Smart Residential Kitchen Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.36 Billion |

| Market Size (2031) | USD 28.77 Billion |

| Growth Rate (2026 - 2031) | 11.96% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Residential Kitchen Appliances Market Analysis by Mordor Intelligence

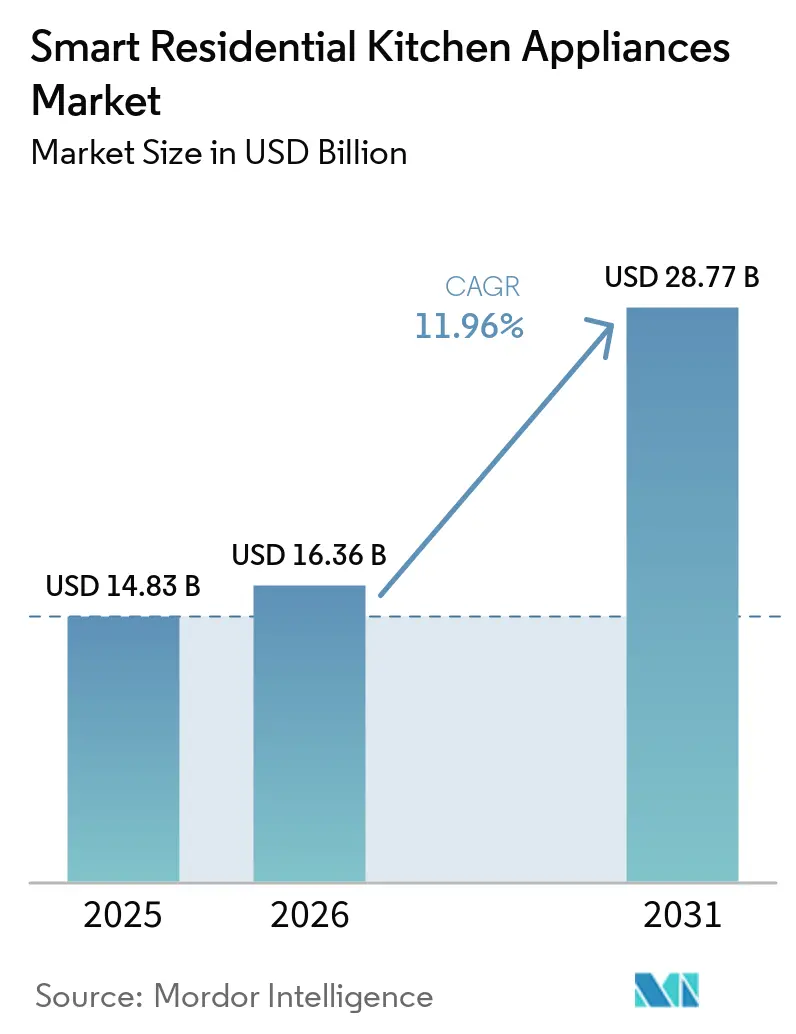

The smart residential kitchen appliances market size was valued at USD 14.83 billion in 2025 and estimated to grow from USD 16.36 billion in 2026 to reach USD 28.77 billion by 2031, at a CAGR of 11.96% during the forecast period (2026-2031). The smart residential kitchen appliances market is entering a scale phase as AI-powered, IoT, and app-controlled kitchen appliances move from premium to mid-range price points. At the same time, builders standardize connected suites in new homes to align with buyer expectations and permitting timelines. Policy shifts now emphasize energy-efficient design and low-power connectivity, accelerating redesign cycles and pushing vendors to adopt lower-standby architectures across their portfolios in the smart residential kitchen appliances market [1]Staff Editorial, “Standby and Off Mode Requirements for Networked Devices,” European Commission, ec.europa.eu. Voice-controlled and Alexa-enabled kitchen appliances transition from add-on features to core experience layers, and early forms of smart kitchen automation coordinate multi-appliance tasks to achieve more consistent outcomes. Brand playbooks increasingly blend hardware upgrades with software updates, subscriptions, and remote-controlled appliances to support retention and post-sale value as domestic production investments raise resilience in the smart residential kitchen appliances market.

Key Report Takeaways

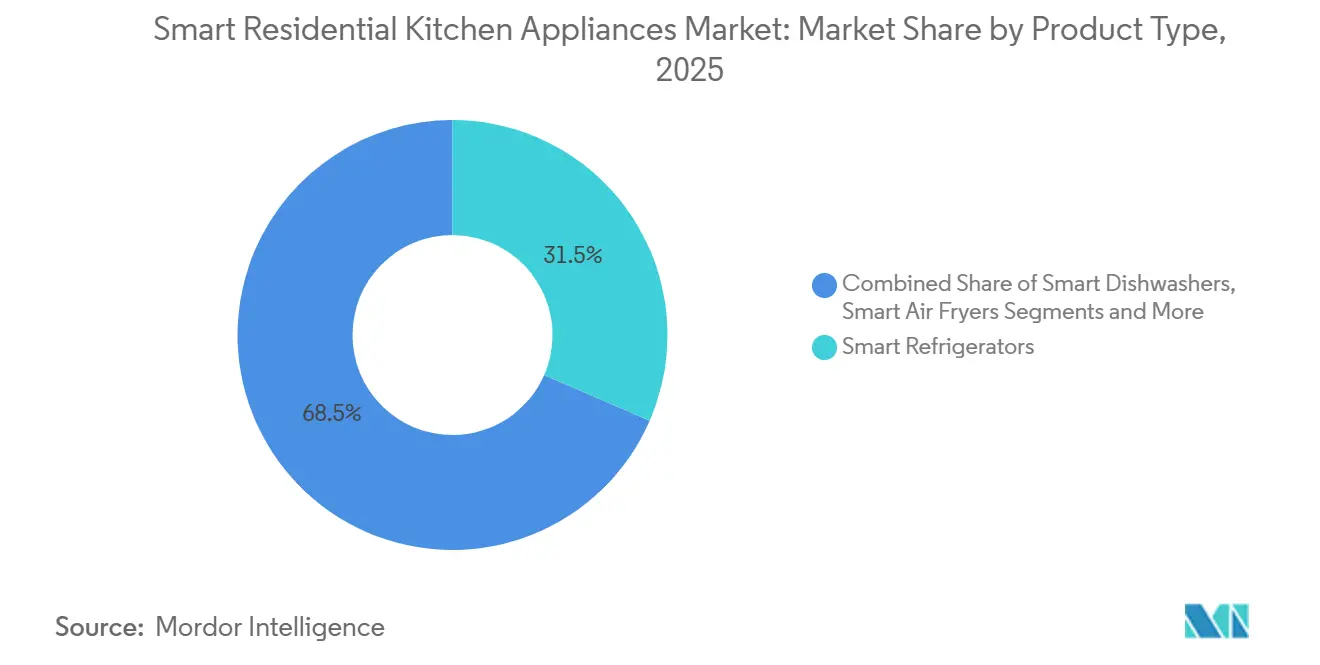

- By product type, smart refrigerators led with 31.53% revenue share in 2025 in the smart residential kitchen appliances market; smart cooktops and hobs are projected to expand at a 12.45% CAGR through 2031.

- By installation type, freestanding models accounted for 65.62% of revenue share in 2025 in the smart residential kitchen appliances market, and built-ins are projected to grow at a 12.53% CAGR through 2031.

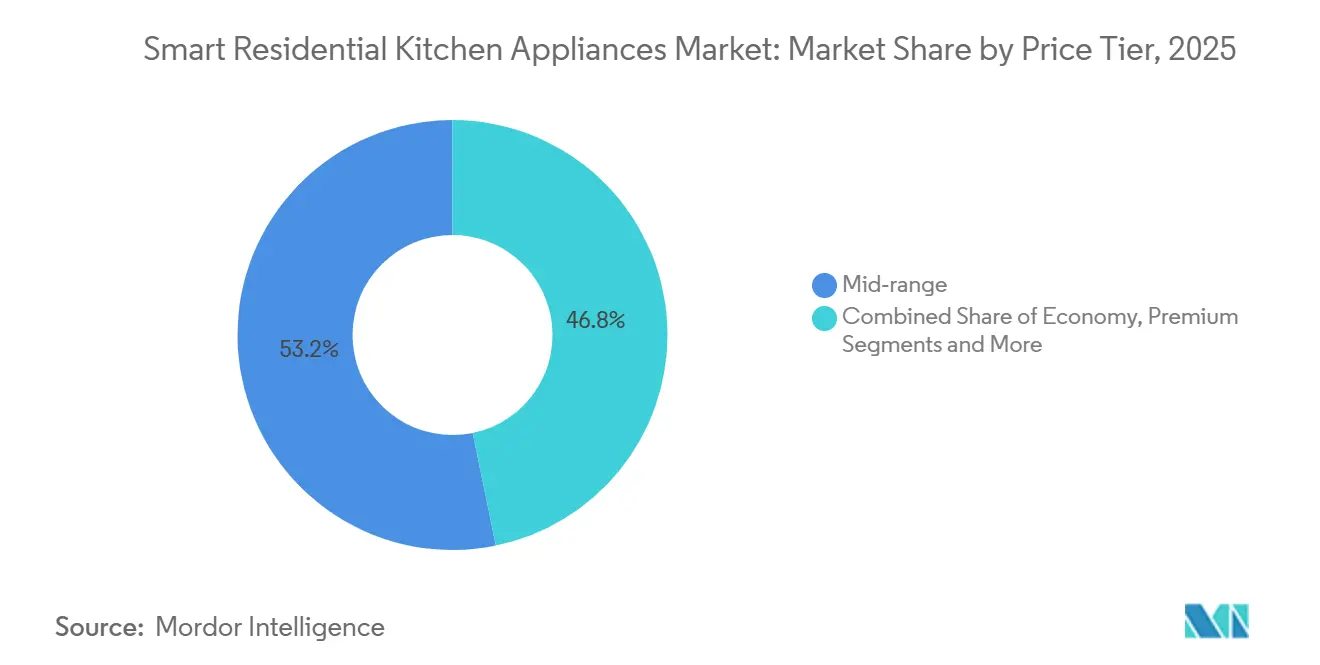

- By price tier, the mid-range captured 53.23% of the 2025 value in the smart residential kitchen appliances market, and the premium tier is projected to advance at a 12.27% CAGR through 2031.

- By distribution channel, multi-brand stores accounted for 43.92% of the market share in 2025 in the smart residential kitchen appliances market, and online channels are projected to grow at a 12.88% CAGR through 2031.

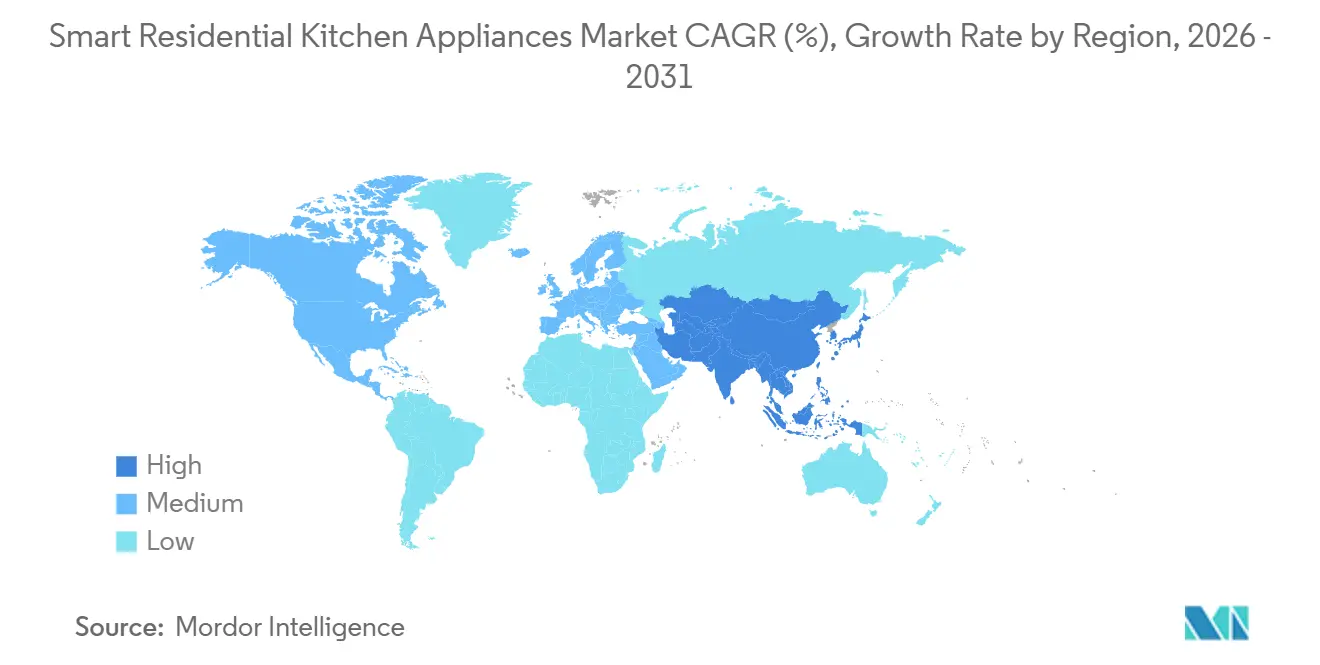

- By geography, the Asia-Pacific region accounted for 31.54% of the market share in 2025 in the smart residential kitchen appliances market, and Asia-Pacific leads growth with a 13.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Residential Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid smart-home adoption and Wi‑Fi ubiquity accelerate connected kitchen uptake | +2.8% | Global, led by North America, Developed Asia, and Europe | Medium term (2-4 years) |

| Energy-efficiency mandates and rebates drive premium smart replacements | +2.1% | Europe (European Union Ecodesign), North America (state incentives) | Short term (≤ 2 years) |

| Voice-assistant and app-based convenience shifts purchase criteria | +1.9% | Global, the highest in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Premium kitchen renovation and built‑in integration boost smart majors | +2.4% | North America, Western Europe, GCC states | Medium term (2-4 years) |

| Matter/Thread Standardization reduces setup friction and vendor lock‑in | +1.3% | North America, Europe, and the Asia-Pacific are slower. | Long term (≥ 4 years) |

| Grid‑interactive, demand‑response capable appliances create utility savings | +1.5% | Europe, California, Great Britain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Smart-Home Adoption and Wi Fi Ubiquity Accelerate Connected Kitchen Uptake

Mainstream connectivity and builder programs are moving the smart residential kitchen appliances market from one-off upgrades to standardized deployments in new builds, which accelerates exposure to AI-powered kitchen appliances for first-time buyers. Vendors are scaling app-controlled kitchen devices and membership models that package monitoring, auto-replenishment, and service into monthly plans to raise engagement after the initial sale. Partnerships that link refrigerators and pantries to ordering convert camera-based inventory into practical restocking, deepening the utility of IoT kitchen appliances in everyday routines. Policy in the United Kingdom now requires transparent security and updated support windows for connected devices, reducing lifecycle uncertainty for remote-controlled appliances in the smart residential kitchen market [2]Guidance Team, “Product Security and Telecommunications Infrastructure Act,” UK Government, gov.uk. Brand assistants are shifting toward natural conversation, and Alexa- and voice-controlled kitchen appliances are becoming easier to use across cooking and cleaning tasks, which raises satisfaction among buyers who want less setup complexity.

Energy-Efficiency Mandates and Rebates Drive Premium Smart Replacements

The European Commission’s 2025 standby-mode limits push brands to redesign connected products around low-power communications and predictive wake logic, which lowers idle consumption and aligns with grid-oriented programs in core regions. Germany’s Section 14a requires controllability for high-load appliances and offers fee reductions for devices that can shift or limit draw during peak periods, which strengthens the business case for upgrading certain cookers and ovens in the smart residential kitchen appliances market. Energy-schedule features that run cycles during high-renewable-generation or low-price windows demonstrate measured savings in pilots that pair policy with software innovation. California’s demand-side support programs also validate enrollment pathways for connected devices, even as awareness remains a gating factor for broad household participation. Together, these measures shorten payback horizons for efficient, grid-ready models and favor portfolios that treat IoT kitchen appliances as responsive assets rather than static loads.

Voice-Assistant and App-Based Convenience Shifts Purchase Criteria

Consumer behavior centers on simpler outcomes in the kitchen, which is why brands are improving guidance and automating routine steps with smart kitchen automation features that hide complexity behind natural interactions. Flagships in 2026 illustrate how software optimizes extraction, heating, and timing in real time, which validates a premium narrative for enthusiasts and busy families who want predictable results. Touchless kitchen appliances ease daily use by reducing physical effort through proximity and light-touch actuators, keeping surfaces cleaner. Attention to this detail supports adoption among older users. Voice-controlled kitchen appliances remove menu-diving by translating plain-language prompts into precise sequences and settings for ovens, hobs, and dishwashers across the smart residential kitchen appliances market. As mainstream buyers experience immediate convenience from app-controlled kitchen devices and assistants, the upgrade logic spreads from single devices to multi-appliance routines that align with a smart home integration kitchen experience.

Grid-Interactive, Demand-Response Capable Appliances Create Utility Savings

Great Britain’s standards roadmap establishes two-way communication and open protocols for energy-smart appliances later in the decade, which positions households to contribute to flexibility markets. Aggregation programs in California and Europe already enroll distributed resources and are beginning to include kitchen devices alongside HVAC and water heating as coordination improves. Germany’s Section 14a caps induction-range draw during peak periods while preserving most functionality and offering grid-fee reductions, aligning user incentives with grid stability and bolstering the value of controllable models in the smart residential kitchen appliances market. International toolkits outline how demand-response-ready appliances can reduce kitchen electricity use when paired with dynamic tariffs and automated participation, pointing to long-term potential as enrollment improves. As utilities simplify opt-ins and improve credit transparency, adoption can rise across everyday categories, expanding practical savings for households that use remote-controlled appliances for routine cooking and cleaning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and lifecycle costs vs. conventional alternatives | -2.3% | Global, acute in Latin America, South Asia, and Southeast Asia | Short term (≤ 2 years) |

| Data privacy and cybersecurity risks dampen adoption | -1.4% | Europe, North America | Medium term (2-4 years) |

| App and firmware end-of-life risk erodes utility and resale value | -1.1% | Global, regulatory backstops in the United Kingdom, emerging elsewhere | Medium term (2-4 years) |

| Fragmented after-sales and software support increases returns and churn | -0.9% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Costs Versus Conventional Alternatives

Price premiums for connected models and electrical upgrades for induction systems increase the initial outlay in many homes, which slows near-term conversion in regions with older housing stock. Field studies show higher problem incidence for connected models than for non-connected peers, resulting in service costs that erode savings when update support windows are short [3]Research Team, “U.S. Appliance Reliability and Satisfaction 2025,” J.D. Power, jdpower.com. Retailers bundle extended warranties and subscription maintenance to reduce uncertainty. Yet, these add-ons increase lifetime totals and raise hesitation among price-sensitive buyers in the smart residential kitchen appliances market. Policy transparency on minimum support durations, along with improved setup and reliability, can reduce total cost concerns for households considering migrating to IoT kitchen appliances during their next upgrade cycle. In the interim, buyers prioritize reliability and energy efficiency in core categories and delay more advanced features until economics align with budgets.

Data Privacy and Cybersecurity Risks Dampen Adoption

Security exposure remains a sticking point as large-scale exploitation attempts continue to target consumer IoT devices, and every new device adds new pathways into the home network. Recent high-volume DDoS events traced to compromised routers and connected devices underscore the systemic risk that spans categories beyond classic computing. Regulators in the United Kingdom now require transparency around data collection and firmware updates for Wi-Fi-enabled appliances, which aims to rebuild trust. The European Union’s Cyber Resilience Act moves toward effect with requirements for secure-by-design practices, encryption, and patching, which will raise compliance costs but should standardize baselines across the smart residential kitchen appliances market. Over time, brands that process more data locally and clearly disclose their handling practices can differentiate on privacy for buyers evaluating voice-controlled kitchen appliances and app-controlled kitchen devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cooktops Emerge as Fastest-Growing Category Amid Precision-Cooking Demand

Smart refrigerators held 31.53% of the smart residential kitchen appliances market share in 2025 and led purchase decisions with camera-driven food visibility, expiration tracking, and direct links to replenishment. Smart cooktops and hobs post the fastest 12.45% CAGR through 2031 as induction teams with precision sensors and integrated ventilation to deliver more control in compact kitchens across the smart residential kitchen appliances market. In 2026, an extractor induction hob combined a cooktop with 720 m³/h suction in a single appliance, achieving A+ efficiency, removing the need for separate range hoods and freeing up space [4]Newsroom Editors, “Bespoke AI Dishwasher and Extractor Induction Hob,” Samsung Global Newsroom, news.samsung.com . Premium cooktops now auto-detect cookware dimensions and stabilize target temperatures to prevent burning or boiling over, which helps less experienced cooks succeed more often. Ovens and microwaves add embedded cameras and AI recognition to recommend precision modes for common dishes, making advanced techniques accessible in everyday routines. Dishwashers benefit from adaptive wash logic and AI-powered sensing that cut water and energy use, reduce pre-rinsing, and shorten cycles, boosting satisfaction in the smart residential kitchen appliances market.

Small appliances extend connectivity and guidance into daily rituals, and this pull-through effect expands relevance beyond major domestic appliances. Dual-zone air fryers synchronize finish times across chambers to improve meal coordination. At the same time, premium espresso systems tune the grind and flow in real time based on resistance readings, reducing guesswork. Sensors, on-device intelligence, and streamlined interfaces improve win rates for novice users, which encourages repeat engagement and brand loyalty across the smart residential kitchen appliances market. As cooktops accelerate, spending gradually rebalances away from historical refrigerator dominance and into categories that deliver hands-on performance gains during preparation and cleanup in the smart residential kitchen appliances market.

By Installation Type: Built-Ins Outpace Countertop Despite a Smaller Base

Freestanding models dominated 2025, with a 65.62% share, as buyers favored simpler retrofits and lower initial costs, while built-ins accounted for 34.38% of the value that year. Built-ins are projected to expand the smart residential kitchen appliances market at a 12.53% CAGR through 2031, outpacing freestanding as premium renovations and new construction standardize integrated designs. New built-in suites pair efficient compressors, precision ovens, and hood-integrated induction with unified control that supports a smart home integration kitchen experience without switching apps. Multi-brand showcases present layered options from dependable mid-range to premium finishes while maintaining consistent cutouts and controls to ease planning. In high-spec developments across the Gulf, builders target cohesive built-in kitchens as a baseline for connected living, thereby elevating the visibility of AI-powered kitchen appliances in aspirational projects.

Freestanding remains essential in rental-heavy markets and in regions where cabinetry redesign is costly, which sustains broad access points for the smart residential kitchen appliances market. Vendors reduce installation risk for built-ins by providing clearer fit guides and modular kits that shorten downtime, making the path from planning to handover more predictable. As connectivity spreads evenly across both formats, shoppers choose based on room layout and renovation timing rather than feature differences, which supports a measured mix shift toward built-ins. The result is steady gains for integrated designs in new builds, while freestanding anchor replacements in legacy housing stock across the smart residential kitchen appliances market.

By Price Tier: Premium Segment Accelerates as AI Justifies Price Differentials

Mid-range captured 53.23% of the 2025 value as brands mainstreamed Wi Fi, app control, and voice integration at accessible price points across the smart residential kitchen appliances market. Premium is projected to expand the smart residential kitchen appliances market size at a 12.27% CAGR through 2031 as personalization, advanced sensing, and ecosystem services justify higher price points. High-end coffee systems and precision cookers illustrate how real-time control and guided workflows can reduce effort while achieving barista- or chef-level outcomes. Premium suites also link to subscription services for proactive maintenance and consumables, which shifts buyer relationships from one-time sales to ongoing value in the smart residential kitchen appliances market. Luxury lines keep elevated margins through design and materials, and they reinforce leadership by pairing curated experiences with smart home integration and kitchen controls for showpiece installations.

Competitive price pressure persists in the entry segment as Chinese brands leverage local supply chains to add connectivity without steep premiums, which compels incumbents to differentiate through reliability and service. The smart residential kitchen appliances industry, therefore, maintains a tiered upgrade path, with value-focused lines introducing connectivity and premium lines layering on automation that drives willingness to pay. As ecosystems consolidate around a few control platforms, premium providers can defend positions by combining industrial design, on-device intelligence, and content that keeps daily use fresh. Over the forecast horizon, premium growth complements a stable mid-range, and together they shape a balanced ladder for households that are modernizing kitchens in phases across the smart residential kitchen appliances market.

By Distribution Channel: Online Surges as Subscriptions and AR Tools Reshape Buying Journeys

Multi-brand stores accounted for 43.92% of the 2025 value, as in-store demos, bundled installation, and immediate availability remain decisive factors in the smart residential kitchen appliances market. Online channels are projected to grow at a 12.88% CAGR through 2031, supported by rich content, financing, and on-site planning tools that lower return risk for built-in purchases. Brand memberships that include package monitoring, auto-replenishment, and extended coverage convert one-time transactions into recurring relationships across connected suites. Augmented previews and placement tools reduce misfit risks for cabinetry and utilities, making online ordering more practical for integrated layouts that require precise measurements in the smart residential kitchen appliances market. Showrooms still play a key role for premium built-ins by allowing shoppers to evaluate alignment across finishes and controls before committing to a full-suite purchase.

Omnichannel shoppers who research across digital and physical touchpoints tend to finalize complex purchases with more confidence when inventory and pricing are consistent across platforms. Vendors are blending direct-to-consumer storefronts with marketplaces to broaden reach, then using subscriptions and updates to support retention in the smart residential kitchen appliances market. As logistics and service scheduling synchronize, online and store-based options complement rather than compete, which sustains a rising share of digital fulfillment over the forecast window.

Geography Analysis

Asia-Pacific led with a 31.54% share in 2025 and is projected to grow at a 13.63% CAGR through 2031, supported by large-scale manufacturing, rapid e-commerce adoption, and urban buyers' preference for connected cooking and cleaning. The smart residential kitchen appliances market in the region benefits from compact living spaces, where induction, integrated ventilation, and smart home-integrated kitchen controls improve usability. In India, cooking appliances captured a significant share of smart-category sales in 2026 as Wi Fi connectivity gained traction in mainstream models through partnerships and channel expansion. Japan’s aging buyers value hands-free operation and simplified guidance, and product roadmaps are adding proactive food management and safety features tailored to reduce routine complexity. As global and regional brands co-invest in localized content and services, the smart residential kitchen appliances market consolidates its leadership position in Asia-Pacific for the forecast period.

North America sustains double-digit growth from a mature base as manufacturers expand domestic capacity and leverage builder relationships to embed connected suites in new homes. A long-term supply agreement with a leading builder underscores how construction pipelines can accelerate deployments and smooth replacement cycles in the smart residential kitchen appliances market. Ecosystems that pair devices with assistants, content, and replenishment increase the value of installed bases, reinforcing retention and encouraging cross-category upgrades. Demand-side programs in California enroll responsive devices through aggregators, showing how policy can create parallel value in energy markets for households that opt in. As major replacement cycles for large appliances remain long, builders, utility partnerships, and subscription offers form new entry points that keep adoption resilient in the smart residential kitchen appliances market.

Europe shows robust momentum with unified policy, strong local brands, and a growing code of conduct for energy-smart appliances that promotes interoperability and market transparency. Standby-mode limits in force since 2025 drive low-power connectivity and predictive wake strategies that reduce idle draw and inform SoC choices. Germany’s Section 14a and the United Kingdom’s standards path align household incentives with grid priorities, which lifts demand for controllable models in the smart residential kitchen appliances market. Product examples highlight practical AI and agent-based workflows that coordinate ovens, hobs, and even espresso systems through conversational prompts to simplify cooking steps. Beyond the largest regions, premium projects in the Gulf are standardizing connected, built-in kitchens as part of broader smart living plans, elevating the visibility of AI-powered kitchen appliances in new residential clusters.

Competitive Landscape

Competition balances ecosystem lock-in with openness across the smart residential kitchen appliances market, and the most effective strategies now blend hardware launches with software updates, memberships, and content. Vertical integration leverages proprietary assistants across refrigerators, ovens, and dishwashers to coordinate guidance, replenishment, and care, which deepens engagement after purchase. Openness revolves around standards like Matter and Thread, where brands commit selectively to reduce setup friction while retaining differentiation through premium app features. Product launch velocity has increased, and execution on durability, software reliability, and service now carries greater weight than isolated feature wins in the smart residential kitchen appliances market.

Concrete moves illustrate how leading players pair hardware and software. In 2026, an agentic AI platform emerged to orchestrate multi-appliance cooking and translate user goals into timed steps across ovens and hobs, signaling a shift from device control to workflow management in the smart residential kitchen appliances market. A United States major introduced a smart convection wall oven with a camera that recognizes food and enables precision modes via voice input, reducing reliance on cloud backends during everyday use. Espresso systems that adjust grind mid-extraction based on resistance narrow the skill gap and broaden premium appeal for enthusiasts who value consistency.

Challengers use local semiconductor supply and scaled manufacturing to undercut entry prices while matching baseline connectivity, which raises the bar for incumbents to compete on industrial design and trusted ecosystems. Sustainability credentials and design awards act as signals in Europe, where recognition for energy performance and user-centered UX supports brand selection. Subscriptions like proactive maintenance and auto-replenishment turn post-sale engagement into predictable revenue, raising switching costs and shifting competition to a focus on lifetime value in the smart residential kitchen appliances market. Partnerships between appliance majors and software specialists accelerate the development of assistant features without rebuilding ML stacks from scratch, helping teams ship reliable guidance faster within a smart home integration kitchen environment.

Smart Residential Kitchen Appliances Industry Leaders

Samsung Electronics

LG Electronics

Whirlpool Corporation

Haier Smart Home (incl. GE Appliances)

BSH Hausgeräte

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: LG Electronics unveiled its LG Built-in kitchen suite at EuroCucina 2026, featuring AI Inverter Compressor refrigerators with A-grade efficiency, Camera Ovens with AI Gourmet food-recognition technology, and Hood Integrated Induction Cooktops that earned an iF Design Award 2026. The suite enables seamless SmartThings control across all appliances, targeting premium renovators in Europe seeking energy-optimized, design-forward solutions.

- April 2026: Samsung Electronics launched three Bespoke AI appliances: the Bespoke AI Single 1Door Fridge & Freezer with AI Precise Cooling that auto-adjusts defrost cycles via SmartThings; the Bespoke AI Dishwasher with AI Wash turbidity sensor eliminating pre-rinsing; and the Extractor Induction Hob combining cooking and ventilation at 720 m³/h suction and A+ efficiency. These products reinforce Samsung's strategy of embedding machine-learning logic into hardware to adapt to real usage patterns.

- April 2026: Beko showcased its multi-brand portfolio at EuroCucina 2026, including Whirlpool's WCollection oven with Cook4 technology for four simultaneous dishes without flavor transfer, Beko's HomeWhiz Energy & Water Management platform, and Hotpoint's VitalCare refrigeration with three-tone lighting to preserve antioxidants. The exhibition underscored Beko's strategy of addressing diverse income tiers while maintaining sustainability leadership.

- March 2026: GE Appliances introduced the Smart Convection Wall Oven with Cooking Assistant, manufactured at its LaFayette, Georgia, plant, following a USD 180 million expansion. The oven features CookCam AI for food recognition, voice-control temperature and time setting, and Precision Cooking modes, and the launch is part of GE's broader USD 3 billion 2025-2029 United States manufacturing investment.

Global Smart Residential Kitchen Appliances Market Report Scope

Smart residential kitchen appliances are designed for enhanced user-friendliness, aiming to eliminate the need for manual labor. The market for smart kitchen appliances is highly fragmented.

The Global Smart Residential Kitchen Appliances Market Report is Segmented by Product Type (Smart Refrigerators, Smart Microwaves and Ovens, Smart Cooktops & Hobs, Smart Dishwashers, Smart Blenders and Food Processors, Smart Air Fryers, Smart Coffee Machines, Smart Multi Cookers, Smart Toasters, Others), Installation Type (Built in, Countertop / Freestanding), Price Tier (Economy, Mid range, Premium, Luxury), Distribution Channel (Multi-brand Stores, Exclusive Brand Outlets, Online, Other Distribution Channels), and Geography (North America, South America, Europe, Asia-Pacific, Middle East And Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smart Refrigerators |

| Smart Microwaves and Ovens |

| Smart Cooktops & Hobs |

| Smart Dishwashers |

| Smart Blenders and Food Processors |

| Smart Air Fryers |

| Smart Coffee Machines |

| Smart Multi‑Cookers |

| Smart Toasters |

| Others (Range Hoods,Kettles) |

| Built‑in |

| Countertop / Freestanding |

| Economy |

| Mid‑range |

| Premium |

| Luxury |

| Multi-brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia‑Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia‑Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Smart Refrigerators | |

| Smart Microwaves and Ovens | ||

| Smart Cooktops & Hobs | ||

| Smart Dishwashers | ||

| Smart Blenders and Food Processors | ||

| Smart Air Fryers | ||

| Smart Coffee Machines | ||

| Smart Multi‑Cookers | ||

| Smart Toasters | ||

| Others (Range Hoods,Kettles) | ||

| By Installation Type | Built‑in | |

| Countertop / Freestanding | ||

| By Price Tier | Economy | |

| Mid‑range | ||

| Premium | ||

| Luxury | ||

| By Distribution Channel | Multi-brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia‑Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia‑Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the smart residential kitchen appliances market size in 2026 and the projected value for 2031?

The smart residential kitchen appliances market size is USD 16.36 billion in 2026 and is projected to reach USD 28.77 billion by 2031 at an 11.96% CAGR.

Which product segment currently leads, and which is growing fastest?

Smart refrigerators led with 31.53% of revenue in 2025, while smart cooktops and hobs are projected to post the fastest 12.45% CAGR through 2031.

Which region contributes the most to near-term growth?

Asia-Pacific leads with 31.54% share in 2025 and is projected to grow at a 13.63% CAGR to 2031, driven by manufacturing scale and connected adoption.

How are brands differentiating beyond hardware features?

Vendors combine AI guidance, subscriptions for service and replenishment, and standards-based connectivity to increase engagement and lifetime value across suites.

What role will grid programs play for connected kitchens by 2031?

Standards in Europe and utility programs in North America are expanding enrollment pathways for controllable devices, which can add value for households that opt in.

What buying channels are expanding fastest for large appliances?

Online channels are projected to grow at a 12.88% CAGR as better content, financing, and planning tools reduce return risks for integrated installations.

Page last updated on: