South America Air Freight Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

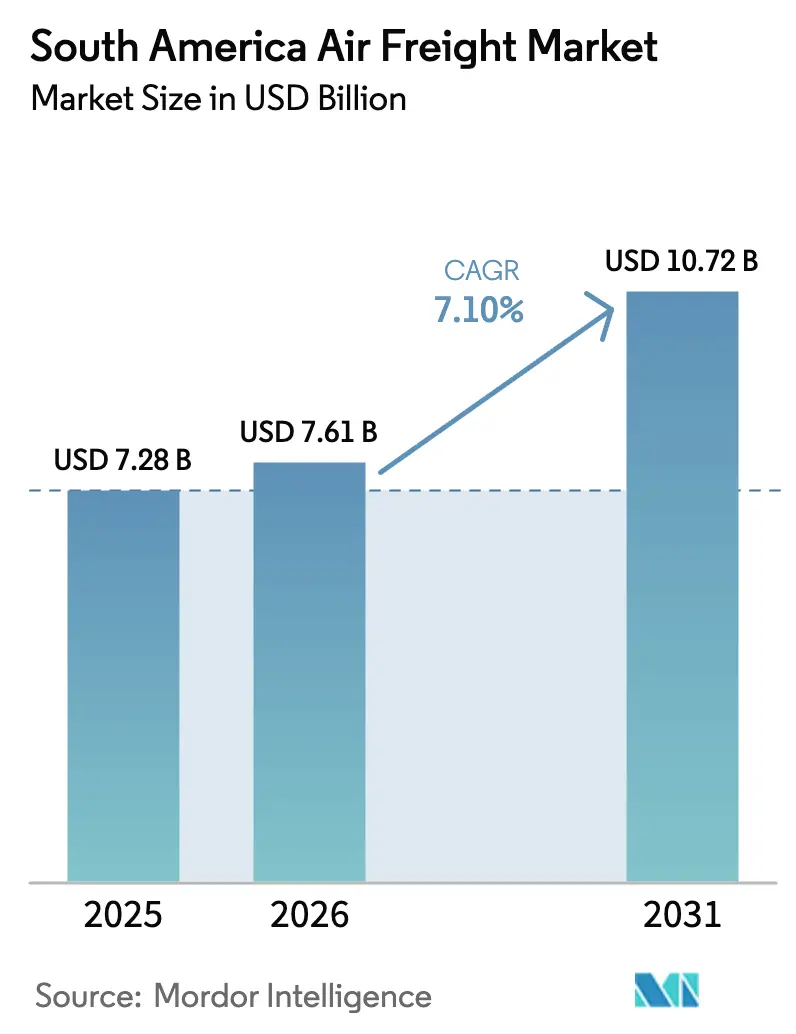

| Base Year Market Size (2025) | USD 7.28 Billion |

| Market Size (2026) | USD 7.61 Billion |

| Market Size (2031) | USD 10.72 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

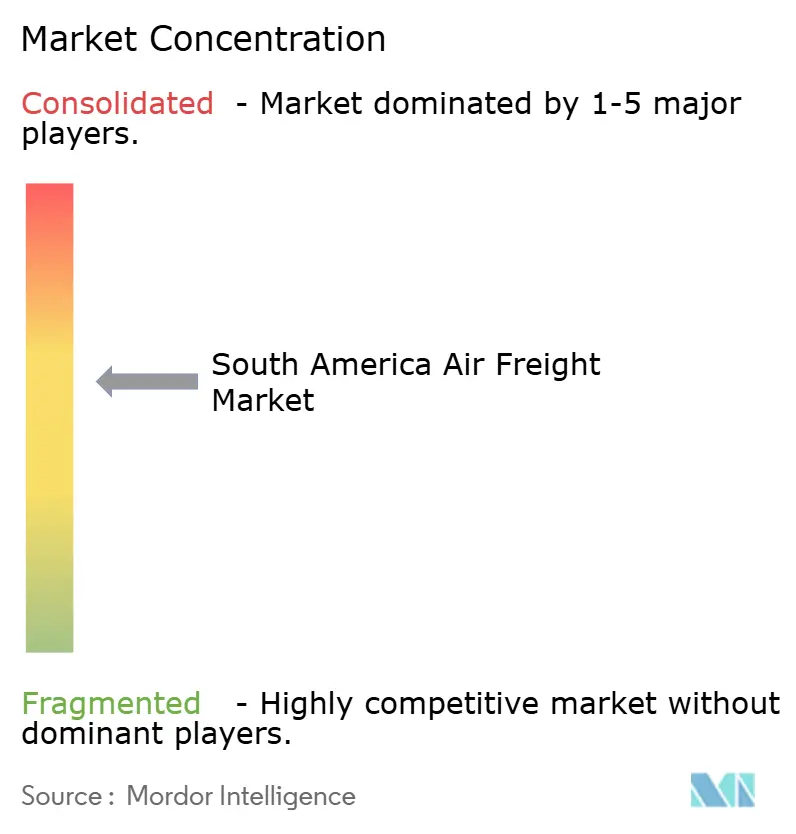

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Air Freight Market Analysis by Mordor Intelligence

The South America Air Freight Market size is expected to increase from USD 7.28 billion in 2025 to USD 7.61 billion in 2026 and reach USD 10.72 billion by 2031, growing at a CAGR of 7.10% over 2026-2031.

Expanded single-window customs portals, swelling e-commerce parcel volumes, and a younger fleet of converted freighters are supporting structural, not merely cyclical, expansion of the South America air freight market. Brazil accounted for 46.47% of regional revenue in 2025, yet Peru is forecast to record the fastest 9.23% CAGR through 2031, thanks to a new Jorge Chavez cargo terminal and a surge in agro-exports. International shipments held a 68.24% share in 2025, though domestic flows are accelerating at 8.41% annually as Mercado Libre, Magazine Luiza, and other platforms replicate Amazon-style hub-and-spoke models. Freight transport (Cargo/CEP) contributed 44.81% of 2025 service revenue, but other value-added services are expanding at 7.89% CAGR as shippers pay premiums for customs API integration, insurance, and real-time exceptions handling.

Key Report Takeaways

- By service, freight transport held 44.81% of the South America air freight market size in 2025, whereas other value-added services are projected to register a 7.89% CAGR through 2031.

- By destination, international shipments captured 68.24 of % South America air freight market share in 2025; domestic flows are advancing at an 8.41% CAGR during 2026-2031.

- By carrier type, belly cargo accounted for 56.87% of the South America air freight market size in 2025, yet dedicated freighters are forecast to grow at a 7.63% CAGR thanks to A321 P2F and 767 BCF additions.

- By cargo type, general cargo represented a 61.33% share in 2025, while special cargo, including pharmaceuticals and lithium batteries, is poised for an 8.62% CAGR.

- By end-use industry, e-commerce and retail accounted for 30.92% of the South America air freight market size in 2025, and Perishables and Fresh Produce are the fastest climbers at an 8.76% CAGR through 2031.

- By geography, Brazil led with 46.47% of South America air freight market share in 2025, yet Peru delivers the region’s quickest 9.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Air Freight Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming Cross-Border E-Commerce Parcels | +1.3% | Brazil, Argentina, Chile, with spillover to Colombia and Peru | Short term (≤ 2 years) |

| Rapid Growth of Pharma Cold-Chain Exports | +1.1% | Brazil, Chile, Colombia, plus secondary gains in Peru and Argentina | Medium term (2-4 years) |

| Rise in Near-Shoring of Electronics Assembly | +0.6% | Brazil, Argentina, and limited in Chile and Colombia | Long term (≥ 4 years) |

| Implementation of Single-Window Customs Systems | +0.9% | Brazil, Peru, Colombia, Chile, and Argentina are lagging | Short term (≤ 2 years) |

| Fleet Renewal Toward Fuel-Efficient Freighters | +0.8% | Region-wide, led by LATAM, Azul, Avianca | Medium term (2-4 years) |

| Free-Trade-Zone Expansion Around Secondary Airports | +0.7% | Colombia, Uruguay, Chile; emerging in Peru and Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Cross-Border E-Commerce Parcels

Parcel flows looking for 24- to 48-hour delivery are propelling the South America air freight market. Regional e-commerce sales exceeded USD 190 billion in 2025 and should top USD 200 billion in 2026, with cross-border orders rising as Argentine, Chilean, and Colombian shoppers buy from Brazilian merchants[1]McKinsey & Company, “Latin America’s E-Commerce Opportunity,” mckinsey.com. Mercado Libre invested USD 13.2 billion in logistics for 2025, contracting Azul Cargo and GOLLOG to guarantee one-day delivery on trunk routes. Peak-season surges push parcels off passenger bellies onto freighters such as Azul’s A321 P2F, which cuts truck transit by two days on São Paulo-Brasília-Manaus corridors. The entire South America air freight market benefits from the consistent density these parcels deliver year-round.

Rapid Growth of Pharma Cold-Chain Exports

A decade ago, outbound pharmaceuticals were niche; today, they underpin special-cargo uplift in the South America air freight market. Brazil’s regulated cold-chain pharma segment will double to more than USD 1 billion by 2030. Avianca Cargo earned IATA CEIV Pharma certification in 2024 and now loads active temperature-controlled containers that earn 20-25% yield premiums. Similar investments by LATAM and DHL create a virtuous circle: stricter handling unlocks larger contracts, lifting revenue quality across the South America air freight industry.

Rise in Near-Shoring of Electronics Assembly to South America

FDI into Brazil’s Manaus free zone reached USD 3.8 billion in 2024. While most finished units remain for domestic sale, inbound semiconductor and battery flows already move by air, and incremental board fabrication tightens capacity on intra-regional lanes. Weak Argentine demand and policy risk still curb scaling, limiting near-shoring’s contribution to the wider South America air freight market to roughly +0.6% on forecast CAGR.

Implementation of Single-Window Customs Systems

Customs digitalization compresses door-to-door times that previously muted the air advantage. Brazil’s Siscomex Remessa clears parcels in 18 hours on average. Peru’s VUCE sliced export formality by 30%, vaulting Lima’s blueberries to United States shelves within 36 hours of harvest. Combined, these upgrades reinforce the South America air freight market’s competitiveness against ocean and ground options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Airport Infrastructure Bottlenecks | -0.9% | Sao Paulo, Lima, Santiago, Bogota, plus Buenos Aires | Short term (≤ 2 years) |

| Currency-Exchange Volatility Impacting Rates | -0.7% | Argentina, Brazil; moderate in Colombia, Chile, Peru | Short term (≤ 2 years) |

| Stringent Wildlife & Agro-Sanitary Inspection Delays | -0.5% | Chile, Peru, Colombia, Ecuador; United States & EU entry points | Medium term (2-4 years) |

| High Jet-Fuel Price Pass-Through to Shippers | -0.6% | Region-wide, sharpest for smaller carriers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Airport Infrastructure Bottlenecks

Runway closures and constrained parking availability at key South American hubs like Guarulhos (GRU), Lima (LIM), Santiago (SCL), and Bogota are creating persistent 15-20 minute delays for taxiing aircraft, driving up ground handling costs by 10-15% amid already tight airport infrastructure. Meanwhile, long-awaited cargo terminal upgrades at Lima's Jorge Chavez International Airport have been postponed to 2027, severely limiting near-term capacity to absorb growing air freight volumes despite robust demand expansion across the South American air cargo market.

Currency-Exchange Volatility Impacting Rates

The Argentine peso’s 54% step-devaluation in December 2023 compelled carriers to urgently reprice customer contracts in dollars while continuing to compensate staff in rapidly weakening pesos, severely squeezing operational margins. Similarly, sharp swings in Brazil’s real prompted a 12% fuel surcharge increase in Q1-2025, as fiscal concerns eroded currency stability. Such persistent currency volatility across the region undermines margin predictability and long-term planning throughout the South America air freight market segment Analysis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Services Gain Momentum

Value-added services covering customs brokerage, insurance, and real-time tracking are expected to post a 7.89% CAGR, outstripping freight transport’s growth through 2031. Freight transport still delivered 44.81% of South America air freight market share in 2025, yet rising digital compliance demands nudge shippers toward integrated solutions that cost 10-15% more but eliminate paperwork. DHL’s MyGTS, launched region-wide in 2024, links directly into Brazil, Peru, and Colombia’s customs APIs, trimming clearance paperwork by 70%[2]DHL Global Forwarding, “MyGTS Platform,” dhl.com. Kuehne + Nagel’s blockchain ePOD, available in Argentina and Brazil since 2025, accelerates proof of delivery by 2 hours, reducing invoice cycles for time-sensitive pharmaceuticals. These platforms redefine the South America air freight market from commodity lift to visibility-rich logistics.

Freight forwarding, though smaller than transport, is consolidating as manual brokers exit under the twin pressures of API customs clearance and capital-intensive IT. Global players like Expeditors and DSV capture vacated share by bundling air with ocean and road freight, and cross-docking, an approach attractive to multinationals hedging against volatility in the South American air freight market.

By Destination: Domestic Lanes Accelerate

International uplift remains dominant at 68.24%, but domestic air freight is forecast to compound at 8.41% CAGR as consumer expectations pivot to next-day delivery even across Brazil’s continental distances. Azul Cargo’s A321P2F provides 27 tonnes of payload, shrink-wrapping Manaus electronics dispatch to Sao Paulo’s SE marketplace inside 24 hours. In 2025, GOLLOG’s dedicated 737 800 BCF freighter fleet for Mercado Libre expanded to eight aircraft, helping the unit move more than 170,000 tons of cargo for the year, around 12.4 percent more tonnage than in 2024. The domestic boom enlarges the South America air freight market without cannibalizing long-haul corridors, a dual-engine dynamic supporting steady fleet utilization.

International demand still anchors yields. LATAM’s 767 freighters log superior load factors on Brazil-United States lanes, while Chile-Asia exports of cherries and salmon depend on freighters because passenger frequencies remain sparse. The blended network allows carriers to balance domestic growth with global trade volatility, reinforcing resilience in the South America air freight market.

By Carrier Type: Freighters Climb the Share Ladder

Belly capacity controlled 56.87% of total tonnage in 2025, but its share will erode as passenger wide-bodies remain below pre-2020 levels. Dedicated freighters, forecast to grow 7.63% CAGR, plug the gap, particularly during Valentine’s Day and Mother’s Day flower peaks in Bogota. Avianca’s A330-200Fs and A330 P2Fs handled more than 100,000 tons of Colombian flowers in 2025. The freighter surge underpins schedule certainty, essential to premium perishables and the broader South America air freight market.

Still, bellies thrive on dense Brazil-United States routes where wide-body passenger flights resumed early. Price-sensitive apparel and electronics importers often accept the lower priority of bellies, preserving a sizable but no longer dominant share in the South America air freight industry.

By Cargo Type: Special Cargo Delivers Premium Yields

General cargo held a 61.33% share in 2025, but special cargo is projected to expand at an 8.62% CAGR as regulators tighten lithium-battery rules and drug makers escalate biosimilar exports. Avianca and LATAM use CEIV-certified corridors with IoT temperature monitors, charging 20-25% premiums that lift average yields across the South America air freight market. Live-animal moves mainly involve pedigree cattle and aquaculture broodstock; they also favor carriers with trained staff and specialized pens, offering another protected niche.

General cargo remains critical for volume density. E-commerce parcels, textiles, and automotive parts fill day-to-day capacity; however, rate competition erodes margins. To hedge, carriers prioritize special cargo on trunk lanes, granting overflow space to commoditized lifts, a balancing act that sustains profitability in the South America air freight market.

By End-Use Industry: Perishables Lead Growth Curve

Perishables and fresh produce will lead South America’s air freight market, growing at an 8.76% CAGR through 2031. Although e-commerce parcels held the largest revenue share at 30.92% in 2025, their growth is stabilizing as fulfillment networks mature. The perishables surge is driven by high-value exports. Chile shipped 1.1 million tons of fruit in 2023-24, 30% by air to major global markets, while Peru’s avocado and mango exports topped USD 1.7 billion in 2025. Flowers from Colombia, shrimp from Ecuador, and gourmet beef from Uruguay further diversify the region’s perishables portfolio.

Manufacturing and high-tech segments remain cyclical, influenced by currency movements and regional GDP trends, yet demand for just-in-time automotive parts continues to sustain high-yield emergency charter operations.

Geography Analysis

Brazil, with 46.47% of the South American air freight market share in 2025, retains primacy through sheer scale. Guarulhos is investing USD 250 million to add 50,000 m² warehouse space and eight freighter stands by 2029[3]GRU Airport, “Cargo Expansion,” gru.com.br. Azul Cargo, leveraging Amazon as anchor client, already claims 35% of domestic payload and together with GOLLOG’s 737-800 BCFs makes Brazil’s internal skies the busiest within the South America air freight market. Currency tremors remain an operational wild card, but continuous e-commerce demand cushions downside exposure.

Peru posts the region’s fastest 9.23% CAGR through 2031, as Jorge Chavez’s phased cargo expansion lifts capacity by 40% by 2027. Single-window VUCE trimmed agro-export clearance 30%, enabling blueberries to land in Miami within 36 hours of harvest. Private cold-storage operators, including DHL and Kuehne + Nagel, opened a 5,000 m² temperature-controlled space in 2025, broadening the South America air freight market’s perishables pipeline.

Runway resurfacing at Santiago cut freighter slots by 30% in Q2-2025, prompting LATAM Cargo to divert to Iquique and Antofagasta. Nevertheless, high-value cherry charters to Shanghai, supported by a 72-hour delivery promise, keep Chile integral to the South America air freight industry. Cold-storage improvements at ocean ports could shift some volume back to sea, but top-grade fruit will remain airborne.

Competitive Landscape

Moderate concentration defines the South America air freight market. The top five carriers, LATAM Cargo, Azul Cargo, DHL Aviation, FedEx Express, and UPS Airlines, together held a majority of shares in 2025. LATAM’s 21 Boeing 767 BCFs anchor Brazil-United States and Chile–Europe corridors and generated USD 1.2 billion revenue in 2023[4]LATAM Airlines Group, “Investor Update,” latamairlinesgroup.net. DHL, FedEx, and UPS leverage proprietary hubs and customs APIs to court e-commerce and pharma shippers, while Avianca Cargo’s Amazon partnership strengthens its cross-border parcel appeal.

Strategic moves skew toward digitalization. DHL’s MyGTS logged 40% shipper adoption by late 2025, cutting clearance delays by 25%. Kuehne + Nagel scaled its blockchain ePOD to six South American stations, accelerating receivables and shrinking disputes. Cold-chain differentiation is another battleground: LATAM’s Pharma Corridor offers blockchain chain-of-custody and real-time temperature alerts, winning contracts with Roche, Pfizer, and Novartis. Secondary-airport specialization provides white space for niche operators like GOLLOG, Aerosucre, and Sky Airline Cargo that value spool-up flexibility over scale in the South America air freight market.

Capital discipline remains mixed. LATAM focuses on standardized 767s; Avianca prefers a split A330F/P2F mix; Azul eyes narrow-body conversions to flood domestic routes. Integrators bankroll ground infrastructure instead, widening service depth. The multitrack investment thesis implies durable competition yet leaves enough margin headroom for regional specialists that master local currency hedging and regulatory nuance within the South America air freight industry.

South America Air Freight Industry Leaders

LATAM Cargo

Avianca Cargo

DHL Aviation

FedEx Express

Azul Cargo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Avianca Cargo and Amazon Air formed a strategic alliance to route parcels through Bogota’s Eldorado hub, adding new Colombia–Peru and Colombia–Ecuador freighter sectors.

- February 2025: Mercado Libre earmarked USD 13.2 billion for logistics, deepening air partnerships with Azul Cargo and GOLLOG across Brazil.

- December 2024: DHL opened a 5,000 m² cold-chain hub at Santiago Airport to target fruit and pharma traffic.

- December 2024: Peru’s new passenger terminal at Jorge Chavez began initial cargo operations; a dedicated cargo building will phase in by 2027.

South America Air Freight Market Report Scope

| Freight Transport (Cargo/CEP) |

| Freight Forwarding |

| Other Value-Added Services (Customs Brokerage, Insurance, etc.) |

| Domestic |

| International |

| Belly Cargo |

| Freighter |

| General Cargo |

| Special Cargo |

| E-commerce and Retail |

| Manufacturing and Automotive |

| Healthcare and Pharmaceuticals |

| Perishables and Fresh Produce |

| High-Tech and Electronics |

| Others |

| Argentina |

| Brazil |

| Chile |

| Peru |

| Colombia |

| Rest of South America |

| By Service | Freight Transport (Cargo/CEP) |

| Freight Forwarding | |

| Other Value-Added Services (Customs Brokerage, Insurance, etc.) | |

| By Destination | Domestic |

| International | |

| By Carrier Type | Belly Cargo |

| Freighter | |

| By Cargo Type | General Cargo |

| Special Cargo | |

| By End-Use Industry | E-commerce and Retail |

| Manufacturing and Automotive | |

| Healthcare and Pharmaceuticals | |

| Perishables and Fresh Produce | |

| High-Tech and Electronics | |

| Others | |

| By Country | Argentina |

| Brazil | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

How large will the South America air freight sector be by 2031?

The South America air freight market size is projected to reach USD 10.72 billion by 2031, up from USD 7.61 billion in 2026.

Which country is expanding fastest in regional air cargo?

Peru is forecast to post a 9.23% CAGR through 2031, buoyed by its new Jorge Chávez cargo terminal and diversified agro-exports.

Which cargo type delivers the highest yield growth?

Special cargo chiefly pharmaceuticals, live animals, and lithium batteries will rise at an 8.62% CAGR, commanding premiums of 20-40% over general cargo.

Why are airlines adding dedicated freighters?

Reduced passenger wide-body fleets, plus perishable peak periods, have spurred carriers to deploy converted 767, A330, and A321 freighters for schedule certainty and greater payload flexibility.

How do currency swings affect freight rates?

Volatile currencies like the Argentine peso and Brazilian real prompt carriers to shorten contract tenors and lift fuel surcharges, shifting risk to shippers and tightening budgets.

What technology upgrades are most valued by shippers today?

Real-time tracking, blockchain-verified proof of delivery, and API links to single-window customs systems are cutting clearance times and supplying end-to-end visibility that earns service premiums.

Page last updated on: