Software As A Medical Device (SaMD) For Oncology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

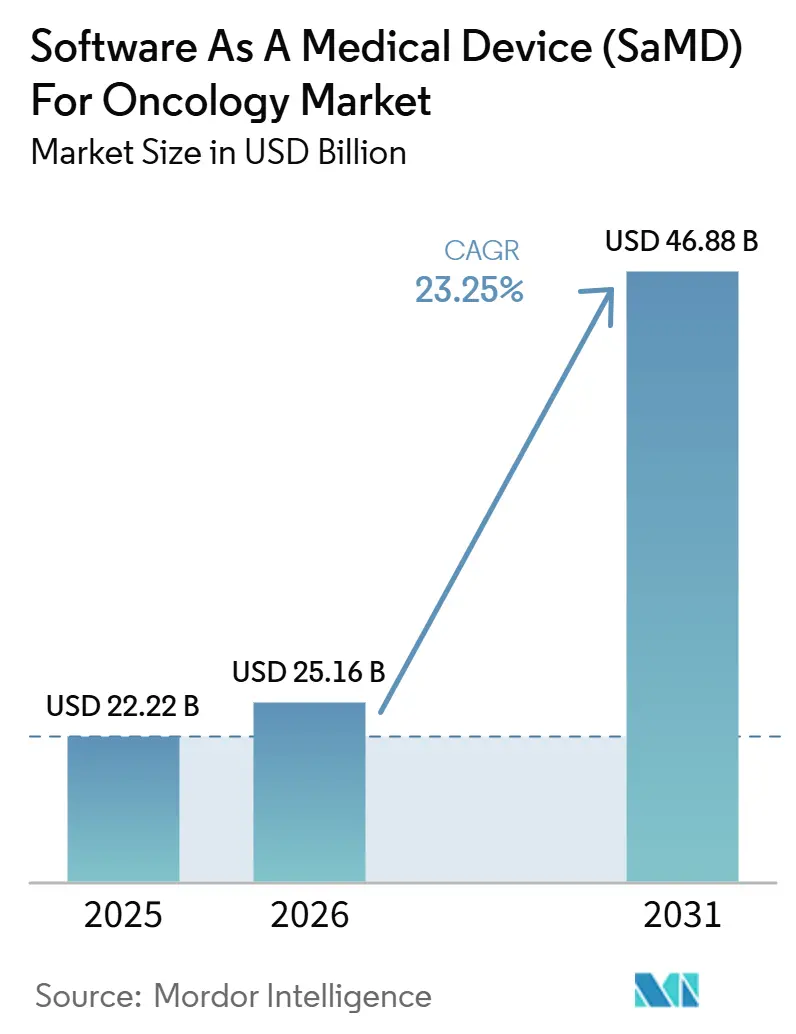

| Market Size (2026) | USD 25.16 Billion |

| Market Size (2031) | USD 46.88 Billion |

| Growth Rate (2026 - 2031) | 23.25% CAGR |

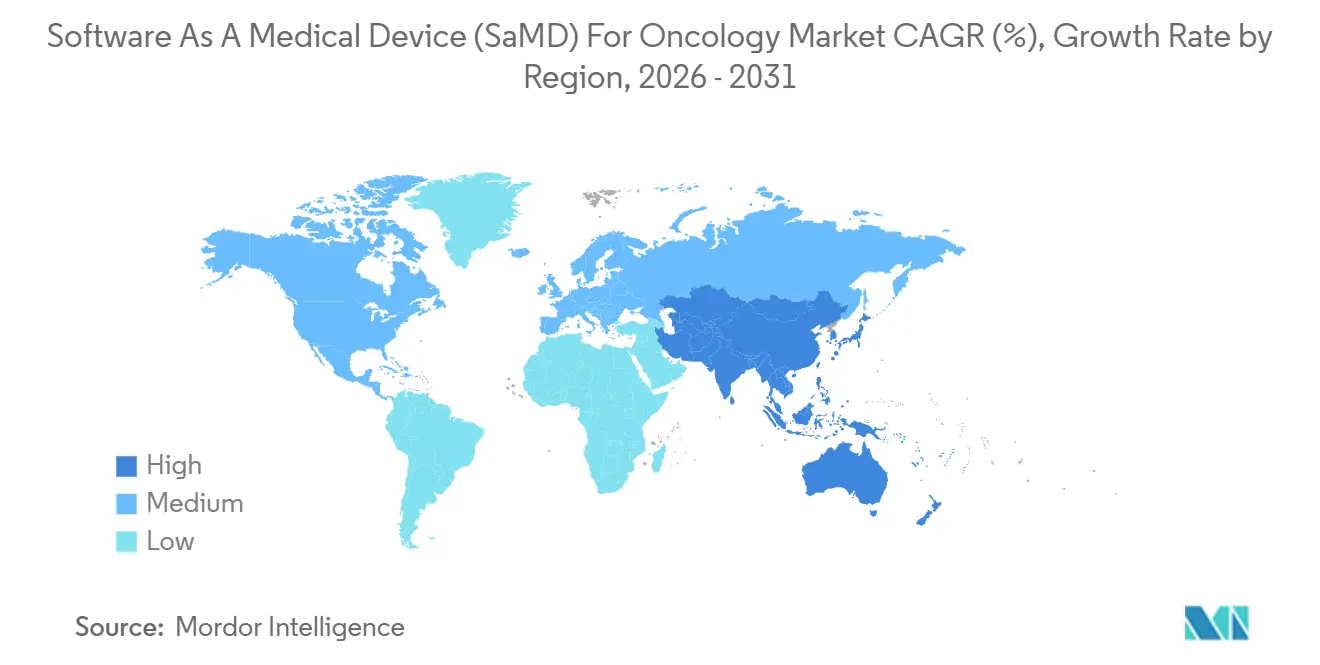

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software As A Medical Device (SaMD) For Oncology Market Analysis by Mordor Intelligence

The Software As A Medical Device For Oncology Market size is projected to expand from USD 22.22 billion in 2025 and USD 25.16 billion in 2026 to USD 46.88 billion by 2031, registering a CAGR of 23.25% between 2026 to 2031.

The growth trajectory reflects the rising cancer burden, with the IARC estimating 20.6 million new cancer cases and 9.8 million cancer deaths worldwide in 2024, while a 2026 Lancet Oncology modeling study projected diagnosed incidence to increase from 13.58 million in 2025 to 19.32 million by 2050. As patient volumes increase, manual-only workflows are becoming less practical for diagnosis, triage, reporting, and follow-up, prompting health systems to adopt clinically validated software tools. The Software as a Medical Device (SaMD) for oncology market is gaining momentum as radiology, pathology, genomic, and clinical record data are integrated into unified, AI-enabled platforms that support care decisions. North America remains the largest regional base, while Asia-Pacific is the fastest-growing region, with competition strengthening through acquisitions, product expansion, and workflow integration despite uneven reimbursement pathways across countries and care settings.

Key Report Takeaways

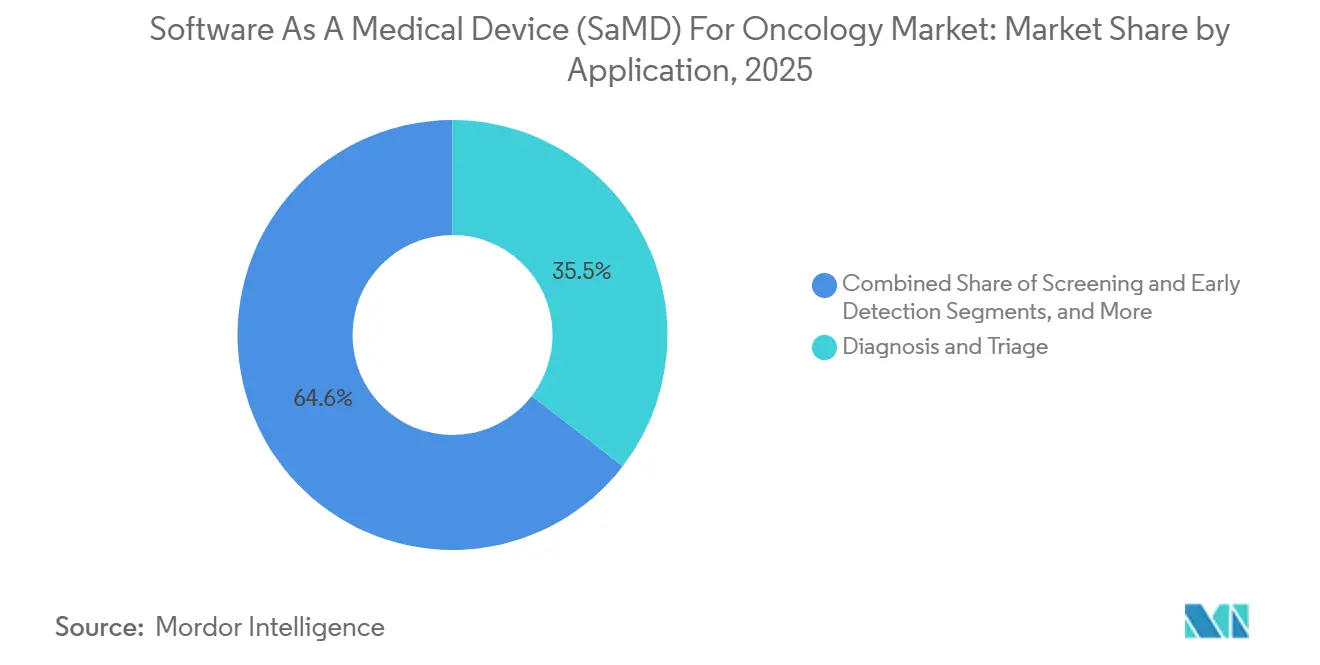

- By application, diagnosis and triage held 35.45% revenue share in 2025, while screening and early detection is forecast to expand at a 16.93% CAGR through 2031.

- By technology, machine learning and deep learning held 41.23% share in 2025, while computer vision and imaging AI is projected to record the highest CAGR of 19.67% through 2031.

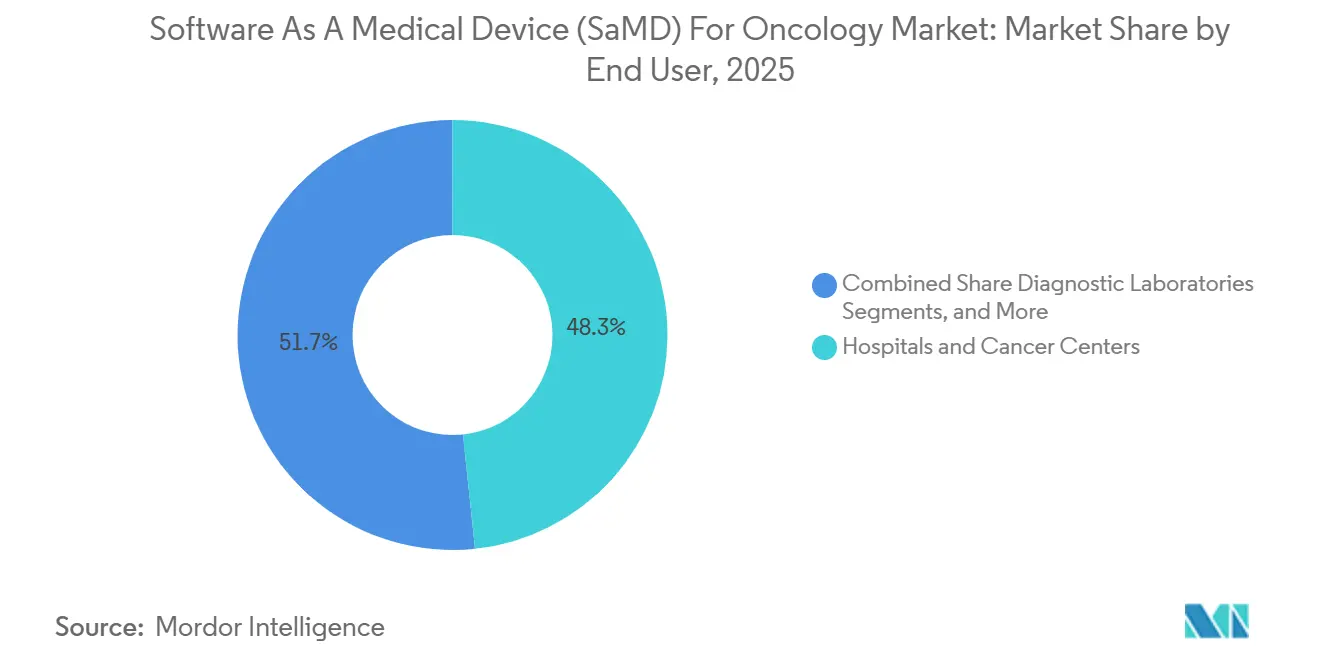

- By end user, hospitals and cancer centers accounted for 48.34% of revenue in 2025, while diagnostic laboratories are projected to grow at a 15.35% CAGR through 2031.

- By deployment mode, cloud-based deployment represented 62.88% of revenue in 2025, while on-premise deployment is projected to expand at a 17.78% CAGR through 2031.

- By geography, North America held 41.52% share in 2025, while Asia-Pacific is projected to grow at a 17.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Software As A Medical Device (SaMD) For Oncology Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing use of AI-based cancer triage and decision support | +2.8% | Global, with stronger near-term pull in North America and Europe | Short term (≤ 2 years) |

| Regulatory preference for SaMD with traceable clinical evidence | +1.5% | North America, Europe, Australia, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Expansion of multimodal oncology data platforms | +2.0% | Global, led by the United States, United Kingdom, and China | Medium term (2-4 years) |

| Hospital demand for workflow automation in imaging, pathology, and genomics | +1.8% | North America, Europe, and core Asia-Pacific markets | Short term (≤ 2 years) |

| Rising need for earlier cancer detection and risk stratification | +2.5% | Global, with high urgency in North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing use of software to support precision oncology and therapy selection | +1.6% | North America and Europe first, followed by Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Use of AI-Based Cancer Triage and Decision Support

The Software as a Medical Device (SaMD) for oncology market is generating near-term demand from clinical decision support tools embedded directly within radiology and pathology workflows. A 2025 JAMA Network Open analysis of 222 FDA-cleared AI medical device software products showed that the 510(k) pathway had become the primary route to commercialization, helping accelerate deployment while maintaining high performance expectations.[1]The Lancet Oncology, “Estimating Total and Diagnosed Global Cancer Incidence and Stage Distribution From 1990 to 2050,” The Lancet Oncology, thelancet.com Aidoc’s CARE foundation model and its broader clinical AI initiatives showed that buyers were shifting from single-use tools to platforms capable of managing multiple triage tasks through one system. This trend is significant because hospitals rarely operate a single imaging stack, making integration easier for platform vendors than for narrow algorithm suppliers and supporting larger enterprise deals over isolated department-level purchases.

Rising Need for Earlier Cancer Detection and Risk Stratification

The Software as a Medical Device (SaMD) for oncology market is gaining momentum from the shift from single-cancer screening to broader multi-cancer detection programs. GRAIL submitted the Premarket Approval application for its Galleri multi-cancer early detection test to the FDA in January 2026 under its existing Breakthrough Device Designation. At the 2026 ASCO Annual Meeting, PATHFINDER 2 results showed that Galleri increased cancer detection by more than sevenfold when added to U.S. Preventive Services Task Force-recommended screenings, while the NHS-Galleri trial reported a 25% reduction in Stage IV cancer diagnoses in the third screening year across 12 pre-specified cancer types. As these programs expand, providers need software for test result delivery, call handling, routing, tracking, and follow-up coordination, making early detection a durable demand driver even when assays and software are sold through different channels.

Expansion of Multimodal Oncology Data Platforms

The Software as a Medical Device (SaMD) for oncology market is shifting from single-data models to platforms that combine imaging, pathology, genomics, and longitudinal clinical records. Tempus relaunched its Lens platform in May 2026 and integrated it more closely with the Paige foundation model base, expanding its role in patient stratification and oncology drug development. SOPHiA GENETICS introduced Digital Twins in 2025 to simulate patient outcomes for treatment decisions, showing how software was moving deeper into decision support rather than serving only as a data display tool. A 2025 study in npj Digital Medicine also supported the value of continuous multimodal data pipelines that connect imaging, genomic, and EMR inputs to accelerate AI development cycles.

Hospital Demand for Workflow Automation in Imaging, Pathology, and Genomics

The Software as a Medical Device (SaMD) for oncology market is benefiting from hospital demand for faster and more reliable workflow execution in imaging, pathology, and genomics. GE HealthCare received FDA 510(k) clearance in June 2026 for MIM Contour ProtégéAI+ 2.0, including a Predetermined Change Control Plan that allows future model expansion without requiring a new submission for each update. This clearance is important because treatment planning remains one of the most time-intensive steps in cancer care, and software that reduces contouring or review time can help increase capacity without a proportional rise in staffing. The same demand is visible in pathology and imaging, where hospitals aim to reduce system handoffs and minimize manual review steps, keeping the market closely tied to workflow savings, turnaround time, and clinical throughput.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented reimbursement for oncology software claims | -1.2% | Global, with sharper friction in the United States and Europe | Medium term (2-4 years) |

| High clinical validation burden across tumor types and geographies | -1.0% | Global, with added complexity under EU MDR and China review pathways | Long term (≥ 4 years) |

| Data access constraints across imaging, pathology, and genomics | -0.8% | Europe, Asia-Pacific, and emerging markets with localization rules | Medium term (2-4 years) |

| Compliance complexity due to evolving ai and medical device regulations | -0.6% | Europe, North America, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Reimbursement for Oncology Software Claims

The Software as a Medical Device (SaMD) for oncology market still faces a major commercial hurdle because reimbursement rules have not kept pace with product approvals and clinical use. Oncology software vendors often must manage country-level or payer-level negotiations even after market entry. In the United States, uneven coding and payment treatment for AI-assisted digital pathology and multi-cancer early detection workflows limits adoption beyond large health systems. GRAIL’s Galleri process has highlighted the gap between growing clinical evidence and the payment certainty required for large-scale screening adoption.

High Clinical Validation Burden Across Tumor Types and Geographies

The Software as a Medical Device (SaMD) for oncology market also faces a high evidence burden because tumor biology, imaging quality, and patient demographics vary widely across care settings. The FDA’s 2025 draft guidance on AI-enabled device software functions called for stronger data lineage documentation, subgroup bias analysis, and total product lifecycle planning, increasing the workload before and after submission. A 2024 JMIR regulatory analysis highlighted that China places AI medical devices in a stricter risk category than the mostly Class II path used by the FDA, making dual-market clearance harder for many vendors. Smaller developers are likely to face the most pressure as they fund broader validation while maintaining post-market compliance.[2]Hyuna Sung et al., “Global Cancer Statistics 2024, GLOBOCAN Estimates of Incidence and Mortality Worldwide for 34 Cancers in 186 Countries,” PMC, ncbi.nlm.nih.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Diagnosis-Led Volume, Screening-Led Growth

Diagnosis and Triage held 35.45% of the Software as a Medical Device (SaMD) for oncology market share in 2025, making it the largest application area in revenue terms. The segment addressed an immediate clinical need, as radiology and pathology backlogs directly affected patient flow and treatment timelines. Paige PanCancer Detect received FDA Breakthrough Device Designation in April 2025, underscoring the value of tools that flag suspicious findings across tissue types and anatomic sites. Diagnosis and triage tools also fit existing reading workflows, which supported faster adoption than software requiring a separate review pathway.

The Software as a Medical Device (SaMD) for oncology market size for Screening and Early Detection is projected to expand at a 16.93% CAGR through 2031, making it the fastest-growing application segment. Growth is linked to multi-cancer early detection programs, AI-assisted mammography, and low-dose CT screening workflows moving toward wider deployment. Tempus launched Paige Predict in January 2026, and the platform analyzed standard H&E slides to predict 123 biomarkers across 16 cancer types using tissue that would otherwise require separate molecular assays. This launch showed how diagnosis, pathology support, and therapy selection were becoming increasingly connected through the same software base.

By Technology: Foundation Models Disrupt the Incumbent Algorithm Market

Machine Learning and Deep Learning represented 41.23% of revenue in 2025 and remained the core technology base for the Software as a Medical Device (SaMD) for oncology market. The segment remained anchored by deep learning methods in imaging review and newer transformer-based approaches in biomarker and genomic interpretation. Buyers drew a clearer distinction between narrow algorithms and foundation-model-style platforms, as larger models supported several downstream tasks from the same training base. Philips expanded its partnership with Ibex Medical Analytics in 2025 to strengthen AI-enabled pathology workflows and capture more software value on installed systems.

Computer Vision and Imaging AI is projected to grow at a 19.67% CAGR through 2031, making it the fastest-rising technology area. This growth reflects the shift in digital pathology and radiology from hardware-led purchases toward recurring software subscriptions and inference services. Natural Language Processing became more useful in trial matching and structured reporting, as unstructured oncology notes continued to contain important clinical details. Predictive Analytics and Risk Scoring remained smaller, but products such as SOPHiA GENETICS Digital Twins showed how software was beginning to model likely treatment response using combined genomic and clinical inputs.

By End User: Hospital Dominance with Lab-Sector Disruption

Hospitals and Cancer Centers accounted for 48.34% of revenue in 2025, making them the largest end-user base in the Software as a Medical Device (SaMD) for oncology market. Their lead came from higher case volumes, stronger enterprise software budgets, and the need to connect AI tools with PACS, LIS, and electronic health records. Hospitals also gained more value when software reduced re-entry work and shortened diagnostic or treatment planning steps across departments. This made integrated deployment more valuable than stand-alone tools that added another screen or workflow stage.

Diagnostic Laboratories are projected to grow at a 15.35% CAGR through 2031, making them the fastest-expanding end-user segment. High-throughput labs derived clear value from automated slide analysis and liquid biopsy informatics, as turnaround time and case volume directly affected margins and service differentiation. Ibex Medical Analytics deployed its prostate cancer AI at HNL Lab Medicine in March 2026 under a laboratory developed test framework, showing how labs commercialized AI-enhanced testing without waiting for a separate standalone product route. Pharmaceutical and biotechnology companies also increased procurement for companion diagnostics, trial matching, and real-world evidence generation, while academic and research institutes continued to support validation studies.

By Deployment Mode: Cloud Dominance, On-Premise Resilience

Cloud-Based deployment represented 62.88% of revenue in 2025 and remained the leading delivery model in the Software as a Medical Device (SaMD) for oncology market. Cloud systems were easier to maintain, supported elastic compute for AI workloads, and allowed vendors to update models without major site-level intervention. SOPHiA GENETICS stated that its cloud-native SOPHiA DDM Platform connected more than 800 institutions across over 70 countries, showing the scale advantage of cloud architecture. For many buyers, interoperability and remote update capability reduced the practical burden of scaling across multiple sites.

On-Premise deployment is projected to expand at a 17.78% CAGR through 2031, showing that cloud adoption is not uniform across all user profiles. Some hospitals and networks continued to prefer local deployment because of data residency rules, cybersecurity controls, or latency requirements in high-volume imaging and pathology workflows. This preference created more room for hybrid models, where inference stayed local while updates, logging, and selected management functions remained cloud-connected. In the Software as a Medical Device (SaMD) for oncology market, deployment strategy became a commercial differentiator rather than a basic technical choice.

Geography Analysis

North America held 41.52% of the Software as a Medical Device (SaMD) for oncology market share in 2025, making it the clear regional leader. The region benefited from a mature FDA pathway, strong venture and strategic capital support, and health systems familiar with software subscriptions in clinical settings. The Federal Register final order issued in June 2026 for radiological machine learning-based quantitative imaging software provided a clearer regulatory base for a key market segment. Lunit reported more than 330 screening sites and approximately 1 million annual mammography screenings across the Americas in April 2026, showing that cleared oncology AI tools were moving into population-scale use.

Europe remained the second-largest region in the Software as a Medical Device (SaMD) for oncology market, supported by established oncology care networks in Germany, the United Kingdom, and France. The region combined strong demand for clinically validated tools with a stricter compliance culture, raising barriers to entry while favoring well-prepared vendors. The NHS-Galleri trial results presented in 2026 strengthened the United Kingdom’s role as an important test bed for software-enabled multi-cancer screening pathways. Europe remained important due to its revenue base and the influence of its regulatory and public health decisions on deployment standards in other regions.

Asia-Pacific is projected to grow at a 17.56% CAGR through 2031, making it the fastest-growing regional segment in the Software as a Medical Device (SaMD) for oncology market. The region is expanding from a lower installed base, supported by rising cancer care demand, growing digital health investment, and active local developer ecosystems. Hospitals and laboratories are adopting these tools to manage higher diagnostic volumes amid limited specialist capacity. Outside the major markets, the Middle East and Africa remain at an earlier stage, but modernization programs and hospital-level deployments are beginning to create measurable demand.

Competitive Landscape

The Software as a Medical Device (SaMD) for oncology market has a two-layer competitive structure, with a smaller group of broad platform companies and a larger base of specialized AI developers. Tempus AI, Roche after the PathAI deal, GE HealthCare, and Siemens Healthineers compete on integrated workflow reach, while Lunit, Ibex Medical Analytics, SOPHiA GENETICS, GRAIL, and Aidoc maintain strong positions in selected clinical or data domains. Roche agreed in May 2026 to acquire PathAI for USD 750 million upfront, plus up to USD 300 million in milestone payments, reinforcing the role of AI-enabled pathology as core diagnostics infrastructure. The market is moving toward fewer, larger platform groups, although specialist innovation remains active.

Tempus AI’s platform strategy became more visible through the Paige acquisition, the launch of Paige Predict in January 2026, and the next-generation Lens platform introduced in May 2026. Tempus also reported a USD 97.3 million year-over-year improvement in EBITDA for fiscal year 2025, indicating that multimodal oncology software economics can improve as the database and product mix expand. Viz.ai added NCCN Clinical Practice Guidelines to its Viz Oncology platform and launched a collaboration with Novartis in 2025 for cancer patient identification. This dual revenue model is becoming more attractive in the Software as a Medical Device (SaMD) for oncology market as it reduces dependence on a single buyer group.

The competitive field still offers opportunities in trial matching, care coordination, and software that connects pathology, imaging, and genomics within a single clinical workflow. Intellectual property is becoming more important as vendors strengthen positions in foundation models, preprocessing methods, and multimodal data handling. Buyers increasingly prefer platforms that demonstrate clinical value, support updates through regulated change plans, and integrate with existing hospital software. Specialist vendors still have room to grow, but scaling internationally may require partnerships, channel support, or acquisition pathways.

Software As A Medical Device (SaMD) For Oncology Industry Leaders

GE HealthCare Technologies Inc.

Siemens Healthineers AG

Koninklijke Philips N.V.

Median Technologies

Aidoc Medical Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Aidoc raised USD 150 million in Series E funding led by Goldman Sachs Alternatives, with participation from SoftBank Vision Fund 2 and NVIDIA’s NVentures, increasing its total funding to over USD 500 million.

- June 2026: GE HealthCare secured FDA 510(k) clearance for MIM Contour ProtégéAI+ 2.0, an AI-enabled auto-contouring software for radiation oncology treatment planning.

- May 2026: Tempus AI received FDA approval for the tumor-only indication of its xT CDx next-generation sequencing platform and launched its Lens agentic AI platform to support oncology drug development.

- May 2026: GRAIL presented PATHFINDER 2 study results from 35,878 participants at the 2026 ASCO Annual Meeting, showing that Galleri significantly increased cancer detection when added to standard screenings.

Global Software As A Medical Device (SaMD) For Oncology Market Report Scope

As per the scope of the report, Software as a Medical Device (SaMD) for oncology is standalone software used to diagnose, treat, or monitor cancer without relying on physical hardware like an MRI or X-ray machine. It runs on general-purpose computers, smartphones, or cloud servers to process cancer data.

The Software as a Medical Device (SaMD) for oncology market is segmented by application, technology, end user, deployment mode, and geography. By application, the market is segmented into screening and early detection, diagnosis and triage, treatment planning and therapy selection, monitoring, recurrence, and response assessment, clinical trial matching and patient stratification, and pathology and molecular analysis support. By technology, the market is segmented into machine learning and deep learning, computer vision and imaging AI, natural language processing, and predictive analytics and risk scoring. By end user, the market is segmented into hospitals and cancer centers, diagnostic laboratories, pharmaceutical and biotechnology companies, and academic and research institutes. By deployment mode, the market is segmented into cloud-based and on-premise. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Screening and Early Detection |

| Diagnosis and Triage |

| Treatment Planning and Therapy Selection |

| Monitoring, Recurrence, and Response Assessment |

| Clinical Trial Matching and Patient Stratification |

| Pathology and Molecular Analysis Support |

| Machine Learning and Deep Learning |

| Computer Vision and Imaging AI |

| Natural Language Processing |

| Predictive Analytics and Risk Scoring |

| Hospitals and Cancer Centers |

| Diagnostic Laboratories |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Cloud-Based |

| On-Premise |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Screening and Early Detection | |

| Diagnosis and Triage | ||

| Treatment Planning and Therapy Selection | ||

| Monitoring, Recurrence, and Response Assessment | ||

| Clinical Trial Matching and Patient Stratification | ||

| Pathology and Molecular Analysis Support | ||

| By Technology | Machine Learning and Deep Learning | |

| Computer Vision and Imaging AI | ||

| Natural Language Processing | ||

| Predictive Analytics and Risk Scoring | ||

| By End User | Hospitals and Cancer Centers | |

| Diagnostic Laboratories | ||

| Pharmaceutical and Biotechnology Companies | ||

| Academic and Research Institutes | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for Software as a Medical Device in oncology?

The sector is projected to reach USD 46.88 billion by 2031 from USD 25.16 billion in 2026, advancing at a 13.25% CAGR over the forecast period.

Which application area generates the most revenue today?

Diagnosis and Triage leads current demand with a 35.45% share in 2025 because hospitals and cancer centers need faster reading and decision support in high-volume workflows.

Which use case is expanding the fastest through 2031?

Screening and Early Detection is projected to post the fastest application growth at a 16.93% CAGR, supported by multi-cancer early detection programs and broader population screening efforts.

Why does North America lead current demand?

North America held 41.52% share in 2025 due to a more established FDA pathway, stronger software funding, and faster health system adoption of AI-enabled clinical tools.

What is changing competition among vendors?

Competition is moving from single-point tools toward broader platforms, with deals such as Roche's PathAI acquisition and Tempus AI's Paige integration showing how scale and workflow coverage are becoming more important.

What is the biggest commercial barrier to wider adoption?

Reimbursement remains the main hurdle because clinical and regulatory progress is moving faster than coverage, coding, and payer alignment for many oncology software workflows.

Page last updated on: