South America Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

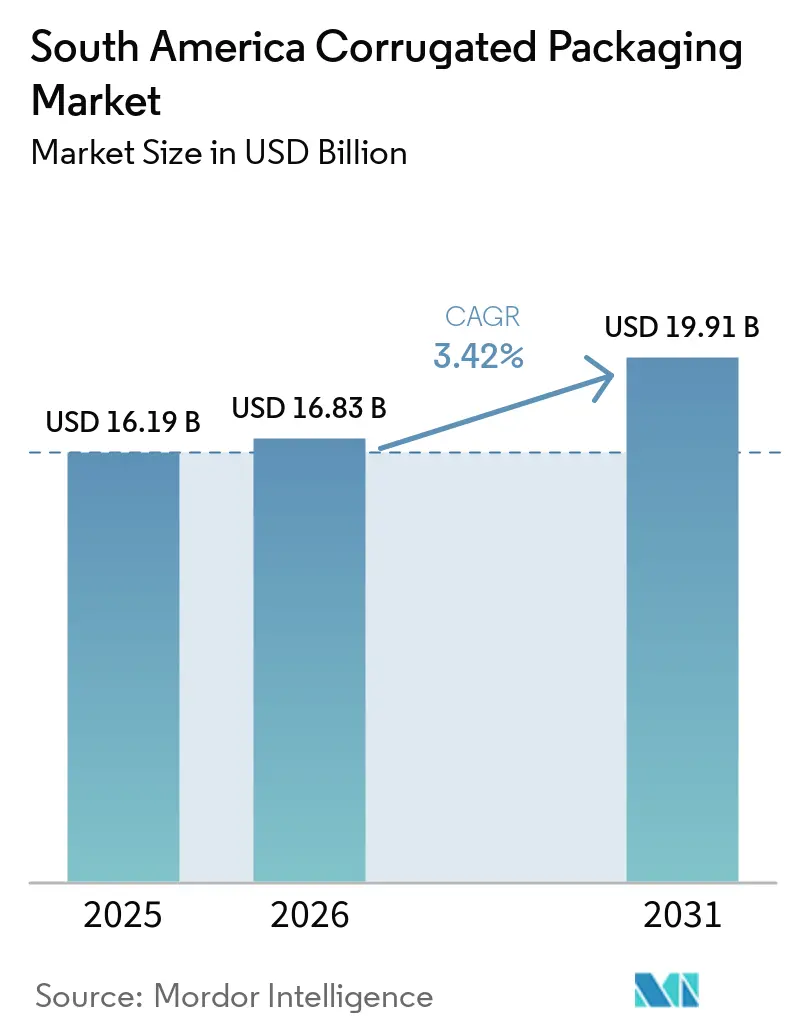

| Base Year Market Size (2025) | USD 16.19 Billion |

| Market Size (2026) | USD 16.83 Billion |

| Market Size (2031) | USD 19.91 Billion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Corrugated Packaging Market Analysis by Mordor Intelligence

The South America corrugated packaging market size is expected to increase from USD 16.19 billion in 2025 to USD 16.83 billion in 2026 and reach USD 19.91 billion by 2031, growing at a CAGR of 3.42% over 2026-2031. Rising export-quality mandates, the fast expansion of e-commerce fulfillment corridors, and a decisive shift toward virgin kraft linerboard are transforming substrate choices and cost structures throughout the region. Larger integrated converters are funding micro-flute equipment that shrinks dimensional-weight fees and unlocks stronger stacking performance, while produce exporters lock in higher-grade packaging that endures 35-day sea voyages. Recovered-paper price swings and port congestion temper short-term margins, yet balanced capacity additions in Brazil and Peru keep supply in line with the South America corrugated boxes market demand trajectory. Multinational producers are pursuing vertical integration and sustainability-linked financing, signaling a capital cycle focused on efficiency retrofits rather than green-field mills.

Key Report Takeaways

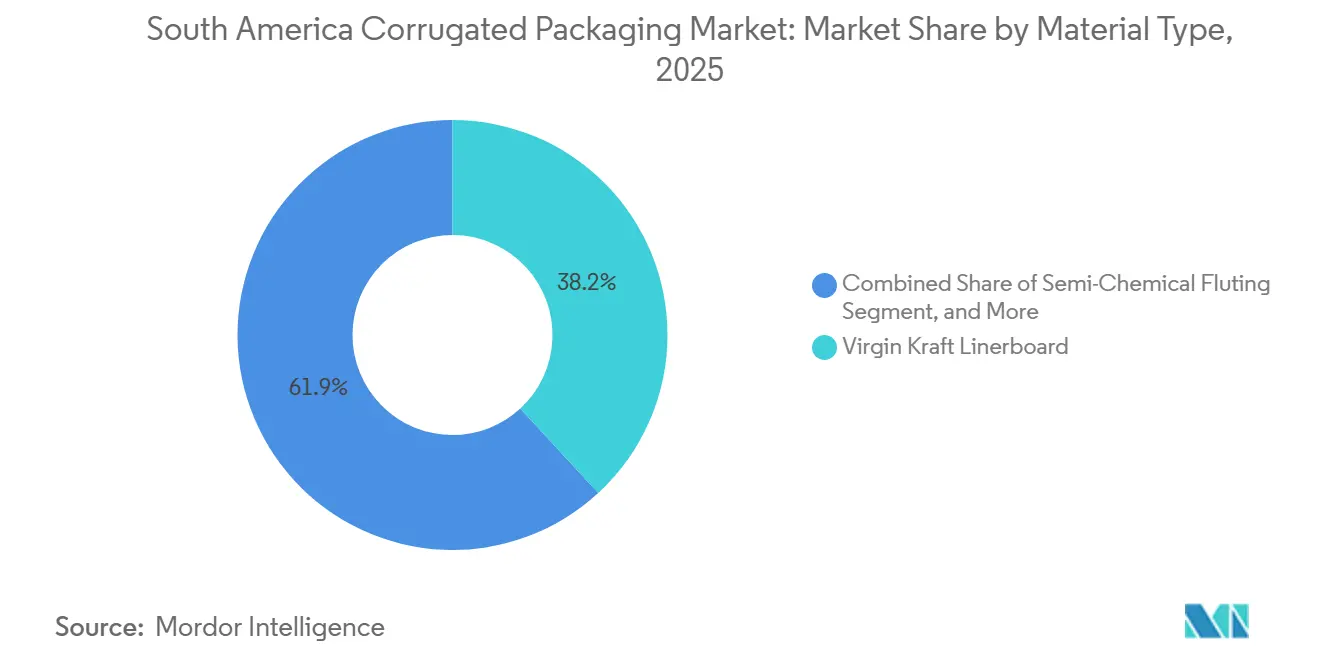

- By material type, the virgin kraft linerboard segment captured 38.15% of the South America corrugated packaging market share in 2025.

- By flute type, the South America corrugated packaging market size for f flute is projected to grow at an 5.23% CAGR through 2031.

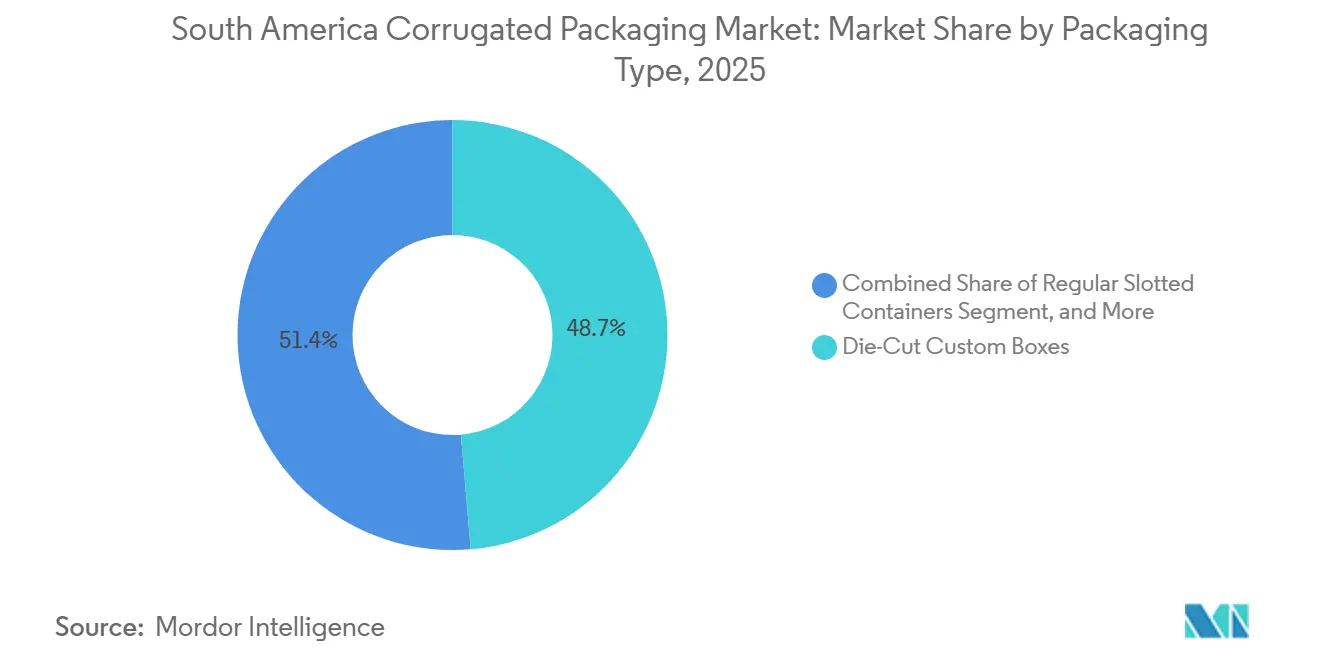

- By packaging type, the die-cut custom boxes segment captured 48.65% of the South America corrugated packaging market share in 2025.

- By wall type, the South America corrugated packaging market size for double-wall is projected to grow at an 5.56% CAGR through 2031.

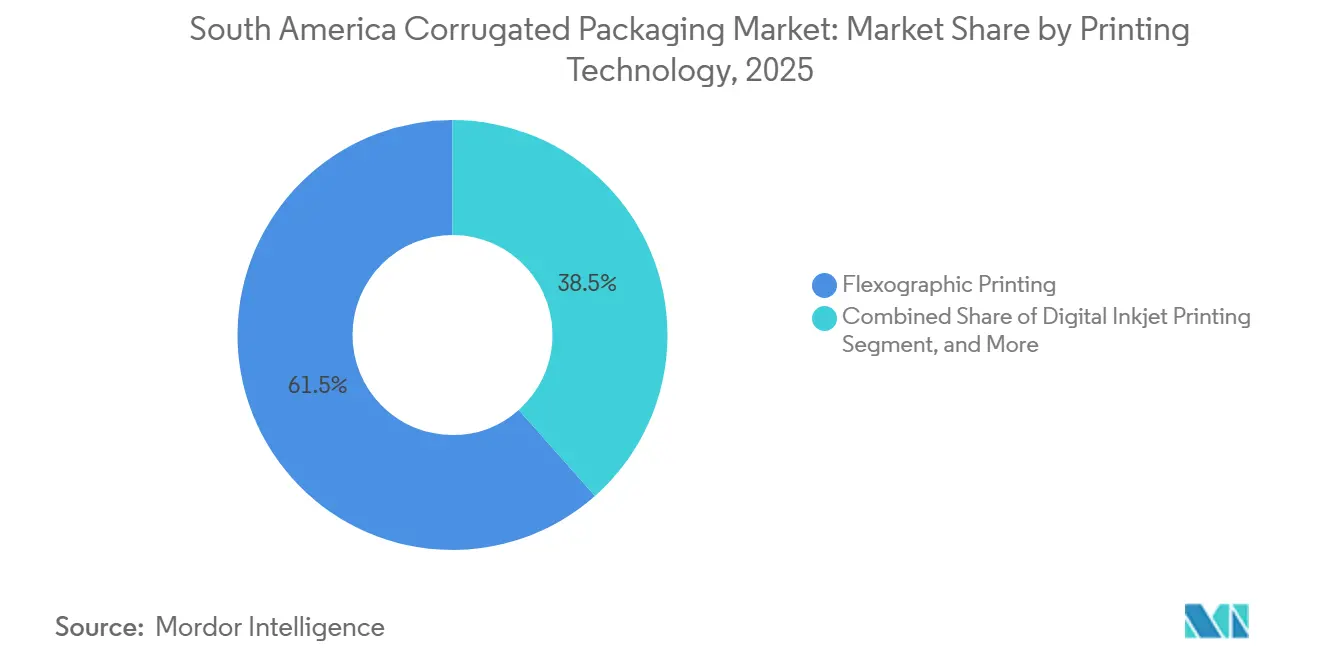

- By printing technology, the flexographic printing segment captured 61.53% of the South America corrugated packaging market share in 2025.

- By end-user industry, the South America corrugated packaging market size for electrical products is projected to grow at an 5.68% CAGR through 2031.

- By geography, the Brazil segment captured 52.37% of the South America corrugated packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Expansion Accelerating Corrugated Demand | +1.2% | Brazil, Argentina, Chile, Colombia | Medium term (2-4 years) |

| Shift Toward Lightweighting for Logistics Cost Savings | +0.8% | Brazil, Chile, Peru | Short term (≤ 2 years) |

| Growth of Fresh Produce Exports Requiring Ventilated Boxes | +0.9% | Chile, Peru, Brazil | Medium term (2-4 years) |

| Increasing Adoption of Digital Printing for Short Runs | +0.6% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Resurgence of Near-shoring Manufacturing in South America | +0.7% | Brazil, Argentina, Mexico spillover | Long term (≥ 4 years) |

| Sustainability-Linked Financing Boosting Green Packaging Capex | +0.5% | Brazil, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Expansion Accelerating Corrugated Demand

Online retail in Brazil generated 1.2 million tons of packaging in 2023, marking a 22% year-on-year jump that directly lifted the South America corrugated boxes market. Fulfillment centers increasingly favor modular 300 mm × 200 mm × 150 mm regular slotted containers that glide through automated sorters, cutting void-fill material and operator touches. Colombia’s e-commerce sector posted 15% growth in 2024, adding steady corrugated volume around the distribution hubs of Bogotá and Medellín. Cross-border marketplaces that ship Argentine orders from Brazilian inventories extend the same packaging standards across Mercosur lanes, embedding structural demand into the South America corrugated boxes market. Implementation across secondary cities should accelerate over the next two to three years as last-mile infrastructure matures.

Shift Toward Lightweighting for Logistics Cost Savings

Regional freight carriers enforce dimensional-weight tariffs that penalize bulky packaging, prompting shippers to move from single-wall B flute at 450 g m-² to double-wall E flute or F flute at 380 gm-², slashing airfreight bills by as much as 18%. Chilean cherry exporters cut per-unit mass 12% during the 2024-2025 season after adopting F flute cartons, while pallet cube efficiency improved 8%. Peruvian avocado shippers employed ventilated E flute boxes that meet ISPM 15 pallet protocols and maintain airflow across 35-day transits, further boosting the South America corrugated boxes market profile. Upgrading to micro-flute corrugators requires capital expenditure exceeding USD 15 million, creating an adoption gap between major converters and smaller regional plants. Nonetheless, high aviation fuel surcharges keep the payback period short for firms operating large airfreight programs.

Growth of Fresh Produce Exports Requiring Ventilated Boxes

Chile recorded USD 3.091 billion in cherry exports during 2024, a 50.6% increase that translated into millions of ventilated cartons of 5 kg and 2 kg.[1]Circlepack Chile, “Chile rompe récord de exportación de cerezas,” circlepack-chile.com Peru’s non-traditional farm exports jumped 14.4%, led by avocado shipments climbing 35.1% and mangoes up 41.8%. Modified-atmosphere liners inserted inside corrugated boxes add 7 to 10 extra shelf-life days, safeguarding quality during lengthy voyages and anchoring a new revenue stream in the South America corrugated boxes market. Brazil’s coffee exporters now specify triple-wall corrugated for 60 kg cargoes to comply with European food-contact codes. Because growers fix packaging specifications 12-18 months before harvest, demand remains consistently locked in, buffering converters from broader economic swings.

Increasing Adoption of Digital Printing for Short Runs

Digital inkjet commanded 38.47% of corrugated print volume in 2025, yet is scaling fastest at 5.78% CAGR through 2031. Colombian converter Papelsa introduced inline heads that embed QR codes and graphics, reducing customer lead times from 14 days to 48 hours. Smurfit WestRock installed HP PageWide T1195i presses across its Brazilian plants, achieving 305 m min-¹ and reducing pre-print inventory burdens. The transformation lowers minimum order quantities to 500-unit runs, inviting brand owners to pilot localized SKUs and deepening the South America corrugated boxes market. Although a digital press needs around two years to amortize, rising SKU fragmentation keeps investment cases compelling for large integrated mills.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recovered Paper Prices | -0.9% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Intensifying Competition from Flexible Packaging Formats | -0.6% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Capital Intensity of High-Speed Corrugators | -0.4% | Regional, focused in Brazil and Chile | Long term (≥ 4 years) |

| Port Congestion Disrupting Containerboard Supply | -0.5% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Recovered Paper Prices

Brazilian old-corrugated-container prices spiked 90% year-on-year in October 2024, elevating recycled linerboard costs 24.6% and compressing converter margins by roughly 400 basis points. Argentina’s supply tightened sharply when Celulosa Argentina closed in September 2025, stripping 120,000 tons of domestic capacity and lifting import prices 17% above regional benchmarks. While integrated mills hedge volatility through captive collection networks, independent plants remain exposed until price cycles normalize inside 18 months, affecting profitability across the South America corrugated boxes market. Industry consolidation could accelerate if margin stress repeats in future peaks.

Intensifying Competition from Flexible Packaging Formats

Stand-up pouches deliver 40-50% mass savings compared with corrugated boxes, gaining share in snacks, pet food, and liquid concentrates. Brazil’s pet-food category, which expanded 9% in 2024, now favors flexible formats that offer single-serve convenience, trimming the need for corrugated secondary packs. Colombia’s Green Tax regime unexpectedly accelerates the use of multilayer film by levying lower fees on flexible formats than on rigid plastics, while corrugated remains tax-exempt but loses differentiation. Flexible encroachment unfolds over 24-36 months as supply chains redesign case counts, but export logistics and e-commerce still depend on stacking strength, preserving the South America corrugated boxes market core volume. Converters are therefore diversifying into pouch lines alongside box capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Virgin Kraft Linerboard Gains on Export Quality Mandates

Virgin kraft linerboard captured 38.15% share in 2025, and its 5.62% CAGR implies enduring preference among exporters that ship cherries, avocados, and roasted coffee to distant buyers. The South America corrugated boxes market for virgin grades is expanding as importers inspect cartons for water absorption and crush resistance after five weeks at sea. Recycled linerboard remains essential for local distribution, yet recovered-paper volatility that drove 90% price swings in late 2024 pressures converters that lack captive collection networks. Specialty coatings, including water-repellent barriers for salmon exports, are gaining traction as converters chase higher-margin niches aligned with sustainability goals.

Klabin’s Piracicaba II plant, inaugurated in April 2026, adds 300,000 tons of recycled board and anchors domestic supply security. Exporters tolerate 12-15% higher unit costs for virgin substrates to avoid USD 50,000 rejection claims at destination ports, reinforcing the premium’s economic logic within the South America corrugated boxes market. ANVISA and MAPA rules on food-contact migration further align specifications with certified virgin kraft, simplifying compliance for meat, coffee, and fresh-produce shippers while signaling a steady shift in material mix through 2031.[2]ANVISA, “Embalagens para alimentos,” gov.br/anvisa

By Flute Type: Micro-Flutes Reshape E-Commerce Economics

B flute accounted for 34.63% of shipments in 2025, remaining the historical workhorse for balanced stacking strength and cushioning. However, the F flute’s predicted 5.23% CAGR highlights a migration to slimmer walls that cut dimensional weight fees and maximize pallet cube, especially in rapidly scaling fulfillment centers. Switching from single-wall B flute at 450 g m-² to a B-E double-wall at 380 g m-² reduces airfreight charges up to 18%, a saving that resonates across the South America corrugated boxes market.

C flute remains vital for appliance packaging where load capacities exceed 1,000 psi, while A flute maintains a low share due to its cube inefficiency. Colombian converter Papelsa retooled corrugators to produce B and E flute combos, giving agro-export customers vented designs that protect blueberries and grapes during long-haul transport. F flute’s sub-1.5 mm height also unlocks offset-like graphics, attracting cosmetics and electronics brands that help diversify revenue streams inside the South America corrugated boxes market.

By Packaging Type: Regular Slotted Containers Gain E-Commerce Momentum

Die-cut custom boxes led with a 48.65% share in 2025, but regular slotted containers are expected to expand 5.45% per year, as fulfillment nodes crave cartons that auto-erect on high-speed tapers and nest efficiently on mixed-SKU pallets. A standard 300 mm × 200 mm × 150 mm footprint saves up to 25% compared to custom die-cutting, once tooling and setup labor are factored in, a delta increasingly material in grocery-led e-commerce waves.

Folding cartons address shelf-ready cosmetics and small electronics, where print vibrancy justifies 30-40% cost premiums. Pallet boxes made with triple-wall board are encroaching on bulk coffee and soy exports by phasing out jute sacks to comply with European food-contact regulations. In-store displays and octagonal bins remain niche but are climbing steadily as Brazilian supermarkets chase impulse-end cap sales, keeping the South America corrugated boxes market diversified across value tiers.

By Wall Type: Double-Wall Gains on Export Durability Needs

Single-wall cartons supplied 45.17% of 2025 demand, yet double-wall variants will grow 5.56% annually because they deliver 40% greater stacking strength while adding only 22% board weight. Peruvian avocado exporters reduced damage claims by 18% after switching to double-wall, vented designs, proving that upfront packaging premiums recoup quickly through lower rejection fees.

Triple-wall, though with a share below 10%, is gaining traction in heavy-duty machinery and bulk chemical drums where pallet loads exceed 2 metric tons. Brazilian coffee exporters already apply triple-wall to 60 kg roasted-bean consignments to satisfy EU labeling rules, reinforcing multi-wall economics in select lanes. Single-face sheets remain restricted to void-fill, signaling minimal cannibalization risk to box volumes inside the South America corrugated boxes market.

By Printing Technology: Digital Inkjet Disrupts Short-Run Economics

Flexographic presses held a 61.53% share in 2025, yet digital inkjet, rising 5.78% annually, is quickly eroding that dominance by eliminating costly plates and enabling sub-2,000-unit runs. Smurfit Westrock’s HP PageWide lines hit 305 m min-¹ and furnish serialized QR codes that tie into brand loyalty apps, a functionality impossible on legacy presses. Additionally, the growing demand for customization and shorter turnaround times is further driving the adoption of digital inkjet technology.

Litho-lamination retains prestige packs for perfumes and premium spirits, but screen printing now survives mainly in Argentina and Peru, where converters cannot justify USD 2 million presses. UV-curable ink systems add moisture-barrier value for aquaculture cartons stocked on iced docks, illustrating niche persistence. As SKU proliferation continues across the South America corrugated boxes market, digital inkjet’s agility will cement its role as converters’ go-to technology for quick-turn campaigns.

By End-User Industry: Electrical Products Surge on Nearshoring

Fresh food and produce commanded 43.56% of the 2025 value, and its volume base still underpins corrugator utilization across Brazil, Peru, and Chile, where seasonality locks in predictable quarterly peaks. Electrical products, however, are set to grow at a 5.68% CAGR, as newly commissioned automotive and electronics plants in Brazil create incremental dunnage demand that favors double- and triple-wall cartons over expendable wood. Processed foods remain a resilient second pillar, but snack foods and pet food are increasingly adopting flexible pouches, diverting some corrugated secondary cases, particularly in urban supermarkets where shelf efficiency dominates merchandising strategy.

The South America corrugated boxes market linked to e-commerce fulfillment centers is comparatively small today, accounting for under 12% of 2025 tonnage, yet it is advancing at double-digit rates as online grocery penetration deepens beyond tier-one cities and regional couriers refine last-mile coverage. Beverages deploy corrugated trays and shrink film bundles, although certain can lines migrate straight to palletized wrap configurations, marginally diluting box volumes. Pharmaceuticals and personal-care brands pay 40-50% premiums for litho-laminated or digital F flute packs that deliver print vibrancy, tamper evidence, and temperature insulation in the cold chain, lifting value share faster than raw tonnage. Industrial chemicals, building materials, and assorted heavy goods round out the residual share, underscoring that diversified downstream exposure cushions converters from category-specific shocks and keeps overall growth on a stable, mid-single-digit trajectory through 2031.

Geography Analysis

Brazil generated 52.37% of 2025 revenue and produced 6.1 million tons of corrugated, underpinned by 85% recycled content that secures local fiber balance. Klabin’s Piracicaba II project, online since April 2026, injects substantial recycled board into São Paulo and Rio logistics corridors and reduces dependence on containerboard imports. Smurfit Westrock invested BRL 205 million (USD 41 million) to install HP digital presses and expand corrugator speeds, cementing Brazil’s role as the technology leader in the South America corrugated boxes market. Yet Santos port ran at full capacity during 2024 with only 23% on-schedule departures, inflating inventory costs and complicating supply reliability for boxmakers awaiting linerboard deliveries.[3]S and P Global, “Santo's port congestion Brazil 2024,” spglobal.com

Peru leads in growth with a 6.15% CAGR projected through 2031, fueled by non-traditional farm exports rising 14.4% and concentrated in avocados, blueberries, and grapes. Mining equipment packaging supplements food volume, requiring double- and triple-wall cartons that withstand vibration and humidity across Andes-to-Pacific routes. Chile posted a USD 3.091 billion cherry export record in 2024 that absorbed ventilated cartons, while CMPC’s USD 250 million green bond unlocks Guaíba II pulp capacity to back virgin kraft supply. These developments reinforce Andean producers’ importance inside the South America corrugated boxes market supply chain.

Argentina’s 12% production contraction in 2023 and Celulosa Argentina’s 2025 bankruptcy created a 120,000-ton supply gap, lifting hardwood pulp imports from Uruguay by 17% and squeezing converters’ margins. Colombia’s 15% e-commerce growth encourages corrugated adoption, bolstered by tax incentives that penalize single-use plastics yet favor fiber packs. Ecuador’s banana exporters and Uruguay’s beef shippers drive localized demand, but limited mill capacity prevents these countries from challenging Brazilian dominance in the South America corrugated boxes market. Regional capacity remains geographically uneven, preserving entry barriers for new players in smaller economies.

Competitive Landscape

The South America corrugated boxes market displays moderate concentration, with the top five multinationals accounting for roughly 55-60% of installed capacity, leaving meaningful room for agile regionals. Smurfit Westrock’s 2025 merger with DS Smith created a trans-Atlantic heavyweight targeting USD 400 million savings by 2027 through mill optimization and cross-selling design platforms.[4]Smurfit Westrock, “Investor Relations 2025,” smurfitkappa.com Klabin’s Piracicaba II and ongoing Puma II expansions collectively add nearly 800,000 tons of linerboard, strengthening the firm’s domestic grip and exporting flexibility. International Paper redirected USD 1.5 billion from its cellulose fibers divestiture into higher-margin containerboard assets in Brazil and Chile, raising competitive intensity across premium virgin grades.

Regional independents such as Cartones América, Papelsa, and Carvajal Empaques chase niche export contracts, leveraging micro-flute versatility and digital printing lead times under 48 hours. Papelsa’s Barbosa facility, now equipped with inline inkjet heads, closed a 200-basis-point margin gap versus multinationals and widened service coverage throughout the Andean corridor. CMPC and Arauco both secured over USD 2.2 billion in sustainability financing, channeling funds into bleached eucalyptus kraft pulp that feeds virgin kraft linerboard streams and aligns with global decarbonization mandates. Such funding spreads best-in-class environmental metrics across the South America corrugated boxes market, pressuring peers to follow suit or risk procurement exclusion.

White-space opportunities center on micro-corrugated cold-chain inserts and molded-pulp salmon trays that outperform legacy slotted boxes on insulation and moisture resistance. Integrated players deploy HP PageWide presses that reach 305 m min-¹, shrinking SKU launch cycles to days, while late adopters still rely on manual die-cutting and screen printing. Regulatory hurdles such as ANVISA food-contact migration tests and SENASA ISPM 15 protocols favor firms with in-house labs, effectively raising entry barriers. Ultimately, scale, technology adoption, and captive fiber remain the decisive levers that differentiate winners inside the South America corrugated boxes market.

South America Corrugated Packaging Industry Leaders

Smurfit Westrock plc

International Paper Company

Mondi plc

Klabin S.A.

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Klabin inaugurated the Piracicaba II recycled containerboard unit, adding 300,000 tons capacity that targets e-commerce and food shippers.

- February 2026: Smurfit Westrock presented a medium-term plan that aims for USD 400 million in annual synergies from its DS Smith merger by 2027.

- January 2026: International Paper completed a USD 1.5 billion cellulose fibers divestiture and reallocated proceeds to containerboard lines in Brazil and Chile.

- December 2025: Smurfit Westrock invested BRL 205 million (USD 41 million) to upgrade Brazilian corrugators and install HP PageWide T1195i digital systems.

South America Corrugated Packaging Market Report Scope

The South America Corrugated Packaging Market encompasses the production, distribution, and utilization of corrugated packaging solutions across various industries in the region. Corrugated packaging, made from corrugated fiberboard, is widely used for its durability, lightweight nature, and recyclability. This market includes applications in sectors such as food and beverage, pharmaceuticals, electronics, e-commerce, and others, catering to the growing demand for sustainable and efficient packaging solutions.

The South America Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries), and Geography (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America corrugated boxes market in 2026?

The market is valued at USD 16.83 billion in 2026 and is forecast to reach USD 19.91 billion by 2031.

Which material segment is expanding fastest?

Virgin kraft linerboard is advancing at a 5.62% CAGR as exporters demand higher crush resistance, according to Mordor Intelligence.

Why are micro-flute profiles becoming popular?

F flute and E flute reduce dimensional-weight costs while retaining stacking strength, a key benefit for e-commerce shipments.

Which country will grow the quickest through 2031?

Peru is projected to lead with a 6.15% CAGR, driven by booming fresh-produce and mining-equipment exports.

What printing method is disrupting flexography?

Digital inkjet presses eliminate plate costs and cut lead times to 48 hours, growing at a 5.78% CAGR per Mordor Intelligence.

How do port bottlenecks influence supply?

Congestion at Santos port raises inventory costs and delays imports, although new long-term leases aim to unlock additional capacity.

Page last updated on: