South Africa Cleaning Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

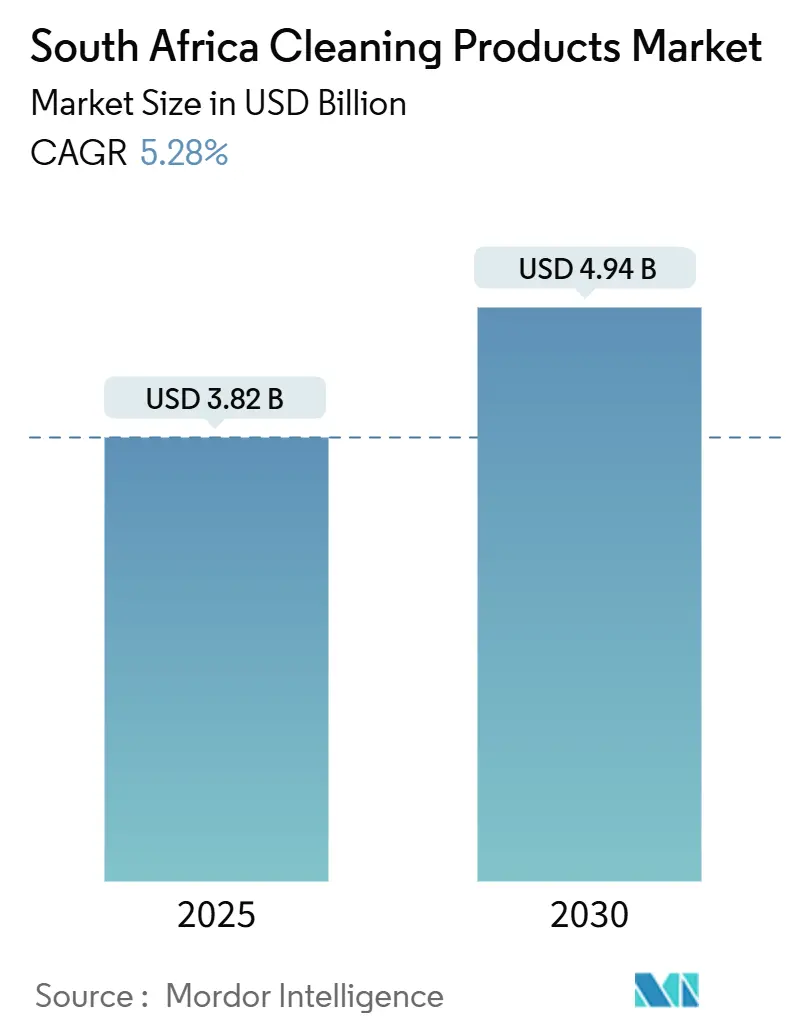

| Market Size (2025) | USD 3.82 Billion |

| Market Size (2030) | USD 4.94 Billion |

| Growth Rate (2025 - 2030) | 5.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Cleaning Products Market Analysis by Mordor Intelligence

The South African cleaning products market is projected to grow steadily, reaching USD 3.82 billion in 2025 and USD 4.94 billion by 2030, with a compound annual growth rate (CAGR) of 5.28% during the forecast period. This growth is primarily driven by the rising urban population, which increases the demand for cleaning products, and a heightened focus on hygiene. Manufacturers are also introducing eco-friendly and refillable product options, which are gaining popularity among environmentally conscious consumers. Concerns about water scarcity are driving the demand for innovative solutions, such as low-water enzymatic detergents, which are designed to be effective while conserving water. Regulatory changes promoting ingredient transparency and the use of digital labeling tools are transforming how companies share product information with consumers, making it easier for buyers to make informed choices. The competitive landscape in the market is moderately intense. Multinational corporations are leveraging their strong research and development capabilities to introduce advanced products, while local players are using their flexibility to meet specific regional demands.

Key Report Takeaways

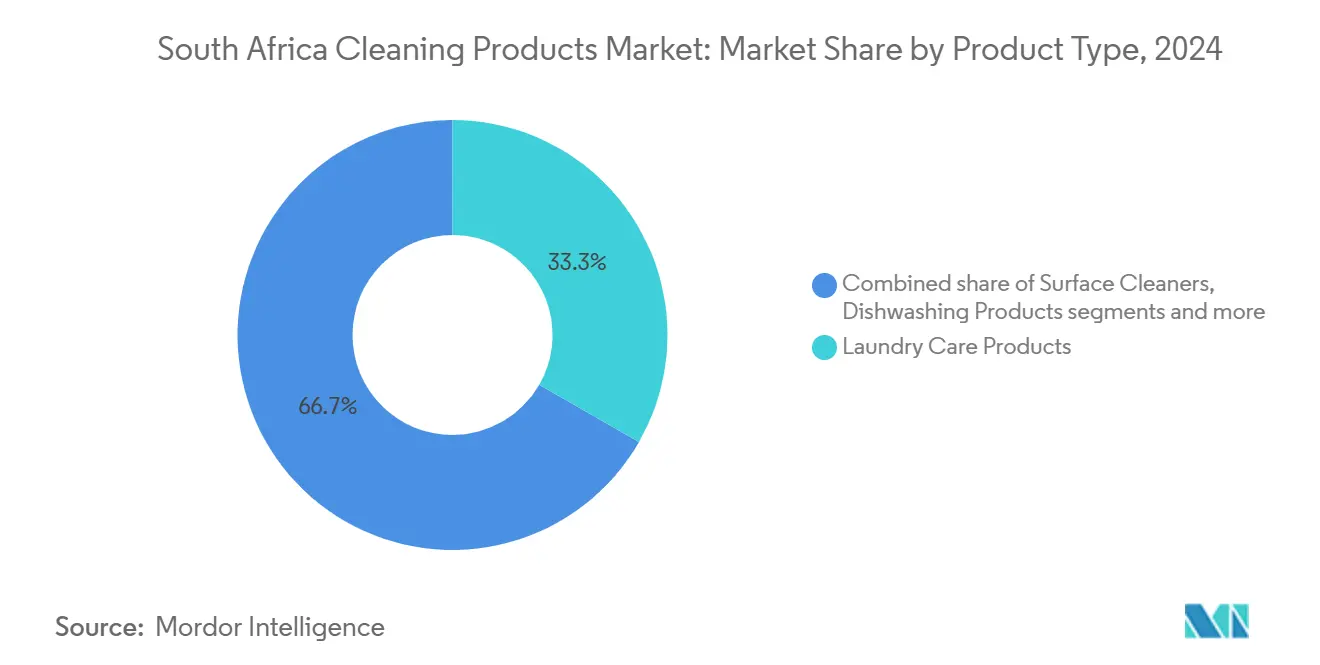

- By product type, laundry care led with 33.32% revenue share in 2024; glass and metal cleaners are projected to grow at a 6.08% CAGR to 2030.

- By category, conventional items held 89.12% of the South Africa cleaning products market share in 2024, while organic/natural alternatives are on track to expand at a 6.72% CAGR through 2030.

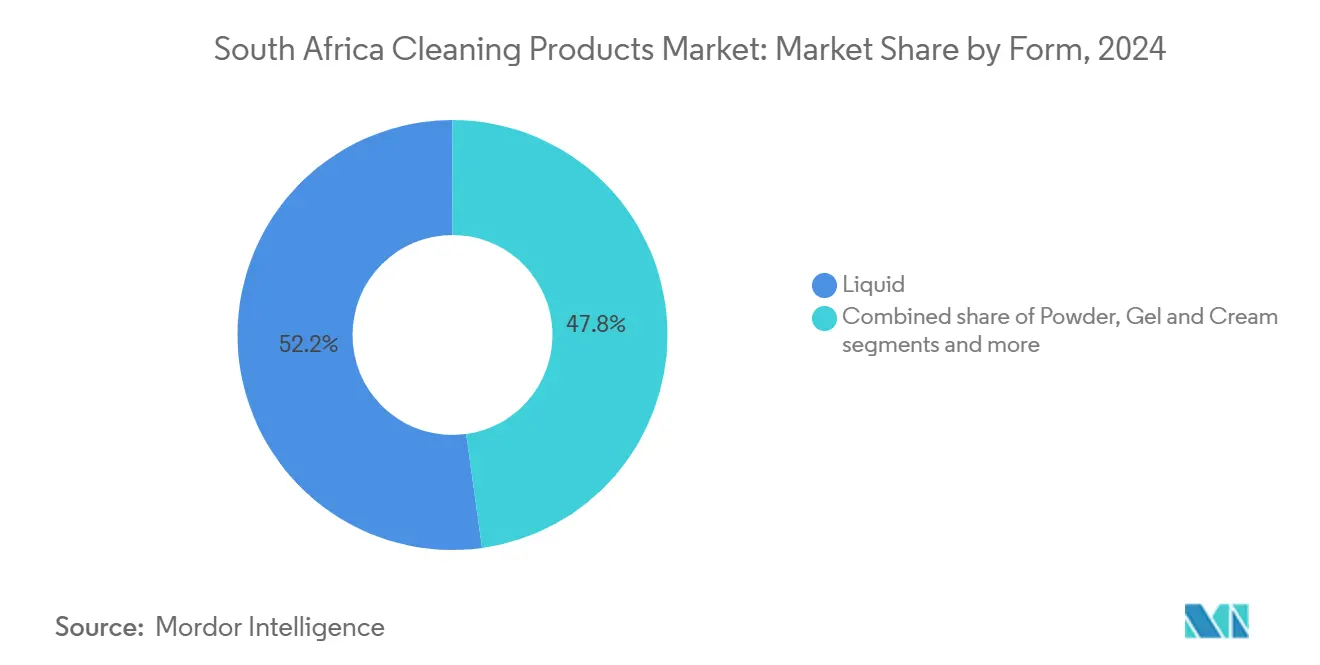

- By form, liquid products accounted for 52.16% of the South Africa cleaning products market size in 2024; tablets and aerosols represent the fastest format with a 7.22% CAGR forecast.

- By application, household/residential captured 70.21% value in 2024, whereas institutional and commercial spending is poised for a 7.85% CAGR through 2030.

- By distribution channel, retail B2C accounted for 81.98% of sales in 2024, but wholesale and corporate procurement are expected to grow at a 7.61% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with South africa representing one among them. The global report on cleaning products market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

South Africa Cleaning Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVERS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increased demand for antimicrobial and health-focused formulations | +1.2% | National, concentrated in urban metros | Medium term (2-4 years) |

| Growing emphasis on ingredient transparency and digitally accessible product information | +0.8% | National, higher in Western Cape and Gauteng | Long term (≥ 4 years) |

| Adoption of enzymatic and bio-based cleaners optimized for low-water use | +0.7% | National, priority in water-stressed regions | Long term (≥ 4 years) |

| Growing preference for customizable and refillable product formats | +0.9% | Urban metros, expanding to secondary cities | Medium term (2-4 years) |

| Accelerated antimicrobial innovations targeting resistant pathogens | +1.0% | National, institutional focus | Short term (≤ 2 years) |

| Retail modernization and e-commerce adoption | +0.6% | National, metro-led expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased demand for antimicrobial and health-focused formulations

Post-pandemic hygiene awareness continues to drive strong demand for antimicrobial cleaning products, especially in healthcare and institutional settings where infection control is critical. The South African Society of Anaesthesiologists emphasizes the importance of using disinfectants that are validated and safe for medical equipment, encouraging healthcare facilities to adopt more precise and specification-driven purchasing practices. Manufacturers are adapting to changing consumer preferences, as demonstrated by Sunlight's launch of extra antibacterial dishwashing liquid, which uses lactic acid as its active antimicrobial ingredient. This shift highlights a growing demand for food-safe and familiar ingredients, moving away from synthetic biocides. Research shows significant differences in the effectiveness of commercial hand sanitizers across South African brands, creating opportunities for premium products with proven efficacy. This trend is particularly beneficial for institutional and commercial sectors, where purchasing decisions are increasingly based on verified antimicrobial performance rather than just cost considerations.

Growing emphasis on ingredient transparency and digitally accessible product information

Urban consumers, particularly those with higher education and increasing familiarity with digital tools, are paying closer attention to the ingredients and safety of cleaning products. This has led to a growing demand for clear and transparent information about product contents and easy online access to this information. South Africa’s Foodstuffs, Cosmetics and Disinfectants Act has further pushed manufacturers to provide detailed information about product formulations, potential allergens, and safety compliance. To meet these expectations, companies are incorporating QR codes on product packaging, creating online ingredient databases, and offering mobile-friendly safety data sheets. These efforts enable consumers to verify product claims, understand potential health or environmental risks, and make more informed purchasing decisions. Additionally, this trend is encouraging brands to improve their communication strategies and build trust with their customers by being more transparent about their products.

Adoption of enzymatic and bio-based cleaners optimized for low-water use

Water scarcity across South African provinces is accelerating the shift toward enzymatic and bio-based cleaning formulations that require less water. Research by the University of Fort Hare, funded by the Department of Science and Innovation, has led to the successful development of lipolytic enzymes derived from Raoultella terrigena. These enzymes are now compatible with leading South African detergent brands, including Sunlight, Surf, and Omo. The bio-additive formulations not only reduce water usage but also ensure effective cleaning and integrate seamlessly with existing product lines. With many South African households experiencing water interruptions lasting two days or more annually, the demand for concentrated and water-efficient cleaning solutions is increasing. Enzymatic cleaners are particularly attractive to institutional users dealing with water restrictions, as they deliver high cleaning performance while significantly reducing water consumption per cleaning cycle. This trend highlights the growing importance of sustainable and efficient cleaning solutions in water-scarce regions.

Growing preference for customizable and rellable product formats

Urban consumers are increasingly opting for refillable and customizable cleaning products due to growing environmental awareness and the desire to reduce costs. Unilever, in partnership with South African start-up Sonke, has introduced an innovative concept in Johannesburg through automated rell stores known as Skubu. These stores utilize IoT technology to dispense Sunlight and Handy Andy products, enabling consumers to save up to 60% compared to single-use packaging. This initiative addresses two major challenges: making products more affordable and reducing packaging waste. This is particularly important in South Africa, where recycling rates remain low, and many metropolitan households fail to separate their waste. Moreover, the ability to customize product concentration levels enables consumers to adjust the cleaning strength according to their specific needs, ensuring both cost savings and a reduced environmental footprint. The success of this model in Johannesburg suggests significant potential for expansion nationwide, particularly in urban areas with higher smartphone penetration and greater adoption of digital payment systems.

Restraints Impact Analysis*

| DRIVERS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory complexity and compliance burden | -0.9% | National, varying provincial enforcement | Long term (≥ 4 years) |

| Counterfeit and low-quality products | -0.7% | National, concentrated in informal markets | Medium term (2-4 years) |

| Raw material volatility and supply risk | -1.1% | National, import- dependent regions | Short term (≤ 2 years) |

| Private-label competition and price pressure | -0.8% | National, retail- concentrated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory complexity and compliance burden

Manufacturers, especially smaller local producers without dedicated regulatory affairs teams, are facing growing challenges due to increasingly complex regulatory frameworks. The National Regulator for Compulsory Specifications (NRCS) is responsible for setting standards for cleaning products, while the Department of Health enforces the Foodstuffs, Cosmetics and Disinfectants Act, creating overlapping regulatory requirements. In April 2024, draft regulations on Hazardous Chemical Agents were introduced to improve workplace safety for cleaning products used in commercial and institutional settings[1]Source: The South African Department of Employment & Labour: "White Paper on National Labour Migration Policy for South Africa", labour.gov.za . Furthermore, stricter lead content limits of 90 ppm in coatings and paints, set to take effect in May 2025, indicate a stronger regulatory focus on chemical ingredients across various product categories. These changes are driving up compliance costs, particularly for smaller manufacturers, who must invest in testing, documentation, and regulatory expertise to meet these requirements. This financial burden is likely to accelerate market share consolidation, beneting larger companies with robust compliance systems and greater resources to adapt to these regulatory demands.

Raw material volatility and supply risk

Raw material price fluctuations and supply issues continue to be significant challenges for South Africa’s cleaning products market. These supply chain problems are affecting both the cost and availability of essential materials. Petrochemical-based ingredients, such as those used in surfactants and solvents, are particularly vulnerable. Sasol Secunda, which provides nearly 30% of the country’s liquid fuels and key petrochemical feedstocks, is under increasing pressure due to stricter environmental regulations, rising carbon taxes, and declining gas reserves. These factors increase the risk of operational disruptions, which could impact the entire manufacturing sector. Additionally, ingredient processors, such as Barloworld’s ingrain mills, are facing steam shortages, which reduce their production capacity and limit the supply of starches and other critical inputs needed by cleaning product manufacturers. Currency instability further worsens the situation. The fluctuating value of the rand against major global currencies raises the cost of imported chemicals, packaging materials, and specialized additives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Laundry Care Dominance Faces Specialty Growth

In 2024, laundry care products hold a 33.32% market share, making them the largest product segment. Their dominance is driven by their essential role in households and strong consumer loyalty. This leadership is further supported by South Africa's 2023 data, which shows a 39.1% washing machine penetration in households, ensuring consistent demand for specialized laundry products[2]Source: Statistics South Africa: "General Household Survey", statssa.gov.za. Leading brands such as Surf, Omo, and Sunlight capitalize on extensive retail networks that span premium supermarkets and informal spaza shops, catering to all income levels. Research conducted by the University of Fort Hare highlights advancements in bio-based enzyme additives compatible with major laundry brands. These innovations address environmental concerns while maintaining cleaning performance, reflecting the segment's adaptability. The frequent purchase cycles and price flexibility of laundry care products contribute to their resilience and ability to grow even during economic downturns.

Glass and metal cleaners are the fastest-growing product segment, with a projected CAGR of 6.08% through 2030. This growth is fueled by increasing demand from commercial and institutional sectors for specialized cleaning solutions. The expansion aligns with South Africa's growing construction industry, which includes new healthcare facilities, office buildings, and hospitality venues that require effective cleaning for large glass facades and metal xtures. In institutional markets, purchasing decisions are often based on performance standards rather than cost, enabling premium pricing for high-quality products. Recent innovations, such as the Blue Sapphire multipurpose cleaner, manufactured in South Africa with food-safe certication, target commercial kitchens and food service establishments. Healthcare facilities are a key driver of demand, as their infection control protocols require cleaning agents that are both effective against resistant pathogens and safe for sensitive medical equipment.

By Category: Conventional Products Retain Dominance Despite Natural Acceleration

In 2024, conventional cleaning products held a significant 89.12% share of the South African cleaning products market. These products are popular due to their affordability and easy availability in both modern retail stores and informal markets. Consumers are familiar with these products, which encourages repeat purchases and slows the adoption of more expensive alternatives. Manufacturers offer a wide variety of options to meet different household needs, ensuring they remain accessible to people across various income levels. Their consistent performance and well-established supply chains further strengthen their dominance in the market, making them a reliable choice for most households.

The organic and natural cleaning products segment is expected to grow at a CAGR of 6.72% through 2030, driven by increasing awareness of health and environmental sustainability. Consumers are becoming increasingly mindful of the ingredients in their cleaning products, opting for safer and more eco-friendly options. Certifications like Eco-Choice Africa are helping shoppers identify genuine sustainable products, boosting confidence in this category. Retailers are also dedicating more shelf space to these products, especially in urban areas and among higher-income groups. To meet this rising demand, manufacturers are focusing on creating plant-based and biodegradable formulations, which are gradually making this segment more appealing and premium in nature.

By Form: Liquid Leadership Challenged by Innovative Formats

In 2024, liquid cleaning products dominated the South African market, accounting for 52.16% of the total share. Their popularity stems from their ease of use and effectiveness in everyday cleaning tasks, such as laundry and surface cleaning. These products dissolve quickly and spread evenly, ensuring efficient cleaning results. They are also available in various packaging formats, including spray bottles, squeeze bottles, and refillable containers, which enhance their convenience for consumers. Additionally, their widespread availability in retail stores and frequent discounts make them an affordable and accessible option for households across different income levels. This combination of practicality and affordability has solidified their position as the leading choice in the market.

Tablets and aerosols are projected to grow at the fastest rate, with a CAGR of 7.22% expected through 2030, driven by the rising demand for convenient and eco-friendly cleaning solutions. These formats are compact and lightweight, making them easier to transport and store, which benefits both manufacturers and consumers. They also align with sustainability goals by offering portion-controlled usage and reducing the need for single-use plastic packaging. Additionally, their consistent dosing and stable formulations ensure reliable performance, which appeals to consumers seeking effective cleaning options. As more brands introduce these innovative products, tablets and aerosols are becoming increasingly popular as modern, efficient, and environmentally friendly alternatives in the cleaning products market.

By Application: Household Dominance Contrasts Institutional Acceleration

In 2024, household use accounted for 70.21% of the South African cleaning products market, driven by frequent household activities such as dishwashing, laundry, and surface cleaning. The affordability of these products, combined with their easy availability in both urban and rural areas, ensures steady demand. Consumers often prefer trusted brands and multipurpose cleaning solutions, which further boost sales. Additionally, the expansion of modern retail channels has improved access to a wider variety of products, making it easier for households to meet their cleaning needs. Overall, household applications remain the largest contributor to the market's growth, reflecting their essential role in daily life.

Institutional and commercial use of cleaning products is expected to grow at a CAGR of 7.85% through 2030, as hygiene standards continue to rise in public and private facilities. The healthcare sector, supported by the National Health Insurance program, is driving demand for disinfectants and sanitation supplies. Similarly, the foodservice and hospitality industries are adopting stricter cleaning protocols to comply with safety regulations and audits. Manufacturers are addressing these needs by offering high-performance, bulk, and concentrated cleaning solutions designed for professional use. As these sectors expand, institutional and commercial buyers are becoming a key growth segment in the market.

By Distribution Channel: Retail Dominance Faces B2B Acceleration

Retail B2C outlets, including supermarkets, convenience stores, and e-commerce platforms, accounted for 81.98% of the South African cleaning products market in 2024. These outlets benefit from their wide geographic presence and frequent promotional campaigns, which attract a large customer base. Loyalty programs and bundled discounts encourage consumers to shop more often and purchase in larger quantities. Additionally, these channels offer a variety of product options and transparent pricing, which helps build consumer trust. The growing availability of online delivery services has further improved access to cleaning products, especially for urban households, making retail B2C the leading distribution channel for everyday cleaning needs.

Wholesale and corporate procurement is expected to grow at a CAGR of 7.61% through 2030, driven by increasing demand from sectors like healthcare, hospitality, and professional cleaning services. Many organizations are now utilizing digital tender platforms to streamline bulk purchasing, ensuring standardized product quality and facilitating more effective price negotiations. Institutional buyers are focusing on high-performance cleaning products that comply with hygiene and safety regulations. Additionally, rising investments in healthcare facilities and hotels are boosting demand for cleaning supplies in these sectors. As digital procurement tools become more common, wholesale channels are likely to play a more significant role in supporting market growth.

Geography Analysis

South Africa's cleaning products market is shaped by regional factors such as economic development, infrastructure, and population distribution. Gauteng province dominates the market due to its high population density, industrial hubs, and vibrant commercial activities, which drive both household and institutional demand. The province's advanced logistics, strong retail presence, and higher household incomes support the adoption of premium cleaning products. Western Cape is the second-largest market, driven by its environmentally conscious population, a tourism-driven hospitality sector, and a well- established manufacturing base that aids local product development and distribution.

KwaZulu-Natal ranks as the third major market, beneting from its signicant port infrastructure that supports trade activities and a growing manufacturing sector that boosts institutional cleaning demand. The province's coastal location and thriving tourism industry create a need for specialized cleaning products designed to address salt air corrosion and maintain hygiene in hospitality settings. Variations in water quality across provinces influence consumer preferences for cleaning products. Regions with frequent water shortages show a higher demand for concentrated and water-efficient solutions. Rural provinces like Limpopo, Eastern Cape, and North West, despite facing infrastructure challenges, offer growth opportunities. Expanding retail networks and rising household formations in these areas are driving demand for basic cleaning products.

Economic development programs, such as infrastructure investments and small business support initiatives, provide opportunities for local manufacturers to establish regional production and distribution facilities. However, differences in regulatory enforcement across provinces impact market entry strategies, particularly for smaller manufacturers with limited regulatory expertise. The expansion of retail chains into secondary cities and rural areas improves product availability and brand visibility. However, these markets remain highly price-sensitive due to lower average incomes and a greater reliance on social grants for household expenses.

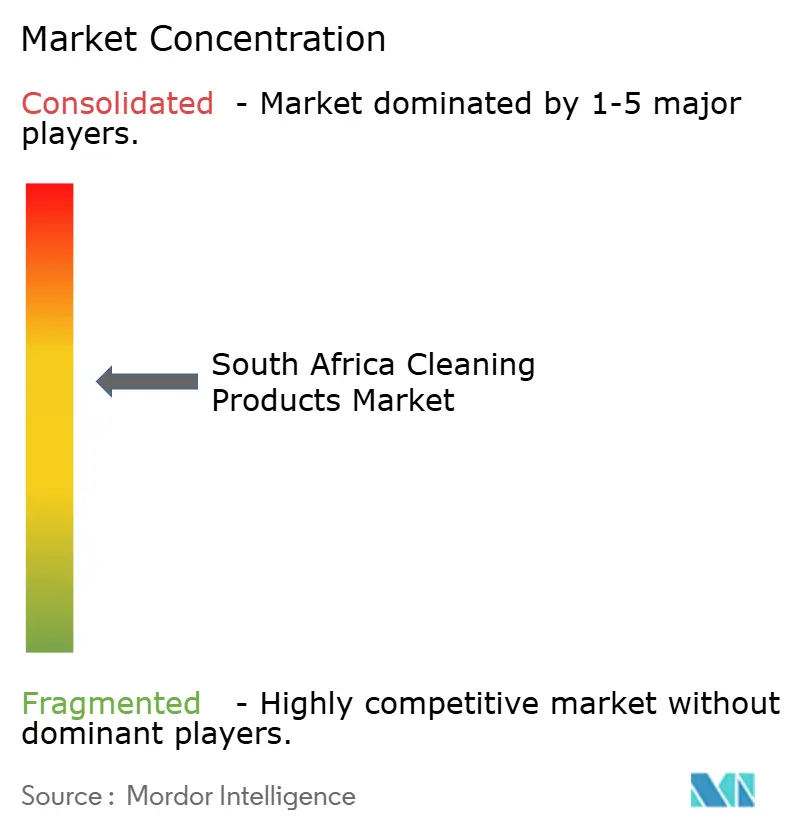

Competitive Landscape

The South African cleaning products market is moderately concentrated, with major players such as Unilever, Procter & Gamble, and Reckitt Benckiser holding a significant market share. These companies regularly update their product lines to maintain their competitive edge and attract consumers. For example, Unilever has introduced Handy Andy with probiotic cleaning properties, while P&G has launched bacterial-spore laundry additives to enhance cleaning efficiency. Additionally, recent patent filings reveal innovations such as collapsible refill pouches and solid cleansing bars, which aim to reduce plastic waste and appeal to eco-conscious buyers. These efforts underscore the importance of innovation in maintaining a competitive edge in the market.

Local companies, such as PCS Phatsima and Envirochem, are gaining ground by leveraging their regional distribution networks and offering cost-effective cleaning solutions. These firms often secure municipal cleaning contracts by providing affordable and tailored products that meet local needs. At the same time, private-label products from retailers like Shoprite’s Ritebrand and Pick'n Pay’s no-name range are disrupting the market by offering cheaper alternatives to branded products. In response, multinational companies are introducing smaller packaging options and loyalty card discounts to retain price-sensitive customers and protect their market share.

Digital transformation is playing a significant role in reshaping the cleaning products market. Direct-to-consumer subscription services for products like laundry pods are becoming more popular, often integrated with mobile payment platforms to bypass traditional retail channels. Companies like Dyson are also combining cleaning equipment with proprietary probiotic solutions, reflecting a trend toward merging hardware and consumables. Additionally, partnerships between chemical suppliers and contract-cleaning firms are on the rise. These collaborations offer bundled services, including training and dosing equipment alongside cleaning products, helping companies secure long-term contracts and strengthen customer relationships.

South Africa Cleaning Products Industry Leaders

-

Unilever plc

-

Reckitt Benckiser Group plc

-

The Procter & Gamble Company

-

Alfred Kärcher SE & Co. KG

-

Nilfisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Unilever launched the new Domestos Power Foam Toilet and Bathroom Spray in South Africa. According to the brand, Power Foam delivers multi-surface cleaning performance, targeting not only toilets but also a wide range of bathroom fixtures, including tiles, sinks, taps, mirrors, and showers.

- June 2025: Unilever partnered with South African start-up Sonke to launch automated rell stores (Skubu) in Johannesburg, featuring IoT-enabled dispensing systems for Sunlight and Handy Andy products offering 60% cost savings versus single-use formats.

- September 2024: Sunlight, one of the household heritage brands, launched its latest innovation: Sunlight 5-in-1 washing powder. The launch took place at the DStv Delicious Festival in Johannesburg. In South Africa, the 5-in-1 range appears in both automatic laundry and automatic dishwashing formats, according to the brand.

- May 2024: Alsysco introduced two aluminium-specic cleaners: a non-toxic, non-corrosive Powder Coating Cleaner for window frames, doors, and balustrades, and a Mill Finish & Anodised Cleaner for curtain walls that is corrosive and must be kept out of direct sunlight. Both are non-abrasive, spray-on formulations designed to leave aluminium streak-free, with guidance to use gloves, eye protection, and good ventilation during application.

South Africa Cleaning Products Market Report Scope

The South Africa cleaning products market is segmented into product type, category, form, application, and distribution channel. By product type, the market is segmented into laundry care products, surface cleaners, dishwashing products, toilet/bathroom cleaners, floor cleaners, glass and metal and other specialty cleaners. By category, the market is segmented into conventional and organic/natural. By form, the market is segmented into liquid, powder, gel and cream, wipes, tablets, and aerosol. By application, the market is segmented into household/residential, institutional, and commercial. By distribution channel, the market is segmented into wholesale/corporate procurement (B2B) and retail (B2C).

| Laundry Care Products |

| Surface Cleaners |

| Dishwashing Products |

| Toilet/Bathroom Cleaners |

| Floor Cleaners |

| Glass and Metal |

| Other Specialty Cleaners |

| Conventional |

| Organic/Natural |

| Liquid |

| Powder |

| Gel and Cream |

| Wipes |

| Tablets and Aerosol |

| Household/Residential |

| Institutional and Commercial |

| Wholesale/Corporate Procurement (B2B) | |

| Retail (B2C) | Supermarkets and Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail | |

| Other Distribution Channels |

| By Product Type | Laundry Care Products | |

| Surface Cleaners | ||

| Dishwashing Products | ||

| Toilet/Bathroom Cleaners | ||

| Floor Cleaners | ||

| Glass and Metal | ||

| Other Specialty Cleaners | ||

| By Category | Conventional | |

| Organic/Natural | ||

| By Form | Liquid | |

| Powder | ||

| Gel and Cream | ||

| Wipes | ||

| Tablets and Aerosol | ||

| By Application | Household/Residential | |

| Institutional and Commercial | ||

| By Distribution Channel | Wholesale/Corporate Procurement (B2B) | |

| Retail (B2C) | Supermarkets and Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the current value of South Africa’s cleaning products sector and its expected size by 2030?

The sector is valued at USD 3.82 billion in 2025 and is projected to reach USD 4.94 billion by 2030, reflecting a 5.28% CAGR.

Which product category commands the highest share?

Laundry care items lead with a 33.32% revenue share in 2024 thanks to their non-discretionary nature and entrenched brand loyalty.

How fast are organic or natural cleaners expanding?

Organic/natural alternatives are forecast to grow at a 6.72% CAGR through 2030, well above the overall sector pace.

Which distribution channel is gaining ground beyond supermarkets?

Institutional and corporate procurement is rising at a 7.61% CAGR as hospitals, hotels, and contract cleaners centralize bulk purchasing.

Page last updated on: