South America Fintech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

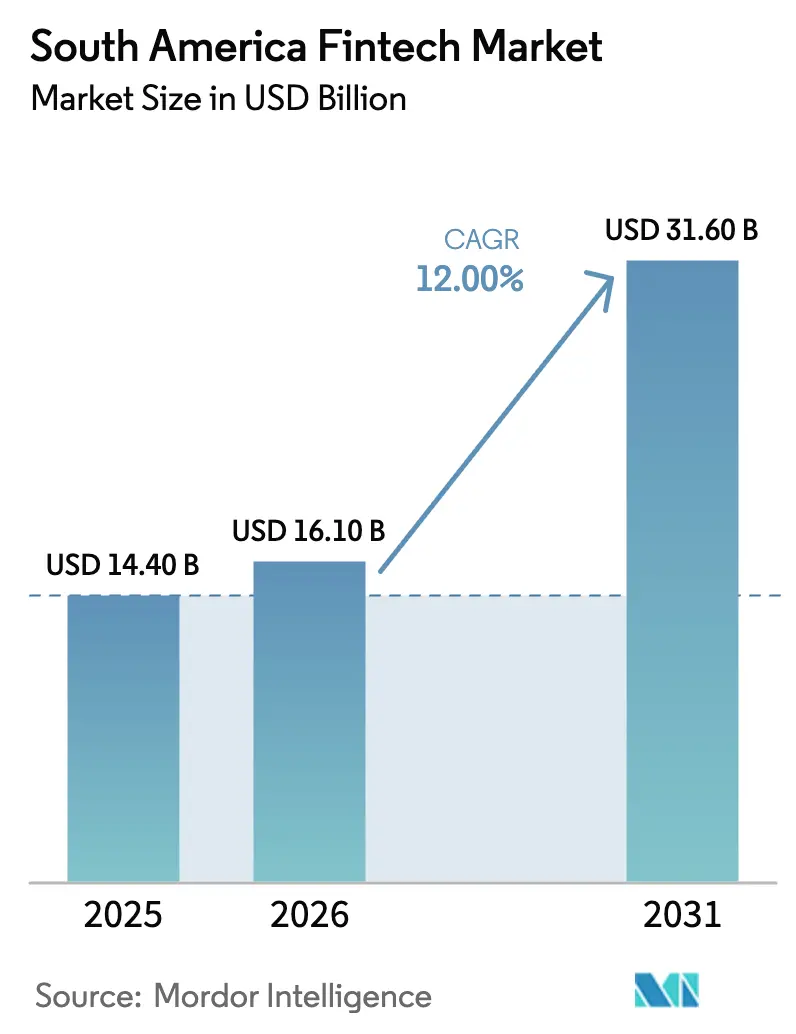

| Base Year Market Size (2025) | USD 14.40 Billion |

| Market Size (2026) | USD 16.10 Billion |

| Market Size (2031) | USD 31.60 Billion |

| Growth Rate (2026 - 2031) | 12.00% CAGR |

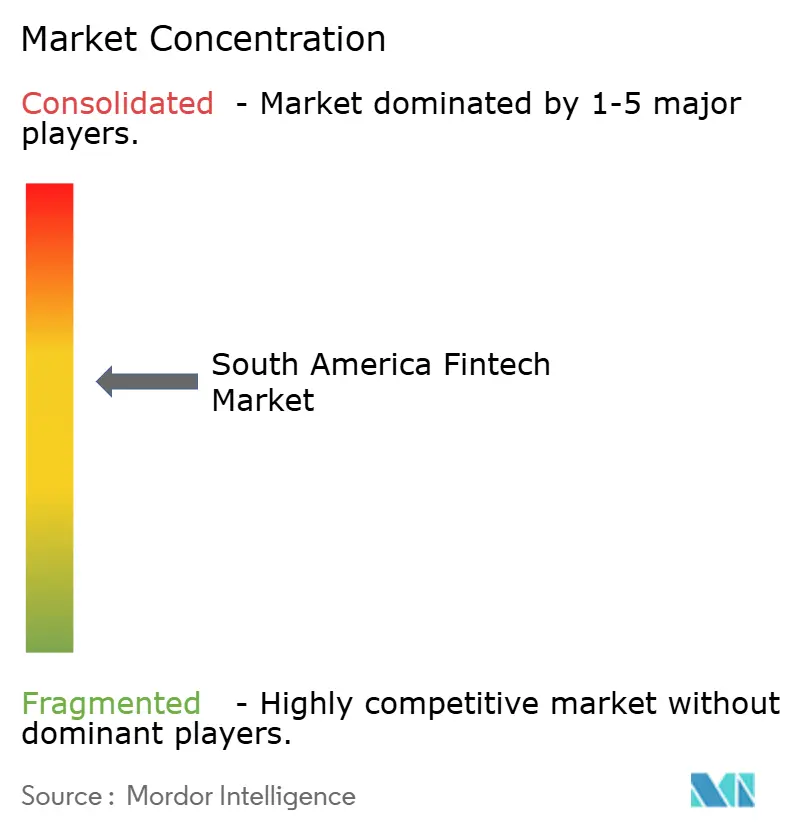

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Fintech Market Analysis by Mordor Intelligence

The South America Fintech Market size is expected to grow from USD 14.40 billion in 2025 to USD 16.10 billion in 2026 and is forecast to reach USD 31.60 billion by 2031 at 12% CAGR over 2026-2031.

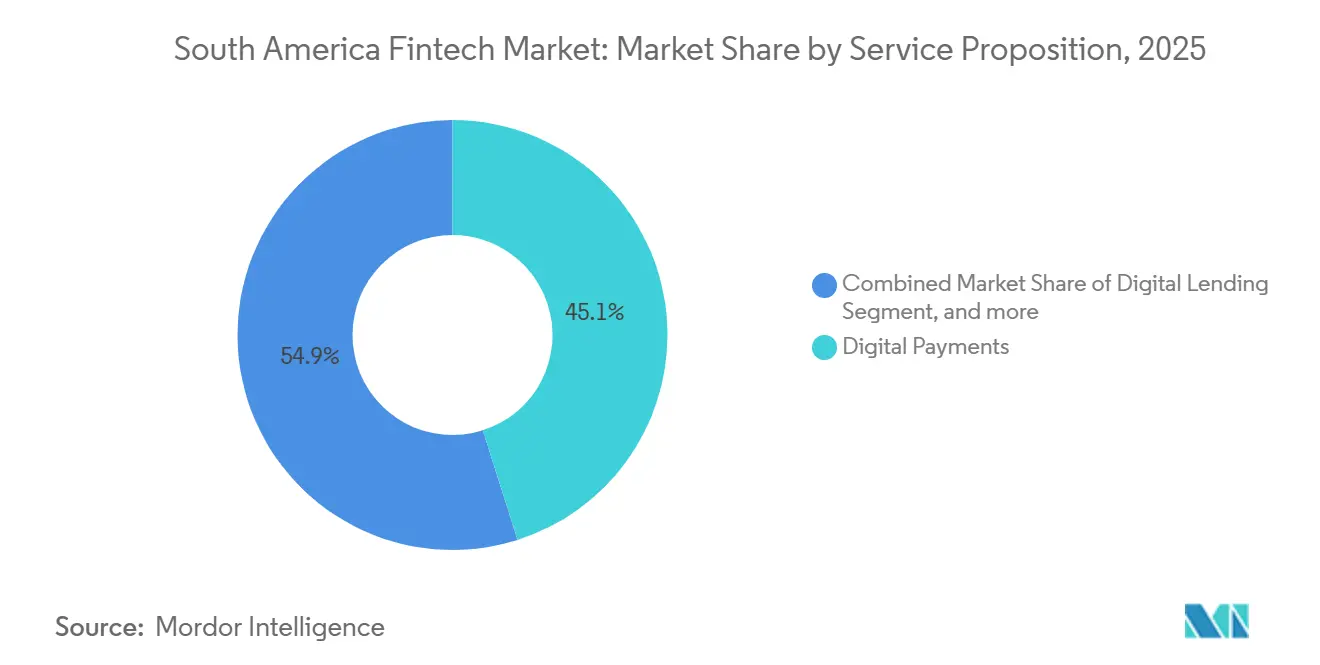

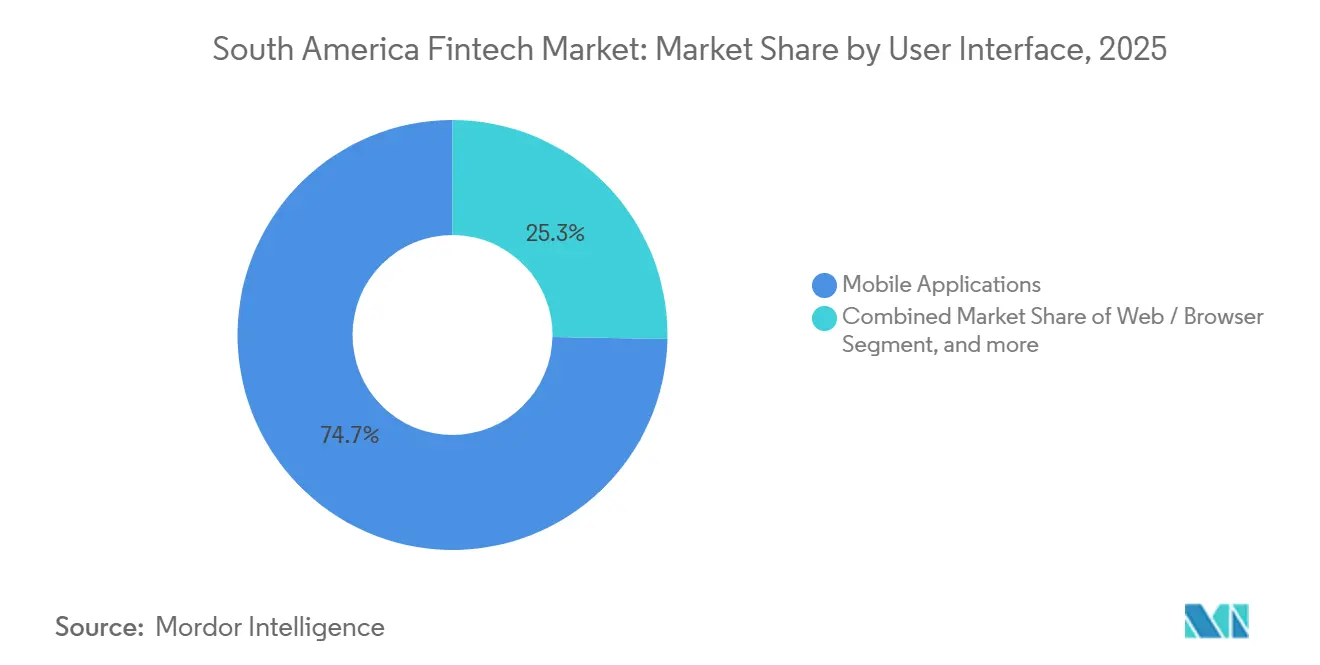

Digital payments led activity with a 45.0% share, while digital lending is set to expand at the fastest pace, with a 21.3% CAGR, as consumer credit and SME financing continue to scale. Retail users drove 68.6% of usage in 2025, and mobile applications accounted for 74.7% of interface interactions, underscoring a mobile-centric pathway for onboarding and engagement. Short-term headwinds persist from interchange caps, elevated interest rates, and FX controls that compress take rates and settlement economics, particularly in Brazil and Argentina. Competitive intensity is high as neobanks and embedded-finance platforms cross-sell credit, insurance, and investment products, illustrated by Nubank’s 127 million customers[1]Nu Holdings Ltd., “Nu Holdings Ltd. Reports Third Quarter 2025 Financial Results,” Nu Holdings Ltd., international.nubank.com.br and Mercado Pago’s 72 million monthly active users across the region[2]Mercado Libre, “Financial Results Third Quarter 2025,” Mercado Libre, news.mercadolibre.com.

Key Report Takeaways

- By service proposition, digital payments accounted for 45.0% of the South America fintech market in 2025, while digital lending is forecast to expand at a 21.3% CAGR through 2031.

- By end user, the retail segment accounted for 68.6% of the South America fintech market share in 2025 and is projected to grow at a 13.3% CAGR through 2031.

- By user interface, mobile applications commanded a 74.7% share of the South America fintech market in 2025 and are expected to post a 15.7% CAGR to 2031.

- By geography, Brazil led the South America fintech market with a 62.3% share of the South America fintech market in 2025, while Peru is projected to record the fastest growth at a 17.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Fintech Market Trends and Insights

Drivers Impact Analysis*

| (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|

| RTP scale-up and features | +3.2% | Brazil, spill-over to Argentina, Peru, Chile | Medium term (2-4 years) |

| Open finance data portability | +2.1% | Brazil, Chile, Colombia, Mexico, Argentina | Medium term (2-4 years) |

| Embedded finance in platforms | +1.8% | Brazil, Argentina, Mexico | Short term (≤ 2 years) |

| SoftPOS and low-cost acceptance | +1.5% | Brazil, Peru, Chile | Short term (≤ 2 years) |

| Dollar-linked savings via fintech | +2.0% | Argentina, Brazil, region-wide | Medium term (2-4 years) |

| Tokenized deposits and CBDC | +1.4% | Brazil, Argentina, region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

RTP Scale-Up and Features Propel Volume Growth

Real-time payments now anchor transaction growth across the South America fintech market, led by Brazil’s Pix, which handled 63.4 billion transactions in 2024 as adoption approaches ubiquity among adults. Pix’s 24/7 availability and rapid settlement underpinned a surge to 163 million registered users by late 2024, while new features such as Pix Automático and contactless tap-to-pay expanded use cases for subscriptions and point-of-sale payments. Peru’s interoperable rails, anchored by Yape and PLIN, support merchant acceptance in urban retail and micro-commerce. Early cross-border pilots linking Pix with neighboring markets are shortening settlement windows and reducing FX spreads for remittance and e-commerce corridors in the South America fintech market. Platform adoption has been reinforced by large ecosystems, with Mercado Pago enabling instant disbursements to its 72 million monthly active users and StoneCo reporting a 95% year-over-year increase in Pix transactions among MSMB clients in early 2025. Regulatory clarity supports scale, including Brazil’s interoperability mandates and ongoing instant payment initiatives in Chile and Colombia for mid-2026 timelines, as well as enhanced KYC and biometric checks in response to elevated APP fraud reports.

Open Finance Data Portability Unlocks Credit and Advisory

Brazil’s open finance system records more than 43 million active user consents and processes over 1.5 billion API calls weekly, placing it among the largest initiatives globally by transaction volume. Central bank directives require data sharing across transactional, credit, and investment domains for qualifying institutions, enabling third parties to price unsecured, payroll-linked, and secured credit using verified account and salary flows. Nubank’s secured-lending portfolio rose 133% year over year in 2025, assisted by consented access to income and account data that tightened underwriting and collection performance. Chile’s CMF issued General Rule No. 514 in July 2024 to require standardized APIs by July 2026, and Colombia published a draft decree in June 2025 to extend coverage beyond banking into insurance and pensions. Argentina’s Executive Decree No. 353 of 2025 formalized an open finance system with BCRA oversight and consent-based data sharing, further lowering barriers to multi-product financial advice in the South America fintech market. Despite momentum, differing data field standards and nascent cross-border interoperability raise integration costs and complexity for smaller providers.

Embedded Finance in E-Commerce and Super Apps

Embedded finance deepened distribution in the South America fintech market as platforms integrated payments, credit, and insurance natively in checkout and app journeys. Mercado Libre’s fintech unit generated USD 3.2 billion in net revenue in Q3 2025, up 65% year over year on an FX-neutral basis, driven by in-checkout BNPL, merchant credit, and working-capital loans. Its credit portfolio reached USD 11 billion, with credit-card balances representing a significant portion, underwritten using marketplace transactions and delivery touchpoints that provide rich behavioral signals. Neobanks raised engagement through partner offers and embedded protections, with Nubank highlighting customer savings from strategic partnerships that reinforce usage and lift lifetime value. Brazil’s central bank classifies embedded-finance providers as payment institutions or credit intermediaries depending on product scope, applying capital and prudential standards that anchor stability while allowing innovation. Chile’s draft open-finance rules enable third-party payment initiation from consumer accounts, which can bypass traditional card networks and reduce merchant discount rates in the South America fintech market.

Dollar-Linked Savings and Stablecoin Adoption

Stablecoins gained traction as a hedge against local-currency volatility, with Latin America processing USD 1 trillion in stablecoin transactions from mid-2022 to mid-2025 and Argentina leading in penetration among adults[3]Chainalysis, “The 2025 Geography of Cryptocurrency Report,” Chainalysis, chainalysis.com. Brazilian fintechs integrated on-ramps, and Nubank reported significant growth in USDC balances during 2024 as customers used tokenized dollars for remittances and cross-border e-commerce. Mercado Libre introduced a dollar-denominated savings product backed by USDC reserves, extending accessible dollar-linked yield to retail clients within a unified app experience. Brazil’s Law 14,478 positions the central bank as the AML and CFT authority for virtual assets and supports supervised custody by payment institutions, which brings crypto services into regulated perimeters. Argentina’s Law 27,739 and CNV resolutions during 2024 and 2025 established a VASP registration regime that requires capital adequacy, segregated client funds, and periodic disclosures, reinforcing safeguards for tokenized savings flows. Taxes and on-ramp charges still shape adoption, including Brazil’s 3.5% IOF on FX transactions, which raise the effective cost of crypto conversions and remittances.

Restraints Impact Analysis*

| Driver / Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High customer acquisition costs & low financial literacy | -1.6% | Peru, Colombia, Ecuador, rural Brazil | Long term (4+ years) |

| Fee caps squeeze economics | -1.2% | Argentina, Brazil | Short term (≤ 2 years) |

| APP fraud on instant rails | -0.9% | Brazil, spill-over to Argentina, Chile | Short term (≤ 2 years) |

| FX controls, settlement frictions | -1.4% | Argentina, Brazil, region-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Customer Acquisition Costs and Low Financial Literacy as Structural Growth Barriers

High customer acquisition costs, coupled with persistently low financial literacy across several South American markets, continue to constrain fintech scalability. Despite rapid digital adoption, consumer onboarding still requires significant marketing spend, offline verification, and education-driven engagement. This raises blended CAC and depresses lifetime value economics, particularly in underbanked and rural segments. The challenge is structural and long‑duration, pushing fintechs to invest in financial education, agent-assisted onboarding, and data-led personalization to improve conversion and retention.

FX Controls, Settlement Frictions

Strict capital controls in Argentina and related FX settlement constraints delay cross-border flows and add costs for remittances and merchant payouts in the South America fintech market. Brazil’s 3.5% IOF on FX transactions increases costs for stablecoin on- and off-ramps and other foreign-currency purchases. These constraints have accelerated the adoption of specialized Orchestration-as-a-Service models that aggregate local methods and route payments to avoid costly correspondent chains where regulations allow. Even with orchestration and instant rails, reconciliation and currency conversion often require buffers and hedges that weigh on unit economics for providers serving frontier corridors. Momentum toward bilateral regulatory cooperation will be central to reducing friction and improving the availability of funds across currencies in the South American fintech market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Digital Lending Leads CAGR as Credit Appetite Expands

Digital payments captured 45.1% of the South American fintech market share in 2025, underpinned by rails such as Brazil’s Pix and Argentina’s Transferencias 3.0, which have lowered acceptance costs for consumers and merchants. Within the segment mix, digital lending is forecast to expand at a 21.3% CAGR between 2026 and 2031, highlighting acceleration in the South American fintech market as thin-file underwriting scales through open-finance data and embedded-credit channels. Lenders now combine consented bank data with marketplace and logistics histories to assess repayment behaviour for consumer and MSMB borrowers, compressing approval times while lifting acceptance rates for previously underserved cohorts. Nubank’s secured-lending portfolio grew 133% year over year in 2025, aided by access to verified salary deposits and account flows that strengthened origination quality and collections. Mercado Libre’s fintech arm scaled credit issuance to USD 11 billion by Q3 2025, using marketplace transaction data and delivery touchpoints to calibrate revolving balances, delinquency, and pricing.

Momentum in investment and insurance adjacencies has supported a more complete proposition for retail and MSMB users. Mercado Pago’s assets under management doubled year over year to USD 15.1 billion in Q3 2025 as money-market products were bundled into daily-wallet experiences with attractive benchmark-linked yields. Neobanks and payments platforms have introduced targeted protection products for small businesses, embedding coverage options into onboarding and checkout flows to increase attach rates over time. As providers expand into lending at scale, compliance standards linked to data protection and AML have increased fixed costs and favoured players with robust governance and capital, reinforcing consolidation dynamics in the South American fintech market. On balance, the South America fintech industry continues to shift from single-product payments toward multi-product financial services, with credit-led monetization driving the next leg of growth, where consented data support underwriting and collections.

By End-User: Retail Dominates Share While Business Fintech Deepens Penetration

Retail users accounted for 68.6% of overall activity in 2025 and are projected to grow at a 13.3% CAGR through 2031 as digital wallets, neobank accounts, and in-app financing extend reach across the consumer base. Nubank serves 127 million customers across Brazil, Mexico, and Colombia, with more than 83% of engagement via mobile apps that streamline payments, credit, and savings in a single interface. Retail consolidation of bill payments, P2P transfers, and investments into a single mobile wallet has increased cash-in volumes and deepened savings behaviour in key markets such as Brazil. Embedded payments and BNPL at checkout improve conversion and average order value, encouraging repeat usage and strengthening platform network effects in the South American fintech market. As retail adoption matures, providers are layering advisory features, biometric security, and AI-driven assistance to sustain engagement and reduce support costs.

Business end users, including MSMBs, gig workers, and enterprises, increasingly adopt multiple services, spanning acquisition and cash management to credit and cross-border payouts. Merchant platforms integrate payment acceptance, working capital financing, and settlement tools into unified dashboards to reduce reconciliation friction and improve cash flow visibility. Large enterprises expand local collection capabilities across countries through payment orchestration that supports alternative payment methods, instant payments, and multi-currency reconciliation under a single integration. Regulatory initiatives such as Pix Automático for recurring charges and open-finance data-sharing mandates in Chile and Colombia are expanding access to richer SME data, unlocking more accurate scoring and lower loss rates for business credit. Over the forecast period, the South America fintech industry is set to see faster uptake of embedded trade finance, supply-chain payments, and B2B BNPL as providers standardize data, streamline onboarding, and scale interoperable instant-payment acceptance.

By User Interface: Mobile Applications Lead Share and Growth

Mobile applications accounted for 74.7% of usage in 2025 and are projected to expand at a 15.7% CAGR through 2031, reflecting the region’s mobile-first internet adoption and the rapid advancement of in-app financial features. Smartphone penetration exceeds 75% across Brazil, Argentina, Chile, and Colombia, and app-first experiences now bundle QR payments, P2P transfers, and merchant checkout flows in a single journey. Nubank processes tens of billions of dollars in quarterly card purchase volume through its mobile-native interface, with the vast majority of customers engaging on iOS and Android rather than web portals. Mercado Pago’s 72 million monthly active users conduct billions of payment transactions annually within a unified app that links daily payments, credit, and savings.

Desktop web and browser-based interfaces serve enterprise dashboards, B2B portals, and workflows that require complex reconciliation and reporting. Payment orchestrators offer real-time settlement tracking and multi-country reconciliation through merchant portals that complement API integrations. POS and IoT devices, including SoftPOS-enabled smartphones, account for a meaningful minority of interactions as micro-merchants adopt contactless acceptance without dedicated hardware. Security-by-design is standardizing mobile development across the South American fintech market, with PCI’s SPoC requirements promoting biometrics, tokenization, and device-level encryption to protect card data. Privacy rules such as Brazil’s LGPD and Argentina’s Personal Data Protection Law reinforce consent and data-portability frameworks that guide product design and raise compliance rigor for mobile teams. As a result, the South American fintech market continues to favor mobile-first distribution, while web and device channels serve specialized use cases and enterprise requirements.

Geography Analysis

Brazil held 62.3% of the South American fintech market share in 2025, supported by Pix’s near-universal adoption and a mature open finance framework that processes over 1.5 billion API calls weekly. Pix processed 63.4 billion transactions in 2024 and continues to deepen merchant acceptance with QR and tap-to-pay features across retail and services. Nubank’s base in Brazil reached 110 million customers by Q3 2025, and Mercado Libre’s fintech operations contributed materially to consolidated results, underscoring the strength of platform-led financial ecosystems. Brazil’s VASP authorization regime, published in November 2025, takes effect in February 2026 with tiered capital requirements ranging from BRL 10.8 million (USD 1.95 million) to BRL 37.2 million (USD 6.72 million), consolidating crypto services under licensed players and signalling ongoing regulatory leadership for the South American fintech market.

Peru is projected to post the fastest geographic growth, with a 17.6% CAGR from 2026 to 2031, anchored by interoperable instant-payment rails and a growing user base across Yape and PLIN. The Central Reserve Bank’s collaboration with NPCI International on UPI-style infrastructure positions Peru to pioneer cross-border instant settlement within the Andean corridor, with design choices aimed at reducing FX spreads and speeding up fund availability. Licensing frameworks for electronic money and wallet providers clarify entry paths for neobanks, while financial inclusion gaps remain a growth lever for mobile wallets and embedded borrowing. According to the World Bank's Global Findex, a large share of Peruvian adults remains outside the formal banking system, which supports continued wallet adoption and targeted credit built on verified transaction histories.

Chile’s open-finance mandate, formalized in July 2024 through CMF General Rule No. 514 with a July 2026 implementation date, is expected to support innovation in scoring, wealth management, and payment initiation, with all CMF-supervised institutions required to participate. Digital wallets led by MACH and account-to-account payment specialists such as Khipu continue to expand consumer and merchant adoption as open-finance standards take shape. In Argentina, regulatory volatility coexists with the rapid uptake of dollar-linked savings and widespread wallet usage, and the central bank authorized licensed financial institutions to provide crypto custody and trading beginning April 2026 under Resolution 2026-03, signaling a shift toward regulated tokenized services. The rest of South America, including Colombia and Uruguay, remains important to regional expansion, with Colombia advancing instant-payment modernization and Uruguay piloting open-banking trials with multiple commercial banks. Cross-border regulatory cooperation remains a priority to enhance interoperability and scale across the South America fintech market.

Competitive Landscape

The South American fintech market remains moderately fragmented, with the top five players collectively accounting for a significant share of transaction volume, as platform ecosystems, regional neobanks, and specialized orchestrators compete on price, cross-sell, and distribution. Mercado Pago leverages the marketplace’s scale to cross-sell payments, credit, and savings, processing strong third-quarter volumes in 2025 and recording 65% year-over-year FX-neutral revenue growth in its fintech unit. Nubank focuses on AI-enabled underwriting and collections while expanding product breadth, which increased engagement and supported monetization uplift during 2025. Payment acquirers and processors sharpened their value propositions by integrating instant payments into merchant acceptance, while maintaining card acceptance flexibility to retain share in the South American fintech market.

White-space opportunities have concentrated around SME embedded finance, where merchant platforms and acquirers leverage transaction data to extend working capital and receivables finance. Brazil’s open-finance data portability equips lenders with richer SME histories for scoring and collections, helping to narrow long-standing access gaps for formal credit. StoneCo’s unified acceptance of Pix QR and SoftPOS reduced merchant churn in 2024 by expanding options for instant and card-based payments on a single device, thereby improving retention economics. Enterprise-focused orchestrators such as dLocal increased conversion by adding local alternative methods and account-to-account flows, strengthening cross-border acceptance while maintaining compliance with national licensing rules. As fee caps and FX frictions continue to shape unit economics, diversified revenue from lending, savings, and insurance has become central to resilience in the South America fintech market.

Regulation has raised capability thresholds and favored well-capitalized players with strong risk, AML, and data-governance programs. Brazil’s VASP authorization regime, effective February 2026, requires tiered capital ranging from BRL 10.8 million (USD 1.9 million) to BRL 37.2 million (USD 6.7 million) and prescribes disclosure and AML standards that will consolidate crypto services among licensed entities. In parallel, Argentina’s CNV and central bank rules formalize open finance and VASP registration, increasing the compliance burden for smaller entrants but clarifying pathways for scaling tokenized savings within regulated channels. Against this backdrop, leaders in the South American fintech market are differentiating through platform bundling, faster product cycles, and partnerships that add local payment methods and reduce cross-border settlement frictions.

South America Fintech Industry Leaders

Nubank (Nu Holdings)

Mercado Pago (Mercado Libre)

PagSeguro (PagBank)

StoneCo

PicPay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: dLocal partnered with DHL Express Brazil to automate Pix payments and accelerate parcel release processes in the country.

- December 2025: dLocal and Yuno expanded their partnership to simplify expansion for enterprises in emerging markets by combining local expertise and payment orchestration across 1,000-plus methods.

- August 2025: dLocal introduced SmartPix in Brazil to enable merchants to store Pix credentials and streamline recurring and on-file payments.

South America Fintech Market Report Scope

| Digital Payments |

| Digital Lending and Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

| Retail |

| Businesses |

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

| Brazil |

| Peru |

| Chile |

| Argentina |

| Rest of South America |

| By Service Proposition | Digital Payments |

| Digital Lending and Financing | |

| Digital Investments | |

| Insurtech | |

| Neobanking | |

| By End-User | Retail |

| Businesses | |

| By User Interface | Mobile Applications |

| Web / Browser | |

| POS / IoT Devices | |

| By Geography | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size and growth outlook for the South America fintech space?

The South America fintech market size is estimated at USD 16.1 billion in 2026 and is projected to reach USD 31.6 billion by 2031 at a 12% CAGR.

Which segment is expanding the fastest across South America?

Digital lending is the fastest-growing service proposition, forecast to expand at a 21.3% CAGR between 2026 and 2031 as open finance and embedded credit improve underwriting and access.

How dominant are mobile apps in user interactions?

Mobile applications accounted for 74.7% of interactions in 2025 and are expected to grow at a 15.7% CAGR through 2031, reflecting the region’s strong smartphone adoption.

Which country leads the region and which is growing the fastest?

Brazil leads with a 62.3% share on the back of Pix and open finance, while Peru is projected to post the fastest growth with a 17.6% CAGR to 2031.

How are real-time payments shaping competitive dynamics?

Pix has become the primary rail in Brazil with 63.4 billion transactions in 2024, and new features like Pix Automático plus cross-border pilots are broadening use cases and compressing settlement times.

What regulatory developments should operators watch in 2026?

Brazil’s VASP authorization regime effective February 2026 with tiered capital, and Argentina’s authorization for banks to offer crypto custody and trading by April 2026, are central changes for scaling tokenized services.

Page last updated on: