South America Consumer Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

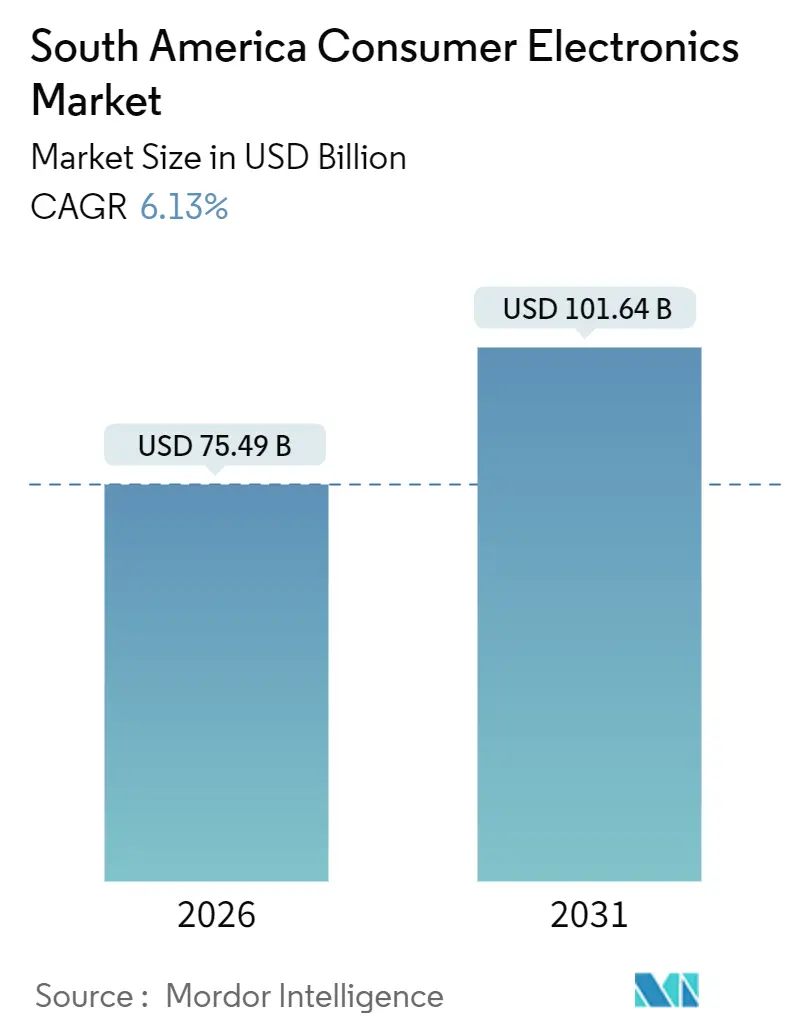

| Market Size (2026) | USD 75.49 Billion |

| Market Size (2031) | USD 101.64 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Consumer Electronics Market Analysis by Mordor Intelligence

The South America consumer electronics market size stands at USD 75.49 billion in 2026 and is projected to reach USD 101.64 billion by 2031, registering a 6.13% CAGR over the forecast period. Digitally enabled payment rails, local manufacturing incentives, and 5G expansion are converting pent-up demand into real transactions, while gray-market volumes keep shrinking as regulators tighten product certification requirements. Brazil’s PIX real-time payment network has already shifted high-ticket purchases away from costly credit cards, and the Manaus Free Trade Zone’s duty exemptions are turning the region from a pure import destination into a credible production base. Ecommerce platforms are compressing delivery times to less than 24 hours for two-thirds of Brazilians, amplifying competitive pressure on legacy store-only chains. At the same time, millennials and Generation Z buyers allocate a larger share of their discretionary income to electronics, stimulating cross-category upgrades from connectivity devices to health-oriented wearables and energy-efficient appliances.

Key Report Takeaways

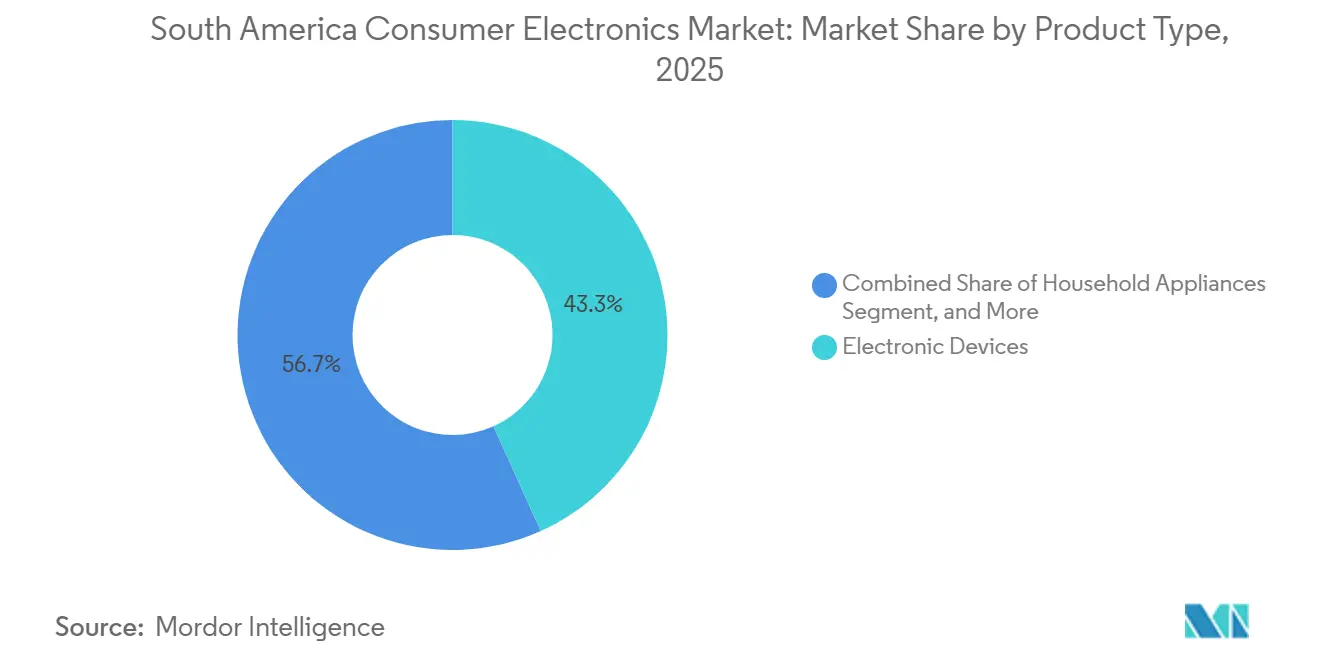

- By product type, electronic devices led with 43.26% of the South America consumer electronics market share in 2025 and are projected to grow at a 6.73% CAGR through 2031.

- By price range, the budget tier captured 48.32% share in 2025; the premium tier is advancing at a 6.79% CAGR to 2031.

- By connectivity, smart devices commanded a 67.17% share in 2025; the segment is forecast to expand at a 6.54% CAGR through 2031.

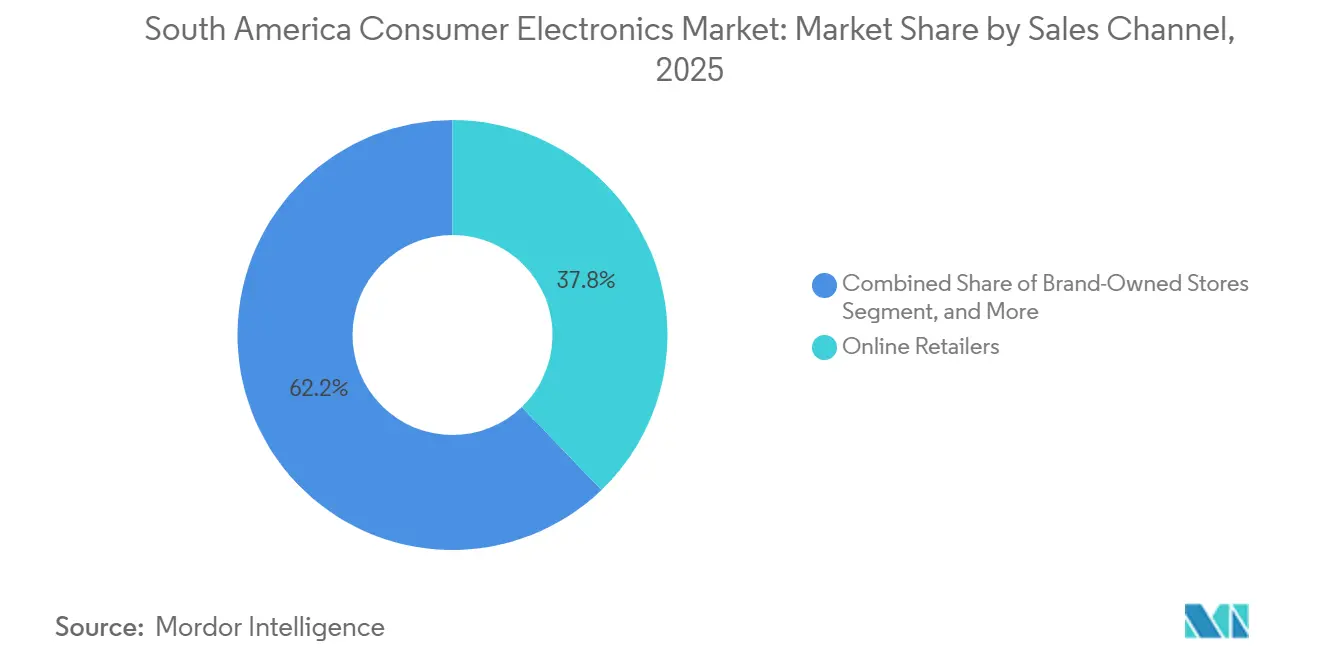

- By sales channel, online retailers accounted for 37.82% of the South America consumer electronics market share in 2025 and hold the highest projected CAGR of 7.19% through 2031.

- By end-user age group, millennials held a 42.79% of the South America consumer electronics market share in 2025; Generation Z recorded the fastest CAGR at 6.91% over the same period.

- By geography, Brazil led with a 53.38% revenue share in 2025; Colombia is expected to post the fastest growth at a 6.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Consumer Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased access to the internet | +0.9% | Brazil, Colombia, Argentina, Rest of region | Medium term (2-4 years) |

| Growing inclination towards smart devices | +1.1% | Brazil, Colombia, spillover to Argentina | Long term (≥ 4 years) |

| Expanding ecommerce and omnichannel retail | +1.3% | Brazil, Colombia, Argentina | Short term (≤ 2 years) |

| Rising disposable income of the middle class | +0.8% | Colombia, Brazilian urban hubs, Rest of region | Long term (≥ 4 years) |

| PIX instant payments boosting affordability | +1.0% | Brazil (national) | Short term (≤ 2 years) |

| Manaus Free Trade Zone incentives | +0.7% | Brazil (Manaus) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased Access to the Internet

Brazil ended 2024 with 181 million internet users, translating into 84% penetration, while Colombia reached 73% and Argentina 88%.[1]International Telecommunication Union, “Measuring Digital Development 2025,” itu.int Fiber accounts for 77.7% of Brazil’s 52.6 million fixed-broadband connections, enabling low-latency 4K streaming and cloud gaming, which stimulate demand for large-screen TVs and higher-spec smartphones. Satellite services such as Starlink added 372,000 Brazilian subscribers during 2024, bypassing legacy copper in rural areas and lifting average connected-device ownership to 4.2 units per broadband household. Monthly mobile data usage jumped to 18.3 GB per user in 2024, favoring devices with advanced displays and larger batteries. As always-on connectivity broadens, multi-device ecosystems deepen, and replacement cycles accelerate, driving cross-selling of peripherals and sustaining value growth for the South America consumer electronics market.

Growing Inclination Towards Smart Devices

Smart connected products already account for over two-thirds of regional spending and will keep outpacing traditional appliances as consumers seek remote control, energy savings, and voice-assistant integration. Brazil’s 5G smartphone base surpassed 40 million units in 2024 and will top 60 million by end-2025.[2]Anatel, “Telecommunication Indicators 2024,” anatel.gov.br Compliance with ETSI EN 303 645 security standards and Brazil’s LGPD privacy law raises the bar for firmware support, widening the gap between certified brands and gray-market imports. Established vendors, notably Samsung, LG, and Xiaomi, capitalize on in-country service footprints to reassure buyers, turning cybersecurity into a purchase criterion rather than a hurdle. The continued tilt toward smart devices underpins the medium-term expansion of the South America consumer electronics market.

Expanding Ecommerce and Omnichannel Retail

Online retailers accounted for 37.82% of regional electronics sales in 2025 and are on track for a 7.19% CAGR through 2031 as they expand same-day delivery coverage and add augmented-reality product views. Mercado Libre invested BRL 34 billion (USD 6.8 billion) in Brazilian logistics in 2025, doubling the number of fulfillment centers to 21 and reducing delivery times to below 24 hours for 68% of households.[3]Mercado Libre, “Q3 2025 Earnings Release,” investor.mercadolibre.com Amazon Brazil answered by waiving seller fees for the category, intensifying price competition. Black Friday 2025 web sales reached BRL 33.6 billion (USD 6.7 billion), up 35.5% year-on-year, with electronics contributing 22% of turnover. Omnichannel chains like Magazine Luiza merge showroom experiences with digital inventory, meeting the tactile needs of high-ticket appliance buyers while reducing real estate costs. Faster fulfillment and broader assortment collectively enlarge the total addressable base for the South America consumer electronics market.

Rising Disposable Income of the Middle Class

Colombia’s GDP per capita climbed to USD 7,240 in 2024, and Brazil’s middle class expanded to 104 million people, forming a consumer segment with headroom for non-essential electronics. Urban centers such as São Paulo, Rio de Janeiro, and Bogotá, where wages in finance and technology outpace national averages, account for 48% of premium purchases. Millennials and Gen Z allocate 18% of their discretionary outlays to electronics, compared with 12% for Gen X, underscoring sales of gaming consoles, soundbars, and robotic vacuums. Although Argentina’s purchasing power remains fragile, stabilization measures that lowered monthly inflation to single digits by mid-2025 may unlock deferred replacement cycles. Rising urban incomes, therefore, give the South America consumer electronics market a steady lift, even if gains remain uneven across countries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security concerns related to smart devices | -0.4% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Macroeconomic volatility and devaluation | -0.9% | Argentina, Brazil, Colombia | Short term (≤ 2 years) |

| Grey-market and parallel imports | -0.5% | Brazil, Argentina, Rest of region | Short term (≤ 2 years) |

| Rising energy tariffs | -0.3% | Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Security Concerns Related to Smart Devices

High-profile breaches and inconsistent enforcement of Brazil’s LGPD privacy law keep some households from using internet-connected appliances. Only 14 penalties were issued against electronics vendors between 2021 and 2024, limiting deterrence. While Anatel’s 2024 cybersecurity seal mandates encrypted firmware updates and the removal of default passwords, audits still cover fewer than one-third of models on sale. Surveys show that 41% of Brazilian households skip buying smart cameras or locks due to privacy concerns. Brands that invest in local education campaigns and transparent data dashboards, such as Samsung’s Knox or LG’s ThinQ, capture a disproportionate slice of security-minded buyers, but pervasive skepticism nonetheless clips the near-term upside for the South America consumer electronics market.

Macroeconomic Volatility and Currency Devaluation

Argentina’s peso plunged 54% against the dollar in 2024, pushing inflation to 211% and collapsing electronics demand by 28% year over year. Although monthly inflation slowed to single digits by mid-2025, real wages remain 15% below 2022 levels, delaying discretionary purchases. Brazil’s real oscillated between 4.85 and 5.40 per USD during 2024-2025, prompting retailers to revise prices weekly, while Colombia’s peso weakened 8%, inflating landed costs. Premium devices priced in USD, especially Apple and Sony flagships, saw sticker increases of up to 22% between 2023 and 2025. Consequently, macro swings remain the single largest drag on the near-term trajectory of the South America consumer electronics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smartphones Dominate, Wearables Surge

In 2025, electronic devices commanded a leading 43.26% share of the revenue pie and are set to expand at a 6.73% CAGR, continuing through 2031. Tablets, desktop PCs, and laptops together accounted for 18% of sales, with volumes tied to public-sector laptop programs that create sporadic spikes in demand. Televisions accounted for 12% of value, with 4K and OLED models gaining ground as streaming subscriptions reached 74% of broadband homes. Gaming consoles remained niche at 3% because high import duties keep headline prices elevated.

Brazil’s smartwatch shipments climbed 37% in 2024, with Apple Watch and Samsung Galaxy Watch controlling 62% of unit sales despite competition from Xiaomi’s sub-BRL 300 (USD 60) Mi Band line. Household appliances, refrigerators, washing machines, dishwashers, and vacuum cleaners collectively supplied 24% of 2025 turnover, anchored by air conditioners that are growing 6.8% CAGR, as only 22.6% of Brazilian homes own cooling equipment. Personal audio gear, such as earbuds and soundbars, accounted for 9% of spending, buoyed by falling entry-level prices that now dip below BRL 150 (USD 30).

By Price Range: Budget Leads, Premium Accelerates

The budget tier accounted for 48.32% of the South America consumer electronics market in 2025, reflecting a region where 62% of households earn less than USD 1,000 per month and shop for core functionality. Mid-range products represented 31% of revenue, balancing specification depth and affordability with popular lines such as Samsung Galaxy A and Motorola Moto G assembled in Manaus to skirt import tariffs.

Premium devices are advancing at a 6.79% CAGR to 2031 as affluent consumers upgrade to foldable screens, OLED televisions, and AI-powered cameras that command 40-60% price premiums. Apple’s Vision Pro launch at BRL 29,999 (USD 6,000) drew 8,000 preorders in Brazil, underscoring the resilience of high-income spending even amid macro volatility. Chinese challengers compress mid-range margins by cascading flagship features downward, forcing incumbents to accelerate trickle-down of technology, while gray-market pressure fades as Anatel tightens EAN-code enforcement.

By Connectivity: Smart Devices Outpace Traditional

Smart connected products accounted for 67.17% of 2025 revenue and are forecast to expand at a 6.54% CAGR through 2031, outstripping legacy devices as 5G coverage reaches towns of more than 30,000 people in Brazil. Always-on broadband is steering households toward connected ecosystems that enable voice control, energy monitoring, and remote diagnostics.

Traditional non-smart models retain a 32.83% share but are contracting 1.2% annually, concentrated in rural areas with limited broadband and among older buyers who see little value in connectivity. Voice-assistant platforms, including Alexa, Google Home, and HomeKit, are now present in 12% of Brazilian households, clustering in cities where fiber penetration exceeds 85%. Security certification under ETSI EN 303 645 and LGPD compliance raise barriers for uncertified imports, shifting incremental demand to established brands that offer over-the-air firmware updates.

By Sales Channel: Online Retailers Advance

Online outlets delivered 37.82% of 2025 turnover, the highest for any channel, and are expected to grow at a 7.19% CAGR as Mercado Libre and Amazon shave delivery windows below 24 hours for two-thirds of Brazilians. Black Friday 2025 web sales surged 35.5% year over year to BRL 33.6 billion (USD 6.7 billion), with electronics accounting for 22% of receipts.

Omnichannel chains such as Magazine Luiza and Via hold a 28% share, blending showroom touchpoints with digital inventory to satisfy appliance shoppers who value in-person evaluation. Brand-owned stores contribute 16% and focus on curated experiences that lift accessory attach rates, while multi-brand physical outlets, at 14%, continue a gradual decline as rent escalates and foot traffic migrates online. Direct sales, corporate procurement, and other channels account for the remaining 4%.

By End-User Age Group: Millennials Anchor Demand, Gen Z Gains

Millennials accounted for 42.79% of 2025 spending, at peak earning age and forming new households that buy across categories, from smartphones to washing machines. Generation X followed with 24%, heavily skewed toward replacement purchases and brand loyalty in traditional appliances.

Generation Z shows the fastest growth rate at a 6.91% CAGR as social commerce and influencer marketing convert scrolls into sales, particularly for wearables and personal audio. Baby boomers, representing 11% of demand, gravitate toward large displays and simplified user interfaces but are shrinking 1.8% annually as fixed incomes and lower tech adoption restrain upgrades. PIX installment functionality, launched in September 2025, disproportionately benefits younger cohorts who avoid credit card interest, further amplifying Gen Z’s future contributions.

Geography Analysis

Brazil accounted for 53.38% of South America's consumer electronics market in 2025, anchored by its 215 million population, 84% internet penetration, and the fiscal benefits of the Manaus Free Trade Zone, which lured USD 1.2 billion in 2024 electronics investment. Nationwide, the 5G rollout now covers towns with populations as low as 30,000, boosting advanced-device adoption and enabling cloud gaming and smart-home use cases.

Colombia, though smaller, is the fastest riser, with a 6.96% CAGR through 2031, propelled by digital-banking penetration reaching 73% of adults in 2024 and GDP per capita gains that enlarge the middle-income bracket. Fiscal stability and broadband subsidies also nurture ecommerce adoption beyond Bogotá, spreading demand into mid-tier cities like Medellín and Cali.

Argentina retains an 18% share but remains hostage to currency swings. Inflation fell to single digits by mid-2025, yet real wages remain depressed, delaying discretionary replacement cycles. Should macro stability persist through 2026, pent-up demand could trigger a rebound in a market where smartphone lifespans already exceed 3 years.

The remaining countries, Chile, Peru, Ecuador, Uruguay, and Paraguay, collectively account for 22% of revenue. Chile leads in per-capita consumption owing to higher household income and tariff concessions that temper retail prices. Smartphone penetration there reaches 92%, and Apple claims a 38% share of the premium tier, the highest anywhere in Latin America.

Competitive Landscape

Competition in the South America consumer electronics market is moderate, with the top five brands, Samsung, LG, Apple, Xiaomi, and Motorola capturing 48% of 2025 revenue. Chinese entrants leverage Manaus production to sidestep import duties and underprice incumbents. Xiaomi already controls up to 17% of Brazil’s smartphone market, while Honor, Vivo, and Oppo collectively opened 2,000 outlets between 2024 and 2025. Samsung and LG retain loyalty via ecosystem stickiness. SmartThings and ThinQ link phones, TVs, and appliances, raising customer switching costs. Apple holds 38% of Chile’s smartphone rollouts and 22% of Brazil’s premium slice, leaning on iOS exclusivity and curated retail experiences.

Domestic challenger Positivo Tecnologia, Brazil’s largest PC assembler, is now venturing into smartphones and tablets priced 20-30% below imports, aiming at the education and public-sector markets. Anatel’s joint-liability rule for non-certified devices slashed gray-market smartphone volume from 19% in 2024 to 12% in 2025, shifting share to vendors that offer local warranty and after-sales support.

Strategically, leading players focus on AI as a differentiator. Samsung’s Galaxy AI suite brings on-device translation and smart photo editing, while LG embeds predictive maintenance into appliances. Such feature creep protects pricing power even as competition intensifies, sustaining profitability in the South America consumer electronics market.

South America Consumer Electronics Industry Leaders

Samsung Electronics

LG Electronics

Apple Inc.

HP Inc.

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Mercado Libre partnered with Casas Bahia to list the retailer’s inventory on its marketplace and use 700 stores for pickup and returns, enhancing omnichannel reach.

- September 2025: Brazil’s Central Bank enabled PIX installment payments, allowing consumers to split bills over 12 months at merchant fees below 2.5%, directly benefiting high-ticket electronics.

- June 2025: Vivo inaugurated a Manaus smartphone plant with 1.5 million-unit annual capacity, targeting budget and mid-range segments.

- June 2025: Huawei re-entered Brazil with Pura 70 phones and MatePad tablets in partnership with Mercado Libre and Magazine Luiza.

South America Consumer Electronics Market Report Scope

The South America Consumer Electronics Market Report is Segmented by Product Type (Electronic Devices, Household Appliances, Personal Audio and Accessories), Price Range (Premium, Mid-Range, Budget), Connectivity (Smart Connected, and Non-Smart/Traditional), Sales Channel (Online Retailers, Omni-channel Retailers, Brand-Owned Stores, Multi-brand Physical Stores, Others Sales Channel), End-User Age Group (Generation Z (10-25), Millennials (26-41), Generation X (42-57), Baby Boomers (Above 58)), and Country (Brazil, Argentina, Colombia, Rest of South America). Market Forecasts are Provided in Terms of Value (USD).

| Electronic Devices | Smartphones |

| Tablets | |

| Desktop PCs | |

| Laptops/Notebooks | |

| Television | |

| Gaming Consoles | |

| Wearables | |

| Other Electronic Devices | |

| Household Appliances | Refrigerators |

| Air Conditioners | |

| Washing Machines | |

| Dishwashers | |

| Vacuum Cleaners | |

| Other Household Appliances | |

| Personal Audio and Accessories | Headphones and Earbuds |

| Speakers and Soundbars | |

| Other Personal Audio and Accessories |

| Premium |

| Mid-Range |

| Budget |

| Smart Connected |

| Non-Smart/Traditional |

| Online Retailers |

| Omni-channel Retailers |

| Brand-Owned Stores |

| Multi-brand Physical Stores |

| Others Sales Channel |

| Generation Z (10-25) |

| Millennials (26-41) |

| Generation X (42-57) |

| Baby Boomers (Above 58) |

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Product Type | Electronic Devices | Smartphones |

| Tablets | ||

| Desktop PCs | ||

| Laptops/Notebooks | ||

| Television | ||

| Gaming Consoles | ||

| Wearables | ||

| Other Electronic Devices | ||

| Household Appliances | Refrigerators | |

| Air Conditioners | ||

| Washing Machines | ||

| Dishwashers | ||

| Vacuum Cleaners | ||

| Other Household Appliances | ||

| Personal Audio and Accessories | Headphones and Earbuds | |

| Speakers and Soundbars | ||

| Other Personal Audio and Accessories | ||

| By Price Range | Premium | |

| Mid-Range | ||

| Budget | ||

| By Connectivity | Smart Connected | |

| Non-Smart/Traditional | ||

| By Sales Channel | Online Retailers | |

| Omni-channel Retailers | ||

| Brand-Owned Stores | ||

| Multi-brand Physical Stores | ||

| Others Sales Channel | ||

| By End-User Age Group | Generation Z (10-25) | |

| Millennials (26-41) | ||

| Generation X (42-57) | ||

| Baby Boomers (Above 58) | ||

| By Country | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America consumer electronics market in 2026?

The market is valued at USD 75.49 billion in 2026 and is forecast to reach USD 101.64 billion by 2031 at a 6.13% CAGR.

Which product type sells the most units?

Smartphones dominate, supplying 43.26% of 2025 revenue as they are the main internet access device for 68% of households.

Why are wearables growing faster than other categories?

Health-monitoring features and falling entry prices drive a 6.73% CAGR for wearables through 2031, making them the fastest-expanding segment.

Which sales channel will grow quickest?

Online retailers post the highest forecast CAGR at 7.19% thanks to same-day delivery coverage and lower checkout friction.

What is the main challenge to growth?

Macroeconomic volatility, notably currency depreciation in Argentina and Brazil, can quickly erode consumer purchasing power and slow premium sales.

Which country offers the strongest upside?

Colombia carries the fastest projected CAGR at 6.96% through 2031, fueled by middle-class expansion and high digital-banking penetration.

Page last updated on: