Software As A Medical Device (SaMD) For Cardiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 28.67 Billion |

| Market Size (2031) | USD 58.30 Billion |

| Growth Rate (2026 - 2031) | 15.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

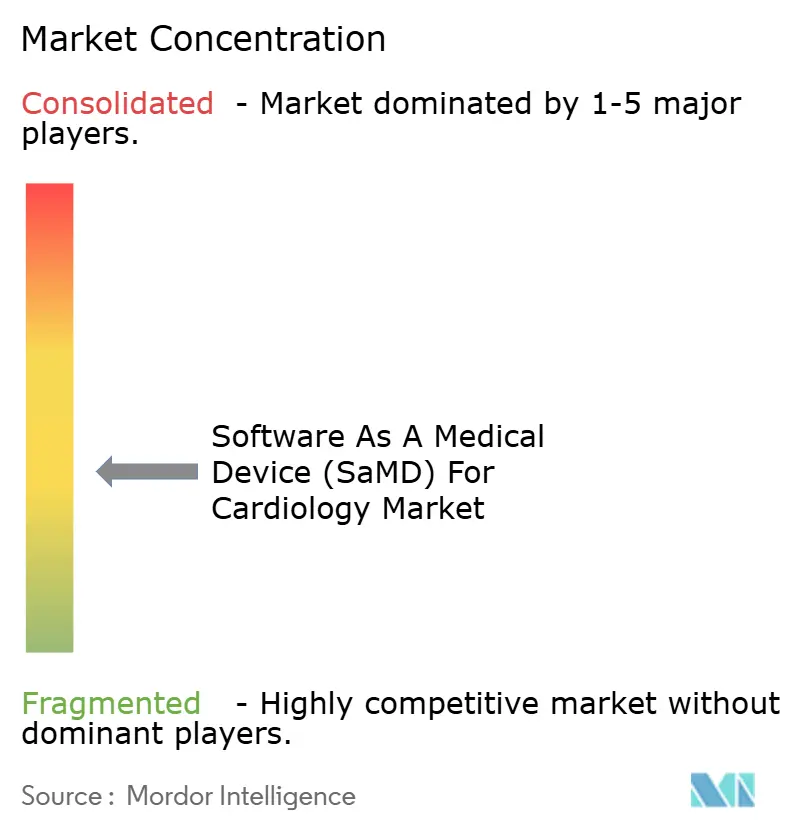

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software As A Medical Device (SaMD) For Cardiology Market Analysis by Mordor Intelligence

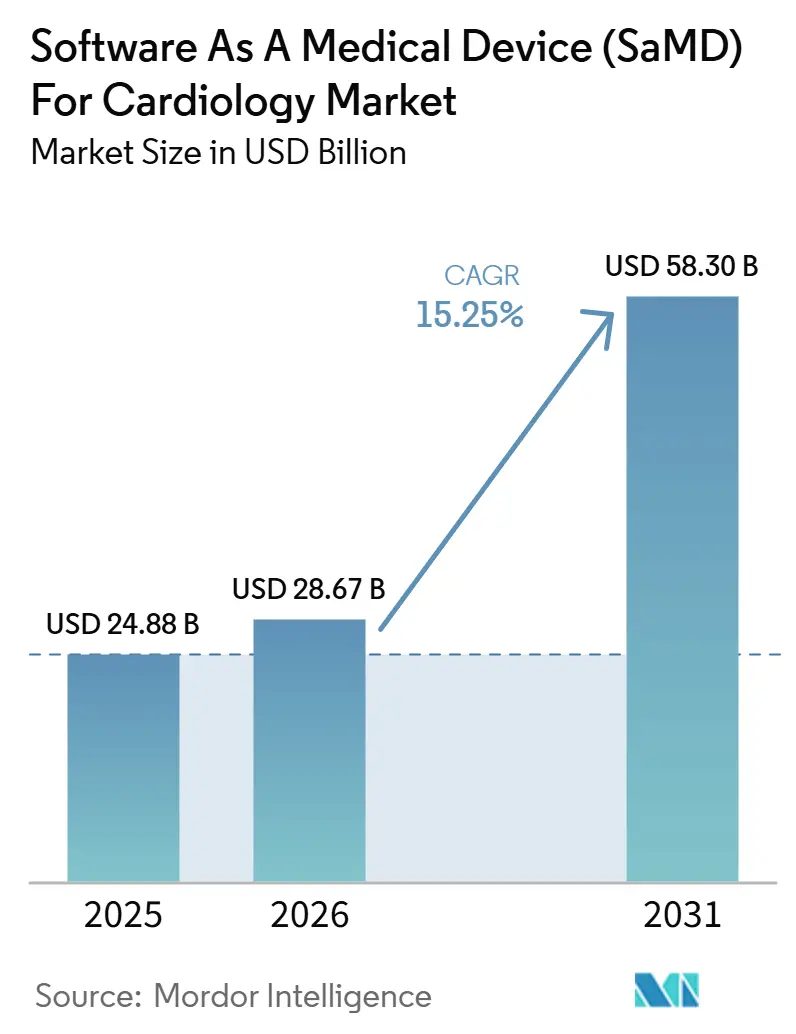

The Software As A Medical Device For Cardiology Market size is expected to increase from USD 24.88 billion in 2025 to USD 28.67 billion in 2026 and reach USD 58.30 billion by 2031, growing at a CAGR of 15.25% over 2026-2031.

Permanent reimbursement support for AI-enabled cardiac analysis is helping the market move from limited pilots toward routine clinical use, especially where providers can link software outputs to clear payment pathways. FDA cardiology AI and ML clearance activity also expanded from 62 in 2024 to 92 in 2025, widening the pool of deployable tools and strengthening the commercial pipeline. As deployed products collect more annotated patient data, vendors with approved update pathways can keep improving algorithm performance after launch, giving early movers a stronger position. Despite strong demand, gaps in clearance speed, real-world evidence quality, and deep EHR integration continue to separate scalable vendors from those that only secure approvals.

Key Report Takeaways

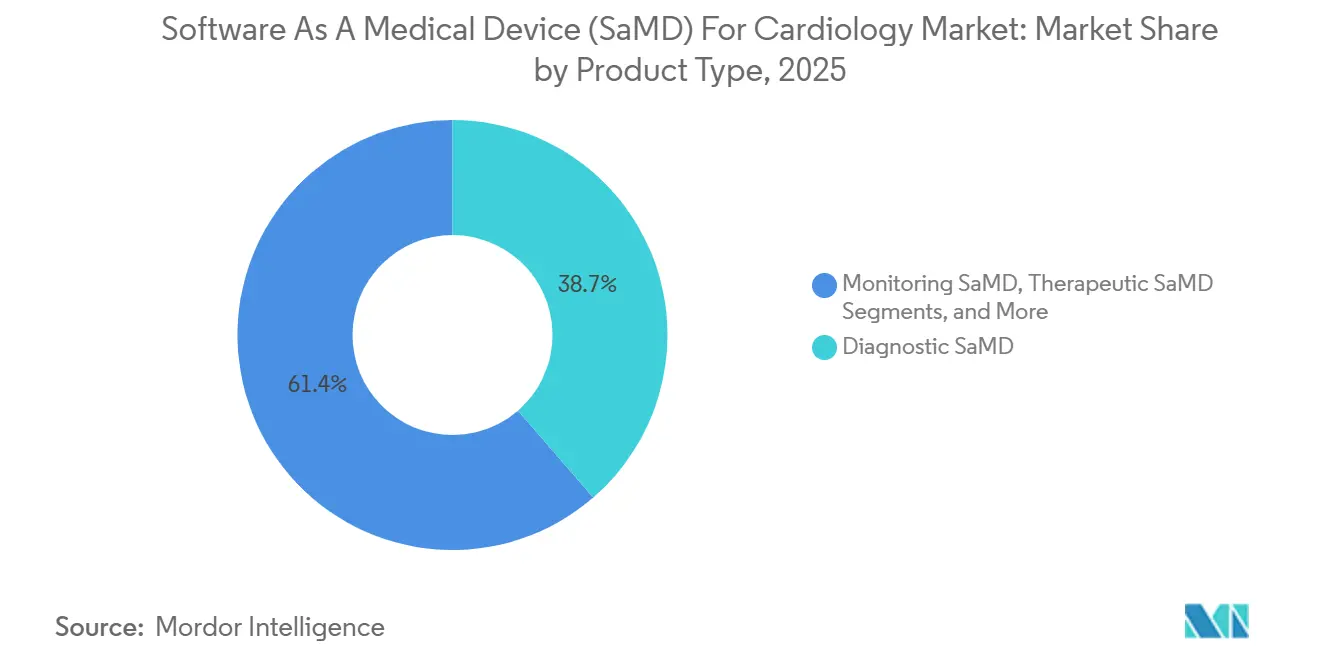

- By product type, diagnostic SaMD held 38.65% of the Software as a Medical Device (SaMD) for cardiology market in 2025, while Monitoring SaMD is projected to grow at 18.93% CAGR through 2031.

- By clinical application, arrhythmia detection accounted for 35.23% of the Software as a Medical Device (SaMD) for Cardiology market in 2025, while heart failure management is projected to expand at 19.67% CAGR through 2031.

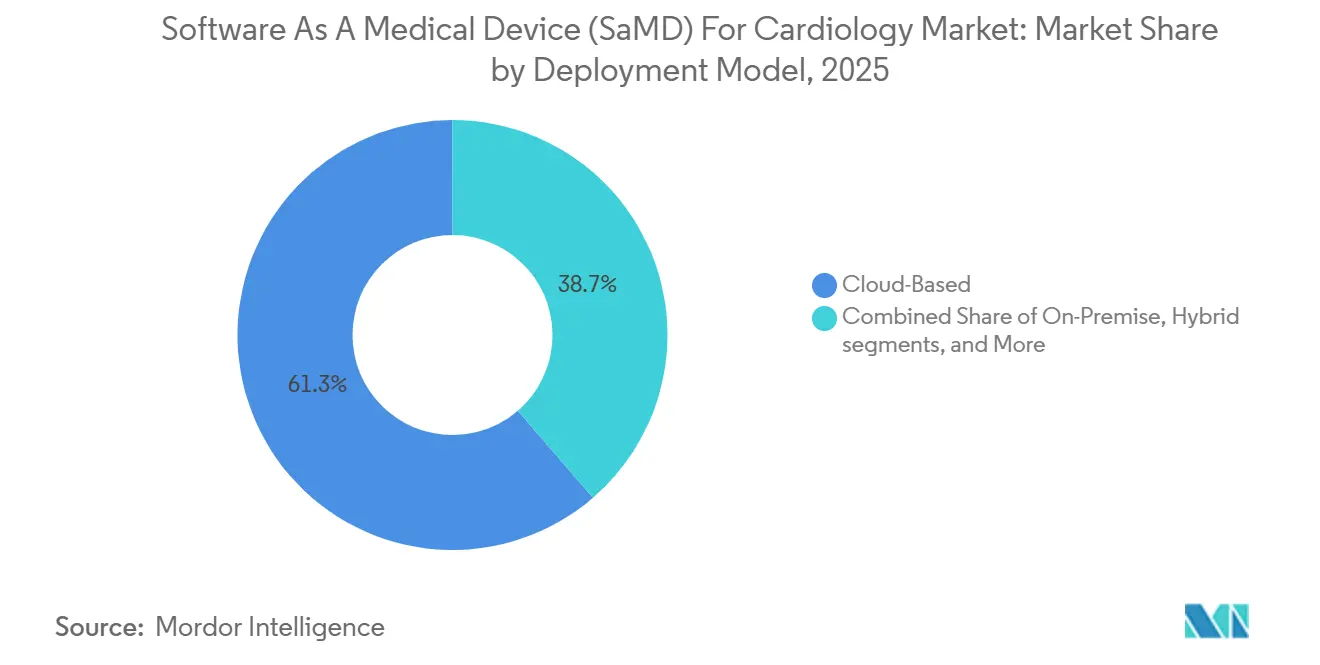

- By deployment model, cloud-based deployment held 61.34% of the Software as a Medical Device (SaMD) for Cardiology market in 2025, while the hybrid model is projected to advance at 18.35% CAGR through 2031.

- By end user, hospitals and health systems captured 42.88% of the Software as a Medical Device (SaMD) for Cardiology market in 2025, while Home healthcare and remote monitoring providers are expected to grow at 19.78% CAGR through 2031.

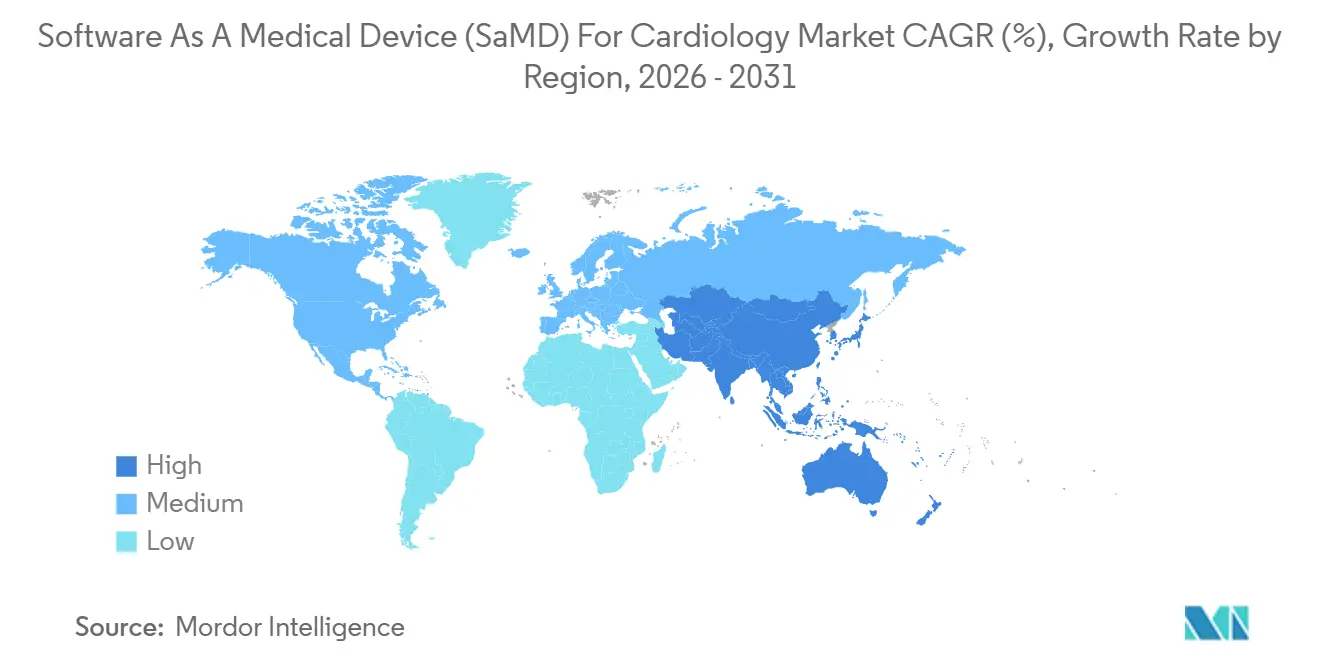

- By geography, North America held 40.56% of the Software as a Medical Device (SaMD) for Cardiology market in 2025, while Asia-Pacific is projected to record the highest regional CAGR of 17.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Software As A Medical Device (SaMD) For Cardiology Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory push for AI-enabled cardiovascular decision support | +3.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Rising burden of arrhythmia and coronary imaging workload | +2.9% | Global, with stronger acceleration in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Shift to remote, software-led cardiac monitoring pathways | +2.1% | North America, Asia-Pacific, and Western Europe | Medium term (2-4 years) |

| Reimbursement expansion for evidence-backed cardiac SaMD | +2.4% | North America primarily, with spillover into Europe | Short term (≤ 2 years) |

| Edge-to-cloud interoperability with HER and imaging systems | +1.2% | North America and Europe, with gradual spillover into Asia-Pacific | Long term (≥ 4 years) |

| Real-world evidence loops improving algorithm performance | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push Is Creating a First-Mover Reimbursement Moat

Regulatory momentum is giving the Software as a Medical Device (SaMD) for Cardiology market a faster route from approval to revenue. FDA cardiology AI and ML clearances rose to 92 in 2025 from 62 in 2024, widening the pool of tools ready for deployment. Eight of the 2025 clearances included a Predetermined Change Control Plan, which allows post-market algorithm updates within an approved framework. This gives early-cleared vendors an advantage in improving performance with live clinical data while staying within the approved regulatory pathway.

Reimbursement Expansion Is the Demand Unlock the Market Was Waiting For

Payment expansion is removing one of the last major barriers in the Software as a Medical Device (SaMD) for Cardiology market. CMS made CPT code 75577 effective on January 1, 2026, with a USD 950.50 hospital outpatient payment for AI-enabled coronary plaque analysis from CCTA. CMS also created code G0680 for AI-based coronary artery calcium and aortic valve calcium analysis on chest CT, while trade reporting showed a USD 128.90 national Medicare payment rate for AI-enabled ECG analysis under CPT codes 0764T and 0765T. Predictable payment is helping hospitals and outpatient sites link software adoption to a defined reimbursement pathway.[1]Centers for Medicare & Medicaid Services, “Billing and Coding: Artificial Intelligence Enabled CT Based Quantitative Coronary Topography (AI-QCT)/Coronary Plaque Analysis (AI-CPA) (A59716),” CMS, cms.gov

The Arrhythmia Detection Burden Is Larger Than Reported Incidence Suggests

The scale of undiagnosed rhythm disorders is also pulling the Software as a Medical Device (SaMD) for Cardiology market forward. iRhythm stated that 27 million people in the United States are at risk for undiagnosed arrhythmias each year, keeping screening demand well above the diagnosed patient base. A 2025 Nature Medicine study on 14,606 ambulatory ECG recordings found that DeepRhythmAI achieved 98.6% sensitivity for critical arrhythmias, compared with 80.3% for certified human technicians. iRhythm's 2026 revenue guidance of USD 870-880 million further showed that large-scale rhythm monitoring platforms are converting clinical demand into commercial scale.[2]A. Hussain et al., “Is the FDA Regulation of Cardiology AI Devices Supporting Innovation?,” BMJ Heart, heart.bmj.com

Remote Cardiac Monitoring Is Shifting Clinical Gravity from Hospitals to the Home

Remote care is shifting part of the Software as a Medical Device (SaMD) for Cardiology market away from hospital settings and toward continuous follow-up. Home Healthcare and Remote Monitoring Providers are projected to expand at a 19.78% CAGR from 2026 to 2031, making them the fastest-growing end-user group in the draft. This growth reflects rising demand for software that can interpret ECG data, stratify risk, and route patients into follow-up without repeated in-person visits. As cardiac follow-up moves into homes and outpatient settings, vendors that connect data capture, interpretation, and care coordination are in a stronger position.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Clinical validation burden across heterogeneous cardiac populations | -2.2% | Global, with stronger pressure in emerging markets | Medium term (2-4 years) |

| Cybersecurity, privacy, and data governance risk | -1.4% | Global, with the highest litigation and compliance pressure in North America and Europe | Short term (≤ 2 years) |

| Workflow resistance and liability concerns among providers | -0.9% | Global, with stronger impact in community and rural settings | Medium term (2-4 years) |

| Fragmented reimbursement and coding pathways across payers | -1.3% | North America primarily, with developing pathways in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thin Clinical Evidence Is the Structural Vulnerability Beneath the Clearance Headline

Evidence quality remains a key constraint in the Software as a Medical Device (SaMD) for Cardiology market. A 2026 review of 277 FDA-cleared cardiology AI and ML devices found that bench studies accounted for 69.3% of validation studies, while prospective multicenter clinical trials accounted for only 3.2%. The same review reported a high risk of predicate creep in 52.2% of cleared cardiology AI devices, raising concerns over how far newer claims had moved from the original validated use case. CMS had already applied strict procedural criteria in LCD L39881 for AI-enabled coronary plaque analysis, showing that reimbursement can tighten as evidence standards rise.[3]L.S. Johnson, P. Zadrozniak, G. Jasina et al., “Artificial Intelligence for Direct-to-Physician Reporting of Ambulatory Electrocardiography,” Nature Medicine, doi.org Vendors with broader multi-site validation and cleaner clinical datasets are better positioned to defend coverage and pricing as scrutiny increases.

Cybersecurity Incidents Are Reshaping the Risk Calculus for Payers and Providers

Cybersecurity and data governance are slowing adoption in the Software as a Medical Device (SaMD) for Cardiology market, even when clinical need is clear. These platforms handle protected health information across cloud, edge, and hospital systems, making privacy reviews part of the full operating environment. Providers are spending more time on security due diligence, contract terms, data flow mapping, and third-party risk reviews before deployment, which extends enterprise sales cycles and raises implementation costs. Vendors that demonstrate strong governance, interoperable architecture, and clear accountability for incident response are better positioned to win large health system contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostic Tools Define the Market's Foundation

Diagnostic SaMD held 38.65% of the Software as a Medical Device (SaMD) for Cardiology market share in 2025, making it the foundation of current revenue. Its leadership reflected the smooth integration of diagnostic outputs into established cardiology workflows, especially in imaging-led hospital settings. In 2025, coronary CT tools alone accounted for 9 plaque quantification clearances, 7 calcium scoring clearances, and 3 FFR-derived clearances in the United States. This concentration kept diagnostic software closely aligned with routine ordering patterns, reimbursement use, and physician acceptance.

Monitoring SaMD is projected to grow at a CAGR of 18.93% from 2026 to 2031, making it the fastest-growing product type in the Software as a Medical Device (SaMD) for Cardiology market size. Growth is moving beyond simple ambulatory ECG patches toward software that combines ECG, impedance, and activity data in a single monitoring stream. Clinical decision support tools are also gaining traction as payment models begin to reward specific outputs, such as AI-enabled ECG interpretation, rather than only raw signal review. Therapeutic software remains the smallest product group as regulators continue to take a cautious approach to closed-loop or therapy-adjusting cardiac applications.

By Clinical Application: Heart Failure Management Is Re-Shaping the Market's Growth Profile

Arrhythmia detection accounted for 35.23% of the clinical application mix in 2025, keeping it at the center of current spending. The segment benefited from a large undiagnosed population, a longer history of cleared rhythm tools, and clearer reimbursement visibility than many newer cardiac applications. Hospitals and ambulatory rhythm programs already understood how to use ECG-based software, which reduced adoption friction. This installed base also allowed arrhythmia tools to become the first software layer within broader digital cardiology strategies.

Heart failure management is forecast to grow at a CAGR of 19.67% through 2031, giving it the fastest expansion profile within the Software as a Medical Device (SaMD) for Cardiology market. Remote hemodynamic monitoring, AI-driven risk stratification, and the ongoing need to reduce readmissions across health systems support this growth. Coronary artery disease assessment is also advancing after reimbursement support for AI-enabled plaque analysis, although the patent dispute between HeartFlow and Cleerly showed intensifying competition in this sub-segment. Structural heart disease assessment and cardiac imaging analysis continue to benefit from automation that reduces manual review time and supports standardized interpretation.

By Deployment Model: Cloud Dominates, but Hybrid Architecture Is Where the Enterprise Deals Are

Cloud-based deployment held 61.34% of the model mix in 2025, making it the operating default for much of the Software as a Medical Device (SaMD) for Cardiology market. Providers favored cloud delivery because it supported subscription pricing, centralized updates, and scalable computing for imaging and ECG review. It also suited platforms that required continuous retraining, feature refreshes, and broader data aggregation after launch. For vendors, cloud delivery shortened rollout timelines across multi-site health systems that preferred one administrative layer over multiple local installations.

Hybrid deployment is projected to grow at a CAGR of 18.35% from 2026 to 2031, making it the fastest-growing model in the Software as a Medical Device (SaMD) for Cardiology market. Health systems increasingly want local edge processing for time-sensitive arrhythmia alerts and cloud processing for higher-volume imaging analytics. Hybrid architecture gives them tighter latency control without sacrificing enterprise scale, centralized management, or easier software updates. On-premise deployment still retains a role in parts of APAC and the Middle East, where data residency rules or public hospital IT policies limit cloud use.

By End User: Hospitals Lead, but the Growth Opportunity Lies Beyond the Clinic

Hospitals and health systems held 42.88% of end-user demand in 2025, keeping them as the largest buyers in the Software as a Medical Device (SaMD) for Cardiology market. Their leadership was supported by the fact that most decision support tools still depended on enterprise EHR integration, imaging connectivity, and formal clinical governance. Large health systems also justified deployment spending more easily when software supported cardiology, radiology, emergency, and outpatient service lines. This gave an advantage to vendors that supported procurement, security review, clinician training, and multi-site implementation at system scale.

Home healthcare and remote monitoring providers are forecast to grow at a CAGR of 19.78% through 2031, making them the fastest-growing end-user group. Consumer-connected ECG tools and software-led review workflows are creating care coordination models that reach patients between visits and after discharge. Cardiology clinics remain a structurally underserved channel, especially for AI-assisted ECG interpretation and remote monitoring review. Ambulatory care centers and diagnostic imaging centers are also responding quickly to reimbursable CCTA plaque analysis workflows that align with outpatient throughput expectations.

Geography Analysis

North America held 40.56% of the Software as a Medical Device (SaMD) for Cardiology market share in 2025, maintaining its global lead. The United States moved faster than other countries on reimbursement, with separate Medicare payment pathways in place for AI-enabled coronary plaque analysis, ECG analysis, and calcium analysis. This payment clarity supported commercial scale for pure-play vendors and imaging incumbents. The region also benefited from a large installed hospital base, while Canada and Mexico advanced despite reimbursement frameworks trailing the United States.

Asia-Pacific is projected to grow at a 17.56% CAGR from 2026 to 2031, making it the fastest-growing regional bloc in the Software as a Medical Device (SaMD) for Cardiology market. Growth is being driven by cardiovascular disease burden, national digitization efforts, and stronger regulatory alignment across major countries. Japan and South Korea are advancing with clearer product approvals, while China is attracting investment that links procedural hardware with software-enabled cardiac workflows. India and Southeast Asia remain earlier in adoption, where public health digitization programs are shaping near-term demand more than private reimbursement.

Europe held the third-largest regional share in 2025, with Germany, the United Kingdom, and France forming the main demand base. A stricter compliance environment is raising entry and product maintenance requirements while favoring vendors with stronger regulatory depth. The Middle East and Africa are still earlier in adoption, but Gulf markets are using FDA and CE pathways as reference points for local registration and early procurement. South America is gradually building its position as Brazil and Argentina work on reimbursement frameworks for AI diagnostics.

Competitive Landscape

The Software as a Medical Device (SaMD) for Cardiology market remains moderately fragmented, with large imaging vendors and pure-play software companies competing in parallel. GE HealthCare, Siemens Healthineers, Philips, Canon Medical, and Medtronic use established hardware relationships to embed AI features within broader imaging and monitoring contracts. This approach helps protect renewal cycles by positioning software as part of a larger clinical system rather than a standalone purchase. Pure-play companies, such as iRhythm, Viz.ai, Anumana, HeartFlow, and Cleerly, compete on algorithm depth, reimbursement alignment, and integration speed.

Medtronic’s planned acquisition of CathWorks for up to USD 585 million in February 2026 showed how established device companies acquired software capabilities instead of building every function internally. Its June 2026 investments in Beluga Medical and CardioACC further showed a push to connect cardiac procedures more closely with software-led assessment and guidance. Viz.ai’s partnership with Alnylam in March 2026 to launch a cardiac amyloidosis care pathway across its broader cardiology suite reflected a care coordination strategy rather than a single-algorithm approach. Anumana followed a focused approach by targeting cardiac amyloidosis and pulmonary hypertension, where early clearance created opportunities before larger firms committed major resources.

Competitive pressure increased in high-value imaging niches, as reflected in HeartFlow’s April 2026 patent lawsuit against Cleerly over coronary anatomy analysis. The dispute suggested that intellectual property became more important as reimbursement support and clinical adoption improved in coronary assessment. Newer entrants still had opportunities because predictive and prescriptive cardiac AI remained much smaller than diagnostic software within the cleared mix. The Software as a Medical Device (SaMD) for Cardiology market still offered room for disruption, especially for vendors with strong validation, clear payment pathways, and practical integration.

Software As A Medical Device (SaMD) For Cardiology Industry Leaders

AliveCor, Inc.

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Medtronic plc

Cardiologs Technologies SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Anumana Inc. received FDA 510(k) clearance (K253801) for its ECG-AI Cardiac Amyloidosis algorithm, the first cleared solution for this indication using a standard 12-lead ECG.

- March 2026: GE HealthCare announced its lead industrial role in the five-year, EUR 50.5 million EU-funded COMPASS consortium to advance AI-enabled cardio-oncology care across Europe.

- March 2026: Viz.ai partnered with Alnylam Pharmaceuticals to launch the Viz Cardiac Amyloidosis Care Pathway, a multi-site pilot integrated into the Viz Cardio Suite.

- February 2026: Medtronic announced plans to acquire CathWorks, developer of the AI-powered FFRangio coronary assessment system, at a valuation of up to USD 585 million.

- January 2026: AliveCor received FDA 510(k) clearance (K252589) for Corvair Monza, a PCCP-authorized SaMD analyzing 10-second ECGs for rhythm, morphology, and acute MI patterns.

Global Software As A Medical Device (SaMD) For Cardiology Market Report Scope

As per the scope of the report, Software as a Medical Device (SaMD) for cardiology is standalone software that runs on standard computers or mobile platforms to diagnose, treat, or manage heart conditions. Instead of relying solely on a physical machine, cardiologists use this software to analyze heart data, detect irregular rhythms, and predict heart attacks.

The software as a medical device (SaMD) for cardiology market is segmented by product type, clinical application, deployment model, end user, and geography. By product type, the market includes diagnostic SaMD, monitoring SaMD, clinical decision support SaMD, and therapeutic SaMD. By clinical application, the market is segmented into arrhythmia detection, coronary artery disease assessment, heart failure management, structural heart disease assessment, and cardiac imaging analysis. By deployment model, the market is categorized into cloud-based, on-premise, and hybrid. By end user, the market is segmented into hospitals and health systems, cardiology clinics, ambulatory care centers, home healthcare and remote monitoring providers, and diagnostic imaging centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Diagnostic SaMD |

| Monitoring SaMD |

| Clinical Decision Support SaMD |

| Therapeutic SaMD |

| Arrhythmia Detection |

| Coronary Artery Disease Assessment |

| Heart Failure Management |

| Structural Heart Disease Assessment |

| Cardiac Imaging Analysis |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Hospitals and Health Systems |

| Cardiology Clinics |

| Ambulatory Care Centers |

| Home Healthcare and Remote Monitoring Providers |

| Diagnostic Imaging Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Diagnostic SaMD | |

| Monitoring SaMD | ||

| Clinical Decision Support SaMD | ||

| Therapeutic SaMD | ||

| By Clinical Application | Arrhythmia Detection | |

| Coronary Artery Disease Assessment | ||

| Heart Failure Management | ||

| Structural Heart Disease Assessment | ||

| Cardiac Imaging Analysis | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Hospitals and Health Systems | |

| Cardiology Clinics | ||

| Ambulatory Care Centers | ||

| Home Healthcare and Remote Monitoring Providers | ||

| Diagnostic Imaging Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of Software as a Medical Device (SaMD) for Cardiology by 2031?

The Software as a Medical Device (SaMD) for Cardiology market is projected to reach USD 58.30 billion by 2031, rising from USD 28.67 billion in 2026 at a 15.25% CAGR.

Which product segment leads current demand in digital cardiology software?

Diagnostic SaMD led in 2025 with 38.65% share, supported by stronger workflow fit and a mature imaging AI pipeline.

Which application is growing fastest through 2031?

Heart Failure Management is the fastest-growing clinical application, with a forecast CAGR of 19.67% through 2031.

Why is North America ahead of other regions?

North America led with 40.56% share in 2025 because reimbursement pathways in the United States moved faster and supported broader commercialization.

What is driving adoption in outpatient and home-based cardiac care?

Home Healthcare and Remote Monitoring Providers are projected to grow at 19.78% CAGR because software can support follow-up, ECG interpretation, and risk routing outside the hospital.

How are large companies competing with pure-play software firms?

Large vendors are using hardware relationships and acquisitions such as Medtronic's planned CathWorks deal, while pure-play firms compete on focused algorithms, reimbursement alignment, and integration speed.

Page last updated on: