South Africa Canned Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

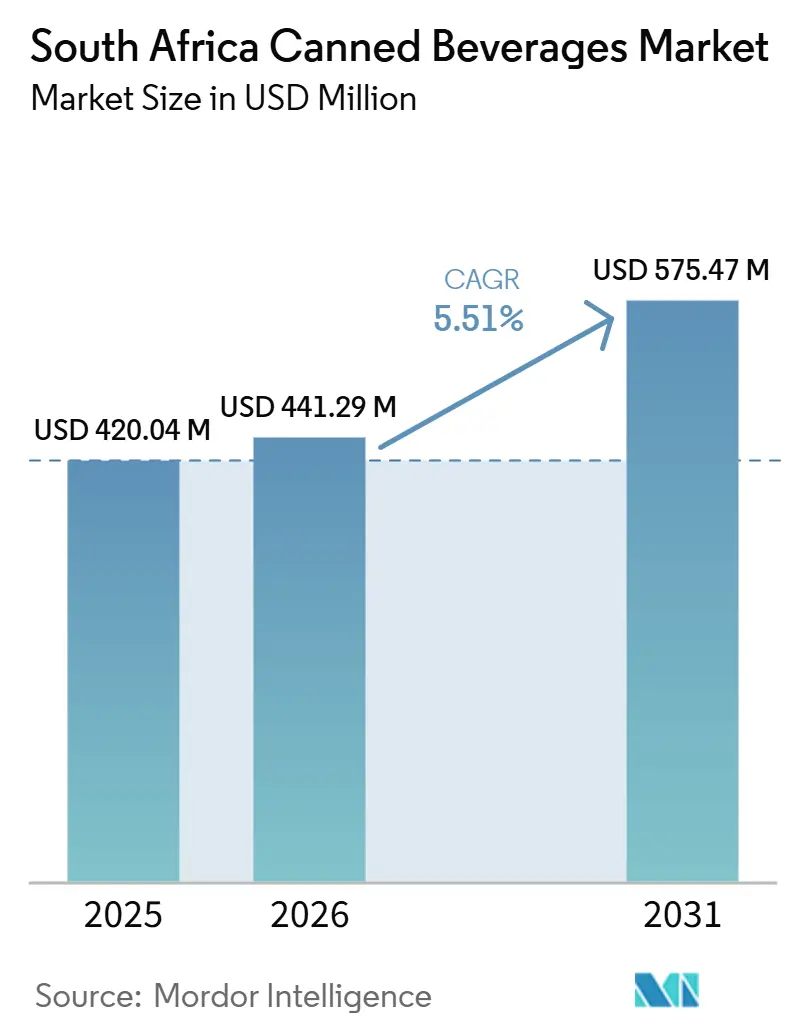

| Base Year Market Size (2025) | USD 420.04 Million |

| Market Size (2026) | USD 441.29 Million |

| Market Size (2031) | USD 575.47 Million |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

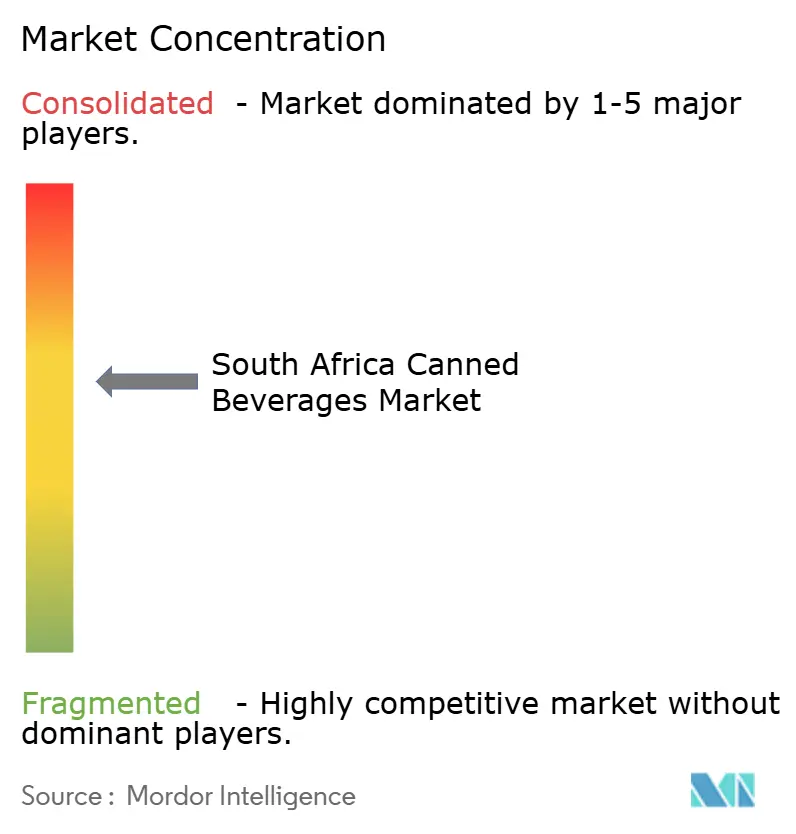

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Canned Beverages Market Analysis by Mordor Intelligence

The South Africa canned beverages market was valued at USD 420.04 million in 2025 and is expected to increase from USD 441.29 million in 2026 to USD 575.47 million by 2031, registering a CAGR of 5.51% during the forecast period 2026-2031. Alcoholic beverages remained the primary volume driver in the South Africa canned beverages market, with demand spanning retail shelves and hospitality outlets. Rising urban disposable incomes, the recovery of cold-chain operations after power disruptions, and the shift toward convenience-led grocery formats continue to support packaged beverage demand in the country. Packaging substitution from PET bottles, cartons, and pouches remains a clear restraint on growth, although strong collection and recycling rates, along with ongoing investment in supply and product innovation, support the medium-term outlook for the South Africa canned beverages market. The market is moderately consolidated.

Key Report Takeaways

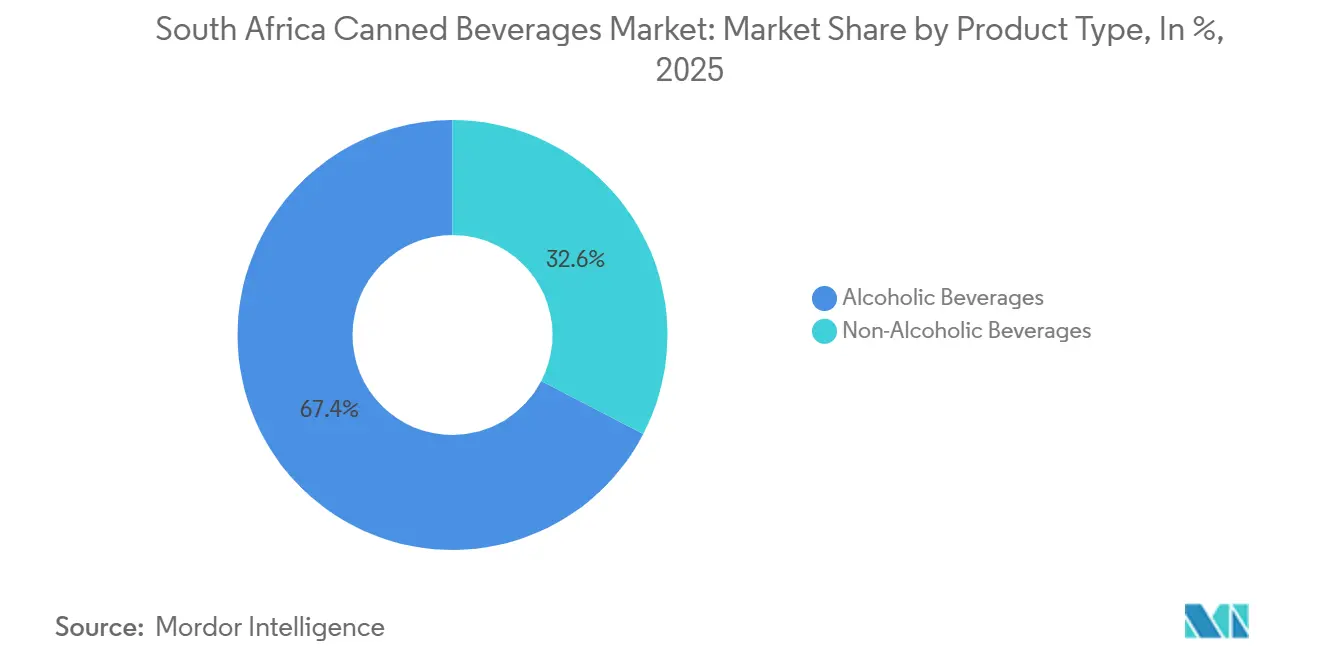

- By product type, alcoholic beverages led with 67.38% of the South Africa canned beverages market share in 2025, while non-alcoholic beverages are forecast to expand at a 6.47% CAGR through 2031.

- By material, aluminum cans accounted for 68.41% of the South African canned beverage market in 2025, while steel and tinplate cans are projected to grow at a 6.06% CAGR through 2031.

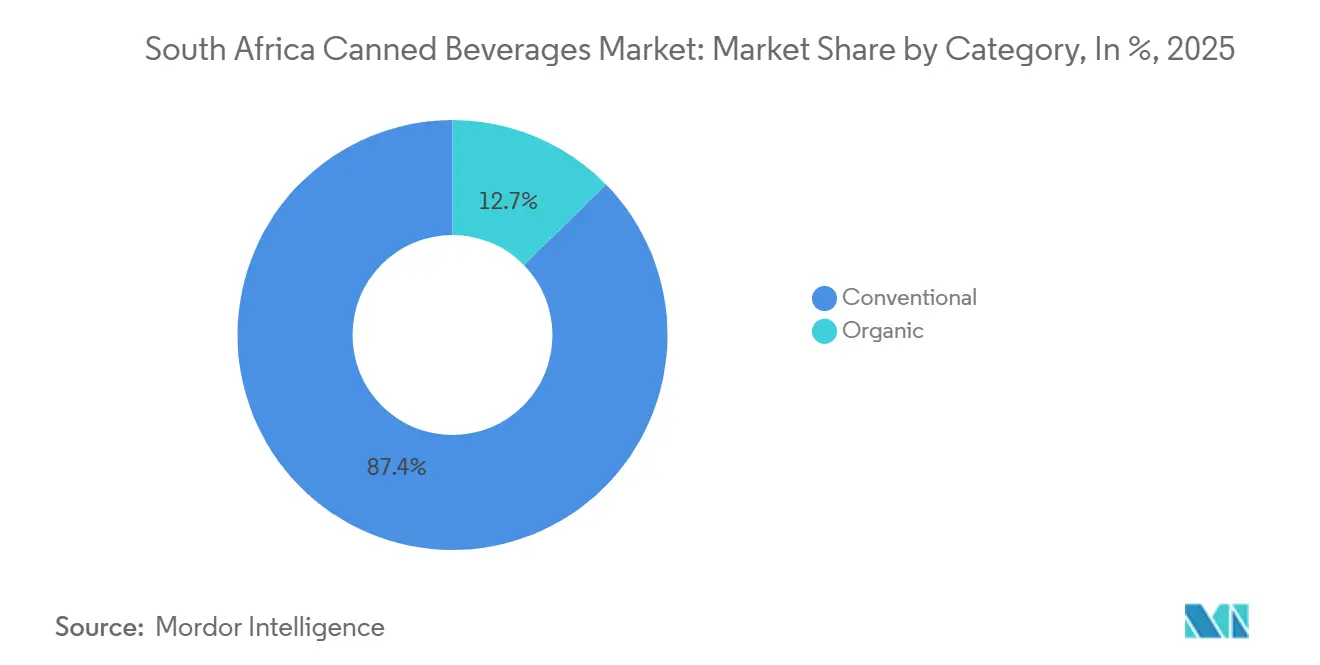

- By category, conventional products held 87.35% share in 2025, while organic products are projected to advance at a 6.38% CAGR through 2031.

- By distribution channel, off-trade retained 64.08% share in 2025, while on-trade is forecast to grow at a 6.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Canned Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience and on-the-go consumption | +1.4% | National; concentrated in Gauteng, Western Cape, KwaZulu-Natal metropolitan corridors | Medium term (2-4 years) |

| Growing preference for longer shelf-life beverages | +0.6% | National, with stronger uptake in peri-urban and rural retail | Long term (≥ 4 years) |

| Increasing tourism and hospitality activities | +0.5% | Coastal and urban centres, Cape Town, Durban, Johannesburg; spill-over to game and eco-tourism corridors | Medium term (2-4 years) |

| Strong demand for beer, cider, and canned alcoholic beverages | +1.2% | National; on-trade growth concentrated in Gauteng and KwaZulu-Natal | Medium term (2-4 years) |

| Demand for low-sugar and functional beverages | +0.7% | National, with early-adopter concentration in urban premium retail clusters | Short term (≤ 2 years) |

| Advancements in can manufacturing technology | +0.5% | National supply-side effect; upstream benefit from Richards Bay and Gauteng manufacturing corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenience and on-the-go consumption

Convenience and on-the-go consumption are supporting growth in the South Africa canned beverages market, as more consumers prefer drinks that are easy to carry, store, and consume during busy daily routines. Urbanization, longer working hours, commuting, and changing shopping habits are encouraging consumers to choose ready-to-drink options that require no preparation. According to GroundUp in November 2025, South Africa had approximately 17 million employed people at the end of the third quarter of 2025, indicating a large working population that may prefer convenient beverage formats during travel, work breaks, and quick shopping trips[1]Source: GroundUp, "How South Africa’s Job Market Has Changed", groundup.org.za. Cans are lightweight, durable, and portable, making them suitable for impulse purchases through supermarkets, convenience stores, forecourt retailers, and spaza shops. As more working professionals and students look for quick refreshment options, demand for canned soft drinks, energy drinks, ready-to-drink coffee, and alcoholic beverages is expected to remain strong.

Increasing tourism and hospitality activities

Growing tourism and hospitality activities are supporting the growth of the South Africa canned beverages market, as more people consume beverages in hotels, restaurants, bars, resorts, events, and entertainment venues. According to Statistics South Africa, the country recorded 36.5 million travelers in 2025, including 18.9 million arrivals, showing strong travel activity from both domestic and international visitors[2]Source: Statistics South Africa, "South Africa Tourism Surpasses Pre‑Pandemic Levels in 2025", statssa.gov.za. As more tourists visit the country for leisure, business, and events, demand for easy-to-carry, ready-to-drink beverages continues to rise. This is increasing the consumption of canned soft drinks, beer, cider, energy drinks, and RTD alcoholic beverages across hospitality and tourism channels. The convenience, portability, and longer shelf life of canned beverages make them suitable for busy on-trade locations, outdoor events, and travel-related consumption. As tourism, leisure, and business travel continue to grow, the demand for canned beverages in South Africa is expected to strengthen further.

Strong demand for beer, cider, and canned alcoholic beverages

Demand for beer, cider, and other canned alcoholic beverages is driving growth in the South African canned beverages market, as many consumers continue to buy alcoholic drinks in retail stores, as well as hotels, restaurants, bars, and entertainment venues. According to a South African Medical Journal (SAMJ) survey published in April 2026, 32.2% of South Africans reported alcohol consumption, with the highest levels seen among women aged 20–24 years (36.1%) and residents of Cape Town (52.8%) and Tshwane (51.6%)[3]Source: South African Medical Journal (SAMJ), "Prevalence Of Alcohol Use, Associated Risk Factors, And the Impact on the HIV Care Cascade Among Adolescent Girls and Young Women in South Africa: Findings from the Herstory Study", samajournals.co.za. This consumer base is increasing demand for canned beer, cider, and ready-to-drink (RTD) alcoholic beverages because cans are easy to carry, quick to chill, suitable for outdoor and social occasions, and convenient for both at-home and on-the-go consumption. Beverage companies are also adding more premium options, new flavors, and convenient pack sizes, which is helping attract more consumers and support market growth.

Advancements in can manufacturing technology

Advancements in can manufacturing technology are supporting the growth of the South Africa canned beverages market by making cans easier to produce, more sustainable, and more attractive to consumers. Manufacturers are using lightweight aluminum cans, high-speed digital printing, 360-degree decorative printing, BPA-NI (Bisphenol A Non-Intent) internal coatings, and smart packaging features such as QR codes and digital traceability to make products stand out and give consumers more information. Modern production lines with AI-enabled quality inspection, automated filling systems, and energy-efficient canning technologies are also helping companies improve production speed, reduce errors, and cut waste. These improvements help extend product shelf life, reduce transportation costs, support recycling and circular-economy goals, and make canned beverages more competitive across South Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory environmental compliance | -0.5% | National; compliance obligations under NEMWA EPR framework apply to all producers | Medium term (2-4 years) |

| Intense competition from alternative packaging formats | -0.6% | National; most acute in modern trade (supermarkets, hypermarkets) | Short term (≤ 2 years) |

| Environmental concerns despite recyclability | -0.3% | Urban consumer segments in Gauteng and Western Cape | Long term (≥ 4 years) |

| High packaging and manufacturing costs | -0.4% | National supply-side effect; most acute for smaller and mid-tier producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense competition from alternative packaging formats

Strong competition from other packaging formats is limiting the growth of the South Africa canned beverages market. Many consumers still prefer cheaper and familiar options such as PET bottles, aseptic cartons, and flexible pouches, especially for soft drinks, juices, bottled water, and ready-to-drink tea. These packaging formats often offer larger quantities at a lower cost per liter, appealing to price-sensitive buyers. PET bottles are also widely available, easy to carry, and supported by well-established production and distribution systems across South Africa. With inflation and rising living costs affecting purchasing decisions, consumers are becoming more careful about what they buy. As a result, beverage companies continue to invest in various packaging options rather than focusing solely on cans, slowing the growth of canned beverages across several non-alcoholic drink categories.

Mandatory environmental compliance

Mandatory environmental rules are slowing the growth of the South Africa canned beverages market because they make production and packaging more expensive for beverage manufacturers. Under South Africa's Extended Producer Responsibility (EPR) regulations, companies must help cover the costs of collecting, recycling, and properly handling packaging waste, including used cans. This increases overall operating costs and requires companies to invest more in recycling systems, reporting processes, and sustainability programs. Large beverage companies are usually better prepared to manage these requirements because they have stronger budgets and established recycling partnerships. However, smaller and mid-sized manufacturers may find it harder to meet these rules, as compliance can add financial pressure and require additional resources. As environmental regulations, packaging recovery targets, and sustainability reporting requirements continue to evolve, they create challenges for new entrants and raise the cost of doing business in the canned beverages market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Alcoholic Beverages Power Volume, Non-Alcoholic Formats Accelerate

Alcoholic beverages accounted for 67.38% of the South African canned beverages market in 2025, making them the largest product segment by revenue. Canned beer, cider, ready-to-drink (RTD) cocktails, and flavored alcoholic drinks remained widely popular among consumers. Many consumers preferred cans because they are easy to carry, chill quickly, and are convenient for outdoor and social occasions. Premium products and new flavor launches also supported demand, while strong availability across supermarkets, liquor stores, and convenience outlets helped the segment maintain its leading position.

The non-alcoholic beverages segment is expected to record the fastest CAGR of 6.47% during 2026-2031. Growth is driven by rising consumer interest in healthier, more convenient drink options. Demand is increasing for energy drinks, sparkling water, ready-to-drink coffee, iced tea, and low-sugar beverages. Manufacturers are also launching functional drinks with vitamins, minerals, and natural ingredients to attract health-conscious consumers. Wider retail availability, growing on-the-go consumption, and regular product innovation are expected to support the segment’s strong growth during the forecast period.

By Can Material: Aluminum Maintains Structural Lead, Steel Finds Growth in Niche Applications

Aluminum cans are expected to hold 68.41% of the South Africa canned beverages market in 2025, making them the leading packaging material. Beverage companies prefer them because they are light, strong, and easy to transport, which helps lower logistics costs. They also protect drinks well and help maintain freshness and quality for a longer period. Aluminum cans are easy to print on, allowing brands to use clear designs and attractive packaging. Their high recyclability and strong collection network also make them a preferred choice as companies focus more on sustainable packaging.

The steel and tinplate cans segment is projected to grow at the fastest CAGR of 6.06% during 2026–2031. These cans are gaining demand because they are strong, cost-effective, and suitable for specific beverage categories. They offer good product protection and support a longer shelf life, which makes them useful for long-distance distribution. New coatings that reduce corrosion and improvements in lightweight manufacturing are making steel cans more competitive. Growing investment in recyclable metal packaging is also expected to support the wider use of steel and tinplate cans during the forecast period.

By Category: Conventional Dominance with Organic as Fastest-Growing Challenger

Conventional canned beverages are expected to account for 87.35% of the South Africa canned beverages market in 2025, showing their strong position in the country’s beverage industry. These products remain popular because they are affordable, easy to find, and widely accepted across alcoholic and non-alcoholic beverage categories. Major brands continue to offer conventional canned beverages to meet demand from a large group of everyday consumers. Their wide availability through supermarkets, convenience stores, and wholesale outlets is expected to help the segment maintain its leading position over the forecast period.

The organic canned beverages segment is projected to grow at the fastest CAGR of 6.38% during 2026–2031, driven by rising consumer interest in health and wellness. More consumers are choosing drinks made with natural ingredients, clean labels, and fewer artificial additives. Premium product launches and better availability through modern retail stores and online platforms are also supporting the segment’s growth. Younger consumers and urban households are showing a higher willingness to pay more for organic beverage options, which is expected to strengthen demand during the forecast period.

By Distribution Channel: Off-Trade Anchors Volume, On-Trade Leads Growth

Off-trade channels accounted for 64.08% of the South African canned beverages market in 2025, making them the main channel through which consumers bought these products. This channel includes supermarkets, hypermarkets, convenience stores, liquor stores, and wholesale outlets. Consumers prefer these stores because they offer better prices, regular discounts, and the ease of buying drinks for home use. The strong availability of alcoholic and non-alcoholic canned beverages across these outlets continues to support the segment’s leading position.

The on-trade channels segment is expected to grow at the fastest CAGR of 6.85% during 2026–2031, supported by the recovery and growth of the hospitality industry. Restaurants, bars, pubs, hotels, and entertainment venues are selling more canned beverages as consumers spend more on social outings. Premium ready-to-drink beverages and craft alcoholic drinks are becoming more popular in these locations. Growth in tourism, social events, and dining-out trends is also expected to increase demand through this channel.

Geography Analysis

Gauteng, the Western Cape, and KwaZulu-Natal are the main demand centers for the South Africa canned beverages market. These provinces have large urban populations, well-developed retail networks, and higher consumer spending. Gauteng records strong beverage consumption because it is the country’s key economic hub. The Western Cape supports demand through rising interest in premium, craft, and organic beverages. KwaZulu-Natal also contributes through tourism activity, port infrastructure, and a broad retail network.

Tourism further increases demand for canned beverages in these provinces. Hotels, restaurants, bars, entertainment venues, and convenience stores sell more beverages in popular tourist locations. The Western Cape, Gauteng, and KwaZulu-Natal see strong demand for premium alcoholic beverages, ready-to-drink products, and refreshing non-alcoholic drinks. Seasonal travel, festivals, and outdoor activities also support higher beverage sales. The growing hospitality industry continues to make these provinces important to the national canned beverages market.

The Eastern Cape, Northern Cape, Free State, and Limpopo offer new growth opportunities for the market. These provinces have lower consumption levels than the main regions, but demand is gradually increasing. The Eastern Cape remains an important manufacturing hub, with beverage production facilities that support domestic distribution and regional exports. Better retail reach, urbanization, and the growth of modern trade formats are improving access to canned beverages in inland provinces. Continued investments in logistics and organized retail are expected to support long-term growth in these developing regional markets.

Competitive Landscape

The South Africa canned beverages market is moderately consolidated, with major players such as The Coca-Cola Company, PepsiCo, Inc., Anheuser-Busch InBev, Red Bull GmbH, and Monster Beverage Corporation holding strong positions across key beverage categories. These companies have wide distribution networks, strong brand portfolios, and high marketing reach. They sell their products through supermarkets, convenience stores, and hospitality channels. Their strong retail partnerships and steady product supply help them remain competitive in the market.

Companies in the market compete strongly through new products and not only through size or scale. This trend is clear in fast-growing categories such as energy drinks, ready-to-drink beverages, flavored alcoholic drinks, and functional beverages. Leading manufacturers are adding new flavors, premium products, and easy-to-carry packaging formats to meet changing consumer needs. They are also focusing on premiumization and product variety to strengthen their position in the market.

Sustainability and efficient packaging are becoming more important for companies in this market. Beverage manufacturers are investing in recyclable metal packaging and better packaging recovery systems. They are also working to meet changing environmental regulations in South Africa. These efforts support circular economy goals, improve brand value, and help companies compete through sustainability, operational efficiency, and regulatory compliance.

South Africa Canned Beverages Industry Leaders

-

The Coca-Cola Company

-

Anheuser-Busch InBev

-

PepsiCo, Inc.

-

Monster Beverage Corporation

-

Red Bull GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Castle Lite launched its new Draught in a Can at the LIV Golf South Africa tournament, broadening its draught beer portfolio with a portable canned format. The launch aimed to offer consumers a draught-style drinking experience beyond traditional on-premise settings.

- November 2025: SA Canegrowers, through its subsidiary Womoba, introduced Shesha, a sugarcane-based energy drink positioned as the world's first beverage to use fresh raw sugarcane juice as its primary ingredient.

- September 2025: Heineken Beverages expanded its packaging portfolio in South Africa by launching a 500ml aluminum can for Savanna Premium Cider, offering consumers a more portable and convenient format.

- May 2025: The Coca-Cola Company expanded its energy drink portfolio in South Africa with the launch of Charged, a strawberry-flavored caffeinated beverage available in 500ml cans.

South Africa Canned Beverages Market Report Scope

Canned beverages include ready-to-drink alcoholic and non-alcoholic drinks packaged in sealed metal cans for easy storage, transport, and consumption. The South Africa canned beverages market is segmented into product type, can material, category, and distribution channel. Based on product type, the market is classified into alcoholic and non-alcoholic beverages. Based on the can material, the market is classified into aluminum and steel/tinplate cans. Based on category, the market is classified into conventional and organic. Based on the distribution channel, the market is classified into on-trade and off-trade. The market forecasts are provided in terms of value (USD) and volume (Liters).

| Alcoholic Beverages | Beer |

| Wine | |

| Spirits | |

| Others | |

| Non-Alcoholic Beverages | Carbonated Soft Drinks |

| Energy Drinks | |

| Sports Drinks | |

| Juices | |

| RTD Tea and Coffee | |

| Others |

| Aluminum Cans |

| Steel/Tinplate Cans |

| Conventional |

| Organic |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Off-Trade Channels |

| By Product Type | Alcoholic Beverages | Beer |

| Wine | ||

| Spirits | ||

| Others | ||

| Non-Alcoholic Beverages | Carbonated Soft Drinks | |

| Energy Drinks | ||

| Sports Drinks | ||

| Juices | ||

| RTD Tea and Coffee | ||

| Others | ||

| By Can Material | Aluminum Cans | |

| Steel/Tinplate Cans | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Off-Trade Channels | ||

Key Questions Answered in the Report

What is the projected value of South Africa canned beverages demand by 2031?

The South Africa canned beverages market is projected to reach USD 575.47 million by 2031, rising from USD 441.29 million in 2026 at a 5.51% CAGR.

Which product type contributes the most to canned beverage sales in South Africa?

Alcoholic beverages led the product mix with 67.38% share in 2025, supported mainly by beer, cider, and ready-to-drink alcohol formats.

Which material leads beverage can usage in South Africa?

Aluminum cans held 68.41% share in 2025 because of strong printability, lightweight handling, and established recycling systems.

Why are on-trade channels growing faster than off-trade channels?

On-trade is forecast to grow at 6.85% CAGR through 2031 because tourism, conferences, hotels, bars, and leisure venues are expanding beverage consumption occasions.

Page last updated on: