Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

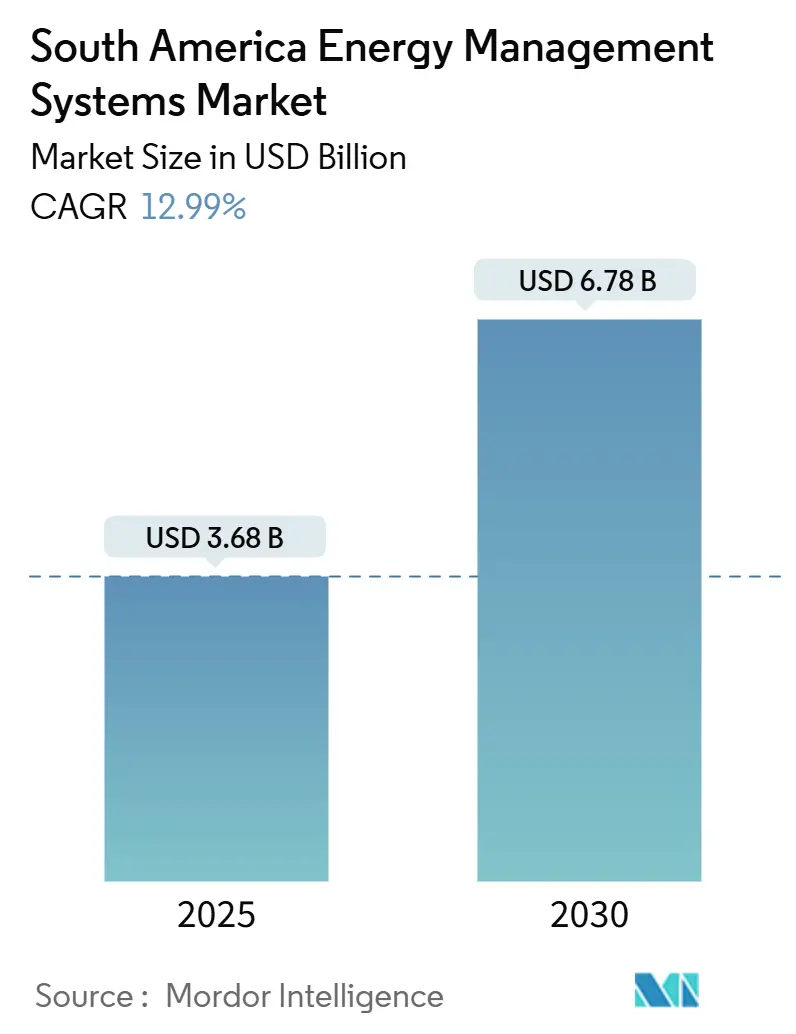

| Market Size (2025) | USD 3.68 Billion |

| Market Size (2030) | USD 6.78 Billion |

| Growth Rate (2025 - 2030) | 12.99% CAGR |

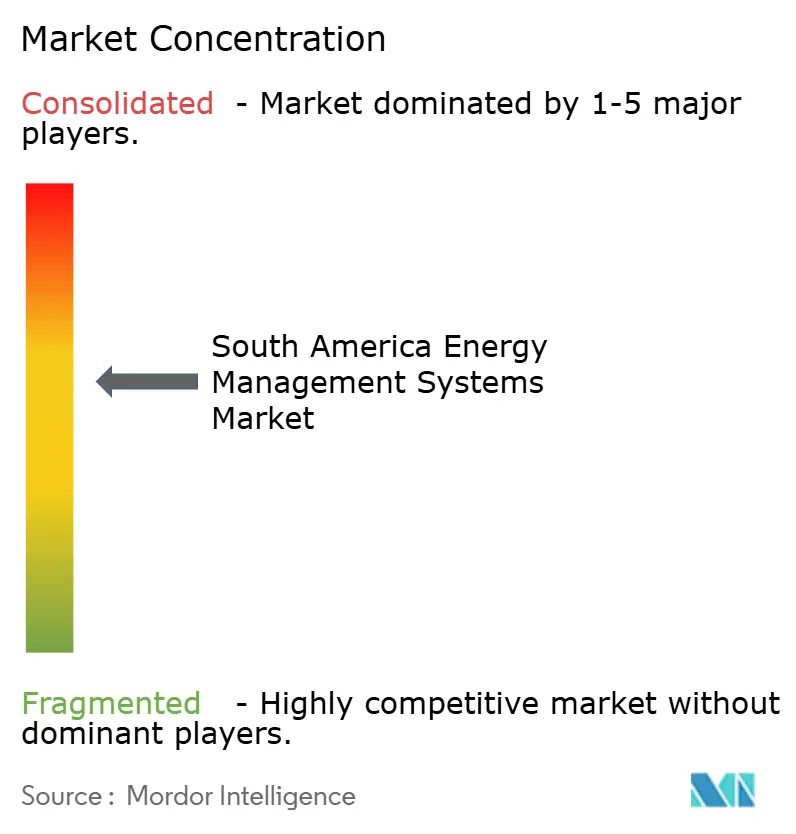

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Energy Management Systems Market Analysis by Mordor Intelligence

The South America energy management systems market size is valued at USD 3.68 billion in 2025 and is projected to climb to USD 6.78 billion by 2030, reflecting a robust 12.99% CAGR that mirrors the region’s push for grid modernization, renewable integration, and industrial decarbonization. Software-led architectures dominate today because analytics unlock real-time insights from the 200 TWh of renewable generation already flowing through Brazilian grids.[1]Brazilian National Electric Energy Agency, “Resolution 1000/2021,” GOV.BR, gov.br Complex ISO 50001 reporting requirements and rising corporate ESG audits are shifting spend toward managed services, while falling sensor prices widen access for small and midsize enterprises. Brazil’s smart-meter mandate, Chile’s 24-month compliance clock for large consumers, and Colombia’s consumption audits embed EMS in national policy fabrics. Concurrently, pilots in green hydrogen, lithium mining, and data-center cooling are stretching latency and cybersecurity requirements, catalyzing edge and hybrid deployment modes.

Key Report Takeaways

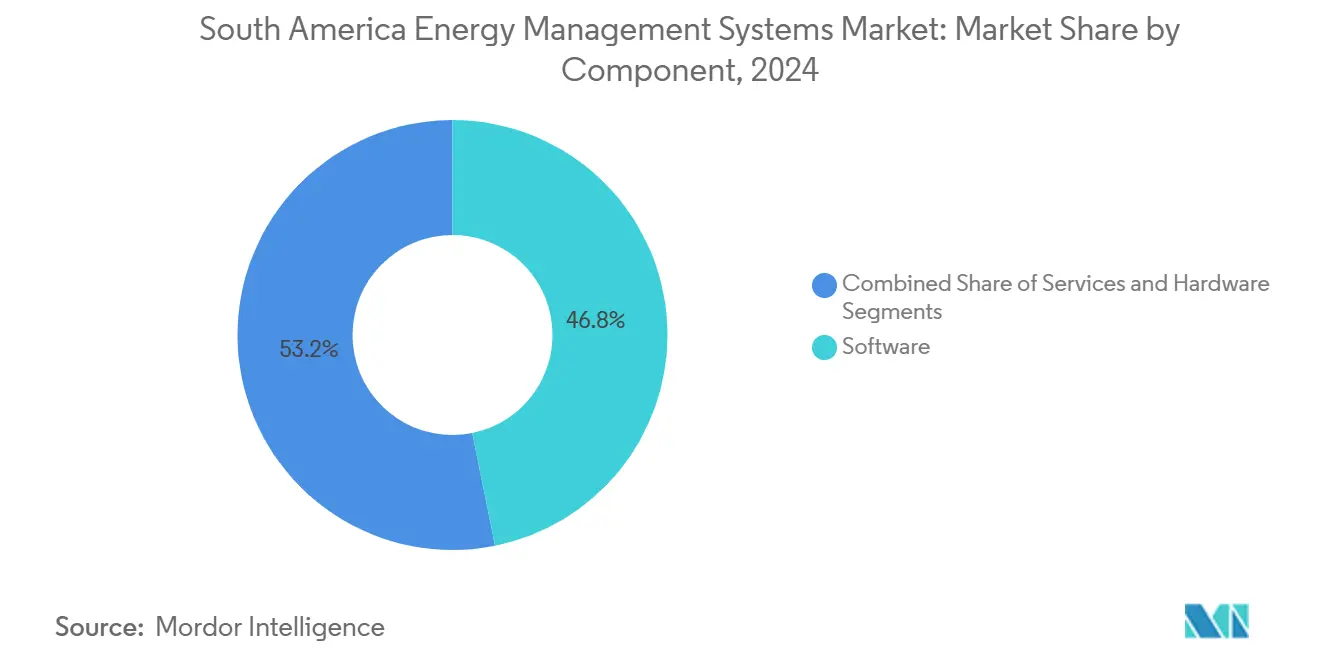

- By component, software led with 46.83% of South America energy management systems market share in 2024, whereas services are forecast to rise at a 13.66% CAGR through 2030.

- By system type, Building EMS captured 43.73% revenue in 2024 of South America energy management systems market, while Industrial EMS is projected to accelerate at a 13.32% CAGR to 2030.

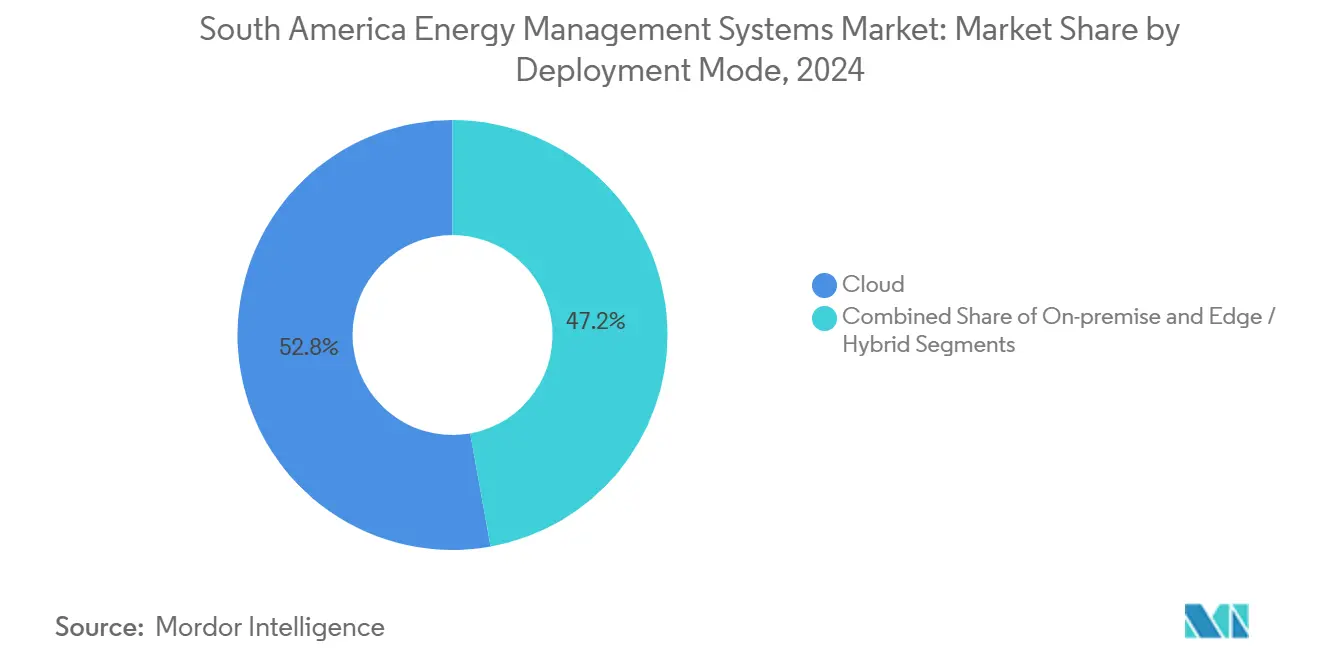

- By deployment mode, cloud held 52.83% share in 2024 of South America energy management systems market, yet edge and hybrid architectures are set to grow at 13.88% CAGR through 2030.

- By geography, Brazil accounted for a commanding 34.45% share of the South America energy management systems market size in 2024 and is expected to post a 13.55% CAGR to 2030.

South America Energy Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-mandated energy-efficiency targets | +1.8% | Brazil, Chile, Colombia; spillover to Argentina and Peru | Medium term (2-4 years) |

| Utility AMI roll-outs accelerating EMS adoption | +2.1% | Brazil dominant; Chile recovering from delays; Colombia and Peru emerging | Short term (≤ 2 years) |

| Fast-declining cost of connected sensors and controllers | +1.6% | Global, with strongest uptake in Brazil manufacturing belt and Chilean mining operations | Short term (≤ 2 years) |

| Corporate ESG disclosure pressure from EU-based buyers | +1.4% | Brazil, Chile, Argentina export corridors; concentrated in pulp, soy, lithium, copper sectors | Medium term (2-4 years) |

| Green-hydrogen pilot projects requiring advanced EMS | +1.3% | Brazil (Bahia, Ceará, Rio de Janeiro), Chile (Magallanes, Antofagasta), Argentina (Río Negro) | Long term (≥ 4 years) |

| Start-up-led EMS-as-a-Service models for SMEs | +1.2% | Brazil urban centers (São Paulo, Rio de Janeiro); early adoption in Santiago, Buenos Aires, Bogotá | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

State-Mandated Energy-Efficiency Targets

Mandatory plans in Brazil, Chile, and Colombia now require large facilities to install and certify EMS platforms, turning what was once a voluntary best practice into a legal obligation. Subsidized credit lines in Brazil lower the cost of capital by 300 basis points, accelerating adoption even among mid-tier manufacturers. Chile’s 24-month compliance deadline ensures a predictable project funnel for vendors despite recent tariff declines. Colombia’s energy audits link ISO 50001 certification to cap-ex approvals, embedding continuous monitoring into board-level investment decisione. Argentina and Peru trail but provincial programs signal convergence by 2027, extending the regional runway for the South America energy management systems market.

Utility AMI Roll-Outs Accelerating EMS Adoption

Brazil alone will install millions of smart meters by 2029, creating the granular interval data EMS algorithms require. The Siemens–CPFL Energia roll-out of 1.6 million meters in São Paulo embeds Gridscale X software, converting meter data into open APIs for third-party optimization. Uruguay’s near-universal AMI penetration shows smaller grids can leapfrog when regulations mandate interoperability. Chile’s revised tariff scheme unlocked new funding, restarting deployments stalled since 2022. As utilities shift to hourly tariffs, EMS becomes a profit center through demand response, reinforcing the growth trajectory of the South America energy management systems market.

Fast-Declining Cost of Connected Sensors and Controllers

Average selling prices for industrial IoT sensors now sit below USD 25 per node, making plant-wide instrumentation accessible to SMEs. The adoption of LoRaWAN in Brazilian and Chilean plants demonstrates that low-power networks can overcome cabling constraints. Affordable ARM-based gateways deliver sub-10 ms response times, meeting closed-loop motor control requirements on the factory floor. With hardware commoditized, vendors pivot toward software-as-a-service to protect margins, a shift pivotal to the future shape of the energy management systems industry. Open-source firmware reduces integration labor, making outcome-based contracts feasible for thousands of brownfield sites.

Corporate ESG Disclosure Pressure from EU Buyers

The EU’s CSRD extends Scope 3 reporting to South American suppliers by 2026, forcing pulp, soy, copper, and beef exporters to produce meter-verified energy data or risk delisting. Monthly attestation clauses in buyer contracts translate directly into EMS installations across export-oriented factories. Lithium and copper producers use EMS to document renewable sourcing and meet EU battery carbon-intensity caps. Argentina’s wineries are adopting ISO 50001 at a rate of double digits as European distributors tie payment terms to verified reductions. Cloud EMS platforms with audit dashboards therefore gain an edge, intensifying competitive focus within the South America energy management systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front CAPEX for legacy facility retrofits | -1.5% | Argentina, Peru, Colombia; secondary cities in Brazil and Chile | Medium term (2-4 years) |

| Low electricity tariffs in hydro-dominant grids | -1.0% | Brazil, Colombia, Paraguay; spillover to Argentina and Peru during wet seasons | Long term (≥ 4 years) |

| Scarcity of certified EMS integrators outside Brazil | -1.2% | Peru, Colombia, Argentina; interior regions of Brazil and Chile | Long term (≥ 4 years) |

| Cyber-security compliance gaps for OT networks | -0.8% | Regional, with acute exposure in Argentina, Peru, and secondary industrial zones across Brazil and Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-Front CAPEX for Legacy Facility Retrofits

Retrofit costs often exceed USD 50 per m², pushing paybacks beyond five years in Argentina and Peru where credit spreads run 400–600 bp above Brazilian levels. Brazil still counts 34,000 large industrial buildings without integrated EMS, representing USD 8–12 billion in potential but capital-intensive upgrades. Foreign-exchange controls in Argentina and interest rates above 20% erode investment appetite. Leasing and performance-contracting instruments remain nascent, fewer than 10 specialized ESCOs operate region-wide, so many SMEs wait for natural equipment-replacement cycles.[2]International Energy Agency, “Electricity 2024,” IEA, iea.org These financial realities temper near-term growth even as long-term fundamentals remain intact for the South America energy management systems market.

Scarcity of Certified EMS Integrators Outside Brazil

Fewer than 50 firms in Brazil offer turnkey ISO 50001 integration, with wait times up to 18 months in Manaus or Recife.[3]International Organization for Standardization, “ISO 50001 Certification Survey,” ISO.ORG, iso.org Chile, Argentina, Colombia, and Peru together have under 200 certified organizations, pushing travel and lodging costs 20–30% higher on projects outside capital cities. University curricula seldom cover protocols such as OPC UA or BACnet, creating a structural skills gap. Schneider Electric and Siemens training centers graduate only a fraction of required technicians each year. Consequently, vendors must absorb higher opex for field support or risk elongated sales cycles, a headwind that subtracts 1.2 percentage points from forecast CAGR across the South America energy management systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads, Services Surge

Software captured 46.83% of 2024 revenue as enterprises prioritized cloud analytics, automated reporting, and API-centric ecosystems that transform disparate data streams into actionable insights. Hardware sales remain essential, yet commoditized sensor nodes priced below USD 25 shift bargaining power toward platform vendors and consultants. Services are poised to grow at a 13.66% CAGR through 2030, reflecting ISO 50001 audit cycles and the complexity of integrating smart meters, edge gateways, and legacy SCADA. Siemens’ contract with CPFL Energia shows the weighting: 65% of deal value stems from software and ten-year managed services, not the 1.6 million meters themselves.

The South America energy management systems market size attributed to services will therefore rise more rapidly than that of hardware, redrawing profit pools. Vendors are bundling sensors, licenses, and consulting into savings-indexed contracts priced per kWh of verified reduction, dissolving traditional component silos. As audits recur annually, recurring revenue outpaces one-time equipment margins, reinforcing investor focus on SaaS multiples within the energy management systems industry. Hardware innovation now centers on secure boot and IEC 62443 compliance, features that enable premium pricing despite falling bill-of-materials cost.

By System Type: Buildings Dominate, Industry Accelerates

Building EMS delivered 43.73% of 2024 revenue, buoyed by São Paulo codes that compel integrated BMS in commercial towers above 5,000 m². Yet Industrial EMS is forecast to log the fastest 13.32% CAGR thanks to energy-intensive cement, steel, and chemical plants racing to cut costs and qualify for green-hydrogen offtake agreementS. Industrial demand already accounts for 31.63% of the South America energy management systems market size, and every 1% efficiency improvement drops directly to EBITDA lines.

Electrolyzer clusters, such as the 60 MW Bahia plant, require sub-10 ms response, a specification only industrial-grade controllers meet. In contrast, home EMS adoption lags because household tariffs rarely include dynamic pricing. Commercial real estate growth is steady but incremental, industrial retrofits can yield 15-20% savings in a single budget cycle, generating the business-case urgency that propels the South America energy management systems market.

By Deployment Mode: Edge and Hybrid Architectures Gain Ground

Cloud deployments held a 52.83% revenue share in 2024, as subscription models ease upfront spending and streamline updates. However, edge and hybrid solutions will advance 13.88% CAGR through 2030 as latency-sensitive manufacturing and hydrogen assets move analytics to the shop floor to comply with NIST SP 800-82r3 security guidelines.

Industrial motor control requires feedback below 10 ms, cloud round-trips average 50 ms, even on fiber, pushing critical loops to on-premises ARM-based gateways. Hybrid designs partition real-time control locally while synchronizing historical datasets to the cloud for AI and audit functions, aligning with ISO/IEC 27019 segmentation rules. These dual-mode architectures increase software complexity but unlock cross-site fleet optimization, raising switching costs and driving stickier revenue for the South America energy management systems market.

By End-User Industry: Manufacturing Leads, Commercial Buildings Accelerate

Manufacturing commanded 31.63% of 2024 demand, reflecting energy costs that consume up to 12% of OpEx in cement and steel plants. Colombia’s hydropower-dominated grid offers cheap off-peak electricity at USD 0.11/kWh, encouraging sophisticated load-shifting strategies deployed through EMS.

Commercial buildings are set to expand at a 13.29% CAGR because 1,500+ LEED projects in Brazil must document continuous energy improvement to maintain certification. EU Scope 3 mandates place additional pressure on exporters operating offices, warehouses, and cold storage, driving fresh installations and reinforcing growth for the South America energy management systems market. Utilities, data centers, and healthcare facilities round out demand, with AI-driven cooling and mission-critical redundancy requirements steering procurement toward advanced platforms.

Geography Analysis

Brazil will remain the anchor of the South America energy management systems market., holding 34.45% revenue share in 2024 and charting a 13.55% CAGR through 2030 as ANEEL Resolution 1000 mandates smart meters for every consumer. The country’s green-hydrogen laws (14.990 and 15.269) further obligate advanced EMS for electrolyzer clusters, ensuring multi-year project pipelines. Hydro dominance flattens tariff volatility but creates lucrative negative-price windows that EMS software exploits to trim industrial bills and monetize grid services.

Chile’s renewable fleet already tops 60% of generation, yet tariff collapses slowed ROI on EMS between 2022–24. The National Energy Commission’s 2024 directive compels large users to install management systems within two years, reigniting demand despite low spot prices. Transmission auctions worth USD 5 billion will expand north–south interties, widening canvases for plant-wide optimization and boosting the regional South America energy management systems market.

Argentina, Colombia, Peru, and the rest of South America contribute smaller but rising portions. Argentina’s Hychico project pairs 2 GW wind with 200,000 t hydrogen, showcasing EMS roles in hybrid asset orchestration. Colombia’s hydropower grid and Law 2407 that links energy audits to cap-ex approvals create a policy-driven floor for EMS procurement. Peru’s market is nascent, constrained by capital costs and integrator scarcity, yet multilateral bank funding earmarked for AMI pilots sets the stage for future growth.

Competitive Landscape

The South America energy management systems market is moderately concentrated. ABB, Schneider Electric, and Siemens jointly capture about 40-45% of revenue through hardware-software-services bundles that lock in ten-year cash flows. Siemens’ CPFL deal illustrates the pivot toward recurring software: meters ship once, but data-management and analytics fees flow annually. Schneider’s EcoStruxure and Honeywell’s Forge embed AI routines that predict equipment failure and optimize real-time demand response, amplifying value beyond mere energy savings.

Cloud-native challengers, C3.ai, EnergyHub, GridPoint, target the mid-market with EMS-as-a-Service subscriptions under USD 500 per site, slashing payback periods and enlarging the total addressable market. Integrator scarcity shapes go-to-market choices: newer entrants vertically integrate installation, while incumbents run certification academies that graduate roughly 500 technicians annually against demand exceeding 2,000. Sensor commoditization below USD 25 forces all vendors to mine margin from software IP and compliance consulting, reinforcing platform stickiness within the South America energy management systems market.

Technology moats increasingly rest on cybersecurity and hybrid-edge orchestration. ISO/IEC 27019 and IEC 62443 demand segmented networks, and vendors with proven dual-mode stacks win bids from hydrogen developers and data-center operators. As utilities open APIs around DLMS/COSEM meters, third-party applications proliferate, threatening vendor lock-in but expanding ecosystem value. Market entrants that master open standards and provide turnkey field support will capitalize on white-space in Peru and Colombia, where certifications remain below 100 organizations each.

South America Energy Management Systems Industry Leaders

ABB Ltd.

IBM Corporation

Schneider Electric SE

Siemens AG

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens partnered with CPFL Energia to install 1.6 million smart meters across São Paulo by 2029, bundling Gridscale X data-management software and a 10-year managed-services package that makes up 65% of the deal’s value.

- February 2025: Schneider Electric introduced EcoStruxure Resource Advisor to South America, a cloud platform that lets multi-site companies track energy, water, and carbon ahead of the EU CSRD reporting deadline in 2026.

- January 2025: ABB committed USD 50 million to expand its Sorocaba, Brazil factory, adding lines for edge gateways and IoT sensors to serve fast-growing industrial retrofit and hydrogen projects.

- January 2025: Unigel brought its 60 MW green-hydrogen plant in Bahia online, delivering 10,000 tons a year for ammonia production and using sub-10 ms control loops to keep electrolyzers in sync with variable wind power.

South America Energy Management Systems Market Report Scope

The South America energy management systems market report is segmented by Component (Hardware, Software, Services), System Type (Home Energy Management Systems (HEMS), Building Energy Management Systems (BEMS), Industrial Energy Management Systems (IEMS)), Deployment Mode (On-premise, Cloud/SaaS, Edge/Hybrid), End-user Industry (Manufacturing, Power and Energy, IT and Telecommunication, Healthcare, Commercial Buildings), and Geography (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). Market Forecasts are Provided in Terms of Value (USD).

By Component

| Hardware |

| Software |

| Services |

By System Type

| Home Energy Management Systems (HEMS) |

| Building Energy Management Systems (BEMS) |

| Industrial Energy Management Systems (IEMS) |

By Deployment Mode

| On-premise |

| Cloud / SaaS |

| Edge / Hybrid |

By End-user Industry

| Manufacturing |

| Power and Energy |

| IT and Telecommunication |

| Healthcare |

| Commercial Buildings |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Component | Hardware |

| Software | |

| Services | |

| By System Type | Home Energy Management Systems (HEMS) |

| Building Energy Management Systems (BEMS) | |

| Industrial Energy Management Systems (IEMS) | |

| By Deployment Mode | On-premise |

| Cloud / SaaS | |

| Edge / Hybrid | |

| By End-user Industry | Manufacturing |

| Power and Energy | |

| IT and Telecommunication | |

| Healthcare | |

| Commercial Buildings | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size and growth rate of South America’s energy management systems sector?

Valued at USD 3.68 billion in 2025, the sector is forecast to reach USD 6.78 billion by 2030, advancing at a 12.99% CAGR.

Which South American country is expected to post the fastest EMS adoption through 2030?

Brazil is projected to log a 13.55% CAGR, driven by mandatory smart-meter roll-outs and large-scale green-hydrogen investments.

Why are edge and hybrid deployments gaining traction in South American EMS projects?

Latency-sensitive applications such as electrolyzers and mining equipment need sub-10 ms response times, prompting analytics to shift from cloud to on-prem gateways that still sync historical data to the cloud.

How do green-hydrogen projects in Brazil and Chile influence EMS demand?

Multi-hundred-megawatt electrolyzer clusters require high-speed control loops and real-time load balancing, creating new revenue streams for industrial-grade EMS platforms.

What financial hurdles slow EMS retrofits for older factories in Argentina and Peru?

Retrofit costs can top USD 50 per m², while local loans carry real interest rates above 20%, extending payback periods beyond five years for many facilities.

Page last updated on: