Smart Cards In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 12.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Cards In Healthcare Market Analysis by Mordor Intelligence

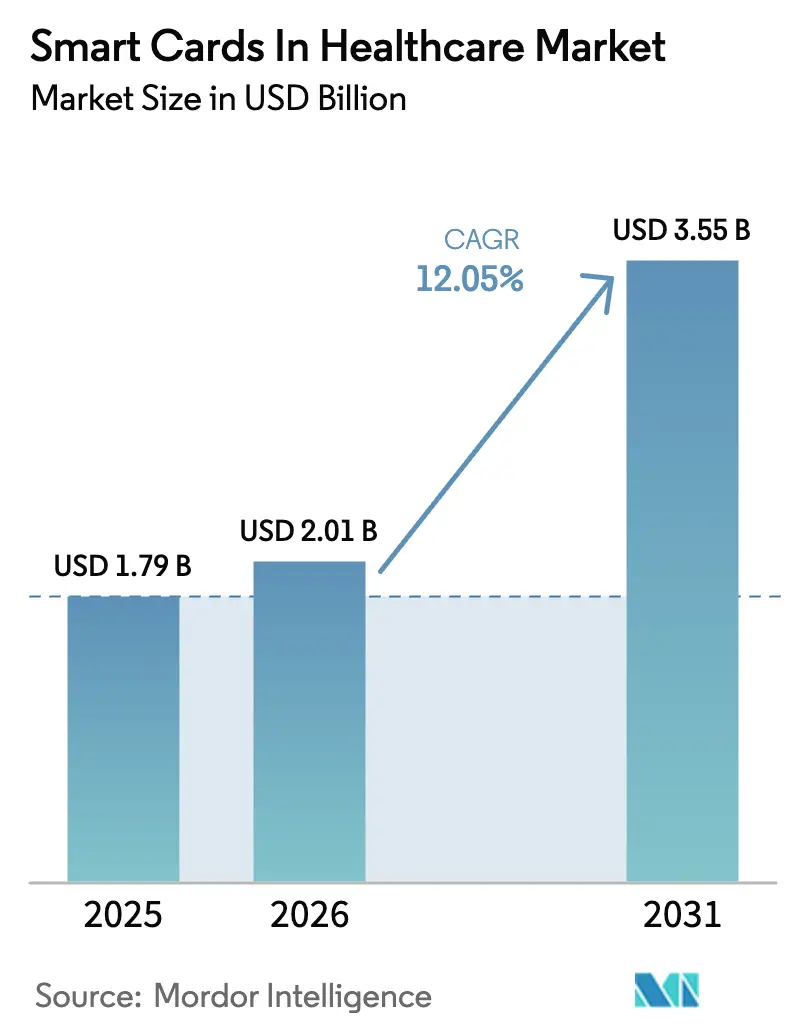

Smart Cards In Healthcare Market size in 2026 is estimated at USD 2.01 billion, growing from 2025 value of USD 1.79 billion with projections showing USD 3.55 billion, growing at 12.05% CAGR over 2026-2031.

The transition from paper credentials to hardware-backed identity systems, widespread regulatory mandates for multi-factor authentication, and demand for post-pandemic contactless workflows form the structural backbone of this growth. Hospital groups now budget specifically for cryptographic patient and staff credentials, and vendors are locking in multi-year supply contracts that blend card issuance with lifecycle management services. Regional dynamics are shifting as Asia-Pacific accelerates population-scale eHealth card rollouts, Europe localizes secure-element manufacturing, and North America upgrades legacy infrastructure in response to federal interoperability rules.

Key Report Takeaways

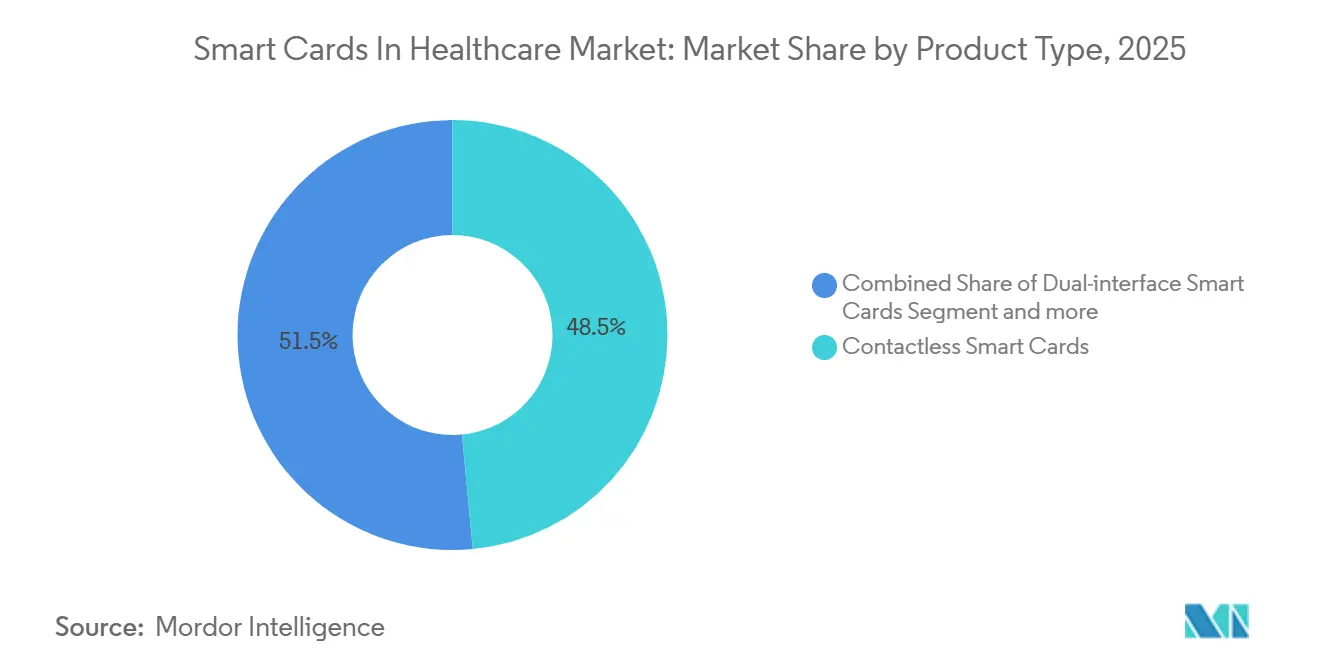

- Contactless smart cards led with 48.55% Smart Cards in Healthcare market share in 2025. Dual-interface smart cards are advancing at a 13.25% CAGR, the fastest among product types, through 2031.

- Microcontroller-based cards captured 62.23% of the Smart Cards in Healthcare market size in 2025. The microcontroller segment is forecast to expand at a 13.15% CAGR between 2026 and 2031.

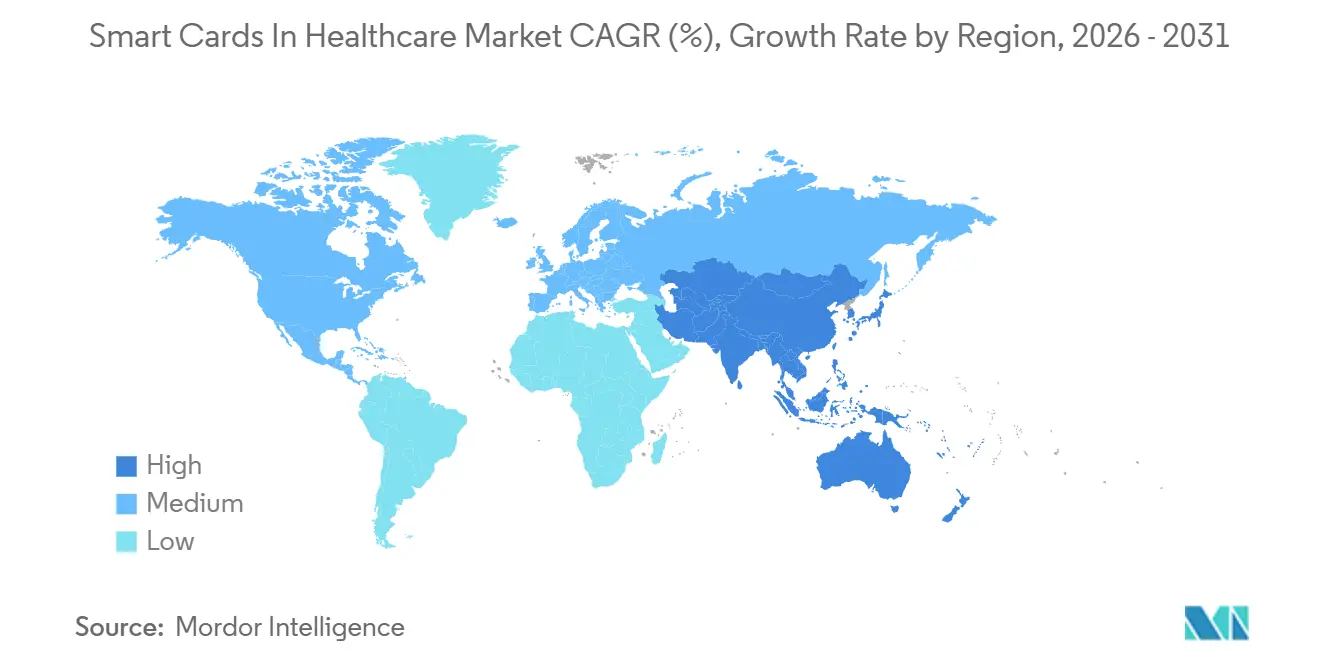

- North America accounted for 42.25% regional share of the Smart Cards in Healthcare market in 2025, while Asia-Pacific is tracking a 12.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Cards In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government eHealth card programs (EU, Asia) | +3.2% | Asia-Pacific core, Europe, spillover to Middle East & Africa | Long term (≥ 4 years) |

| Shift to contactless workflows post-COVID-19 | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rising medical identity theft & fraud prevention needs | +2.1% | North America, Europe | Medium term (2-4 years) |

| EHR integration mandates | +1.9% | Global, led by North America & EU | Long term (≥ 4 years) |

| Dual-interface cards powering disposable smart patches | +1.5% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| On-card AI accelerators enabling offline triage | +1.2% | Asia-Pacific, Middle East & Africa, rural/remote areas globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government eHealth Card Programs Accelerate Population-Scale Deployments

National smart-card programs in China, Japan, and the Philippines have turned billions of citizens into active users of secure hardware credentials, creating predictable, multi-year demand for cards, personalization services, and PKI middleware. China’s electronic social security card surpassed 1 billion users by mid-2024, handling more than 15 billion annual service transactions through 24,000 hospitals and 60,000 pharmacies. Japan switched entirely to the My Number ID system in December 2024, eliminating paper insurance cards and unifying authentication workflows nationwide. The Philippines added secure digital ID services in June 2024, reducing enrollment fraud in public health programs. European Union policy updated in April 2025 requires Member States to support secure electronic identification under the European Health Data Space, reinforcing card demand across 27 countries. These deployments send long-term demand signals to secure-element suppliers and card bureaus.

Shift to Contactless Workflows Post-COVID-19 Drive Interface Upgrades

Hospitals accelerated contactless check-in, payment, and prescription-pickup processes to cut surface-borne infection risk. Dual-interface cards solve the retrofit challenge by retaining contact pads for back-office readers while enabling NFC taps at kiosks and mobile terminals. NIST updated Digital Identity Guidelines in August 2024 to highlight hardware authenticators that resist phishing, a specification satisfied by contactless smart-card protocols[1]Boutin C., “NIST Releases Second Public Draft of Digital Identity Guidelines,” nist.gov. Infineon’s August 2025 healthcare brochure showcases NFC secure elements that authenticate staff and pair medical devices without touching shared surfaces. The tap-and-go model is now embedded in outpatient pharmacy chains, where transaction speed directly improves throughput.

Rising Medical Identity Theft Amplifies Demand for Cryptographic Credentials

The HHS breach report, published in February 2024, attributes many large incidents to compromised log-ins, citing inadequate multi-factor authentication under HIPAA. Smart cards that house non-extractable keys and enforce PIN or biometric match mitigate these attack vectors. The Pew Charitable Trusts emphasized hardware credentials combined with biometrics to curb patient mismatches and fraudulent billing. With stolen health records fetching USD 50 each on illicit markets, hospital CFOs are green-lighting smart-card projects as cost-effective risk controls.

EHR Integration Mandates Formalize Authentication Standards

The U.S. Trusted Exchange Framework and Common Agreement, finalized in December 2024, compels Qualified Health Information Networks to adopt multi-factor authentication and certificate life-cycle governance aligned with PKI hardware tokens. ONC’s HTI-2 proposed rule from July 2024 references hardware authenticators for API security, nudging EHR vendors toward smart-card compatibility. China’s National Health Commission and the National Administration of Traditional Chinese Medicine likewise require unified patient IDs and authenticated e-signatures, functions enabled by card-resident keys. Compliance deadlines translate into capital budgets earmarked for card issuance and reader rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High infrastructure upgrade costs for legacy hospitals | -1.8% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Competition from mobile-ID & digital-wallet apps | -1.5% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Data-privacy compliance complexity (GDPR, HIPAA) | -1.3% | North America, Europe | Medium term (2-4 years) |

| Supply-chain volatility for secure microcontrollers | -0.9% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Infrastructure Upgrade Costs Constrain Legacy Hospital Adoption

Replacing mag-stripe readers, installing PKI servers, and training staff push smart-card project costs beyond the capital budgets of rural and community hospitals. The European Commission’s Health at a Glance 2024 highlights fragmented technical standards and budget gaps that slow cross-border credential adoption[2]European Commission, “Health at a Glance: Europe 2024,” europa.eu. Smaller U.S. hospitals often defer hardware tokens in favor of smartphone-based single sign-on because the latter piggybacks on existing Wi-Fi networks.

Competition from Mobile-ID and Digital-Wallet Apps Pressures Physical Card Demand

The European Digital Identity Wallet initiative positions phone-resident credentials as full substitutes for plastic cards, eroding new-card issuance volumes in digitally savvy urban populations. IDEMIA’s January 2025 launch of remote biometric card enrollment underscores the vendor pivot toward hybrid physical-plus-mobile offerings. Card makers now hedge by bundling NFC cards with matching wallet credentials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-Interface Cards Bridge Legacy and Mobile Ecosystems

Contactless smart cards held 48.55% Smart Cards in Healthcare market share in 2025, reflecting their dominance in quick-tap registration desks and pharmacy counters. Yet the dual-interface segment is on track to register a 13.25% CAGR through 2031, outpacing all other product types. Hospitals prefer dual-interface because it works with existing contact readers while enabling NFC at bedside tablets. This hybrid support reduces the total cost of reader refresh cycles. Vendors such as NXP introduced the NTAG X-DNA family in February 2025, featuring AES countermeasures to combat cloning in high-throughput outpatient settings. During the forecast window, twin pressures of infection control and mobile-first clinical workflows will drive dual-interface card penetration deeper into nurse-administered point-of-care routines. Contact-only cards will persist in highly regulated inpatient pharmacies that still rely on sealed contact terminals certified for drug-dispensing audit trails. Hybrid cards combining mag-stripe, contact, and contactless layers will occupy niche roles where insurance reimbursement kiosks continue to demand magnetic swipes, but their higher bill-of-materials cost will cap growth.

Looking forward, dual-interface shipments will account for a growing slice of the Smart Cards in Healthcare market size, particularly as reader manufacturers embed ISO 14443 antennas into new all-in-one workstations. Pilot programs pairing dual-interface ID cards with disposable infusion-pump patches demonstrate how a single credential can authenticate both the patient and the medication delivery device in one tap. As more clinical mobile apps support card-over-NFC login, physicians will carry one credential that services both the legacy desktop EHR and the ward’s iPad-based order entry.

By Component: Microcontroller-Based Cards Dominate Cryptographic Workloads

Microcontroller smart cards captured 62.23% of the Smart Cards in Healthcare market size in 2025, underlining the sector’s preference for on-card cryptography. The segment’s forecast 13.15% CAGR is a direct result of NIST SP 800-63B requirements for phishing-resistant, hardware-bound private keys. Memory cards, which only store data, cannot sign transactions or host FIPS-validated encryption engines, limiting their role to low-risk visitor passes. Secure microcontrollers like NXP’s EdgeLock SE05x integrate ECC, RSA, and true random number generators, enabling digital signature of electronic prescriptions and audit log entries. Hospitals deploying zero-trust network architectures increasingly bind each clinician’s smart card to workstation certificates, leveraging the microcontroller’s on-chip attestation to authorize device access.

The migration toward software-as-a-service EHRs is also boosting microcontroller demand because cloud hosts require client-side certificate authentication for privileged API calls. With private keys locked in silicon, risk officers gain higher assurance that credentials cannot be exfiltrated by malware. In emerging markets, donor-funded immunization programs adopt microcontroller cards to store childhood vaccine histories securely, ensuring verifiable evidence even in clinics lacking connectivity. As artificial-intelligence-enabled triage models begin running directly on card silicon, compute-capable secure elements will further distance themselves from simple memory-card alternatives.

Geography Analysis

North America commanded 42.25% of the Smart Cards in Healthcare market in 2025 owing to federal interoperability mandates and high per-capita IT spending. The December 2024 TEFCA final rule formalized certificate-based authentication across nationwide exchange networks, prompting immediate reader refresh cycles in integrated delivery systems. Updated NIST guidelines in July 2025 reinforced the hardware-token imperative for phishing resistance. Growth continues, but capital budgets in community hospitals remain tight, slowing full penetration.

Asia-Pacific is the standout growth engine, set to record a 12.82% CAGR through 2031. China alone added hundreds of millions of electronic social security card users in 2024, with 6 billion insurance settlement transactions processed via credential scans. Japan’s My Number adoption and India’s Ayushman Bharat digital mission expand the addressable base dramatically. The Philippines and Indonesia allocate budget to rural clinics for card issuance kiosks, while Australia experiments with blockchain-anchored credential registries that rely on card-generated keys for signature submissions. Vendor localization—STMicroelectronics partnering FAB plants in Singapore and Malaysia—shortens supply routes, further catalyzing adoption.

Europe retains solid share as large Member States—Germany, France, Italy—continue national eHealth card rollouts. The April 2025 European Health Data Space regulation mandates cross-border recognition of professional and patient credentials, effectively standardizing card specifications across the bloc. IDEMIA’s EUR 20 million Vitré plant and its joint venture with GlobalFoundries promise a sovereign supply chain by 2026, easing security-of-supply concerns[3]IDEMIA, “IDEMIA Secure Transactions pledges to a sovereign European value chain,” idemia.com. However, heterogeneous funding models and mobile wallet pilots in Scandinavia temper new-card volume growth.

Competitive Landscape

The Smart Cards in Healthcare market exhibits moderate concentration. IDEMIA, NXP, Thales, Infineon, and STMicroelectronics anchor the top tier, leveraging vertical integration from chip design through personalization bureaus. IDEMIA’s partnership with GlobalFoundries secures European chip supply and appeals to governments prioritizing digital sovereignty. NXP’s NHS52S04 microcontroller targets wearable medical devices, giving the company an edge in growing patch-based therapy niches. Thales’ May 2024 win in Mauritius ties digital national identity to a mobile wallet, signaling vendor readiness to deliver blended card-and-wallet ecosystems.

Mid-tier players chase specialization. SecureKey focuses on federated identity middleware, while CardLogix supplies white-label card operating systems optimized for low-cost public-insurance programs. Mobile-wallet disruptors such as Apple Health Records and Google Wallet integrate verifiable credentials, threatening card issuance volumes among tech-savvy populations. Incumbents respond by bundling card applets with wallet credentials to preserve account control.

Component suppliers pursue co-design initiatives: ST integrates GlobalPlatform profiles with IDEMIA operating systems, and Infineon collaborates with reader makers to ship reference designs certified to both ISO 14443 and FIPS 140-3. Competitive edge hinges on achieving Common Criteria EAL5+ or higher and aligning with country-specific cryptographic suites. No single vendor exceeds 30% revenue share, leaving room for regional champions to win public tenders.

Smart Cards In Healthcare Industry Leaders

Thales DIS (Gemalto)

HID Global

Infineon Technologies AG

NXP Semiconductors

Giesecke+Devrient

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Centers for Medicare & Medicaid Services adopted a QR-code workflow that lets patients share full medical histories with a single scan at check-in.

- July 2025: All India Institute of Medical Sciences began the national rollout of its “One AIIMS, One Card” smart-payment credential, expanding beyond the pilot at AIIMS Delhi.

Global Smart Cards In Healthcare Market Report Scope

As per the scope of the report, smart cards in healthcare are specialized plastic cards embedded with integrated circuits (microchips) that store and process patient information securely. They are used to efficiently manage and access medical records, insurance details, and other healthcare-related data, enhancing security, accuracy, and convenience in healthcare services.

The segmentation for the Smart Cards in Healthcare Market is categorized by product type, component, and geography. By product type, the market includes hybrid smart cards, contactless smart cards, contact-based smart cards, and dual-interface smart cards. By component, it is divided into memory-card based smart cards and microcontroller based smart cards. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Hybrid Smart Cards |

| Contactless Smart Cards |

| Contact-based Smart Cards |

| Dual-interface Smart Cards |

| Memory-card Based Smart Cards |

| Microcontroller Based Smart Cards |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hybrid Smart Cards | |

| Contactless Smart Cards | ||

| Contact-based Smart Cards | ||

| Dual-interface Smart Cards | ||

| By Component | Memory-card Based Smart Cards | |

| Microcontroller Based Smart Cards | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the Smart Cards in Healthcare market expected to grow between 2026 and 2031?

It is projected to expand at a 12.05% CAGR, rising from USD 2.01 billion in 2026 to USD 3.55 billion in 2031.

Which product type is gaining the most momentum?

Dual-interface cards are the fastest-growing segment, posting a 13.25% CAGR through 2031.

Why are microcontroller-based cards preferred over memory cards?

They house on-chip cryptographic engines and non-extractable keys, meeting NIST SP 800-63B requirements for phishing-resistant multi-factor authentication.

What region offers the highest growth opportunity?

Asia-Pacific, led by China and Japan, is forecast to record a 12.82% CAGR through 2031.

What is the biggest restraint to adoption in legacy hospitals?

High upfront costs for card readers, PKI infrastructure, and staff training slow deployments, especially in resource-constrained facilities.

Are mobile wallets eliminating the need for physical cards?

Mobile credentials are gaining traction, but hospitals still rely on physical smart cards for offline authentication and compatibility with existing contact readers, so hybrid card-plus-wallet models dominate current procurement.

Page last updated on: