South Africa Pet Treats Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

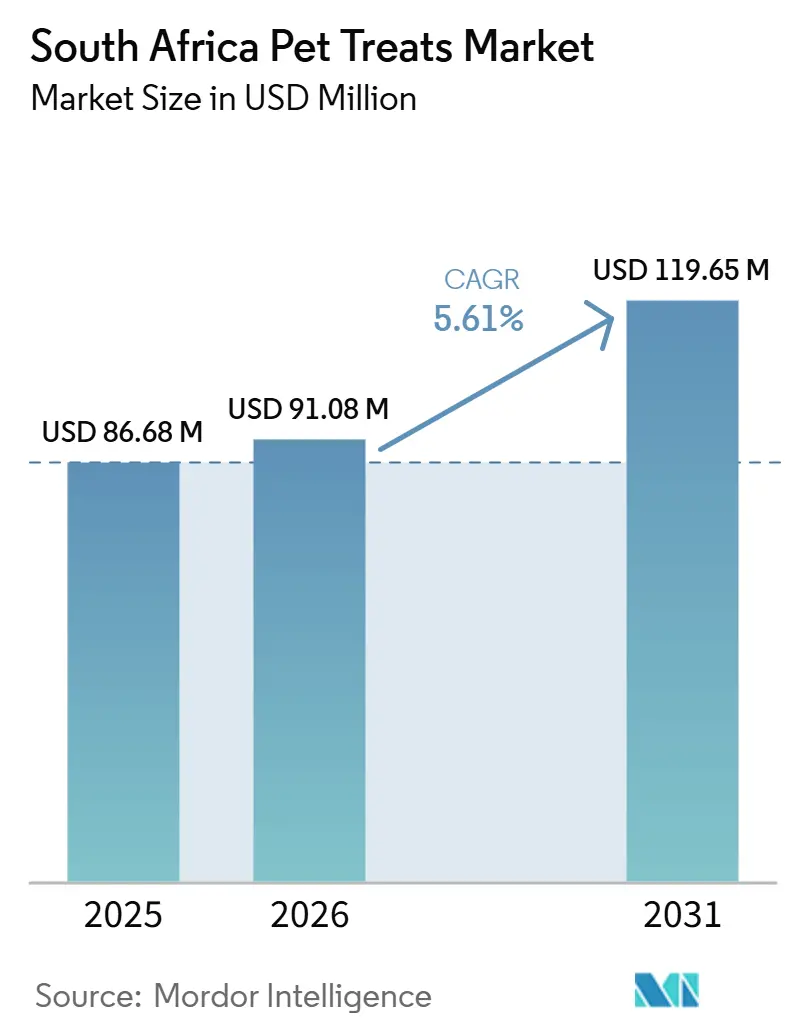

| Base Year Market Size (2025) | USD 86.68 Million |

| Market Size (2026) | USD 91.08 Million |

| Market Size (2031) | USD 119.65 Million |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

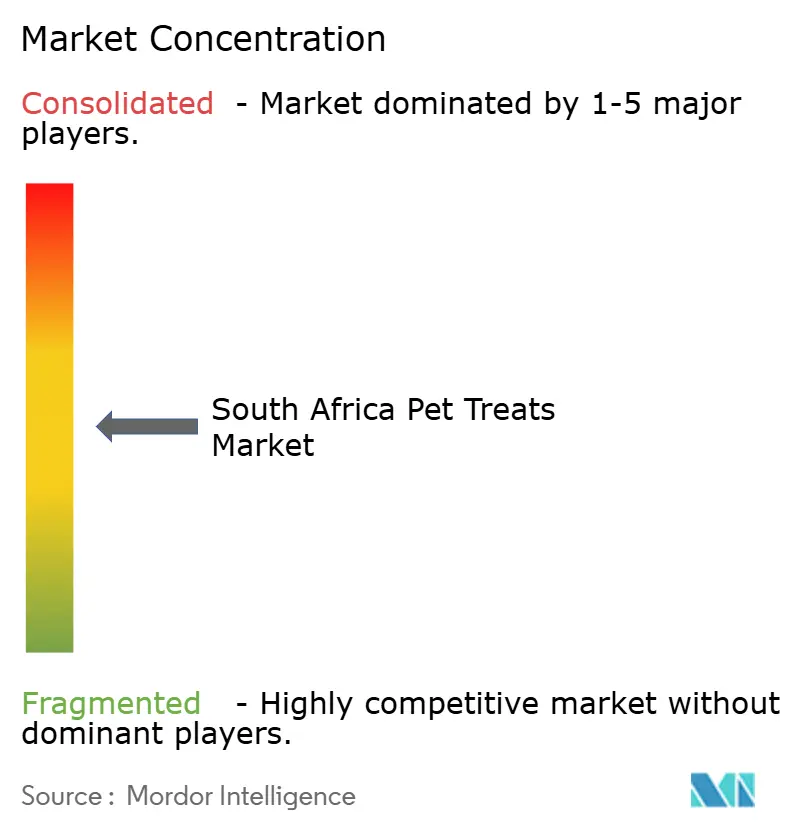

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Pet Treats Market Analysis by Mordor Intelligence

The South Africa pet treats market was valued at USD 86.7 million in 2025 and is estimated to grow from USD 91.1 million in 2026 to USD 119.7 million by 2031, at a CAGR of 5.61% during the forecast period 2026-2031. Statistics South Africa's General Household Survey 2025, released in June 2026, confirms a broad companion animal base with 7.4 million dogs across 4.2 million households and 2 million cats across 1.3 million households, providing the market with a large and stable demand base. Pet spending has also become difficult for many households to reduce, with 45% of owners classifying monthly pet spending as essential, which supports market resilience relative to many other consumer categories. Demand is shifting toward more purposeful purchases, as owners seek products linked to oral health, joint support, cleaner ingredients, and greater ingredient transparency, influencing product design and pricing across the market. Distribution is also expanding through large grocery chains, specialist retail, and same-day fulfillment, while local manufacturers with export-grade quality systems are strengthening their position in premium segments. The outlook remains tempered by protein inflation, mainstream price sensitivity, and supply disruption following RCL Foods' late 2025 recall, which has kept shelf space and competitive positions in flux through 2026.

Key Report Takeaways

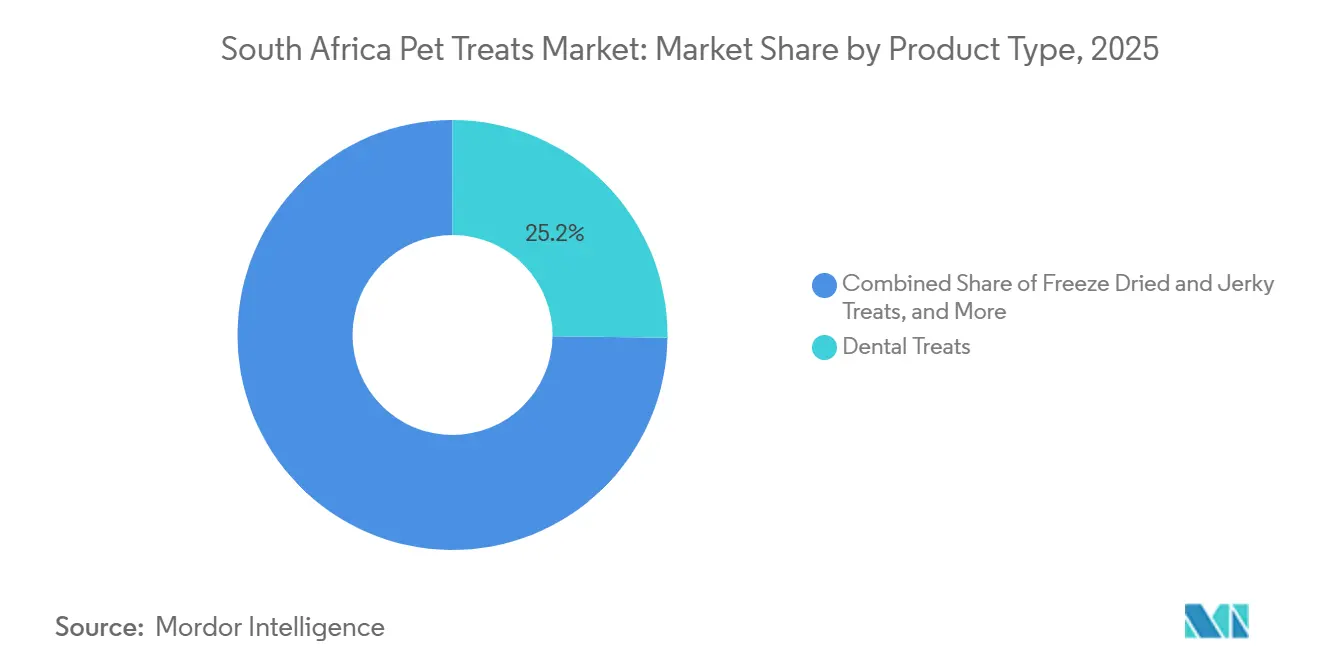

- By product type, dental treats led with 25.2% of the South Africa pet treats market share in 2025, while freeze-dried and jerky treats are forecast to expand at a 6.6% CAGR between 2026 and 2031 in the South Africa pet treats market.

- By pet type, dogs held 79% of the South Africa pet treats market share in 2025, while cats recorded the highest projected CAGR at 6.2% between 2026 and 2031.

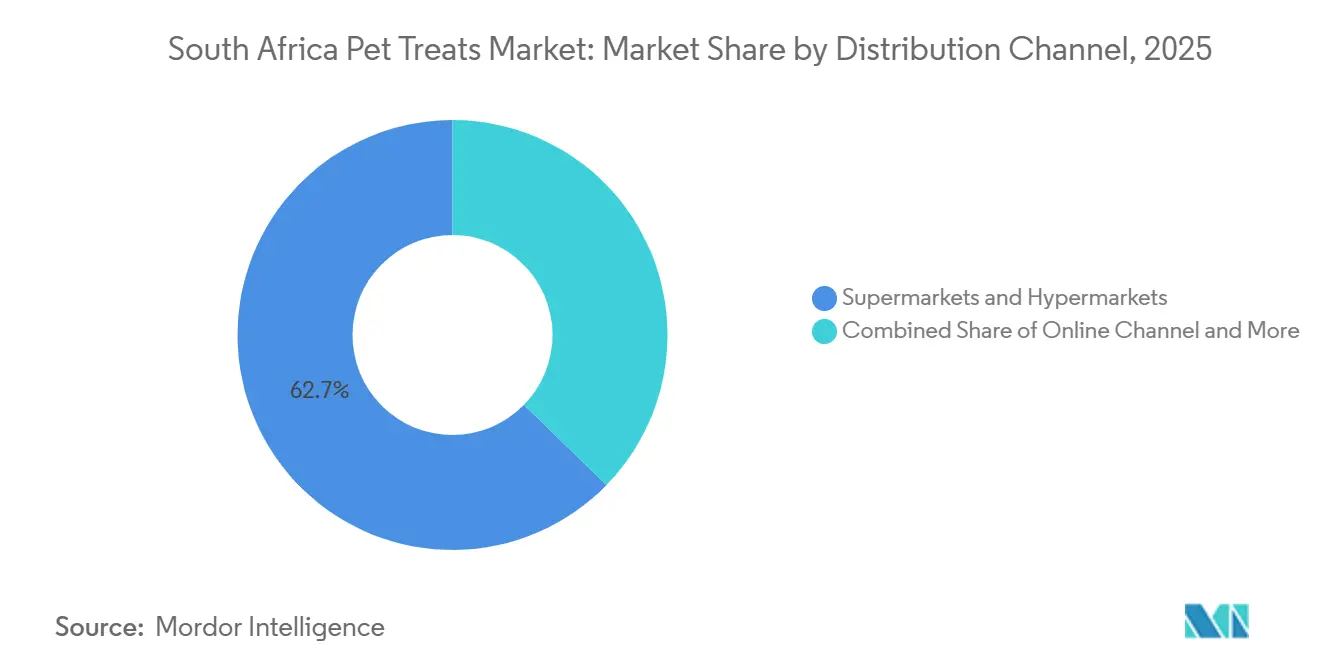

- By distribution channel, supermarkets and hypermarkets accounted for 62.7% of the South Africa pet treats market size in 2025, while specialty stores are advancing at a 6.5% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Pet Treats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Humanization and premiumization of pet diets | +1.4% | Global, with South Africa demand concentrated in Gauteng and Western Cape urban corridors | Short term (≤ 2 years) |

| Rising demand for dental and functional treats | +1.1% | National, led by urban metros and veterinary referral networks | Medium term (2-4 years) |

| Expansion of online replenishment and quick-commerce fulfillment | +0.8% | National, with early gains concentrated in Gauteng, Western Cape, and Eastern Cape | Short term (≤ 2 years) |

| Retailer private-label expansion in mass channels | +0.6% | National, across major grocery and specialist retail chains | Medium term (2-4 years) |

| Sustainability-led use of upcycled animal by-products | +0.4% | South Africa, with spillover to wider Southern African Development Community (SADC) and export markets | Long term (≥ 4 years) |

| Veterinary endorsement of specialized treat formats | +0.5% | National, urban-led and aligned with veterinary clinic density | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Humanization and Premiumization of Pet Diets

The South Africa pet treats market is benefiting from a shift in how owners view pets within the household. Pets are increasingly treated as family members, driving higher interest in treats that offer quality, wellness, and emotional value beyond simple indulgence. This has broadened purchasing patterns from a single core food purchase to a basket that also includes treats, functional toppers, and wet formats, lifting purchase frequency and spend across the South Africa pet treats market. Spending remains uneven across income groups, with the strongest premium uptake concentrated in higher-income urban households where brand loyalty and format trial are more established. Montego Pet Nutrition's 2024 launch of 49 new products, including PURE Collagen Protein treat formulations with hydrolyzed collagen for joint stability, illustrates how manufacturers are targeting this more aspirational buyer base with specialized propositions[1]Source: PetfoodIndustry, "Montego Pet Nutrition: 25 years of being “Better Every Day,” petfoodindustry.com.

Rising Demand for Dental and Functional Treats

Dental treats represent the largest functional segment in the South Africa pet treats market, holding a 25.2% value share in 2025. Their market position is supported by a clear value proposition, as owners can justify the purchase as both a reward and an oral care product, giving retailers and veterinarians a stronger basis for recommendation. The Veterinary Oral Health Council seal has become an important trust marker in this space, with Pedigree Dentastix receiving acceptance for plaque and tartar control in 2024 and Blue Buffalo Dental Chews following in 2025. Functional positioning is also expanding beyond oral care into joint support, digestive support, and skin and coat support, which drives repeat purchases and supports stronger pricing in the South Africa pet treats market. The clinical and regulatory requirements associated with health claims favor larger players that can manage product testing, veterinary relationships, and compliance work, limiting opportunities for smaller local brands competing on health claims alone.

Expansion of Online Replenishment and Quick-Commerce Fulfillment

Digital convenience is changing how routine purchases are made in the South Africa pet treats market, particularly in major urban areas. Petshop Science launched in 2021 and had reached 143 stores across 8 provinces by mid-2025, establishing a strong physical presence before adding faster fulfillment options. This arrangement favors dependable, repeat-purchase items such as dental sticks, training treats, and portioned soft chews, as convenience-driven shoppers tend to prioritize replenishment over in-store browsing. As a result, placement within a quick-commerce catalog is becoming a more important distribution channel in the South Africa pet treats market than many traditional in-store secondary displays.

Veterinary Endorsement of Specialized Treat Formats

Veterinary influence is playing a larger role in the South Africa pet treats market as owners place more weight on science-backed positioning. Scientifically backed ingredients shape the dog and cat owner purchase decisions in South Africa, which helps explain the rising value of clinical claims and ingredient transparency in this market. Veterinary endorsement tends to convert occasional treat buyers into more regular buyers who focus on efficacy, label clarity, and product purpose rather than flavor novelty alone. Virbac's CET Veggiedent FR3SH dental chews, sold through veterinary channels and carrying Veterinary Oral Health Council (VOHC) acceptance for plaque and tartar control, demonstrate how multinational brands combine clinic access with clinical positioning in the South Africa pet treats market. This raises the entry barrier for smaller domestic suppliers, as veterinary sales coverage and supporting trial data are harder to fund, keeping premium functional leadership concentrated among a limited group of better-resourced players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Protein input inflation and margin pressure | -1.2% | Global supply shock, acutely felt in South Africa due to rand weakness and local protein supply disruption | Short term (≤ 2 years) |

| Price sensitivity in mainstream households | -0.9% | National, especially in mass market channels and non-metro regions | Medium term (2-4 years) |

| Compliance burden for functional and novel ingredients | -0.5% | National, with added complexity for export market compliance | Medium term (2-4 years) |

| Homemade treat substitution and informal feeding habits | -0.3% | National, more pronounced in lower-income and rural households | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Protein Input Inflation and Margin Pressure

Protein cost pressure remains one of the clearest constraints on margin expansion in the South Africa pet treats market. The National Agricultural Marketing Council reported that animal protein prices rose 11.4% year on year through November 2025, driven by Foot-and-Mouth Disease outbreaks, high electricity costs, and elevated imported ingredient prices. In June 2025, South African meat processors warned of a supply crisis following the Brazil poultry import ban, with substitute proteins from alternative origins priced above USD 1,000 per metric ton, directly tightening ingredient budgets for meat-based treats. These pressures affect chicken meal, beef by-products, and imported functional protein concentrates such as hydrolyzed collagen, all of which are relevant inputs in the South Africa pet treats market. Smaller domestic producers are more exposed to these pressures due to limited sourcing flexibility and weaker hedging capacity compared to larger multinational groups, which increases consolidation pressure over time.

Price Sensitivity in Mainstream Households

The South Africa pet treats market operates within strict household budget constraints for a large share of owners. Netwerk24 reported in 2026 that 45% of South African pet owners classify monthly pet spending as essential and non-cuttable, which supports resilience in repeat demand but does not remove affordability limits. The same reporting showed that some households spend between ZAR 32,000 (USD 1,778) and ZAR 60,000 (USD 3,333) in a pet's first year as of 2025, but this spending pattern sits above the mainstream mass buyer. This leaves the South Africa pet treats market divided between a premium buyer willing to pay for product credentials and a larger value-focused buyer anchored to economy formats. Brands positioned in the middle often face the most pressure, as they absorb price competition from below while still needing stronger quality signals to gain trust at the higher end.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dental Treats Lead While Novel Proteins Redefine Premium

Dental treats held the largest product segment at 25.2% of total value in the South Africa pet treats market. This position reflects a shift away from purely reward-led purchasing, as oral care claims give the product a practical role that owners can justify more readily. That practical role also strengthens retail and veterinary recommendations, which improves purchase frequency and reduces price resistance compared to simpler snack formats. Freeze-dried and jerky treats are the fastest-growing product format, projected to expand at a 6.6% CAGR from 2026 to 2031, indicating where premium demand is moving within the South Africa pet treats market.

This growth in premium formats is tied to demand for minimal-processing, single-ingredient, and novel-protein products, particularly among urban buyers already familiar with cleaner-label food choices in other areas of household spending. The South Africa pet treats market also has a compliance layer that shapes product launch timing, as Act 36 of 1947 registration requirements for functional claims can extend the path to market for more specialized formulations. Crunchy treats and soft and chewy treats form the middle of the category, with crunchy formats benefiting from shelf life and price flexibility, while soft and chewy products are better suited to training, puppy, and senior applications. Other treats, including raw, air-dried, artisanal, and limited-ingredient products, remain smaller but indicate that the South Africa pet treats market is becoming more format-specific rather than remaining concentrated in a few conventional products. Maneli Pets operates Africa's only SQF-accredited pet treat facility in Johannesburg and exports freeze-dried ostrich, venison, and crocodile jerky to the United States, the United Kingdom, Europe, Hong Kong, and Singapore. Montego's KAROO Wild antelope-based treats reached more than 500 European stores and distribution across 22+ United States by early 2025, adding credibility to South African premium products both domestically and internationally.

By Pet Type: Dog Segment Anchors Volume While Cat Ownership Accelerates

Dogs generated USD 68.5 million in 2025 and accounted for 79% of category value, placing them at the center of the South Africa pet treats market. Statistics South Africa confirmed 7.4 million dogs across 4.2 million households in the 2025 General Household Survey, with dog ownership reaching 21% of all households, providing the segment with a broad demand base. This scale supports a wide product range spanning economy biscuits and training rewards to veterinary dental formats and freeze-dried products. It also creates a competitive field where mid-tier brands face pressure from premium multinational offerings and local propositions.

Cats are the fastest-growing pet type in the South Africa pet treats market and are projected to grow at a 6.2% CAGR from 2026 to 2031. Their growth is tied to a rising ownership base, as cat ownership reached 6.4% of households in the 2025 national survey, with further gains anticipated as apartment-oriented urban living becomes more common. The cat segment tends to lean toward functional products, which supports stronger revenue per ownership unit in premium and specialty channels compared to many volume-led dog formats. Purina DentaLife for cats holds the VOHC seal, positioning Nestlé where cat ownership growth and dental care adoption overlap in the South Africa pet treats market. Other pets, including small mammals, birds, and reptiles, remain a niche with limited formulated options, though younger urban owners are gradually widening the commercial scope of this smaller part of the market.

By Distribution Channel: Specialty Retail and Digital Platforms Reshape Category Access

Supermarkets and hypermarkets generated USD 54.3 million in 2025 and held a 62.7% share of the South Africa pet treats market, making them the largest distribution channel. This dominant position reflects the tendency of most households to purchase pet food and treats during regular grocery trips. Large-format grocery retailers also benefit from expanding pet aisles and greater visibility across entry, mid, and premium price bands within a single shopping trip.

Specialty stores are smaller in absolute value but represent the fastest-growing channel, forecast to rise at a 6.5% CAGR from 2026 to 2031. The growth is supported by broader product assortments, more premium options, and store staff better equipped to explain functional or health-linked products compared to general grocery staff. The channel structure is also shifting as specialist retail and digital fulfillment increasingly operate together rather than as separate paths. This digital layer favors repeat-purchase products such as dental sticks, training treats, and portioned soft chews, concentrating demand around high-velocity stock keeping units in the South Africa pet treats market. Convenience stores remain relevant in township and peri-urban settings, providing quick access for smaller pack replenishment where large-format specialist retail has limited presence. Petshop Science's 2025 launch of a premium own-label pet food and treat range, featuring local manufacturing and 100% recyclable packaging, adds further competitive pressure on entry-level national brands operating in the same price band.

Geography Analysis

In South Africa, dog ownership reached 21% of households and cat ownership reached 6.4% of households in 2025. Commercial activity is most concentrated in Gauteng and the Western Cape. These two provinces combine higher household incomes, stronger specialist retail coverage, and denser veterinary networks than most other parts of the country. Netwerk24 reported that 45% of pet owners classify monthly pet spending as essential, which supports more stable demand in these urban centers even when broader household budgets come under pressure. This concentration allows new premium and functional formats to gain traction first in Gauteng and the Western Cape before expanding more gradually into secondary locations.

The South Africa pet treats market shows an uneven internal growth pattern across income bands and local retail environments. Premium and functional formats are most visible in metro-adjacent retail in areas such as Sandton, Constantia, and Stellenbosch, while more affordable mainstream formats dominate township grocery and convenience channels. Rural areas remain underpenetrated due to thinner formal distribution, limited cold-chain access, and household income constraints that limit conversion into formulated treats. As a result, a significant share of dog-owning households remains outside the full commercial reach of the South Africa pet treats market, which preserves long-term growth potential but slows nationwide premium uptake.

South Africa also serves as the main export hub for the broader African pet treats market, given its deeper channels, stronger brand development, and more advanced manufacturing credentials relative to many nearby markets. Egypt and Nigeria are emerging as secondary African markets in urban pet care, though the pet treats category in those countries remains at an earlier stage than in South Africa. Monic Group (Montego Pet Nutrition) distributes to 13 countries across Africa, the Middle East, and Europe, demonstrating that locally built brands can compete outside the home market. Maneli Pets also ships to five international markets from its Johannesburg facility, and this export activity reinforces product quality standards within the South Africa pet treats market. Regional trade links are anticipated to continue supporting expansion into nearby markets as formal pet retail infrastructure develops further over time.

Competitive Landscape

The South Africa pet treats market is moderately concentrated, with the top five players holding a major share of the market 2025. Mars Inc., the strongest single-company position, supported by established brands and broad route-to-market coverage. Nestlé S.A., driven by the Purina portfolio, dental treat offerings for cats and dogs, and stronger alignment with premium and veterinary-linked product segments. This level of concentration means the market is shaped largely by companies that already control shelf access, pricing discipline, and promotional reach across grocery and specialist retail channels. Domestic challengers are nonetheless gaining ground where they can combine local manufacturing, export-grade quality standards, and focused niche positioning.

The most significant strategic development in 2026 is the formation of Monic Group, which combines Montego Pet Nutrition and Marltons Pet Care, bringing together food, treats, accessories, and hygiene products under a single local pet care platform. This combination is commercially relevant because Montego's existing depot network can reduce Marltons' distribution unit costs, giving the group an advantage rooted in local logistics rather than imported scale. RCL Food's position weakened after a late November 2025 recall which halted 60% of its production capacity and removed nearly 50% of dry dog food from supermarket shelves[2]Source: News Article, "RCL’s pet food crisis opens door for Monic Group's ambitious expansion," dailymaverick.co.za. The market is still absorbing the commercial effects of that disruption in 2026, as rivals work to capture displaced shelf space and shift buyer habits. RCL also signed an agreement in February 2026 to acquire Martin and Martin, signaling a move into wet pet food manufacturing and a broader effort to diversify its product mix.

Smaller local companies are using premium differentiation rather than scale to maintain relevance in the market. Maneli's SQF-accredited facility in Johannesburg, South Africa provides a verifiable quality credential that supports both export sales and premium local positioning[3]Source: Global Pets, "South Africa’s pet industry heats up with new acquisitions," Global Pets, globalpetindustry.com. Montego's FSSC 22000 certification and in-house freeze-drying capability widen its operational advantage over artisan-scale competitors that cannot match the same level of process control or output flexibility. The clearest opportunities currently exist in cat-specific functional treats, veterinary-exclusive premium formats, and subscription-based replenishment models, where midsized brands can build defensible positions without competing directly against Mars or Nestlé across the full shelf.

South Africa Pet Treats Industry Leaders

-

Mars, Incorporated

-

Nestle S.A.

-

Monic Group (Montego Pet Nutrition)

-

Colgate-Palmolive Company (Hill's Pet Nutrition)

-

RCL Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Montego Pet Nutrition showcased new super-premium Karoo Wild functional dog treats at Interzoo 2026 in Nuremberg. The products feature novel African proteins and functional ingredients targeting key health needs. The exhibition reinforced Montego's position as a globally competitive treat brand with FSSC 22000-accredited manufacturing, expanding its international presence beyond the 22+ US states and 500+ European stores already established.

- February 2026: RCL Foods signed an agreement to acquire Cape Town-based Martin and Martin, marking its entry into wet pet food manufacturing. The acquisition reflects RCL's effort to diversify its product portfolio into higher-margin formats as the company works to recover from its November 2025 recall-related production disruption.

- January 2026: Monic Group completed the acquisition of Marltons Pet Care, merging it into the Montego Pet Nutrition portfolio. The deal brings together over a century of combined South African pet care experience and is anticipayed to utilize Montego's depot network for cost-effective distribution of Marltons' accessories and hygiene products.

South Africa Pet Treats Market Report Scope

Pet treats are snack and reward products formulated for companion animals and are used for indulgence, training, oral care, and functional health support.

The South Africa Pet Treats Market is Segmented by Sub Product Type (Crunchy Treats, Dental Treats, Freeze-Dried and Jerky Treats, Soft and Chewy Treats, and Other Treats), by Pet Type (Dogs, Cats, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets and Hypermarkets, and Other Channels). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Crunchy Treats |

| Dental Treats |

| Freeze-dried and Jerky Treats |

| Soft and Chewy Treats |

| Other Treats |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Crunchy Treats |

| Dental Treats | |

| Freeze-dried and Jerky Treats | |

| Soft and Chewy Treats | |

| Other Treats | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the current size of South Africa pet treats revenue?

The South Africa pet treats market stands at USD 91.1 million in 2026.

Which product type leads spending on pet treats in South Africa?

Dental treats lead the category, holding 25.2% of 2025 value, supported by stronger owner interest in oral health and functional benefits.

Which pet type is growing fastest in treat consumption?

Cats are the fastest-growing pet type with a projected 6.2% CAGR between 2026 and 2031.

What is pushing premium treat demand higher?

Humanization, oral health positioning, cleaner-label preferences, and stronger veterinary influence are moving buyers toward more functional and premium treat formats.

What are the main risks for companies in this space?

The biggest risks are protein cost inflation, household price sensitivity, compliance demands for functional claims, and ongoing competitive disruption.

Page last updated on: