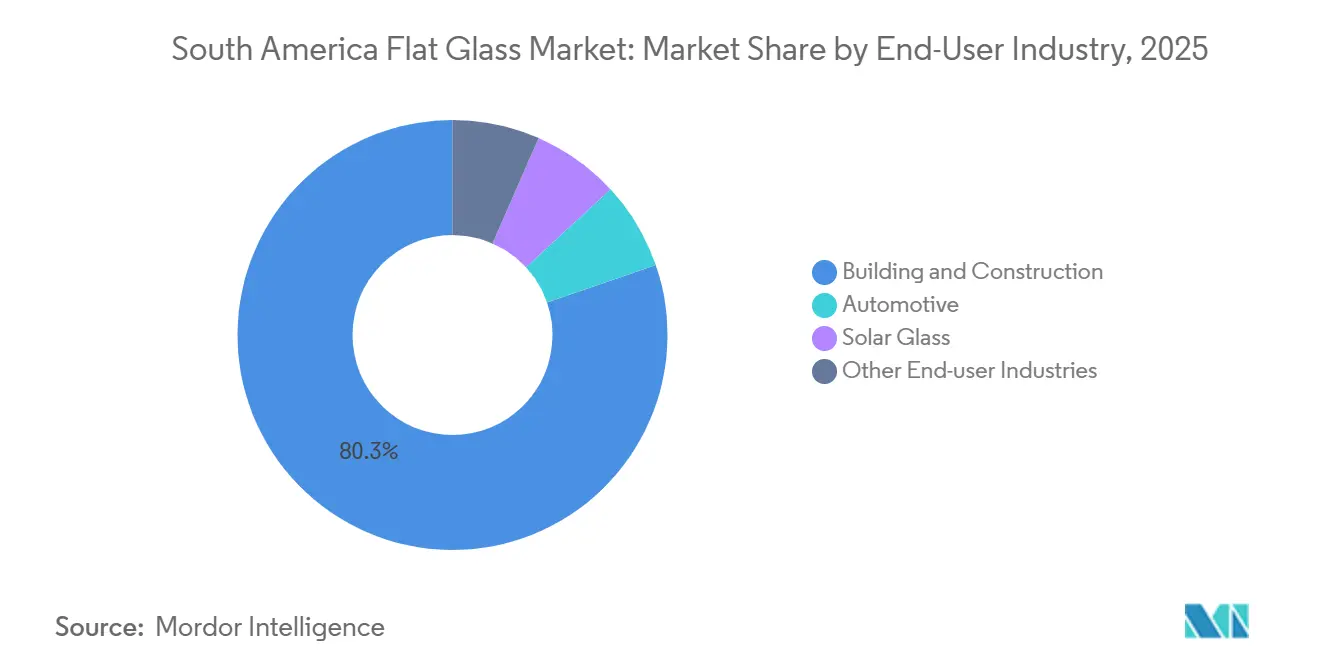

- By end-user industry, building and construction accounted for 80.27% of the South America flat glass market share in 2025, while solar glass is forecast to expand at a 5.52% CAGR through 2031.

- By geography, Brazil commanded 64.44% of the South America flat glass market share in 2025 and is set to grow at a 3.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Flat Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom in Tier-2 Brazilian cities | +0.8% | Brazil, with early gains in Curitiba, Belo Horizonte, Recife | Medium term (2-4 years) |

| Rapid scale-up of regional automotive output | +0.6% | Brazil and Argentina, spill-over to Colombia | Short term (≤ 2 years) |

| Expansion of utility-scale solar farms | +0.7% | Brazil Northeast, Chile Atacama, Argentina Patagonia | Long term (≥ 4 years) |

| Government green-building tax incentives | +0.4% | Colombia national, Brazil select municipalities, Chile urban centers | Medium term (2-4 years) |

| On-shoring of ultra-thin display glass lines | +0.2% | Minimal near-term relevance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Boom in Tier-2 Brazilian Cities

Secondary metropolitan areas outside São Paulo and Rio de Janeiro are receiving public infrastructure investments and private real estate funding at a faster pace compared to the saturated primary markets. Building permits issued in Curitiba, Belo Horizonte, and Recife increased by 9% to 14% in 2025, contributing an estimated 180,000 square meters of façade area[1]Instituto Brasileiro de Geografia e Estatística, “Pesquisa da Construção 2025,” ibge.gov.br. Developers in these cities continue to prioritize cost-effective annealed and heat-strengthened glass, ensuring consistent float-line utilization, even as premium low-E coatings gain popularity in other regions. The geographic spread of demand requires producers to establish regional service centers, increasing working capital needs but enhancing customer retention in areas where Asian exporters face challenges in providing just-in-time deliveries. This construction growth supports stable demand for standard substrates while allowing processors to expand magnetron-sputtering and laminating capabilities.

Rapid Scale-Up of Regional Automotive Output

Stellantis has allocated USD 385 million for its Córdoba, Argentina facility as part of its USD 6.22 billion South America manufacturing roadmap through 2030. This upgrade will boost capacity by 50,000 units annually, supporting Mercosur duty-free trade into Brazil, Paraguay, and Uruguay. Brazil’s hybrid-flex vehicle rollout, which integrates ethanol capability with electric motors, is increasing acoustic requirements, necessitating larger, multi-layer windshields and side glazing. Glass content per vehicle is expected to grow by 8-12%, further driving flat-glass demand beyond its 10-12% volume share. Consequently, automotive growth is directing fabrication investments toward tempering, lamination, and acoustic interlayers, strengthening the South America flat glass market even during construction slowdowns.

Expansion of Utility-Scale Solar Farms

Solar energy deployments in Brazil reached 55 GW by March 2025, advancing at a 23% CAGR, while Chile’s Atacama Desert hosts 12 GW of operational capacity with an additional 8 GW under construction. Homerun Resources has initiated a 1,000-ton-per-day low-iron float line project, financed at EUR 150 million with Banco Nacional de Desenvolvimento Econômico e Social (BNDES) support, reducing the region’s 99% import dependence for photovoltaic glass. The facility’s 365,000-ton annual capacity represents approximately 12% of projected 2031 demand, shifting production from commodity substrates to high-margin solar glass. Procurement policies favoring bifacial modules and anti-reflective coatings further enhance processed-glass penetration, supporting long-term volume growth in the South America flat glass market.

Government Green-Building Tax Incentives

Colombia’s March 2026 technical guide on sustainable construction offers a 19% VAT exemption, 33.3% accelerated depreciation, and loans at rates as low as 6.5% for projects utilizing energy-rated glazing. Brazil extended USD 2.1 billion in BNDES green-building credit lines in 2025, while Chile’s Sustainable Bond Framework, launched in March 2026, directs institutional funds toward timber-and-glass façades that reduce energy consumption by 30%. These fiscal incentives improve the economic viability of low-E and triple-silver coatings in mid-market residential projects, expanding demand beyond premium commercial segments. Producers with magnetron-sputtering capacity benefit directly, while commodity suppliers face margin pressures unless they transition to higher-value products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile soda-ash and LNG prices | -0.4% | Brazil, Argentina, Chile (furnace-intensive regions) | Short term (≤ 2 years) |

| Rising low-cost imports from Asia | -0.3% | Brazil coastal markets, Argentina Buenos Aires corridor | Short term (≤ 2 years) |

| Stricter furnace-emission regulations | -0.2% | Brazil national, Chile Santiago metropolitan, Colombia urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Soda-Ash and LNG Prices

Soda-ash prices at Santos increased by 18% year-on-year in Q4 2025 due to export restrictions from Turkey’s Kazan Soda Elektrik, while Petrobras raised liquefied natural gas tariffs by 22% in January 2026, aligning with European benchmarks. These cost increases reduced float-line operating margins by 200-300 basis points. Developers were forced to either absorb these costs or switch to alternative materials like aluminum and polycarbonate, reducing glass demand. Smaller furnaces without hedging mechanisms delayed rebuilds, accelerating ownership consolidation among multinationals with long-term soda-ash contracts and LNG swaps.

Rising Low-Cost Imports from Asia

Flat-glass imports in Brazil surged from 0.7% of apparent consumption in 2022 to 12% in 2023, driven by Malaysian, Pakistani, and Turkish suppliers undercutting domestic prices by up to 20%. Provisional anti-dumping duties, imposed nine months after investigations began, allowed importers to secure multi-year contracts. A sunset review of existing tariffs on Chinese, Egyptian, UAE, and Mexican glass commenced in February 2026, creating uncertainty around pricing stability. Expansion plans, such as Saint-Gobain’s potential sixth float line, depend on the outcome, making trade policy a critical factor for the South America flat glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Processed Glass Builds Momentum

The South America flat glass market size for annealed glass accounted for 79.32% of the total volume in 2025. Although still dominant, its share is expected to decline as processed glass is projected to grow at a 3.65% CAGR through 2031. Laminated and tempered glass meet hurricane code requirements in Brazil’s Northeast, while low-E coatings comply with Chile’s Decreto Nº5 thermal-performance standards. Producers like Guardian Glass and Saint-Gobain have installed triple-silver sputtering lines to cater to Minha Casa Minha Vida projects, which require solar heat-gain coefficients below 0.35. Processed glass offers higher margins, offsetting feedstock volatility and providing pricing power despite gradual volume increases.

Cebrace’s Atmos low-carbon series reduces embedded emissions by 50% to approximately 5 kg CO₂ per square meter, aligning with Leadership in Energy and Environmental Design (LEED) and Excellence in Design for Greater Efficiencies (EDGE) certifications in Colombia, where Law 1715/2014 allows 50% tax deductions for efficiency investments. Mirror and patterned glass remain niche, catering to décor and automotive rear-view mirrors. As processed products gain traction, annealed glass pricing softens, as seen in Saint-Gobain’s 2025 results, where Latin America revenue increased by 13.5% against an 8% volume rise, indicating a significant product mix shift. This trend positions processed substrates as the primary growth driver for the South America flat glass market.

By End-User Industry: Solar Glass Takes the Growth Lead

Building and construction accounted for 80.27% of flat glass consumption in 2025, but its growth is tied to macroeconomic trends. Solar glass is projected to grow at a 5.52% CAGR through 2031, the fastest among end-user industries. Homerun Resources’ 1,000-ton-per-day plant will localize 365,000 tons of low-iron capacity, meeting approximately 40% of Brazil’s 2031 module needs. Photovoltaic substrates require advanced coatings and higher iron-removal standards, driving value per ton and prompting furnace conversions.

Automotive demand is also rising, driven by hybrid-flex vehicles requiring acoustically damped, larger windshields. Appliances, furniture, and electronics represent smaller shares, growing in line with GDP. The combined growth of solar and automotive segments mitigates market cyclicality, ensuring long-term stability.

Geography Analysis

Brazil retained 64.44% of regional volume in 2025 and is on track for a 3.25% CAGR to 2031. The BNDES released USD 2.1 billion in green-building loans during 2025, and Federal Decree 7,762/2012 requires energy-rated glazing in public works, anchoring demand even during broader construction lulls[2]Banco Nacional de Desenvolvimento Econômico e Social, “Relatório Anual 2025,” bndes.gov.br. São Paulo and Rio de Janeiro still represent more than half of national tonnage, yet double-digit permit growth in Curitiba, Belo Horizonte, and Recife indicates geographic diversification. Homerun Resources’ solar-glass complex, scheduled for 2027 commission, will divert 12% of Brazilian output into photovoltaic applications, lowering annealed prices in traditional channels while raising aggregate margins through product-mix gains.

Argentina leverages Stellantis’ Córdoba upgrade and Mercosur duty-free flows for automotive glazing. Colombia’s new tax guide secures 19% VAT relief and cheap credit below 6.5% for energy-rated façades, steering Bogotá and Medellín developers toward low-E coatings despite smaller absolute volumes. Chile enforces Decreto Nº5 thermal standards on residential projects above 1,000 m², making accredited laboratory tests mandatory and favoring domestic processors with ISO-certified labs.

Peru and the rest of South America capture the remaining regional demand. Peru’s 491,904-unit housing deficit signals long-run construction potential, yet per-capita glass consumption remains below 15 kg, half Brazil’s level, due to informal self-build housing. Smaller economies depend on Brazilian exports, which means Brazilian trade policy and furnace downtime ripple across the subcontinent.

Competitive Landscape

The South America flat glass market is highly concentrated, with the five largest firms being AGC Inc., Saint-Gobain, Vitro, Guardian Industries, LLC, and Cebrace Cristal Plano Ltda. Saint-Gobain disclosed that a sixth float line depends on continued anti-dumping duties. Capacity plans, therefore, hinge on regulatory shields more than pure demand. AGC and Saint-Gobain are piloting hybrid electric melters capable of halving natural-gas use, a response to Brazil’s CONAMA Resolution 436 that caps NOx at 500 mg/Nm³. Decarbonization technology will separate leaders from laggards once emission standards tighten.

Homerun Resources introduced disruptive capacity in solar glass that challenges incumbents reliant on construction float. Guardian and Saint-Gobain added triple-silver sputtering lines to capture tax-incentivized low-E demand in Colombia and Chile. Smaller regional furnaces face capital hurdles in retrofitting electrostatic precipitators or selective catalytic reduction units, accelerating consolidation. Imports from Turkey, Malaysia, and Pakistan proved competitive until mid-2025, when duties curbed landed volumes, yet the February 2026 sunset review on China, Egypt, UAE, and Mexico glass tested domestic pricing power again.

The competitive dynamic to 2031 revolves around three unknowns. First, whether incumbents can roll out hybrid melters ahead of fuel-price spikes. Second, if solar-glass localization lifts or cannibalizes construction float margins. Third, whether trade-defense frameworks remain intact long enough to justify new float lines. Players who solve these variables stand to deepen their share in the South America flat glass market.

South America Flat Glass Industry Leaders

Guardian Industries, LLC

Vitro

Cebrace Cristal Plano Ltda.

AGC Inc.

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Homerun Resources Inc. signed a Letter of Intent with Nikolaus Sorg GmbH & Co. KG to develop a 1,000-ton-per-day solar glass manufacturing plant in Santa Maria Eterna, located in the municipality of Belmonte, Bahia, Brazil. The Solar Glass Project is expected to incorporate advanced technology for solar glass manufacturing, including an electric boosting system designed to enhance energy efficiency and reduce the carbon footprint.

- September 2025: Cebrace Cristal Plano Ltda. introduced ATMOS, South America's first low-carbon flat glass, composed of approximately 70% recycled materials and produced using renewable energy. This glass reduces greenhouse gas emissions by about 50% compared to traditional production methods, representing a notable advancement in sustainable construction within the region.

South America Flat Glass Market Report Scope

Flat glass is a sheet-form glass primarily manufactured using the float process, where molten glass is floated on molten tin to produce high-quality, distortion-free surfaces. It is extensively utilized in construction, automotive, and electronics industries for applications such as windows, mirrors, and displays. The main types of flat glass include float glass, sheet glass, and rolled glass, which can undergo additional treatments to become tempered safety glass or laminated glass.

The South America Flat Glass Market is segmented into product type, end-user industry, and geography. By product type, the market is segmented into annealed glass, coater glass, processed glass, mirror glass, and patterned glass. By end-user industry, the market is segmented into building and construction, automotive, solar glass, and other end-user industries. By geography, the market is segmented into Brazil, Argentina, Colombia, Chile, Peru, and rest of South America. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Annealed Glass |

| Coater Glass |

| Processed Glass |

| Mirror Glass |

| Patterned Glass |

| Building and Construction |

| Automotive |

| Solar Glass |

| Other End-user Industries |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Product Type | Annealed Glass |

| Coater Glass | |

| Processed Glass | |

| Mirror Glass | |

| Patterned Glass | |

| By End-user Industry | Building and Construction |

| Automotive | |

| Solar Glass | |

| Other End-user Industries | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of the South America flat glass market?

The South America flat glass market size stands at at 2.53 million tons in 2026 and is projected to reach 2.91 million tons by 2031.

Which product type is growing fastest through 2031?

Processed glass is expected to post a 3.65% CAGR through 2031.

What is driving demand for solar glass in the region?

Rapid photovoltaic rollouts in Brazil’s Northeast and Chile’s Atacama, coupled with Homerun Resources’ local low-iron float capacity, are expected to push solar glass volumes at a 5.52% CAGR to 2031.

Why is Brazil critical to regional supply dynamics?

Brazil controls 64.44% of the South America flat glass tonnage, benefits from BNDES green-building loans, and houses most float lines, so its trade and environmental policies steer regional pricing.

Page last updated on: