South America Automotive Carbon Fiber Composites Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

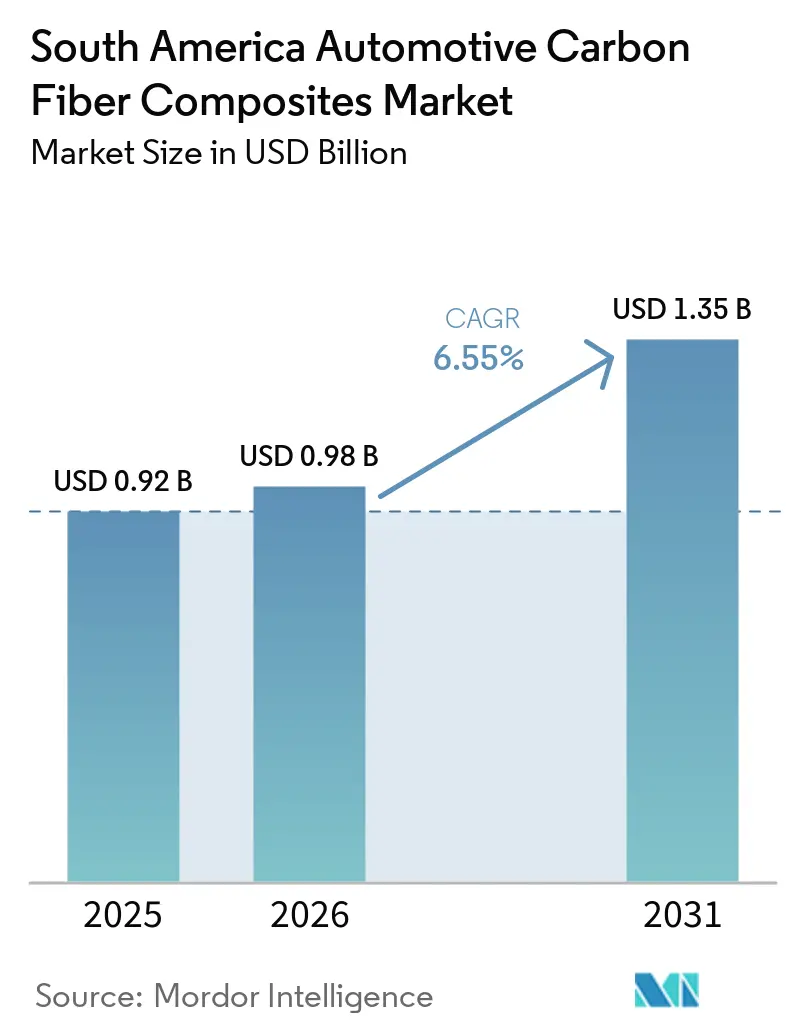

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Automotive Carbon Fiber Composites Market Analysis by Mordor Intelligence

The South America Automotive Carbon Fiber Composites Market size is projected to expand from USD 0.92 billion in 2025 and USD 0.98 billion in 2026 to USD 1.35 billion by 2031, registering a CAGR of 6.55% between 2026 to 2031. Electrification, new sustainability mandates, and the bonus-malus tax design under Brazil’s Mobilidade Verde e Inovação (MOVER) program are accelerating the substitution of steel and aluminum with carbon-fiber structures in passenger-car and light-truck platforms. Tariff relief embedded in the Mercosur-EU agreement rewards vehicles that meet recyclability thresholds, which is steering OEM materials teams toward bio-based epoxy systems and recycled fiber. Supply-chain vulnerabilities remain because no South American facility carbonizes polyacrylonitrile (PAN) precursor at a commercial scale, leaving molders exposed to acrylonitrile price swings and import-duty shifts. Skills shortages add pressure, yet recent investments in high-pressure resin transfer molding (RTM) cells and servo-driven injection presses indicate that automation is closing the gap between regional capacity and demand.

Key Report Takeaways

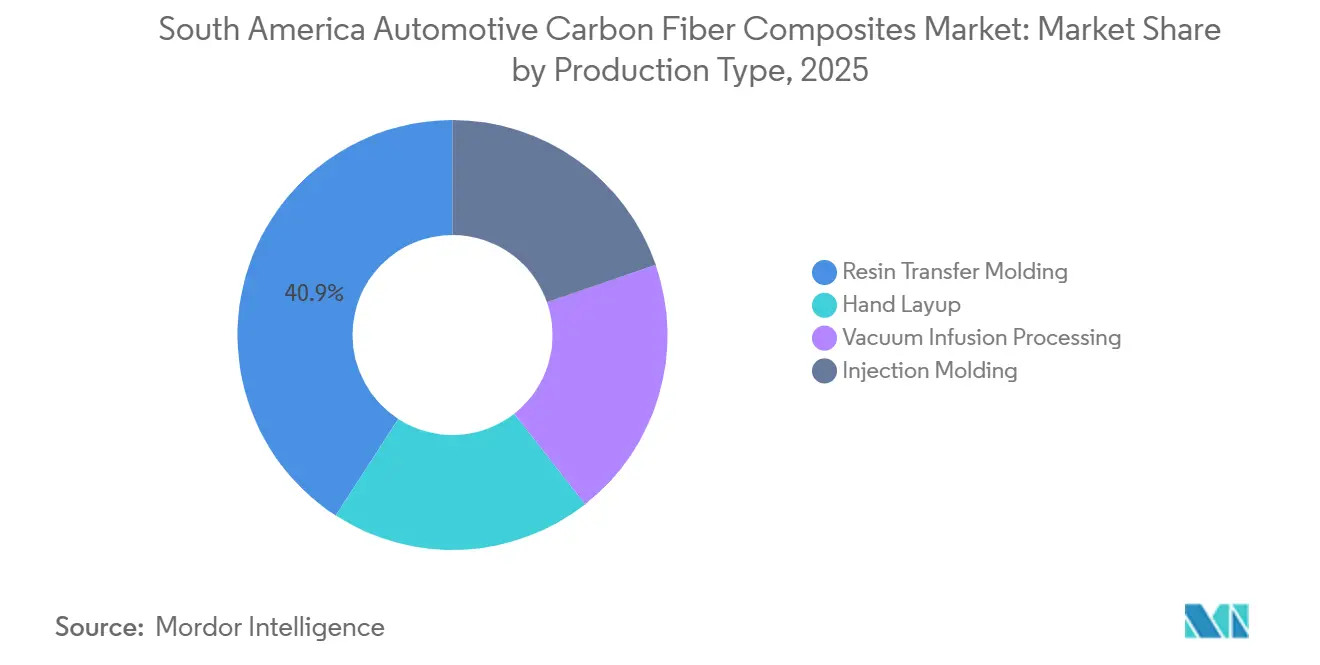

- By production type, resin transfer molding led with 40.87% of the South America automotive carbon fiber composites market share in 2025, while injection molding is projected to expand at a 6.95% CAGR through 2031.

- By application, structural assemblies captured 38.56% of the South America automotive carbon fiber composites market share in 2025; powertrain components are forecast to advance at a 7.44% CAGR through 2031.

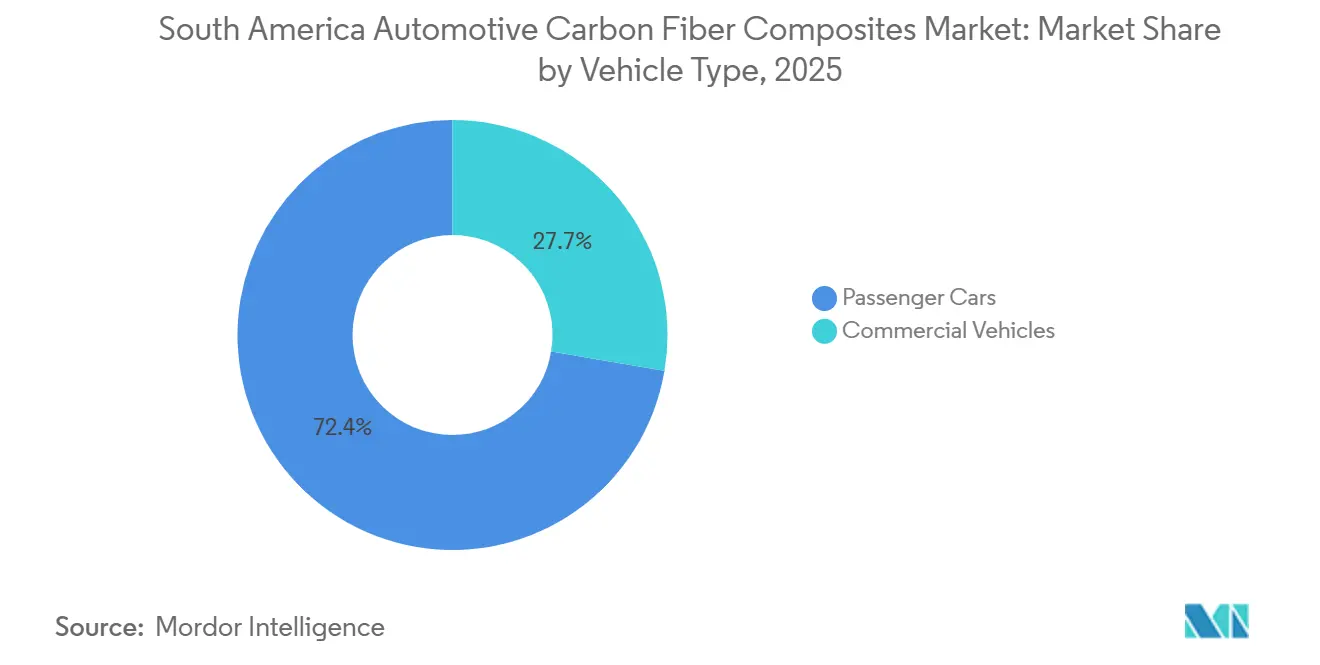

- By vehicle type, passenger cars accounted for 72.35% of the South America automotive carbon fiber composites market share in 2025 and are expected to grow at a 7.15% CAGR through 2031.

- By geography, Brazil dominated with 60.86% of the South America automotive carbon fiber composites market share in 2025 and is set to progress at a 7.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Automotive Carbon Fiber Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE-to-EV lightweighting push | +1.8% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Stringent regional CO₂-fleet targets | +1.5% | Brazil (PROCONVE L-8), Argentina | Medium term (2-4 years) |

| Government incentives for sustainable materials | +1.2% | Brazil (MOVER, Carro Sustentável), Colombia | Short term (≤ 2 years) |

| Domestic-content rules within Mercosur bloc | +0.9% | Brazil, Argentina, Paraguay, Uruguay | Long term (≥ 4 years) |

| Modular battery-pack designs demanding CFRP enclosures | +1.1% | Brazil, Argentina, with spillover to Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ICE-to-EV Lightweighting Push

Battery-electric platforms carry a 300-400 kg mass penalty versus internal-combustion counterparts, which erodes range unless chassis weight drops. Every 10% curb-weight cut extends EV range by 6-8%, and carbon fiber delivers 50-60% savings against steel in body panels and 30-35% against aluminum in structural nodes[1]SAE International, “Weight Reduction Strategies for EV Range Extension,” sae.org. Integrated press-molding that cures roof panels in under five minutes demonstrates the productivity gains now possible, making continuous-fiber parts viable once annual volumes pass 15,000 units. Latin American passenger-car demand is set to rise past 9 million units by 2035, so OEM platforms engineered for lightweighting today will bank scale benefits later. Early commercial success is visible in Brazil, where electric trucks that haul pulp for Suzano show how mass savings can raise payload without breaching axle limits.

Stringent Regional CO₂ Fleet Targets

Brazil’s Programa de Controle da Poluição do Ar por Veículos Automotores (PROCONVE) L-8 caps fleet-average emissions at 101 g CO₂/km by 2028, backed by penalties of BRL 150 per excess gram per vehicle. Automakers will incur material-neutral fines unless mass reductions offset combustion or battery penalties, so composite hoods, roof panels, and tailgates are climbing priority lists. Argentina rolled out a similar framework in 2024, though its enforcement remains uneven because currency controls complicate prepreg imports. The Mercosur-EU pact overlays lifecycle-carbon accounting on export models, nudging OEMs toward recycled fiber streams and bio-based resins that carry published environmental product declarations.

Government Incentives for Sustainable Materials

Brazil’s Carro Sustentável decree removes federal Imposto sobre Produtos Industrializados (IPI) taxes from vehicles that hold 80% recyclable content and emit under 83 g CO₂/km, a benefit that trims showroom prices by up to 12%[2]Brazilian Federal Revenue Service, “Carro Sustentável Decree Details,” receita.economia.gov.br. MOVER then layers USD 4.8 billion in R&D tax credits, 35% of which funds advanced-material integration. Syensqo’s ReGen resin family, featuring 30% bio-content, slots neatly into this incentive combo, giving molders a financing route for pilot lines in São Paulo. Colombia subsidizes 40% of composite-equipment capex, but low vehicle output delays payback and holds demand at a niche scale.

Domestic-Content Rules Within Mercosur Bloc

Autonomous tariff treatment applies only to vehicles with 60% regional value-added, propelling interest in local prepreg coating, tow spreading, and even precursor carbonization. The absence of domestic PAN capacity means molders pay 14-18% duties on imported fiber, expanding landed costs by double digits when feedstock spikes. Frasle’s Sheet Molding Compound (SMC) line in Caxias do Sul hints at how Brazilian firms can climb the value chain, yet structural-grade carbon fiber still enters through ports at a cost premium. Western suppliers that publish ISO 14001 lifecycle audits are advantaged, because the Mercosur-EU documentation requirements exceed the capabilities of many smaller processors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High carbon-fiber cost and precursor price spikes | -1.4% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Skills shortage in advanced-composite processing | -0.8% | Brazil (São Paulo, Curitiba), Argentina (Córdoba) | Medium term (2-4 years) |

| Limited acrylonitrile precursor availability regionally | -0.6% | Brazil, with spillover to Argentina | Medium term (2-4 years) |

| Uncertain Brazilian import tariff policy on PAN fibers | -0.5% | Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Carbon-Fiber Cost and Precursor Price Spikes

Carbon fiber trades at USD 15-30 per kg, many multiples above steel and aluminum, because PAN precursor forms more than half of the final production cost. Petrobras prioritized acrylic fiber over export precursor in 2025, which lifted spot PAN pricing 21% inside six months. Since a ton of fiber consumes up to 30,000 kWh, Brazil’s industrial power tariff adds nearly USD 2,700 to production cost, deterring local carbonization. Chinese large-tow grades are lower on a free-on-board basis, yet a 35% antidumping duty blocks easy arbitrage inside the bloc.

Skills Shortage in Advanced-Composite Processing

High-pressure resin transfer molding (HP-RTM), Vacuum-assisted Resin Transfer Molding (VaRTM), and automated fiber placement require technicians versed in cure kinetics and nondestructive inspection, but annual enrollment at Brazil’s leading composites course sits below 100 students. New presses installed by Bucci Composites can cycle structural parts in three minutes, though limited operator depth forces extended commissioning phases. German-Brazilian R&D partnerships promise a talent pipeline, yet graduates will not reach plant floors before 2027, so producers must automate to compensate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Type: Injection Molding Compresses Cycle Times

Injection molding’s 6.95% CAGR through 2031 shows how servo-driven presses and in-mold coatings are scaling toward 50,000 parts per year. Syensqo’s Fibreject process supports short-fiber thermoplastic housings that drop cycle times below two minutes, a critical gate for high-volume sedans in the South America automotive carbon fiber composites market. In contrast, resin transfer molding held 40.87% of the South America automotive carbon fiber composites market share in 2025. Hand Layup persists in low-volume bus and truck parts where tool amortization stays minor, but rising Brazilian wage inflation narrows its cost edge.

Vacuum Infusion splits the difference, with mid-volume battery enclosures molded in 4-8 hours and tooling costs half that of autoclaves. Toray’s next-gen press-molding could displace RTM for roof panels by 2030 if local fiber cost hurdles fall. Demand for Injection Molding aligns with passenger-car electrification because lower part cost offsets the battery premium. Producers betting on automated fiber placement still need a domestic tow-spreading line to lock in feedstock security, reinforcing the strategic case for upstream integration.

By Application Type: Powertrain Components Outpace Structures

Structural assemblies remained dominant at 38.56% share in 2025, anchored by body-in-white nodes that shave 1-2 g CO₂/km from fleet averages. Yet powertrain components are expected to accelerate at a 7.44% CAGR through 2031 because electric-motor housings, inverter cases, and battery lids must offset cell mass in the South America automotive carbon fiber composites market. Mubea Carbo Tech produces monocoques that trim 30% weight over aluminum, and though parts arrive imported today, tariff pressure is spurring talks on a Brazilian molding JV. Interiors and exteriors sit flat by comparison, hindered by cost sensitivity and glass-fiber competition, but exposed-weave finishes still command price premiums in SUVs above USD 40,000.

The application pivot aligns with policy: Brazil’s IPI exemptions reward recyclability, so composite battery boxes that combine lower thermal conductivity with closed-loop resin systems tick both safety and sustainability boxes. The South America automotive carbon fiber composites market size tied to powertrain components is therefore positioned to move ahead of structural assemblies before the close of the decade.

By Vehicle Type: Passenger Cars Hold the Major Share

Passenger cars delivered 72.35% of demand in 2025, and their 7.15% CAGR through 2031 reflects stiff fleet-average penalties that make lightweighting non-negotiable. Each composite hood and tailgate combo removes up to 60 kg, equal to 3-5 g CO₂/km under PROCONVE rules. Commercial vehicle uptake is slower, yet electric buses in Bogotá and São Paulo present niche opportunities for roof structures that lower the center of gravity and extend range. Carbon-fiber wheels show promise but still face cost barriers in freight duty cycles.

OEMs shipping more than 100,000 sedans annually could see exposure above USD 50 million if they overshoot CO₂ caps, so the South America automotive carbon fiber composites market will remain passenger-car skewed. High-volume EVs landing in 2027-2029 will intensify that bias, particularly once Brazilian molders bring injection molding and HP-RTM lines fully online.

Geography Analysis

Brazil anchors the South America automotive carbon fiber composites market with 60.86% revenue share in 2025, linked to its 2.1-million-unit car output and dense supplier corridor from São Paulo to Curitiba. The MOVER tax-credit pool and Carro Sustentável decree provide unmatched fiscal pull, and IPT’s Lightweight Structures Laboratory offers local Automated Fiber Placement (AFP), RTM, and VaRTM validation. Domestic demand also benefits from the 101 g CO₂/km fleet target that forces OEMs to lightweight popular SUVs and pickup trucks.

Argentina struggles to scale composites while inflation tops 40% and import financing tightens. Prepreg deliveries face 8-12 week transit plus currency-hedge charges, so molders limit orders to motorsport and premium trim niches. The country’s policy ambition matches Brazil’s on paper, yet capital scarcity delays plant investments that would localize supply.

Colombia’s 80,000-unit assembly base limits upside, but electric-bus fleets make the country a testbed for Carbon Fiber Reinforced Polymer (CFRP) roof segments and battery enclosures. Law 1964 incentives have spurred early demand, though the absence of tier-one suppliers keeps part count low. Chile, Peru, Paraguay, and Ecuador collectively represent the remaining volume, mainly in mining-truck and agricultural fairings that prize weight savings under rough-road duty cycles.

Competitive Landscape

The South America automotive carbon fiber composites market remains moderately fragmented, with the five largest companies being Toray Industries, Inc., SGL Carbon, Syensqo, Hexcel Corporation, and Mitsubishi Chemical Carbon Fiber and Composites, Inc. Toray, Hexcel, SGL Carbon, and Mitsubishi Chemical ship fiber and prepreg into the region but operate no local carbonization lines, so value capture skews overseas and import duties cut regional margins. Bucci Composites and NTC Composites run HP-RTM and VRTM cells in Brazil, yet they depend on European feedstock subject to 14%-18% customs charges. Syensqo’s agreement with Fairmat to recycle scrap at its German plant creates a compliance-ready stream of secondary fiber that could land in Brazil without antidumping duties, offering a hedge against virgin-fiber volatility.

Frasle’s Smart Composites line is Brazil’s first home-grown play, focusing on non-structural SMC parts that slash trailer weight by more than half. The strategic gap remains upstream: no firm produces PAN precursor in South America, leaving the door open for a vertically integrated entrant that marries fiber conversion with HP-RTM capacity next to OEM assembly hubs. Cost-down pressure is also rising from Chinese large-tow suppliers, but the 35% antidumping barrier shields domestic pricing, at least through 2027.

South America Automotive Carbon Fiber Composites Industry Leaders

Hexcel Corporation

TORAY INDUSTRIES, INC.

SGL Carbon

Mitsubishi Chemical Carbon Fiber and Composites, Inc.

Syensqo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Hyundai Motor Group and TORAY INDUSTRIES, INC. signed a joint development agreement to focus on advanced materials and components designed for future mobility applications. This collaboration is expected to influence the South America automotive carbon fiber composite market by fostering the development of high-performance composites for vehicles, enhancing their efficiency and functionality.

- June 2025: Researchers from the National Renewable Energy Laboratory (NREL), as part of the BOTTLE consortium, developed a method to fully recycle carbon fiber composites. This cost-effective process, utilizing hot acetic acid to break down epoxy-amine resins, is expected to influence the South American automotive carbon fiber composite market by enabling the recovery of high-strength carbon fibers and chemical components.

South America Automotive Carbon Fiber Composites Market Report Scope

Automotive carbon fiber composites (CFRP) are high-performance materials composed of carbon fibers embedded in a polymer resin. They provide exceptional strength-to-weight ratios, being approximately 70% lighter than steel and 40% lighter than aluminum. These composites contribute to improved fuel efficiency, enhanced structural integrity, and play a crucial role in extending the range of electric vehicles (EVs).

The South America Automotive Carbon Fiber Composites Market is segmented into production type, application type, vehicle type, and geography. By production type, the market is segmented into resin transfer molding, hand layup, vacuum infusion processing, and injection molding. By application type, the market is segmented into structural assemblies, power-train components, interiors, and exteriors. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By geography, the market is segmented into Brazil, Argentina, Colombia, and rest of South America. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Resin Transfer Molding |

| Hand Layup |

| Vacuum Infusion Processing |

| Injection Molding |

| Structural Assemblies |

| Power-train Components |

| Interiors |

| Exteriors |

| Passenger Cars |

| Commercial Vehicles |

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Production Type | Resin Transfer Molding |

| Hand Layup | |

| Vacuum Infusion Processing | |

| Injection Molding | |

| By Application Type | Structural Assemblies |

| Power-train Components | |

| Interiors | |

| Exteriors | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of the South America automotive carbon fiber composites market?

The South America automotive carbon fiber composites market stands at USD 0.98 billion in 2026 and is forecast to reach USD 1.35 billion by 2031.

Which production type is expanding fastest through 2031?

Injection molding is advancing at a 6.95% CAGR to 2031 as servo-driven presses compress part cycle times.

How much revenue share does Brazil contribute in 2025?

Brazil commands 60.86% of the South American demand in 2025.

What policy measures are boosting composite adoption in passenger vehicles?

Brazil’s PROCONVE L-8 fleet-average CO₂ cap and the Carro Sustentável tax exemption directly reward lightweight, recyclable vehicle designs.

Page last updated on: