South America Contract Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

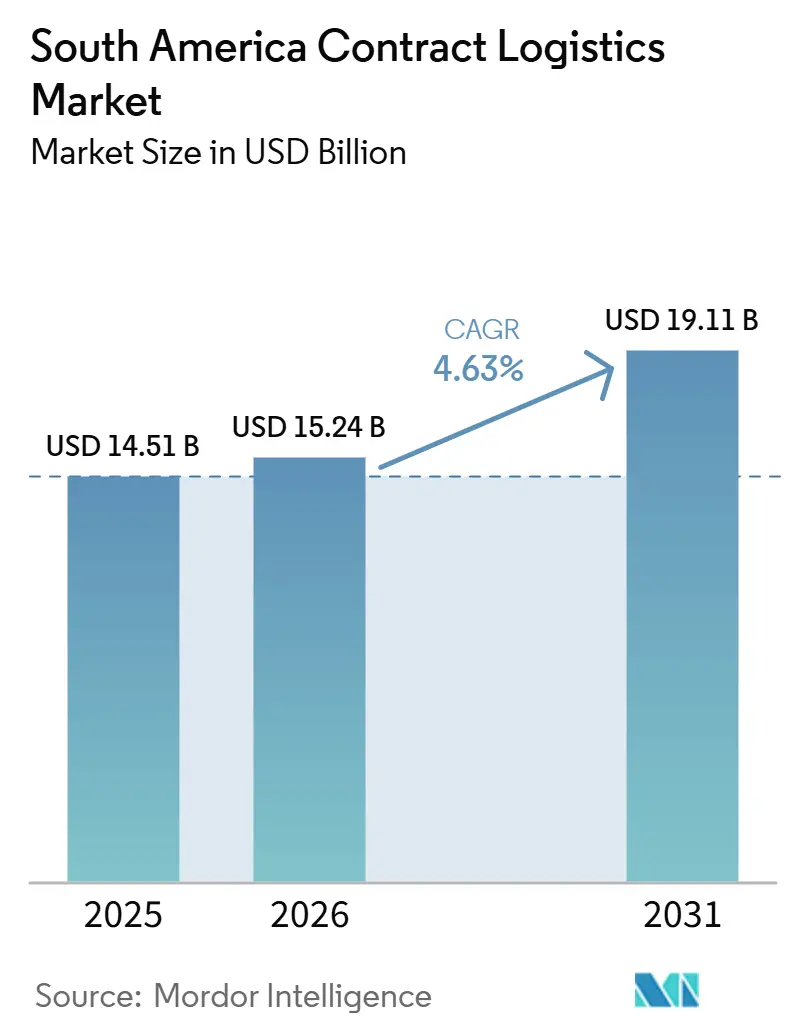

| Base Year Market Size (2025) | USD 14.51 Billion |

| Market Size (2026) | USD 15.24 Billion |

| Market Size (2031) | USD 19.11 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

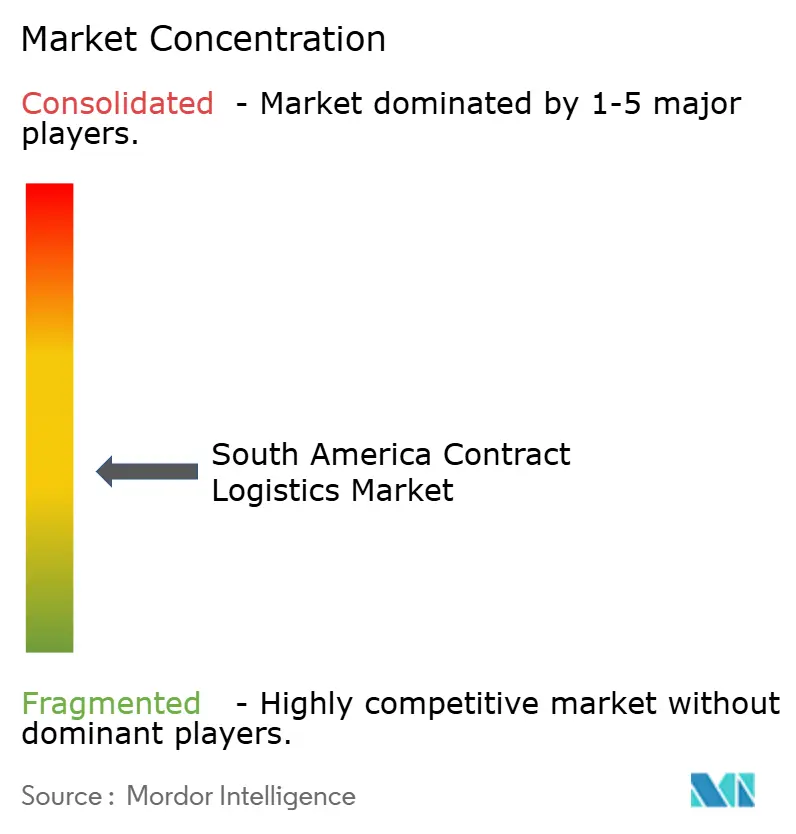

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Contract Logistics Market Analysis by Mordor Intelligence

The South America contract logistics market size was valued at USD 14.51 billion in 2025 and estimated to grow from USD 15.24 billion in 2026 to reach USD 19.11 billion by 2031, at a CAGR of 4.63% during the forecast period (2026-2031).

E-commerce fulfillment, near-shoring of automotive assembly, and cold-chain mandates are reshaping service portfolios, while multiyear, dollar-denominated contracts hedge currency swings and underpin the rapid build-out of high-throughput, technology-enabled distribution centers. Brazilian platform operators turned logistics into a competitive moat through owned infrastructure, and their investment signals are echoed across Colombia, Peru, and Chile, where new deep-water ports and cold stores are already attracting value-added services. Competitive intensity is elevating as global integrators collide with domestic specialists that command dense last-mile networks, forcing margin protection through automation, fleet electrification, and micro-fulfillment expansion. Headline challenges remain: congested ports, manual customs regimes, and a widening shortage of warehouse labor add friction costs that can erode the region’s cost advantage, yet infrastructure programs, tariff reductions under the EU-Mercosur accord, and strong consumer demand continue to offset these risks.

Key Report Takeaways

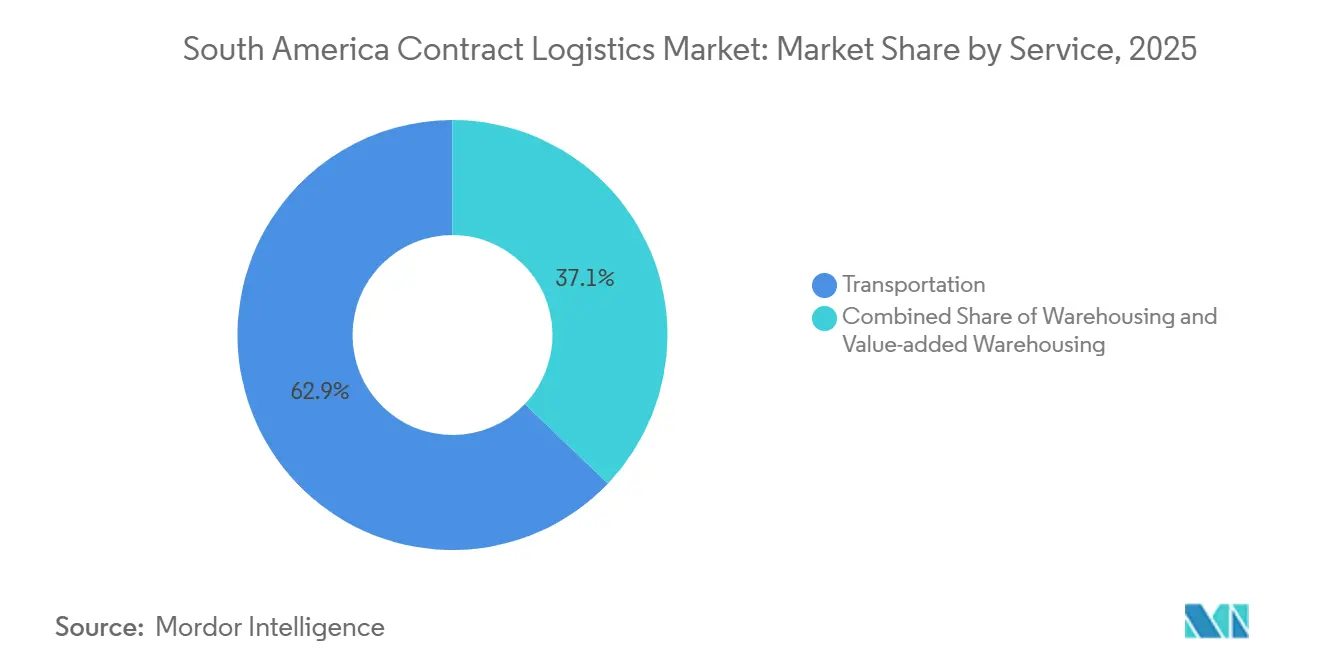

- By service, transportation services led with 62.87% of the South America contract logistics market share in 2025, value-added services are projected to expand at a 6.18% CAGR through 2031, the fastest pace of any service line.

- By contract duration, contracts exceeding three years held 57% of the South America contract logistics market size in 2025 and are advancing at a 5.64% CAGR to 2031.

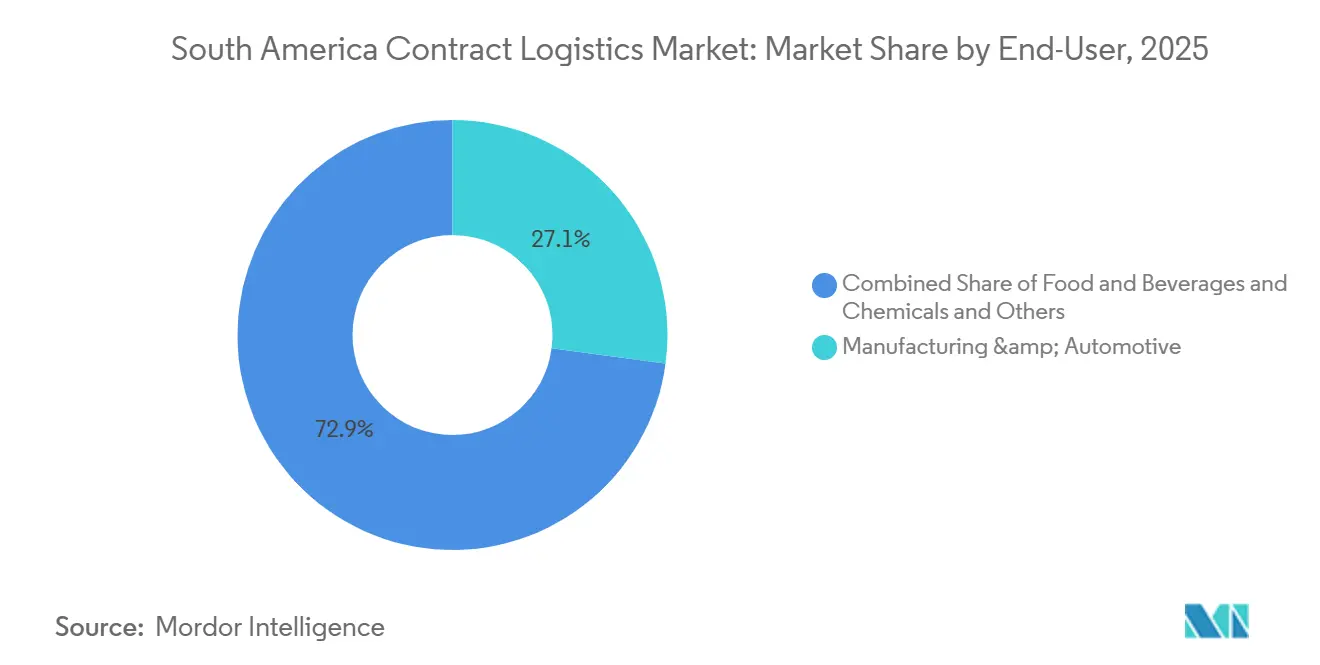

- By end-user, manufacturing and automotive captured 27.11% of 2025 demand, while healthcare and pharmaceuticals are forecast to post a 6.33% CAGR to 2031.

- By country, Brazil accounted for 48.21% of the South America contract logistics market size in 2025, whereas Colombia is expected to record the highest national CAGR at 6.09% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and same or next-day fulfillment demand | +1.2% | Brazil, Argentina, Chile, and Colombia urban corridors | Short term (≤ 2 years) |

| Automotive production and export growth | +0.9% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Infrastructure modernization programs | +0.7% | Chile, Peru, Brazil | Long term (≥ 4 years) |

| Near-shoring of North American and EU supply chains | +0.8% | Brazil, Colombia | Medium term (2-4 years) |

| Cold-chain needs for agrifood and vaccines | +0.6% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Pay-as-you-go 3PL micro-fulfillment in secondary cities | +0.4% | Argentina, Brazil, Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom and Same- or Next-Day Fulfillment Demand

Platform operators converted logistics from a variable cost into a fixed asset because fulfillment speed now dictates share in corridors that host 60% of regional e-commerce volume. Mercado Libre doubled Brazilian distribution centers to 21 by 2025, adding 880,000 square meters and securing same-day delivery in Sao Paulo, Rio de Janeiro, and Belo Horizonte. Shopee followed by opening a 220,000-square-meter Sao Paulo warehouse in March 2026, cutting order-to-dispatch time below 12 hours. Amazon’s 67,000-square-meter Brasília fulfillment center, built by CEVA in eleven weeks, processes 135,000 packages daily. Argentina already delivers 30% of online orders within 24 hours, pushing inventory closer to Cordoba and Rosario. Reverse-logistics flows in Brazil earn 8-12% incremental margin for providers who inspect, repackage, and relist imports that face a combined 77% tax burden[1]Shopee Brazil, “Press Room,” shopee.com.br.

Automotive Production and Export Growth

Near-shoring mitigates U.S.-China tensions and ensures compliance with strict USMCA content rules. BYD’s Camaçari plant reached 150,000 units in 2025 and, following a USD 1.06 billion investment, will double output by the end of 2026, requiring dedicated sequencing centers within 30 minutes of the production line. Great Wall Motors is constructing a USD 20 billion complex, while Nissan invested USD 540 million to add a second shift in Resende, enabling twelve daily milk-run circuits. Rising EV tariffs in Brazil, set to reach 35% by July 2026, are accelerating local assembly and increasing the premium for battery-module installation, software flashing, and compliance labeling. Mexico’s 3.95 million-unit output serves as a benchmark that regional governments aim to emulate.

Infrastructure Modernization Programs

Chilean, Peruvian, and Brazilian port and river upgrades add capacity and slash dwell times. The USD 4.45 billion San Antonio expansion boosts throughput to 2 million TEU and cuts dwell to under two days. Peru’s Chancay deep-water terminal shortens Shanghai transit by 13 days and handled 450,000 TEU in its first year. Brazil is deepening the Paraguay River channel to 3.5 meters, trimming soybean transport costs by 18%.

Near-Shoring of North American and EU Supply Chains

Manufacturers relocate final assembly to secure duty benefits and lower Asia-Pacific exposure. Electronics brands increased requests for configuration and kitting services by 35% in 2025, converting imported components into Mercosur-compliant finished goods held in free-trade zones until customization. The EU-Mercosur accord, provisionally applied on 1 May 2026, removes more than 90% of tariffs on industrial goods, making South America a viable alternative to Eastern Europe for EU-bound exports.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Road and port infrastructure bottlenecks | −0.8% | Brazil, Chile, Argentina | Short term (≤ 2 years) |

| Complex cross-border customs and tax regimes | −0.5% | Mercosur, Andean crossings | Medium term (2-4 years) |

| FX-volatility risk to long-term 3PL contracts | −0.6% | Argentina, Brazil | Short term (≤ 2 years) |

| Skilled warehouse-labor shortages | −0.4% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Road and Port Infrastructure Bottlenecks

Santos moved 1.3 million TEU in 2025, yet still averages four to five-day dwell times, double that of Panama Canal peers, because the Tecon 10 project will only reach full capacity in 2040. Valparaíso relies on trucks for 85% of its Santiago-bound cargo, adding USD 150-200 per container and up to a full day of transit. Argentina’s network downgraded during its fiscal crisis, leaving 70% of highways below acceptable standards and inflating carrier maintenance costs by up to 20%.

Complex Cross-Border Customs and Tax Regimes

Manual declarations still cover 40% of Argentina-bound trucks, driving eight-to-twelve-hour waits at main crossings, four times longer than USMCA borders. While the EU-Mercosur accord cuts tariffs, its 5% safeguard trigger forces shippers to layer 10-15% contingencies into multi-year rate cards. Brazil’s Remessa Conforme Program cuts federal duty to 20% on parcels under USD 50, yet state ICMS rates vary, pushing sellers toward a 3-5% fee for third-party tax services[2]Central Bank of Brazil, “Monetary Policy,” bcb.gov.br .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates but Kitting Captures Margin

Transportation services accounted for 62.87% of the South America contract logistics market share in 2025, underlining the scale of a continent where 60% of cargo still moves by truck. Value-added services are poised for a 6.18% growth trajectory, benefiting from postponement strategies that cut inventory costs by up to 25%, and from new labeling mandates tied to recycled-content disclosure.

Road haulage should benefit from Argentina’s allowance of bitrenes, which lowers per-pallet costs by 12%. Rail remains limited at 15% of Brazil's freight share, though modernization of the Urquiza line could redirect up to two million tonnes from road to rail by 2028. Air freight centers on pharmaceuticals and perishables moving through Guarulhos, where shippers now pre-book apron-adjacent cold rooms. Sea freight growth aligns with DP World’s plan to raise Santos capacity to 1.7 million TEU by 2026, reflecting strong containerized flows tied to the South America contract logistics market.

By Contract Duration: Multiyear Deals Hedge Currency Risk

Contracts above 3 years dominate 57% of the South America contract logistics market share in 2025, and are advancing at a 5.64% CAGR to 2031, underscoring the South America contract logistics market preference for fixed-rate certainty when policy rates sit at or above double digits. Currency adjustment clauses indexed to United States PPI or local CPI shelter providers, yet 60-90 day lags still expose them to temporary margin compression.

Short-term contracts continue where demand is volatile. E-commerce platforms favor one-to-three-year terms that allow rapid rerouting, while Argentine peso instability keeps local shippers from committing beyond annual budgets. Automotive suppliers also lean short because model changes can shift volumes 30-40% in a single year.

By End-User Industry: Automotive Leads Share, Healthcare Leads Growth

Manufacturing and automotive took 27.11% of South America contract logistics market share in 2025 spend as BYD, Great Wall, and Nissan expand assembly footprints. Sequencing centers located within 30 minutes of the line manage inbound parts and outbound finished vehicles under just-in-time rules, and they sustain premium pricing inside the South America contract logistics market. Healthcare and pharmaceuticals will grow at 6.33% CAGR thanks to cold-chain compliance after Brazil’s vaccine losses and to new GDP-certified facilities across Colombia and Peru.

Retail and e-commerce remain a structural demand pillar. Mercado Libre’s USD 5.76 billion outlay doubled its national footprint by 2025, while Shopee’s São Paulo build moved inventory from eight third-party sites into a single high-throughput node. Food and beverage flows benefit from stricter temperature variance tolerances in Chile’s berry exports, and chemicals transport stays steady, anchored by petrochemical clusters that insist on ISO-accredited providers.

Geography Analysis

Brazil commanded 48.21% of 2025 spend inside the South America contract logistics market, supported by its 215 million consumers, diverse industry base, and platform-driven fulfillment expansion. Mercado Libre alone added 880,000 square meters and 21 distribution centers by 2025, achieving same-day coverage across its three largest metros. In 2025, JSL generated BRL 9.6 billion (USD 1.72 billion) in revenue and maintains 1.7 million square meters across 65 sites, providing last-mile density that challenges foreign entrants. Port congestion and labor shortages remain obstacles, but the EU-Mercosur tariff elimination enhances export competitiveness.

Colombia is forecast to grow 6.09% to 2031. Puerto Antioquia’s February 2026 opening reduced Medellín transit times by 47% and set the template for deeper Pacific access once the Uraba Megaport comes online. Emergent Cold’s Cartagena store and the USD 1.7 billion airport expansion accelerate pharmaceutical flows[3]Puerto Antioquia, “Operational Launch,” puertoantioquia.com.

Argentina improves as 82% of logistics firms invest in 2026, mainly into WMS and warehouse builds that leverage bitrenes' efficiency savings. Yet manual customs and peso swings temper growth. Chile benefits from the San Antonio expansion that cuts dwell time to under two days, and Peru’s Chancay terminal now offers a 10-day Shanghai route, lifting Pacific competitiveness. The rest of South America draws capital toward barge upgrades on the Paraguay River and transshipment expansion in Montevideo, both essential to the broader South America contract logistics market.

Competitive Landscape

The top five providers hold roughly 35-40% combined revenue, placing the South America contract logistics market in a moderately fragmented state. JSL’s BRL 9.6 billion (USD 1.72 billion) revenue, plus recent acquisitions of TPC and FSJ, consolidate automotive and pharmaceutical capacity, while its network of 65 sites gives it reach into secondary Brazilian cities. DHL pursues a hub-and-spoke model anchored by the new Jundiaí mega-hub and fleet electrification, targeting 30% volume growth by end-2026. CEVA aims for 620,000 square meters by 2028, supported by quick-build Amazon projects that showcase accelerated construction techniques[4]DHL Brazil, “Press Releases,” dhl.com.

Technology differentiators surge: Correo Argentino’s fully robotic hub processes 9,000 parcels per hour, trimming labor costs up to 50%, and iFlow adopted a cloud WMS that cut order cycle time 25%. Cold-chain specialists like Emergent Cold and Multilog leverage GDP compliance to maintain double-digit margins, while micro-fulfillment challengers capture SMEs through pay-as-you-go pricing in secondary cities.

South America Contract Logistics Industry Leaders

DHL Supply Chain

Kuehne + Nagel International AG

DSV A/S

UPS

Expeditors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: CEVA Logistics announced to open a 20,000 m² Iveco parts center in Pouso Alegre after a BRL 93 million (USD 18 million) investment.

- February 2026: Puerto Antioquia began operations, cutting Medellín transit 47% and handling post-Panamax vessels.

- February 2026: Maersk launched a 17,500 m² cold-chain hub in Olmos to extend produce shelf life by 14 days.

- December 2025: DHL Group partnered with Robust.AI to deploy Carter™ collaborative robots, establishing an automation model for the wider Latin American region. DHL Group is expected to extend these capabilities into South America to improve warehouse efficiency and strengthen its contract logistics operations.

South America Contract Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing & Distribution | |

| Value-added Services (Assembly, Labelling, Kitting) |

| 1-3 Years |

| Above 3 years |

| Manufacturing and Automotive |

| Food and Beverage |

| Retail and E-commerce |

| Healthcare and Pharmaceuticals |

| Chemicals |

| Other Industries |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing & Distribution | ||

| Value-added Services (Assembly, Labelling, Kitting) | ||

| By Contract Duration | 1-3 Years | |

| Above 3 years | ||

| By End-user Industry | Manufacturing and Automotive | |

| Food and Beverage | ||

| Retail and E-commerce | ||

| Healthcare and Pharmaceuticals | ||

| Chemicals | ||

| Other Industries | ||

| By Country | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America |

Key Questions Answered in the Report

How large will South American contract logistics spending be by 2031?

The South America contract logistics market is projected to reach USD 19.11 billion by 2031, up from USD 15.24 billion in 2026.

Which service line grows fastest?

Value-added services, led by kitting and labeling, are forecast to grow at a 6.18% CAGR over 2026-2031.

Why are multiyear logistics contracts common in Brazil?

Shippers favor contracts longer than three years because fixed dollar-denominated rates hedge local currency volatility and high policy interest rates.

Which country shows the highest growth potential?

Colombia is expected to post a 6.09% CAGR to 2031, lifted by new port capacity at Puerto Antioquia and other infrastructure upgrades.

What limits market growth in the near term?

Port congestion, manual customs processes, exchange-rate swings, and skilled labor shortages collectively subtract up to 0.8 percentage points from forecast CAGR.

How are providers addressing last-mile speed?

Operators invest in micro-fulfillment centers inside secondary cities, deploy autonomous mobile robots, and electrify vehicle fleets to accelerate urban delivery.

Page last updated on: