SMBs Cloud ERP Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

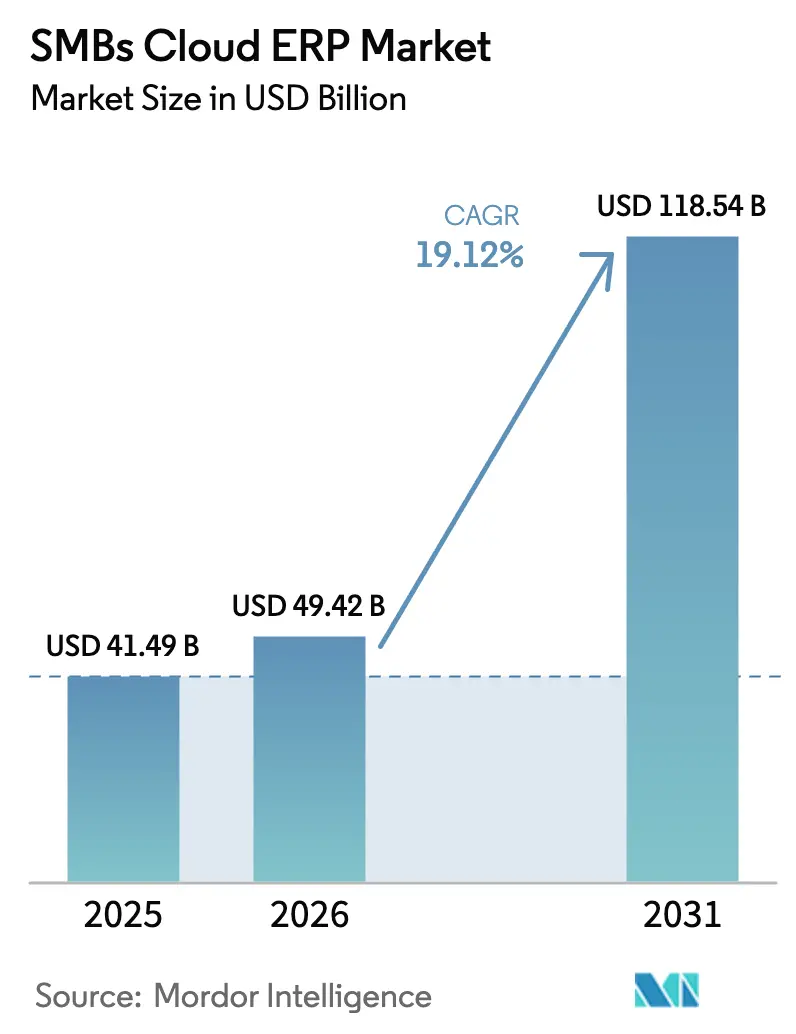

| Market Size (2026) | USD 49.42 Billion |

| Market Size (2031) | USD 118.54 Billion |

| Growth Rate (2026 - 2031) | 19.12% CAGR |

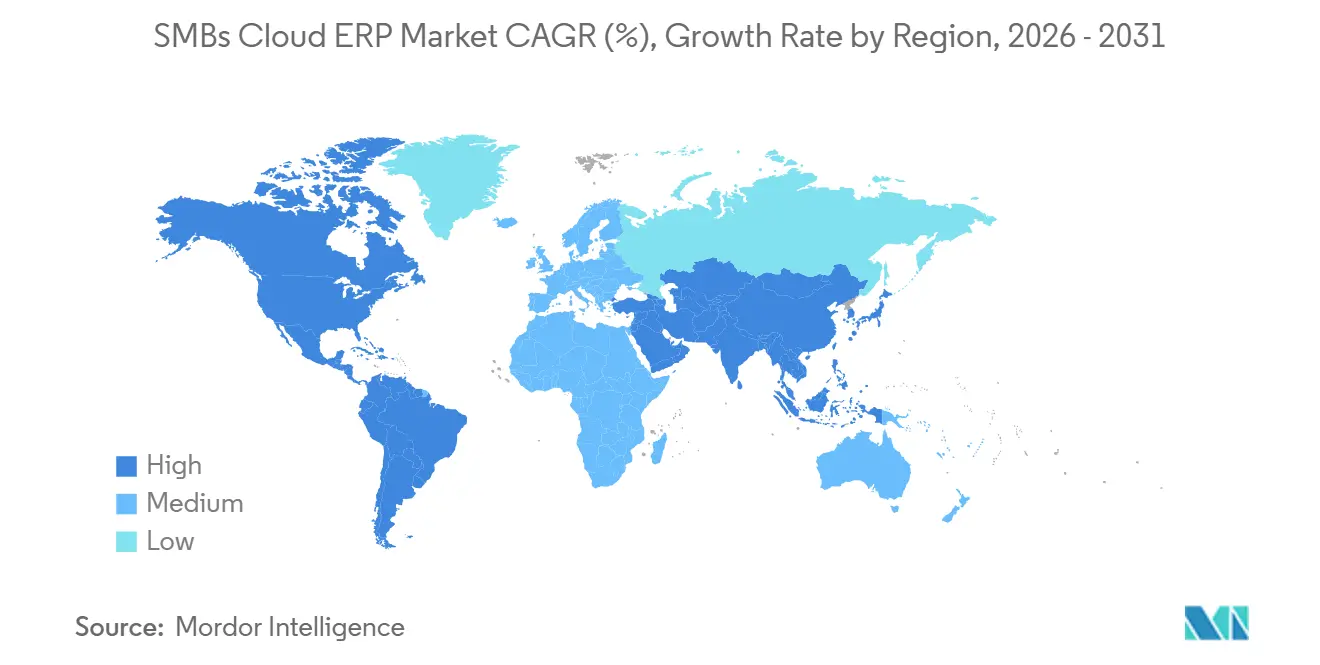

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SMBs Cloud ERP Market Analysis by Mordor Intelligence

The SMBs Cloud Enterprise Resource Planning market size was valued at USD 41.49 billion in 2025 and estimated to grow from USD 49.42 billion in 2026 to reach USD 118.54 billion by 2031, at a CAGR of 19.12% during the forecast period (2026-2031). Subscription pricing, real-time compliance mandates, and embedded artificial intelligence are converging to remove historic budget and skills barriers that slowed adoption among smaller businesses. Public cloud deployments still dominate the market, yet hybrid deployments are accelerating as sovereign-data rules in China, India, and the Middle East push workloads toward localized infrastructure. Vertically tailored modules for healthcare, manufacturing, and retail continue to gain traction because they shorten implementation timelines and embed regulatory templates out of the box. Intense vendor competition around AI-agent orchestration and low-code integration is further compressing time-to-value while creating new monetization pathways tied to consumption expansion.

Key Report Takeaways

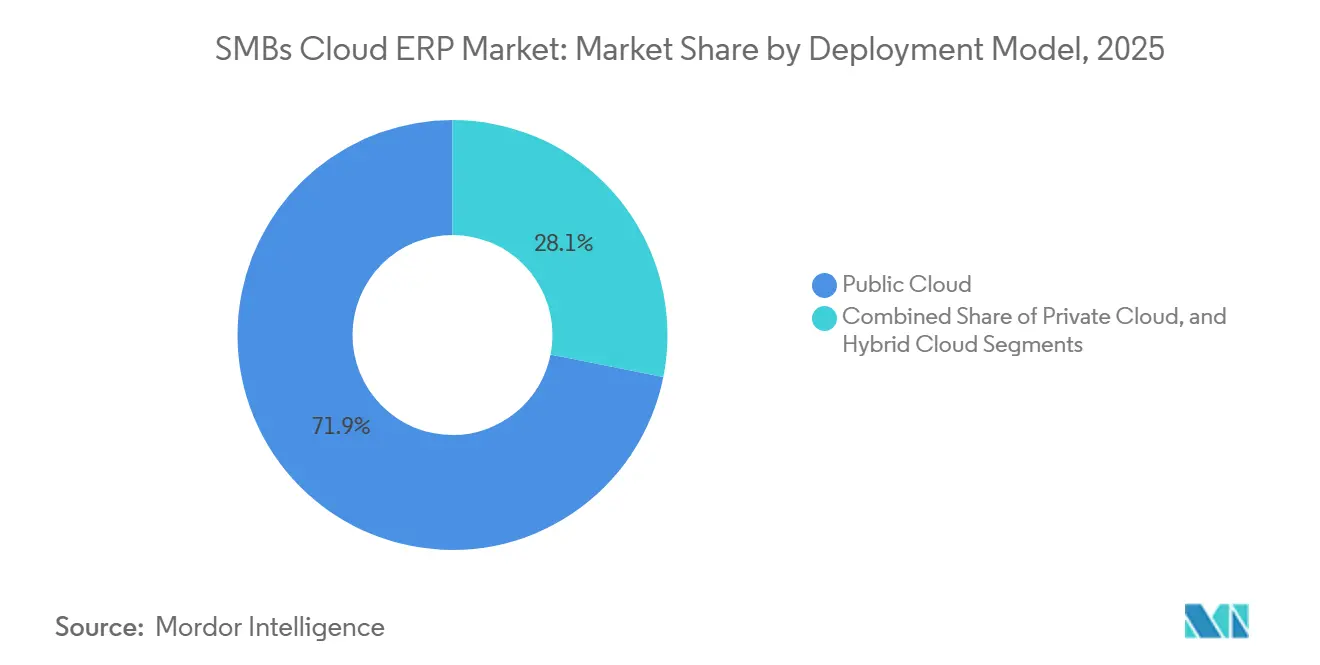

- By deployment model, public cloud held 71.87% of the SMBs Cloud Enterprise Resource Planning market share in 2025, whereas hybrid cloud is projected to expand at a 15.87% CAGR from 2026 to 2031.

- By module, financial management led with a 31.53% share of the SMBs Cloud ERP market in 2025, while human capital management is forecast to grow at a 15.23% CAGR through 2031.

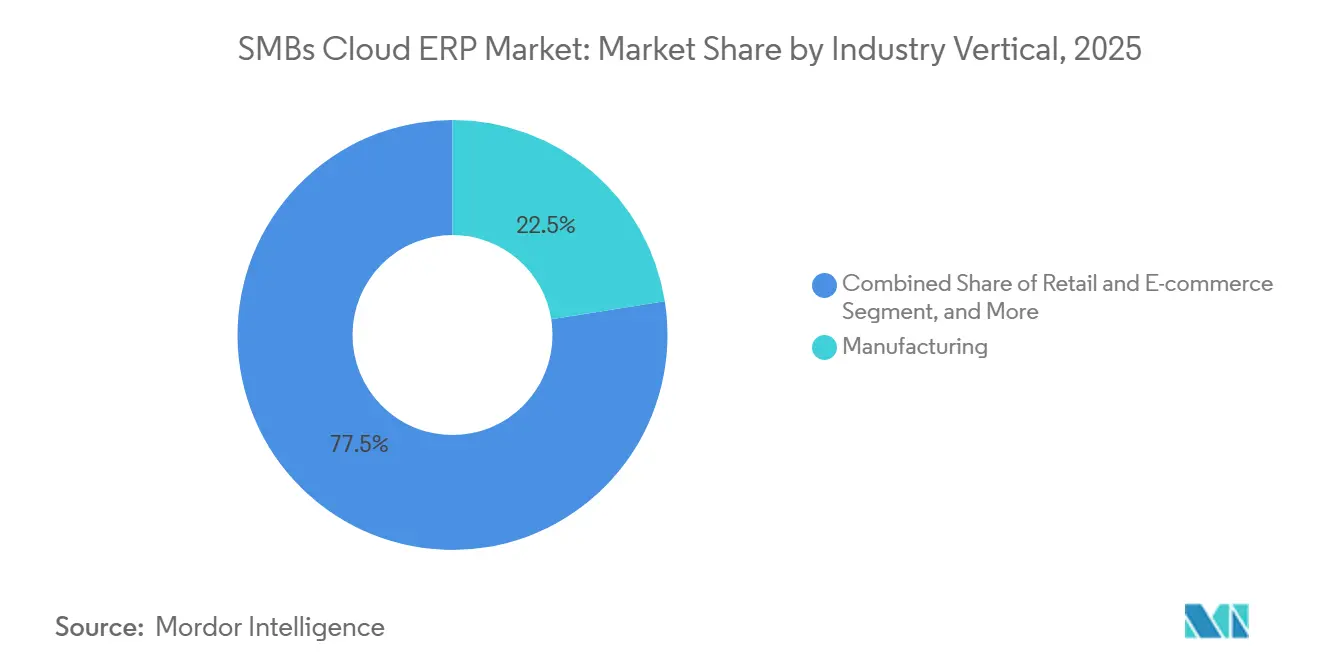

- By industry vertical, manufacturing accounted for 22.49% revenue share in 2025; healthcare is expected to record the fastest growth at a 17.32% CAGR to 2031.

- By geography, North America captured 36.12% share in 2025, but Asia-Pacific is set to be the fastest-growing region at a 15.19% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SMBs Cloud ERP Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Public Cloud Adoption Among SMBs | +5.2% | Global, strongest in North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Accelerating Digital Transformation Post-COVID-19 | +4.8% | Global, acute in retail, professional services, healthcare | Short term (≤ 2 years) |

| Growing Affordability of Subscription Pricing Models | +3.9% | Global, bigger lift in emerging markets | Medium term (2-4 years) |

| Government Incentives for SME Digitization | +3.1% | Asia-Pacific, Middle East, Europe | Long term (≥ 4 years) |

| Emergence of Vertical-Specific Cloud ERP | +2.7% | North America and Europe manufacturing, healthcare; Asia-Pacific retail | Medium term (2-4 years) |

| Integration Capabilities with Low-Code Platforms | +2.4% | Global, early adopters in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Public Cloud Adoption Among SMBs

Low-touch provisioning and pay-as-you-grow elasticity have pushed 83% of mid-sized businesses and 61% of small businesses to migrate the majority of workloads to public cloud. Monthly release cycles, automated patching, and near-instant scaling deliver operational agility that on-premise ERP cannot match. Hyperscalers are responding with new regional data centers that satisfy data-residency mandates. Oracle and SAP announced plans to expand their data centers in Asia by 2025, aiming to meet sovereign-cloud requirements in China, India, and the Middle East, thereby reducing latency and easing compliance friction.[1]Industry Today Editorial Team, “Asia Pacific ERP Software Market Expected to Reach USD 77.04 Billion by 2035,” industrytoday.co.uk As availability zones proliferate, the SMBs cloud enterprise resource planning market benefits from a feedback loop in which local compliance confidence accelerates additional workload migration. Vendor roadmaps now center on sovereign cloud blueprints and zero-trust security features, making the public cloud the default choice for new deployments.

Accelerating Digital Transformation Post-COVID-19

Lockdowns exposed the fragility of legacy accounting and inventory systems that lacked APIs for ecommerce and mobile access. SMB leaders continue to treat digital workflows as standard operating procedure rather than contingency planning. Cloud ERP vendors have bundled ecommerce connectors, embedded analytics, and mobile apps into base tiers, removing the integration cost that once deterred smaller buyers. CRM and supply-chain modules that previously required bolt-on purchases now ship standard, reflecting the expectation of end-to-end visibility from quote to cash. These shifts sustain premium growth in the market even as pandemic shocks recede.

Growing Affordability of Subscription Pricing Models

Per-user fees starting at USD 31 per month let firms pilot core finance functions without large capital expenditure. As revenue scales, customers add HCM, CRM, and manufacturing modules, aligning vendor success with ongoing customer value. SMEs report roughly 30% reductions in first-year IT costs after eliminating servers and manual reconciliations. Public grant programs such as Malaysia’s Budget 2026 and Canada’s CDAP further reduce effective costs, bringing cloud ERP within reach of microenterprises. This economic realignment underpins sustained double-digit expansion for the SMBs Cloud ERP market.

Government Incentives for SME Digitization

Digital India, Made in China 2025, and Saudi Vision 2030 funnel grants, tax relief, and mandatory e-invoicing rules toward cloud-ready accounting systems. Slovenia and the United Kingdom have likewise earmarked multimillion-dollar funds for SME cloud adoption. Mandatory real-time tax reporting effectively obliges SMBs to modernize finance systems, turning regulatory compliance into a catalyst rather than a burden. Vendors now craft go-to-market playbooks around co-funded migrations and government partnerships, expanding the total addressable market for the SMBs cloud enterprise resource planning market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited IT Skills Within Small Businesses | -3.8% | Global, acute in rural Asia-Pacific, South America, Africa | Medium term (2-4 years) |

| Data Security and Compliance Concerns | -2.9% | Global, strictest in Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Legacy System Integration Complexities | -2.1% | North America and Europe manufacturing, retail, emerging markets | Medium term (2-4 years) |

| Rising Cloud Computing Cost Inflation | -1.7% | Global, heavier impact on price-sensitive emerging regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited IT Skills Within Small Businesses

Many technology leaders struggle to recruit cloud-ERP specialists, while only 35% of employees receive AI-related upskilling. Rural and tier-2 cities face the steepest shortages, forcing SMBs to rely on managed services that add cost and dilute customization freedom. Vendors have introduced guided setup wizards and no-code extensions, yet these tools cannot fully replace domain expertise. This shortage of skilled professionals is further exacerbated by the rapid pace of technological advancements, which outpaces the availability of trained personnel. The resulting skills gap slows rollouts and dampens ROI, placing a structural drag on the SMBs' cloud enterprise resource planning market.

Data Security and Compliance Concerns

83% of organizations experienced a cloud security incident within the past 18 months, with average breach costs nearing USD 4.88 million. Healthcare sector penalties exceed USD 9.7 million per incident, driving increased scrutiny of encryption protocols, privileged access controls, and incident response strategies. SMBs frequently lack the resources to thoroughly validate vendor certifications or perform penetration testing, heightening perceived risks. This gap in preparedness often leads to downstream fines and reputational damage for customers when audits fail, rather than impacting the providers. Consequently, adoption in regulated industries remains slow, further constraining growth opportunities in the SMBs' cloud enterprise resource planning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Balance Sovereignty and Agility

Public cloud retained 71.87% of the market share in 2025 as smaller firms gravitated toward instant scalability and minimal maintenance. Hybrid architectures, however, are projected to deliver a 15.87% CAGR over 2026-2031, reflecting regulatory pressures that compel local data storage while preserving the analytic flexibility of the public cloud. Sovereign-cloud offerings and unified management consoles let finance and HR workloads remain on private instances, with AI-driven forecasting and dev-test environments burst to public infrastructure on demand. SAP has teamed up with Syngenta to roll out its SAP Cloud ERP Private solutions. These private editions not only ensure dedicated tenancy and customer-controlled encryption keys but also seamlessly integrate with SAP's expansive cloud ecosystem.[2]SAP Newsroom, “SAP and Syngenta Announce Partnership to Scale AI-Assisted Agriculture,” news.sap.com

Second-generation hybrid deployments also hedge against network instability in emerging markets, where consistent and reliable internet connectivity remains a challenge. These deployments use local caching to ensure mission-critical transactions continue uninterrupted during network outages. Once connectivity is restored, the system reconciles the locally cached data with cloud-based ledgers, ensuring data integrity and operational continuity. This level of resilience is enabling the SMBs cloud enterprise resource planning market to expand into regions previously constrained by unreliable broadband infrastructure.

By Module: HCM Surges as Workforce Analytics Rise in Priority

Financial management dominated the market, accounting for 31.53% of revenue in 2025, but human capital management is set to expand at a 15.23% CAGR through 2031. Compliance-driven payroll, skills-gap dashboards, and predictive retention analytics now rank alongside finance automation as board-level imperatives. Inventory and order management remain core among retailers and manufacturers, underpinning omnichannel fulfillment and lot traceability. Supply chain modules with AI forecasting have trimmed stockouts and boosted on-time delivery, accelerating cross-module upsell momentum.

Adoption sequencing typically follows a well-established land-and-expand curve. Companies usually begin by implementing finance systems as the foundational layer. Once finance systems are in place, they proceed to integrate inventory management solutions. Subsequently, they incorporate Human Capital Management (HCM) systems, particularly when the workforce size surpasses compliance thresholds, necessitating more robust employee management tools. Customer Relationship Management (CRM), which was traditionally purchased as a standalone solution, is now being integrated earlier in the technology stack. This shift is driven by the need for unified customer data, which significantly enhances quote-to-cash processes and improves operational efficiency. Vendors capable of delivering cross-module analytics with minimal reliance on extensive consulting services are contributing to increased market stickiness, as their solutions offer greater value and ease of adoption.

By Industry Vertical: Healthcare Emerges as the Growth Pacesetter

Manufacturing accounted for 22.49% of 2025 revenue, aided by IoT integration and predictive maintenance capabilities that reduce unplanned downtime. Yet healthcare is projected to pace the market at 17.32% CAGR as HIPAA updates mandate multi-factor authentication and 72-hour recovery objectives. Cloud ERP platforms that embed HL7 FHIR interoperability and AES-256 encryption are becoming the default choice for clinics seeking to unify clinical, financial, and supply-chain data.

Retail and ecommerce adoption is driven by the increasing complexity of managing omnichannel operations, with 89% of merchants now requiring native marketplace connectors to streamline their processes. In the construction and professional services sectors, businesses are increasingly adopting project accounting and certified payroll systems to safeguard their already narrow profit margins. The distinct compliance requirements across verticals further underscore the value of purpose-built templates, which not only deliver tailored solutions but also create a competitive advantage for vendors. This approach enhances customer retention and increases total contract value, thereby contributing to market growth.

Geography Analysis

North America retained 36.12% revenue share in 2025, buoyed by mature SaaS mindsets, dense partner ecosystems, and large public-sector projects. Continued investments, such as Workday’s CAD 1 billion (USD 0.71 billion approximately) expansion, will deepen payroll and security localization, but overall growth is moderating as penetration approaches saturation.[3]ERP Today, “Workday to Invest CAD $1 Billion in Canada,” erp.today Upsell opportunities around AI-agent modules and industry add-ons now outpace net-new logos in driving North American revenue for the SMBs cloud ERP market.

Asia-Pacific is projected to be the fastest-growing region, with a 15.19% CAGR. National digitization targets, such as Digital India and Saudi Arabia’s Vision 2030, are driving growth by combining tax incentives with e-invoicing mandates that effectively require businesses to adopt cloud-ready finance systems. Hyperscalers, including major cloud service providers, are continuing to localize compute regions, which helps reduce latency and ensures compliance with data-sovereignty statutes that previously hindered adoption. Domestic vendors, such as Zoho, as well as global incumbents, are establishing R&D hubs and introducing local-language packs. These efforts are significantly compressing deployment timelines for regional SMBs, thereby fueling market expansion and adoption of cloud ERP solutions.

Europe is experiencing steady growth, supported by GDPR-compliant architectures and EU funding programs designed to offset the adoption costs for smaller firms. Initiatives such as Slovenia’s digitization fund and the UK’s SME Digital Adoption Taskforce exemplify a coordinated policy push to encourage digital transformation among SMBs. Meanwhile, the Middle East and Africa are benefiting from regulatory advancements, such as ZATCA Phase 2 real-time invoicing in Saudi Arabia, along with similar rules emerging across the Gulf region. These developments are prompting accelerated migrations to cloud ERP systems. South America, while trailing in total market value, is gaining momentum as countries like Brazil and Argentina implement overhauls to their VAT frameworks. These changes favor automated tax-filing processes enabled by cloud platforms, further driving adoption in the region.

Competitive Landscape

The SMBs Cloud Enterprise Resource Planning market is moderately fragmented: the top 10 vendors accounted for roughly 33% of global revenue in 2025, leaving significant opportunities for regional specialists and open-source challengers to carve out niches. SAP leads the market with a 6.2% share, followed by Oracle, Intuit, Microsoft, and Constellation Software. However, no single player has achieved double-digit dominance, highlighting the competitive and dynamic nature of this market. Established players are equipping their customer bases with advanced cloud-migration toolkits, AI copilots, and data-fabric connectors to effectively counter the agility and innovation of emerging competitors.

Cloud-native providers leverage consumption pricing, rapid release cadences, and mobile-first UX to win greenfield deals. SAP’s partnership with Databricks and Microsoft Azure has elevated data-fabric integration, while Workday’s Pipedream acquisition brings 3,000-plus connectors that transform its ERP from a system of record into a system of coordinated action. IFS’s 2026 Softeon acquisition deepens end-to-end supply chain intelligence across asset-intensive verticals, signaling a shift toward composable suites.[4]ERP Today, “IFS Expands Industrial AI Strategy with Softeon Acquisition,” erpnews.com

Private equity capital continues to play a pivotal role in shaping the SMBs cloud enterprise resource planning market landscape. For instance, Vista Equity’s acquisition of Acumatica and Elliott Management’s USD 2 billion investment in Workday underscore investor confidence in the long-term growth potential and profitability of this market. Emerging opportunities in the sector include sovereign-cloud editions tailored for regulated industries, AI-agent marketplaces designed to monetize orchestrated workflows, and micro-SaaS vertical modules that address specific compliance challenges. Vendors that focus on refining vertical blueprints and integrating autonomous agents into their offerings are well-positioned to increase their wallet share while maintaining healthy profit margins.

SMBs Cloud ERP Industry Leaders

Oracle Corporation

SAP SE

Sage Group Plc

Microsoft Corporation

Infor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: IFS finalized its Softeon acquisition, rebranding the platform as IFS Softeon and integrating warehouse robotics orchestration across 30 countries.

- January 2026: Workday committed approximately USD 740 million over five years to expand AI engineering and Protected B-compliant payroll capabilities in Canada.

- January 2026: SAP and Syngenta entered a multiyear partnership to deploy SAP cloud enterprise resource planning private solutions, embed Joule AI copilots across manufacturing and grower-facing operations, and grow.

- January 2026: Deloitte launched INTEGRATE, a preconfigured suite of industry solutions for SAP cloud ERP, promising go-lives in as little as 8 weeks.

Global SMBs Cloud ERP Market Report Scope

The SMBs Cloud ERP Market is the global market for cloud-based Enterprise Resource Planning (ERP) solutions for small and medium-sized businesses (SMBs). These solutions are delivered through cloud infrastructure and enable organizations to integrate and manage core business processes such as finance, operations, human resources, sales, and supply chain through a centralized digital platform.

The SMBs Cloud ERP Market Report is Segmented by Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Module (Financial Management, Inventory and Order Management, Human Capital Management, Customer Relationship Management, Supply Chain Management, and Other Modules), Industry Vertical (Manufacturing, Retail and E-commerce, Professional Services, Healthcare, Construction, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Financial Management |

| Inventory and Order Management |

| Human Capital Management |

| Customer Relationship Management |

| Supply Chain Management |

| Other Modules |

| Manufacturing |

| Retail and E-commerce |

| Professional Services |

| Healthcare |

| Construction |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Module | Financial Management | ||

| Inventory and Order Management | |||

| Human Capital Management | |||

| Customer Relationship Management | |||

| Supply Chain Management | |||

| Other Modules | |||

| By Industry Vertical | Manufacturing | ||

| Retail and E-commerce | |||

| Professional Services | |||

| Healthcare | |||

| Construction | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the SMBs Cloud Enterprise Resource Planning market be by 2031?

It is projected to reach USD 118.54 billion by 2031, rising from USD 49.42 billion in 2026.

Which deployment model is growing the fastest?

Hybrid cloud is forecast to post a 15.87% CAGR between 2026 and 2031 as firms balance data sovereignty and flexibility.

What is the most rapidly expanding module?

Human capital management modules are expected to grow at 15.23% CAGR through 2031 because of rising workforce-analytics and compliance needs.

Which industry vertical offers the highest growth outlook?

Healthcare is set to register a 17.32% CAGR to 2031, driven by stringent interoperability and security mandates.

Why are micro enterprises accelerating adoption?

Consumption-based licensing, mobile-first interfaces, and government incentives reduce upfront costs, enabling an 18.43% CAGR in micro-enterprise deployments.

What primary risk could slow market growth?

A persistent shortage of cloud-ERP skills, cited by 95% of IT leaders, could delay implementations and erode projected ROI.

Page last updated on: