Smart Commercial Kitchen Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

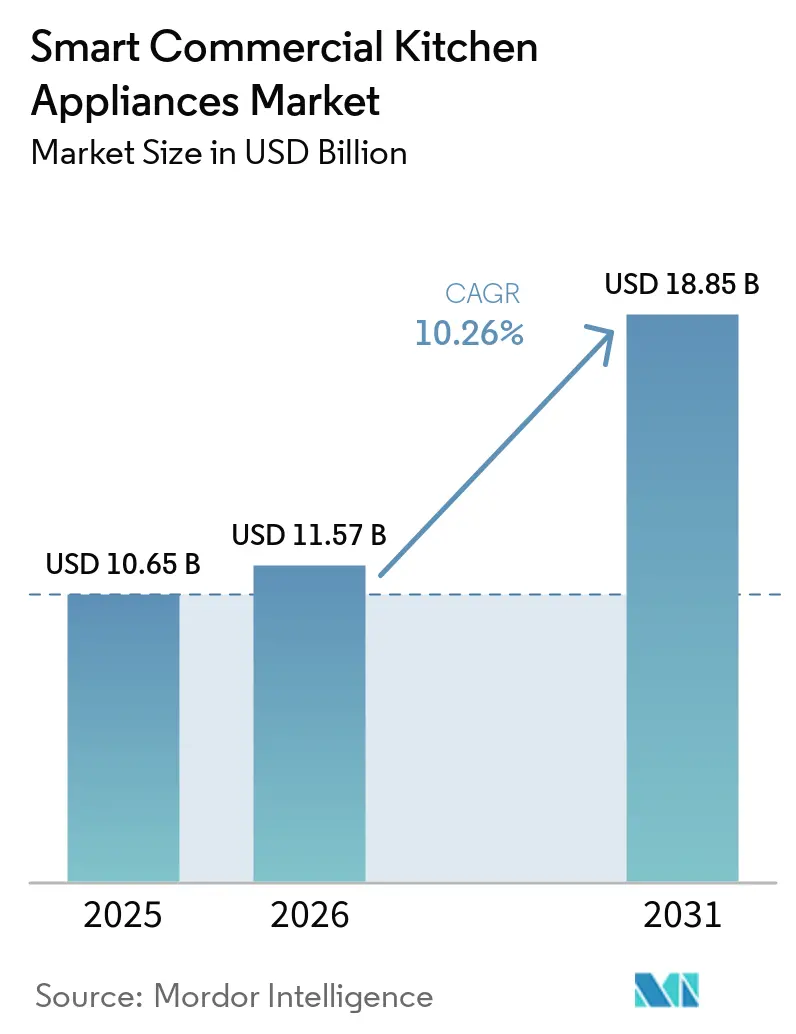

| Market Size (2026) | USD 11.57 Billion |

| Market Size (2031) | USD 18.85 Billion |

| Growth Rate (2026 - 2031) | 10.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Commercial Kitchen Appliances Market Analysis by Mordor Intelligence

The Smart Commercial Kitchen Appliances market size was valued at USD 10.65 billion in 2025 and estimated to grow from USD 11.57 billion in 2026 to reach USD 18.85 billion by 2031, at a CAGR of 10.26% during the forecast period (2026-2031). Labor shortages and rising wage floors have pushed operators to adopt connected and automated back-of-house equipment that lifts throughput and consistency while reducing reliance on manual oversight. Intelligent equipment offers a path forward: automation shifts the coordination burden from manual oversight to predictive systems, while IoT sensors reduce manual temperature logging tasks that typically take 30-60 minutes daily with 30-40% inaccuracy into unalterable digital records satisfying health inspectors[1]Envigilance, “Restaurant Equipment Monitoring,” Envigilance, envigilance.com. The latest product wave embeds predictive analytics and remote fleet control so multi-site chains can standardize execution and proactively resolve equipment issues before they create service disruptions. Refrigerant phase-outs and energy-efficiency rules force upgrade cycles, but they also align incentives for connected systems that optimize loads and participate in demand-response programs. Vendors now pair hardware with software platforms that centralize HACCP logging, recipe distribution, and service diagnostics to deliver measurable operational savings across distributed sites.

Key Report Takeaways

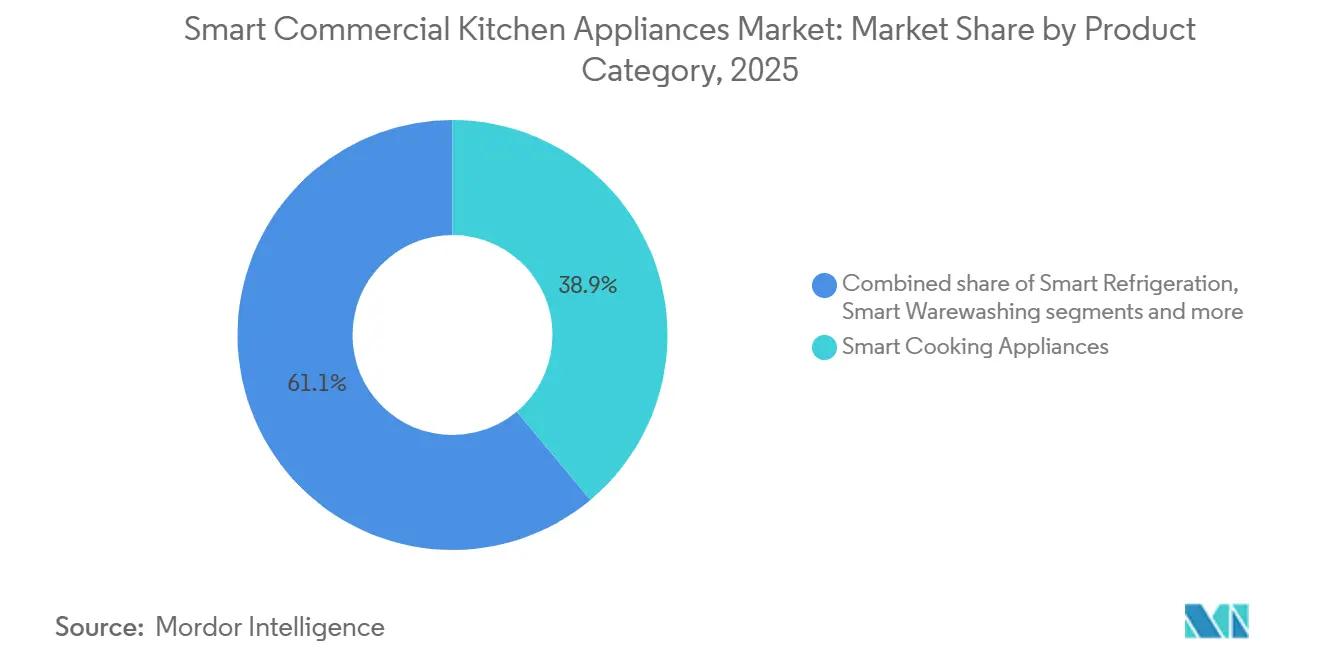

- By product category, smart cooking appliances led with 38.91% of the smart commercial kitchen appliances market share in 2025, while smart beverage appliances are projected to expand at a 10.45% CAGR through 2031.

- By installation type, floor-standing and back-of-house units held 56.46% of the smart commercial kitchen appliances market share in 2025, whereas countertop and compact units are forecast to grow at a 10.83% CAGR through 2031.

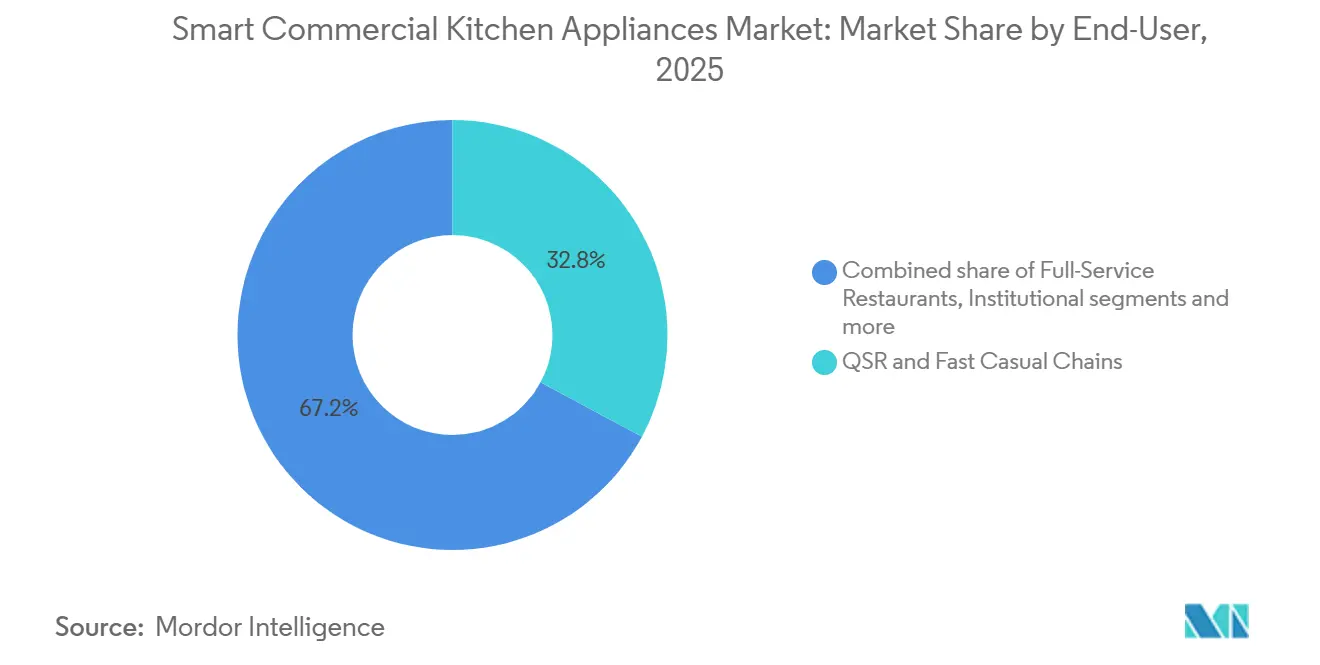

- By end-user, QSR and fast-casual chains accounted for 32.84% of the smart commercial kitchen appliances market share in 2025, while cafes, bakeries, and coffee chains are expected to record a 10.36% CAGR through 2031.

- By distribution channel, dealers/distributors held 46.35% of the kitchen appliances market share in 2025, while direct (mainly through D2C channels) are set to grow at a 10.59% CAGR through 2031.

- By geography, North America captured 32.73% of the kitchen appliances market share in 2025, while Asia-Pacific is projected to post the highest growth at an 11.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Commercial Kitchen Appliances Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages push automation and connected equipment ROI | +2.8% | Global, with acute pressure in North America, Western Europe, Japan | Medium term (2-4 years) |

| Energy efficiency mandates and utility costs accelerate smart retrofits | +1.9% | North America (DOE standards), EU (refrigerant phase-out), Asia-Pacific core | Long term (≥ 4 years) |

| Digital HACCP and food safety compliance standardize connected equipment | +1.6% | United States (FDA FSMA 204), EU, major export hubs | Short term (≤ 2 years) |

| Chain standardization and multi-site remote fleet control | +2.2% | Global chains, franchise networks | Medium term (2-4 years) |

| Demand-response and grid incentives for connected electric kitchens | +0.9% | North America (California, Texas, Northeast), EU pilot markets | Medium term (2-4 years) |

| Insurance and compliance credits for IoT-verified operations | +0.8% | United States (multi-state), Canada, select EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages Push Automation and Connected Equipment ROI

Persistent staffing gaps and wage inflation have made automation financially viable in many kitchens, which strengthens adoption across the Smart Commercial Kitchen Appliances market as operators seek predictable output and lower on-the-line labor exposure. Robotic fry stations, AI-enabled makelines, and connected prep systems deliver measurable benefits by increasing throughput, reducing rework, and minimizing safety incidents during peak service windows. Deployed systems that automate repetitive, high-heat tasks show clear reductions in injuries and oil waste while stabilizing food quality at scale for chains with uniform menus. Automation of oil handling and filtration, paired with digital verification, also helps operators qualify for premium credits because it lowers the risk profile for burns and spills. The technology's second-order effect is labor redeployment: servers handling 40% more tables with Bear Robotics' Servi bots report 12% higher guest satisfaction, transforming headcount debates into service-quality arbitrage[2]Silicon Valley Robotics, “Restaurant Robots: Deployments and ROI,” Silicon Valley Robotics, roboticscenter.ai.

Energy Efficiency Mandates and Utility Costs Accelerate Smart Retrofits

The United States Department of Energy commercial refrigeration standards (effective January 2029, compliance deadline extended from 2025) will tighten maximum daily energy consumption limits by 6.5% versus current baselines, with projected cumulative savings of 1.11 quadrillion BTUs through 2058[3]United States Government, “Energy Conservation Standards for Commercial Refrigerators, Freezers, and Refrigerator-Freezers,” Federal Register, federalregister.gov. Platforms that integrate sensors, edge logic, and centralized dashboards help sites reduce total energy use while improving compliance with equipment-level limits and audit requirements. Operators that coordinate startup sequences and schedule high-load processes outside billing peaks cut demand charges without sacrificing speed of service or food safety when capacity constraints are tight. Participation in demand-response programs creates a new incentive layer for connected electric kitchens, since kitchens can pre-cool or pre-heat and then coast during events with minimal guest impact. Integrated demand-response solutions both streamline enrollment and automate response at the device level, which reduces operational friction for multi-unit chains.

Digital HACCP and Food Safety Compliance Standardize Connected Equipment

The FSMA 204 food traceability rule, effective January 20, 2026, requires electronic records for specific foods that can be retrieved within 24 hours, which is accelerating adoption of IoT sensors and digital platforms in the Smart Commercial Kitchen Appliances market. Analog logs cannot satisfy the 24-hour electronic-spreadsheet conversion requirement, driving adoption of IoT temperature sensors and cloud platforms. Kelsius FoodCheck 2.0, offering FDA 21 CFR Part 11 compliance, automates HACCP refrigeration logging and provides tamperproof, timestamped digital records for EHO inspections[4]Kelsius, “Quick Service Restaurants,” Kelsius, kelsius.com. Operators report material savings from spoilage avoidance and labor reductions when refrigeration units are monitored in real time with automated alerting and standardized workflows. Predictive analytics that learn from critical control point data enable off-hours repair scheduling and a drop in unplanned downtime, which maintains menu availability and peak service stability. Global oversight bodies recognize that continuous monitoring outperforms periodic manual checks, so digital HACCP is becoming the default in multi-site chain implementations and export-oriented facilities.

Chain Standardization and Multi-Site Remote Fleet Control

Multi-unit operators benefit from centralized control of recipes, settings, maintenance alerts, and compliance dashboards that reduce manual work and variability across locations in the Smart Commercial Kitchen Appliances market. IoT-native equipment ecosystems distribute updates, log HACCP data, and expose energy-usage metrics through a single pane, which supports predictable costs and faster technician triage. Documented case studies show meaningful savings from remote updates and diagnostics, including reduced on-site visits and better-prepared service calls when truck rolls are required. At high store counts, uptime improvements and faster repair cycles compound into sales stabilization, as seen in deployments where failure incidence fell and average repair times dropped after IoT rollout. Digital checklists and exception reporting raise franchise-level compliance by flagging missed tasks in real time and consolidating corrective actions, which reduces audit failures in distributed networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex and retrofit complexity | -1.4% | Global, particularly acute for smaller operators | Short term (≤ 2 years) |

| Interoperability and standards fragmentation across brands/platforms | -1.1% | Global, with concentrated pain in multi-vendor kitchens | Medium term (2-4 years) |

| Cybersecurity, data ownership, and IT integration risks | -0.7% | Global, escalating in multi-brand chains and cloud-dependent models | Medium term (2-4 years) |

| Electrical capacity constraints in older sites limit electrification | -0.6% | North America, Europe, legacy buildings, select Asia-Pacific metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and Retrofit Complexity

Initial equipment purchases and site modifications create budget friction for smaller operators and independents, especially when floor plans must be reconfigured for robotics or higher-capacity electric loads in the smart commercial kitchen appliances market. Payback periods can stretch when deployment requires cabinetry changes, ventilation modifications, or panel upgrades to meet code and handle new duty cycles. Subscription and Robotics-as-a-Service models help some operators shift these investments into operating expense, but total cost of ownership still depends on maintenance diligence and training consistency. Older facilities face electrical capacity constraints when moving to induction or higher-wattage equipment, and integrating sensors with legacy HVAC or fire systems often requires custom gateways that add time and cost. Where building systems do not support modern protocols, BACnet or Modbus bridges can close gaps, but they introduce added complexity and require careful change control.

Interoperability and Standards Fragmentation Across Brands/Platforms

Kitchen ecosystems increasingly mix equipment from multiple OEMs, yet proprietary control stacks and dashboards can force staff to juggle several apps and portals, which erodes efficiency gains in the Smart Commercial Kitchen Appliances market. Security posture is a parallel issue because unencrypted device-to-cloud connections and under-protected APIs create exposure for recipe IP, operational logs, and payment data. Case evidence shows how misconfigurations in messaging protocols can enable long dwell-time intrusions that manipulate equipment data and exfiltrate sensitive information. Many breaches exploit unpatched firmware on legacy devices, which complicates upgrades because fixes sometimes break compatibility elsewhere in the stack. OEM programs that support open interfaces and multi-brand monitoring, such as Open Kitchen and KitchenConnect, reduce integration work and bring more devices under centralized control for diagnostics and compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Smart Cooking Appliances Lead, Yet Beverage Automation Surges on Cafe Margins

Smart cooking appliances captured 38.91% of 2025 Smart Commercial Kitchen Appliances market share, led by connected combi ovens, smart fryers with oil-management sensors, and induction solutions that meet electrification goals without sacrificing speed. The segment’s role evolves from reactive monitoring toward predictive automation as equipment self-adjusts to load variability and supports centralized recipe control across fleets. Fry stations that pair filtration with digital verification reduce waste and elevate consistency, while connected multi-cookers enable remote firmware updates that keep HACCP features aligned with changing standards. Refrigeration appliances are navigating refrigerant rules that phase out high-GWP gases, which accelerates transitions to A2L and R-290 systems and promotes supervisory controls that protect inventory with continuous temperature tracking. Smart warewashing adds automated logging and consumption optimization, with new models integrating connected assistants that support HACCP and energy alerts.

Smart beverage appliances will be the fastest-growing category at a 10.45% CAGR, as cafes and bakery chains standardize barista-quality output with bean-to-cup systems that lift peak-hour throughput and reduce training demands. Documented performance from commercial bean-to-cup systems shows large gains in drinks per hour and tight variance control that keeps quality consistent across shifts and sites. OEMs are extending data layers into beverage dispense for waste reduction and automated quality checks, which both improves margins and sustains guest experience at high transaction volumes. Refrigeration and display case connectivity aligns with food-safety logging mandates and helps reduce spoilage losses in smaller formats where a single failure can disrupt daily sales. The Smart Commercial Kitchen Appliances market continues to benefit where beverage, refrigeration, and warewashing modules operate on unified platforms that offer single-pane monitoring and push-based updates.

By Installation Type: Countertop and Compact Units Accelerate on Ghost-Kitchen and Convenience-Retail Density

Floor-standing and back-of-house systems held a 56.46% share in 2025 within the Smart Commercial Kitchen Appliances market, reflecting long-standing adoption in full-service and institutional kitchens with higher-capacity needs. Large combi ovens, blast chillers, and walk-in refrigeration remain anchors for batch-based production and banquet output, and their connectivity brings recipe control, HACCP automation, and remote diagnostics across fleets. Compact countertop units, however, are forecast to grow the fastest at a 10.83% CAGR, as ghost kitchens, forecourts, and convenience operators invest in space-efficient, ventless tools that install quickly and scale modularly. AI-vision combi ovens and modular, multi-technology platforms pack more cooking types into smaller footprints, while leasing models reduce the barrier to trial for new locations.

As digital ordering concentrates transactions during peaks, compact ventless systems help maintain service times in sites that cannot support full kitchen retrofits, and they integrate cleanly into unified dashboards for staff who rotate tasks. Efficiency standards tighten in coming years and reward smaller cavities and smarter control logic, so compact systems that coordinate with building management save energy while preserving output. For beverage and front-of-house applications, high-flow dispense controls and accurate mixture management improve speed and product quality while lowering wastage, which compounds returns in small formats. The Smart Commercial Kitchen Appliances market benefits where these compact systems integrate natively with enterprise platforms for recipe pushes and firmware updates that maintain compliance and consistency over time.

By End-User: Cafes, Bakeries, and Coffee Chains Outpace QSR Growth on Specialty-Margin Arbitrage

QSR and fast-casual chains accounted for a 32.84% share in 2025 within the Smart Commercial Kitchen Appliances market, as uniform menus and high transaction density favor connected cooking, automated oil handling, and centralized controls. Many chains have brought connected platforms into back-of-house to standardize recipes, automate HACCP data capture, and enable remote diagnostics that reduce downtime during peak hours. Cafes, bakeries, and coffee chains will grow the fastest at a 10.36% CAGR through 2031, led by beverage automation that raises consistency and reduces training time from dozens of hours to a short onboarding window for standardized recipes. Full-service restaurants deploy service robots and connected cooklines selectively to expand server coverage per shift and raise guest-satisfaction scores without diluting menu breadth. Hotels and resorts emphasize blast chilling, connected dishwashing, and integrated HACCP dashboards to manage banquet workloads at stable quality.

Institutional buyers in education and healthcare push for continuous monitoring that fits specific oversight regimes, so connected sensors and automated checklists are replacing manual temperature logs and paperwork at scale. As consumers continue to shift to digital ordering and pickup, investments extend beyond kiosks into back-of-house coordination where predictive systems align prep cadence with order inflow and reduce rework. Specialty-beverage formats prioritize equipment that encodes recipes and locks in consistency to protect margins, while front-of-house dispense controls reduce waste and keep service times short. The Smart Commercial Kitchen Appliances industry is consolidating behind OEM platforms that close the loop between prep, cooking, chilling, washing, and service for tighter compliance and better labor productivity.

By Distribution Channel: Direct OEM and D2C Gain on Subscriptions and Remote Onboarding

Dealers and distributors held 46.35% share in 2025 in the Smart Commercial Kitchen Appliances market, underpinned by installation support, financing options, and multi-brand portfolios valued by independents and small chains. Direct OEM and D2C channels are projected to grow the fastest at a 10.59% CAGR through 2031, driven by subscription models that bundle maintenance, remote updates, and compliance documentation into a simple monthly fee aligned with unit economics at the store level. Remote recipe pushes and firmware updates reduce onsite service needs, and centralized fleets gain energy, HACCP, and performance visibility across brands through open-interface platforms. As operators adopt more automation tools per site, OEM platforms that ensure firmware continuity and automated compliance reporting grow in value versus one-off devices that require separate apps.

Data-enabled services also expand through direct channels, where OEMs and partners offer insurance incentives for IoT-verified hygiene and traceability, and financing that matches lease terms to the useful life of equipment as defined by connected maintenance signals. Dealers retain advantages in complex retrofits and multi-vendor environments, especially where HVAC and building systems require BACnet or Modbus integration to connect legacy devices to centralized dashboards. Over the forecast period, the Smart Commercial Kitchen Appliances market is expected to see hybrid models where OEM direct platforms coordinate software and analytics while dealers deliver on-site integration and local service capacity at scale.

Geography Analysis

North America accounted for 32.73% of the Smart Commercial Kitchen Appliances market size in 2025, supported by large chain penetration, tighter food-safety oversight, and strong vendor ecosystems for connected kitchens. Wage pressures in key states since 2024 have further sharpened the case for automation as chains look to protect margins with predictive systems and safer, standardized workflows. Regulatory tailwinds shape purchase timing, with the region preparing for DOE efficiency compliance cycles and EPA refrigerant restrictions on high-GWP gases in new and retrofit contexts. Utilities reinforce adoption with demand-response programs that pay for load shed during events, and purpose-built solutions integrate directly into OEM platforms so multi-unit chains can monetize flexibility without adding operational risk. Canada and Mexico expand through cafe, bakery, and convenience formats that value compact connected units and IoT oversight across refrigeration, cooking, and warewashing workflows.

Asia-Pacific is projected to post the highest growth at an 11.63% CAGR, led by markets where demographic constraints and government programs push toward robotics and digital oversight. Japan continues to deploy service robots at scale in full-service and family-dining formats, which supports higher throughput and improves safety without adding back-of-house headcount. China expands investment in cloud kitchens and connected prep lines, moving toward consistent, high-volume output under software-driven coordination with centralized data layers. South Korea and India diversify demand, while Southeast Asian markets like Singapore adopt continuous monitoring for HACCP and leverage open-interface platforms to connect multi-brand fleets in small footprints. Documented Asia-Pacific deployments show large reductions in equipment failure incidence and faster repair cycles when fleets are brought under unified IoT control with edge computing for local failover.

Europe grows at a moderate pace due to high baseline automation in key countries, but evolving food-safety practices and energy standards still support replacement cycles that favor connected systems. Germany sets the tone in premium connected combi ovens and remote-fleet control, with OEM platforms that push standardized recipes, log HACCP data, and reduce on-site maintenance. OEMs in the region also integrate sustainability into manufacturing and product design, including use of low-GWP refrigerants and renewable-energy operations, which aligns with buyer priorities in public and private tenders. South America sees steady adoption in hospitality hubs, while the Middle East and Africa add capacity through hotel and food-court expansions that pair connected cooking with centralized monitoring to maintain standards at scale. Across regions, the Smart Commercial Kitchen Appliances market advances where local rebate programs, building-code changes, and data-protection regimes converge with chain strategies for standardized execution and compliance.

Competitive Landscape

The smart commercial kitchen appliances market is moderately concentrated. It features a mix of global incumbents and focused specialists, with OEMs investing in vertically integrated IoT stacks that unify cooking, chilling, washing, and beverage dispense under common data and control layers. Middleby sharpened its strategic focus in 2026 with portfolio moves and continued expansion of Open Kitchen, a platform that connects multi-brand fleets and supports remote updates, HACCP logging, and diagnostics across diverse device types. Product innovation complements software advances, with high-throughput ovens and ventless systems that compress multiple cooking modes into smaller footprints while improving energy performance. Ali Group’s portfolio strategy adds multifunction capabilities and training ecosystems that help chefs and operators adopt connected workflows faster and with less disruption to service.

Premium players build on sensor-driven autonomy and remote orchestration, using centralized platforms to distribute recipes, capture compliance data, and optimize energy across sites. Rational’s deployments document material savings from remote updates and maintenance, including fewer technician dispatches and better diagnostics before site visits. Electrolux Professional advances OnE Connected to integrate chillers, combi ovens, and dishwashers into automated HACCP workflows with energy alerts that help operators reduce avoidable consumption. Security posture is moving to the forefront as OEMs and operators confront unencrypted protocols and under-protected APIs, which creates room for zero-trust approaches and edge anomaly detection to protect recipe IP and operational data. Open interfaces and multi-brand monitoring platforms like Open Kitchen and KitchenConnect position incumbents to reduce integration friction and consolidate value around software and services.

Newer entrants emphasize cloud-native architectures and subscription models that align costs with measurable performance improvements, such as uptime, throughput, waste reduction, and verified hygiene. Cluster management for multi-device orchestration at the store level uses edge AI for low-latency control loops and centralized observability for fleet health and compliance. Partnerships around data and risk-sharing extend the value of connected systems by monetizing verified hygiene and traceability for insurance benefits and financing options. Across the forecast window, competitive intensity will favor vendors that combine reliable hardware with robust software, secure connectivity, and service models that help operators deploy, maintain, and continuously improve at fleet scale in the Smart Commercial Kitchen Appliances market.

Smart Commercial Kitchen Appliances Industry Leaders

The Middleby Corporation

Ali Group

ITW Food Equipment Group

Rational AG

Electrolux Professional AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Middleby reported Q4 2025 results, showing early progress in new ice and beverage innovations and continued success in Total Line Solutions in food processing. For 2026, Middleby projects organic growth of 1–3% in commercial foodservice and 4–6% in food processing. The company completed a 51% residential sale in Q1 2026 and plans to spin off the food processing division by Q2 2026.

- January 2026: Electrolux Professional launched the NeoBlue Touch Undercounter Dishwasher, the first in the industry to achieve accreditation under the Repairability Rating Program. This dishwasher features the MyEco cycle, which reduces energy, water, and chemical usage by 40% (260 Wh per rack) compared to earlier models, potentially saving up to 3,000 kWh per year. It also includes the OnE Connected App for HACCP compliance and a fast cycle capable of handling 65 baskets or 1,170 dishes per hour, increasing productivity by 60%.

- January 2026: Ali Group acquired JIPA, a multifunction pan manufacturer based in the Czech Republic, to expand its capabilities in electronic multifunction devices, including pressure cooking, frying, braising, grilling, and sous vide. This acquisition complements the Ali Group portfolio of over 110 brands and extends its global presence.

- December 2025: Middleby Corporation completed the sale of a 51% stake in its residential kitchen business to 26North Partners. The transaction, valued at USD 885 million, included an upfront cash payment of USD 540 million and a seller note of USD 135 million. This sale allows Middleby to focus on commercial foodservice, with an emphasis on automation and ice and beverage markets.

Global Smart Commercial Kitchen Appliances Market Report Scope

Smart commercial kitchen appliances are designed to enhance efficiency, automation, and connectivity in professional foodservice environments. The smart commercial kitchen appliances market is segmented by product type, installation type, end-user, distribution channel, and geography. By product type, the market is segmented into smart cooking appliances (including smart ovens such as combi and convection ovens, smart air fryers and fryers with open/pressure configurations and smart oil management, multi-cookers and multifunctional cookers, smart grills/griddles/induction hobs, smart ranges and cooktops, and others such as steamers and sous-vide/precision cookers), smart refrigeration appliances (commercial refrigerators and freezers), smart warewashing appliances, and smart beverage appliances (including coffee/espresso machines, tea brewers, and dispensers). By installation type, the market is segmented into countertop/compact units, floor-standing/back-of-house units, and built-in/backbar/front-of-house units. By end-user, the market is segmented into QSR and fast casual chains, full-service restaurants, cafes/bakeries and coffee chains, hotels and resorts, institutional establishments (including education, healthcare, and corporate), and others (including ghost/cloud kitchens, convenience retail and forecourt, and catering and events). By distribution channel, the market is segmented into direct OEM and dealers/distributors. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report provides the market size in USD for all the above-mentioned segments.

| Smart Cooking Appliances | Smart Ovens (combi ovens, convection ovens etc) |

| Smart Air Fryers and Fryers (Open/Pressure; smart oil management) | |

| Multi-Cookers & Multifunctional Cookers | |

| Smart Grills/Griddles/Induction Hobs | |

| Smart Ranges & Cooktops | |

| Others (Steamers & Sous-vide/Precision Cookers) | |

| Smart Refrigeration Appliances (Commercial Refrigerators and Freezers) | |

| Smart Warewashing Appliances | |

| Smart Beverage Appliances (Coffee/Espresso; Tea Brewers; Dispensers) |

| Countertop/Compact |

| Floor-standing/Back-of-house |

| Built-in/Backbar/Front-of-house |

| QSR & Fast Casual Chains |

| Full-Service Restaurants |

| Cafes/Bakeries & Coffee Chains |

| Hotels & Resorts |

| Institutional (Education, Healthcare, Corporate) |

| Others (Ghost/Cloud Kitchens, Convenience Retail & Forecourt, Catering & Events) |

| Direct OEM |

| Dealers/Distributors |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Smart Cooking Appliances | Smart Ovens (combi ovens, convection ovens etc) |

| Smart Air Fryers and Fryers (Open/Pressure; smart oil management) | ||

| Multi-Cookers & Multifunctional Cookers | ||

| Smart Grills/Griddles/Induction Hobs | ||

| Smart Ranges & Cooktops | ||

| Others (Steamers & Sous-vide/Precision Cookers) | ||

| Smart Refrigeration Appliances (Commercial Refrigerators and Freezers) | ||

| Smart Warewashing Appliances | ||

| Smart Beverage Appliances (Coffee/Espresso; Tea Brewers; Dispensers) | ||

| By Installation Type | Countertop/Compact | |

| Floor-standing/Back-of-house | ||

| Built-in/Backbar/Front-of-house | ||

| By End-User | QSR & Fast Casual Chains | |

| Full-Service Restaurants | ||

| Cafes/Bakeries & Coffee Chains | ||

| Hotels & Resorts | ||

| Institutional (Education, Healthcare, Corporate) | ||

| Others (Ghost/Cloud Kitchens, Convenience Retail & Forecourt, Catering & Events) | ||

| By Distribution Channel | Direct OEM | |

| Dealers/Distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the Smart Commercial Kitchen Appliances market growth outlook to 2031?

The Smart Commercial Kitchen Appliances market size is projected to increase from USD 11.57 billion in 2026 to USD 18.85 billion by 2031 at a 10.26% CAGR, driven by labor constraints, compliance requirements, and energy-efficiency initiatives.

Which product categories are leading and growing fastest?

Smart cooking appliances led with 38.91% share in 2025, while smart beverage appliances are expected to grow the fastest at a 10.45% CAGR as cafes and bakeries standardize barista-quality output.

Which installation types will see the highest growth?

Countertop and compact units are forecast to grow the fastest, at a 10.83% CAGR, as ghost kitchens, forecourts, and convenience operators favor space-efficient, ventless, plug-and-play systems.

Which end users are adopting connected equipment the fastest?

Cafes, bakeries, and coffee chains are set to record a 10.36% CAGR through 2031, supported by beverage automation that improves consistency and reduces training time.

How are regulations influencing buying decisions?

FSMA 204’s electronic traceability rules and EPA refrigerant phase-outs are accelerating adoption of connected systems that support digital HACCP, low-GWP refrigerants, and energy optimization.

Which regions will lead growth?

Asia-Pacific is projected to post the highest growth at 11.63% CAGR, led by Japan’s large-scale robotics adoption and broader regional investments in connected kitchen platforms.

Page last updated on: