Solid Phase Peptide Synthesis Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

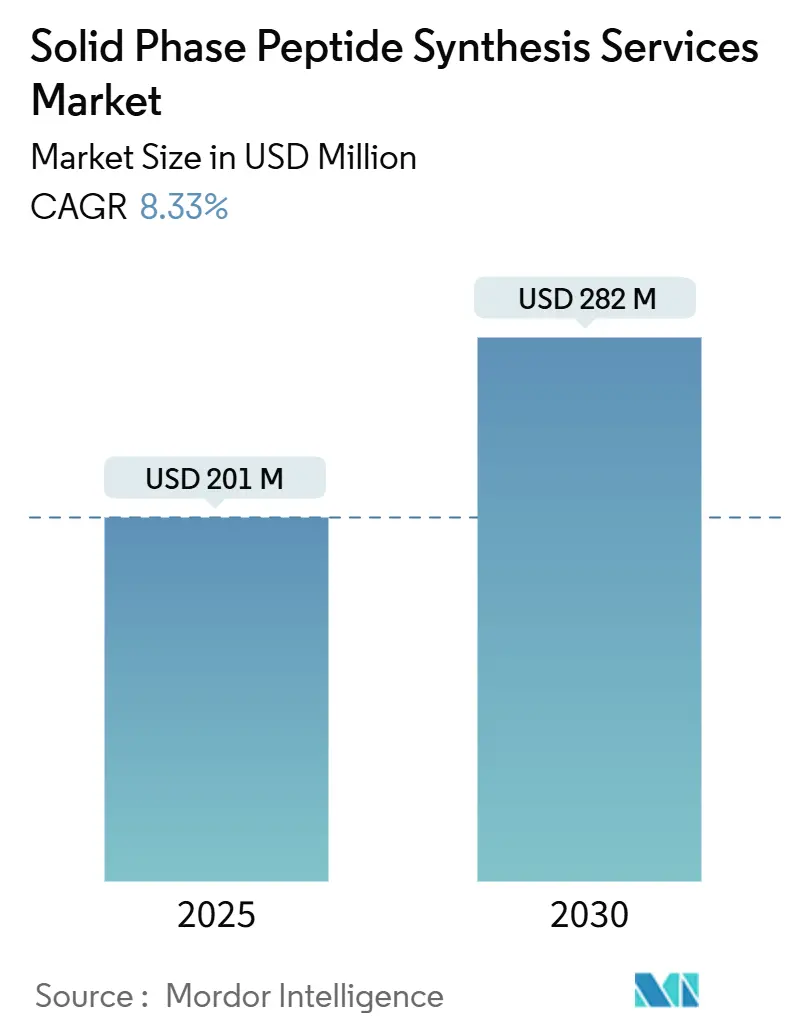

| Market Size (2025) | USD 201 Million |

| Market Size (2030) | USD 282 Million |

| Growth Rate (2025 - 2030) | 8.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solid Phase Peptide Synthesis Services Market Analysis by Mordor Intelligence

The Solid Phase Peptide Synthesis Services Market size is estimated at USD 201 million in 2025, and is expected to reach USD 282 million by 2030, at a CAGR of 8.33% during the forecast period (2025-2030).

Rising demand for multi-tonne GLP-1 receptor agonists, accelerating adoption of continuous-flow and microwave synthesizers, and the fast-growing pipeline of personalized neo-antigen cancer vaccines serve as the primary growth engines for the solid phase peptide synthesis services market. Contract development and manufacturing organizations (CDMOs) are scaling 5,000-liter to 10,000-liter reactors to secure long-term volume commitments from large pharma, while academic laboratories and small biotech firms continue to request rapid, gram-scale batches. The shift toward on-site micro-factories at hospital networks is creating a new service tier that prizes turnaround speed over unit cost. Meanwhile, higher resin and protected amino-acid prices and purification bottlenecks beyond 1 kg remain structural headwinds across the solid phase peptide synthesis services market.

Key Report Takeaways

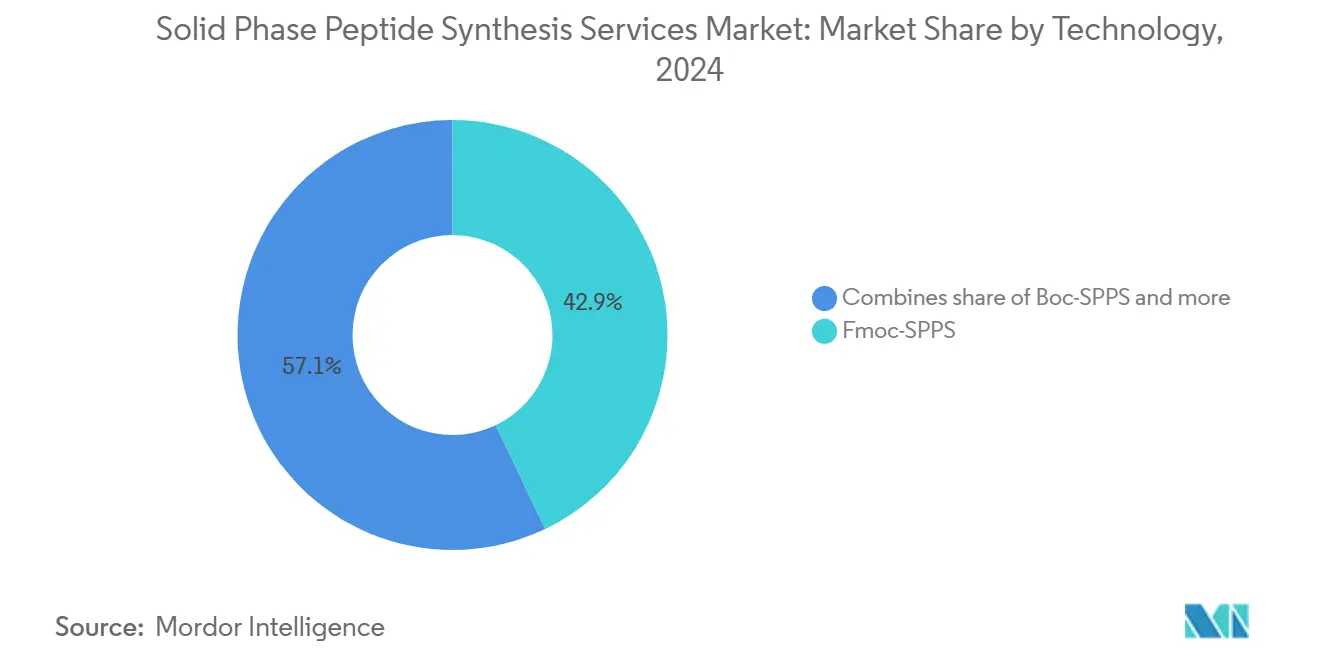

- By technology, Fmoc-SPPS led with 42.9% of the solid phase peptide synthesis services market share in 2024, while microwave-assisted synthesis is advancing at a 12.4% CAGR to 2030.

- By end user, pharmaceutical and biotechnology companies held 48.6% revenue share in 2024; CDMOs and CROs record the fastest expansion at 10.8% CAGR through 2030.

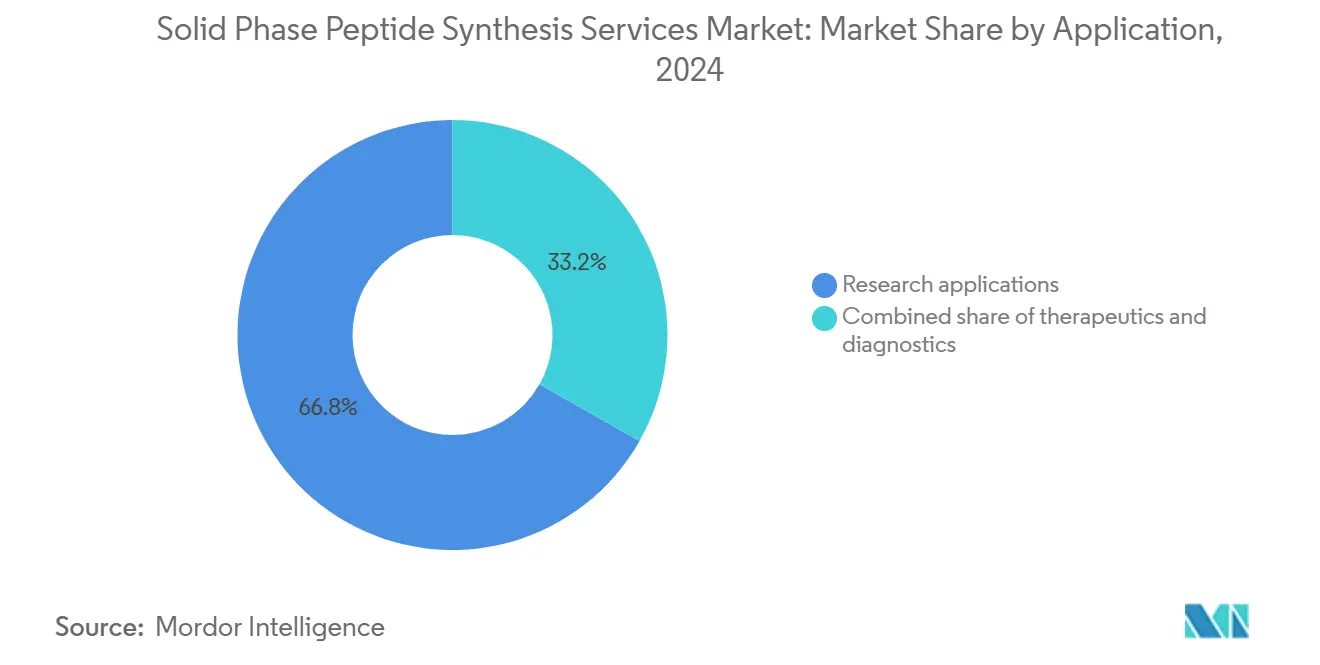

- By application, research accounted for 66.8% of the solid phase peptide synthesis services market size in 2024, whereas diagnostics is projected to rise at an 11.2% CAGR between 2025 and 2030.

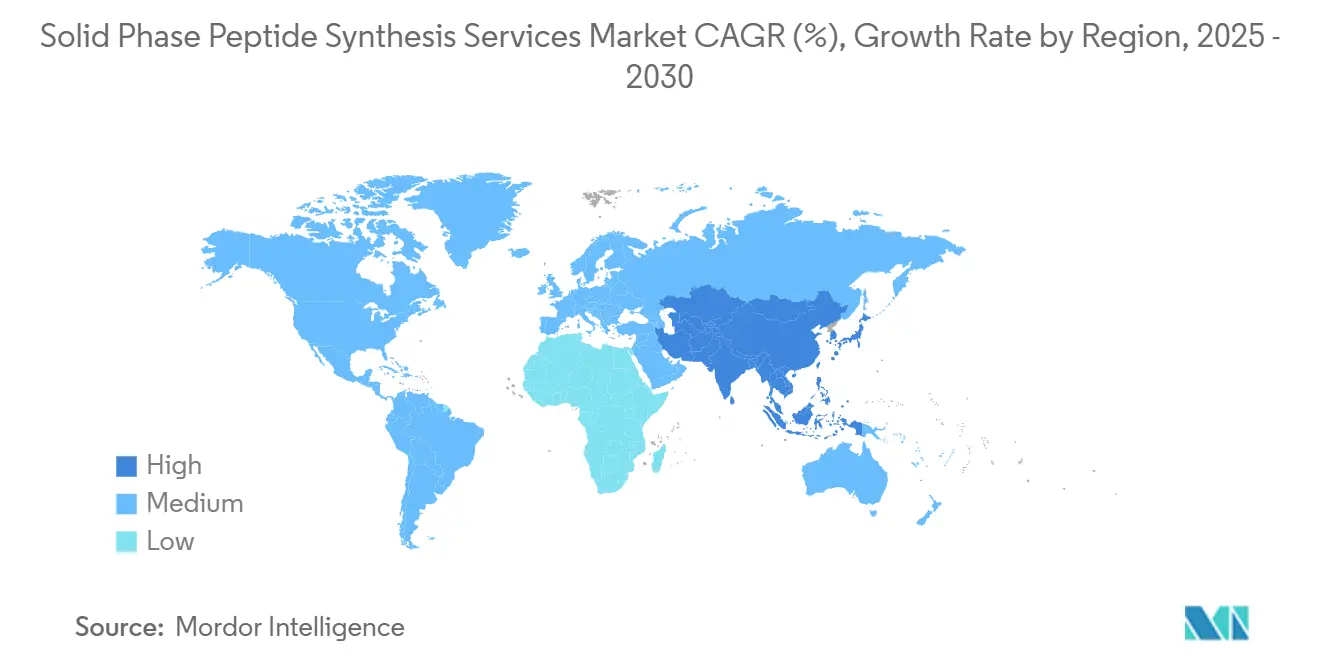

- By geography, North America commanded 38.9% of 2024 demand, yet Asia-Pacific is poised to register the fastest growth at 10.5% between 2025 and 2030.

Global Solid Phase Peptide Synthesis Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 agonist boom boosting large-scale SPPS outsourcing | +2.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Automation and high-throughput synthesizers | +1.5% | Global, early adoption in North America & Asia-Pacific | Short term (≤ 2 years) |

| Expanding clinical peptide pipeline | +2.1% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Pharma capacity constraints favoring CDMO partnerships | +1.4% | North America & Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| On-site neo-antigen vaccine micro-factories | +0.8% | North America & Europe | Long term (≥ 4 years) |

| Peptide-radiopharmaceutical theragnostics | +0.9% | Global, regulatory momentum in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GLP-1 Agonist Boom Boosting Large-Scale SPPS Outsourcing

The rising demand for GLP-1 antagonist is expected to significantly contribute in growing demand of phase peptide synthesis services. Eli Lilly’s cumulative USD 18 billion outlay for tirzepatide plants and Bachem’s CHF 1 billion five-year supply contract highlight how branded peptide blockbusters overwhelm in-house capacity, pushing orders toward specialized CDMOs. Site-specific lipidation and 30-plus-residue sequences make SPPS the dominant route despite higher cost per gram versus recombinant biologics. Each 5,000-liter reactor delivers roughly 5-8 kg per batch, obliging suppliers to run overlapping campaigns to meet annual demand. Contract manufacturers therefore invest in parallel chromatography trains and solvent-recovery loops to mitigate cycle-time constraints across the solid phase peptide synthesis services market.

Automation & High-Throughput Synthesizers Slashing Cost Per Residue

Microwave instruments cut coupling steps from hours to minutes, enabling a single Liberty Blue unit to output 20-30 peptides daily with 99.5% efficiency [1]CEM Corporation, “Liberty Blue Peptide Synthesizer,”. Continuous-flow reactors lower solvent use by 40% while reducing batch-to-batch variability. The FDA’s 2024 guidance supporting continuous manufacturing grants early adopters a regulatory head start [2]U.S. Food and Drug Administration, “Continuous Manufacturing for Pharmaceutical Products,” . Automated mega scale lines in China and South Korea showcase how digital controls and inline analytics shrink labor dependence, strengthening price competitiveness across the solid phase peptide synthesis services market.

Expanding Clinical Peptide Pipeline Driving GMP Demand

Roughly 150 peptide candidates are in active trials, 38 of which sit in Phase III for oncology or metabolic disease indications. Personalized neo-antigen vaccines from BioNTech and Moderna require 10-20 patient-specific peptides within eight weeks, spawning a fast-turnaround micro-factory model tied to regional hospital systems. The FDA now allows abbreviated stability testing for these batches, halving time-to-clinic and solidifying a premium niche within the solid phase peptide synthesis services market.

Pharma Capacity Constraints Favoring CDMO/CRO Partnerships

Outsourcing reached 70% of small-molecule volume in 2024 as large pharma redeployed capital toward biologics and cell therapies. North American reshoring efforts encouraged Bachem’s Vista, California scale-up and CordenPharma’s 42,000-liter expansion in Boulder, closing the gap left by potential BIOSECURE Act restrictions on Chinese supply. These moves increase regional redundancy and boost premium pricing power across the solid phase peptide synthesis services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prices of specialty resins & protected amino acids | -1.2% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Scale-up limits beyond 1 kg | -0.9% | Global, major hubs | Medium term (2-4 years) |

| Stricter impurity specifications elongate validation cycles | -0.6% | North America & Europe | Medium term (2-4 years) |

| Enzymatic cell-free peptide factories emerging | -0.5% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Prices of Specialty Resins & Protected Amino Acids

China supplies roughly two-thirds of protected amino acids, exposing Western buyers to currency swings and quality variability. Price jumps of 20-30% since 2024 for Wang and Rink resins have lengthened lead times to 16–20 weeks. Dual-sourcing from European vendors at a significant markup protects compliance but compresses gross margin across the solid phase peptide synthesis services market.

Scale-Up Limits Hamper Blockbuster Production

Purification represents up to 60% of manufacturing cost for 30-residue peptides. Three sequential HPLC steps limit batch size to 8 kg, forcing parallel campaigns and raising failure risk to 15–20% during validation. Continuous-flow SPPS helps but capital expenditure and process-specific hardware slow uptake to less than 10% of commercial volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Microwave Acceleration Reshapes Synthesis Economics

Microwave-assisted platforms captured rapid adoption by shrinking cycle time to 15 minutes and cutting energy use by 50%, placing them on a 12.4% CAGR trajectory toward 2030. FMOC-SPPS retained 42.9% share of the solid phase peptide synthesis services market size in 2024 based on equipment familiarity and compatibility with acid-labile sequences. Boc-SPPS persists for peptides that demand harsher deprotection, often those bearing multiple disulfide bonds, while continuous-flow lines remain below 5% today but are expected to reach double-digit penetration once CordenPharma’s PeptiSystems pilot plant scales in 2026.

Sustainability mandates under the European Green Deal give early adopters of microwave and flow systems a compliance edge. Automation allows 30-40% higher throughput per technician, supporting aggressive delivery timelines that win discovery-stage contracts. Chinese giants deploying fully robotic 10,000-liter lines are challenging Western incumbents on both price and volume, yet BIOSECURE legislation limits their U.S. access, partially insulating the North American solid phase peptide synthesis services market.

By End User: CDMO Ascendancy Reflects Pharma’s Capital Reallocation

Pharmaceutical and biotechnology organizations held 48.6% revenue in 2024, chiefly due to proprietary pipeline projects. Nevertheless, CDMOs and CROs are expected to outpace them at 10.8% CAGR as outsourcing surpasses 70% of production needs. The solid phase peptide synthesis services market size allocated to CDMOs will widen because mid-tier companies prefer asset-light models, while onshoring pressures push contracts to North American and European specialists.

Emerging CRDMO players now bundle design, synthesis, and scale-up under one roof, capturing end-to-end programs valued at USD 5–10 million each. Academic institutes, although the smallest slice, wield outsized influence on novel modalities such as cyclic and stapled peptides. Persistent raw-material inflation and the 0.1% EBITDA margin recorded by PolyPeptide highlight the profitability squeeze in pure-play models, advocating for either scale or specialization across the solid phase peptide synthesis services market.

By Application: Diagnostics Surge Driven by Peptide Biomarkers

Research applications remained dominant at 66.8% share in 2024 owing to antibody production and structural biology needs, but diagnostics is set to climb at 11.2% CAGR. Early cancer-detection assays and metabolic biomarker kits adopt synthetic peptides as calibration standards, securing reimbursement and regulatory clearance. Therapeutics command premium pricing because GMP requirements elevate cost per gram to USD 500–2,000.

Neo-antigen vaccines blur boundaries between therapy and diagnostics, with each patient requiring bespoke peptide pools synthesized within six weeks. Radiopharmaceutical theragnostics further boost demand for impurity thresholds below 0.1%, creating a protected high-margin niche within the solid phase peptide synthesis services market

Geography Analysis

North America led with 38.9% value share in 2024, driven by Bachem’s Vista scale-up to nearly 1 tonne per year and CordenPharma’s 42,000-liter Boulder plant, both designed to supply reshore-ed GLP-1 APIs. Incentives embedded in proposed BIOSECURE legislation encourage further onshoring, while academic funding sustains a robust discovery ecosystem that feeds gram-scale service demand. Pricing premiums of 15–20% compared with Asian suppliers persist owing to shorter logistics chains and perceived regulatory advantages.

Europe follows closely, anchored by Switzerland’s peptide corridor where Bachem, PolyPeptide, and CordenPharma deploy multi-kilogram reactors and continuous-flow pilots. The EUR 500 million Muttenz build-out slated for 2028 will lift regional capacity and support blockbuster contracts. Environmental compliance costs under REACH elevate operating expenses yet favor microwave systems that reduce solvent use.

Asia-Pacific is the fastest-growing at 10.5% CAGR as South Korea’s SK Pharmteco invests USD 260 million in a 12,600 square-meter site and Chinese CDMOs add fully automated 10,000-liter lines [3]SK Pharmteco, “USD 260 million Peptide Plant,”. Although BIOSECURE restrictions limit direct U.S. supply, Asian firms pivot to European and regional clients. India’s 11.34% advance reflects its “China-plus-one” positioning, and government incentives lower capital outlays for new SPPS capacity. Collectively, these dynamics increase competitive density yet expand the overall pie for the solid phase peptide synthesis services market

Competitive Landscape

Five players Bachem, PolyPeptide Group, GenScript, Thermo Fisher Scientific, and CordenPharma command the majority of revenue, making the solid phase peptide synthesis services market moderately concentrated. Scale-focused firms pour hundreds of millions into 5,000-liter reactors to secure long-term GLP-1 orders, while specialization-focused peers target cyclic, conjugated, or radiolabeled peptides that fetch three-to-five-fold premiums. Capital intensity and 18–36-month paybacks pose entry barriers.

Technology differentiation is critical: CEM’s microwave instruments and CordenPharma-PeptiSystems continuous-flow lines deliver 50–60% cost savings, enticing price-sensitive accounts. Chinese CDMOs leverage extensive automation to offset labor gains but face geopolitical headwinds. Emerging enzymatic synthesis platforms remain pre-commercial yet threaten to disrupt the incumbent SPPS cost curve once regulatory comparability is proven.

Profitability pressure is acute; PolyPeptide’s 5.3% gross margin and near-break-even EBITDA reflect resin inflation and purification bottlenecks. Vertical integration into conjugation or final drug-product fill-finish, plus focus on ultra-complex peptides, will be decisive for margin recovery across the solid phase peptide synthesis services market.

Solid Phase Peptide Synthesis Services Industry Leaders

Bachem Holding AG

PolyPeptide Group

Ambio Pharmaceuticals

CPC Scientific Inc.

GenScript Biotech Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: SK Pharmteco announced a USD 260 million South Korean peptide facility, employing 300 staff, set for late-2026 launch.

- August 2024: Bachem secured a USD 531 million five-year supply agreement effective 2027–2031, one of the largest peptide contracts to date.

- May 2024: Eli Lilly confirmed a USD 5.3 billion Indiana expansion, part of USD 9 billion total, boosting tirzepatide capacity by 2026.

Global Solid Phase Peptide Synthesis Services Market Report Scope

As per the scope of the report, solid phase peptide services are specialized contract or custom synthesis offerings provided by biotech, CROs, and peptide manufacturing companies to produce synthetic peptides for research, diagnostics, and therapeutics.

The solid phase peptide services market is segmented by technology, end user, application, and geography. By technology, the market is categorized into Fmoc-SPPS, Boc-SPPS, microwave-assisted SPPS, and continuous-flow SPPS. By end user, it is segmented into pharmaceutical & biotechnology companies, CDMOs & CROs, and academic & research institutes. By application, the market is divided into therapeutics, diagnostics, and research. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Fmoc-SPPS |

| Boc-SPPS |

| Microwave-assisted SPPS |

| Continuous-flow SPPS |

| Pharmaceutical & Biotechnology Companies |

| CDMOs & CROs |

| Academic & Research Institutes |

| Therapeutics |

| Diagnostics |

| Research |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Fmoc-SPPS | |

| Boc-SPPS | ||

| Microwave-assisted SPPS | ||

| Continuous-flow SPPS | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| CDMOs & CROs | ||

| Academic & Research Institutes | ||

| By Application | Therapeutics | |

| Diagnostics | ||

| Research | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the solid phase peptide synthesis services market in 2025?

The sector is valued at USD 201 million in 2025 and is forecast to expand to USD 282 million by 2030, reflecting an 8.33% CAGR.

Which region leads current spending on peptide projects?

North America holds 38.9% of global revenue, backed by recent capacity expansions in California and Colorado.

What technology is growing fastest?

Microwave-assisted solid phase peptide synthesis is accelerating at a 12.4% CAGR thanks to 15-minute cycle times and high coupling efficiency.

Why are CDMOs gaining share?

Outsourcing exceeds 70% because pharma reallocates capital to biologics, and BIOSECURE legislation pushes U.S. contracts toward regional suppliers.

Page last updated on: