Social Media Advertising Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Market Size (2026) | USD 227.88 Billion |

| Market Size (2031) | USD 422.58 Billion |

| Growth Rate (2026 - 2031) | 13.15% CAGR |

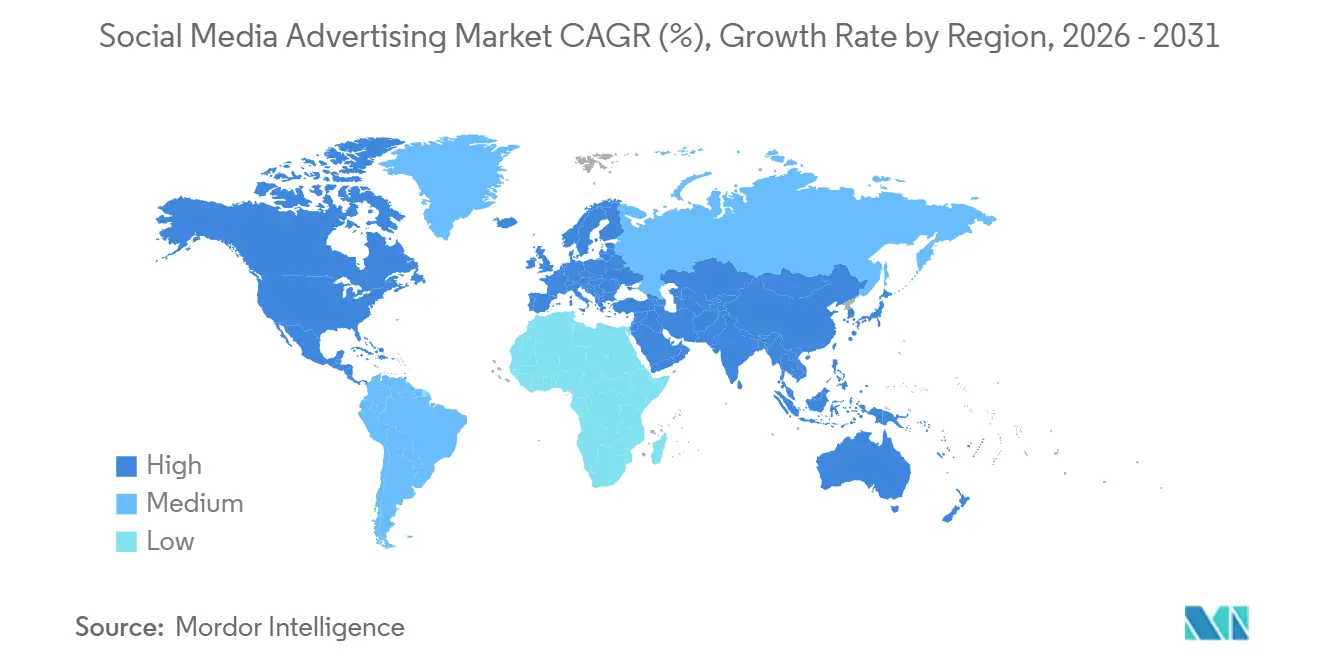

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Social Media Advertising Market Analysis by Mordor Intelligence

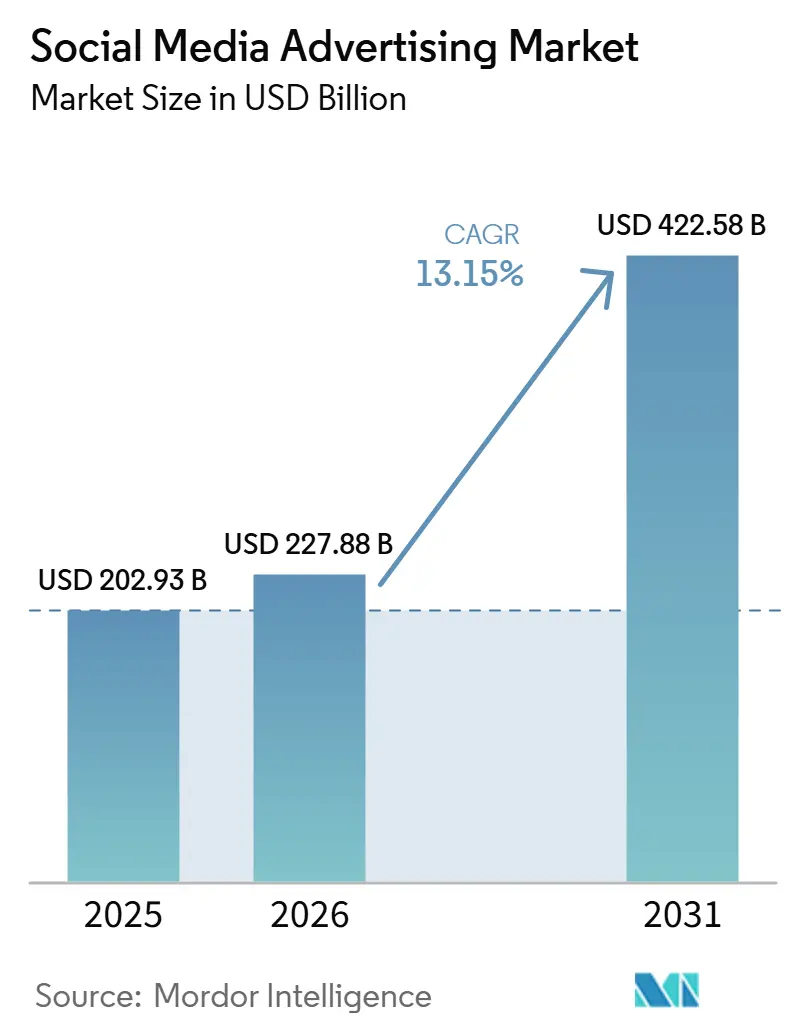

The social media advertising market size was valued at USD 202.93 billion in 2025 and estimated to grow from USD 227.88 billion in 2026 to reach USD 422.58 billion by 2031, at a CAGR of 13.15% during the forecast period (2026-2031). The social media advertising market is expanding as platforms improve monetization with AI-based ad tools, stronger commerce links, and better measurement systems that help advertisers connect spending more directly to outcomes. The category now captures close to 40% of global digital advertising revenue, and that position continues to strengthen as spending shifts away from traditional display formats and linear media. Platform economics also remained favorable in 2025 because major networks lifted both ad inventory and pricing, which showed that stronger targeting and placement efficiency could support revenue growth without relying only on audience expansion. The social media advertising market also benefits from a growing gap between user time spent and advertiser spending, since monetization per impression is improving even in places where usage growth has slowed. At the same time, macroeconomic caution, tariff-related pressure on advertiser budgets, and brand safety concerns are keeping competition focused on AI-based optimization, creative quality, and dependable performance measurement.

Key Report Takeaways

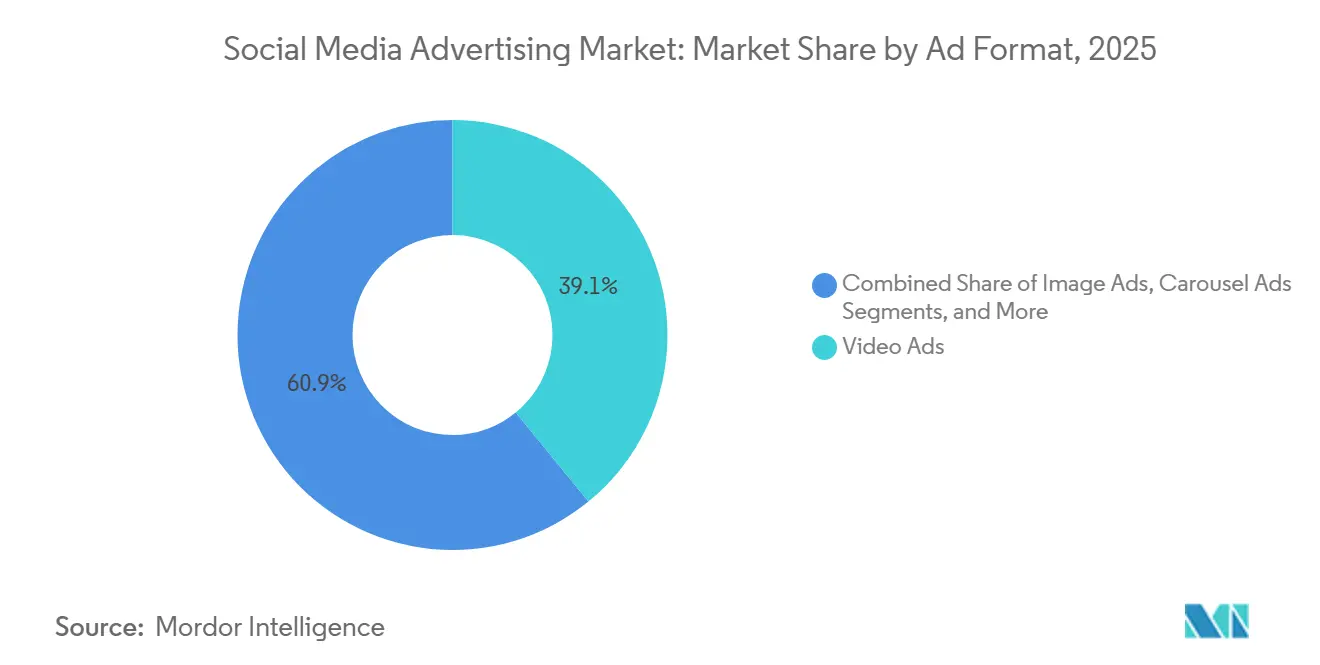

- By Ad format, video ads accounted for 39.11% of the social media advertising market size in 2025, and the same segment is projected to expand at a 14.52% CAGR through 2031.

- By platform, social networking platforms held 46.32% of the social media advertising market share in 2025, while video-sharing platforms are expected to record the fastest CAGR at 16.34% through 2031.

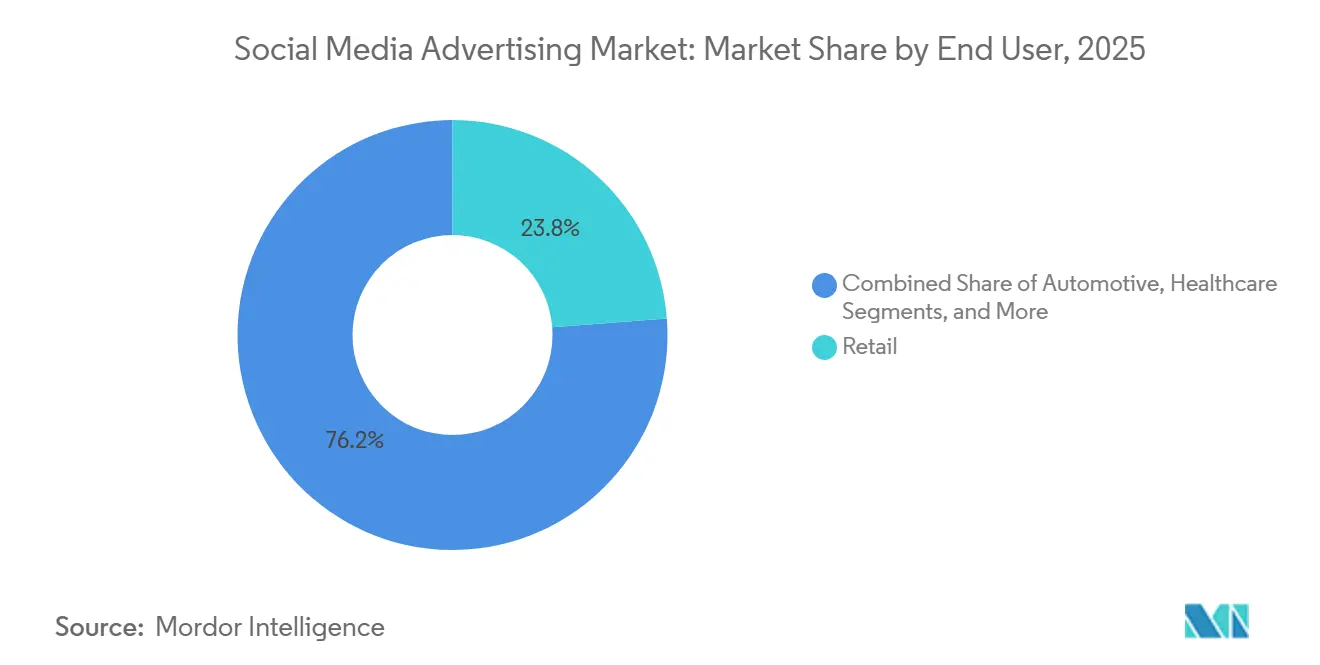

- By end user, retail captured 23.77% of the social media advertising market size in 2025, while healthcare is projected to grow at the fastest CAGR of 15.78% through 2031.

- By geography, North America held 40.45% of the social media advertising market size in 2025, while Asia-Pacific is forecast to expand at the highest CAGR of 15.22% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Social Media Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Share of Mobile-First Social Commerce | +2.5% | Global, strongest in Asia-Pacific and South America | Short term (≤ 2 years) |

| Short-Form Video Ad Inventory Expansion | +2.0% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of Creator-Led Performance Advertising | +2.0% | Global, North America and Europe leading | Short term (≤ 2 years) |

| Growth in First-Party Audience Targeting | +1.8% | North America and EU, extending to APAC | Medium term (2-4 years) |

| Retail Media Spillover Into Social Platforms | +1.5% | North America and EU, with APAC emerging | Medium term (2-4 years) |

| Better Incrementality Measurement and Attribution Tools | +1.2% | Global, North America and Europe ahead in adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Share of Mobile-First Social Commerce

The social media advertising market is seeing faster convergence between ad discovery and purchase activity, and platforms that keep the full shopping journey inside the app are benefiting the most. This shift is making ad spending more conversion-focused because the value of an impression is now tied more closely to a completed transaction than to reach alone. Retailers are also moving more budget into native commerce campaigns, which shows that lower-funnel social buying has become part of regular planning rather than a limited test program. Platforms with strong visual search and product discovery features are in a favorable position because they can capture planning intent earlier in the purchase process and keep users inside a monetizable environment. Pinterest reported 619 million monthly active users and 80 billion monthly searches in 2025, which points to the scale of product discovery behavior that commerce-linked formats can monetize. The social media advertising market is therefore gaining support from stronger retailer-platform alignment, faster mobile-native creative cycles, and a clearer link between ad delivery and sales outcomes.

Short-Form Video Ad Inventory Expansion

The social media advertising market continues to gain momentum from the rapid expansion of short-form video inventory across major platforms. Video already held the largest format share in 2025, and its position is being reinforced because Reels, Shorts, and similar placements give advertisers large scale, high frequency, and faster creative testing in the same buying environment. This format is also attracting more budgets from categories that once relied on television or static digital placements because it combines storytelling with clear performance signals. Meta reported that ad impressions across its Family of Apps grew 12% in 2025 and that average price per ad rose 9%, which shows that additional inventory is being absorbed without weakening pricing.[1]Meta Platforms, Inc., “Form 10-K, Annual Report for Fiscal Year Ended December 31, 2025,” Meta Platforms, last10k.com Alphabet stated that YouTube surpassed USD 60 billion in combined advertising and subscription revenue for the first time, which underscores the commercial depth of video-led platform ecosystems.[2]Alphabet Inc., “Alphabet Earnings, Q4 2025, CEO's Remarks,” Alphabet Inc., blog.google As this inventory base keeps widening, the social media advertising market is becoming more dependent on creative speed, AD relevance, and ranking quality than on pure audience growth.

Expansion of Creator-Led Performance Advertising

The social media advertising market is also being lifted by creator-led campaigns that now serve direct response goals instead of only awareness goals. Creator placements are moving deeper into performance budgets because advertisers can connect creator content to measurable traffic, conversion, and purchase activity with far more precision than before. Creator-led advertising spend has become a major media allocation rather than a side channel. This matters for the social media advertising market because creator content expands premium inventory in a format that feels native to user feeds and often carries stronger engagement than standard brand creative. Smaller creators are also drawing more advertiser attention because tightly engaged communities can deliver strong response quality even without the largest audience scale. As a result, platforms are treating creator ecosystems as core supply infrastructure, and that is strengthening the link between content economics, inventory growth, and advertiser retention.

Growth in First-Party Audience Targeting

The social media advertising market is adapting to a stricter privacy environment by relying more heavily on first-party audience signals. Changes to third-party tracking have reduced the availability of open-web signals, which has increased the value of platform-owned data, CRM integration, email lists, and on-site behavioral inputs. This is shifting competitive advantage toward companies that can maintain effective event tracking through direct integrations and server-based data connections. The social media advertising market therefore rewards advertisers that invested early in data pipelines, because those systems support better audience matching and more stable optimization even when external identifiers weaken. Platforms are also working to rebuild signal depth through proprietary user interactions and internal ecosystems, which keeps targeting performance from falling as sharply as it might have under a fully open-web model. The practical result is that first-party data is no longer a support tool in the social media advertising market, and it is now part of the basic operating model for efficient media delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Platform Policy Volatility and Auction Complexity | -0.8% | Global, EU most exposed to policy shifts | Short term (≤ 2 years) |

| Measurement Gaps From Privacy Restrictions | -0.6% | North America and EU (GDPR, ATT-affected markets) | Medium term (2-4 years) |

| Creative Fatigue and Rising Cost Per Outcome | -0.4% | Global | Short term (≤ 2 years) |

| Brand Safety and Content Moderation Risk | -0.3% | Global, amplified in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Platform Policy Volatility and Auction Complexity

The social media advertising market still faces pressure from sudden policy changes, moderation shifts, ownership changes, and unstable auction conditions that make budget planning harder for advertisers. These disruptions do not usually lead to a broad exit from social platforms, but they do encourage spending diversification across more channels and partners. That pattern limits how much any single platform can increase its share even when total category spending is rising. Auction conditions also remain difficult for smaller advertisers because pricing can move quickly during competitive periods, which reduces forecasting confidence and makes campaign pacing more complicated. The social media advertising market therefore remains sensitive to platform-specific reputation changes, even when overall advertiser demand stays intact. This restraint matters most in a market where automation is increasing, because advertisers still need confidence in platform rules and delivery conditions before they allow larger shares of budget to be managed automatically.

Measurement Gaps from Privacy Restrictions

The social media advertising market continues to operate with weaker attribution precision because privacy-related signal loss has reduced the number of deterministic identifiers available across devices and websites. This has made the gap wider between platform-reported conversions and independently measured performance, especially for advertisers that still rely on last-click or identifier-heavy multi-touch models. The challenge is more serious for smaller advertisers because they often lack the scale needed for advanced holdout testing, robust modeling, or data clean room approaches. The social media advertising market is responding through probabilistic attribution, marketing mix modeling, and cleaner first-party integrations, but these steps reduce uncertainty rather than remove it. In regulated environments, consent requirements further limit retargeting precision and create a structurally lower signal baseline for campaign optimization. This means the social media advertising market can still grow strongly, yet advertisers will continue to scrutinize return on spend more closely where measurement quality remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ad Format: Video Commands Scale and Consistent Growth

Video ads held 39.11% share in 2025, and the segment is also expected to post the fastest 2026-2031 CAGR at 14.52%, which keeps it at the center of the social media advertising market. The segment leads because short-form viewing behavior has become embedded across major apps, and advertisers now treat video as both a reach format and a response format. The social media advertising industry is seeing short-form video formats strengthen further, as Reels, Shorts, and similar placements absorb more brand and performance budgets within the same campaign cycle. Combined Instagram and Facebook Reels crossed a USD 50 billion annual revenue run rate in October 2025, and more than half of all ads on Instagram ran in the Reels placement throughout 2025, up from 35% in 2024, while users spent 46% of their time on Instagram in Reels, up from 37% the previous year.[3]Meta Platforms, Inc., "Q3 2025 Earnings Call Transcript" This momentum has been reinforced by heavier AI investment behind the scenes, with video generation tools reaching a combined revenue run-rate of USD 10 billion in Q4 2025, growing nearly three times faster than the overall ads business alongside a scaled-up ads ranking model that drove measurable lifts in ad clicks and conversions across Facebook and Instagram, showing how quickly monetization has followed user engagement into short-form environments.

The format mix remains broader than video alone, and that balance is important for the social media advertising market because advertisers still use image and carousel ads where creative cost, product depth, or sequential storytelling matters more than motion. Image ads remain relevant for efficient upper-funnel reach, especially for brands that do not have the resources to produce large volumes of video assets. Carousel units continue to support retail and financial services campaigns where multiple products, steps, or features need to be presented in one placement. Sponsored content and native formats also keep a clear role because they fit more naturally into feed environments and are often less exposed to AD avoidance behavior than interruptive units. As AI-based creative tools reduce production barriers, format choice in the social media advertising market is likely to depend less on budget constraints and more on the role each format plays across discovery, education, and conversion.

By Platform: Social Networks Anchor Share as Video-Sharing Accelerates

Social networking platforms held 46.32% of the social media advertising market share in 2025, which made them the largest platform group by revenue. Their lead comes from a combination of very large user bases, mature targeting tools, deep advertiser familiarity, and broad adoption across both brand and performance budgets. Meta Platforms generated USD 196.2 billion in full-year 2025 advertising revenue, and the company reported 12% growth in ad impressions along with a 9% rise in average price per ad, which confirms how effectively major social networks are monetizing scales through ranking and optimization improvements. These conditions make social networks a dependable foundation for the social media advertising market because they give advertisers stable reach, strong data depth, and automated buying tools in one system. They also remain central for categories that need a mix of awareness, retargeting, and commerce-linked placements rather than a single campaign objective.

Video-sharing platforms are forecast to expand at a 16.34% CAGR through 2031, which makes them the fastest-growing platform type in the social media advertising market. Their growth reflects the continued movement of budgets toward short-form video environments where content discovery is fast, creative refresh cycles are constant, and performance feedback arrives quickly. Messaging platforms are also becoming more commercially active, although monetization remains less mature than in networks and video-sharing services. Professional networking platforms keep a distinct role because they support business targeting, higher-value lead generation, and category-specific education that is harder to deliver on more entertainment-led surfaces. The social media advertising market is therefore developing along two tracks, with broad networks defending scale and data depth, while video-sharing platforms gain share through faster inventory growth and stronger fit with current content behavior.

By End User: Retail Anchors Spend as Healthcare Emerges

Retail led spending with a 23.77% share in 2025, which kept it as the largest end-user group in the social media advertising market. That position reflects retail's strong use of shoppable formats, direct-to-consumer acquisition campaigns, and platform-native buying journeys that shorten the path from discovery to checkout. The social media advertising industry has become especially valuable for retailers because campaign optimization can be tied more closely to product-level outcomes and seasonal conversion windows. Retail demand is also supported by the way platform tools now blend catalog data, automation, and creative variation into one lower-funnel workflow. This makes social placements harder to replace with broader digital channels that offer reach but weaker in-platform commerce continuity.

Healthcare is expected to record the fastest 2026-2031 CAGR at 15.78%, which shows how quickly the vertical is redirecting spending toward targeted digital channels. The shift is being helped by the declining role of linear television and the growing appeal of formats that can deliver education, precision targeting, and measurable engagement in one campaign structure. The social media advertising market also benefits from diversification across automotive, financial services, entertainment and media, education, and other verticals, which reduces reliance on any single demand pool. Financial services advertisers are using more professional networking and video-based educational content, while entertainment and media brands are aligning social campaigns more closely with streaming releases and subscription sign-up goals. Education remains smaller in terms of value, but the segment is growing in markets where social platforms function as the primary discovery layer for online learning offers, which broadens the long-term advertiser base of the social media advertising market.

Geography Analysis

North America maintained a 40.45% share of the social media advertising market in 2025, and that lead was supported by high digital advertising penetration, strong advertiser sophistication, and the home-market advantage of several dominant platforms. The region generates the highest social ad revenue per capita, which reflects both consumer digital maturity and the heavy use of performance-oriented buying models. The United States remains the world's largest social media advertising market. U.S. social network advertising spending is projected to exceed USD 121 billion in 2026, reflecting continued adoption of automated advertising tools that lower the barrier for small and medium-sized businesses to run campaigns at scale. Meta reported USD 42.3 billion in revenue in Q1 2026, highlighting the continued strength of large-scale digital advertising demand.

Europe is the second-largest regional market for social media advertising. The region's advertising environment is shaped by stringent privacy and digital regulations, making consent-based targeting and first-party data strategies increasingly important across major markets such as Germany, France, and the United Kingdom. Despite stricter regulatory requirements, the UK continues to rank among Europe's strongest social advertising markets, demonstrating sustained advertiser investment.

Asia-Pacific is the fastest-growing region for social media advertising. In Japan, social media advertising expenditure reached approximately JPY 1.31 trillion (USD 8.7 billion) in 2025, with video advertising accounting for 39.2% of social advertising spending, reflecting the continued shift toward video-first formats. India is also experiencing rapid expansion, driven by short-form video, creator-led marketing, and increasing digital advertising adoption. China remains the region's largest market, supported by major domestic platforms including Douyin, WeChat, Weibo, and Kuaishou.

South America, the Middle East, and Africa currently account for a smaller share of global social media advertising expenditure but continue to record steady growth. Expanding smartphone penetration, improving mobile internet affordability, and rising digital engagement are supporting increased advertiser investment across markets such as Brazil, Saudi Arabia, the United Arab Emirates, Nigeria, South Africa, and Egypt.

Competitive Landscape

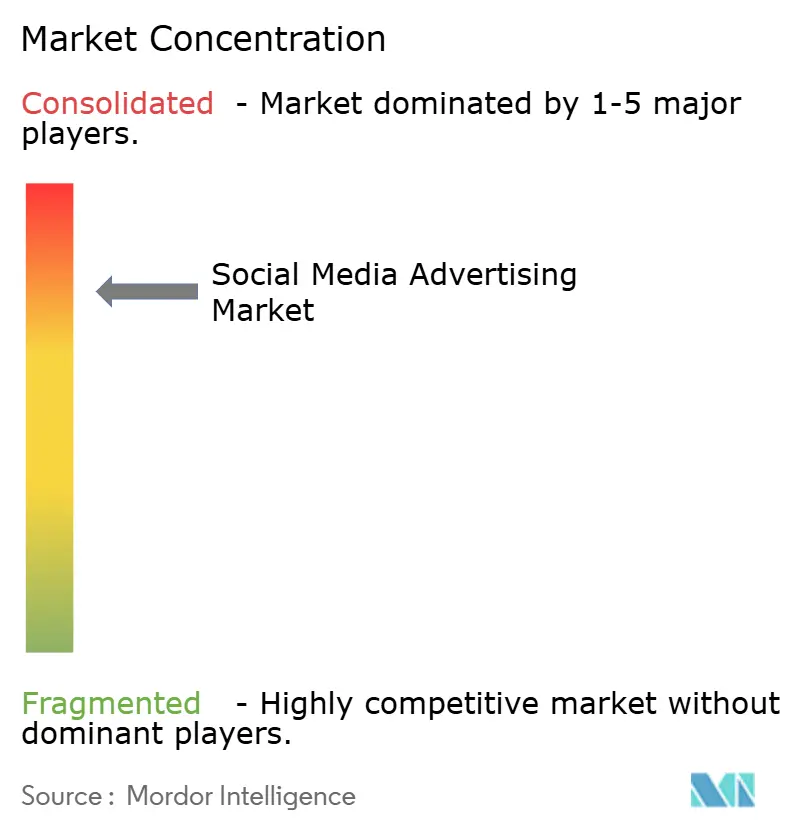

The social media advertising market remains highly concentrated at the platform level, even though the broader ecosystem of tools, agencies, and service providers is much more fragmented. Facebook, Instagram, Douyin, YouTube, TikTok, and WeChat collectively generated approximately 90% of global social media advertising revenue in 2025, which created high barriers for smaller platforms that want to scale monetization. Meta's Family of Apps alone accounted for roughly 54% of the social media advertising market share in 2025, which shows how much influence a small group of platform owners still holds over global advertiser access and inventory economics. This structure makes scale, first-party data, and cross-format reach more important than niche audience growth for the largest participants. It also means most competitive moves now center on improving automation, measurement, commerce links, and creator supply rather than trying to invent entirely new ad units.

Meta, TikTok, Pinterest, and Snap are all competing for the same performance budgets through increasingly similar optimization systems, which is narrowing product differences at the campaign execution level. Meta's 2025 results showed that the company could raise both impression volume and pricing at the same time, which points to strong execution in AI-based ranking and monetization. Alphabet reported that YouTube passed USD 60 billion in combined advertising and subscription revenue, which reinforces the financial strength of video-led ecosystems in the social media advertising market. Pinterest used product discovery and shopping intent to support user and revenue growth, which shows that strong commercial context can still create a defendable position beside larger platforms. These examples show that the social media advertising market is no longer being shaped only by audience size, and it is also being shaped by how effectively a platform turns intent, automation, and merchant connections into measurable advertiser returns.

Another important area of competition is measurement credibility, because advertisers are asking for clearer proof that social spending produces incremental results rather than only platform-attributed conversions. That is why independent verification and brand safety controls are becoming more strategic inside the social media advertising market. Integral Ad Science launched independent brand safety and suitability measurements for Meta Threads in October 2025, which reflected the growing need for third-party controls as newer social surfaces try to scale advertiser confidence.[4]Integral Ad Science, “IAS Launches First AI-Driven, Independent Brand Safety and Suitability Measurement for Meta Threads,” Integral Ad Science, integralads.com The social media advertising market is therefore moving toward a model where concentration still favors the largest platforms, but competitive advantage within that group increasingly depends on transparent reporting, reliable moderation, creator ecosystem depth, and commerce-ready infrastructure.

Social Media Advertising Industry Leaders

-

Meta Platforms, Inc.

-

Alphabet Inc.

-

Snap Inc.

-

Pinterest, Inc.

-

Tencent Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Yahoo DSP launched its Agent Network, an open AI framework that allows advertisers to integrate third-party AI agents directly into campaign workflows. The system supports use cases across targeting, activation, creative development, and measurement while maintaining governance and transparency controls. The launch reflects Yahoo’s broader AI strategy to build a more interoperable advertising ecosystem, enabling brands to combine native and external AI tools for improved campaign efficiency and flexibility.

- December 2025: Meta expanded its Partnership Ads offering by introducing AI-powered tools that enabled brands to discover, evaluate, and scale creator content more efficiently across Facebook and Instagram. The updates included enhanced creator discovery, performance insights, a new Partnership Ads API, and streamlined content permission workflows, allowing advertisers to convert organic creator and user-generated content into paid campaigns at scale.

- October 2025: Integral Ad Science (IAS) launched independent brand safety and suitability measurement for Meta Threads, extending third-party, AI-driven content verification to the platform for the first time and enabling advertisers to manage ad adjacency risk at scale.

- September 2025: Pinterest introduced Top of Search Ads and a suite of new advertising tools to strengthen visual shopping and improve advertiser performance. The launch included Top of Search Ads, which place brands within the first ten search results and Related Pins, alongside enhancements to Pinterest Performance+, expanded Local Inventory Ads, and Media Network Connect. These innovations were designed to help advertisers capture high-intent shoppers, improve campaign automation, and deliver stronger measurement and conversion outcomes.

Global Social Media Advertising Market Report Scope

The Social Media Advertising Market Report is Segmented by Ad Format (Video Ads, Image Ads, Carousel Ads, Sponsored Content, and More), Platform (Social Networking Platform, Video-Sharing Platforms, Messaging Platforms, Professional Networking Platforms, and More), End User (Retail, Automotive, Healthcare, Financial Services, Entertainment and Media, Education, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Video Ads |

| Image Ads |

| Carousel Ads |

| Sponsored Content |

| Other Ad Formats |

| Social Networking Platforms |

| Video-Sharing Platforms |

| Messaging Platforms |

| Professional Networking Platforms |

| Other Platforms |

| Retail |

| Automotive |

| Healthcare |

| Financial Services |

| Entertainment and Media |

| Education |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Ad Format | Video Ads | |

| Image Ads | ||

| Carousel Ads | ||

| Sponsored Content | ||

| Other Ad Formats | ||

| By Platform | Social Networking Platforms | |

| Video-Sharing Platforms | ||

| Messaging Platforms | ||

| Professional Networking Platforms | ||

| Other Platforms | ||

| By End User | Retail | |

| Automotive | ||

| Healthcare | ||

| Financial Services | ||

| Entertainment and Media | ||

| Education | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the social media advertising market?

The social media advertising market was valued at USD 202.93 billion in 2025, is estimated at USD 227.88 billion in 2026, and is forecast to reach USD 422.58 billion by 2031 at a 13.15% CAGR.

Which ad format leads revenue generation across social platforms?

Video ads lead the category with 39.11% share in 2025, and they are also projected to grow the fastest at a 14.52% CAGR through 2031.

Which platform type is expanding the fastest through 2031?

Video-sharing platforms are expected to record the highest growth rate at 16.34% through 2031, although social networking platforms remained the largest with 46.32% share in 2025.

Which end-user group spends the most on social platforms today?

Retail remained the largest end-user segment with 23.77% share in 2025 because brands are increasing spending on shoppable formats and direct-to-consumer acquisition campaigns.

Which region is driving the next phase of growth?

Asia-Pacific is the fastest-growing region with a projected 15.22% CAGR, supported by expanding digital ad demand in India, Japan, China, South Korea, and Southeast Asia.

Why are the biggest platforms still hard to displace?

The leading platforms combine scale, first-party data, creator ecosystems, commerce tools, and automation, and 6 major apps together generated approximately 90% of global revenue in 2025.

Page last updated on: