Solid Phase Extraction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.42 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

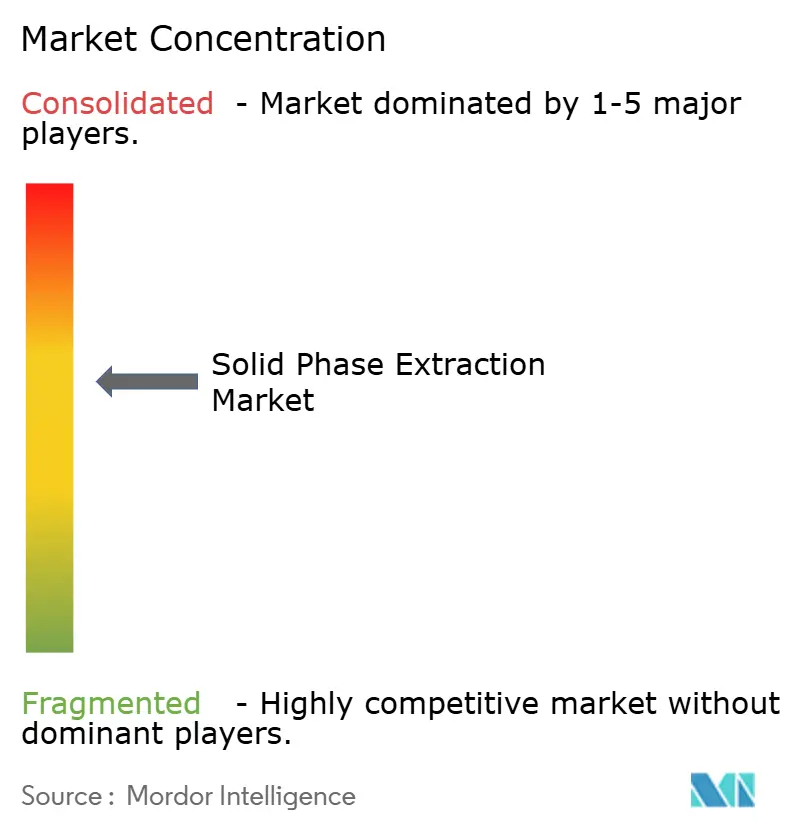

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Solid Phase Extraction Market Analysis by Mordor Intelligence

The Solid Phase Extraction Market size was valued at USD 1.87 billion in 2025 and is estimated to grow from USD 1.94 billion in 2026 to reach USD 2.42 billion by 2031, at a CAGR of 4.54% during the forecast period (2026-2031).

The solid phase extraction market is being supported by pharmaceutical bioanalysis needs, stricter environmental testing rules, and rising forensic workload in North America and parts of Europe. Demand is also moving toward higher-performing cartridges and mixed-mode sorbents because biologics, oligonucleotide drugs, monoclonal antibodies, and cell and gene therapy samples require cleaner extraction from difficult matrices than older methods can provide. At the same time, the solid phase extraction market faces slower capital spending from contract testing laboratories, while procurement uncertainty has delayed some automated platform purchases in Europe and Asia. Reproducibility across different matrices also remains a practical barrier, especially where workflows are decentralized or method transfer is limited. Even with these constraints, the solid phase extraction market continues to have firm support from biotherapeutic pipeline growth, PFAS compliance deadlines, and the need for faster and more traceable laboratory workflows.

Key Report Takeaways

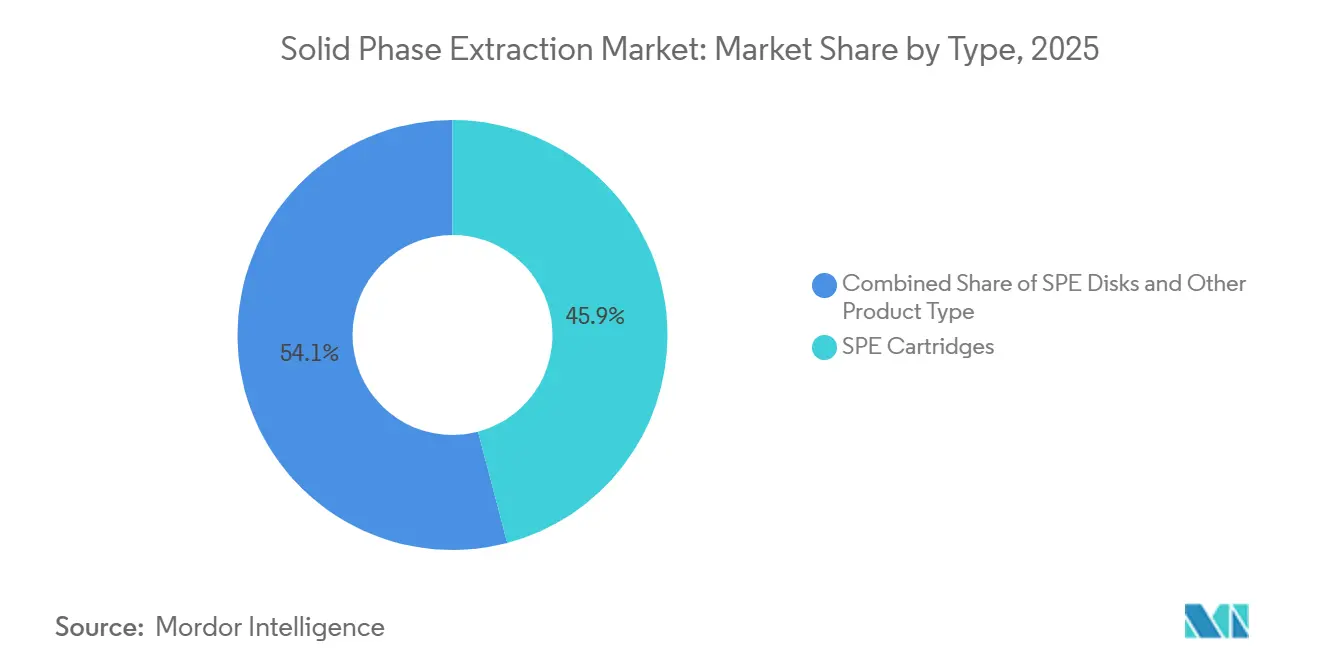

- By type, SPE cartridges held 45.90% revenue share in 2025, while SPE disks are forecast to expand at a 6.10% CAGR through 2031.

- By application, the pharmaceutical industries accounted for 26.94% share in 2025, while academic and research institutes are projected to record the fastest 6.60% CAGR through 2031.

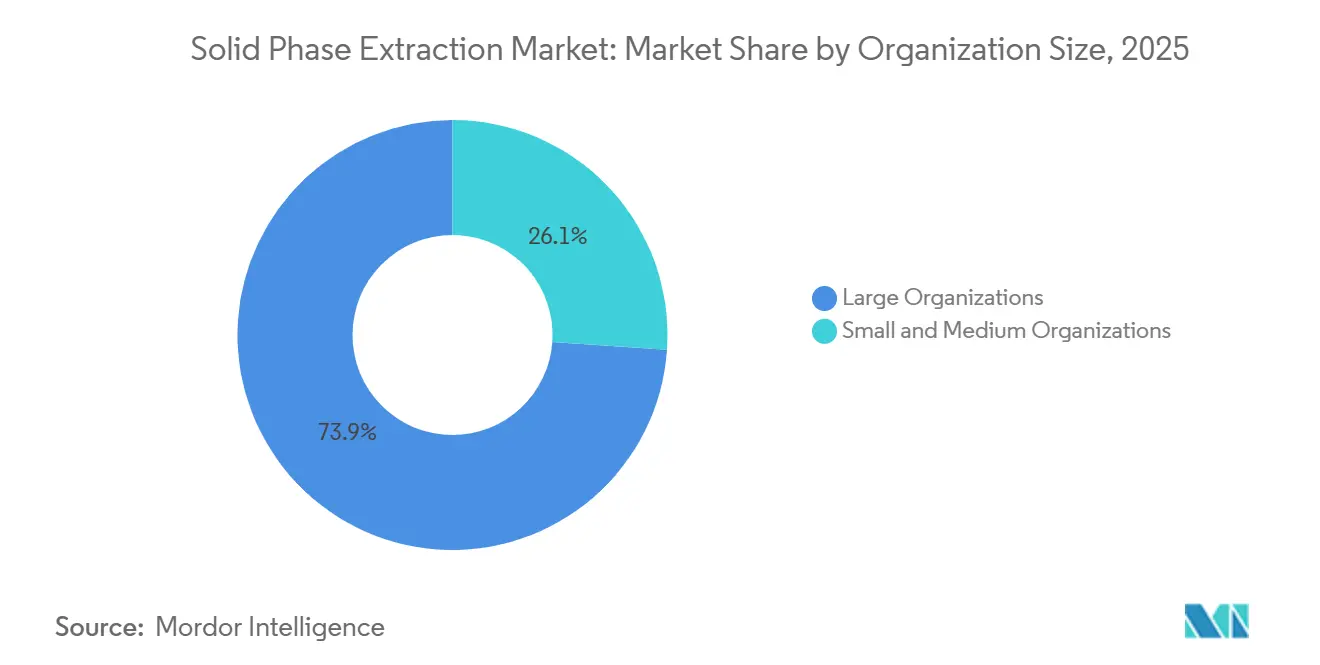

- By organization size, the large organizations accounted for 73.88% share in 2025, while small and medium organizations are projected to record the fastest 5.82% CAGR through 2031.

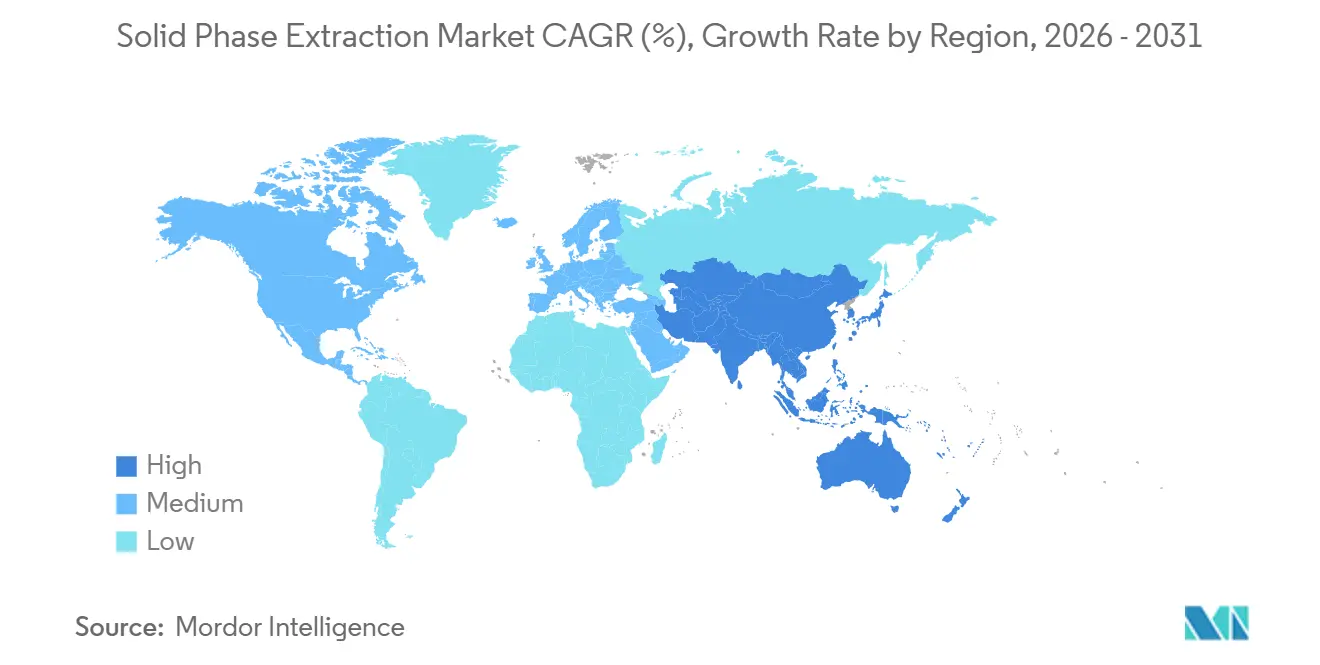

- By geography, North America held 38.80% of revenue in 2025, while Asia-Pacific is expected to grow at the fastest 6.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solid Phase Extraction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Purity Sample Preparation in Pharmaceuticals | +1.3% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Tighter Environmental and Food Safety Compliance Requirements | +1.1% | Global, peak impact in North America and Europe | Short term (≤ 2 years) |

| Shift Toward Automation and High-Throughput Laboratory Workflows | +0.8% | Global, early gains in North America, Europe, and Japan | Medium term (2-4 years) |

| Adoption of Novel Sorbent Chemistries for Complex Matrices | +0.5% | North America and Europe, with spillover to core Asia-Pacific markets | Long term (≥ 4 years) |

| Growth in Forensic, Toxicology, and Cannabis Testing Workflows | +0.4% | North America, with emerging traction in Europe | Short term (≤ 2 years) |

| Rising Use of SPE in Decentralized and Contract Testing | +0.3% | Global, with early gains in North America, India, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Purity Sample Preparation in Pharmaceuticals

Pharmaceutical bioanalysis is asking for cleaner sample preparation because newer drug types are harder to handle than standard small molecules. Oligonucleotide therapeutics, antibody drug conjugates, and cell and gene therapy programs need extraction methods that can deal with tissue homogenates, whole blood, and other difficult matrices. Biotage introduced Biotage Oligo SPE in June 2025 with mixed-mode weak anion exchange chemistry and pore design aimed at oligonucleotide work, and the company stated that the product delivered up to 40 times greater LC-MS/MS signal sensitivity than competitor methods in tissue biodistribution studies [1]Biotage, “Launch of Biotage PrepXpert-8 Smart Automation System for Sample Prep,” Biotage, biotage.com. Phenomenex followed in September 2025 with Clarity OTX Pro, which the company said delivered 90% recovery from complex biological matrices without method re-optimization. These launches show that the solid phase extraction market is not only growing with pharmaceutical volumes but is also moving toward higher-value sorbents designed for specific therapeutic modalities.

Tighter Environmental and Food Safety Compliance Requirements

Environmental and food safety rules are creating one of the clearest near-term demand triggers for the solid phase extraction market. The US EPA finalized Method 1633 in January 2024, and the method covers 40 PFAS compounds across non-potable water, soil, biosolids, and tissue matrices using SPE with WAX cartridges and graphitized carbon black cleanup. In Europe, the Drinking Water Directive set binding PFAS limits and required member-state compliance by January 2026, which created a direct buying event for validated PFAS-grade SPE products across laboratories. These mandates also narrow supplier choice because only low-residual, pre-verified cartridges can reliably meet strict acceptance criteria in regulated testing. The same pattern extends into food testing as pesticide monitoring lists continue to expand, which keeps routine sample preparation demand active in regulated laboratories.

Shift Toward Automation and High-Throughput Laboratory Workflows

Automation is reducing manual handling while making reproducibility easier to document in regulated laboratories. Biotage launched PrepXpert-8 in August 2025, and the system was presented as an 8-channel smart automation platform with real-time clog detection, dual-method operation, and traceable run reporting for regulated environments. Waters also published workflow material for automated PFAS sample preparation under EPA Method 1633, showing how automated execution is moving from an optional efficiency tool to a routine laboratory requirement. As volumes increase, automated platforms become more attractive because they cut analyst time and produce more consistent extraction across batches. This is pushing the solid phase extraction market into a split structure where high-volume laboratories adopt dedicated automated systems, while smaller laboratories stay on manual cartridge workflows.

Adoption of Novel Sorbent Chemistries for Complex Matrices

New sorbent chemistry is expanding the range of compounds that can be handled through SPE workflows. A 2025 study in Polymer Chemistry showed that amphoteric polydivinylbenzene microspheres with both weak anion and weak cation exchange character could extract acidic and basic pharmaceuticals from water samples at quantification limits as low as 1 ng/L. A 2025 study in Food Chemistry: X also reported that MOF-on-MOF composite sorbents improved selectivity in dispersive micro-SPE for pesticide extraction from food samples. A separate 2025 review in Trends in Analytical Chemistry noted that nanomaterial-based and hybrid sorbents are becoming more visible in specialized SPE workflows, even though routine-scale cost and aggregation issues still remain. These developments matter for the solid phase extraction market because they support a future pipeline of differentiated consumables rather than simple volume growth in standard formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Automated SPE Platforms and Ancillary Equipment | -0.8% | Global, most acute in emerging Asia-Pacific markets and smaller CROs | Medium term (2-4 years) |

| Method Development Complexity Across Diverse Sample Matrices | -0.5% | Global, concentrated in environmental and forensic testing laboratories | Medium term (2-4 years) |

| Sorbent Performance Variability and Reproducibility Challenges | -0.4% | Global, most acute in decentralized and contract testing | Long term (≥ 4 years) |

| Stringent Manufacturing and Environmental Regulations | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Automated SPE Platforms and Ancillary Equipment

Automated SPE systems still face a meaningful adoption barrier because full workstation setups can be expensive for many laboratories. Fully integrated systems, including solvent delivery, fraction collection, evaporation, and downstream interfacing capabilities, can exceed USD 100,000 per installation. This burden is heavier for smaller contract testing laboratories and academic facilities that do not buy instruments through large procurement programs. Vendors are introducing smaller systems such as Biotage's PrepXpert-8, but lower-volume automation does not fully solve the economics gap for the most cost-sensitive users. The result is a two-speed adoption pattern inside the solid phase extraction market, where large regulated labs automate faster and smaller users stay with manual workflows.

Method Development Complexity Across Diverse Sample Matrices

Method development remains difficult because SPE performance can change sharply from one sample matrix to another. A protocol that works in clean plasma may not transfer easily to postmortem samples, soil extracts, or cannabis-derived matrices without repeated sorbent screening and pH optimization. A 2026 Bioanalysis paper described a fully automated siRNA tissue SPE method that still required validation across 9 tissue types and 3 species, which shows how resource-intensive advanced workflows can be. This slows adoption and can also affect assay quality when laboratories compress validation work under time pressure. It also creates pricing room for validated kits such as Phenomenex's oligonucleotide offering because ready-to-run methods save specialist time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cartridge Formats Anchor Revenue While Disk Adoption Accelerates in Environmental Workflows

SPE cartridges held 45.90% of solid phase extraction market share in 2025, which kept them as the leading type because they combine broad chemistry choice with compatibility across manual and automated workflows. The format remains difficult to displace because cartridges are available in many volume ranges and support sorbents such as C18, HLB, WAX, SAX, SCX, mixed-mode, and application-specific chemistries. Regulatory methods continue to reinforce this position because EPA Method 1633 and other compliance frameworks are centered on cartridge-based sample preparation for PFAS and related testing needs[2]"Per- and Polyfluoroalkyl Substances (PFAS), Final PFAS National Primary Drinking Water Regulation", epa.gov/sdwa/and-polyfluoroalkyl-substances-pfas. The 2025 launches of Biotage Oligo SPE and Phenomenex Clarity OTX Pro also show that cartridges are still where suppliers place premium pharmaceutical innovation. That pricing power matters because the solid phase extraction industry is not relying only on unit growth, but also on a richer product mix within cartridges.

SPE disks are projected to expand at a 6.10% CAGR through 2031, making them the fastest-growing type as large-volume aqueous testing becomes more common. Their advantage is speed because they can process high sample volumes at stronger flow rates than many cartridge setups, which is useful in water monitoring programs scaling PFAS workloads. TThis trend directly aligns with environmental testing demand, where batch efficiency and shorter extraction times deliver clear operational value. MACHEREY-NAGEL also plans to introduce a 96-well SquareWell format in 2025, increasing per-well sample volume while maintaining compatibility with existing automated systems. This development indicates that throughput-oriented format innovation is expanding beyond conventional cartridges. Other types, such as 96-well plates and pipette-tip formats, are also gaining ground in genomics and proteomics workflows, where miniaturization and robotic handling are more important than bulk liquid processing.

By Application: Pharmaceutical Demand Remains the Structural Anchor, Academics Drive Fastest Volume Growth

Pharmaceutical industries accounted for 26.94% of the solid phase extraction market size in 2025, which kept this application area as the main revenue anchor. The segment benefits from strict regulatory expectations in drug development, where recovery, reproducibility, and matrix cleanup need to support validated LC-MS/MS analysis. Pharmaceutical demand is increasingly linked to the expansion of biologics and oligonucleotide pipelines, which require more advanced sample preparation than legacy small-molecule workflows. A 2025 Journal of Separation Science study reported very strong analytical performance for an HLB-based SPE cartridge method in liposomal oncology drug formulations, which supports the role of SPE in tightly controlled pharmaceutical testing. Hospitals and clinics remain smaller, but they continue to add demand in therapeutic drug monitoring and toxicology screening, where automation can reduce per-sample labor.

Academic and research institutes are forecast to record the fastest 6.60% CAGR from 2026 to 2031, which gives this segment growing strategic importance in the solid phase extraction market. Michigan State University completed a USD 2.2 million renovation of its Mass Spectrometry and Metabolomics Core in June 2025, and Louisiana State University also announced a 2025 enhancement grant for sample preparation and detection upgrades. These facilities matter because academic laboratories work across many analytes and matrix combinations, which creates repeat demand for varied sorbent portfolios. Environmental testing, food and beverage testing, and forensic and toxicology testing also add meaningful revenue, but they do not displace the central role of pharmaceutical demand. The solid phase extraction industry, therefore, has one application base that protects current revenue and another that widens future research-led consumable demand.

By Organization Size: Large Organizations Remain the Core Revenue Base While Smaller Firms Expand Faster

Large organizations accounted for 73.88% of the segment, reflecting their stronger purchasing capacity, broader laboratory infrastructure, and greater ability to adopt validated sample preparation workflows at scale. Their position is also supported by higher testing volumes across pharmaceutical, environmental, and regulated analytical settings where consistency, traceability, and throughput remain critical. These users are better placed to invest in premium cartridges, specialized sorbents, and automation-compatible formats that improve workflow reliability. They also tend to work within stricter compliance environments, which supports repeat demand for established solid phase extraction products. As a result, large organizations continue to form the main revenue base for suppliers serving this market.

Small and medium organizations are projected to grow at the fastest CAGR of 5.82%, showing that demand is widening beyond the largest institutional buyers. This growth is likely to come from expanding contract testing activity, rising outsourcing in analytical services, and broader access to application-specific SPE solutions. Smaller laboratories are also adopting products that reduce method complexity and improve routine testing efficiency without requiring full-scale automation. In many cases, these buyers prefer practical, validated formats that can fit existing workflows and budget limits. This trend should gradually broaden the customer base, even though large organizations are expected to remain dominant over the forecast period.

Geography Analysis

North America held 38.80% of revenue in 2025, which made it the leading regional block in the solid phase extraction market. The region benefits from a high concentration of pharmaceutical CROs, regulated environmental laboratories, and federally funded research infrastructure. The United States remains the core driver because EPA Method 1633 created a direct procurement requirement for WAX-based SPE workflows across PFAS testing programs. The EPA's PFAS drinking water compliance path also extends demand beyond the first purchase cycle because laboratories will continue supporting compliance needs through 2029. Canada adds support through environmental monitoring and biopharma activity, while Mexico contributes through pharmaceutical manufacturing expansion tied to regional investment flows.

Europe remained the second-largest regional contributor, with Germany, the United Kingdom, and France serving as the main revenue centers. The region's position rests on established pharmaceutical manufacturing, contract research, and food safety testing capacity. The January 2026 compliance deadline under the EU Drinking Water Directive created immediate pull for PFAS-validated SPE products across environmental laboratories. This has favored suppliers that already had verified PFAS-focused cartridge portfolios and established technical support for regulated applications.

Asia-Pacific is projected to expand at a 6.57% CAGR through 2031, making it the fastest-growing regional segment in the solid phase extraction market. Growth in the region comes from pharmaceutical manufacturing expansion, stricter environmental oversight, and a wider institutional research base. China is adding compliance demand for analytical protocols in water and soil monitoring, which follows the same regulatory pattern seen earlier in North America and Europe. Japan is also contributing, and GL Sciences reported positive FY2025 results partly linked to domestic growth in SPE cartridges and LC columns for pharmaceutical and environmental uses. India is becoming more important as a source of generic drug makers, and CROs take on more outsourced bioanalytical work that needs FDA- and EMA-aligned methods. The Middle East and Africa and South America remain smaller in scale. However, these regions are expected to record gradual growth as environmental and pharmaceutical quality systems increasingly align with international standards.

Competitive Landscape

The solid phase extraction market shows moderate concentration, with Thermo Fisher Scientific, Waters Corporation, Agilent Technologies, Merck KGaA, and Phenomenex holding a strong position in regulated pharmaceutical and environmental testing. Their advantage comes from offering SPE consumables inside wider analytical workflows rather than selling cartridges as stand-alone items. This makes supplier choice stickier because laboratories often prefer product families that fit with their existing chromatography and sample preparation setups. It also means competition is shaped as much by workflow compatibility and validation support as by cartridge price alone.

Waters has strengthened its position by linking Oasis SPE products closely with broader laboratory workflows for PFAS and regulated testing applications. Thermo Fisher moved in February 2025 to acquire Solventum's Purification & Filtration business for USD 4.1 billion in cash, which broadens its purification reach and supports downstream synergies around sample preparation and laboratory workflows. Waters and BD announced a USD 17.5 billion combination in July 2025, which would expand Waters' role in clinical, diagnostic, and other regulated high-volume testing environments. Merck KGaA also signed a definitive agreement in October 2025 to acquire the chromatography business of JSR Life Sciences, extending its downstream bioprocessing portfolio. These moves show that leading companies are using acquisition and workflow expansion, not only product launches, to improve their position in the solid phase extraction market.

Mid-tier specialists are still influential because application-specific performance matters in many high-value niches. Phenomenex strengthened its oligonucleotide position with Clarity OTX Pro, while Biotage added both Oligo SPE and PrepXpert-8 to address pharmaceutical and PFAS-related workflows. Restek and MACHEREY-NAGEL are also competing through validated products for PFAS, pesticides, and throughput-heavy workflows rather than broad platform breadth. This keeps the solid phase extraction market competitive even though the top tier has meaningful scale in regulated accounts. The competitive balance, therefore, remains shaped by a mix of global workflow vendors and narrower specialists that win through application depth.

Solid Phase Extraction Industry Leaders

-

Agilent Technologies, Inc.

-

Thermo Fisher Scientific Inc.

-

Waters Corporation

-

Merck KGaA

-

Phenomenex, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: LabTech introduced AutoEmpore and SPE2000 as the latest innovations in its Solid Phase Extraction portfolio. These systems support faster, more consistent, and fully automated SPE workflows, enabling laboratories to improve productivity and maintain high-quality results.

- October 2025: Merck KGaA signed a definitive agreement to acquire the chromatography business of JSR Life Sciences, expanding its downstream bioprocessing portfolio with advanced Protein A chromatography capabilities for monoclonal antibody production. The transaction was expected to close by the end of Q2 2026.

- September 2025: Phenomenex launched Clarity OTX Pro, a next-generation SPE sample preparation kit engineered for oligonucleotide bioanalysis, delivering approximately 90% recovery from complex biological matrices without method re-optimization, targeting the fast-growing biotherapeutics pipeline.

Global Solid Phase Extraction Market Report Scope

As per the report’s scope, solid phase extraction (SPE) is a sample preparation technique used to isolate and concentrate target compounds from liquid mixtures by passing them through a solid sorbent. It enables selective retention of desired analytes while removing impurities, supporting the delivery of clean samples for downstream analytical testing, such as chromatography.

The solid phase peptide services market is segmented by type, application, organization size, and geography. By type, the market is categorized into SPE cartridges, SPE disks, and other type segments. By application, it is segmented into pharmaceutical industries, academic and research institutes, environmental testing, hospitals and clinics, food and beverage testing, forensic and toxicology testing, and other application segments. By organization size, the market is segmented into small and medium organizations and large organizations. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| SPE Cartridges |

| SPE Disks |

| Other Type Segments |

| Pharmaceutical Industries |

| Academic and Research Institutes |

| Environmental Testing |

| Hospitals and Clinics |

| Food and Beverage Testing |

| Forensic and Toxicology Testing |

| Other Application Segments |

| Small and Medium Organizations |

| Large Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | SPE Cartridges | |

| SPE Disks | ||

| Other Type Segments | ||

| By Application | Pharmaceutical Industries | |

| Academic and Research Institutes | ||

| Environmental Testing | ||

| Hospitals and Clinics | ||

| Food and Beverage Testing | ||

| Forensic and Toxicology Testing | ||

| Other Application Segments | ||

| By Organization Size | Small and Medium Organizations | |

| Large Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the solid phase extraction market by 2031?

The solid phase extraction market is forecast to reach USD 2.42 billion by 2031, rising from USD 1.94 billion in 2026 at a 4.54% CAGR over 2026-2031.

Which factor is driving the strongest demand in sample preparation for pharmaceuticals?

The strongest push comes from complex biologics and oligonucleotide therapies, which need cleaner extraction from difficult matrices than legacy preparation methods can provide.

Why is PFAS regulation important for solid phase extraction demand?

PFAS rules in the United States and Europe have made validated SPE consumables part of regulated testing workflows, especially for environmental laboratories handling water, soil, biosolids, and tissue samples.

Which product type leads revenue and which one grows the fastest?

SPE cartridges led with 45.90% share in 2025 because of their broad chemistry and validation base, while SPE disks are expected to grow the fastest at a 6.10% CAGR through 2031.

Which application area brings the most revenue today?

Pharmaceutical industries remain the largest application with 26.94% share in 2025 because regulated bioanalysis requires reliable, reproducible cleanup before downstream testing.

Which region is growing the fastest and why?

Asia-Pacific is growing the fastest at a 6.57% CAGR through 2031, supported by pharmaceutical manufacturing growth, tighter environmental rules, and rising research capacity in China, Japan, and India.

Which organization type is expected to adopt Solid Phase Extraction solutions most rapidly?

Small and medium scale organizations are expected to adopt Solid Phase Extraction solutions most rapidly due to their higher sample throughput, strict quality requirements, and need for reproducible analytical workflows.

Page last updated on: