South America Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

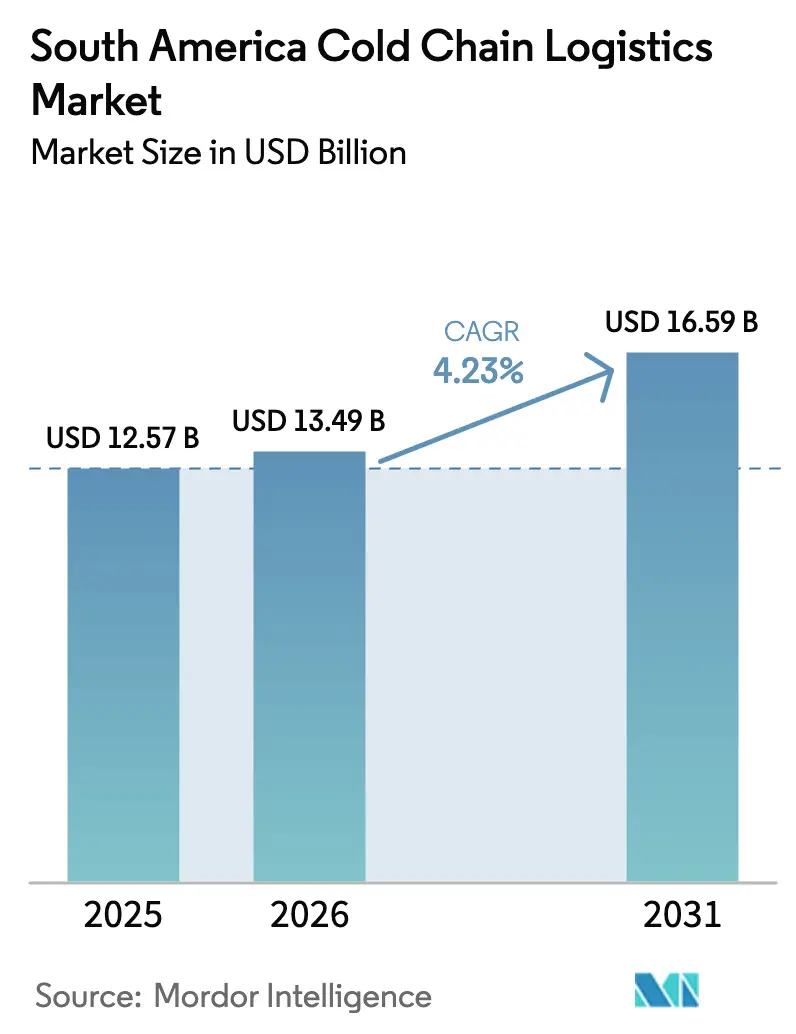

| Base Year Market Size (2025) | USD 12.57 Billion |

| Market Size (2026) | USD 13.49 Billion |

| Market Size (2031) | USD 16.59 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

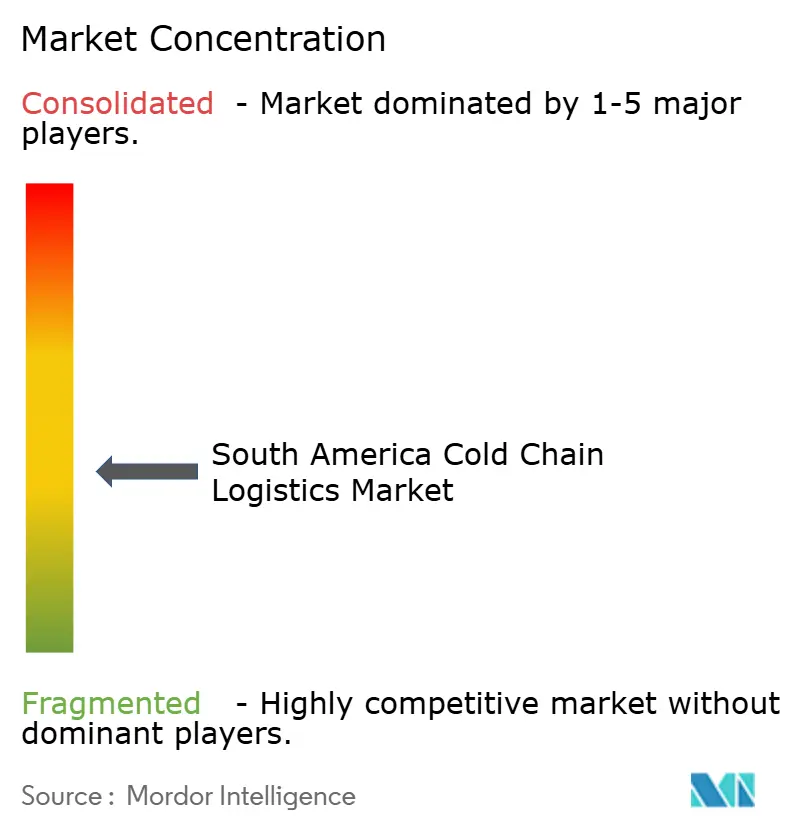

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Cold Chain Logistics Market Analysis by Mordor Intelligence

The South America cold chain logistics market size is projected to expand from USD 12.57 billion in 2025 and USD 13.49 billion in 2026 to USD 16.59 billion by 2031, registering a CAGR of 4.23% between 2026 to 2031.

The market is shifting from its historic role as a commodity-export conduit toward a temperature-controlled hub for biologics, e-grocery micro-fulfillment, and near-shored protein processing. The January 2026 EU-Mercosur interim trade agreement is spurring exporters to install traceability systems that satisfy deforestation-free sourcing rules, while ongoing vaccine-distribution upgrades have accelerated replacement of obsolete refrigeration equipment across multiple countries. Tight cold-storage vacancy in Tier-1 metros is redirecting investment to Tier-2 cities where land is cheaper, grid reliability is better, and first-mile distances are shorter. Rising adoption of natural refrigerants mandated by national Kigali Amendment regulations is lifting capital costs but lowering long-run energy spend, improving total cost of ownership, and bolstering sustainability credentials. Competitive intensity remains moderate as global incumbents buy regional specialists and retrofit assets with automation and IoT monitoring, yet domestic players still hold strong positions in niche high-touch segments.

Key Report Takeaways

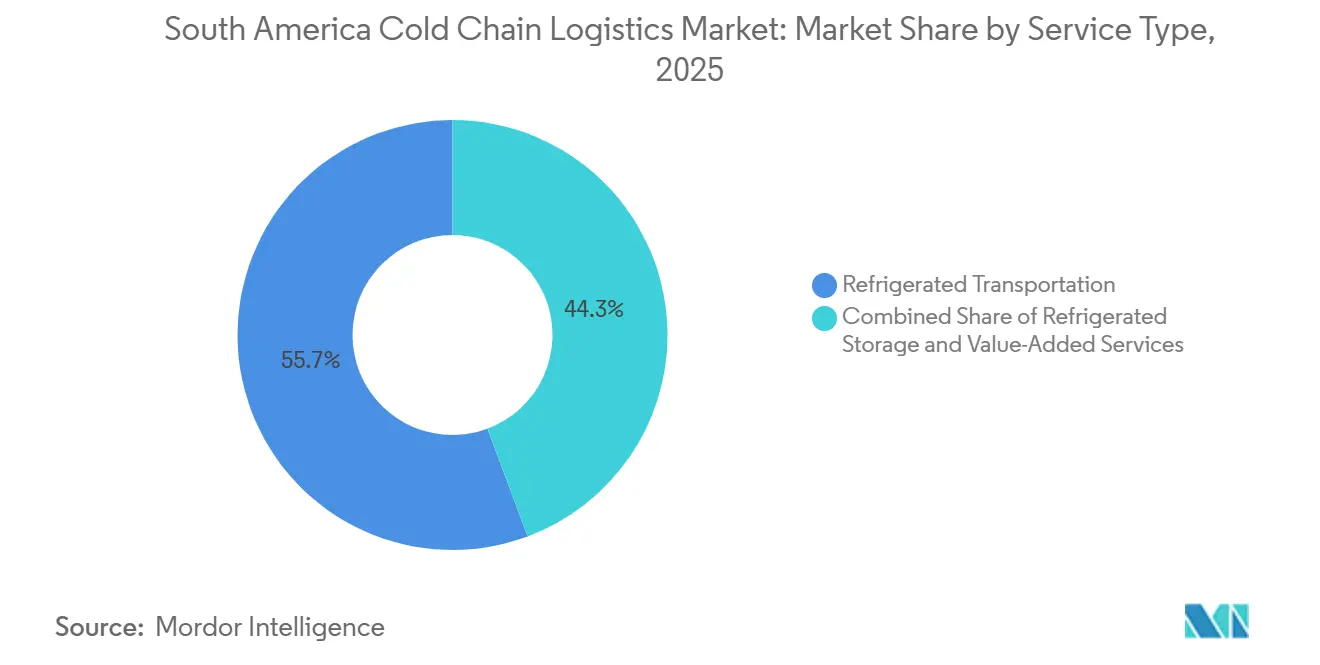

- By service type, refrigerated transportation led with 55.69% of the South America cold chain logistics market share in 2025; refrigerated rail transportation is advancing at a 5.54% CAGR through 2031.

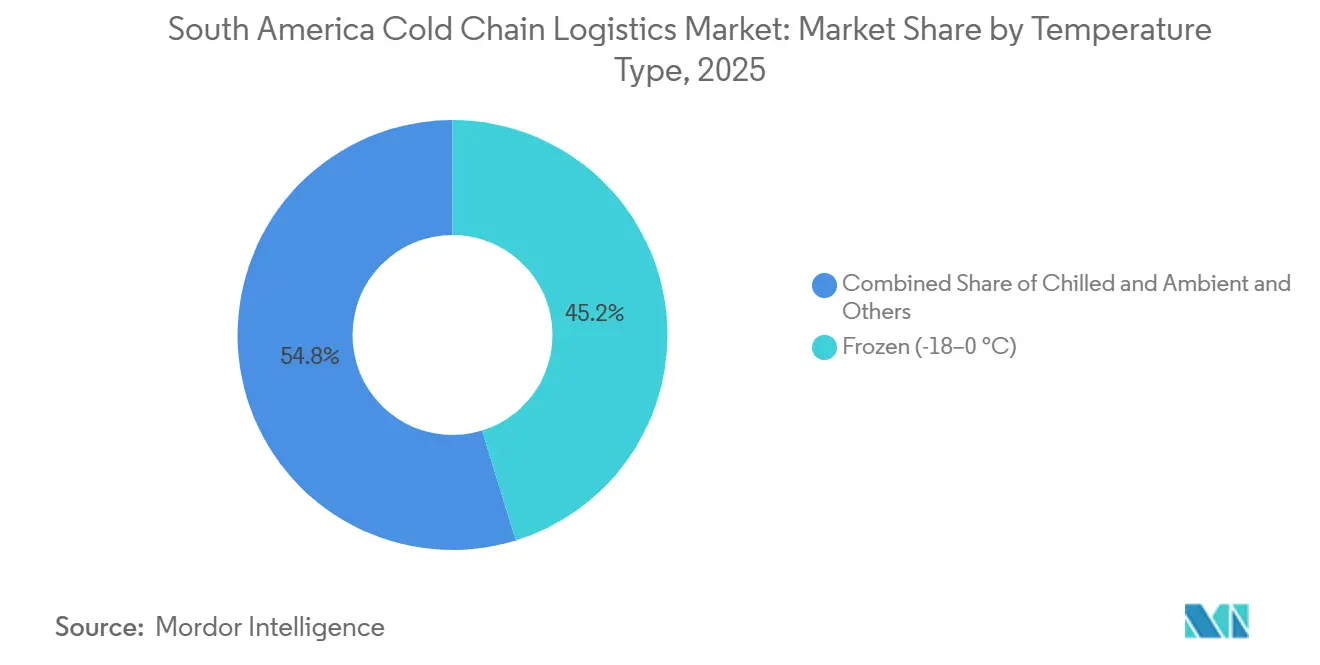

- By temperature type, frozen storage accounted for 45.22% of the South America cold chain logistics market size in 2025, while deep-frozen and ultra-low storage are projected to grow fastest at a 5.67% CAGR.

- By application, meat and poultry captured a 30.64% share of the South American cold chain logistics market size in 2025, and pharmaceuticals and biologics are expanding at a 6.94% CAGR through 2031.

- By country, Brazil held 48.42% of the South American cold chain logistics market share in 2025, whereas Argentina is forecast to record the highest CAGR at 6.98% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South america operates as part of an interconnected international environment rather than as a self-contained unit. The cold chain logistics market research by Mordor Intelligence places together all major regional developments across the globe within that wider frame.

South America Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing urban demand for processed and frozen food products | +0.8% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Expansion of temperature-controlled distribution networks for vaccines and biologics | +0.7% | Brazil, Peru, Colombia, Argentina | Short term (≤ 2 years) |

| Government export incentive schemes emphasizing cold chain compliance | +0.6% | Brazil, Argentina, Uruguay | Long term (≥ 4 years) |

| Shift toward nearshoring North American protein sourcing to Mercosur-based suppliers | +0.9% | Brazil, Argentina, Uruguay | Medium term (2-4 years) |

| Growth of e-grocery micro-fulfillment operations in Tier-2 Brazilian cities | +0.5% | Brazil (Campinas, Ribeirão Preto, Curitiba, Joinville, Londrina) | Medium term (2-4 years) |

| Rising exports of meat, poultry, and seafood from Mercosur countries | +0.7% | Brazil, Argentina, Uruguay, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Urban Demand for Processed and Frozen Food Products

Urbanization surpassed 87% in 2025, and single-person as well as dual-income households are fueling demand for convenience meals that rely on robust refrigeration logistics. Frozen entrées, IQF vegetables, and premium ice creams now occupy 22% of grocery baskets in Sao Paulo and Santiago, up from 16% in 2023. iFood earmarked 30% of its BRL 17 billion (USD 3.4 billion) infrastructure plan for temperature-controlled zones that support 15-minute delivery, forcing warehouse operators to locate within five kilometers of high-density districts. Retailers are adopting modular cold rooms that can be moved as neighborhood demand shifts, cutting stranded-asset risk. Chile and Argentina echo the trend, with per-capita frozen-food intake rising 9% and 11% respectively in 2025, signaling region-wide momentum. [1]iFood, “Infrastructure Investment Program,” ifood.com

Expansion of Vaccine & Biologics Distribution Networks

Multilateral lenders invested USD 180 million in 2025 to modernize vaccine logistics in Peru, Colombia, and Bolivia, replacing obsolete equipment in rural clinics where spoilage once exceeded 10%. The new infrastructure includes solar-powered coolers and real-time data loggers that pharmaceutical firms are re-deploying for investigational therapies, shaving 5-7 days off patient-enrollment timelines. Harmonized drug-regulation protocols have cut import-permit approvals from 90 days to under 45 days in Brazil and Argentina, allowing sponsors to pre-position -80 °C materials. Consequently, pharmaceuticals and biologics now post the fastest segment growth at 6.94% CAGR, doubling the pace of traditional protein categories. [2]Pan American Health Organization, “Cold Chain Assessment,” paho.org

Government Export Incentives Requiring Temperature Compliance

Brazil’s 2025 Agro+ Export program rebates 15% of temperature-controlled logistics costs for shipments verified by accredited auditors, helping exporters meet EU, Japanese, and Gulf quality benchmarks. Argentina followed with subsidies covering up to 20% of capital expenditure for warehouses equipped with blockchain-ready monitoring, expediting the shift from manual logs to IoT-enabled systems. Uruguay pilots carbon credits for natural-refrigerant adoption, aligning profit motives with Kigali commitments. These incentives lower border-clearance disputes and reduce rejection rates for high-value protein consignments destined for premium markets. [3]Brazil Ministry of Agriculture, “Agro+ Export Guidelines,” gov.br

Near-Shoring of North-American Protein Sourcing to Mercosur Suppliers

United States beef imports from South America rose 18% year-over-year in 2025 as buyers diversified away from drought-hit Oceania suppliers. Brazilian poultry gained 12% United States share by offering halal-certified, antibiotic-free lines, prompting cold-chain operators to co-locate blast-freezing capacity at Mato Grosso and Paraná slaughterhouses. The Port of Santos upgraded reefer plugs as container throughput expanded 22% in 2025. Argentina carved a grass-fed niche for premium food-service channels, while Uruguay exploits its traceability edge to command higher prices in Europe and the Middle East[4]United States Department of Agriculture Foreign Agricultural Service, “U.S. Beef Import Data,” usda.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited refrigerated road infrastructure and rising energy costs | -0.9% | Northern Brazil, rural Argentina, Bolivia, Paraguay | Long term (≥ 4 years) |

| Lack of harmonized regulatory standards across borders | -0.6% | Mercosur intra-bloc trade, Andean borders | Medium term (2-4 years) |

| Shortage of skilled personnel in industrial refrigeration operations | -0.4% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Elevated electricity tariffs and recurring power reliability issues | -0.7% | Northern Brazil, rural Argentina, Ecuador | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Refrigerated Road Infrastructure and Rising Energy Costs

Only 12% of Brazil’s paved highways meet “good” or “excellent” standards, limiting average truck speeds to 45 km/h and inflating diesel burn by 20% relative to Chilean hauls. Pothole-induced vibration accelerates compressor wear, shortening overhaul intervals from 18 to 12 months. Northern Brazil’s industrial-power tariff averaged BRL 0.52/kWh (USD 0.10) in 2025, and frequent outages force facilities to run generators for up to 20% of operating hours, eroding profit on low-margin protein cargos. Argentina’s rural grid faces similar blackouts lasting up to six hours, raising spoilage risk in sites without sufficient thermal buffering.

Lack of Harmonized Regulatory Standards Across Borders

Despite Mercosur’s customs union, each member maintains distinct sanitary certificates and temperature-log rules, adding 12-48 hours of border dwell for protein and biologics. A Chile-Argentina seafood load often undergoes re-inspection even when sealed under ISO-accredited certificates, while biologics routed São Paulo-Buenos Aires face triple checks. Pan-American regulatory alignment is underway, but full GDP standardization will not arrive before 2028. Operators estimate that duplicated inspections inflate compliance outlays by 8-12% versus EU lanes, where mutual-recognition eliminates redundancy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Rail Gains as Road Congestion Mounts

Refrigerated transportation captured the largest slice of 2025 revenue at 55.69%, illustrating the dependence of the South America cold chain logistics market on trucking for long hauls. Yet refrigerated rail is registering a 5.54% CAGR to 2031, the strongest within the segment. Rumo Logística’s 1,000-km rail route from Mato Grosso to the Port of Santos trims transit time by 18 hours and cuts per-ton-kilometer emissions 65% for soy derivatives, underscoring environmental and cost advantages. Road remains dominant for last-mile legs under 300 km, but diesel price volatility is nudging shippers toward natural-gas trucks in low-emission zones. Sea-based refrigerated transport holds steady on established routes, while air remains a niche for premium seafood and urgent biologics.

Value-added services are rising as operators seek margin diversity. Blast freezing, kitting, and temperature-controlled e-commerce fulfillment often command 20%-30% premiums over commodity storage. As e-grocery penetration deepens, micro-fulfillment nodes embedded inside urban warehouses are proliferating, requiring high-velocity pick-and-pack systems and real-time temperature monitoring. The South America cold chain logistics market size attributable to such services is projected to expand faster than headline growth, underpinned by shifting consumer behavior and retailer demand for same-day replenishment.

By Temperature Type: Deep-Frozen Rises on Pharma Demand

Frozen storage (-18 °C to 0 °C) delivered 45.22% of 2025 revenue, fueled by traditional protein and dessert flows. However, deep-frozen and ultra-low chambers below -20 °C are growing at a 5.67% CAGR through 2031, outpacing all other temperature bands. Emergent Cold LatAm operates ultra-low chambers in Sao Paulo and Rio, catering to cell-therapy trial sponsors demanding -80 °C stability. Regulatory mandates from CONAMA require new sites above 5,000 m³ to use refrigerants with global-warming potential below 150, effectively entrenching CO₂ or ammonia systems. This shift raises capex 10%-15% yet cuts long-run energy spend, improving lifetime economics of deep-freeze assets.

Chilled rooms (0°C to 5°C) remain essential for produce and dairy, while ambient-controlled zones are bundled into many contracts for packaging materials and dry ingredients. As Kigali phase-downs accelerate, retrofit demand may temporarily tighten contractor availability, but long-term efficiency gains and lower leak liability benefit operators’ bottom lines.

By Application: Pharma Outpaces Traditional Protein

Meat and poultry produced 30.64% of 2025 revenue, underscoring South America’s role as a protein powerhouse. Still, pharmaceuticals and biologics are projected to expand at a 6.94% CAGR, benefiting from diversified patient pools and lower clinical-trial costs. Multinational sponsors increasingly pre-stage investigational products in Brazil and Argentina to expedite enrollment and mitigate trans-Atlantic shipping risks. Fish and seafood volumes hinge on Chilean salmon and Ecuadorian shrimp exports, both of which rely on rapid post-harvest freezing to maintain quality.

Ready-to-eat meals are the fastest-growing food sub-segment in urban Brazil and Chile, advancing at double-digit rates as microwavable lasagna, empanadas, and stir-fry kits gain traction among time-starved consumers. Dairy, fruits, and vegetables continue to ride counter-seasonal export windows, while chemicals and specialty materials, though small, deliver high margins due to stringent quality demands. The South American cold chain logistics market size attached to pharma and specialty cargo is expected to rise disproportionately as regulatory harmonization simplifies cross-border flow.

Geography Analysis

Brazil’s 48.42% 2025 share mirrors its vast protein output, automated warehousing footprint, and multimodal connections. Cold-storage vacancy in Sao Paulo dipped below 3% in 2025, triggering a land grab in Tier-2 cities such as Campinas and Curitiba, where plots cost 40% less, and grid stability is stronger. The Port of Santos processed 22% more reefer boxes year on year, driven by beef and poultry shipments aligned with new EU-Mercosur quotas. iFood’s rapid expansion of micro-fulfillment hubs is pulling logistics providers into high-velocity urban nodes.

Argentina is the regional growth star, posting a 4.98% CAGR to 2031 after lifting beef quota caps and stabilizing the peso in 2025. Foreign direct investment is flowing into cold warehouses in Buenos Aires, Córdoba, and Santa Fe. Rehabilitation of the Belgrano Cargas rail line promises a lower-cost, lower-emission corridor for refrigerated citrus and wine exports once completed in 2027.

Chile’s ecosystem is anchored by salmon and counter-seasonal fruit exports, with operators in Puerto Montt and Valparaíso perfecting blast-freeze and controlled-atmosphere protocols that secure premiums in Northern-Hemisphere off-seasons. Peru’s blueberry and avocado boom is swelling capacity around Lima, yet vaccine-equipment obsolescence signals uneven infrastructure outside major cities. Colombia exhibits a two-tier profile: modern Bogotá and Medellín facilities versus rural zones still hampered by outdated trucks.

Uruguay leverages traceability and grass-fed credentials to command premiums, while Ecuador dominates global shrimp, integrating hatcheries with export consolidators in Guayaquil. Bolivia and Paraguay remain frontier territories, constrained by limited port access and underdeveloped highways, but Brazilian operators are scouting opportunities to extend regional coverage.

The cold chain logistics market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Africa, along with detailed country-level analysis for Mexico, Indonesia, Sweden, Netherlands, and Thailand.

Competitive Landscape

The South America cold chain logistics market shows moderate concentration: the top five players, Emergent Cold LatAm, Solistica By Traxion, DHL Supply Chain, Maersk, and SuperFrio, together controlling the majority of revenue. Global incumbents pursue bolt-on acquisitions, gaining real estate and permits, then retrofit with AS/RS systems, IoT monitoring, and natural-refrigerant plants to align with corporate sustainability targets.

Domestic champions such as Friozem and JSL’s Fadel Logística Fria defend their share through deep know-how of Brazil’s complex tax-substitution rules and port protocols. Smaller specialists thrive in seafood consolidation, artisanal frozen-dough exports, and organic-produce chains where flexibility outweighs scale. Technology adoption is accelerating: blockchain traceability platforms meet EU Deforestation Regulation requirements, while AI-driven forecasting tools reduce spoilage by up to 15%. Autonomous forklifts are being piloted at high-throughput sites to mitigate skilled-labor shortages.

White-space opportunities lie in Tier-2 micro-fulfillment hubs, Andean pharmaceutical corridors, and value-added services commanding higher margins. Investors weigh elevated energy tariffs and grid unreliability in northern Brazil and rural Argentina against favorable demand trends and supportive export incentives. Overall, rivalry is expected to intensify but remain balanced by strong growth fundamentals.

South America Cold Chain Logistics Industry Leaders

Emergent Cold LatAm

SuperFrio Logística

DHL Supply Chain

Maersk

Solistica By Traxion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The EU and Mercosur signed an interim trade agreement unlocking quotas for 99,000 t of beef and 180,000 t of poultry, catalyzing USD 200 million in cold-chain investment projected by 2028.

- October 2025: iFood disclosed BRL 8.5 billion (USD 1.7 billion) of a BRL 17 billion (USD 3.26 billion) program spent on dark kitchens and micro-fulfillment hubs, 30% of which funds cold chambers.

- August 2025: PAHO reported 61.8% obsolescence in Peru’s vaccine refrigeration, prompting a USD 45 million upgrade funded by the Inter-American Development Bank.

- June 2025: Brazil’s MAPA launched Agro+ Export, granting a 15% rebate on verified cold-chain costs for export protein shipments.

South America Cold Chain Logistics Market Report Scope

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

| Argentina |

| Brazil |

| Chile |

| Peru |

| Colombia |

| Rest of South America |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

| By Country | Argentina | |

| Brazil | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America cold chain logistics market in 2026?

It is estimated at USD 13.49 billion in 2026, on track to reach USD 16.59 billion by 2031.

Which country contributes the most revenue?

Brazil leads with 48.42% share owing to its vast protein exports and sophisticated cold-chain infrastructure.

What is the fastest-growing application segment?

Pharmaceuticals and biologics, projected to expand at a 6.94% CAGR between 2026 and 2031.

Why is refrigerated rail gaining traction?

It bypasses congested highways, lowers diesel dependence, and cuts per-ton emissions by up to 65% on corridors such as Mato Grosso-Santos.

How do new refrigerant rules affect investment costs?

Mandating low-GWP CO₂ or ammonia systems raises capital outlays 10%-15% but reduces long-term energy and compliance expenses.

What impact does the EU-Mercosur agreement have?

It unlocks sizable beef and poultry quotas, compelling exporters to invest in traceable, compliant cold-chain assets to access premium EU markets.

Page last updated on: