Soldier Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

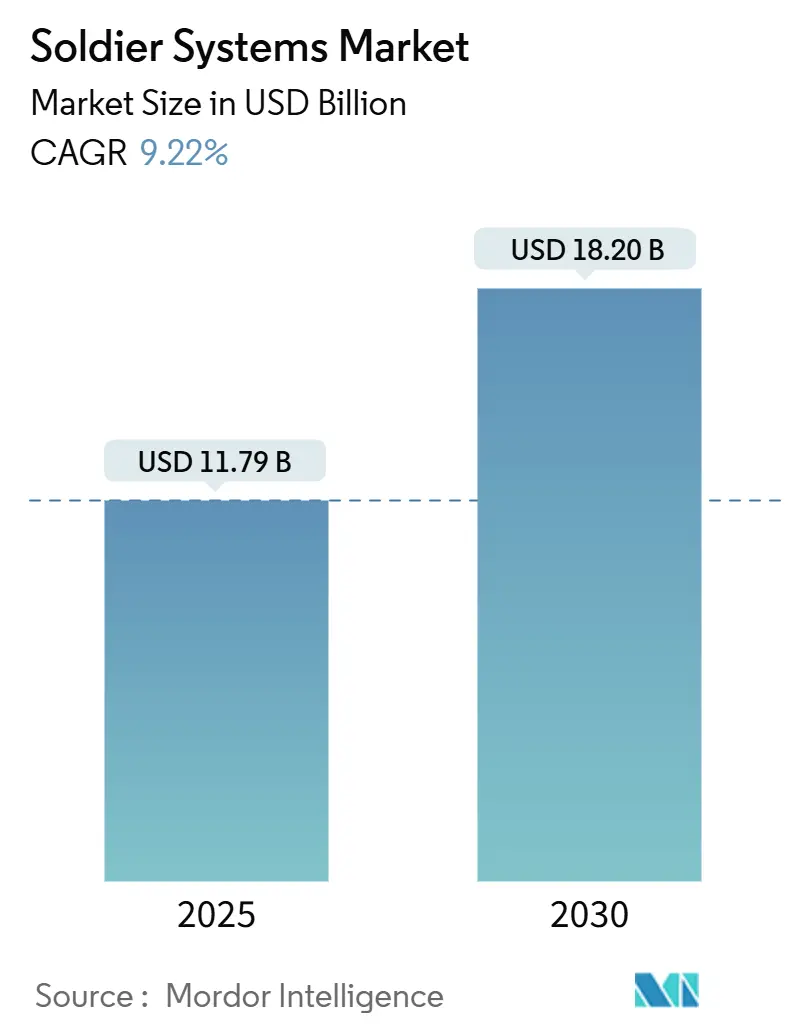

| Market Size (2025) | USD 11.79 Billion |

| Market Size (2030) | USD 18.20 Billion |

| Growth Rate (2025 - 2030) | 9.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soldier Systems Market Analysis by Mordor Intelligence

The soldier systems market size is estimated at USD 11.79 billion in 2025 and is projected to reach USD 18.20 billion by 2030, representing a 9.22% CAGR over the forecast period. The growing adoption of artificial-intelligence-enabled command-and-control suites, multi-year funding commitments such as the U.S. Army’s Integrated Visual Augmentation System (IVAS), and NATO-wide digitalization mandates are expanding addressable budgets across North America, Europe, and the Asia-Pacific region. Defense ministries are prioritizing power and energy upgrades to address battery burden constraints, open-architecture standards that facilitate the integration of third-party sensors, and edge-computing tools that reduce cognitive load for dismounted squads. Competitive momentum is shifting toward suppliers that combine wearable sensors, hybrid batteries, and software-defined radios into cohesive kits, while after-action reviews from Ukraine underscore the need for frequency-agile waveforms resistant to electronic warfare. Procurement offices are also raising demand for gender-specific body-armor geometries and lightweight exoskeletons that enhance endurance during long-haul marches.

Key Report Takeaways

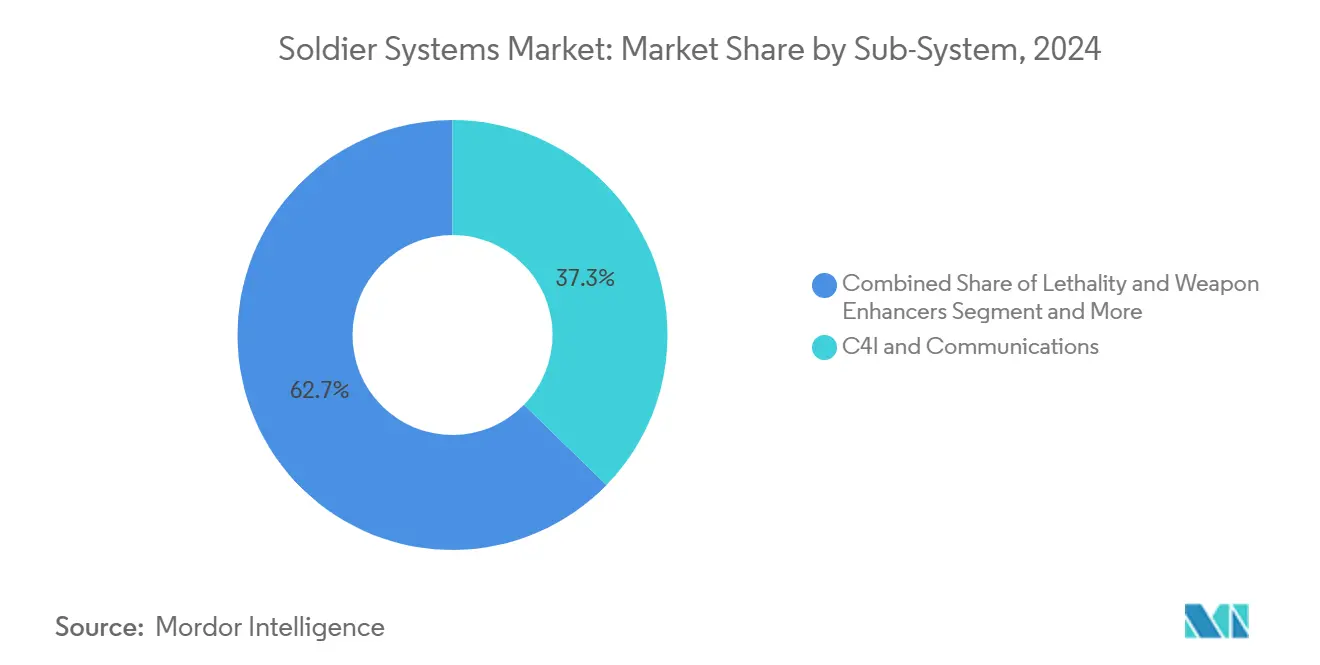

- By sub-system, C4I and communications captured 37.30% of 2024 revenue, whereas power and energy management is advancing at an 11.80% CAGR through 2030.

- By technology, wearable sensors and health monitoring led with 32.10% revenue share in 2024; exoskeletons and robotics are forecast to expand at an 18.00% CAGR to 2030.

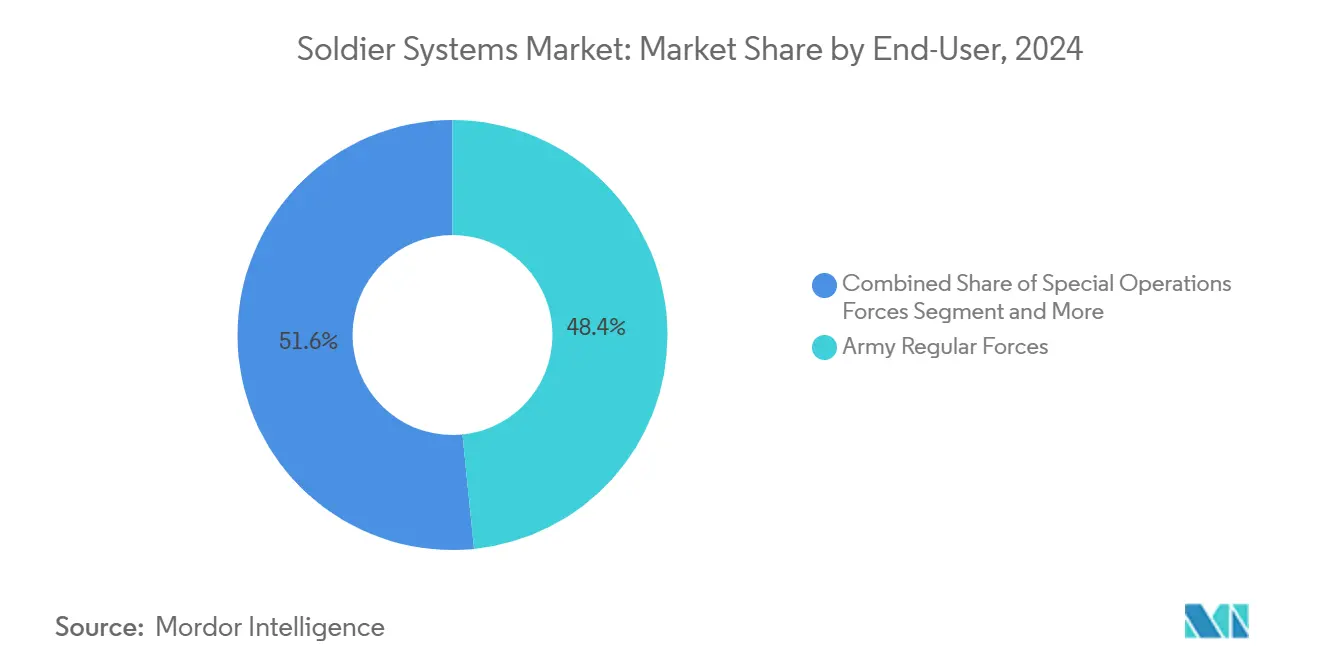

- By end-user, army regular forces held 48.40% share of the soldier systems market size in 2024, while special operations forces are growing at a 9.40% CAGR through 2030.

- By deployment platform, dismounted soldier kits accounted for a 64.50% share of the soldier systems market size in 2024 and vehicle-integrated solutions are progressing at a 10.20% CAGR to 2030.

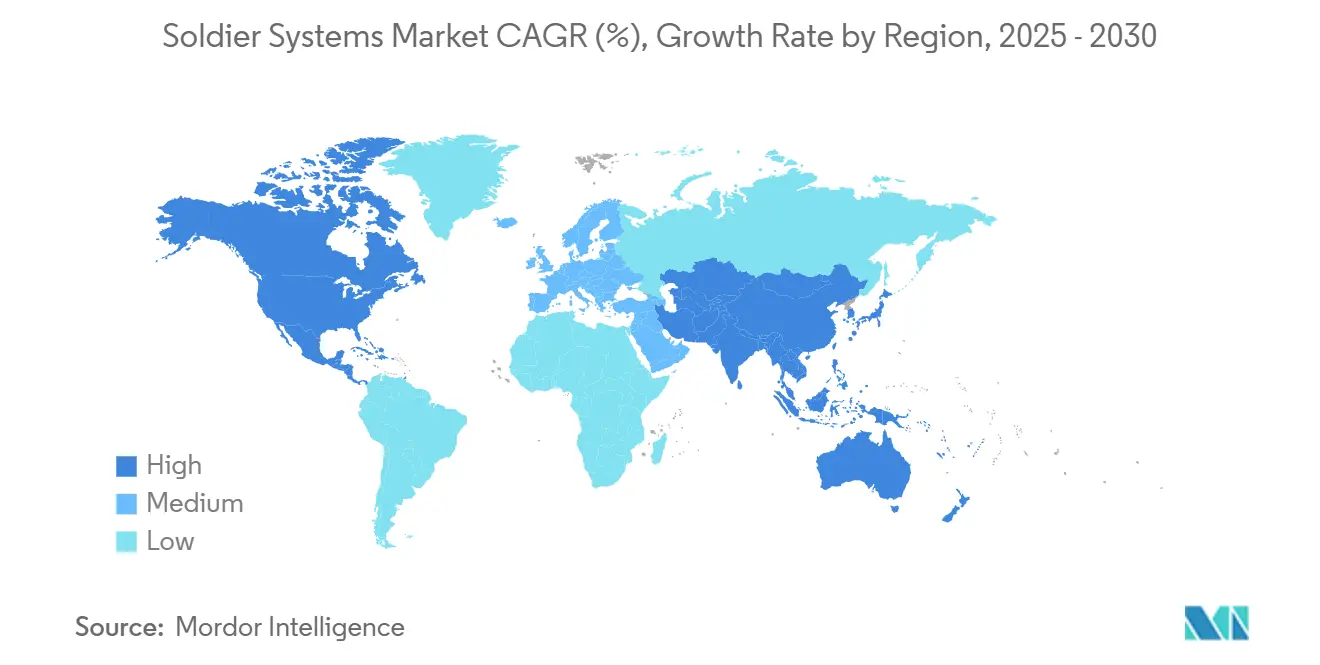

- By geography, North America commanded 46.40% of revenue in 2024; Asia-Pacific records the highest projected CAGR at 9.90% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soldier Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DoD multi-year funding surge for IVAS, ENVG-B and NGSW programs | +2.1% | North America and Five Eyes partners | Medium term (2-4 years) |

| NATO soldier digitalization mandates | +1.8% | Core Europe and Eastern-European aspirants | Long term (≥4 years) |

| Rapid adoption of lightweight power and energy solutions | +1.5% | Global, early traction in the U.S., Israel, South Korea | Short term (≤2 years) |

| AI-enabled tactical C4I and sensor fusion | +1.9% | North America, Europe, and pilot deployments in Asia-Pacific | Medium term (2-4 years) |

| Expansion of exoskeleton pilot buys | +0.7% | U.S., China, South Korea, and selective European trials | Long term (≥4 years) |

| Female-fit modular body-armor standards | +0.6% | North America and Europe, gradual adoption in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DoD Multi-Year Funding Surge for IVAS, ENVG-B and NGSW Programs

Multi-year procurement for IVAS, ENVG-B, and Next Generation Squad Weapon (NGSW) systems signals a structural budget shift favoring block buys over annual increments. Microsoft and Anduril’s IVAS 1.2 variant couples a lighter heads-up display with improved battery endurance, addressing earlier field-of-view and weight critiques raised by the 101st Airborne Division. L3Harris’s USD 256 million ENVG-B award fuses thermal and image-intensification channels, eliminating the need to toggle modes during close-quarters engagements[1]L3Harris Technologies, “ENVG-B Contract Award,” l3harris.com . XM7 and XM250 rifles introduced under NGSW drive parallel demand for networked fire-control optics that interface with squad radios, creating a systems-of-systems pull for integrators. Collectively, these programs prioritize lethality and situational awareness over unit-cost optimization and compel allied ministries to plan for interoperability.

NATO Soldier Digitalization Mandates

France’s FELIN Mk 2, Germany’s Gladius 2.0, Italy’s Soldato Futuro, and the United Kingdom’s Morpheus projects oblige infantry regiments to migrate from analog to software-defined radios by 2026. These mandates compress delivery schedules, force subcontractors to pre-position inventory, and require dual-source strategies that hedge against single-vendor lock-in. Open-architecture clauses built into the GBP 2.6 billion Morpheus contract let commanders integrate commercial sensors without proprietary gateways. Adoption is less about novel hardware and more about organizational change—new maintenance protocols, updated training curricula, and wider bandwidth allocation—all of which foster long-term spending visibility across Europe.

Rapid Adoption of Lightweight Soldier Power and Energy Solutions

Nett Warrior’s Android-based end-user devices drain conventional lithium-ion cells within eight hours, forcing squads to carry multiple spares. Hybrid power packs combining lithium-polymer cells with energy-harvesting fabrics add 30% daytime endurance, as demonstrated by Revision Military and Honeywell prototypes. Israel Defense Forces validated conformal batteries that mold to body-armor contours, achieving a 20% weight reduction over rigid formats. South Korea’s Warrior Platform explores thermoelectric generators that convert body heat into trickle charge, a passive approach that still meets mass constraints. With battery exhaustion documented in Ukraine operations, ministries are elevating power management from afterthought to primary acquisition metric.

AI-Enabled Tactical C4I and Sensor Fusion Reducing Cognitive Load

DARPA’s TRACE trials showed 40% fewer false-positive alerts after merging inputs from helmet cameras, range finders, and drones via machine-learning filters. Infantry in dense urban terrain face 12 alerts per hour, a volume that historically induced decision fatigue. Elbit’s BattleWise ranks threats by proximity and movement vector, displaying only the three most actionable items on the soldier’s visor. Thales’s TopOwl overlays blue-force tracking with predictive route analysis, eliminating paper map consultation. NATO’s 2024 AI strategy now mandates interoperable data formats to accelerate coalition data fusion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral supply risk for night-vision sensors & batteries | -1.2% | Global, acute in North America and Europe | Short term (≤2 years) |

| Single-source contracting dominance | -0.9% | North America and Europe, limited impact in Asia-Pacific | Medium term (2-4 years) |

| Size-weight-power trade-offs in wearable displays | -0.7% | Global, most acute for dismounted infantry | Long term (≥4 years) |

| Cyber-EW vulnerability of soldier radios | -0.8% | Eastern Europe and Indo-Pacific contested zones | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Supply Risk for Night-Vision Sensors and Batteries

China’s export controls on gallium, germanium, and antimony tightened in December 2024, jeopardizing supply of image-intensification tubes and infrared sensors. Spot gallium prices climbed 35% in the first nine months of 2024, prompting primes such as L3Harris and Elbit to pre-purchase 18 months of inventory. Lithium-ion cells rely on cobalt and lithium carbonate, both exposed to electric-vehicle demand swings that push up defense procurement costs. The U.S. Department of Defense Industrial Base Assessment listed 37 critical minerals with single-source bottlenecks and recommended stockpiling as a stop-gap. Because new mines take up to a decade to reach production, pricing volatility is expected to linger into the late 2020s.

Single-Source Contracting Dominance

The IVAS program relies on a single prime despite Microsoft’s collaboration with Anduril, concentrating technical risk and limiting army leverage on schedule and pricing. The United Kingdom’s Morpheus award similarly went exclusively to BAE Systems, leaving no fallback if milestones slip. Soldier-system integration requires classified network knowledge and cryptographic keys, erecting barriers to entry for smaller innovators. NATO’s open-architecture push aims to curb these monopoly dynamics but enforcement remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-System: Power Management Accelerates As C4I Matures

C4I and communications delivered 37.30% of 2024 revenue, reflecting large-scale fielding of software-defined radios and Android-based end-user devices. Growth is plateauing as first-generation systems near saturation, opening budget headroom for power and energy management, which posts the highest 11.80% CAGR through 2030. The soldier systems market size attributed to power solutions is expected to climb steadily as defense ministries fund conformal batteries, solar fabrics, and hybrid capacitors that lengthen mission endurance. After-action reports from Ukraine confirmed that units reverting to paper maps had lost battery power, elevating power management from secondary procurement item to primary mission enabler. Integrated programs such as Germany’s Gladius 2.0 stipulate a single data and power bus for all subsystems, cutting cable bulk and simplifying maintenance. Weapon enhancers tied to the NGSW family are adding networked fire-control optics, while protection gear benefits from female-fit armor mandates. Training and simulation aids, though smallest by value, leverage mixed-reality overlays to reduce ammunition expenditure and improve repetition of high-risk scenarios. The combined effect is a pivot from siloed upgrades toward holistic soldier kits in which energy, data, and protection parameters are optimized as a closed loop.

Second-order interactions reinforce this momentum. Better batteries allow longer runtime for AI edge processors, which in turn cut radio chatter by fusing sensor inputs locally, reducing spectrum congestion for brigade networks. Open-architecture standards embedded in NATO programs lower the cost of integrating third-party power hubs or protection plates, encouraging a more competitive supplier base. Meanwhile, stockpiling of critical minerals functions as a hedge against gallium or cobalt shortages, but adds working-capital requirements that smaller vendors struggle to finance. Consequently, prime contractors capable of forward-buying raw materials are gaining negotiating leverage, particularly when paired with proven integration credentials across multiple subsystems within the soldier systems market.

By Technology: Exoskeletons Transition from Prototype to Field Use

Wearable sensors and health monitoring owned 32.10% of technology-segment revenue in 2024, driven by mandates for physiological tracking that pre-empt heat stress and dehydration. Exoskeletons and robotics are projected to grow at an 18.00% CAGR as early pilot results translate into operational demand. Lockheed Martin’s ONYX lower-body exoskeleton, now cleared for 500-unit procurement, demonstrated quantifiable fatigue reduction and injury-prevention benefits, which resonate with logistics units that haul ammunition and equipment. Sarcos’s Guardian XO targets heavy-lift tasks but faces cost-per-unit and battery runtime barriers. Passive exoskeletons under evaluation by the People’s Liberation Army trade powered assistance for simpler mechanics, signaling a tiered market where cost, endurance, and mass dictate adoption tiers.

Augmented displays mature in parallel. Microsoft’s IVAS 1.2 integrates eye-tracking that shaves two seconds off target designation, translating into tangible survivability gains during close-quarters engagements. Advanced battery packs featuring 250 Wh/kg lithium-polymer cells underpin these sensors without adding mass, closing the design loop between power and performance. AI algorithms embedded at the edge prioritize alerts, trimming the human attention budget required to process incoming data. The soldier systems market therefore increasingly rewards suppliers capable of marrying sensor fidelity, power density, and ergonomic design, a convergence likely to accelerate as component miniaturization continues.

By End-User: Special Operations Absorb Premium Costs for Overmatch

Army regular forces represented 48.40% of 2024 spending, reflecting volume buys that stress affordability and logistic simplicity. Special operations forces, growing at a 9.40% CAGR, willingly pay 30–50% premiums for lighter kits that embed AI fusion, low-light sensors, and hybrid power sources. USSOCOM’s FY2025 priority list highlights modular architectures enabling mission-specific load-outs, a requirement incompatible with one-size-fits-all infantry gear.

Marine and naval infantry demand corrosion-resistant electronics and waterproof batteries suitable for littoral environments, adding 10–15% to bill of materials. Federal law-enforcement units in France and Italy buy soldier-system derivatives primarily for counter-terrorism missions, prioritizing interoperability with body cameras and non-lethal capabilities over battlefield durability. Tiered procurement approaches thus segment the soldier systems market between cost-sensitive volume programs and premium niches where performance outranks price.

By Deployment Platform: Vehicle Integration Gains Momentum

Dismounted soldier kits owned 64.50% of deployment revenue in 2024, but vehicle-integrated solutions are expanding at a 10.20% CAGR as armies retrofit armored personnel carriers with sensor fusion that links crew perspectives to dismounted squads. Germany’s Puma IFV equips the commander with a helmet-mounted display that pipes long-range optics directly to infantry outside the vehicle, extending threat detection beyond line of sight.

Forward operating base protection suites, though a small slice of the soldier systems market, integrate ground sensors, aerostats, and counter-drone effectors into a unified interface that trims manpower needs. Urbanization intensifies demand for seamless hand-off between mounted and dismounted elements, compelling radio makers to deliver common waveforms that maintain data integrity across platforms.

Geography Analysis

North America generated 46.40% of 2024 revenue, propelled by USD 256 million for ENVG-B and the multi-year IVAS commitment totaling USD 21.9 billion. Canada’s Integrated Soldier System Project contracted Rheinmetall and Elbit to modernize 10,000 infantry kits with modular armor and software-defined radios, cementing interoperability with U.S. formations. Mexico’s National Guard procures locally produced ballistic vests under content-mandate rules, cultivating a cost-focused sub-segment. The United States drives technology maturation via edge-AI prototypes and hybrid power trials, accelerating supplier learning curves that benefit allied users.

Asia-Pacific is projected to record a 9.90% CAGR through 2030. India’s F-INSAS aims to equip 465,000 soldiers with helmet-mounted displays, modular armor, and SDRs by 2027, leveraging domestic production offsets to nurture local supply chains[2]Indian Ministry of Defence, “F-INSAS Program Brief 2024,” mod.gov.in. South Korea’s Warrior Platform folds exoskeleton testbeds and thermoelectric generators into a doctrine tailored to counter North Korea’s numerical advantage[3]South Korean Ministry of National Defense, “Warrior Platform Update,” mnd.go.kr . Japan, constrained by constitutional limits on offensive posture, emphasizes protection gear and counter-UAV sensors. China’s opaque yet sizeable procurement of domestic exoskeletons and AI-enabled targeting systems pressures global suppliers to speed innovation. Australia and Singapore allocate funds for power-management upgrades to extend operational reach across vast maritime domains, further lifting regional demand for modular, energy-efficient soldier systems.

Europe’s large-scale digitalization programs unlock replacement cycles as analog kits reach end-of-life. France’s FELIN Mk 2 and Germany’s Gladius 2.0 drive volume for Thales, Rheinmetall, and Leonardo, while the UK’s open-architecture Morpheus program positions BAE Systems to capture downstream sensor integration work. Open data standards encourage small and mid-sized European firms to supply niche subsystems—such as battery hubs or lightweight headsets—without facing proprietary interface barriers. The Middle East emphasizes localized production under sovereign-capability doctrines: Elbit inked co-production deals for helmet displays and radios in the UAE, and Saudi Arabia funds domestic armor manufacturing under Vision 2030. Africa and South America remain emerging markets; South Africa’s Paramount Group and Brazil’s Taurus Armas sell basic infantry gear, but limited budgets stall widescale adoption of AI-enabled or power-intensive technologies.

Competitive Landscape

The soldier systems market is highly concentrated: the top five primes—BAE Systems, Elbit Systems, L3Harris, Thales, and Leonardo—captured 65% of 2024 contract value in the United States and United Kingdom[4]BAE Systems plc, “Morpheus Capability Delivery,” baesystems.com. Vertically integrated leaders bundle radios, sensors, batteries, and armor into turnkey kits, leveraging scale and security clearances to win multi-year awards. Specialized firms such as Revision Military (eyewear) and Savox Communications (headsets) dominate high-margin niches yet lack the breadth to prime entire programs. White-space opportunities persist in power management, where no incumbent exceeds 20% share, and in exoskeletons, where Lockheed Martin and Sarcos compete to set price-performance norms.

Technology differentiation shapes competition. Microsoft’s Azure cloud backbone in IVAS enables over-the-air software updates, shortening patch cycles and keeping deployed devices current. Honeywell leads patent filings for hybrid battery architectures pairing lithium-polymer cells with supercapacitors for burst-power loads. Rockwell Collins, now under Thales, markets modular waveform upgrades that extend legacy radios’ service lives without hardware swaps, undercutting full-replacement rivals. Geopolitics further fragment the arena: export controls on night-vision and encryption restrict Western primes from selling top-tier gear to non-aligned states, allowing South Korea’s Hanwha and Turkey’s Aselsan to fill capability gaps with mid-tier offerings.

Strategic moves in 2024–2025 include Northrop Grumman’s minority investment in a solid-state battery startup, signaling vertical integration into power subsystems. General Dynamics won an USD 85 million award to link dismounted radios to vehicle sensors in Stryker brigades, demonstrating the value of cross-platform data fusion. Leonardo partnered with Italy’s Ministry of Defense on wearable physiological sensors, betting that health-monitoring capabilities will become procurement baselines. As competitive intensity rises, primes race to lock in intellectual property for AI fusion engines, hybrid batteries, and ergonomic armor, all while complying with open-standard directives that theoretically level the playing field.

Soldier Systems Industry Leaders

L3Harris Technologies Inc.

Thales Group

Elbit Systems Ltd.

BAE Systems plc

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Elbit Systems secured a USD 150 million contract from an Asia-Pacific nation to supply helmet-mounted displays and tactical radios.

- December 2024: BAE Systems completed the first delivery phase of the UK’s Morpheus program, equipping 5,000 soldiers with modular body armor and SDRs.

- November 2024: Lockheed Martin confirmed U.S. Army procurement of 500 ONYX exoskeletons for logistics units.

- October 2024: Rheinmetall Canada and Elbit Systems of America won CAD 200 million to modernize 10,000 Canadian infantry kits.

Global Soldier Systems Market Report Scope

Soldier Systems Market is segmented by Sub-System (C4I and Communications, Lethality and Weapon Enhancers, Protection and Survivability Gear, and More), Technology (Wearable Sensors and Health Monitoring, and More), End-User (Army Regular Forces, Special Operations Forces, and More), Deployment Platform (Dismounted Soldier, and More), and Geography (North America, Europe, Asia-Pacific, and more).

| C4I and Communications |

| Lethality and Weapon Enhancers |

| Protection and Survivability Gear |

| Power and Energy Management |

| Training and Simulation Aids |

| Wearable Sensors and Health Monitoring |

| Augmented / Head-Up Displays |

| Exoskeletons and Robotics |

| Advanced Battery and Hybrid Power Packs |

| Army Regular Forces |

| Special Operations Forces |

| Marine / Naval Infantry |

| Federal Law-Enforcement and Gendarmerie |

| Dismounted Soldier |

| Vehicle-Integrated Kits |

| Forward Operating Base (FOB) Protection Suites |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Sub-System | C4I and Communications | |

| Lethality and Weapon Enhancers | ||

| Protection and Survivability Gear | ||

| Power and Energy Management | ||

| Training and Simulation Aids | ||

| By Technology | Wearable Sensors and Health Monitoring | |

| Augmented / Head-Up Displays | ||

| Exoskeletons and Robotics | ||

| Advanced Battery and Hybrid Power Packs | ||

| By End-User | Army Regular Forces | |

| Special Operations Forces | ||

| Marine / Naval Infantry | ||

| Federal Law-Enforcement and Gendarmerie | ||

| By Deployment Platform | Dismounted Soldier | |

| Vehicle-Integrated Kits | ||

| Forward Operating Base (FOB) Protection Suites | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the soldier systems market?

The soldier systems market size is USD 11.79 billion in 2025.

How fast is global demand for soldier systems expected to grow?

Aggregate demand is forecast to expand at a 9.22% CAGR from 2025 to 2030.

Which sub-system shows the fastest growth trends?

Power and energy management leads, registering an 11.80% CAGR through 2030.

Why are exoskeletons gaining traction among defense buyers?

Field trials demonstrate reduced soldier fatigue and injury risk, lifting exoskeleton demand at an 18.00% CAGR.

Which region records the highest projected growth?

Asia-Pacific is expected to post a 9.90% CAGR as India, South Korea, and China scale soldier-modernization programs.

Page last updated on: