South America ESIM Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

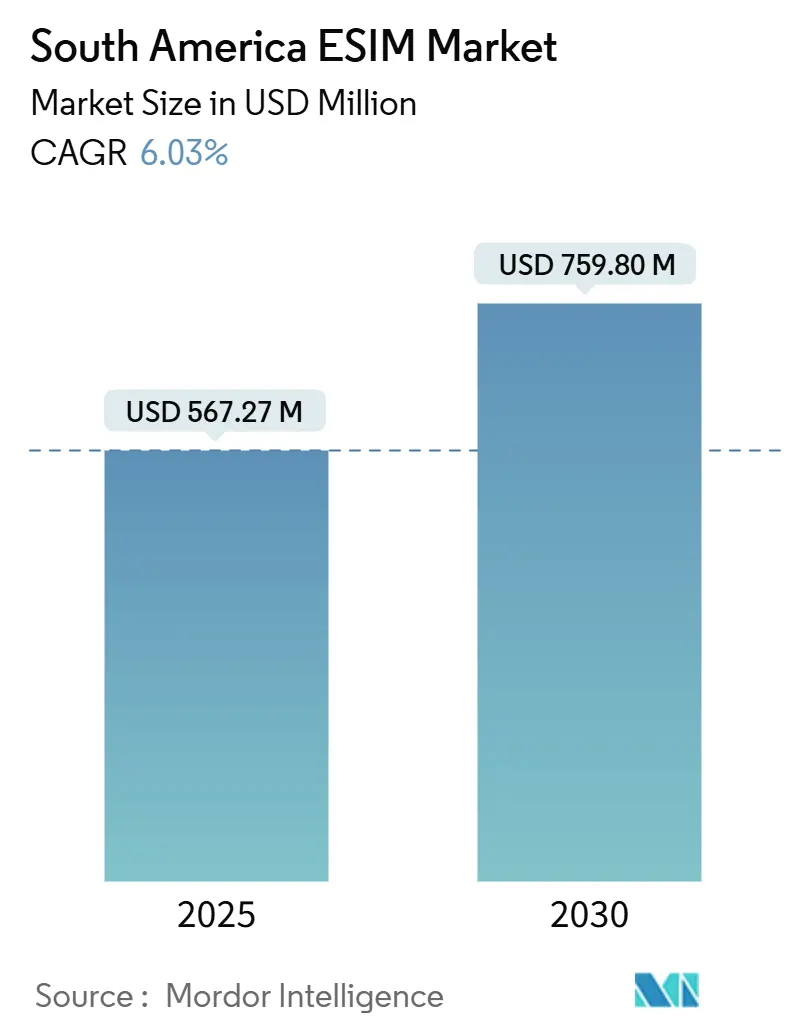

| Market Size (2025) | USD 567.27 Million |

| Market Size (2030) | USD 759.80 Million |

| Growth Rate (2025 - 2030) | 6.03% CAGR |

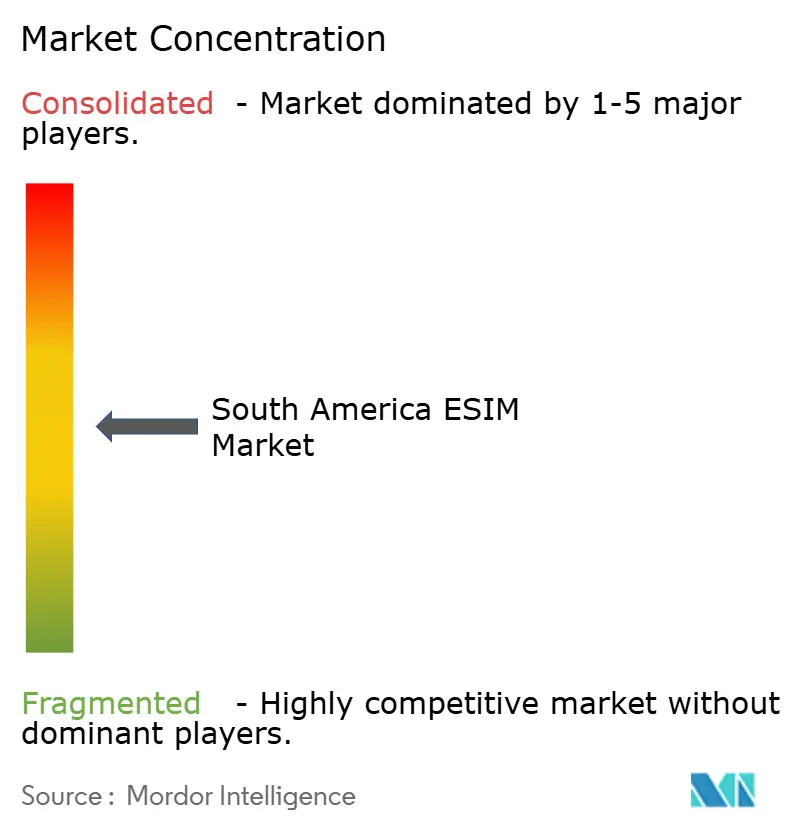

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America ESIM Market Analysis by Mordor Intelligence

The South America ESIM Market size is estimated at USD 567.27 million in 2025, and is expected to reach USD 759.80 million by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

Widening 5G footprints, a surge in eSIM-only smartphone launches, and regulatory push for smart-meter rollouts form the spine of this growth. Brazil’s 53.86% market share underscores the importance of progressive policies from ANATEL and the catalytic effect of the PIX instant-payment rail on digital onboarding. Hardware vendors such as Thales, IDEMIA, and Giesecke + Devrient continue to supply secure elements at scale, while operator-led portals from TIM Brasil and Claro simplify consumer migration. Fast-moving travel eSIM aggregators and fintechs are redrawing channel dynamics, but incumbent mobile network operators (MNOs) retain pricing power through bundled 5G data plans and value-added IoT services.

Key Report Takeaways

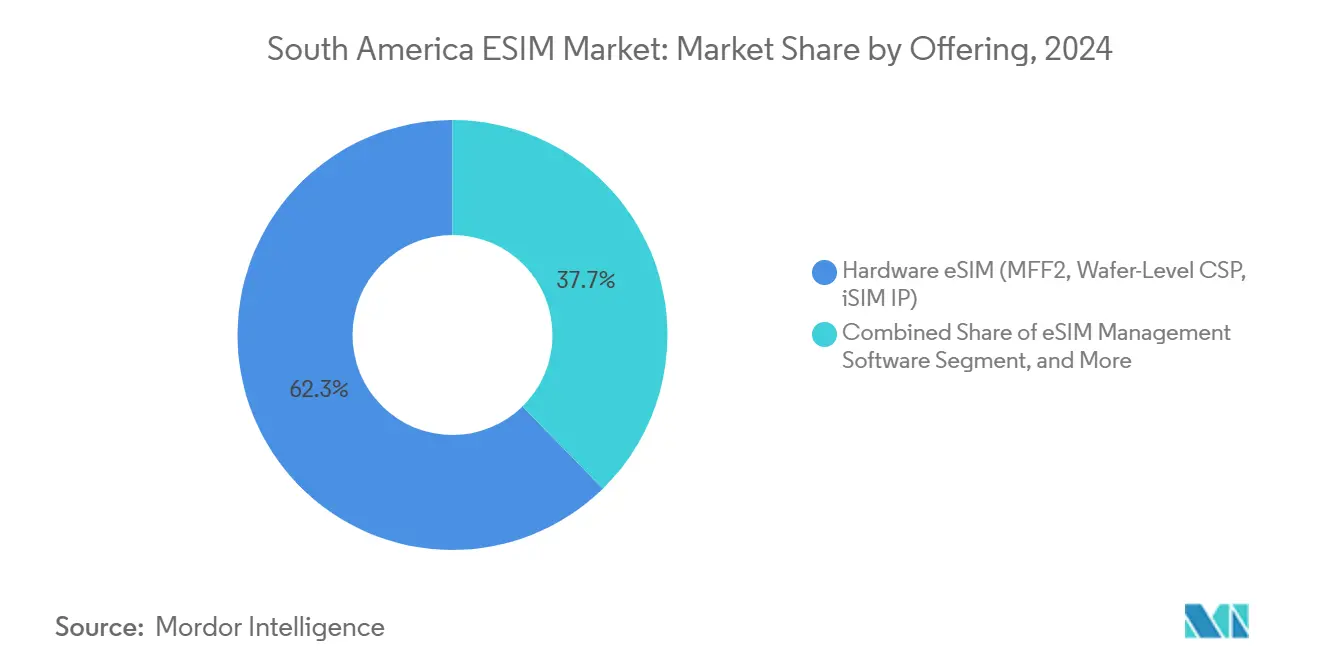

- By offering, hardware represented 62.33% of South America eSIM market share in 2024, whereas remote SIM provisioning services are projected to expand at a 13.01% CAGR through 2030.

- By device type, smartphones and feature phones commanded 73.05% of the South America eSIM market size in 2024, while M2M/IoT modules record the highest 17.48% CAGR to 2030.

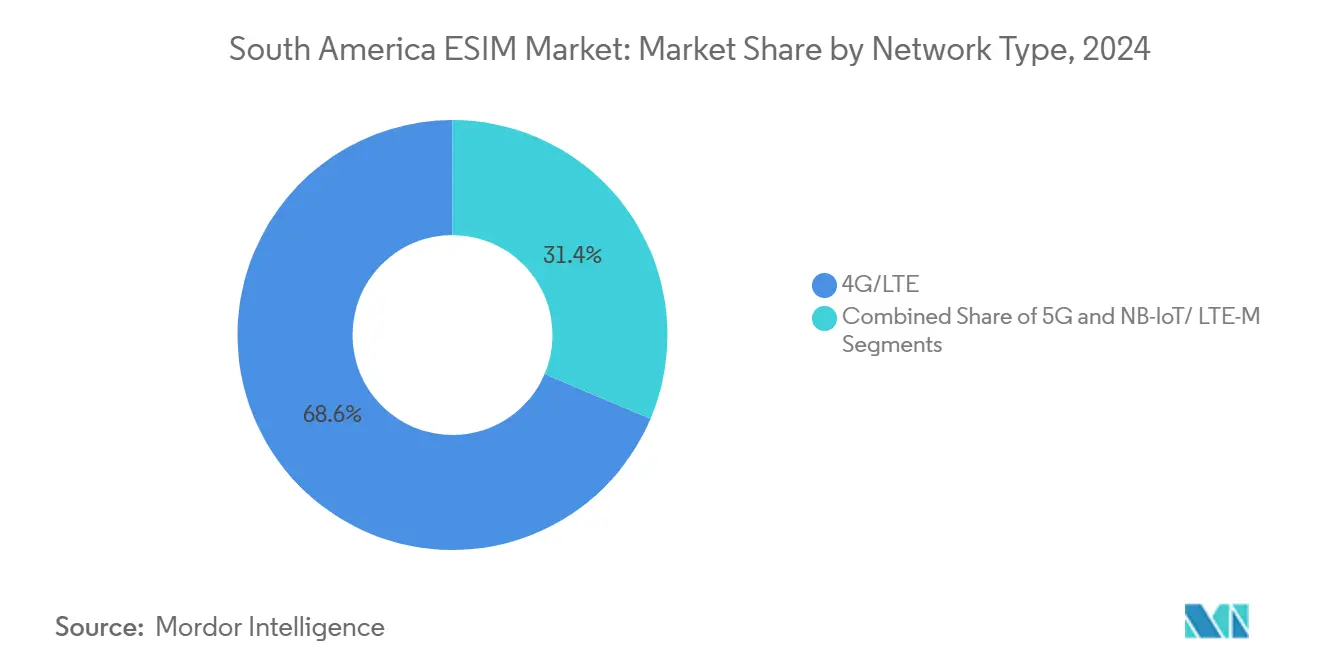

- By network type, 4G/LTE held 68.63% of South America eSIM market share in 2024; 5G exhibits the fastest 16.55% CAGR for the forecast window.

- By end-user industry, consumer electronics accounted for 67.75% of the South America eSIM market size in 2024 and logistics and asset tracking advances at a 17.21% CAGR through 2030.

- By geography, Brazil led with 53.86% revenue share in 2024, whereas the Rest of South America segment is projected to grow at a 10.32% CAGR between 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America ESIM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM shift to eSIM-only smartphones | 1.8% | Global, with early gains in Brazil, Chile, Argentina | Medium term (2-4 years) |

| 5G roll-out and data-heavy use-cases | 1.5% | Brazil, Chile, Colombia, Peru, Argentina core markets | Medium term (2-4 years) |

| Digital-first MNO/MVNO onboarding | 1.2% | Brazil leadership, spillover to regional markets | Short term (≤ 2 years) |

| Post-pandemic travel eSIM demand | 0.9% | Regional tourism hubs, cross-border corridors | Short term (≤ 2 years) |

| PIX-enabled instant eSIM payments | 0.7% | Brazil national, with expansion to Argentina merchants | Medium term (2-4 years) |

| Smart-meter mandates (utilities IoT) | 0.6% | Brazil ANEEL mandates, Chile and Colombia following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Shift to eSIM-Only Smartphones Accelerates Regional Adoption

Apple’s eSIM-only iPhone precedent in 2022 spurred Android peer moves that now ripple through South America. With smartphone penetration already above 80% in Brazil, every upgrade cycle converts physical SIM users into the eSIM mainstream.[1]GSMA Intelligence, “eSIM Consumer Research 2024,” gsma.com TIM Brasil’s September 2024 migration portal, built with IDEMIA, cuts activation steps from five to two and slices call-center traffic by 27%.[2]Nokia, “TIM Brasil Selects Nokia for 5G Expansion,” nokia.comANATEL’s device certification keeps rogue profiles off networks, ensuring secure scaling. As more OEMs seal the SIM tray, even reluctant subscribers adopt the technology, turning a hardware tweak into a structural demand driver.

5G Infrastructure Expansion Drives Data-Heavy eSIM Applications

Thirty-two operators across 13 South American countries switched on 5G by December 2024, opening low-latency lanes for AR, smart-factory, and connected-vehicle workloads that depend on programmable eSIM connectivity. Nokia’s 2025 contract with TIM Brasil spans 15 states and bundles AI-assisted MantaRay network management for near-zero downtime rollouts. In Argentina, a Sencinet-Alvis tie-up melds private LTE with Starlink backhaul, letting agriculture clients roam between terrestrial and satellite bands via a single eSIM profile.[3]BNamericas, “Sencinet and Alvis Forge LTE–Satellite Pact,” bnamericas.comSuch hybrid models amplify the value of remote provisioning, justifying higher-margin enterprise plans.

Digital-First Operator Strategies Transform Customer Acquisition

Latin operators once relied on corner-store SIM swaps; now they push app-based activation that cuts plastic waste and courier logistics. América Móvil, Telefónica, and TIM joined GSMA’s Open Gateway, exposing APIs for SIM swap and number verification that shrink onboarding to minutes. Nubank’s May 2024 travel eSIM for Ultravioleta clients showcases how fintechs bundle connectivity with loyalty perks, bypassing legacy retail stores while expanding cross-sell revenue. Operators counter with zero-touch eSIM top-ups linked to PIX, locking in customers through friction-free digital experiences.

Post-Pandemic Travel Recovery Fuels Cross-Border eSIM Demand

International traffic rebounded 34% year-over-year in 2024, and 51% of global eSIM users activated profiles abroad, often choosing Airalo or Holafly over local operator roaming packs. BTS Group’s April 2025 investment in ZIM Connections unlocks white-label apps supporting 200+ destinations, letting South American carriers launch branded travel eSIMs without deep tech builds. For consumers, tapping an app on arrival replaces swapping a kiosk-sold SIM, making eSIM the de-facto cross-border standard.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low consumer awareness and education gaps | -1.3% | Regional, particularly in mid-tier markets | Short term (≤ 2 years) |

| Mid-tier handset compatibility lag | -0.8% | Price-sensitive segments across all countries | Medium term (2-4 years) |

| Import-tariff inflation on IoT eSIM modules | -0.6% | Brazil, Argentina trade policy impacts | Short term (≤ 2 years) |

| Data-sovereignty delays in RSP certification | -0.4% | Cross-border operations, regulatory harmonization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Awareness Deficits Limit Mainstream Adoption

GSMA found global eSIM awareness at only 36% in late 2022; South American mid-tier markets sit lower, dampening uptake despite operator readiness. Brick-and-mortar dependence slows exposure, and some carriers fear easier churn once switching requires no physical SIM. The gap narrows through targeted campaigns at device-upgrade moments, yet weak awareness still trims 1.3 percentage points from potential CAGR.

Mid-Tier Device Compatibility Creates Market Segmentation

Budget smartphones dominate Latin shipments, and many omit eSIM to save BOM costs, restricting adoption to premium bands. Brazil’s ex-tarifário ends December 2025, dropping duties on 36 ICT items to nudge OEMs toward mid-tier eSIM variants. Until compatibility broadens, the addressable base remains skewed toward high-income users and enterprise IoT endpoints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance Amid Service Innovation

Hardware captured 62.33% of the South America eSIM market share in 2024, owing to robust demand for MFF2 and wafer-level packages across smartphones, wearables, and industrial sensors. The South America eSIM market size for hardware reached USD 353 million, expanding steadily as OEMs integrate secure elements at the factory. Intensive certification, cryptographic IP, and high entry costs anchor incumbent dominance. Remote SIM provisioning, though only 15% of revenue today, clocks a 13.01% CAGR to 2030 as operators license cloud orchestration suites to digitize onboarding. Growth hinges on multi-tenant platforms that slice lead times for adding new MVNOs or enterprise fleets.

Service innovation reshapes margins. TIM Brasil’s eSIM portal condensed SIM migration costs by an estimated USD 1.7 million within six months, according to internal disclosures. eSIM management middleware layers, situated between hardware and user apps, orchestrate profile downloads, revoke stolen credentials, and auto-select the cheapest roaming networks. While hardware remains the revenue bedrock, services convert one-time component sales into annuity streams.

By Device Type: Smartphone Leadership with IoT Acceleration

Smartphones and feature phones owned 73.05% of the South America eSIM market size in 2024, equal to roughly USD 414 million, reflecting high handset replacement cycles in urban centers. Apple, Samsung, and Motorola drive premium volume, but flagship pricing caps penetration in lower-income segments. IoT modules, although only 6% revenue, outpace all categories at a 17.48% CAGR, spurred by ANEEL’s electricity smart-meter decree demanding 99.98% availability for substations.

emnify’s September 2024 roaming-enabled connectivity leverages a single IMSI that hops between Claro, TIM, and Vivo, easing nationwide truck tracking. Wearables and tablets post mid-single-digit growth as health-monitoring and hybrid work persist, but value remains marginal relative to smartphones. Over 2025-2030, IoT’s runway lengthens once chipset prices fall below USD 3, unlocking use cases in cold-chain logistics and smart agriculture.

By Network Type: 4G Maturity Enables 5G Transition

4G/LTE commanded 68.63% of South America eSIM market share in 2024, supporting the bulk of consumer smartphone traffic. As 5G cells proliferate, the South America eSIM market size for 5G profiles climbs at 16.55% CAGR, fueled by enterprise SLA commitments in mining, ports, and manufacturing. NB-IoT and LTE-M satisfy low-power needs in smart-metering and environmental monitoring, while spectrum-auction timelines dictate rollout velocity per country. Regulators that bundle mid-band and millimeter-wave allocations, like Brazil’s 3.5 GHz auction, shorten payback for operators, accelerating eSIM-enabled device shipments.

For consumers, eSIM eases SIM swaps between LTE and 5G plans without store visits, raising ARPU as users trial higher-speed tiers. Enterprise clients exploit profile cycling to shift backup links from LTE-M to 5G when throughput spikes, demonstrating the programmable versatility at the heart of the South America eSIM industry.

By End-User Industry: Consumer Electronics Leadership with Logistics Momentum

Consumer electronics commanded 67.75% of the South America eSIM market size in 2024, driven by smartphone upgrades, tablet sales for education, and rising smartwatch penetration. Operators bundle devices with installment financing and PIX-based instant activation, tying service revenue to hardware refreshes.

Logistics and asset tracking emerge as the speedster with 17.21% CAGR. Cross-border trucking, maritime shipping, and air-cargo boxes traverse customs zones, so eSIM’s ability to preload multiple carrier profiles slashes downtime. emnify notes a 28% reduction in cold-chain spoilage incidents after deploying multi-network IoT tags on Brazil-Argentina routes. Automotive, energy, and industrial verticals also climb as connected-vehicle mandates and predictive-maintenance programs gain policy momentum, reinforcing the South America eSIM market’s diversification beyond phones.

Geography Analysis

Brazil’s 53.86% hold on the South America eSIM market reflects its large economy, mature 4G base, and wide PIX adoption that speeds digital onboarding. ANATEL fast-tracks eSIM certifications, while the 3.5 GHz auction already financed dozens of 5G clusters across São Paulo, Rio de Janeiro, and Brasília. Operators push bundled handset-plus-plan deals that ship with pre-provisioned eSIM profiles, and utilities follow suit as they comply with smart-meter mandates that require 99.98% network uptime. Robust fintech participation also drives add-on travel eSIM purchases inside banking super-apps, widening consumer exposure to the South America eSIM market.

Chile and Colombia form the second tier of adoption with rising 5G footprints and pro-competition spectrum rules that keep tariffs low. Chile’s Subtel opened the 3.5 GHz band in 2024 and tied license renewals to rural-coverage targets, so Claro, WOM, and Entel added eSIM-centric prepaid plans that let users switch networks remotely. Colombia’s MinTIC promotes neutral-host infrastructure, cutting small-cell capex by as much as 30%, which helps MVNOs offer feature-rich plans without storefronts. Together, these countries contribute a growing slice to the South America eSIM market as competitive tension rewards digital-only distribution.

Argentina and Peru advance at a steadier pace because of macro headwinds and difficult terrain, yet both nations leverage sector-specific demand. In Argentina, currency controls hamper handset imports, so operators lean on cloud-managed IoT modules for agritech and logistics corridors linked to Brazil. Peru’s mining clusters in the Andes favor eSIM because trucks cross coverage holes that require seamless network handover. The Rest of South America group—Bolivia, Ecuador, Paraguay, Uruguay, and Venezuela—posts the fastest 10.32% CAGR thanks to regulatory harmonization that cuts roaming surcharges and lets travel eSIM players preload multi-country profiles. These developments collectively ensure the South America eSIM market keeps broadening beyond Brazil’s core.

Competitive Landscape

The South America eSIM market features moderate concentration with global secure-element leaders retaining bargaining power, yet service layers now command investor attention. Thales deploys turnkey eSIM Enablement Centers in São Paulo and Santiago that handle encryption, key injection, and profile hosting for dozens of regional carriers. IDEMIA supports TIM Brasil’s consumer portal and Claro’s enterprise dashboard, showing how hardware expertise must pair with front-end software to defend share. Giesecke + Devrient integrates its AirOn360 platform directly with América Móvil’s billing stack, allowing near-real-time profile swaps in under three seconds.

Fintechs inject fresh rivalry. Nubank’s 2024 travel eSIM added 10 GB roaming data inside its premium card plan and netted 200 000 activations within eight months. Mercado Pago trails with a pilot that bundles cross-border data in its wallet, while traditional MNOs test loyalty points that convert into eSIM packs. White-label aggregators such as ZIM Connections and Telna strike wholesale deals so second-tier MVNOs can launch offerings without deep network ties. This reseller wave nudges incumbents to harden customer experience through AI chatbots, instant refunds, and PIX-based micro-top-ups, ensuring the South America eSIM market remains dynamic.

IoT specialists sharpen vertical playbooks. emnify links a single IMSI to tri-network roaming in Brazil, lifting logistics uptime by double digits and winning contracts with three fleet operators. Sencinet bundles private LTE with Starlink to serve mining and energy majors that need remote redundancy, positioning eSIM as the “always on” credential rather than a simple ID token. Such alliances illustrate how the South America eSIM industry reshapes traditional value chains, rewarding niche expertise over sheer subscriber volume.

South America ESIM Industry Leaders

Thales Group

IDEMIA Group

Samsung Electronics Co., Ltd.

Entel S.A.

América Móvil S.A.B. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nokia and TIM Brasil began 5G expansion across 15 states using AirScale radios powered by ReefShark SoCs, enabling wider eSIM device adoption.

- September 2024: emnify launched roaming-enabled IoT connectivity with Claro, covering 2G, 3G, and 4G footprints nationwide.

- September 2024: TIM Brasil opened an IDEMIA-built migration portal that lets users convert plastic SIMs to eSIM in two steps.

- May 2024: Nubank introduced a travel eSIM for Ultravioleta customers, offering 10 GB data across 40 countries inside its mobile app.

South America ESIM Market Report Scope

| Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software |

| Remote SIM Provisioning Services |

| Smartphones and Feature Phones |

| Tablets and Laptops |

| Wearables |

| M2M/IoT Modules |

| 5G |

| 4G/LTE |

| NB-IoT/LTE-M |

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Logistics and Asset Tracking |

| Energy and Utilities |

| Healthcare and Wearables |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Argentina |

| Rest of South America (Panama, Costa Rica, Uruguay, Guatemala, Others) |

| By Offering | Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software | |

| Remote SIM Provisioning Services | |

| By Device Type | Smartphones and Feature Phones |

| Tablets and Laptops | |

| Wearables | |

| M2M/IoT Modules | |

| By Network Type | 5G |

| 4G/LTE | |

| NB-IoT/LTE-M | |

| By End-user Industry | Consumer Electronics |

| Automotive and Transportation | |

| Industrial and Manufacturing | |

| Logistics and Asset Tracking | |

| Energy and Utilities | |

| Healthcare and Wearables | |

| By Country | Brazil |

| Chile | |

| Colombia | |

| Peru | |

| Argentina | |

| Rest of South America (Panama, Costa Rica, Uruguay, Guatemala, Others) |

Key Questions Answered in the Report

Which nation drives the largest share of South American eSIM revenue?

Brazil accounts for 53.86% of regional sales due to supportive policy, 5G investment, and PIX-enabled digital onboarding.

How fast is the logistics sector adopting eSIM?

Logistics and asset tracking posts a 17.21% CAGR from 2025-2030 as cross-border fleets rely on multi-network profiles for uninterrupted coverage.

What role do fintech companies play in eSIM adoption?

Firms like Nubank embed travel eSIM packs inside banking apps, broadening exposure and spurring competitive innovation.

Why is consumer awareness still a restraint?

GSMA surveys show awareness below 40%, so many mid-tier buyers remain unfamiliar with eSIM benefits, slowing mass migration.

How are IoT players boosting network reliability?

Providers such as emnify and Sencinet pair eSIM with roaming or satellite links, raising uptime for utilities, mining, and logistics clients.

What makes 5G critical to future eSIM growth?

5G’s low-latency architecture unlocks AR, autonomous vehicle, and smart-factory use cases that need remote provisioning and rapid profile swaps.

Page last updated on: