South America Biochar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

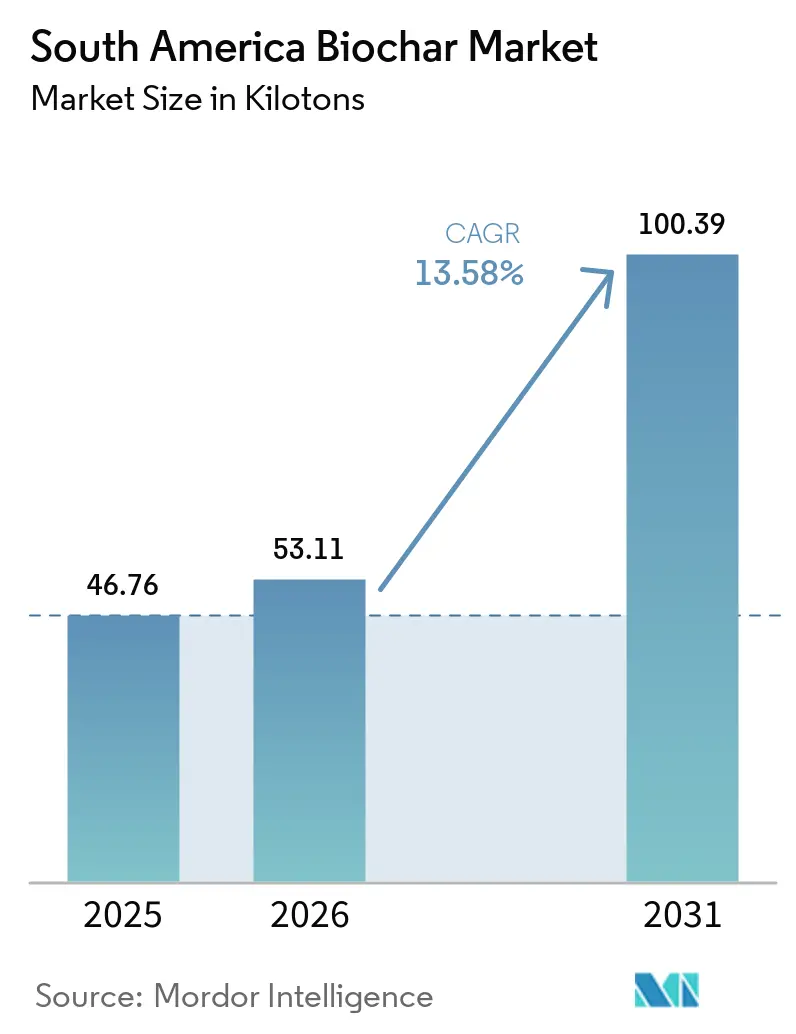

| Base Year Market Size (2025) | 46.76 kilotons |

| Market Volume (2026) | 53.11 kilotons |

| Market Volume (2031) | 100.39 kilotons |

| Growth Rate (2026 - 2031) | 13.58% CAGR |

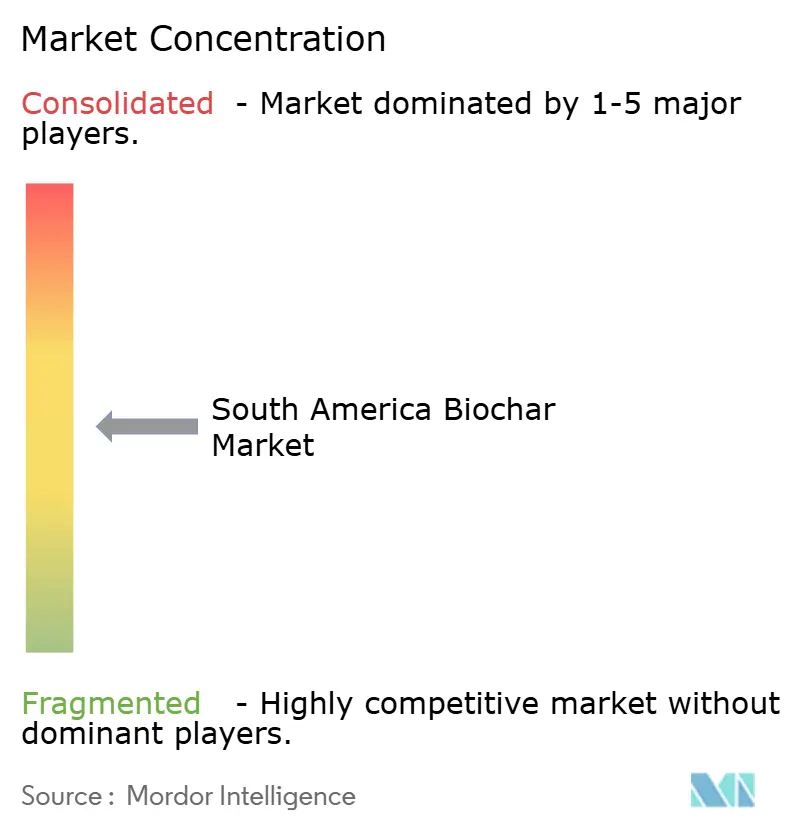

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Biochar Market Analysis by Mordor Intelligence

The South America Biochar Market size stood at 46.76 kilotons in 2025 and is estimated to grow from 53.11 kilotons in 2026 to reach 100.39 kilotons by 2031, at a CAGR of 13.58% during the forecast period (2026-2031). This expansion reflects three intertwined forces: abundant crop and forestry residues that supply low-cost feedstock, a premium carbon-credit environment that values durable carbon storage, and mounting demand for soil-conditioners that counter tropical acidity. Brazil anchors the South America biochar market, leveraging its vast sugarcane and coffee sectors to supply 67.05% of 2025 volume while attracting impact capital for new pyrolysis facilities. Argentina and Colombia are emerging hubs, helped by university-industry pilots that valorize rice straw, coffee husks, and woody biomass. Voluntary carbon credits priced between USD 160 and USD 220 per ton CO₂ underpin project finance, while livestock producers adopt biochar feed additives to curb methane and improve weight gain. At the same time, industrial users in mining, filtration, and metallurgy accelerate uptake as they search for fossil-free process inputs.

Key Report Takeaways

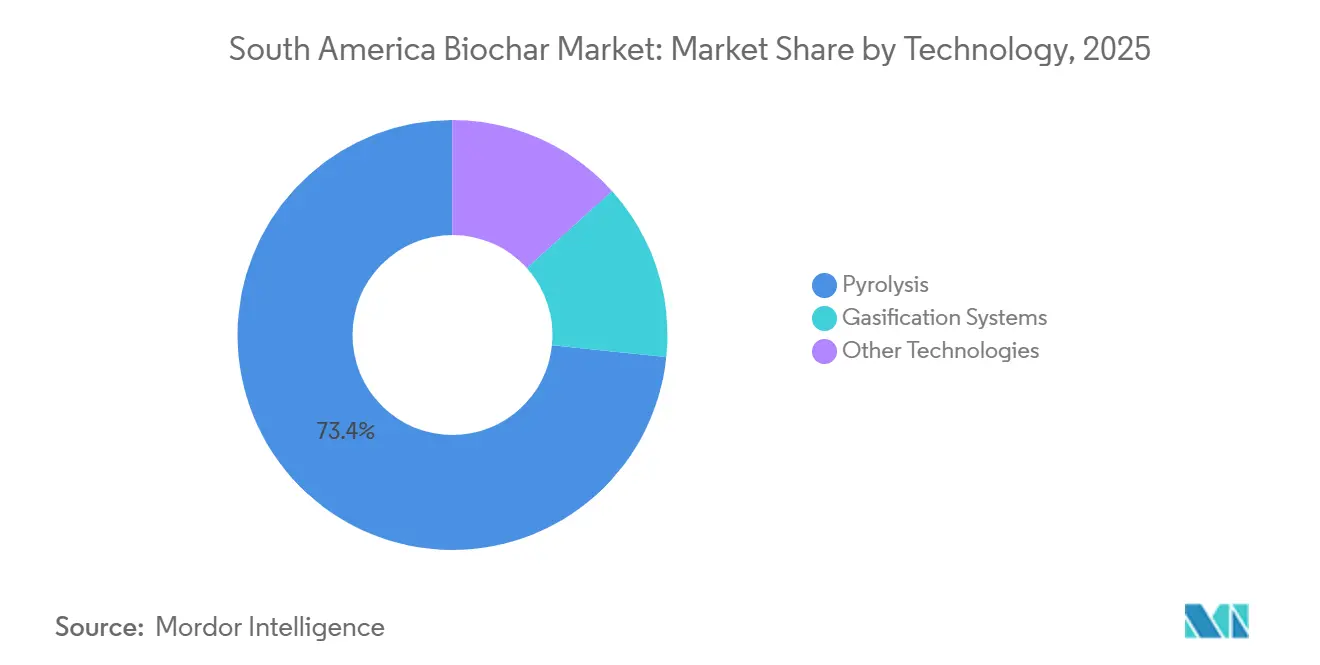

- By technology, pyrolysis captured 73.37% of the South America biochar market share in 2025 and is projected to advance at a 15.96% CAGR through 2031.

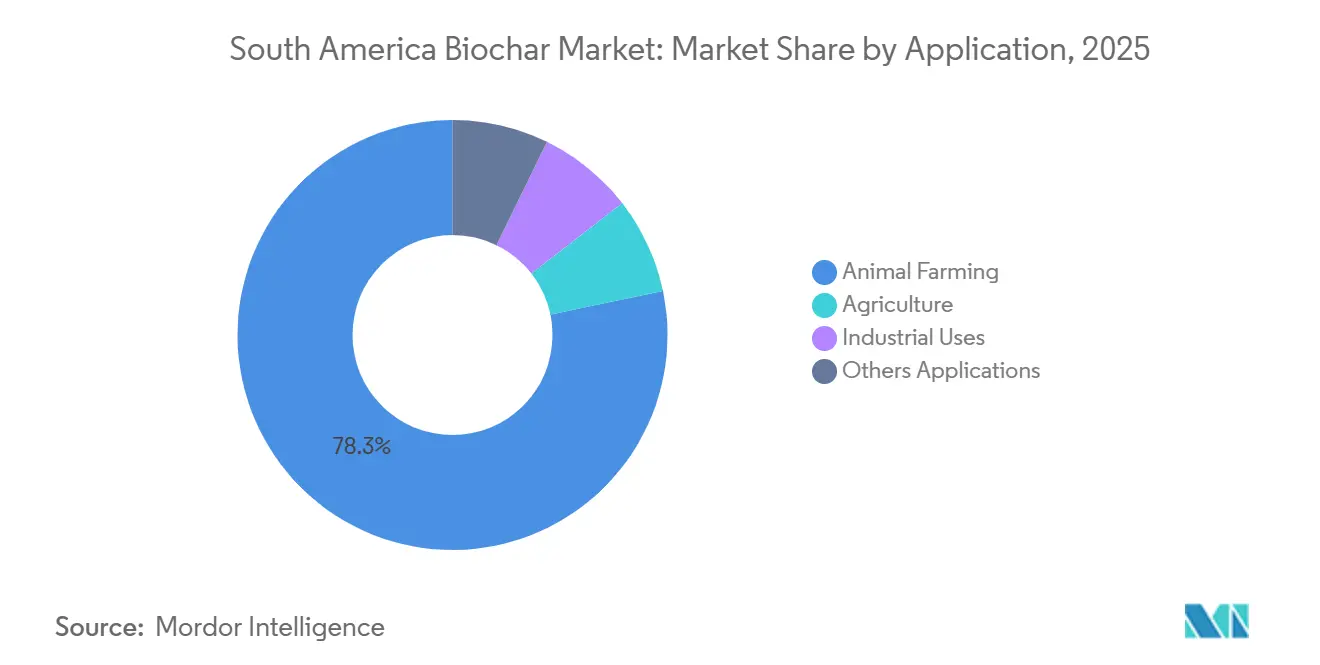

- By application, animal farming accounted for 78.28% of the South America biochar market share in 2025, while industrial uses are forecast to expand at a 14.16% CAGR through 2031.

- By geography, Brazil led with 67.05% of the South America biochar market share in 2025 and is forecast to expand at a 15.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Biochar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Agricultural soil-fertility improvement demand | +3.2% | Brazil, Argentina, Colombia; concentrated in Cerrado, Pampas, and Andean valleys | Medium term (2-4 years) |

| Carbon credits and emerging voluntary carbon markets | +4.1% | Global, with early monetization in Brazil and Bolivia; spillover to Argentina and Paraguay | Short term (≤ 2 years) |

| Adoption in livestock feed additives for methane reduction | +2.8% | Brazil (cattle), Argentina (beef and dairy), Uruguay (sheep); aligns with national methane-reduction pledges | Medium term (2-4 years) |

| Government incentives for sustainable waste management | +1.9% | National, with early gains in São Paulo, Rio de Janeiro, Buenos Aires, and Bogotá municipalities | Long term (≥ 4 years) |

| Mining-tailings rehabilitation using biochar blends | +1.6% | Amazon basin (Brazil), Andean copper/gold zones (Chile, Peru spillover to Colombia); localized to extraction sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Agricultural Soil-Fertility Improvement Demand

Tropical soils are acidic and low in cation-exchange capacity, hampering nutrient availability for soybean, maize, and coffee. Field trials showed that 5-10% biochar by volume raised Agave sisalana biomass by 60% in Brazil, while sugarcane-bagasse biochar lifted soil pH by up to 0.7 units and cut lime use by 40%. Coffee-husk biochar retained 25% more water in sandy soils, easing drought stress during Arabica flowering. With prices of USD 700-1,200 per ton, biochar competes with imported NPK when amortized across three seasons of nutrient-use savings. Brazil’s Ministry of Development formed Study Commission 328 in 2024 to draft national pyrogenic-biocarbon standards, signaling policy readiness for scale.

Carbon Credits and Emerging Voluntary Carbon Markets

Biochar offsets command premiums because carbon remains stable for millennia. Puro.earth’s CORCHAR index valued credits at R$600-1,000 (USD 120-200) in 2025, far above European allowance prices. Exomad Green’s 1.24-million-ton contract with Microsoft priced removals near USD 200-250, financing a doubled Bolivian capacity. Altitude and Empacar’s 1-million-ton deal in 2026 confirms rising corporate appetite for measurable, reportable, verifiable (MRV) carbon storage. Verra’s VM0044 issuance of 161,507 CORCs to Aperam BioEnergia proves that industrial-scale biochar projects can monetize carbon while supplying agronomic markets.

Adoption in Livestock Feed Additives for Methane Reduction

South America’s 330 million cattle generate significant methane. Trials on Nelore steers fed 20 g/kg sugarcane-biochar cut enteric methane 15% and lifted weight gain 12% over 120 days. Biochar’s porous structure adsorbs mycotoxins such as aflatoxin B1, reducing gut inflammation in poultry and swine. Feed savings of 8-26% offset inclusion costs of USD 0.15-0.30 per animal per day. Colombia’s National University found low-temperature woody biochar increased anaerobic-digester methane 30%, closing nutrient-energy loops.

Government Incentives for Sustainable Waste Management

Brazil’s Solid Waste Policy mandates a 50% landfill diversion of recyclables and organics by 2030, steering municipalities toward pyrolysis. Argentina’s General Alvarado pilot intends to process up to 5,000 tons of green waste, financed by VM0044 credits that cover operating costs. Brazil’s Eco.Invest program provides R$500 million in low-interest loans for renewable waste processing, including small pyrolysis units that turn coffee husks and palm bunches into biochar and renewable heat.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insufficient regional production capacity and fragmented supply chain | -2.4% | Brazil (outside São Paulo-Paraná corridor), Argentina (beyond Buenos Aires), Colombia (rural departments); acute in Rest of South America | Short term (≤ 2 years) |

| High capital and operating costs of advanced pyrolysis units | -1.8% | National, with cost barriers highest in Argentina (import tariffs), Paraguay, Uruguay (limited equipment manufacturing) | Medium term (2-4 years) |

| Variable biochar quality causing inconsistent agronomic results | -1.3% | Global, with feedstock heterogeneity most pronounced in Brazil (mixed crop residues) and Colombia (coffee-processing byproducts) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Insufficient Regional Production Capacity and Fragmented Supply Chain

NetZero and Exomad Green together supply 60% of regional output, leaving many areas without commercial product within 300 km. Batch kilns in Colombia’s Santander department turn out just 200-500 kg a week, while Argentina’s rice-straw project remains pilot-scale. Transporting low-density biochar erodes margins, so farmers beyond 100 km rarely adopt. Fewer than 2% of Brazil’s 6 million-ton charcoal sector meets agronomic-grade standards, delaying penetration[1]Empresa de Pesquisa Energética, “Charcoal and Biochar Fact Sheet,” epe.gov.br.

High Capital and Operating Costs of Advanced Pyrolysis Units

Continuous reactors that enable MRV-compliant carbon credits cost USD 80,000 to USD 2 million. Import tariffs add 40-50% to Argentine buyers, and feedstock prices swing seasonally, forcing plants to idle or stockpile. NetZero’s USD 36 million raise funded its February 2026 facility, but smaller cooperatives cannot shoulder similar intensities. Operating expenses range from USD 240-290 per ton, inhibiting new entries in Paraguay and Uruguay.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Pyrolysis Dominates Through Process Control and Co-Product Flexibility

Pyrolysis supplied 73.37% of 2025 volume and is forecast to grow at a 15.96% CAGR through 2031, underpinning the South America biochar market size leadership through 2031. Slow pyrolysis at 300-400 °C leverages longer residence times to sustain functional groups that improve cation exchange, while fast modes at 600-700 °C increase carbon permanence for credit generation. NetZero’s Gen2 units run 20-40-minute cycles at 450-550 °C and capture syngas for onsite heat, lowering cash operating costs. Gasification remains secondary because char yields are just 10-20% of feedstock mass, and other pathways such as hydrothermal carbonization are still pilot level. Verra’s forthcoming VM0044 v2 will allow modular 500-2,000 ton systems into credit schemes, potentially unlocking mid-scale adoption and diversifying the South America biochar industry.

Demand for pyrolysis equipment stretches from municipal waste managers to mining firms. Brazil’s Eco.Invest loans now cover reactor purchases that process coffee husks during off-season months. University groups adapt low-cost nested-drum kilns for açaí seeds, giving cooperatives a USD 150 entry price at the expense of MRV precision. Equipment suppliers that integrate data loggers, cyclone gas cleaning, and condensate recovery may capture higher margins as buyers seek dual revenue from biochar sales and electricity.

By Application: Animal Farming Leads, Industrial Uses Accelerate

Animal farming absorbed 78.28% of 2025 demand, keeping the South America biochar market share concentrated in feed applications tied to methane targets[2]PubMed Central, “Biochar Feed Additive Meta-Analysis,” pubmed.ncbi.nlm.nih.gov. Feed mix inclusion at 1-2% of dry matter lifts gain-to-feed ratios up to 26%, allowing producers to recoup USD 0.30 daily costs within finishing cycles. Regulatory agencies have yet to classify biochar as a feed additive, so uptake relies on private protocols verified by third-party labs. Agriculture is using 5-10 tons per hectare doses to raise pH, store nutrients, and buffer drought in Cerrado and Pampas soils.

Industrial uses are the fastest-growing segment at a 14.16% CAGR through 2031. Mining firms blend biochar into mercury-rich tailings, while steelmakers test high-temperature char as a biocarbon reductant. Water-treatment plants pilot microplastic capture via biochar filters, taking advantage of surface areas that can exceed 3,000 m²/g after activation. As carbon credits co-fund capital expenditure (CAPEX), this niche could claim a larger sliver of the South America biochar market size by 2031.

Geography Analysis

Brazil dominated with 67.05% of 2025 volume and is poised to expand at a 15.05% CAGR through 2031. Its 850 million tons of crop residues and supportive Bio-Inputs Law grant tax incentives and technical standards that attract investors. NetZero’s February 2026 sugarcane-residue facility added 14,000 tons per year capacity, pushing company output toward 50,000 tons per year and supplying cooperatives in Minas Gerais and Espírito Santo. Brazil’s RenovaBio fuel credit system now recognizes biochar co-application, integrating it with ethanol carbon-intensity reductions.

Argentina is strengthened by forestry and rice-straw valorization. The National University of Río Cuarto’s January 2026 pilot transformed 13,600 tons of straw otherwise burned in Corrientes, creating room for commercial scale-up. General Alvarado municipality’s 5,000 tons per year plant demonstrates how VM0044 credits can self-fund waste-processing hubs.

Colombia’s coffee-centric cooperatives treat husks for on-farm use, and National University work shows biochar boosts biogas yields, giving farmers an extra revenue stream. Exomad Green anchors Bolivia’s carbon-removal positioning with Microsoft’s purchase, making the country a net exporter of credits even while domestic agronomic demand stays small. Chile’s Biochar Chile mixes tailings for Atacama reclamation, and Paraguay’s Project Alfheim plans 13,000 tons per year biochar aimed at European buyers. As modular reactors proliferate, these countries can bridge feedstock pockets to broader carbon markets, expanding the footprint of the South America biochar market.

Competitive Landscape

The South America biochar market is moderately concentrated, with the five largest companies being Aperam BioEnergia, Airex Energy, NetZero, ZeroCarbon One, and Pacific Biochar Benefit Corporation. NetZero maintained four Brazilian sites and planned for 50,000 tons per year by end-2025, selling bundled char and credits to sugar mills and cattle ranchers. Exomad Green captured 27% of global carbon-dioxide-removal volume through Microsoft’s 1.24 million-ton deal, pivoting toward large offtake contracts rather than agronomic spot sales. Aperam BioEnergia benefits from integrated charcoal-steel operations that spread fixed costs over 450,000 tons per year, while university-industry pilots in Argentina and Colombia pioneer low-volume, feedstock-specific plays.

Strategic patterns coalesce around vertical integration. NetZero and Exomad monetize both carbon and co-products, shortening payback periods below five years. Smaller entrants differentiate by targeting livestock additives or metallurgical biocarbon, niches that promise higher margins once regulations clarify. The pending VM0044 v2 broadens eligibility for modular units, likely spurring mid-scale adopters and intensifying rivalry across the South America biochar industry.

South America Biochar Industry Leaders

Airex Energy

Aperam BioEnergia

NetZero

ZeroCarbon One

Pacific Biochar Benefit Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Altitude partnered with EcoGaia and Emisiones Neutras to acquire more than 165,000 tons of Carbon Dioxide Removal Certificates (CORCs) from newly established, large-scale biochar facilities in Argentina. This initiative facilitated the transformation of forestry waste into durable biochar, with credits verified and issued through the Puro Registry.

- October 2025: Exomad Green announced the expansion of its Concepción facility, representing a significant step in its efforts to enhance carbon removal and sustainable biomass management. The facility initially operated with three advanced pyrolysis reactors, producing 25,000 tons of biochar annually and capturing 60,000 tons of CO₂ each year.

South America Biochar Market Report Scope

Biochar is a stable, carbon-rich charcoal derived from heating organic waste (biomass) in a low-oxygen environment through pyrolysis. It serves as a long-term soil amendment, enhancing water retention, nutrient efficiency, and microbial activity, while sequestering carbon for extended periods to help address climate change.

The South America Biochar Market is segmented into technology, application, and geography. By technology, the market is segmented into pyrolysis, gasification systems, and other technologies. By application, the market is segmented into agriculture, animal farming, industrial uses, and other applications. By geography, the market is segmented into Brazil, Argentina, Colombia, and the rest of South America. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Pyrolysis |

| Gasification Systems |

| Other Technologies |

| Animal Farming |

| Agriculture |

| Industrial Uses |

| Other Applications |

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Technology | Pyrolysis |

| Gasification Systems | |

| Other Technologies | |

| By Application | Animal Farming |

| Agriculture | |

| Industrial Uses | |

| Other Applications | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of the South America biochar market?

The South America biochar market size stands at 53.11 kilo tons in 2026 and is expected to reach 100.39 kilo tons by 2031.

Which country leads regional production?

Brazil supplies 67.05% of the 2025 volume thanks to abundant sugarcane and forestry residues and supportive Bio-Inputs legislation.

What is the fastest-growing biochar application?

Industrial uses are expanding at a 14.16% CAGR between 2026 and 2031.

Why are carbon credits pivotal for project finance?

Biochar offsets earn premiums of USD 160-220 per ton CO₂ because they deliver 1,000-year permanence, subsidizing capital costs and shortening payback cycles.

Page last updated on: