South America Customs Brokerage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

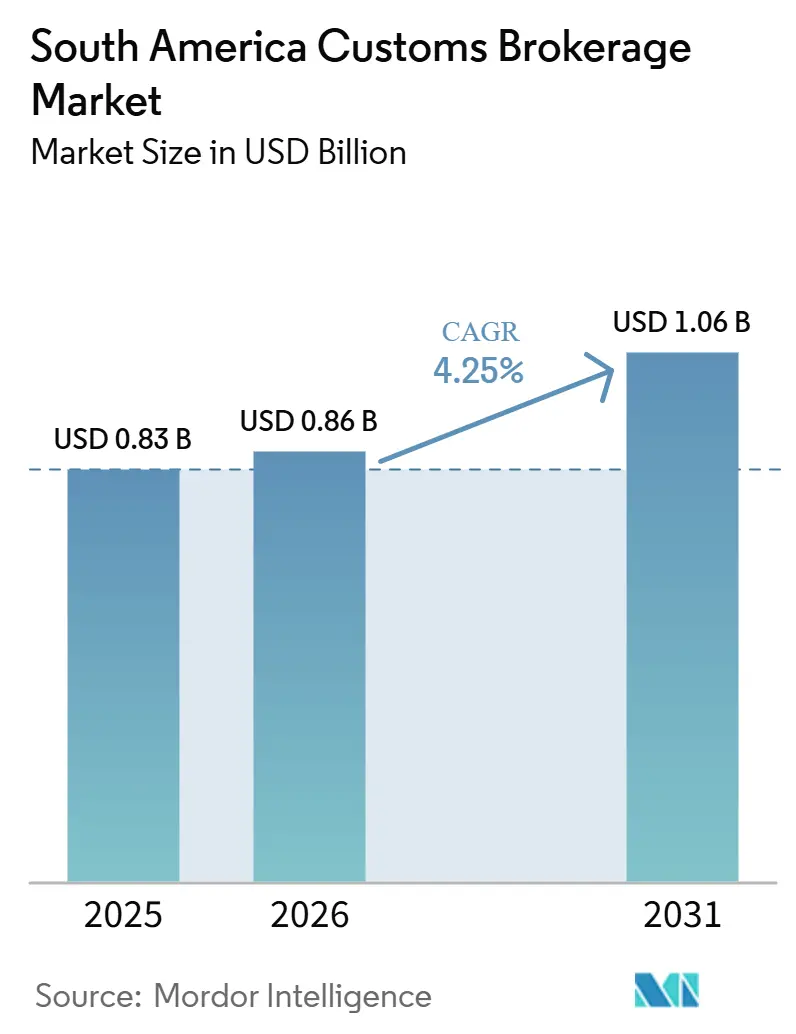

| Base Year Market Size (2025) | USD 0.83 Billion |

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.06 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

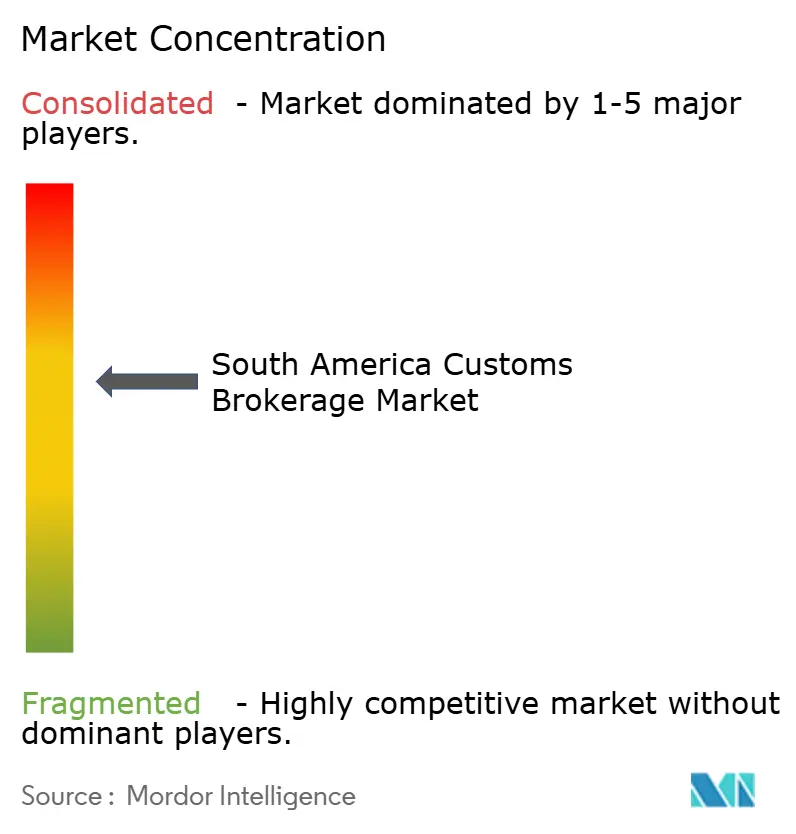

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Customs Brokerage Market Analysis by Mordor Intelligence

The South America customs brokerage market size was valued at USD 826.83 million in 2025 and estimated to grow from USD 862.6 million in 2026 to reach USD 1062.25 million by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

Growing e-commerce parcel flows, regional single-window programs, and near-shoring by automotive and electronics manufacturers keep volumes resilient even as tariff schedules change each quarter. Ocean freight still leads by tonnage, yet the South America customs brokerage market is increasingly shaped by air-express clearances that promise 72-hour door-to-door delivery for small parcels and temperature-controlled pharmaceuticals. Digital import-declaration systems such as Brazil’s DUIMP and Chile’s SICEX shorten filing cycles to minutes, prompting brokers to offer API connections instead of couriering paper. Large 3PL-integrated operators continue bundling clearance into freight contracts, but pure-play brokers that focus on post-clearance audit defense and duty-drawback services are carving out margin-defensible niches. Capital spending on port and airport capacity signals that customs throughput will keep rising even if container rates fluctuate.

Key Report Takeaways

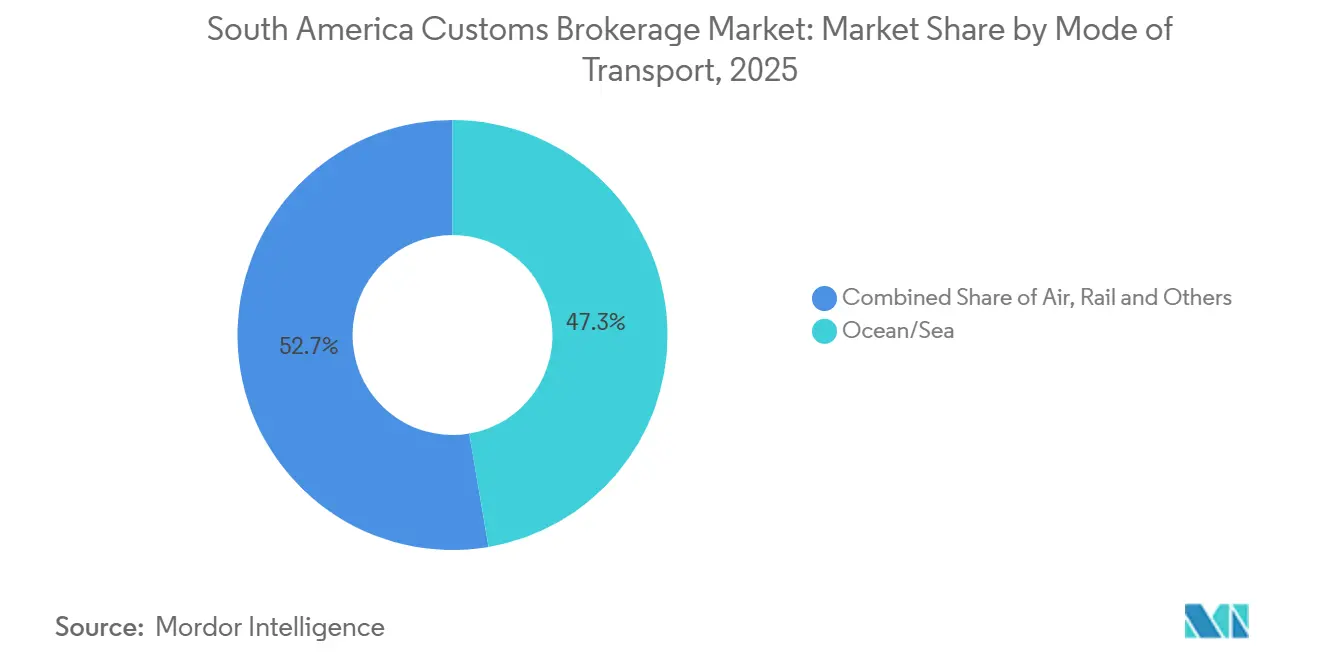

- By mode of transport, ocean freight led with 47.33% of the South America customs brokerage market share in 2025, while air express is forecast to advance at a 5.46% CAGR through 2031.

- By broker type, freight-forwarder and 3PL-integrated operators held 60.67% of the South America customs brokerage market size in 2025, whereas pure customs brokers are projected to grow at a 4.88% CAGR to 2031.

- By importer size, large enterprises accounted for 40.9% of the South America customs brokerage market share in 2025, and SMEs are expanding at a 6.09% CAGR over 2026-2031.

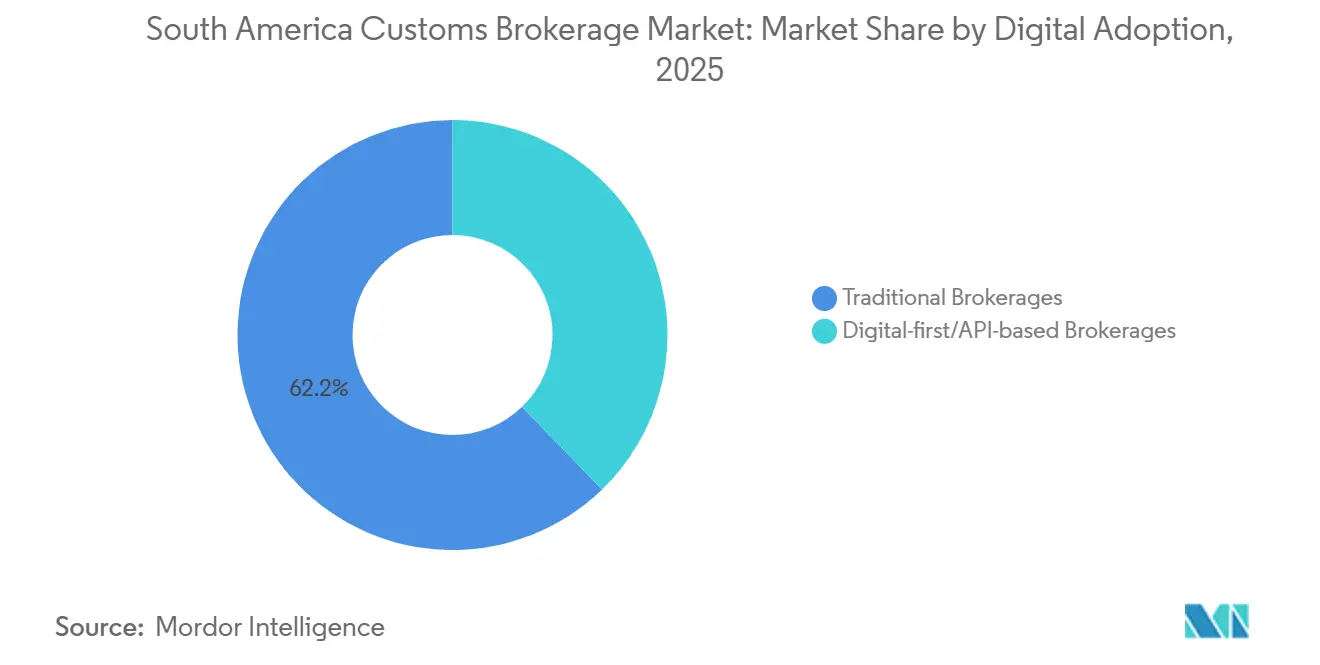

- By digital adoption, traditional brokerages retained 62.24% share in 2025, but API-driven counterparts are set to post an 11.82% CAGR to 2031.

- By end-use industry, retail and e-commerce commanded 26.5% of the South America customs brokerage market size in 2025, while automotive and EV applications are on track for a 7.01% CAGR through 2031.

- By country, Brazil dominated with 47.11% share in 2025, and Colombia represents the fastest-growing market at a 6.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Customs Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border E-Commerce Boom | +0.9% | Brazil, Argentina, Chile, Colombia | Short term (≤ 2 years) |

| Mercosur & Pacific Alliance Trade Facilitation | +0.7% | Mercosur bloc, Pacific Alliance members | Medium term (2-4 years) |

| Digital Customs-Clearance Platforms | +1.2% | Chile, Colombia, Peru, Brazil | Medium term (2-4 years) |

| Near-Shoring of Supply Chains into South America | +0.6% | Brazil, spill-over to Colombia, Argentina | Long term (≥ 4 years) |

| Emergence of Amazonian Free-Trade Zones | +0.4% | Brazil (Manaus), northern tier | Long term (≥ 4 years) |

| Carbon-Footprint Disclosure in Customs Paperwork | +0.3% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cross-Border E-Commerce Boom

Low-value parcels already form more than one-quarter of customs declarations in Brazil, Argentina, and Chile, pushing brokers to process higher transaction counts for lower fees. Brazil’s Remessa Conforme program enrolls 67% of inbound parcels and collects duties upfront, shifting brokerage work upstream to platforms like Mercado Libre. Colombia’s USD 5,000 simplified-declaration ceiling achieves a similar effect and accelerates SME imports. Argentina’s SUCA portal handled 3.2 million parcels in its first year, encouraging brokers to automate rather than re-key data. Accelerated clearance cycles enlarge the addressable South America customs brokerage market as more merchants begin exporting directly[1]Receita Federal do Brasil, “Remessa Conforme Program,” gov.br.

Mercosur & Pacific Alliance Trade Facilitation

The AEO-reciprocity pact signed in 2025 covers 570 Colombian companies and removes duplicate compliance audits across five economies. Brazil and Argentina activated the AFC PLUS system in 2026, imposing 12-hour targets for green-channel cargo and creating predictable dwell times. Chile integrated certificate-of-origin exchanges with Mexico, Peru, and Colombia, while Peru’s VUCE mandates full inter-agency linkage by December 2026. Harmonized processes enlarge the South America customs brokerage market because exporters expand intra-regional trade when clearance risk falls.

Digital Customs-Clearance Platforms (Single Window, Blockchain)

Chile’s Smartflux verifies documents on a CADENA blockchain and cuts container release to 15 minutes, proving that data standardization can replace in-person inspections. Brazil’s DUIMP grades risk at the time of lodgment and routes compliant shipments to immediate delivery. Ecuador’s Palantir-backed AI flags under-invoicing in real time, boosting 2025 customs revenue by 15.24%. Adoption of such tools drives a permanent migration toward API-native workflows inside the South America customs brokerage market[2]Inter-American Development Bank, “CADENA Blockchain for Trade,” iadb.org .

Near-Shoring of Supply Chains into South America

Cosco’s direct China-South America EV loop trims transit by a week and supports OEM inventory models that rely on rapid clearance. DP World and Maersk are spending USD 410 million to raise Santos' capacity to 2.1 million TEU, with on-terminal brokerage offices accelerating inbound component flows. Colombia forecasts 9.1% agro-industry export growth in 2026, adding phytosanitary-certificate demand that brokers monetize. Long-run factory relocations expand the South America customs brokerage market as component trade intensifies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex & Frequently Changing Tariff Schema | -0.5% | Argentina, Brazil | Short term (≤ 2 years) |

| High Logistics Costs & Port Congestion | -0.6% | Argentina, Brazil, Chile | Short term (≤ 2 years) |

| Patchy Digital-Signature Laws Across Countries | -0.3% | Ecuador, Bolivia, Paraguay | Medium term (2-4 years) |

| Aging Certified-Broker Talent Pool | -0.2% | Argentina, Chile, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex & Frequently Changing Tariff Schema

Argentina adjusted Common External Tariff exceptions 14 times in two years, forcing brokers to monitor gazettes daily. Brazil’s dual-VAT rollout runs to 2033, so declarations must calculate legacy and new levies in parallel. Colombia will replace criminal sanctions with administrative fines in 2026, increasing audit volume. Frequent rule changes add cost and slow the South America customs brokerage market growth by deterring smaller entrants.

High Logistics Costs & Port Congestion

Argentine port fees can be 500% above peers, lifting landed costs for importers. Santos operates near 90% capacity, causing two-day dwell times for non-priority cargo. While Chile added nine X-ray scanners in 2025, Valparaiso still experiences truck queues that complicate just-in-time clearances. Elevated logistics expenses compress brokerage fee budgets and marginally restrain the South America customs brokerage market[3]CIRA, “Port Cost Benchmark Report 2025,” cira.org.ar .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Air Express Rises as E-Commerce Scales

Air express and general cargo will post a 5.46% CAGR through 2031, even though ocean freight controlled 47.33% of the South America customs brokerage market share in 2025. Small parcels propel the modal shift under the USD 50 Remessa Conforme ceiling and by vaccine consignments that demand 2-to-8 °C chains of custody. IATA’s ONE Record adoption hit 22% in 2025, allowing brokers to auto-populate declarations from airline data feeds.

Ocean and sea lanes remain vital for grains, chemicals, and automotive knockdown kits, yet importers increasingly negotiate all-in contracts that bundle freight, insurance, and clearance. Truck and rail flows on trans-Andean corridors use TIR carnets that suspend duties until arrival, a service niche for brokers fluent in land-border inspection rules. As digital-first filing systems mature, the South America customs brokerage market size tied to air express should keep widening.

By Broker Type: Integrated 3PLs Versus Niche Specialists

Freight forwarders and 3PL-integrated operators captured 60.67% of the South America customs brokerage market share because enterprise shippers value a single liability point. On-dock brokerage suites in Santos and Buenos Aires shorten door-to-door cycles and encourage “vendor-managed clearance” contracts. However, pure customs brokers are forecast to grow at 4.88% CAGR by offering audit defense, drawback recovery, and classification advice under Mercosur automotive rules.

Traditional relationship capital with inspectors still matters for yellow-channel cargo, but API-driven entrants now match that advantage by hiring ex-officials and overlaying real-time tariff databases. The South America customs brokerage market, therefore, splits between scale-based service bundles and high-skill advisory retainers.

By Importer Size: SME Momentum on Simplified Thresholds

Large enterprises controlled 40.9% of the South America customs brokerage market in 2025, yet SME declarations will register a 6.09% CAGR to 2031. Colombia’s USD 5,000 fast-lane and Brazil’s flat-rate duties on parcels up to USD 50 let micro-shippers bypass full procedures, expanding the filing universe. Mid-market firms importing components for near-shored assembly increasingly engage brokers for AEO-lite consulting packages that cost USD 5,000-15,000.

Enterprises still dominate high-risk areas such as pharmaceuticals requiring Anvisa clearance. That segment’s complexity ensures that the South America customs brokerage market size rooted in enterprise accounts will not erode quickly, even while SME volumes accelerate.

By Digital Adoption: APIs Accelerate Double-Digit Growth

Traditional brokers retained 62.24% share in 2025, but API-native counterparts are on an 11.82% CAGR trajectory through 2031. The Mercosur digital-signature accord removes apostille obligations among the four nations, rewarding brokers that integrate directly with single-window endpoints in DUIMP, SICEX, and VUCE. Chile’s Smartflux blockchain shrank release time to 15 minutes, setting a new customer-service benchmark.

Legacy brokers still secure sensitive cargo where regulator rapport matters more than speed, yet automation gaps are closing. As Peru compels every agency to join VUCE by 2026, lagging firms must adopt APIs or exit. Consequently, digital adoption is the clearest structural growth lever inside the South America customs brokerage market.

By End-Use Industry: Automotive and EV Outpace Retail

Retail and e-commerce delivered 26.5% of 2025 revenue thanks to parcel programs, but automotive and EV requirements drive the fastest growth at 7.01% CAGR. Cosco’s expedited EV service and Mercedes-Benz’s eActros 600 arrival illustrate OEM trust in customs predictability for lithium batteries. Brokers manage Mercosur’s 60% local-content rule, dangerous-goods codes, and temporary-import bonds for tooling.

Electronics assemblers in Manaus need ANATEL homologation before release, while pharma importers comply with Anvisa RDC 977/2025 digital licenses. Each vertical sustains specialist brokerage niches, expanding the overall opportunity set for the South America customs brokerage market.

Geography Analysis

Brazil remained the anchor, holding 47.11% of the 2025 value. Remessa Conforme’s flat-rate tax covers 67% of parcels, and DUIMP’s instant risk score channels compliant cargo to immediate release. The USD 410 million Santos expansion raises capacity to 2.1 million TEU, while Complementary Laws 214/2025 and 227/2026 guarantee Manaus incentives beyond 2070. Parallel tax systems during Brazil’s VAT transition add advisory demand that lifts the South America customs brokerage market.

Colombia is the fastest climber with a 6.04% CAGR forecast. DIAN aims to cut contraband to 1% of GDP by 2026 and supports Puerto Antioquia’s new terminal. Simplified thresholds reduce brokerage touch-points on low-value parcels but expand filing volumes overall. Belt and Road cargo commitments for coffee and bananas add phytosanitary-certificate work, anchoring market expansion.

Argentina, Chile, Peru, Ecuador, and the rest share the remaining. Argentina’s AFC PLUS cuts clearance to 12-48 hours, but port charges remain the region’s highest, dampening throughput. Chile’s Hermes traceability and nine new scanners improve flow through Valparaíso and San Antonio, pushing more shippers to electronic certificates. Peru’s VUCE consolidation promises USD 432 million in annual savings, and Ecuador’s Palantir AI raised customs revenue 15.24% in 2025. Smaller economies such as Bolivia leverage VUCE to slash wait times from months to days, signaling untapped upside for the South America customs brokerage market[4]Planalto, “Complementary Law 227/2026,” planalto.gov.br.

Competitive Landscape

The South America customs brokerage market remains moderately fragmented. Multinational forwarders DHL, DSV, Kuehne + Nagel, CEVA, Maersk, UPS bundle clearance inside door-to-door contracts and own roughly 60% of revenue. They differentiate through API connections to DUIMP, SICEX, VUCE, and CADENA blockchains, offering real-time landed-cost calculators and compliance dashboards.

Regional specialists such as Grupo RAS and Allink Transportes supply high-touch counsel on classified pharmaceuticals or Mercosur automotive parts. Pure brokers defend margins by focusing on post-clearance audit defense and drawback claims that require forensic accounting rather than physical assets. Digital-first entrants leverage cloud tariff engines, ex-inspector hires, and subscription pricing to court SMEs.

Technology is the main battleground. CADENA’s ledger verifies sanitary permits, Chile’s Smartflux shrinks release windows, and Ecuador’s Palantir engine flags anomalies within minutes. Legacy brokers rely on decades-long ties with inspectors, but quarterly tariff revisions erode those moats when API feeds surface the same data publicly. Competitive intensity will rise as carbon-emissions reporting and geolocation tracing create new advisory niches while commoditizing document lodgment.

South America Customs Brokerage Industry Leaders

DHL Global Forwarding

Kuehne + Nagel

DSV

UPS

Expeditors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AGP Aduanas launched the Hermes GPS-and-RFID container traceability system in Chile, cutting demurrage disputes at Valparaiso and San Antonio ports.

- February 2026: DSV continued its acquisition-led consolidation strategy across Latin America forwarding and customs brokerage networks. It also expanded its operational footprint in Mexico–Brazil corridors to strengthen regional logistics integration.

- January 2026: UPS Supply Chain Solutions enhanced its global freight visibility tools as part of its 2026 logistics upgrades. It also improved customs transparency across Latin American trade lanes through upgraded digital tracking systems.

- April 2025: Kuehne + Nagel strengthened its South America airfreight corridors across Chile, Peru, and Brazil in response to rising Asia–LATAM trade demand. It expanded capacity and network connectivity in the region throughout 2025

South America Customs Brokerage Market Report Scope

| Ocean / Sea |

| Air (Express and General Cargo) |

| Cross-Border Land (Truck and Rail) |

| Pure Customs Broker |

| Freight Forwarder / 3PL-Integrated Brokers |

| Large Enterprisess |

| Mid-Market |

| SMEs / Micro-shippers |

| Traditional Brokerages |

| Digital-first / API-based Brokerages |

| Retail and E-commerce |

| Automotive and EV |

| Electronics and Semiconductors |

| Pharmaceuticals and Life Sciences |

| Aerospace and Defense |

| Chemicals and Industrial Goods |

| Others |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Mode of Transport (Value) | Ocean / Sea |

| Air (Express and General Cargo) | |

| Cross-Border Land (Truck and Rail) | |

| By Broker Type | Pure Customs Broker |

| Freight Forwarder / 3PL-Integrated Brokers | |

| By Importer Size | Large Enterprisess |

| Mid-Market | |

| SMEs / Micro-shippers | |

| By Digital Adoption | Traditional Brokerages |

| Digital-first / API-based Brokerages | |

| By End-Use Industry | Retail and E-commerce |

| Automotive and EV | |

| Electronics and Semiconductors | |

| Pharmaceuticals and Life Sciences | |

| Aerospace and Defense | |

| Chemicals and Industrial Goods | |

| Others | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How fast is customs clearance for e-commerce parcels in Brazil now?

Thanks to the Remessa Conforme program, parcels under USD 50 clear in a few minutes once duties are prepaid, with 67% of inbound volumes already using the scheme.

Which transport mode is growing quickest?

Air express brokerage volumes are on a 5.46% CAGR path to 2031 as small parcels and cold-chain drugs prefer 72-hour delivery windows.

Why is Colombia viewed as the fastest-growing country?

DIAN’s simplified thresholds and new Puerto Antioquia terminal, plus a goal to halve contraband by 2026, lift brokerage demand at a 6.04% CAGR.

What digital tools are reshaping brokerage work?

Platforms like Brazil’s DUIMP, Chile’s Smartflux blockchain, and Mercosur’s e-signature accord let API-ready brokers file and release cargo within minutes.

Where do pure customs brokers still win?

They retain an advantage in complex verticals such as pharmaceuticals needing Anvisa clearance and duty-drawback claims that require detailed cost tracing.

What is driving growth in the South America customs brokerage market?

Growth is driven by rising e-commerce shipments, digital customs systems, and increased near-shoring, which boost trade volumes and speed up clearance processes.

Page last updated on: