Smart Patches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.97 Billion |

| Market Size (2031) | USD 15.15 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

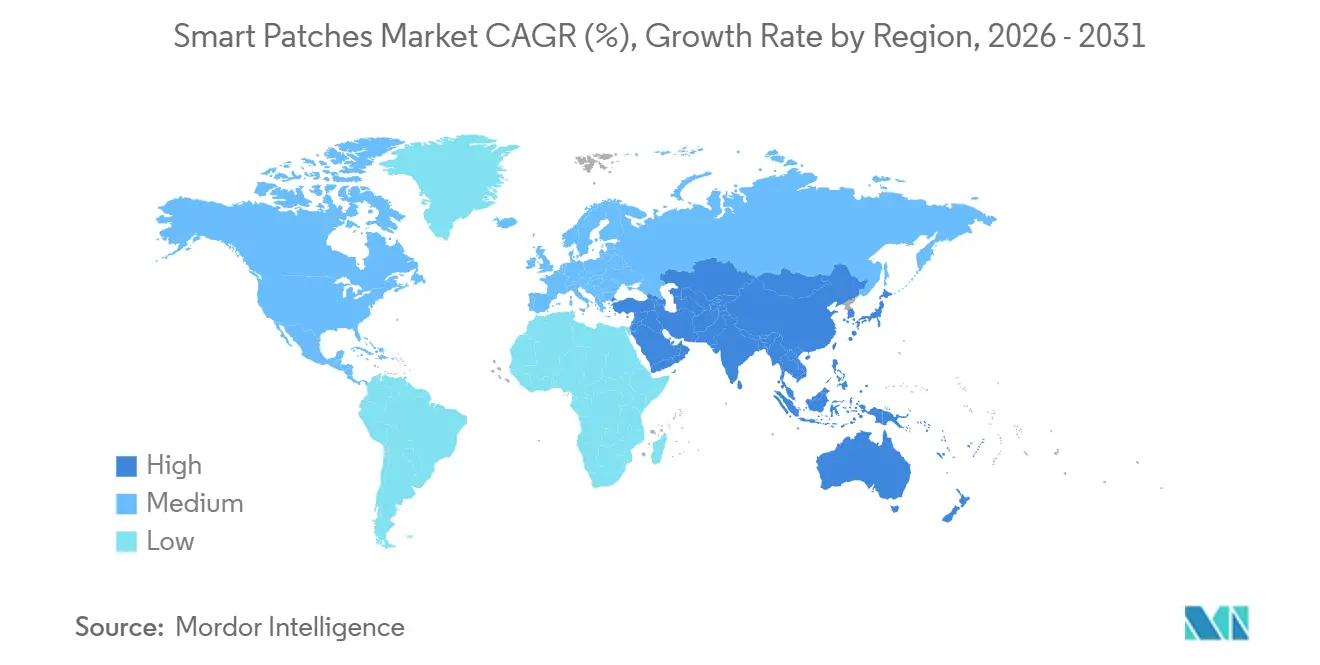

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

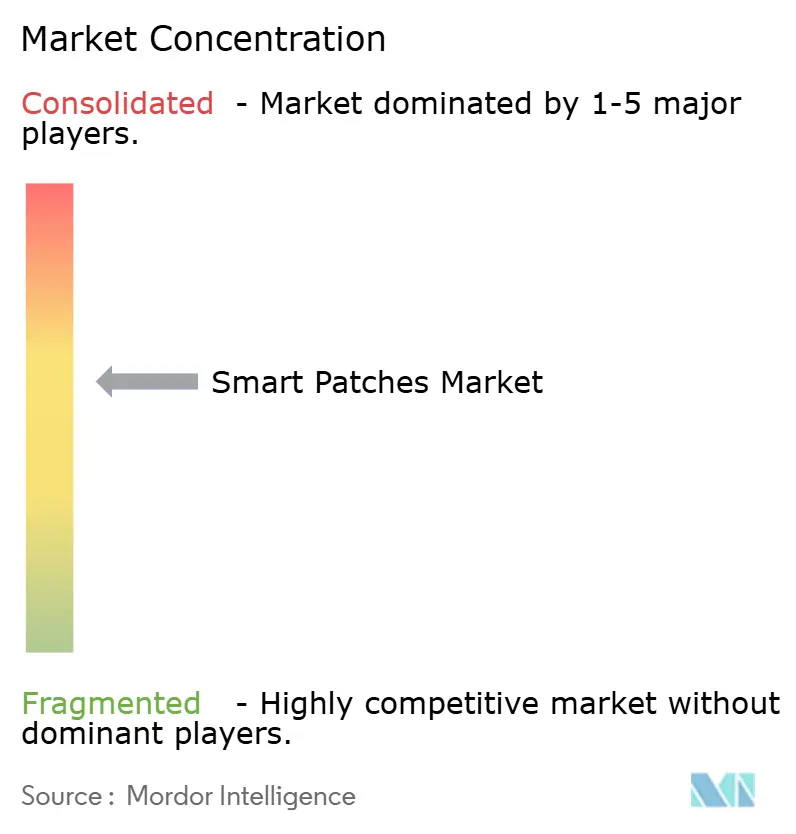

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Patches Market Analysis by Mordor Intelligence

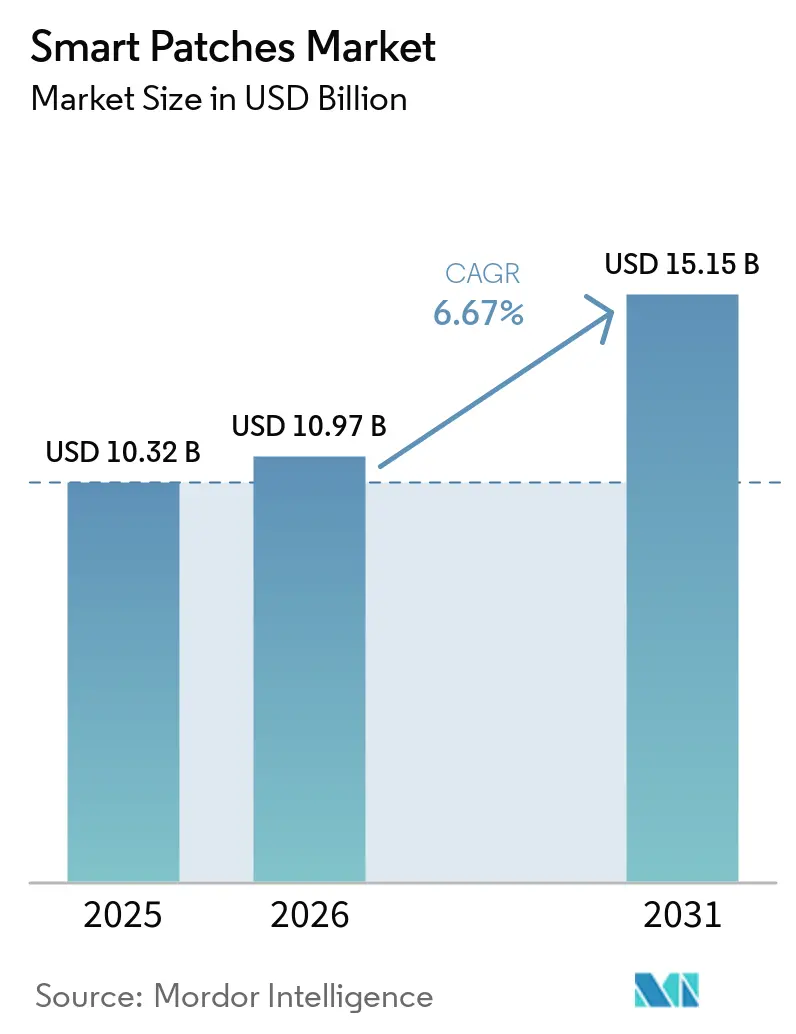

The Smart Patches Market size is expected to grow from USD 10.32 billion in 2025 to USD 10.97 billion in 2026 and is forecast to reach USD 15.15 billion by 2031 at 6.67% CAGR over 2026-2031.

Continuous reimbursement expansion, over-the-counter continuous glucose monitor (CGM) approvals, and sensor miniaturization are moving physiologic monitoring from clinic walls to skin-level wearables, anchoring a mid-single-digit growth trajectory. North America led in 2025 with a majority of revenue share, yet Asia-Pacific is registering the fastest advance on large-population chronic-disease burdens and domestic CGM clearances. Monitoring patches dominated the 2025 value, but drug-delivery formats integrating microneedles and patch pumps are outpacing the core category as insulin-delivery convergence stimulates therapeutic functionality on the epidermis. Regulatory signals including the Food and Drug Administration’s 2026 READI-Home Challenge and new U.S. remote-physiologic monitoring (RPM) billing codes cement patches as reimbursable clinical assets, while advances in intrinsically stretchable electronics remove comfort barriers that once capped multi-day wear.

Key Report Takeaways

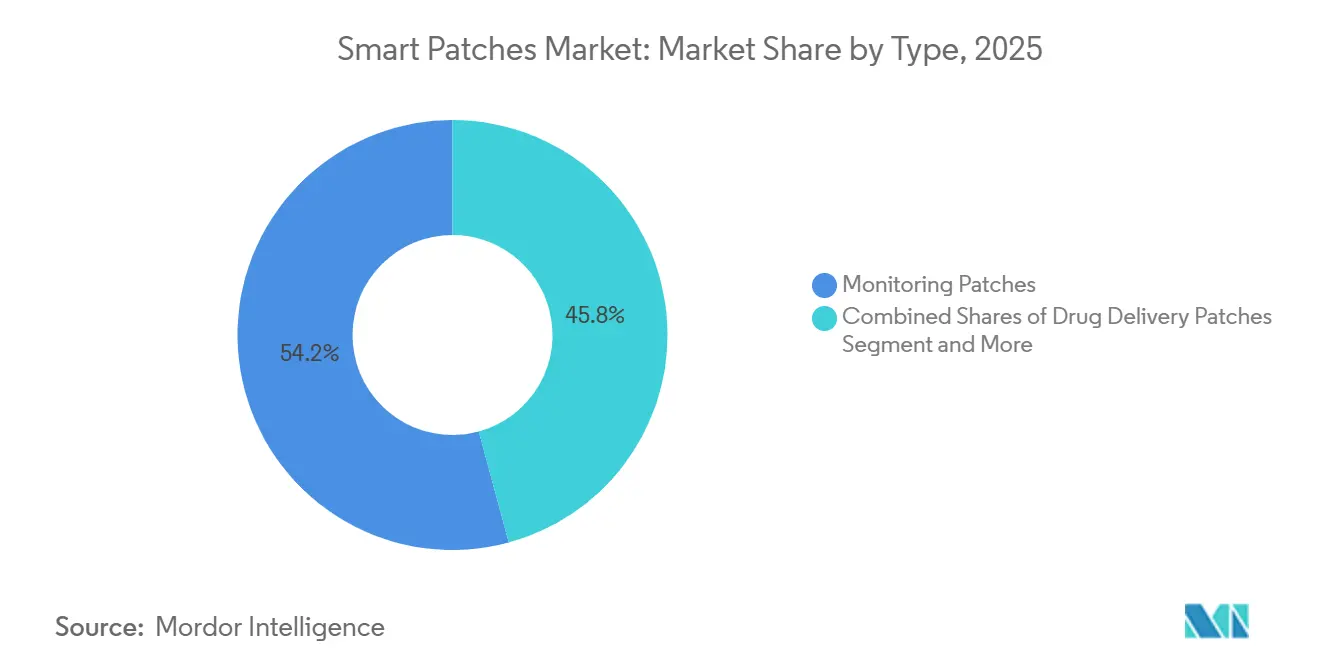

- By type, monitoring patches held 54.21% of the smart patches market share in 2025. Whereas drug-delivery patches are projected to expand at an 8.23% CAGR through 2031.

- By application, diabetes management captured 38.56% of 2025 revenue; cardiac monitoring is forecast to grow at an 8.02% CAGR to 2031.

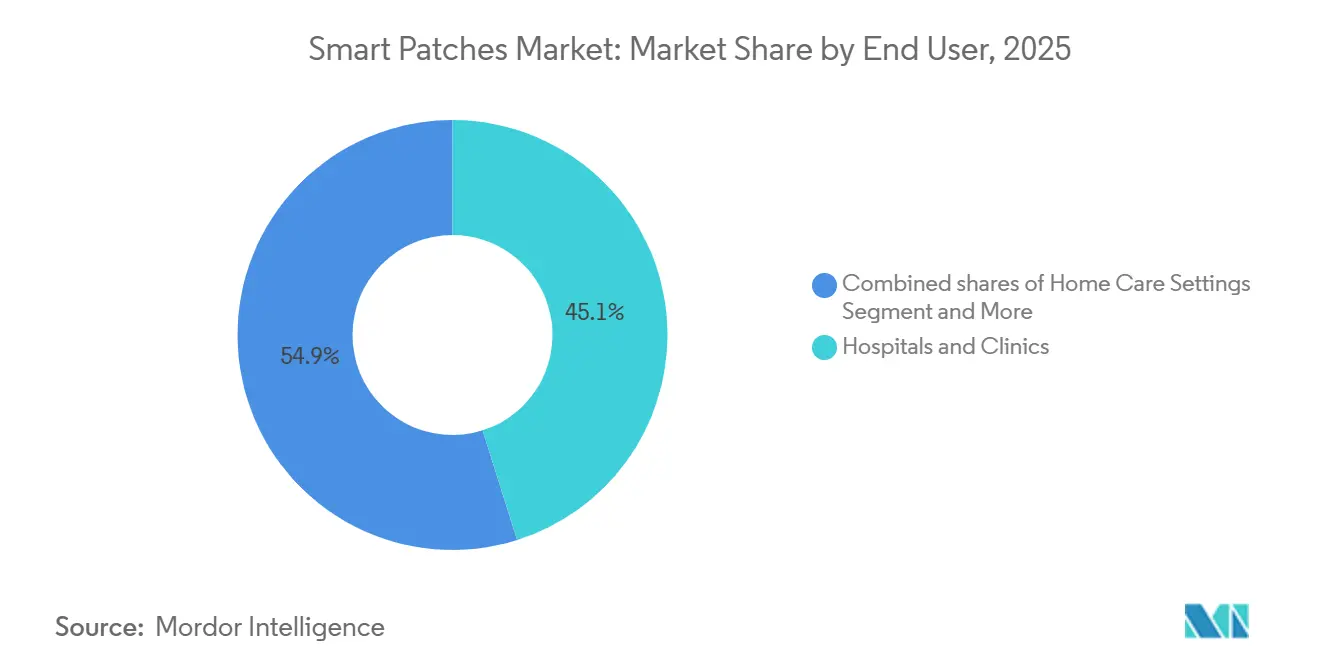

- By end user, hospitals and clinics commanded 45.13% of 2025 sales, although home-care settings will accelerate at an 8.15% CAGR over the forecast horizon.

- By geography, North America generated 46.90% of the 2025 value, while Asia-Pacific is advancing at an 8.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Patches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RPM reimbursement and telehealth expansion sustain continuous, at-home monitoring adoption | +1.2% | North America, spillover to EU and APAC | Medium term (2-4 years) |

| Diabetes and cardiovascular disease burden shifts monitoring to skin patches and CGMs | +1.5% | Global, concentrated in North America, Europe, urban APAC | Long term (≥4 years) |

| OTC CGMs expand TAM beyond insulin users, catalyzing consumer and primary-care uptake | +1.0% | North America and EU, early adoption in Australia and Japan | Short term (≤2 years) |

| Hospital-at-home and early-discharge pathways standardize patch-based vitals monitoring | +0.8% | North America and Western Europe, pilots in APAC | Medium term (2-4 years) |

| FDA digital-health guidance normalizes patch data in clinical trials and endpoints | +0.7% | Global, precedent set in US and EU | Medium term (2-4 years) |

| Miniaturized, flexible electronics and long-wear adhesives unlock multi-day comfort | +0.9% | Global, R&D hubs in US, EU, Japan, South Korea | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

RPM Reimbursement and Telehealth Expansion Sustain Continuous, At-Home Monitoring Adoption

New U.S. RPM codes (99445, 99470), effective January 2026, let providers bill for patch-transmitted respiratory, activity, and multi-parameter data, broadening billable services beyond glucose and blood pressure. Federal telehealth flexibilities, extended through 2027, allow clinicians to start RPM without in-person visits, fueling hospital-at-home models that rely on continuous patch data. Large health-system pilots such as Penn Medicine’s PATH program report reduced readmissions and lower bed-day utilization when patches stream vitals to command centers. Private payers have started mirroring Medicare coverage, turning wearable monitoring into a routine revenue stream for providers. The reimbursement framework repositions patches from wellness gadgets to reimbursable clinical endpoints, removing a primary adoption barrier.

Diabetes and Cardiovascular Disease Burden Shifts Monitoring to Skin Patches and CGMs

Global intensive-insulin populations exceed 11 million, yet automated insulin delivery adoption remains under 15%, leaving large headroom for integrated glucose-sensing pumps[1]Abbott Laboratories, “First-Quarter 2025 Earnings Release,” abbott.com. Abbott recorded USD 1.7 billion in CGM revenue in 1Q 2025, and Dexcom forecasted USD 4.6 billion full-year sales, underscoring robust demand. Parallel cardiac-monitoring growth is evident in the 2024 FDA clearance of Medtronic’s LINQ II insertable cardiac monitor, enabling long-term arrhythmia detection. Overlapping diabetic and cardiac cohorts benefit from multi-parameter patches, prompting vendors to fuse glucose, electrocardiogram, and accelerometry on one adhesive. Clinical studies linking CGM use to lower HbA1c and reduced hospitalization intensify payer willingness to reimburse skin-worn sensors.

OTC CGMs Expand TAM Beyond Insulin Users, Catalyzing Consumer and Primary-Care Uptake

The FDA cleared Dexcom Stelo in March 2024 and Abbott Libre Rio in June 2024, the first prescription-free CGMs in the United States. Targeting non-insulin type 2 diabetics and wellness consumers, these devices swell the total addressable market scope. Abbott integrated Libre data into Epic Systems’ electronic health records, enabling 575,000 clinicians to view readings inside standard workflows. Dexcom’s USD 75 million investment in Oura couples glucose with sleep and activity metrics, attracting health-conscious users seeking metabolic insight[2]Dexcom Inc., “Dexcom Announces Investment in Oura,” dexcom.com. Prescription-free pathways cut lead-time to purchase, and digital-health partnerships open distribution beyond endocrinology clinics.

Hospital-at-Home and Early-Discharge Pathways Standardize Patch-Based Vitals Monitoring

Saint Luke’s Health System deploys VitalConnect’s seven-day patch to monitor early-discharge surgical patients, streaming vitals to remote nurses and triggering alerts before clinical deterioration. The FDA’s April 2026 READI-Home Challenge offers an explicit route for vendors whose patches meet home-use benchmarks, accelerating review of decentralized monitoring platforms. European initiatives, including a Philips–smartQare collaboration, integrate biosensors into hospital-at-home workflows to relieve inpatient capacity. Peer-reviewed German data show continuous patch monitoring in at-home palliative care improved comfort and reduced unplanned visits. Alignment of reimbursement, regulation, and capacity pressures makes patch surveillance financially attractive to providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adhesive-related skin irritation and MARSI limit wear time and compliance | -0.5% | Global, heightened scrutiny in EU and North America | Short term (≤2 years) |

| Cybersecurity and privacy compliance increases cost and integration complexity | -0.4% | Global, enforcement is strongest in the US and the EU | Medium term (2-4 years) |

| RF coexistence and EMC issues in hospitals risk data loss or alarms | -0.3% | Global, critical in high-acuity environments | Medium term (2-4 years) |

| EU battery rules drive redesigns, raising compliance burden | -0.3% | European Union, spillover to global SKU strategy | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Adhesive-Related Skin Irritation and MARSI Limit Wear Time and Compliance

Medical-adhesive skin injury remains the most cited adverse event in wearable-patch trials, presenting as erythema or epidermal stripping that forces premature removal. Silicone gels mitigate irritation but provide weaker initial tack than acrylics, requiring skin-prep steps that deter consumer use. A 2026 npj Flexible Electronics study showed polyurethane-blended nanomesh electrodes retained adhesion after six hours of water flow, while only one-third of poly(vinyl alcohol) electrodes remained functional. Manufacturers must balance secure adhesion with dermatologic tolerance in the absence of standardized MARSI testing, complicating claims for wear beyond seven days.

Cybersecurity and Privacy Compliance Increase Cost and Integration Complexity

March 2024 FDA pre-market guidance compels connected-device makers to submit software bills of materials and threat models, elongating development cycles[3]U.S. Food and Drug Administration, “Cybersecurity in Medical Devices Final Guidance,” fda.gov. Post-market rules require ongoing vulnerability disclosures, straining small-to mid-size innovators. The EU Cyber Resilience Act and GDPR add breach-notification and data-protection-officer mandates, while the U.S. Health Insurance Portability and Accountability Act encryption obligations extend to cloud hosts. Compliance overhead favors incumbents with mature security engineering teams, potentially slowing the entry of agile start-ups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Drug Delivery Outpaces Monitoring on Therapeutic Integration

Monitoring patches accounted for 54.21% of 2025 revenue, anchored by CGM flagships such as Abbott Libre and Dexcom G7. The drug-delivery subset of the smart patches market is on track for an 8.23% CAGR as microneedle vaccines, transdermal analgesics, and patch pumps integrate sensing and therapy. Medtronic’s MiniMed 780G paired with Abbott’s Instinct sensor in early 2026 represents the first open-platform insulin pump-plus-CGM, demonstrating a pathway for cross-vendor therapeutic ecosystems.

The smart patches market size allocated to drug delivery is projected to climb steadily as combination-product exclusivity attracts investment. Electrical-stimulation patches, though still niche, are gaining physician adoption for opioid-sparing pain management. Integrated platforms cut device burden for multi-morbidity patients, unifying consumables and data flows. Combination-product regulation extends timelines but offers competitive moats, encouraging capital allocation toward microneedle manufacturing scale-up. With polymer-semiconductor research now enabling low-power logic on flexible substrates, drug-delivery patches are well positioned to embed closed-loop algorithms that titrate dosing in real time.

By Application: Cardiac Monitoring Gains on Arrhythmia Detection and Remote Telemetry

Diabetes management generated 38.56% of application revenue in 2025, but cardiac monitoring is the fastest riser, poised for an 8.02% CAGR through 2031. SmartCardia’s 7-lead electrocardiogram patch funnels full-disclosure data to a cloud algorithm that flags arrhythmias within minutes, helping cardiologists replace 24-hour Holter monitors with 14-day wearables. iRhythm’s Zio platform keeps winning multi-year health-system deals as payers reimburse mobile cardiac telemetry. The smart patches market size tied to cardiac applications is expanding as the Centers for Medicare & Medicaid Services added telemetry-specific RPM codes in 2026. Temperature and infection-tracking patches, first popularized in pandemic wards, are migrating to post-operative care, delivering early sepsis alerts.

Growing multiparameter RPM bundles heart rate, respiration, oxygen saturation, and activity into one adhesive, supporting hospital-at-home cohorts. Academic wound-monitoring prototypes show promise with pH and enzyme sensors, yet lack reimbursement codes. Once coverage aligns, these platforms could capture incremental smart patches market share by replacing manual dressing checks.

By End-User: Home Care Surges on Early Discharge and Telehealth Policy

Hospitals and clinics retained the largest slice in 2025, but home-care uptake is accelerating at an 8.15% CAGR. CMS now lets providers bill RPM without in-person exams, and the FDA READI-Home Challenge has fast-tracked review of home-use patches. Health-system pilots show inpatient-day reductions when early-discharge patients wear multi-vital patches. Employers and sports franchises comprise a small but rising customer base as patches track hydration and heat stress. Smart worker-safety mandates in high-temperature industries could convert niche thermal patches into steady-volume orders, diversifying revenue beyond medical reimbursement streams.

Geography Analysis

North America commanded 46.90% of 2025 revenue, aided by Medicare RPM payments, OTC CGM launches, and hospital-at-home adoption. The smart patches market size in Asia-Pacific is expected to log the fastest advance, expanding at 8.23% CAGR through 2031. Regional approvals, such as South Korea MFDS clearance for HLB Lifecare’s 15-day Picoling CGM and China NMPA authorization for Sibionics GS3, enable domestic vendors to undercut Western incumbents on form factor and price.

European growth trails as companies grapple with Medical Device Regulation conformity and new battery mandates that prolong redesign cycles. Germany’s DiGA pathway reimburses Class IIa patches, yet uptake centers on diabetes and arrhythmia use cases. Emerging markets in South America and the Middle East rely on CE marks for quick entry but lack robust reimbursement, dampening volume. Asia-Pacific’s chronic-disease base stands to leapfrog clinic-centric pathways by adopting direct-to-consumer CGMs through e-commerce and primary-care networks. India’s 2026 clearance of MicroTech Medical’s LinX CGM hints at broader regional momentum, though integration with insulin pumps remains nascent. Vendors attuned to local pricing and smartphone ecosystems are best placed to capture share in the fastest-growing geography of the smart patches market.

Competitive Landscape

Moderate fragmentation defines the market. Abbott and Dexcom control CGMs but now license sensors to third-party insulin-pump makers, extending reach beyond proprietary ecosystems. Abbott’s August 2024 alliance with Medtronic integrates FreeStyle Libre into MiniMed systems, while Dexcom’s Oura partnership layers glucose onto wellness analytics. Cardiac-telemetry pure-plays iRhythm and VitalConnect lock in long-term health-system contracts that convert disposable patches into recurring revenue. Asian challengers Sibionics and HLB Lifecare field ultra-thin, 15-day sensors that appeal to cost-sensitive markets. Intellectual-property friction surfaced when Abbott filed an injunction against Sinocare at the Unified Patent Court in 2025, confirming that patents remain potent competitive weapons.

Technology differentiation rests on accuracy and wear duration. Abbott’s Instinct sensor promises 15-day life, while Dexcom G7 delivers 8.2% mean absolute relative difference across ten-day wear, setting high performance thresholds. SmartCardia raises the diagnostic bar with seven-lead electrocardiography in a single patch, and Stanford stretchable-circuit discoveries portend further gains in comfort and data richness. Consolidation looms as diversified med-tech firms hunt for skin-worn sensor assets to round out chronic-disease portfolios.

Smart Patches Industry Leaders

Abbott Laboratories

Dexcom, Inc.

Medtronic plc

Koninklijke Philips N.V.

iRhythm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The FDA opened the READI-Home Challenge, pledging expedited review for patches that satisfy home-use safety and performance metrics.

- March 2026: HLB Lifecare secured South Korea MFDS approval for its ultralight Picoling CGM, featuring 15-day wear and 8.66% accuracy.

- February 2026: The FDA issued final pre-market cybersecurity guidance requiring software bills of materials and threat-response processes for connected devices.

Global Smart Patches Market Report Scope

As per the scope of the report, smart patches are wearable, adhesive devices directly applied to the skin to provide continuous, non-invasive health monitoring or controlled drug delivery. Unlike standard wearables like smartwatches, these patches use flexible electronics and advanced sensors to interface intimately with the body, tracking vital signs such as heart rate, body temperature, and hydration, as well as biochemical markers like glucose or lactate.

The smart patches market is segmented by type, application, end-user, and geography. Based on type, the market is segmented into monitoring patches, drug delivery patches, and electrical stimulation patches. By application, the market is segmented into diabetes management (CGM), cardiac monitoring/arrhythmia detection (ECG), temperature/fever & infection surveillance, multiparameter RPM (home and ambulatory), wound monitoring & post‑operative care, and clinical trials data capture (decentralized). By end users, the market is hospitals & clinics, home care settings, ambulatory or diagnostic & cardiac centers, and sports & fitness/workforce health. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Monitoring Patches (vitals, CGM, ECG) |

| Drug Delivery Patches (transdermal, microneedle, patch pumps) |

| Electrical Stimulation Patches (neuromodulation/TENS) |

| Diabetes Management (CGM) |

| Cardiac Monitoring / Arrhythmia Detection (ECG) |

| Temperature / Fever & Infection Surveillance |

| Multiparameter RPM (home and ambulatory) |

| Wound Monitoring & Post‑operative Care |

| Clinical Trials Data Capture (decentralized) |

| Hospitals & Clinics |

| Home Care Settings |

| Ambulatory/Diagnostic & Cardiac Centers |

| Sports & Fitness / Workforce Health |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Monitoring Patches (vitals, CGM, ECG) | |

| Drug Delivery Patches (transdermal, microneedle, patch pumps) | ||

| Electrical Stimulation Patches (neuromodulation/TENS) | ||

| By Application | Diabetes Management (CGM) | |

| Cardiac Monitoring / Arrhythmia Detection (ECG) | ||

| Temperature / Fever & Infection Surveillance | ||

| Multiparameter RPM (home and ambulatory) | ||

| Wound Monitoring & Post‑operative Care | ||

| Clinical Trials Data Capture (decentralized) | ||

| By End‑User | Hospitals & Clinics | |

| Home Care Settings | ||

| Ambulatory/Diagnostic & Cardiac Centers | ||

| Sports & Fitness / Workforce Health | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the smart patches market in 2026?

The smart patches market size was USD 10.97 billion in 2026 and is projected to reach USD 15.15 billion by 2031, reflecting a 6.67% CAGR

Which application generates the most revenue?

Diabetes management led in 2025 with 38.56% of sales as CGMs expanded beyond insulin users

What is the fastest-growing application segment?

Cardiac monitoring is advancing at an 8.02% CAGR through 2031 because extended-wear electrocardiogram patches now qualify for new RPM reimbursement codes

Why is Asia-Pacific considered the high-growth region?

Domestic approvals for ultra-thin CGMs in China and South Korea, coupled with hospital-at-home pilots that bypass legacy infrastructure, drive an 8.23% CAGR in Asia-Pacific through 2031

Page last updated on: