Small Molecule API Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 182.88 Billion |

| Market Size (2031) | USD 250.26 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Molecule API Market Analysis by Mordor Intelligence

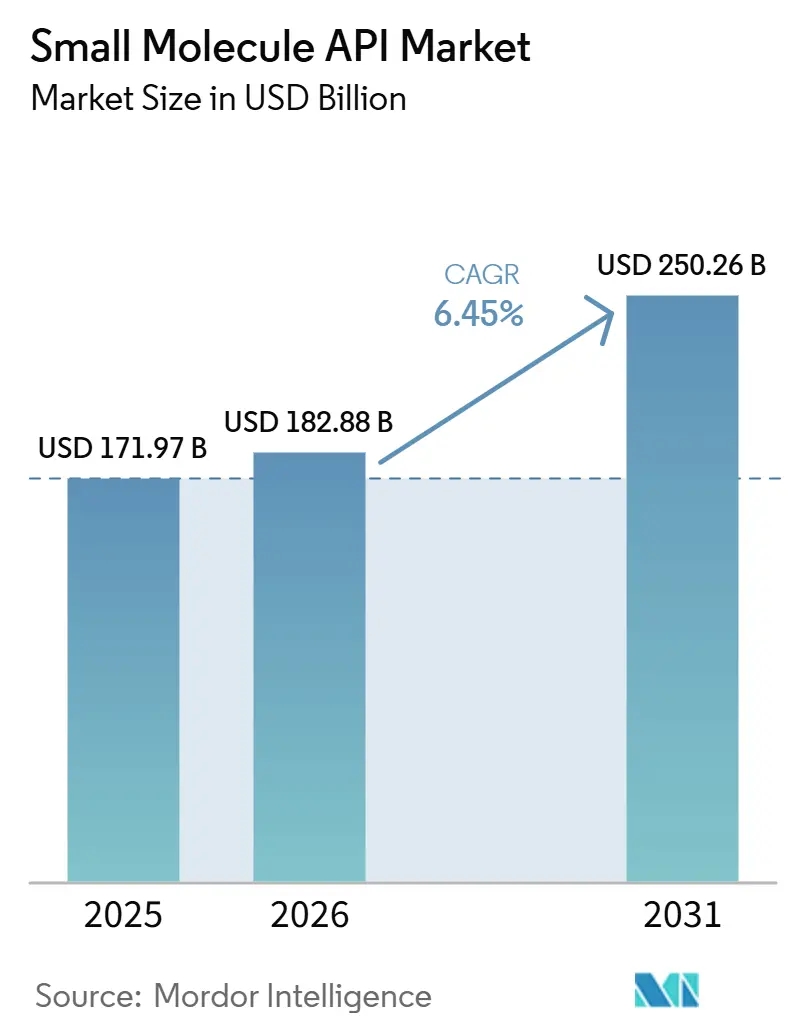

The Small Molecule API Market size is expected to increase from USD 171.97 billion in 2025 to USD 182.88 billion in 2026 and reach USD 250.26 billion by 2031, growing at a CAGR of 6.45% over 2026-2031.

Demand in the Small molecule API market is being supported by a larger chronic disease burden, especially in cancer care, where annual new cases were 20.6 million on a 2024 base and are projected to approach 35 million by 2050.[1]World Health Organization, “WHO Calls for Urgent Action as New Cancer Cases Are Projected to Nearly Double by 2050,” WHO News, who.int A broad loss of exclusivity cycle in major therapies is also widening generic production requirements, which keeps order visibility firm for qualified suppliers in the Small molecule API market. Sponsor companies are also relying more on CDMOs to avoid heavy fixed investment and to scale capacity in line with clinical and commercial milestones, which is reinforcing outsourcing demand in the Small molecule API market. Growth is still being tempered by tighter impurity controls and feedstock volatility, both of which are shifting buyer preference toward suppliers with stronger quality systems, better solvent access, and more resilient procurement networks. This setting is creating room in the Small molecule API market for companies that can combine complex chemistry, regulated-market compliance, and targeted capacity additions in strategic locations.

Key Report Takeaways

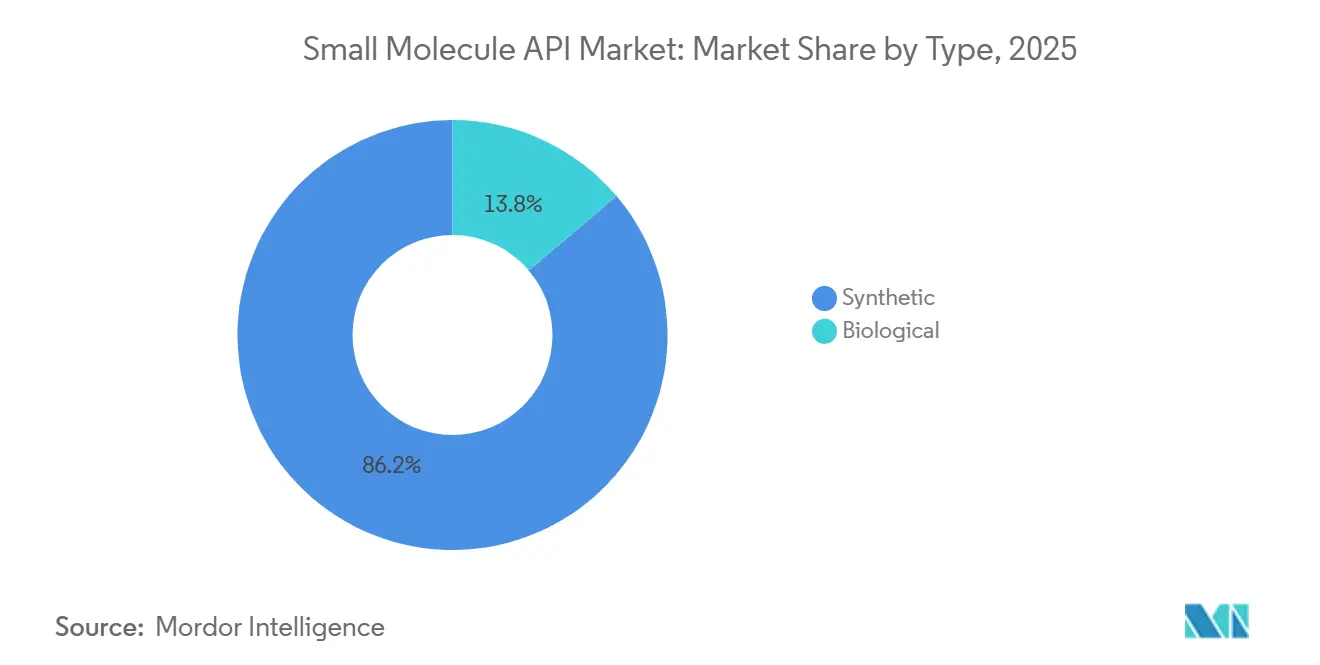

- By type, synthetic APIs held 86.18% share in 2025, while biological APIs are projected to expand at 7.83% CAGR from 2026 to 2031.

- By manufacturer, in-house production accounted for 63.18% share in 2025, while outsourced manufacturing is projected to grow at 8.15% CAGR from 2026 to 2031.

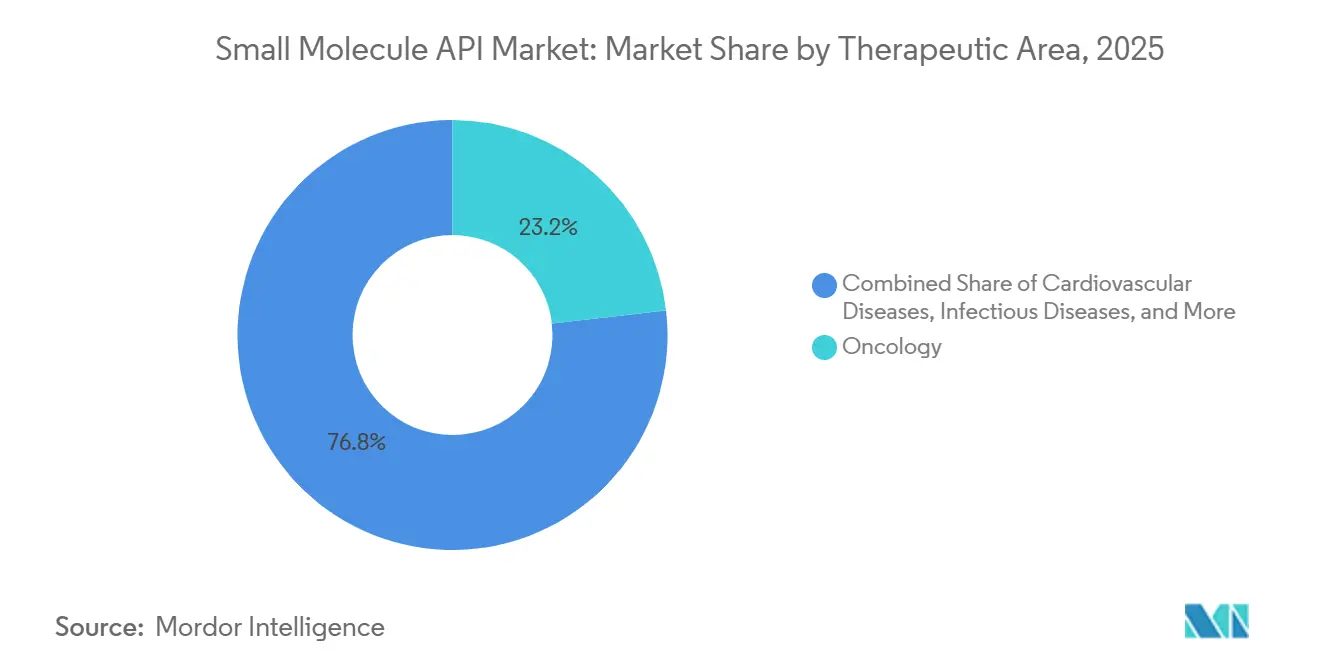

- By therapeutic area, oncology captured 23.18% share in 2025 and is also projected to advance at 8.76% CAGR from 2026 to 2031.

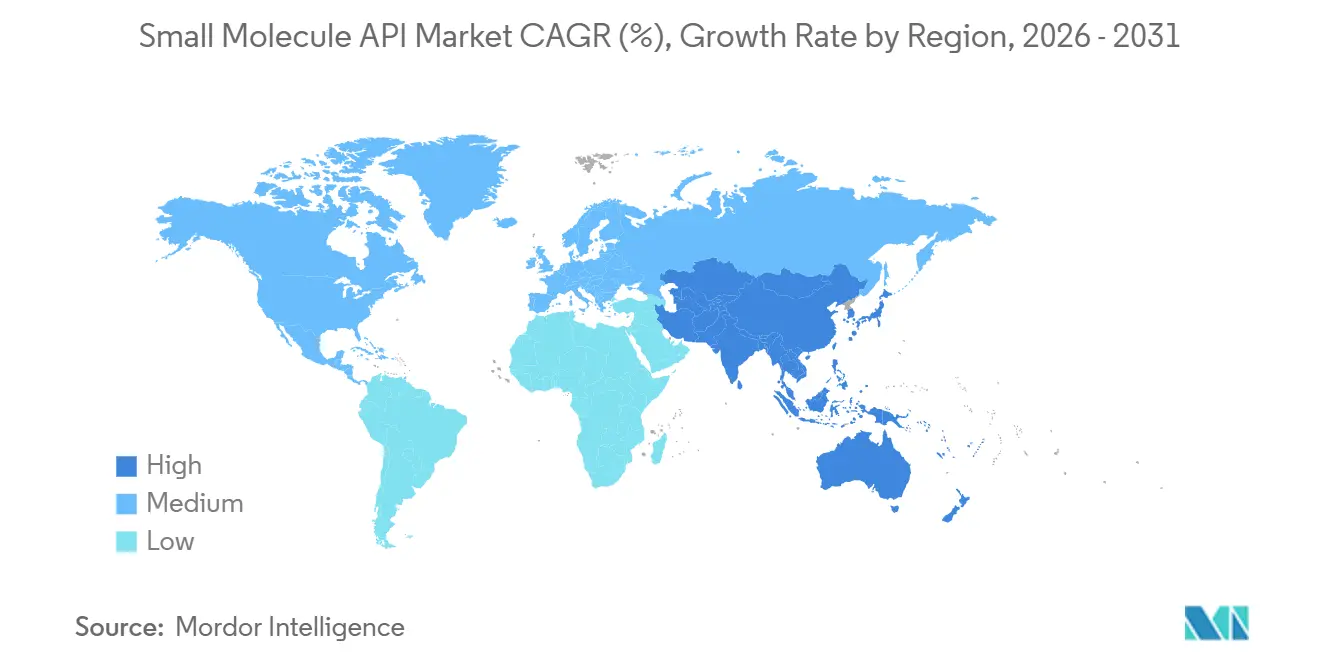

- By geography, Asia-Pacific represented 47.18% share in 2025 and is projected to grow at 8.43% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Small Molecule API Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Burden and Long-Term Therapy Volumes | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Patent Expiries and Generic Substitution Cycles | +1.5% | Global, with India and Europe as primary beneficiaries | Short term (≤ 2 years) |

| Outsourcing Shift Toward CDMOs for Cost and Capacity Flexibility | +1.3% | Global, with North America and Europe leading sponsor base | Medium term (2-4 years) |

| Expansion of High Potency and Complex Small Molecule Pipelines | +0.9% | North America, Europe, and China-linked export flows | Long term (≥ 4 years) |

| Friend-Shoring of Critical API Capacity and Dual-Sourcing Programs | +0.7% | North America, Europe, India, and select Southeast Asian hubs | Medium term (2-4 years) |

| Continuous Manufacturing and Inline Analytics Improving Batch Economics | +0.5% | North America and Europe, with early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden and Long-Term Therapy Volumes

The Small molecule API market is benefiting from a steady rise in chronic disease treatment needs across oncology, cardiometabolic care, and long-duration maintenance therapies. Longer treatment duration matters as much as rising diagnosis volume, because products used over many months or years create recurring API demand rather than short refill cycles. This supports the Small molecule API market because approved therapies in targeted oncology and chronic cardiometabolic care tend to hold predictable replenishment patterns once adoption broadens. It also favors manufacturers with established regulatory files and dependable scale, since buyers usually prefer proven supply continuity when treatment duration is long.

Patent Expiries and Generic Substitution Cycles

The Small molecule API market is entering a favorable period for generic supply preparation as a larger set of established small molecule drugs moves closer to loss of exclusivity. That process tends to increase API qualification activity, filing work, and commercial supply planning well before the first generic launch. India is well-positioned in this cycle, with API exports reaching INR 41,500 crore, or USD 4.88 billion, in FY2025 and exceeding the country’s pharmaceutical imports for the first time.[2]Economic Times Pharma, “India’s Exports of Active Pharma Ingredients at Rs 41,500 Cr Surpassed Imports in FY25,” Economic Times, economictimes.indiatimes.com The effect on the Small molecule API market is broader than a simple volume increase, because generic entry also brings new sourcing bids, second-source qualification work, and tighter lead-time expectations from formulators. Suppliers that already have compliant processes, raw material access, and filing readiness are therefore in a stronger position to capture this wave.

Outsourcing Shift Toward CDMOs for Cost and Capacity Flexibility

The outsourcing case in the Small molecule API market remains strong because many sponsors want variable manufacturing costs instead of fixed plant ownership. This is especially relevant for emerging biotechs and mid-size innovators that need clinical to commercial scale-up without carrying the full capital and compliance burden of an internal API site. DCAT Value Chain Insights noted in 2026 that client interest in rebuilding selected in-house capability has become a key issue for CDMOs, which is pushing outsourcing relationships toward deeper development and supply partnerships rather than simple transactional work. Lonza’s H1 2025 results support that demand pattern, with its Advanced Synthesis business posting 18.3% CER sales growth and a 40.3% CORE EBITDA margin. In the Small molecule API market, this still leaves room for outsourced growth because many customers are choosing dual sourcing and specialist partnerships instead of full backward integration.

Expansion of High Potency and Complex Small Molecule Pipelines

The Small molecule API market is also gaining from a larger mix of high potency and technically demanding programs, especially in oncology-linked development. These projects often require high-containment suites, multi-step synthesis control, and analytical depth that generalist facilities cannot provide at the same standard. Lonza expanded HPAPI capacity at Visp and added commercial-scale payload-linker capability in June 2026, which shows continued investment behind specialized manufacturing demand. Asymchem also launched its OEB5 HPAPI manufacturing facility in Sandwich, UK, in June 2026, adding another example of capacity moving toward high-containment and commercial-ready execution. In the Small molecule API market, this shift supports suppliers that can handle difficult chemistry, safety requirements, and regulated documentation in one operating model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nitrosamine, Impurity, and Traceability Compliance Burden | -0.6% | Global, with FDA and EMA jurisdictions most affected | Medium term (2-4 years) |

| High Containment, Solvent Recovery, and Waste Treatment Capex | -0.5% | Global, with European Union environmental directives most stringent | Long term (≥ 4 years) |

| Feedstock and Solvent Supply Volatility | -0.8% | India, Asia-Pacific, and global logistics corridors | Short term (≤ 2 years) |

| Tender-Led Generic Pricing Pressure in Large Volume APIs | -0.7% | Europe and select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nitrosamine, Impurity, and Traceability Compliance Burden

The Small molecule API market faces a clear restraint from tighter impurity control, especially where nitrosamine risk assessment and traceability requirements are expanding. The FDA updated its nitrosamine impurity guidance in June 2025 and required manufacturers to provide confirmatory testing progress updates by August 1, 2025. The EMA also maintains a detailed framework for managing nitrosamine impurities, which means companies serving multiple regulated markets must sustain broad documentation, analytical, and process review efforts. In the Small molecule API market, these requirements increase cost even before a product change reaches commercial scale, because suppliers must review formation pathways, method suitability, and downstream specifications together. Older batch assets are more exposed where contamination pathways are harder to control, which gradually shifts competitiveness toward plants with newer systems and better process visibility.

Feedstock and Solvent Supply Volatility

Feedstock and solvent volatility remains a direct cost and continuity problem for the Small molecule API market. Deutsche Welle reported in 2026 that conflict in West Asia pushed pharmaceutical-grade solvent prices up by 20% to 30% within weeks, while paracetamol API prices in India more than doubled at the tightest point. Pharmexcil also urged the Indian government to ensure allocation of key petrochemical inputs such as propylene, methanol, ammonia, and butane after inventories tightened across the supply chain. This matters in the Small molecule API market because solvent spikes move quickly into production economics, yet tender-based supply contracts often limit the ability to pass those costs through in time. The result is margin pressure on high-volume generic APIs and a higher risk that some producers step back from low-return product lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Synthetic Scale Still Dominates, While Biological APIs Add the Faster Growth Layer

Synthetic APIs accounted for 86.18% of the Small molecule API market in 2025, which shows how deeply established chemical synthesis remains across cardiovascular, anti-infective, CNS, and metabolic therapies. This category benefits from mature regulatory pathways, broad plant availability, and cost structures that fit large generic and branded volumes. Biological APIs, which include semi-synthetic fermentation-based routes and bio-transformation processes, are forecast to expand at 7.83% CAGR from 2026 to 2031. That makes them the faster-moving complement inside the Small molecule API market, especially where oncology-linked derivatives and more specialized process routes are becoming more relevant.

The split is not purely a volume issue, because many newer programs use a mix of synthetic and biologically assisted steps rather than one route alone. That favors companies that can combine process chemistry, biocatalysis, and analytical control in one development chain. The FDA’s increasing attention to advanced manufacturing methods and the continued regulatory push around process consistency are also raising the execution standard for both categories in the Small molecule API market. Over time, synthetic dominance is likely to stay intact on value share, but the faster expansion of biological APIs should keep the segment mix gradually moving toward more specialized manufacturing content.

By Manufacturer: In-House Control Remains Larger, but Outsourcing Is Expanding Faster

In-house manufacturing represented 63.18% of the Small molecule API market share in 2025, reflecting the continued preference of major pharmaceutical companies to retain control over critical molecules, supply security, and intellectual property. This remains most relevant for large companies with broad commercial portfolios and the balance sheet to support dedicated internal capacity. Pfizer’s USD 465 million investment in Kalamazoo, Michigan, shows that strategic internal production still matters where reliability and controlled execution are central priorities.[3]Pfizer CentreOne, “Pfizer Expands Its Major Manufacturing Network in Kalamazoo, Michigan,” Pfizer CentreOne, pfizercentreone.com Even so, the outsourced side of the Small molecule API market is projected to grow at 8.15% CAGR from 2026 to 2031, which is the faster pace between the two models.

That growth is being supported by biotech sponsors, virtual pharma companies, and mid-size innovators that need development flexibility more than asset ownership. In 2026, DCAT Value Chain Insights described internal build interest as a real issue for CDMOs, yet the more common sponsor response has still been dual sourcing rather than full insourcing. Trade and supply security concerns are also increasing qualification work for U.S.-based and friend-shored production, which helps outsourced providers with regulated-market capacity and stronger location profiles. In the Small molecule API market, this leaves a structure where in-house scale stays larger, while outsourcing captures more of the incremental project flow.

By Therapeutic Area: Oncology Holds the Largest Share and the Fastest Growth Rate

Oncology accounted for 23.18% of the Small molecule API market size in 2025 and is projected to grow at 8.76% CAGR from 2026 to 2031. This dual lead is notable because large, mature segments do not always remain the fastest-growing parts of the revenue mix. In the Small molecule API market, oncology demand is being reinforced by the depth of targeted therapy development and by wider use across earlier treatment settings. The same treatment area also benefits from a steady need for high-value, tightly controlled chemistry, which supports both revenue intensity and long-term manufacturing commitment.

Cardiovascular, CNS, neurology, and metabolic disorders still represent large volume anchors because many therapies in these categories are taken over long periods. Infectious diseases and respiratory products tend to show more pricing sensitivity, especially where tender systems and stewardship measures reduce flexibility on older molecules. Smaller categories such as nephrology, ophthalmology, dermatology, urology, orthopedics, and endocrinology add steadier specialty demand rather than outsized share concentration. Across the Small molecule API market, this creates a therapeutic mix where high-volume chronic care protects the base and oncology keeps raising the growth ceiling.

Geography Analysis

Asia-Pacific held 47.18% of the Small molecule API market share in 2025 and is projected to grow at 8.43% CAGR from 2026 to 2031. China remains central to regional manufacturing depth, while India is strengthening its export and domestic substitution role within the Small molecule API market. India’s bulk drug PLI scheme had commissioned 38 projects across 28 notified products by December 2025, with cumulative sales of INR 2,720 crore, or USD 319 million. The same government update stated that 191 APIs, key starting materials, and drug intermediates were being produced domestically for the first time under the scheme. India also recorded API exports of INR 415.0 billion (~USD 4.88 billion) in FY2025, which marked the first year exports surpassed pharmaceutical imports.

North America remains a critical sponsor and sourcing region for the small-molecule API market because development decisions, regulatory oversight, and commercial qualification activity remain deeply concentrated there. Proposed U.S. tariff measures and broader supply security concerns are accelerating interest in domestic and friend-shored API capacity. Cambrex responded with a USD 120 million plan for a new large-scale API plant in Charles City, Iowa, with groundbreaking scheduled for late 2026.

Europe remains the second major regional base in the Small molecule API market, supported by a mature ecosystem across Germany, the United Kingdom, France, Italy, and Spain. The European Union is pushing supply resilience through policy support, and EUROAPI secured up to EUR 140 million, or USD 154 million, in public aid under the France 2030 plan for three innovation programs tied to pharmaceutical sovereignty. At the same time, Medicines for Europe documented long-term price stagnation and decline in generic medicines across many member states, which limits the cash available for resilience investment.

Competitive Landscape

The Small molecule API market remains moderately fragmented at the global level, with a mix of captive pharmaceutical manufacturers, dedicated CDMOs, and generic API specialists competing on different value propositions. Large pharmaceutical companies such as AbbVie, Pfizer, Bristol-Myers Squibb, and Boehringer Ingelheim retain important internal manufacturing positions. At the same time, Lonza, Cambrex, Siegfried, EUROAPI, Divi’s Laboratories, Aurobindo Pharma, Asymchem, and WuXi Chemistry serve broader third-party demand. Competition in the Small molecule API market is increasingly shaped by location strategy, complex chemistry capability, and the ability to move from development support to commercial supply without regulatory disruption. That is why many companies are adding capacity in regulated markets instead of relying on a single-country manufacturing model. It also explains why high-containment assets, payload-linker capability, and stronger documentation systems are becoming more important competitive filters.

Recent strategic moves show how suppliers are responding. Lonza expanded HPAPI payload-linker manufacturing at Visp in June 2026, which strengthens its position in integrated ADC-related supply. Cambrex advanced both its new Iowa plant and its Milan site expansion in March 2026, adding scale in the United States and more analytical and process development capability in Europe. Siegfried also obtained antitrust clearance in March 2026 for the acquisition of three small-molecule drug substance sites in the United States and Australia, which broadens its controlled substance and clinical API footprint.

The competitive gap is widening between suppliers that can handle specialized projects and those that remain focused on standard commodity volumes. WuXi AppTec reported in 2025 that its small molecule D&M pipeline included 3,430 molecules, with 80 commercial projects and 87 Phase III projects, which shows how scale and project depth can reinforce future positioning. In the Small molecule API market, buyers are likely to keep rewarding providers that combine quality compliance, dual-source readiness, and technical breadth across high-potency, controlled, and specialized chemistries. Smaller producers can still compete effectively in the small-molecule API market, but the strongest pricing power remains with companies that offer proven regulatory execution and broader service integration.

Small Molecule API Industry Leaders

Aurobindo Pharma Ltd.

Cambrex Corporation

Divi’s Laboratories Limited

Lonza Group AG

Siegfried Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Lonza expanded HPAPI payload-linker manufacturing capacity at its Visp, Switzerland site by adding new commercial-scale capabilities within an existing GMP facility, reinforcing its position as a fully integrated CDMO in the ADC space. The investment adds dedicated purification suites and analytical laboratories designed for multipurpose, scale-out payload-linker production.

- March 2026: Cambrex completed initial engineering studies for a new USD 120 million large-scale API manufacturing plant in Charles City, Iowa, with groundbreaking scheduled for late 2026 and operations expected to begin in the second half of 2028. The site will add 140,000 liters of capacity, a 20% increase in large-scale capability, to support controlled substances, HPAPIs, and peptide manufacturing.

- March 2026: Siegfried obtained antitrust clearance for the acquisition of three small molecule drug substance sites in the US and Australia, Noramco in Delaware, Purisys in Georgia, and Extractas Bioscience in Tasmania, expanding its controlled substance and clinical API development capabilities across two continents.

- October 2025: EUROAPI officially launched its innovation programs under the EU Health IPCEI, following a July 2025 contractual agreement with the French government providing up to EUR 140 million, or USD 154 million, in public aid under the France 2030 plan. The three programs target complex API synthesis, peptides, and corticosteroid manufacturing using sustainable microbial processes.

Global Small Molecule API Market Report Scope

The Small Molecule API Market report comprises the global production, development, and commercialization of active pharmaceutical ingredients (APIs) manufactured through chemical synthesis and used in the formulation of prescription and over-the-counter medicines. These APIs form the therapeutic component of a wide range of drugs for the treatment of chronic, acute, and infectious diseases. The market is driven by the increasing demand for generic and branded pharmaceuticals, expanding pharmaceutical manufacturing, growing outsourcing of API production, and continuous advancements in synthetic chemistry and process optimization.

The small molecule API market is segmented by type, manufacturer, therapeutic area, and geography. By type, it is further divided into synthetic and biological. By manufacturer, it is segmented into in-house and outsourced. By therapeutic area, the market is segmented into oncology, cardiovascular diseases, central nervous system and neurology, infectious diseases, metabolic disorders, respiratory disorders, gastroenterology, ophthalmology, dermatology, urology, and other therapeutic areas. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Synthetic |

| Biological |

| In-House |

| Outsourced |

| Oncology |

| Cardiovascular Diseases |

| Central Nervous System and Neurology |

| Infectious Diseases |

| Metabolic Disorders |

| Respiratory Disorders |

| Gastroenterology |

| Ophthalmology |

| Dermatology |

| Urology |

| Others (Endocrinology, Nephrology, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Synthetic | |

| Biological | ||

| By Manufacturer | In-House | |

| Outsourced | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular Diseases | ||

| Central Nervous System and Neurology | ||

| Infectious Diseases | ||

| Metabolic Disorders | ||

| Respiratory Disorders | ||

| Gastroenterology | ||

| Ophthalmology | ||

| Dermatology | ||

| Urology | ||

| Others (Endocrinology, Nephrology, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the small molecule API market in 2026?

The small molecule API market stands at USD 182.88 billion in 2026 and is projected to reach USD 250.26 billion by 2031 at a 6.45% CAGR.

Which region leads global revenue generation?

Asia-Pacific leads with 47.18% share in 2025 and is also the fastest-growing region at 8.43% CAGR through 2031.

Which therapeutic area offers the strongest growth potential?

Oncology leads on both scale and growth, with 23.18% share in 2025 and an 8.76% CAGR from 2026 to 2031.

Why are CDMOs gaining importance in API supply?

Many sponsors want flexible capacity without owning full manufacturing infrastructure, which is why outsourced production is projected to grow at 8.15% CAGR through 2031.

What is the biggest risk to margins in API manufacturing?

Feedstock and solvent volatility remains a major risk because recent disruptions pushed key solvent prices up by 20% to 30% and tightened pass-through options for commodity APIs.

Which product type still dominates supply volumes?

Synthetic APIs remain the core revenue base, holding 86.18% share in 2025, while biological APIs are the faster-growing complement at 7.83% CAGR.

Page last updated on: