South America Enterprise Content Management (ECM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

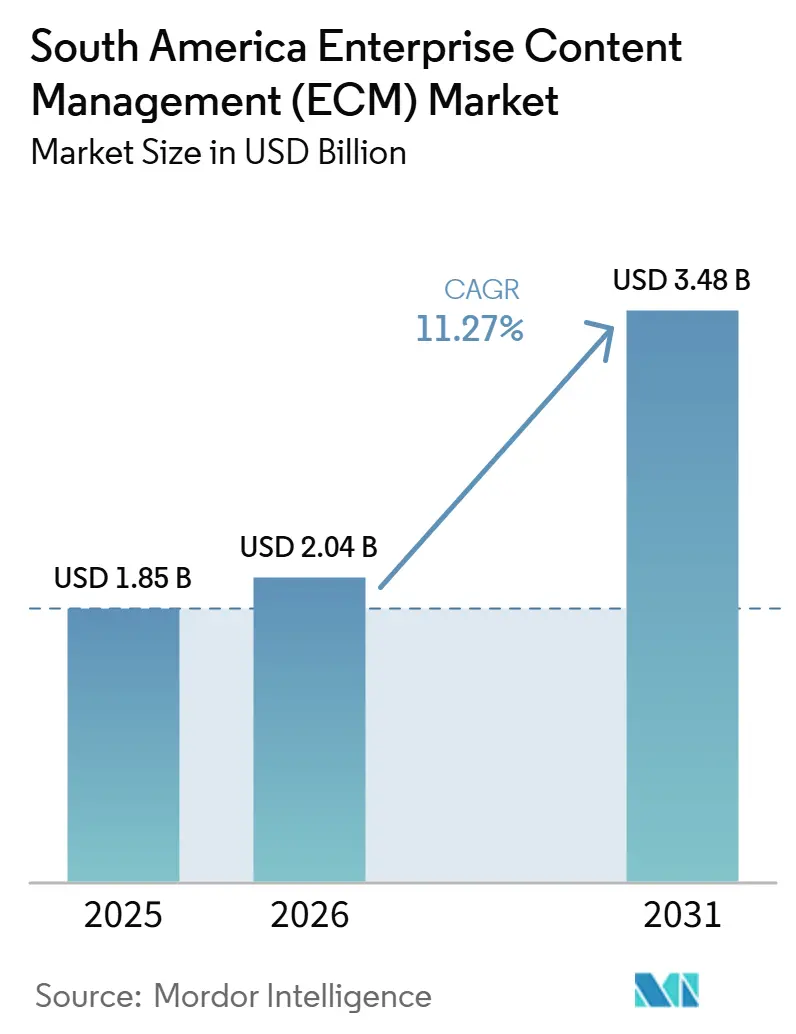

| Base Year Market Size (2025) | USD 1.85 Billion |

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 3.48 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Enterprise Content Management (ECM) Market Analysis by Mordor Intelligence

The South America Enterprise Content Management (ECM) market size was valued at USD 1.9 billion in 2025 and estimated to grow from USD 2 billion in 2026 to reach USD 3.5 billion by 2031, at a CAGR of 11.27% during the forecast period (2026-2031). The South America Enterprise Content Management (ECM) Market is expanding as enterprises treat content systems as part of broader digital operating models rather than stand-alone archives, a shift that sits alongside the region’s USD 126.2 billion digital transformation base in 2026. Demand is rising as financial institutions, public agencies, healthcare providers, and large corporates move paper-heavy processes into digital workflows and need stronger control over records, access, search, and retention. Cloud deployment, workflow orchestration, and AI-based document handling are moving from optional upgrades to core buying criteria, changing how vendors package platforms and services. Competition remains active between global software vendors and regional implementation partners, especially where local compliance settings, language support, and integration depth affect project success. Growth is still constrained by data residency rules, the complexity of migrating legacy repositories, and the cost of connecting content platforms across fragmented application environments.

Key Report Takeaways

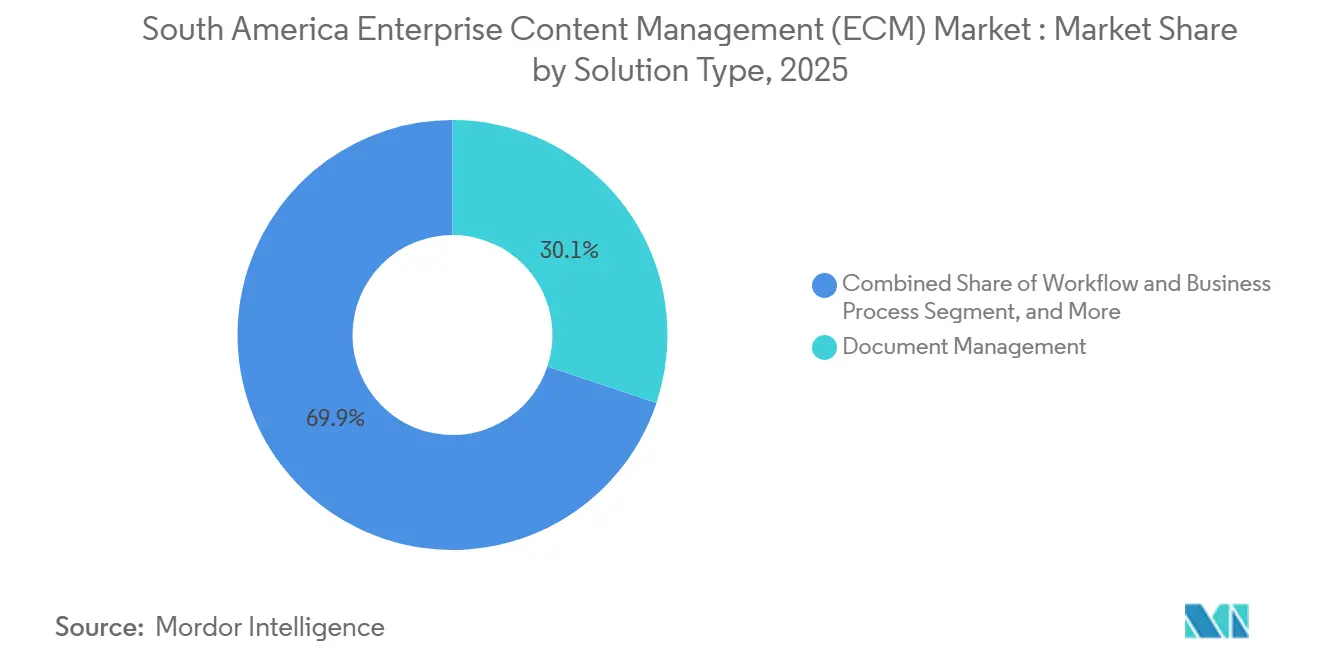

- By solution type, Document Management led with 30.12% revenue share in 2025 in the South America Enterprise Content Management (ECM) Market, while Workflow and Business Process Management is forecast to expand at a 13.48% CAGR through 2031.

- By deployment mode, cloud accounted for 48.53% of revenue in 2025 and recorded the highest projected CAGR of 14.21% through 2031 in the South America Enterprise Content Management (ECM) Market.

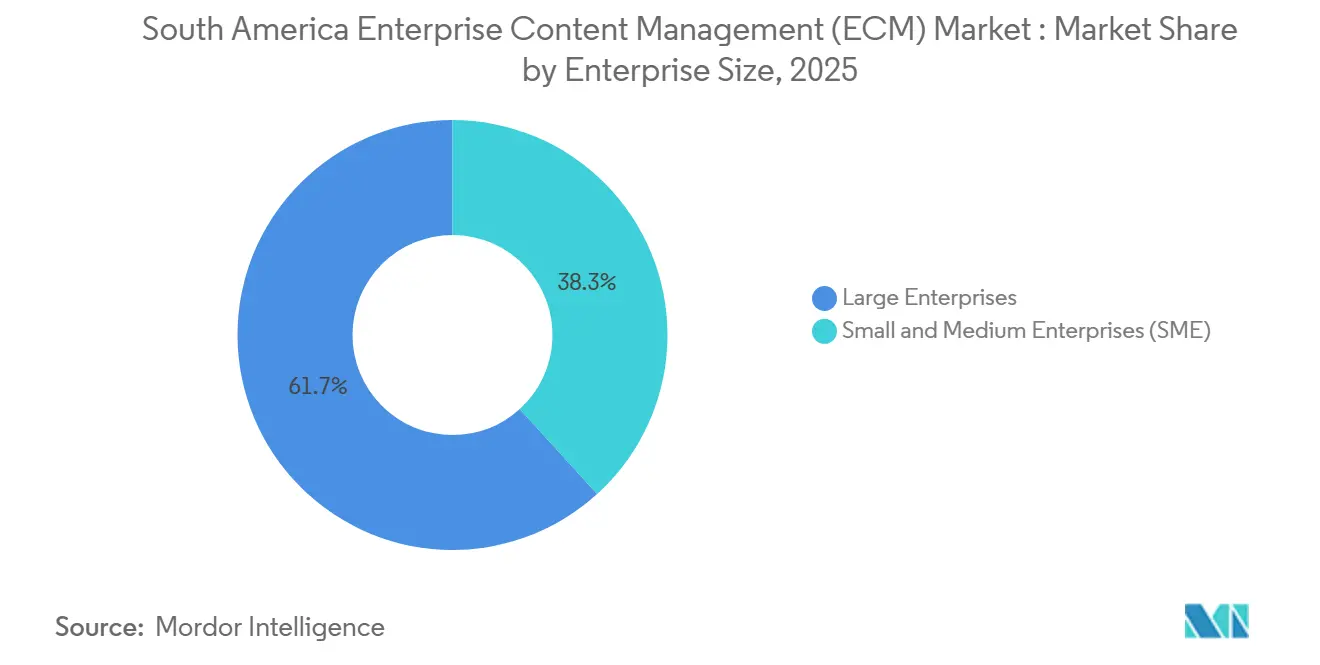

- By enterprise size, large enterprises accounted for 61.74% of revenue in 2025 in the South America Enterprise Content Management (ECM) Market, while SMEs are projected to grow at the fastest rate of 13.69% through 2031.

- By end-user industry, BFSI captured 24.18% of revenue in 2025 in the South America Enterprise Content Management (ECM) Market, while healthcare is advancing at the highest CAGR of 13.82% through 2031.

- By geography, Brazil held 60.24% of regional revenue in 2025 in the South America Enterprise Content Management (ECM) Market, while Argentina is forecast to expand at the fastest CAGR of 14.43% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Enterprise Content Management (ECM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Digitization of Content-Heavy Workflows in Banking and Public Services | +2.8% | Brazil, Argentina, Colombia, Peru | Short term (≤ 2 years) |

| Cloud Migration of Content Repositories and Workflow Engines | +2.5% | Brazil, Argentina, Chile, Colombia | Medium term (2-4 years) |

| AI-Enabled Document Classification, Extraction, and Search | +2.2% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Open Banking and Digital Compliance Requirements in Brazil | +1.8% | Brazil, with spillover to Argentina and Colombia | Short term (≤ 2 years) |

| Rise of Sector-Specific Automation for Insurance, Healthcare, and Legal Workflows | +1.5% | Brazil, Colombia, Peru, Chile | Medium term (2-4 years) |

| Subscription-Based ECM Pricing Lowering Mid-Market Adoption Barriers | +1.2% | Region-wide, concentrated in Brazil and Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitization of Content-Heavy Workflows in Banking and Public Services

Governments across South America are consolidating paper-based administration into digital workflows, which is increasing demand in the South America Enterprise Content Management (ECM) Market. Peru reported more than 6,000 public services digitalized and available online by June 2026, which lifted the volume of records that agencies must capture, store, search, and retain.[1]Presidency of the Council of Ministers of Peru, “Premier Arroyo: Perú Cuenta con Más de 6000 Servicios Públicos Digitalizados y Disponibles en Línea,” TV Perú, tvperu.gob.pe Argentina’s General Inspection of Justice published General Resolution 7/2026 on July 1, 2026, and established the SODA digital documentation system for corporate filings. These mandates increase the amount of governed content that must move through intake, review, approval, and archive steps without manual bottlenecks. Private firms that submit records to public agencies are also being pushed into digital exchange models, even when they did not initiate their own internal transformation programs. That spillover is shortening buying cycles for document management and workflow tools across banking, legal, outsourcing, and public service contractor environments.

Cloud Migration of Content Repositories and Workflow Engines

Cloud deployment already accounted for 48.5% of revenue in 2025 in the South America Enterprise Content Management (ECM) Market, indicating that hosted delivery is the default path for many new projects. The appeal is practical because buyers can scale storage and workflow capacity faster and avoid the infrastructure burden of a full on-premises rollout. Hybrid setups are also gaining relevance as enterprises try to lower operating costs for active content while keeping stricter control over highly sensitive archives. Hyland announced in June 2026 that its Content Innovation Cloud would run on Microsoft Azure, giving customers broader data residency options and regional reach. That kind of hyperscaler alignment matters in Brazil and Argentina, where vendor flexibility now carries more weight in procurement decisions. It also creates steady demand for regional partners that can manage migration, metadata cleanup, permissions design, and post-deployment governance.

AI-Enabled Document Classification, Extraction, and Search

Artificial intelligence is shifting the South America Enterprise Content Management (ECM) Market from passive file storage toward active content intelligence. IBM and CXP Brasil implemented an intelligent automation solution for MDS Brasil in February 2026, multiplying financial statement reconciliation throughput by 7.5x using IBM Robotic Process Automation and the IBM Document Processing Engine on IBM Cloud.[2]ABES, “IBM e CXP Implementam Soluções de IA na MDS Brasil, Melhorando Eficiência da Seguradora,” ABES, abes.org.br Orizon Brasil, which processes more than 500,000 medical events per day, achieved 70% automation in medical guide intake workflows after deploying AI-powered document classification. These examples show that AI is being used in live operational settings rather than in isolated pilot programs. Buyers are placing more value on extraction accuracy, search quality, and workflow routing because those features directly affect cycle time and compliance readiness. Vendors that can train models around Portuguese documents, Brazilian fiscal records, and regional regulatory formats are in a stronger position than platforms that rely only on generic global templates.[3]Santo Digital, “Orizon Brasil,” Santo Digital, sd.insany.co

Open Banking and Digital Compliance Requirements in Brazil

Brazil’s Open Finance framework is pushing institutions to keep cleaner records, stronger consent histories, and more reliable version control in the South America Enterprise Content Management (ECM) Market. Banco Central do Brasil published Instrução Normativa BCB Nº 724 in April 2026 and released version 7.0 of the Open Finance Data and Services Scope Manual for participating institutions. Successive API updates require auditable content trails, policy-based retention, and tighter governance over documents tied to financial customer activity. Argentina’s tax authority also issued General Resolution RG 5824/2026 in July 2026, ending the remaining exceptions to mandatory electronic invoicing. Brazil and the European Union also announced mutual data adequacy decisions in January 2026, reducing friction for cross-border data flows between the two jurisdictions. Together, these rules are making compliance a direct trigger for ECM spending rather than a secondary feature request.[4]LLB Solutions, “Argentina 2026: End of E-Invoicing Exceptions Under RG 5824/2026,” LLB Solutions, llbsolutions.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency and Cross-Border Transfer Constraints | -1.5% | Brazil, Argentina, Chile (national regulatory scope) | Short term (≤ 2 years) |

| Legacy Repository Migration Complexity After Mergers and System Consolidation | -1.2% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Security and Privacy Concerns in Cloud-Hosted Content Stores | -0.8% | Region-wide | Medium term (2-4 years) |

| API Integration Costs and Vendor Lock-In in Multi-App Content Ecosystems | -0.5% | Brazil, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Residency and Cross-Border Transfer Constraints

Data location rules continue to slow multi-country rollouts in the South America Enterprise Content Management (ECM) Market. Brazil’s ANPD issued the International Data Transfer Regulation in August 2024 and required Standard Contractual Clauses for transfers to jurisdictions without adequacy recognition. This means content architectures must account for where personal data is stored, processed, backed up, and shared. The January 2026 EU-Brazil adequacy decision eased one important corridor, but it did not remove the need for careful design across the rest of the region. For multinational buyers, that extends legal review, complicates hosting choices, and slows wider rollout schedules. Vendors with clearer localization controls and stronger policy templates are better placed to reduce this friction.

Legacy Repository Migration Complexity After Mergers and System Consolidation

Legacy repository migration remains a practical brake on new spending in the South America Enterprise Content Management (ECM) Market. Many large institutions still operate parallel content environments built over different periods, under different metadata rules, and on incompatible platforms. When those repositories are consolidated after mergers or infrastructure reviews, teams often find incomplete indexes, inconsistent file structures, and obsolete formats that require manual work before migration can proceed. That extra effort stretches budgets and delays broader modernization plans that would otherwise expand into workflow and AI-led use cases. Smaller banks, cooperatives, and regional organizations are particularly exposed because they often lack the staff and funding needed to maintain live operations while running complex migration programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Document Management Anchors a Shifting Solution Mix

Document Management accounted for 30.12% of the South America Enterprise Content Management (ECM) market in 2025, making it the largest solution block, as capture, indexing, access control, and retention remain the core requirements for most first-time projects. This position reflects the fact that many enterprises still begin by centralizing files before attempting broader process redesign. Records Management continues to attract steady demand in regulated settings where retention periods, legal holds, and audit retrieval are mandatory. Case Management and Web Content Management also remain relevant when customer interaction records and digital publishing must be controlled within formal governance rules.

Workflow and Business Process Management is the fastest-growing solution type, with a 13.48% CAGR through 2031, indicating that buyers increasingly want content systems to move work rather than simply store documents. Invoice routing, claims handling, contract approval, and service request handling are becoming more important buying triggers because they produce visible efficiency gains without requiring a full core system replacement. Digital Asset Management is gaining more room in customer-facing sectors where brand consistency and media control matter, even though it remains smaller than core document-centered functions. The Other Solutions category, which includes email archiving, e-signature management, and compliance vaulting, is also broadening as the definition of digital records expands across South American compliance frameworks.

By Deployment Mode: Cloud Momentum Sustained Across Deployment Tiers

Cloud held 48.53% of the South America Enterprise Content Management (ECM) market share in 2025 and is projected to advance at 14.21% CAGR through 2031, making it both the leading and fastest-growing deployment model. That combination signals structural demand rather than a short-term spike. Buyers are using cloud systems to speed implementation, reduce infrastructure costs, and enable remote access across distributed workforces. The pattern is especially strong where organizations prefer incremental deployment over large upfront software and hardware commitments.

On-premises deployments still retain an important base in government and BFSI environments where data control, existing contracts, and legacy system dependencies remain strong. Hybrid models are expanding because they allow organizations to run active workloads in the cloud while retaining selected archives or sensitive records on internal systems. This model aligns well with the region’s data residency concerns and with the uneven pace of digital modernization across different business units. Hyland’s June 2026 Microsoft Azure partnership reflects this direction because vendors are now packaging ECM around infrastructure flexibility and location control as much as around user features.

By Enterprise Size: Large Enterprises Anchor Spend While SMEs Accelerate Adoption

Large enterprises accounted for 61.74% of revenue in 2025 in the South America Enterprise Content Management (ECM) Market, reflecting the long-standing concentration of ECM budgets among institutions with large compliance obligations, complex process estates, and larger IT teams. These organizations typically manage multiple repositories across multiple departments and need common governance, unified search, and enterprise-wide record control. Their spending also includes the integration and change management work that smaller firms often delay. As a result, large accounts still anchor total revenue even as adoption broadens.

SMEs are the fastest-growing segment, with a 13.69% CAGR through 2031, and that growth is linked to subscription pricing, phased rollouts, and lower barriers to entry for cloud delivery. Smaller buyers can now begin with a narrow document management use case and add workflow or AI tools later as usage expands. This staged approach fits firms that need operational improvement but cannot support a large one-time implementation project. It also widens the addressable market for vendors that can offer simple deployment, local-language interfaces, and partner-led onboarding support.

By End-User Industry: BFSI Leads Share as Healthcare Registers the Highest Growth Rate

BFSI held 24.18% of the South America Enterprise Content Management (ECM) market share in 2025, making it the largest end-user group because financial firms manage large volumes of auditable customer, lending, transaction, and compliance records. The sector’s content burden is continuous and highly regulated, which makes ECM spending less discretionary than in many other industries. Brazil’s Open Finance framework adds another layer of governance need because institutions must preserve consent records, version histories, and traceable digital interactions. Insurance remains an important pocket within BFSI because document throughput, claims handling, and policy administration create clear use cases for workflow and intelligent document processing.

Healthcare is the fastest-growing vertical at a 13.82% CAGR through 2031, supported by national moves toward digital records and interoperable exchange. Colombia made HL7 FHIR R4-based digital health record exchange mandatory nationwide for registered providers from April 15, 2026, which expanded compliance-driven demand for content platforms. Brazil’s ICT in Health Survey 2025 found that 44% of healthcare facilities were integrated into the National Health Data Network, which means a large part of the healthcare base still has room to digitize and formalize content governance. Manufacturing, government, retail, IT and telecom, education, media, and utilities remain active adoption areas, but they are progressing at different speeds depending on the urgency of their document control and regulatory needs.

Geography Analysis

Brazil accounted for 60.24% of the South America Enterprise Content Management (ECM) market in 2025, making it the largest national contributor by a wide margin. The country benefits from the region’s deepest enterprise software base, a large financial services sector, and more advanced regulatory digitization than most neighboring markets. Banco Central do Brasil continues to shape this environment through Open Finance requirements that depend on well-governed digital records and auditable content trails. The January 2026 mutual data adequacy decision between Brazil and the European Union also reduced complexity for cross-border content operations involving those two jurisdictions. Brazil also has a second growth channel in healthcare, where only 44% of facilities were connected to the RNDS national health data network in the 2025 survey, leaving a large base still moving toward more formal digital record management.

Argentina is the fastest-growing country in the South America Enterprise Content Management (ECM) Market, with a 14.43% CAGR through 2031. The country is moving faster because public digital filing rules and tax digitization measures are pulling more organizations into structured document workflows. General Resolution 7/2026 required corporate filings under IGJ jurisdiction to be submitted via the SODA digital platform from July 1, 2026. Argentina’s Digital Government Index score stood at 0.5 against an OECD average of 0.7 in the 2025 benchmark, which suggests there is still meaningful room for digital process expansion across the public sector.

Colombia, Peru, and the rest of South America represent smaller revenue pools, but they are adding new compliance triggers that support steady expansion. Colombia made nationwide HL7 FHIR R4-based health record interoperability mandatory in April 2026, which created a direct requirement for systems that can store, route, and govern clinical content. Peru approved the National Data Governance Strategy 2026-2030 in February 2026 and formalized data interoperability as a policy priority for government systems. Peru also reported more than 6,000 digitalized public services by June 2026, which shows that the regional pipeline is widening beyond the two largest markets.

Competitive Landscape

The South America Enterprise Content Management (ECM) Market remains moderately consolidated at the top, but it is not locked into a single-vendor structure. Global incumbents such as OpenText, IBM, Microsoft, SAP, Oracle, and Hyland continue to hold an advantage in large accounts because they bring scale, partner networks, and better integration with broader enterprise software estates. Their position is strongest where buyers want long-term vendor stability, multilingual support, and established governance features. Even so, regional integrators and specialized providers still play an important role because implementation quality and local compliance adaptation often shape the final buying decision. This leaves the market competitive enough for new wins, especially in projects where industry templates and service depth matter more than brand size alone.

OpenText strengthened its position in November 2025 when its Core Content Management solutions for SAP received certification for SAP S/4HANA Cloud Public Edition, which supports accounts already standardizing around SAP environments. Hyland’s June 2026 Microsoft Azure partnership exemplifies a second strategic pattern: vendors are leveraging hyperscaler alignment to expand reach, enhance infrastructure flexibility, and expand data residency options. IBM’s February 2026 implementation for MDS Brasil also shows that vendors are competing through visible use cases in regulated sectors, not only through product messaging. Laserfiche and M-Files are also reinforcing their positioning through leadership messaging in document management and stronger AI and Microsoft integration capabilities.

A clear opening remains in sector-specific bundles that address regional compliance without heavy customization. Vendors that can package Open Finance workflows for Brazil, health record governance for Colombia, or digital filing controls for Argentina are likely to move faster in new accounts. Language-aware content taxonomies and strong local partner execution can matter as much as core platform breadth in this market. That is why the South America Enterprise Content Management (ECM) Market still allows room for challengers even though a handful of global brands dominate the large-enterprise conversation.

South America Enterprise Content Management (ECM) Industry Leaders

OpenText Corporation

Hyland Software, Inc.

Box, Inc.

Microsoft Corporation

Laserfiche, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Argentina's General Inspection of Justice published General Resolution 7/2026 on July 1, 2026, establishing the "SODA" online documentation system requiring all corporate entities under IGJ jurisdiction to file and manage documentation digitally. The mandate directly expands the compliance-driven ECM addressable market across Argentina's private sector, which must now align filing workflows with the new digital platform.

- July 2026: Argentina's tax authority (ARCA) implemented General Resolution RG 5824/2026, effective July 1, 2026, eliminating all remaining exceptions to mandatory electronic invoicing for previously exempted taxpayer categories. The measure closes the last gaps in Argentina's digital fiscal document ecosystem, driving procurement of integrated ECM and e-invoicing workflow solutions.

- June 2026: Hyland announced a strategic partnership with Microsoft to bring its Content Innovation Cloud to Microsoft Azure, offering enterprise customers data residency options and geographic reach across cloud regions, including South America. The partnership reinforces Hyland's position as a multi-cloud ECM provider expanding its footprint in emerging markets through hyperscaler infrastructure alliances.

- May 2026: Laserfiche was recognized as a Leader in the 2026 Gartner Magic Quadrant for Document Management, with its roadmap including expanded AI agent functionality, specifically agentic workflows and background monitoring agents, targeted at highly regulated industries. Laserfiche has active partner and reseller presence across South America through its Portuguese and Spanish-language platform offerings.

South America Enterprise Content Management (ECM) Market Report Scope

The South America enterprise content management (ECM) market refers to the ecosystem of software solutions and services designed to systematically capture, manage, store, preserve, and deliver an organization's unstructured and structured content and documents. This includes technologies such as document management, records management, workflow, business process management, case management, digital asset management, and web content management. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of all sizes across diverse industries in the region, including BFSI, government, healthcare, manufacturing, and retail. Driven by rapid digital transformation, increasing data volumes, and stringent regulatory compliance requirements across APAC, ECM solutions enable businesses to streamline operations, enhance collaboration, ensure data security, and reduce reliance on manual, paper-based processes, thereby improving overall productivity and decision-making.

The South America Enterprise Content Management (ECM) Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises (SME), and Large Enterprises), End-User Industry (BFSI, Government and Public Sector, Healthcare, IT and Telecommunications, Manufacturing, Retail, Media and Entertainment, Education, Energy and Utilities, and Other End-User Industries), and Geography (Brazil, Argentina, Peru, Chile, Colombia, Ecuador, Venezuela and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Retail |

| Media and Entertainment |

| Education |

| Energy and Utilities |

| Other End-User Industries |

| Brazil |

| Argentina |

| Peru |

| Chile |

| Colombia |

| Ecuador |

| Venezuela |

| Rest of South America |

| By Solution Type | Document Management |

| Records Management | |

| Workflow and Business Process Management | |

| Case Management | |

| Digital Asset Management | |

| Web Content Management | |

| Other Solutions | |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Small and Medium Enterprises (SME) |

| Large Enterprises | |

| By End-User Industry | BFSI |

| Government and Public Sector | |

| Healthcare | |

| IT and Telecommunications | |

| Manufacturing | |

| Retail | |

| Media and Entertainment | |

| Education | |

| Energy and Utilities | |

| Other End-User Industries | |

| By Geography | Brazil |

| Argentina | |

| Peru | |

| Chile | |

| Colombia | |

| Ecuador | |

| Venezuela | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America Enterprise Content Management (ECM) Market?

The South America Enterprise Content Management (ECM) Market is valued at USD 2 billion in 2026 and is projected to reach USD 3.5 billion by 2031 at an 11.27% CAGR.

Which country leads enterprise content management adoption in South America?

Brazil leads with 60.24% of regional revenue in 2025, supported by its large enterprise base, Open Finance framework, and broader healthcare digitization pipeline.

Which deployment model is growing fastest in the region?

Cloud is both the largest and fastest-growing deployment model, holding 48.53% share in 2025 and advancing at a 14.21% CAGR through 2031.

Why is BFSI the largest end-user group for ECM solutions?

BFSI led with 24.18% of revenue in 2025 because banks and insurers manage high volumes of auditable records, customer documents, and compliance files.

Which end-user vertical is expanding most quickly?

Healthcare is the fastest-growing vertical with a 13.82% CAGR through 2031, supported by digital health record mandates and wider interoperability requirements.

What is driving new buying interest among smaller businesses?

SMEs are growing at a 13.69% CAGR because subscription pricing, cloud delivery, and phased rollout models are lowering the entry barrier for ECM adoption.

Page last updated on: