Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

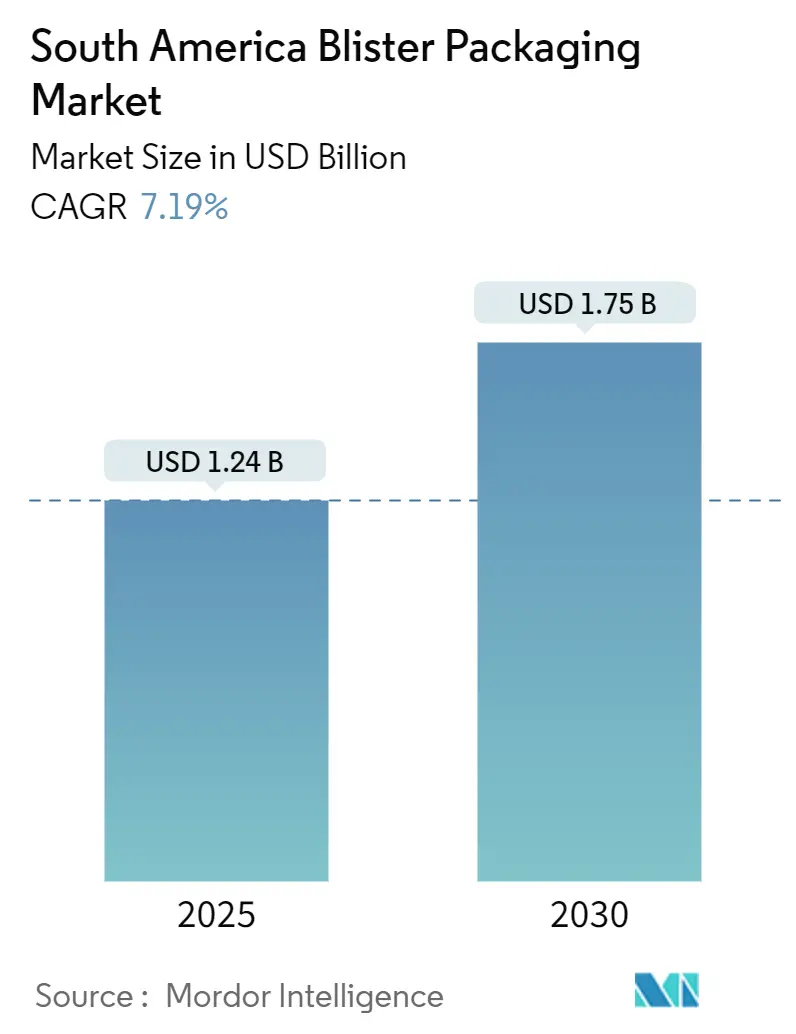

| Market Size (2025) | USD 1.24 Billion |

| Market Size (2030) | USD 1.75 Billion |

| Growth Rate (2025 - 2030) | 7.19% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Blister Packaging Market Analysis by Mordor Intelligence

The South America blister packaging market size reached USD 1.24 billion in 2025 and is forecast to climb to USD 1.75 billion by 2030, advancing at a 7.19% CAGR. Growth is primarily fueled by drug-traceability mandates, rising generic production, and a wave of contract manufacturing projects strategically clustered in Brazil’s industrial corridors. Intensifying brand competition pushes converters to install digital printers that apply compliant 2D DataMatrix codes at line speed, while sustainability rules in Chile and Colombia accelerate the switch to recyclable PET and paper-based webs. Manufacturers also benefit from near-shoring as multinational firms shift fill-finish work to South America for tariff and carbon-footprint advantages. Together, these factors create steady volume gains even as price sensitivity remains high in the regional pharmaceutical supply chain.

Key Report Takeaways

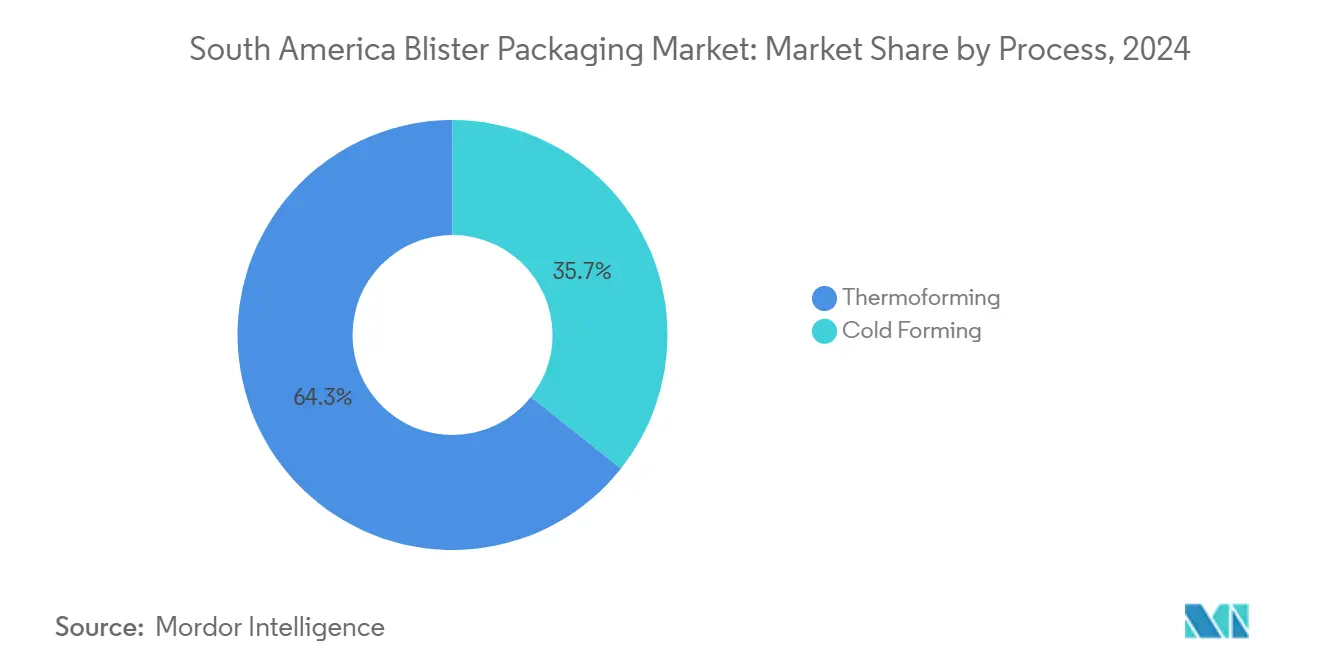

- By process, thermoforming captured 64.34% of the South America blister packaging market share in 2024. Thermoforming is projected to post the fastest 8.32% CAGR through 2030.

- By material, plastic films held 67.87% revenue in 2024; paper and paperboard are expected to expand at 9.01% CAGR to 2030.

- By product type, carded/face-seal packs commanded 51.46% share of the South America blister packaging market size in 2024, while clamshell formats are on track to grow 8.46% CAGR.

- By end-user, pharmaceuticals led with 58.24% share in 2024; nutraceuticals are forecast to accelerate at 9.76% CAGR through 2030.

- By country, Brazil accounted for 39.35% of share of South America blister packaging market in 2024; Chile is projected to grow at 9.7% CAGR to 2030.

South America Blister Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical serialization mandates | +1.8% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Expansion of regional CMOs | +1.5% | Brazil core, spillover to Colombia and Argentina | Long term (≥ 4 years) |

| Growth in self-medication and OTC drugs | +1.2% | Urban Brazil, Chile, Argentina | Short term (≤ 2 years) |

| E-commerce demand for consumer electronics | +0.9% | Brazil Southeast, Chile cities, Argentina AMBA | Medium term (2-4 years) |

| Near-shoring of global supply chains | +1.1% | Brazil manufacturing hubs, Argentina biotech corridor | Long term (≥ 4 years) |

| Digital printing for short-run blisters | +0.8% | Regional pharma manufacturing centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical serialization mandates boosting blister demand

Brazil’s SNCM regulation obliges every commercial-unit blister to carry a unique 2D DataMatrix code that feeds live event data to ANVISA databases, prompting drug makers to retrofit lines with code-resistant inks and laser etchers. Argentina’s nationwide e-prescription rollout widens digital interoperability, pushing pharmacies to scan serialized packs before retail hand-over. Similar rules from Chile’s ISP continue to tighten traceability. Converters thus prioritize film coatings that withstand autoclave heat yet accept crisp coding, while machinery suppliers market turnkey vision-inspection modules. Collectively, these compliance pressures elevate unit-dose blister adoption across brand, generic, and hospital channels, reinforcing the long-run trajectory of the South America blister packaging market.

Expansion of regional Contract Manufacturing Organizations (CMOs)

Brazil’s massive lifescience clusters attract multinationals that want local capacity plus duty-saving incentives. Novo Nordisk’s USD 1.09 billion enhancement of its Montes Claros campus adds aseptic lines that will push annual blister requirements sharply higher once commercial output starts in 2028. EMS and other domestic generics groups are also scaling to supply patent-expiring GLP-1s, further swelling demand for deep-cavity cold-form packs. Colombia’s Procaps Group already fabricates more than 370 million blister units per month for regional export, underscoring the volume potential as CMOs adopt Pharma 4.0 workcells that switch formats on command.

Growth in self-medication and OTC drugs

Low-cost pharmacy chains, typified by Farmacias Similares’ 505-store network in Chile, sell deeply discounted generics linked with walk-in medical consult rooms, a model that lifts OTC blister throughput even during economic lulls. Brazil’s retail antibiotic sales climbed from 45.25 million to 59.32 million packs between 2014 and 2019, revealing entrenched self-care habits. As public payers cap annual price hikes, pharmaceutical firms rely on high-turn blister SKUs to sustain margins, thereby supporting a stable base load for converters across the South America blister packaging market.

E-commerce penetration for consumer-electronics accessories

Contactless payment adoption helped Argentina’s prepaid card transactions jump 39% year-over-year in 2024, mirroring a regional trend where Gen Z accounts for 60% of online orders. Portable earbuds, chargers, and gaming peripherals increasingly ship inside transparent clamshells that prevent pilferage while showcasing design features. As returns handling grows costly, sellers insist on crush-resistant blisters that cut damage claims. This dynamic inserts a fast-moving consumer electronics niche into the wider South America blister packaging market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatility in medical-grade PVC and aluminum | -1.4% | Global supply chains affecting regional converters | Short term (≤ 2 years) |

| Plastic-waste legislation in Chile and Colombia | -0.8% | Chile REP Law, Colombia Resolution 14047 | Medium term (2–4 years) |

| Shortage of GMP cold-form-foil suppliers | -0.6% | Regional pharma clusters | Short term (≤ 2 years) |

| Counterfeit blister formats | -0.5% | Cross-border trade corridors and urban retail centers | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Volatility in medical-grade PVC and aluminum prices

South American converters import the majority of rigid-grade PVC and rolled aluminum, exposing them to currency swings and freight spikes. Sudden cost inflation limits their ability to offer long-term contracts, a challenge that weighs on small family-owned thermoformers. Some buyers shift to PET-G webs with 50% recycled content from regional suppliers such as Evertis, which partially cushions volatility.[1]Evertis, “Evercare Brand for Healthcare Packaging,” evertis.com

Stringent plastic-waste legislation in Chile and Colombia

Chile’s Law 20.920 compels producers to finance post-consumer take-back and meet rising recovery quotas, while Colombia’s Resolution 14047 sets phased recycled-content mandates on medical packs. These statutes raise compliance costs for PVC blisters and encourage mono-material PET or fiber alternatives. Firms that fail to adapt risk market-access barriers within the South America blister packaging industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process: Thermoforming retains value leadership amid cost focus

Thermoforming generated 64.34% of the South America blister packaging market share in 2024 and is on track for an 8.32% CAGR, confirming its role as the volume backbone of regional pack operations. The segment leverages low-cost PVC or PET roll stock, straightforward tool fabrication, and fast cycle times that suit generic-drug megabatches. Enhanced forming stations now accept recyclable PET-G films containing post-consumer flakes, aligning with REP compliance in Chile without sacrificing optical clarity.

Operationally, servo control shortens index lengths and cuts scrap, which is critical because many contracts price blisters per cavity rather than per sheet. The cold-forming niche, while materially expensive, protects moisture-sensitive APIs and supports export shipments to climates where humidity reaches 90%. Converters specializing in cold-forming negotiate capacity premiums that offset aluminum volatility, yet their overall tonnage remains small inside the South America blister packaging market. Continuous R&D focuses on hybrid lines that integrate deep-draw thermoforming with adhesive-laminated aluminum lids, a bridge technology that may unlock mid-tier OTC use cases previously priced out of ALU-ALU formats.

By Material: Plastics dominate, but fiber alternatives gain policy tailwinds

Plastic films delivered 67.87% revenue in 2024, as PVC and PET remain inexpensive, sealable, and compatible with high-speed lines. Post-pandemic freight normalization, however, does little to ease rising pressure from environmental regulators. Chile’s REP law obliges brands to hit stepwise collection targets, pushing multinational drug makers to request mono-material PET-G webs that streamline recycling streams. Suppliers answer with PET formulations containing 30-50% recycled content that still pass USP <661.1> extractables tests, an achievement previously thought unfeasible for pharmaceutical contact layers.

Paper and molded fiber are the fastest-growing slice, climbing at 9.01% CAGR as technology improves barrier coatings that survive humidity cycles common across the Amazon basin. Aluminum sheet maintains a critical role for light-sensitive hormones and antibiotics, especially for products bound for equatorial climates where blackout protection is mandatory. All told, the sustainability pivot is redefining raw-material demand curves inside the South America blister packaging market.

By Product Type: Carded packs remain mainstream while clamshells accelerate

Face-seal designs held 51.46% share of the South America blister packaging market size in 2024, thanks to their compact footprint and automated cartoning compatibility in pharma plants. The format’s clear window supports visual verification during pharmacy dispensing, thereby complementing serialization checks.

Clamshell packs, forecast to grow 8.46% CAGR, capture rising e-commerce traffic for earbuds, memory cards, and small IoT devices, industries that value resealability and impact resistance. Regional electronics brands position clamshells as a premium proposition that mitigates counterfeit substitution because tamper evidence is obvious once hinges are broken. Trapped and full-card blisters remain niche but critical for theft-prone razor cartridges and high-value dietary supplements. As format diversity rises, machinery OEMs are shipping modular feeders that switch from carded to clamshell geometry in under 30 minutes, allowing converters to widen SKU menus without dedicated floor space.

By End-User Industry: Pharmaceuticals anchor demand; nutraceuticals surge

Pharmaceuticals accounted for 58.24% of 2024 revenue, powered by Brazil’s USD 14.7 billion domestic drug market and a steady pipeline of generic launches tied to patent cliffs worth USD 5-6 billion between 2024 and 2028. Mandatory serialization locks in blister usage for prescription drugs, while antibiotics, analgesics, and antihypertensives dominate unit-dose volumes.

Nutraceuticals and dietary supplements, expanding at 9.76% CAGR, ride a wave of gym memberships and preventive-health marketing. Flexible blister cavities permit combined vitamin-mineral sachets that shorten dosing routines for consumers. Consumer electronics accessories claim a modest yet rising slice, driven by cross-border e-commerce that demands protective retail-ready packs. Personal-care items such as whitening strips maintain a steady baseline. Collectively, these end-use patterns reinforce a broad mix that stabilizes the South America blister packaging market against single-sector shocks.

Geography Analysis

Brazil captured 39.35% of share of South America blister packaging market in 2024, reflecting its status as the region’s dominant pharmaceutical producer and home to ANVISA’s rigorous SNCM traceability system that structurally favors blister adoption. Local preference margins of up to 15% for domestically made drugs further stimulate investments in vertically integrated lines, ensuring sustained demand for serialization-ready packs. Southeast states such as São Paulo and Minas Gerais host most converting capacity, benefiting from highway links to port terminals and a deep technical labor pool.

Chile delivers the fastest 9.7% CAGR outlook through 2030 as REP legislation requires brand owners to finance collection schemes, prompting quick migration from PVC to recyclable PET. The country’s retail-pharmacy build-out spearheaded by Farmacias Similares increases OTC shelf facings, thereby multiplying blister facestock requirements. Santiago’s high household-income corridor also favors premium clamshells for imported gadgets, diversifying material flows into PET-G and rPET.

Argentina offers upside despite foreign-exchange turmoil. The biotech corridor around Buenos Aires supports 22% of national biotech firms, with pharmaceuticals absorbing 62% of sector R&D spending.[2]World Bank, “A New Growth Horizon for Argentina,” worldbank.org Mandatory e-prescriptions effective 2025 enhance data integrity and should accelerate serialized blister penetration even in small dispensaries. Import license bottlenecks, however, force converters to carry buffer stocks of foil and barrier films, adding working-capital strain.

Colombia’s Resolution 14047 obliges plastic-waste recovery and recycled-content quotas that gradually reshape resin selection. Local specialist Meprec supplies unit-dose packs for domestic pharma while Procaps exports finished dosages regionwide, anchoring steady demand for thermoformed PVC/PCTFE combinations.

Competitive Landscape

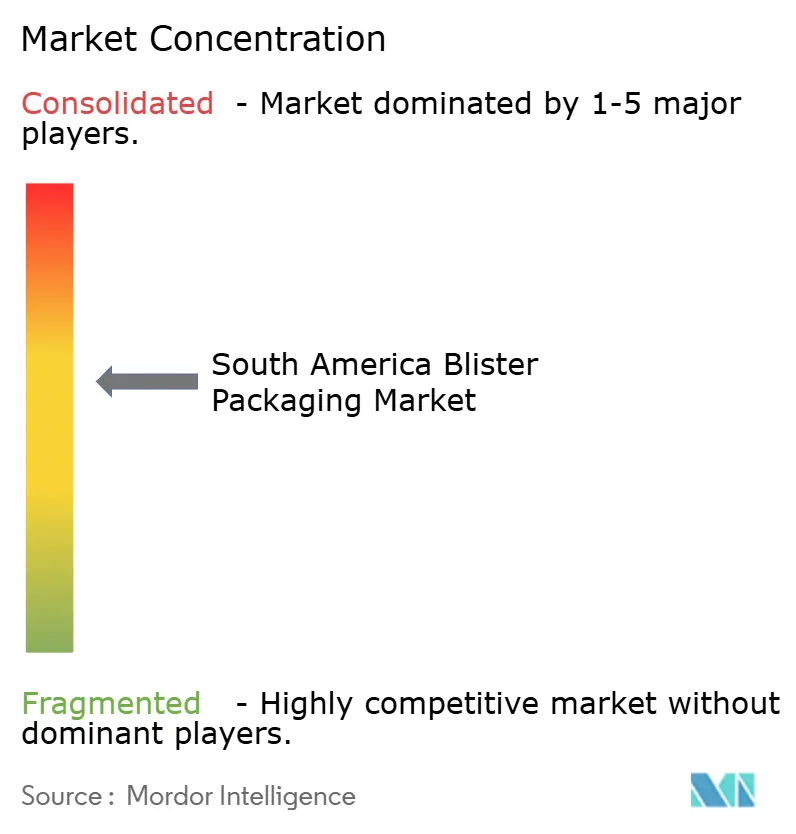

The South America blister packaging market displays moderate concentration. Five leading converters and global film suppliers collectively control a significant share of the installed forming capacity, resulting in a market concentration score of 6 out of 10. Amcor’s South America division operates 19 flexible sites across six countries, supplying PVC, PVdC, and PET laminates that meet USP <661.1> migration limits.[3]Amcor, “Amcor Flexibles Packaging Latin America,” amcor.com TekniPlex Healthcare has recently increased its multilayer-film output in Europe, a move that provides capacity redundancy for its Brazilian customers seeking peelable, recyclable blisters. Evertis, meanwhile, focuses on high-clarity PET-G with recycled content for the healthcare industry, providing regional buyers with access to lower-carbon substrates.

Domestic converters, such as Ricardo Wagner S.A. in Argentina and Meprec in Colombia, compete on proximity, small-batch agility, and local regulatory expertise. Their edge lies in fast artwork approval loops and lower inbound freight compared with imports. Strategic deals amplify distribution power; Nissei’s acquisition of Brazil’s Rede Santa Marta pharmacy chain solidifies downstream control of pack specifications for in-house generics.

Technology rivalry centers on inline digital printing and integrated vision inspection. Early adopters tout error rates below 0.05% on serialized blisters, a threshold that satisfies ANVISA audits while trimming rework. Sustainability credentials also shape bids as buyers request lifecycle data. Suppliers offering PET-only blisters with foil-free paper lids gain traction in Chile and Colombia, though qualification cycles remain lengthy.

South America Blister Packaging Industry Leaders

-

Amcor plc

-

Smurfit WestRock

-

Tekni-Plex, Inc.

-

Constantia Flexibles Group GmbH

-

Klöckner Pentaplast Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novo Nordisk confirmed USD 1.09 billion investment to enlarge its Montes Claros site with aseptic halls and solar-powered utilities, projected to start commercial production in 2028.

- February 2025: Evertis rolled out Evercare medical-grade PET films containing up to 50% recycled content and compliant with ISO 10993 and USP <661.1> for healthcare applications.

- February 2025: The World Bank highlighted South America’s renewable energy edge for low-carbon manufacturing in a regional investment brief.

- February 2025: Argentina enforced e-prescriptions as the only valid modality nationwide, mandating platform interoperability under Decreto 345/2024.

South America Blister Packaging Market Report Scope

The South America Blister Packaging Market Report Is Segmented by Process (Thermoforming and Cold Forming), Material (Plastic Films, Aluminium (ALU-ALU, PTP Foil), and Paper and Paperboard), Product Type (Carded/Face-Seal Blisters, Clamshell Blisters, Trapped and Full-Card Blisters, and Child-Resistant/Senior-Friendly Packs), End-User Industry (Pharmaceuticals, Nutraceuticals and Dietary Supplements, Consumer Electronics and Hardware, Personal Care and Cosmetics, and Other End-User Industries), and Country (Brazil, Argentina, Chile, and the Rest of South America). The Market Forecasts Are Provided in Terms of Value (USD).

By Process

| Thermoforming |

| Cold Forming |

By Material

| Plastic Films |

| Aluminium (ALU-ALU, PTP foil) |

| Paper and Paperboard |

By Product Type

| Carded / Face-Seal Blisters |

| Clamshell Blisters |

| Trapped and Full-Card Blisters |

| Child-Resistant / Senior-Friendly Packs |

By End-User Industry

| Pharmaceuticals |

| Nutraceuticals and Dietary Supplements |

| Consumer Electronics and Hardware |

| Personal Care and Cosmetics |

| Other End-user Industry |

By Country

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Process | Thermoforming |

| Cold Forming | |

| By Material | Plastic Films |

| Aluminium (ALU-ALU, PTP foil) | |

| Paper and Paperboard | |

| By Product Type | Carded / Face-Seal Blisters |

| Clamshell Blisters | |

| Trapped and Full-Card Blisters | |

| Child-Resistant / Senior-Friendly Packs | |

| By End-User Industry | Pharmaceuticals |

| Nutraceuticals and Dietary Supplements | |

| Consumer Electronics and Hardware | |

| Personal Care and Cosmetics | |

| Other End-user Industry | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America blister packaging market?

The market stands at USD 1.24 billion in 2025.

How fast is the market expected to grow?

It is projected to post a 7.19% CAGR, taking revenue to USD 1.75 billion by 2030.

Which process dominates regional production?

Thermoforming leads with 64.34% share and remains the fastest-growing at 8.32% CAGR.

Which country contributes the most demand?

Brazil holds 39.35% of 2024 revenue due to its large pharmaceutical base.

What material is gaining popularity for sustainability reasons?

Recyclable PET-G containing post-consumer content is the leading eco-friendly substitute for PVC.

Why are serialization mandates important?

They require unique 2D codes on every unit-dose pack, driving demand for digitally printed, track-and-trace-ready blisters.

Page last updated on: