South America Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

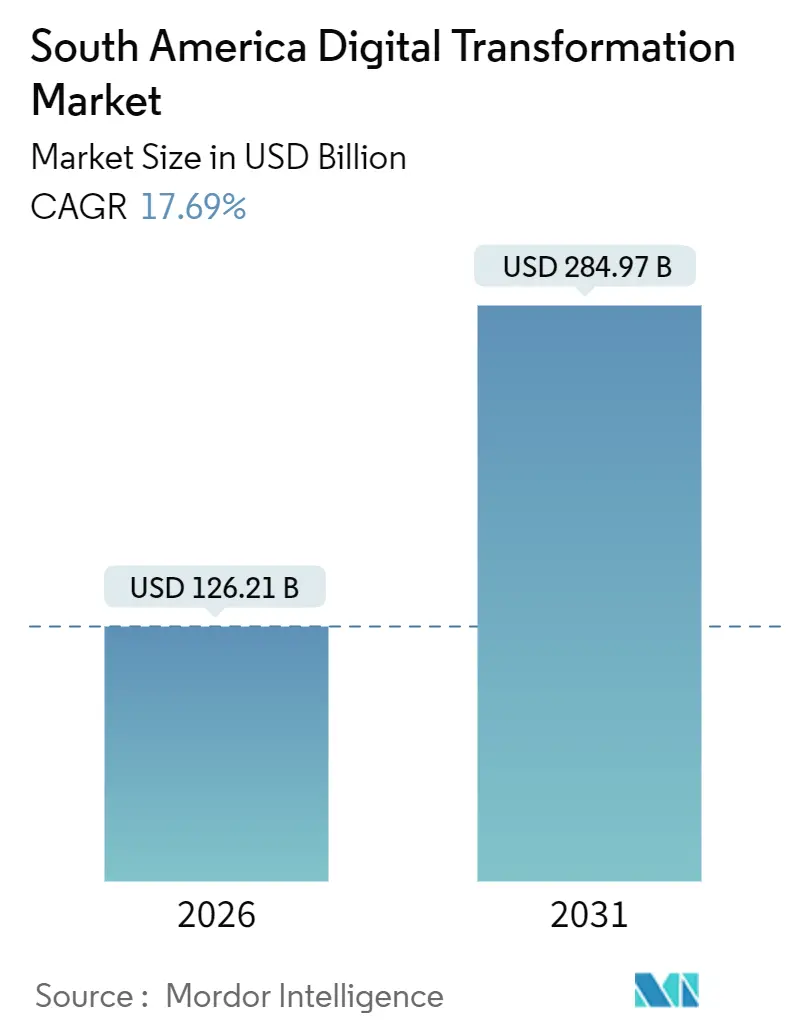

| Market Size (2026) | USD 126.21 Billion |

| Market Size (2031) | USD 284.97 Billion |

| Growth Rate (2026 - 2031) | 17.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Digital Transformation Market Analysis by Mordor Intelligence

The South America digital transformation market size stood at USD 126.21 billion in 2026 and is projected to reach USD 284.97 billion by 2031, reflecting a robust 17.69% CAGR over the forecast period. Investments are shifting decisively from legacy on-premise stacks to hybrid and multi-cloud environments, enabling real-time analytics at the edge, lower-latency 5G connectivity, and programmable payment rails that embed finance into everyday workflows. Brazil’s 2024 launch of the DREX central-bank digital currency formalized programmable money as core infrastructure. Colombia’s 2025 approval of standalone 5G networks accelerated industrial IoT rollouts, enabling manufacturers to control robots and run predictive-maintenance algorithms with sub-10 millisecond latency. Hyperscale clouds continue to localize availability zones to comply with stringent data-residency rules under Brazil’s Lei Geral de Proteção de Dados, while large enterprises experiment with digital twins that replicate mining sites, refineries, and assembly lines in software to cut downtime. Venture capital dry powder remains abundant for artificial-intelligence start-ups, but the region’s chronic talent shortage pushes firms toward low-code and no-code tooling.

Key Report Takeaways

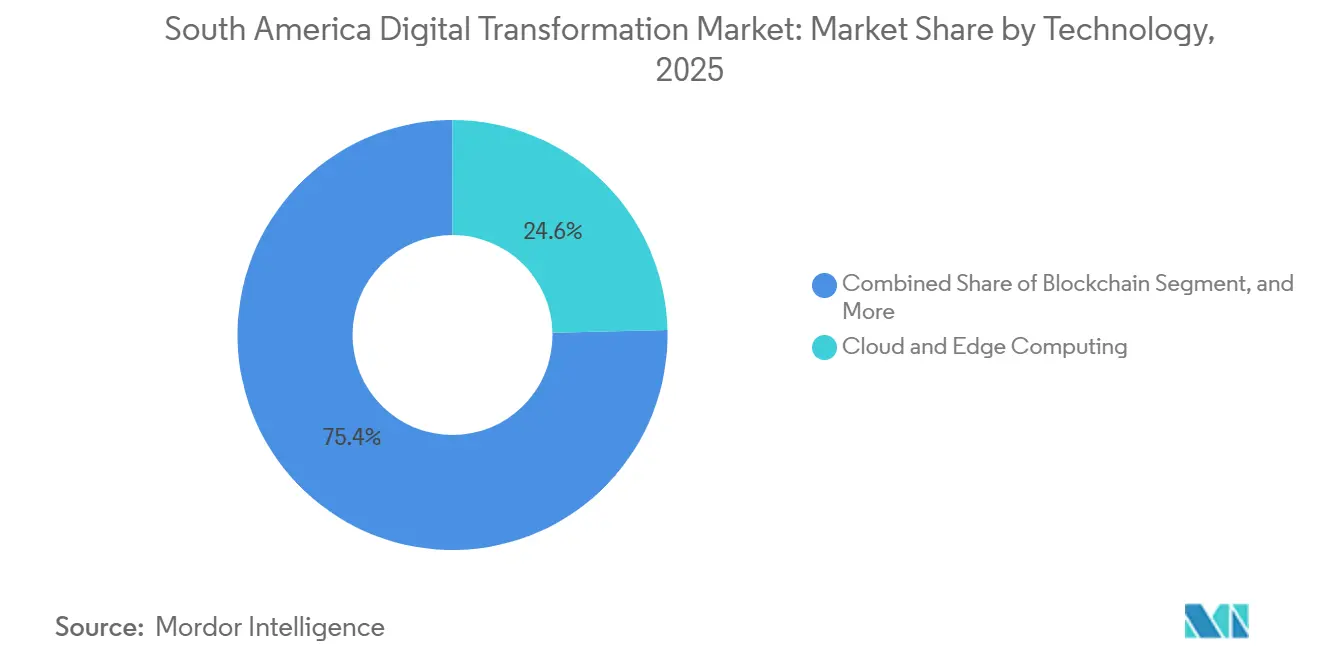

- By technology, cloud and edge computing led with a 24.63% share of the South America digital transformation market in 2025, while 5G-enabled industrial IoT is forecast to expand at a 19.44% CAGR to 2031

- By end-user industry, banking, financial services, and insurance accounted for 23.57% share of the South America digital transformation market in 2025, whereas manufacturing is set to grow at a 19.49% CAGR through 2031

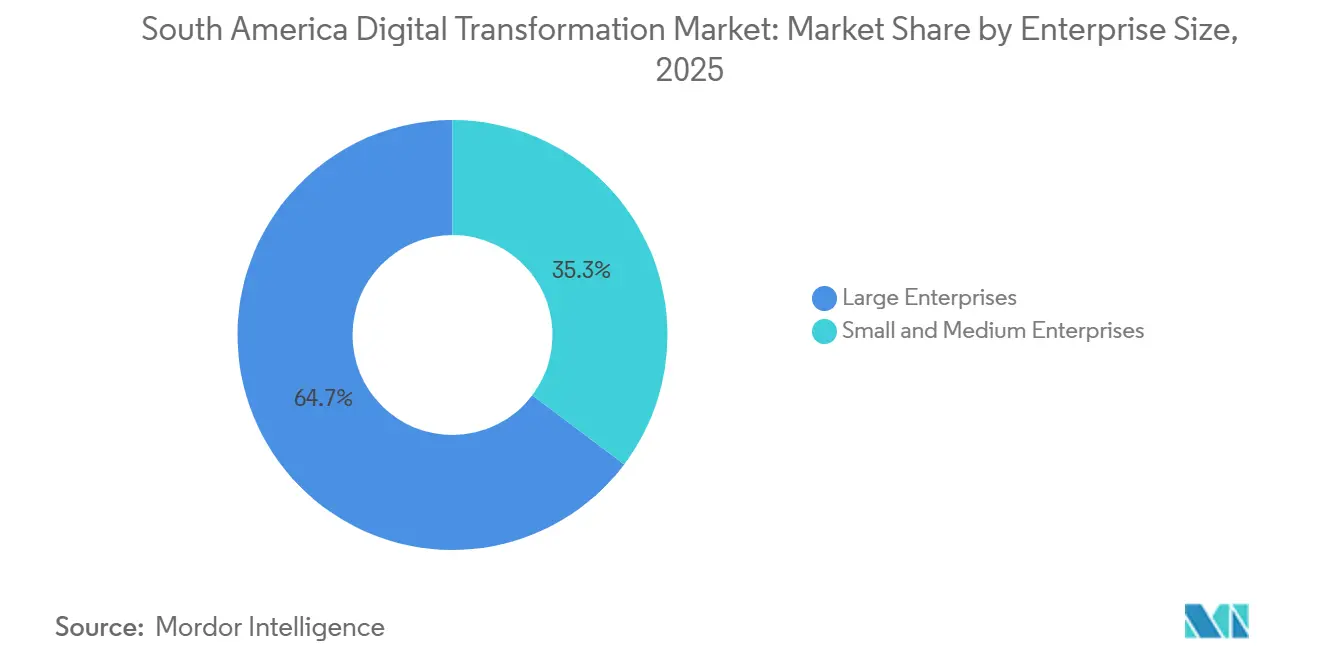

- By enterprise size, large enterprises held 64.72% of the 2025 deployment value, yet small and medium enterprises are projected to rise at an 18.12% CAGR to 2031

- By deployment model, public cloud captured 54.93% share of the South America digital transformation market in 2025, while hybrid and multi-cloud architectures are advancing at an 18.34% CAGR through 2031

- By geography, Brazil commanded 46.89% of 2025 regional expenditure, whereas Colombia is forecast to register the fastest 18.58% CAGR between 2026 and 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Anticipated developments are shaped at a system level, with Latin america signals feeding into a larger global picture. The outlook on global digital transformation (dx) market consolidates these expectations.

South America Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Cloud Adoption Across South American Enterprises | +3.2% | Brazil, Colombia, Chile, spillover to Argentina and Peru | Medium term (2-4 years) |

| Surging Investment in Regional Data Centers and Edge Facilities | +2.8% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Government-Led Open Banking and Instant Payments Initiatives | +3.5% | Brazil, Colombia, Argentina | Short term (≤2 years) |

| Talent-Shoring Boom Attracting Global IT Projects to Near-shore Hubs | +2.1% | Argentina, Colombia, Brazil | Long term (≥4 years) |

| 5G Stand-Alone Roll-outs Unlocking Low-Latency Industrial IoT | +3.4% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Venture Capital Dry Powder Targeting AI-Native Start-ups | +1.9% | Brazil, Argentina, Colombia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government-Led Open Banking and Instant Payments Initiatives

Brazil’s Pix rail handled 42 billion transactions in 2024 and now exceeds credit-card volumes, forcing banks to expose standardized APIs for account aggregation, credit underwriting, and payment initiation.[1]Banco Central do Brasil, “Open Finance and DREX Initiatives,” bcb.gov.br More than 1,000 Brazilian institutions had joined the Open Finance network by mid-2025, catalyzing data-driven lending to micro-enterprises. Colombia followed with its own instant-payments platform in 2024, and Argentina’s Transferencias 3.0 framework went live in early 2025. Because ISO 20022 messages travel with rich metadata, fraud analytics and anti-money-laundering engines can flag anomalies in real time. The regulatory direction is clear, making low-cost instant payments a public good and shifting competition toward value-added analytics and embedded finance.

5G Standalone Roll-outs Unlocking Low-Latency Industrial IoT

Colombia’s 2025 decision to authorize standalone 5G cores opened the door to network slicing reserved for factories, ports, and mines, free from consumer-traffic contention. Standalone 5G supports one million devices per square kilometer and latency below 10 milliseconds, performance thresholds that enable autonomous robots, augmented-reality maintenance, and AI-driven vision systems on assembly lines. Brazil’s earlier spectrum auction imposes coverage obligations on every municipality with more than 30,000 inhabitants by 2029, ensuring that secondary industrial centers also benefit. With these policies, manufacturers can dismantle costly private LTE islands and still meet deterministic networking requirements, accelerating the South America digital transformation market.

Accelerated Cloud Adoption Across South American Enterprises

Amazon Web Services expanded its São Paulo region to six availability zones in 2025, backed by USD 1.8 billion in committed capital.[2]Amazon Web Services, “AWS Expands São Paulo Region,” aws.amazon.com Microsoft pledged BRL 14.7 billion (USD 2.9 billion) for Brazilian cloud and AI infrastructure that same year, alongside a program to upskill 5 million citizens by 2028. Chile earmarked USD 4 billion for data centers in 2024, positioning itself as a disaster-recovery hub powered by renewable energy. Stringent data-residency clauses impose monetary penalties of up to 2% of domestic revenue, making local cloud regions mandatory rather than optional. As a result, organizations migrate core workloads even while keeping certain legacy applications on-premise, driving steady growth in the South America digital transformation market.

Surging Investment in Regional Data Centers and Edge Facilities

Infrastructure funds and real estate investment trusts have directed multibillion-dollar capital toward metro-adjacent data center campuses. Patria Investments, for instance, launched a USD 1 billion platform in 2024 with 120 MW of initial capacity across São Paulo, Rio de Janeiro, and Brasília. Edge nodes reduce latency for point-of-sale analytics, fraud detection, and industrial quality inspection, yet rising electricity tariffs of USD 0.12 to USD 0.15 per kilowatt-hour in Brazil and higher in Argentina threaten operating margins.[3]International Energy Agency, “Electricity Prices in South America 2025,” iea.org Operators are countering volatility through long-term renewable energy purchase agreements, but intermittent generation still requires battery storage, which remains expensive. Even so, edge capacity additions in Latin America grew 22% per year between 2023 and 2025, confirming a sustained shift toward distributed compute architectures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Digital Skills Gap and Brain Drain | -2.4% | Region-wide, acute in Argentina and Venezuela, moderate in Brazil and Colombia | Long term (≥4 years) |

| Fragmented Regulatory Environment Across Countries | -1.8% | MERCOSUR and Andean trade corridors | Medium term (2-4 years) |

| Under-investment in Rural Backbone Connectivity | -1.6% | Rural Brazil, Colombia, Peru | Long term (≥4 years) |

| Rising Energy Costs Threatening Data-Center Economics | -1.3% | Argentina, Southeast Brazil, peak-demand Chile | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Chronic Digital Skills Gap and Brain Drain

The Inter-American Development Bank estimates that South America needs 2.3 million additional technology workers by 2025, yet universities graduate fewer than 400,000 computer science specialists each year. Argentina’s inflationary spiral accelerated outward migration; LinkedIn traffic shows a 28% jump in local software engineers relocating abroad in 2025. Brazilian salaries climbed 18% in nominal terms in 2025 but failed to outpace consumer-price growth, so mid-career engineers increasingly accept remote gigs paying in USD. Microsoft’s upskilling initiative aims to train 5 million Brazilians by 2028, yet the near-term gap compels firms to adopt low-code platforms that favor speed over full customization, moderating overall market growth.

Fragmented Regulatory Environment Across Countries

Brazil’s Lei Geral de Proteção de Dados mirrors Europe’s GDPR and mandates local data processing, whereas Argentina’s older privacy law lacks clarity on cross-border transfers, forcing multinationals to run parallel compliance frameworks. Colombia updated its statute in 2024 to allow transfers under adequacy rulings, yet Chile’s ongoing constitutional debate over digital rights introduces policy uncertainty. The OECD estimates that regional compliance costs rise 15-20% when firms operate across multiple jurisdictions. This fragmentation slows deployment, increases the total cost of ownership, and reduces the South America digital transformation market CAGR by nearly 2 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Edge and IoT Convergence Reshapes Infrastructure Spend

Cloud and edge computing captured 24.63% of 2025 spending, the largest share in the South America digital transformation market, as enterprises route latency-sensitive analytics to distributed nodes closer to data sources. Within the South America digital transformation market size for technology segments, 5G-enabled industrial IoT devices are projected to post the fastest 19.44% CAGR through 2031, reflecting a wave of factory retrofits, sensor meshes, and digital twin overlays that shift data processing from centralized clouds to on-premises gateways.

Edge-native streaming engines now monitor conveyor belts, detect micro-defects, and trigger real-time quality adjustments without a round-trip to distant data centers. Digital twins moved from pilot to production when Peru’s Quellaveco copper complex cut unplanned downtime by 30% during 2025 operations. Meanwhile, blockchain’s footprint expanded into supply-chain traceability after a leading meatpacker slashed fraud claims by 40% with distributed ledger tracking. Extended-reality tools remain niche, mostly in automotive design and mining safety, while quantum computing is still confined to universities. These adoption patterns confirm that diversified, edge-heavy architectures will sustain long-run demand across the South America digital transformation market.

By End-User Industry: Manufacturing Overtakes BFSI in Growth Velocity

Banking, financial services, and insurance accounted for the largest 23.57% share of 2025 spending, underpinned by open finance compliance and instant payment rails that forced banks to modernize their fraud analytics engines. However, manufacturing is poised for the fastest 19.49% CAGR through 2031, positioning the vertical to outpace BFSI in the incremental South America digital transformation market. Automotive lines are re-tooled for software-defined assembly, and mining operators deploy autonomous haulage to lower costs and improve worker safety.

Healthcare spending accelerated once Brazil’s nationwide telemedicine backbone linked 5,000 municipalities in 2024, bringing remote diagnostics to underserved regions. Retail leaders paired last-mile telemetry with e-commerce storefronts that now serve 52 million active buyers. Energy utilities rolled out smart-grid sensors that curb line losses, and public-sector agencies digitized tax filings to widen compliance nets. The common thread is a pivot from siloed IT toward converged information and operational technology, unlocking productivity gains previously unattainable through labor arbitrage alone.

By Enterprise Size: SME Adoption Accelerates on No-Code Platforms

Large organizations still commanded 64.72% of deployment value in 2025, reflecting deep budgets and long procurement cycles. Yet small and medium enterprises are forecast to grow 18.12% a year, eroding the gap as subsidized cloud credits from Brazil’s small-business agency, and Microsoft enabled 50,000 firms to migrate accounting suites to software-as-a-service environments in 2025. SMEs therefore leapfrog on-premise servers and move directly into subscription apps that bundle finance, sales, and invoicing.

Hybrid dynamics emerge as large enterprises keep core ERP on-premises for data sovereignty or latency reasons, but run customer-facing workloads in the public cloud, whereas SMEs remain all-in on browser-based tools that require no dedicated IT staff. This divide shapes vendor strategy. Hyperscalers pursue Fortune-500 affiliates with consultative sales and volume discounts, while independent software vendors rely on digital marketplaces and partner channels to penetrate the SME segment. The resulting dual-track demand ensures that both ends of the customer pyramid fuel the South America digital transformation market.

By Deployment Model: Hybrid Architectures Gain as Lock-In Fears Rise

Public cloud retained 54.93% of deployment outlays in 2025, the single-largest share in the South America digital transformation market at the infrastructure layer, but hybrid and multi-cloud configurations are projected to register an 18.34% CAGR through 2031 as chief information officers hedge against vendor lock-in and outage risk. A leading Brazilian bank disclosed in 2025 that it split workloads across Amazon Web Services, Microsoft Azure, and Google Cloud to align with concentration-risk guidelines and negotiate favorable pricing.

Second-generation hybrids replicate public-cloud APIs on private appliances, keeping data within national borders while applications scale elastically during peak demand. Sensitive healthcare and energy workloads remain on-premises to meet privacy and critical infrastructure directives, but edge gateways now backhaul aggregated insights to centralized data lakes for machine learning training. The net effect is a fluid workload-placement model calibrated around latency, egress fees, and regulatory gravity, which will continue to reallocate the South America digital transformation market size across deployment choices over the forecast horizon.

Geography Analysis

Brazil remained the anchor, representing 46.89% of spending in 2025 on the strength of São Paulo’s financial district and the Manaus Free Zone’s electronics cluster. The country’s unified privacy law, sizable consumer base, and venture-capital pipeline that funded 450 tech start-ups in 2024 give it scale advantages. Colombia is projected to deliver the fastest CAGR of 18.58% to 2031, propelled by mandatory e-invoicing, contactless metro fares, and its 2025 standalone 5G authorization. The South America digital transformation market, driven by Colombia’s industrial sector, is therefore set to outpace aggregate regional growth.

Argentina’s share remains volatile. Inflation exceeded 200% in 2024, and power tariffs climbed above USD 0.20 per kilowatt-hour in certain provinces, undercutting data-center economics. Even so, Córdoba and Rosario continue to court North American clients who value near-shore software teams operating within two time zones, sustaining a pipeline of apps focused on fintech and e-commerce. The rest of South America, which includes Chile, Peru, and Uruguay, benefits from digitalized mining operations, seismic-resistant data center campuses, and high household broadband penetration.

Chile devoted USD 4 billion to new server farms in 2024, betting on renewable energy and disaster recovery services. Peru’s mining complexes rely on digital twins to predict ore grade, boosting output while cutting downtime. Uruguay couples macroeconomic stability with 85% fixed-internet coverage, positioning Montevideo as a regional back-office hub. Enterprises that operate region-wide must therefore craft portfolio strategies that combine Brazil’s scale, Colombia’s momentum, and Chile’s reliability with hedges against Argentina’s macro swings, reinforcing the nuanced country-selection calculus behind South America digital transformation market investments.

Mordor Intelligence delivers a comprehensive view of the digital transformation (dx) market across all major regions such as Middle East, Asia, and Europe, alongside country-level analysis for Mexico, Brazil, Colombia, Qatar, India, and Netherlands, each offering a view of the local market realities.

Competitive Landscape

Competition is moderately fragmented. Amazon Web Services, Microsoft, and Google collectively captured about 40% of infrastructure-as-a-service revenue in 2025 after launching new cloud regions in São Paulo, Rio de Janeiro, and Santiago, moves designed to meet data-residency mandates under Brazil’s privacy act and Argentina’s personal-data statute. Regional systems integrators such as Globant and TOTVS are shifting from bespoke coding to platform-as-a-service bundles that compress roll-out times and sacrifice some consulting margin in favor of recurring subscriptions.

White-space growth now clusters around industrial edge computing. Robotics control, augmented-reality service calls, and vision-based inspection require compute nodes inside factory fences, an area where hyperscalers partner with telecom carriers to embed micro-data centers within 50 kilometers of industrial sites. Artificial-intelligence native start-ups flourish, raising record funding rounds in 2025 despite global venture pullbacks. A Brazilian vendor secured USD 100 million to commercialize a Portuguese-language data-lakehouse optimized for retail and banking clients, underscoring the value of linguistic and regulatory localization.

Product roadmaps emphasize vertical depth over horizontal feature sprawl. SAP and Oracle defend their enterprise resource planning in energy and utilities. Salesforce strengthens customer-relationship management in retail and telecom. TOTVS continues to dominate Brazilian SMEs courtesy of natively compliant tax modules. As customers weigh workload portability, industry-specific data models, and local legal expertise, competitive differentiation is moving up the stack from infrastructure toward compliance and domain-rich applications, reshaping the strategic contours of the South America digital transformation market.

South America Digital Transformation Industry Leaders

Accenture plc

International Business Machines Corporation

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft announced a BRL 14.7 billion (USD 2.9 billion) investment in Brazilian cloud infrastructure and AI capabilities, partnering with the federal government to train 5 million citizens in digital skills by 2028.

- September 2025: Globant acquired a Brazilian AI consultancy for USD 45 million, adding 200 machine-learning engineers and natural-language-processing specialists to support generative AI deployments.

- August 2025: Colombia’s ICT ministry authorized 5G standalone core networks, enabling network slicing for industrial IoT applications.

- June 2025: Amazon Web Services expanded its São Paulo region with three new availability zones, bringing cumulative investment to USD 1.8 billion.

South America Digital Transformation Market Report Scope

The South America Digital Transformation Market Report is Segmented by Technology (Analytics, Artificial Intelligence and Machine Learning, Extended Reality, Internet of Things, Industrial Robotics, Blockchain, Digital Twin, Additive Manufacturing / 3D Printing, Cloud and Edge Computing, Other Technologies), End-User Industry (BFSI, Healthcare and Life-Sciences, Manufacturing and Industrial, Retail and E-commerce, Energy and Utilities, Automotive and Transportation, Government and Public Sector, Telecom and IT, Other End-User Industries), Enterprise Size (Large Enterprises, Small and Medium Enterprises), Deployment Model (Cloud, On-Premise, Hybrid), and Geography (Brazil, Argentina, Colombia, Rest of South America). Market Forecasts are Provided in Terms of Value (USD).

| Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality |

| Internet of Things |

| Industrial Robotics |

| Blockchain |

| Digital Twin |

| Additive Manufacturing / 3D Printing |

| Cloud and Edge Computing |

| Other Technologies |

| BFSI |

| Healthcare and Life-Sciences |

| Manufacturing and Industrial |

| Retail and E-commerce |

| Energy and Utilities |

| Automotive and Transportation |

| Government and Public Sector |

| Telecom and IT |

| Other End-User Industries |

| Large Enterprises |

| Small and Medium Enterprises |

| Cloud |

| On-Premise |

| Hybrid |

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Technology | Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality | |

| Internet of Things | |

| Industrial Robotics | |

| Blockchain | |

| Digital Twin | |

| Additive Manufacturing / 3D Printing | |

| Cloud and Edge Computing | |

| Other Technologies | |

| By End-User Industry | BFSI |

| Healthcare and Life-Sciences | |

| Manufacturing and Industrial | |

| Retail and E-commerce | |

| Energy and Utilities | |

| Automotive and Transportation | |

| Government and Public Sector | |

| Telecom and IT | |

| Other End-User Industries | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Deployment Model | Cloud |

| On-Premise | |

| Hybrid | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America digital transformation market in 2026?

It reached USD 126.21 billion in 2026 and is projected to grow at a 17.69% CAGR through 2031.

Which segment is expanding the fastest?

The 5G-enabled industrial IoT technology segment is forecast to post a 19.44% CAGR to 2031.

Why is Colombia expected to outpace other countries?

Mandatory e-invoicing, standalone 5G approval, and metro contactless fares push Colombia toward an 18.58% CAGR.

What is driving SME adoption?

Subsidized cloud credits and no-code platforms lower upfront costs, allowing SMEs to migrate directly to cloud services.

How are rising energy prices influencing data-center strategy?

Operators sign long-term renewable-energy contracts and deploy edge nodes closer to users to mitigate power-price volatility.

What skills shortage challenges do firms face?

The region lacks 2.3 million tech professionals, forcing companies to rely on upskilling programs or low-code tools to bridge the gap.

Page last updated on: