Slovenia Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

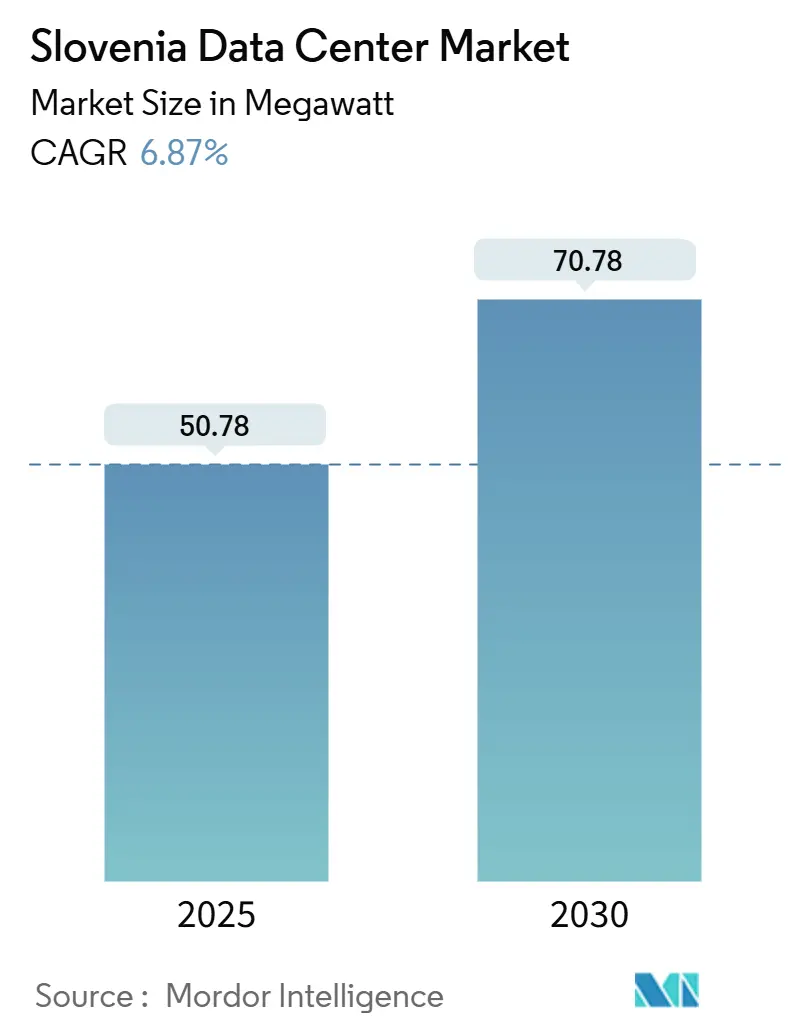

| Market Volume (2025) | 50.78 megawatt |

| Market Volume (2030) | 70.78 megawatt |

| Growth Rate (2025 - 2030) | 6.87% CAGR |

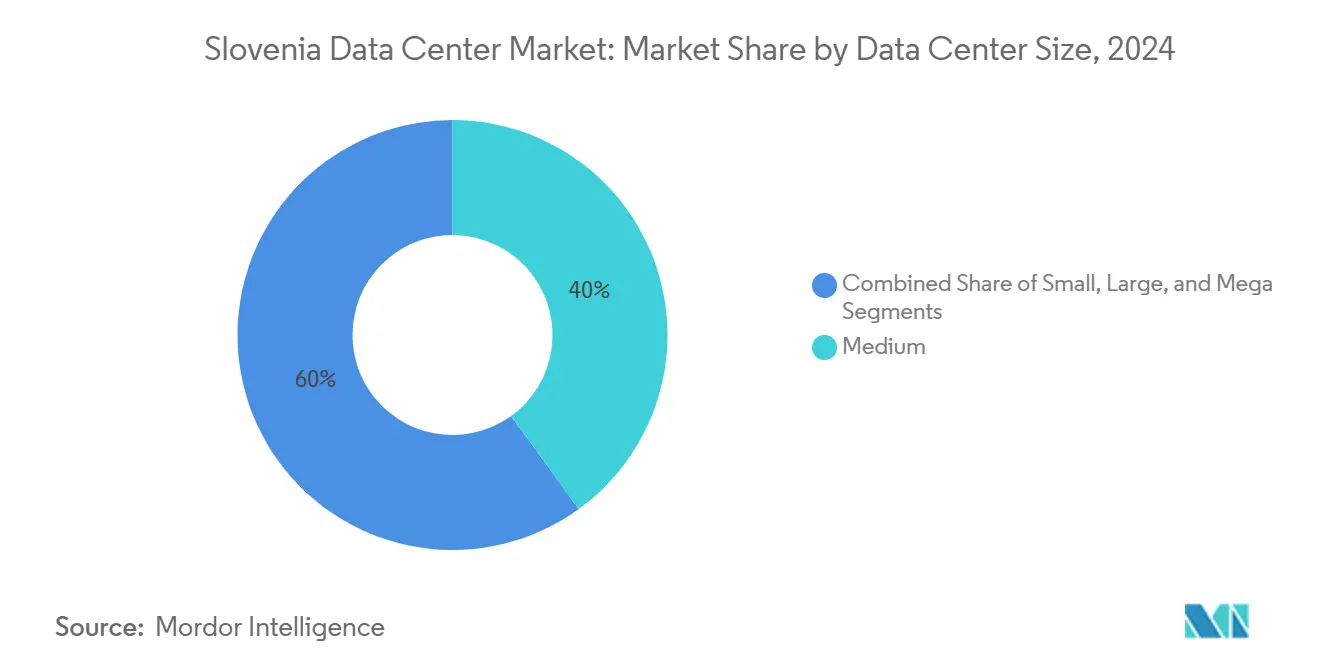

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slovenia Data Center Market Analysis by Mordor Intelligence

The Slovenia data center market size stands at 50.78 MW in 2025 and is forecast to reach 70.78 MW in 2030, advancing at a 6.87% CAGR. This growth anchors the Slovenia data center market as a rising digital backbone for Central Europe, supported by EUR 2.7 billion (USD 3.13 billion) of Recovery and Resilience funding, of which 20% targets digitalization. Cloud-first public-sector programs, rapid 5G rollout, and dependable renewable-energy capacity strengthen investment confidence, while geographic proximity to the Adriatic and DACH corridors positions facilities as low-latency gateways for cross-border workloads. Ljubljana retains the largest installed capacity, but Maribor’s faster build pipeline signals a pivot toward distributed architectures that de-risk grid constraints in the capital. Medium-scale halls still dominate footprints, yet the mega-facility pipeline expands as hyperscale tenants demand clustered power blocks. A 59% utilization rate indicates healthy absorption, and Tier III remains the preferred reliability class, even as Tier IV projects increase for financial, healthcare, and sovereign-cloud needs.

Key Report Takeaways

- By data-center size, the medium category accounted for 40% of the Slovenia data center market size in 2024, while the mega segment is on track for a 7.7% CAGR to 2030.

- By tier standard, Tier III captured 69% revenue share in 2024; Tier IV is set to expand at a 7.1% CAGR between 2025-2030.

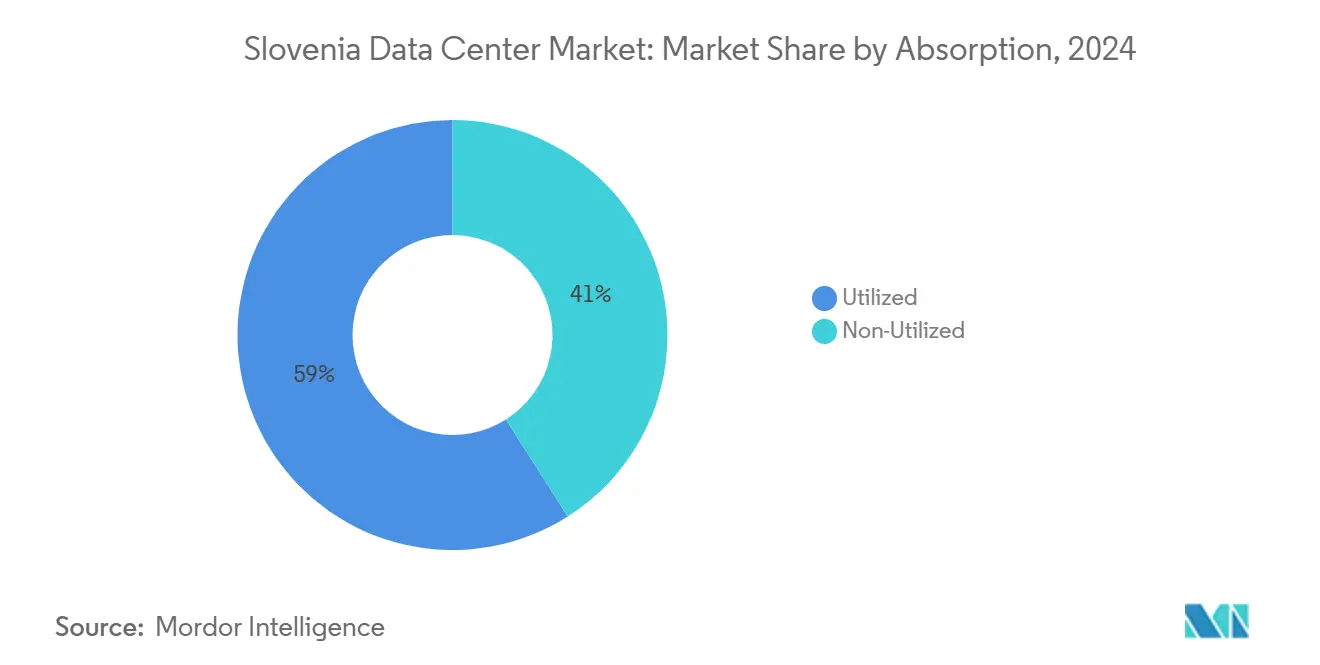

- By absorption, utilized capacity represented 59% of total installed power in 2024; hyperscale colocation within this slice is forecast to grow at 9.2% CAGR to 2030.

- By hotspot, Ljubljana held 48% of the Slovenia data center market share in 2024, whereas Maribor is projected to post the fastest 6.9% CAGR through 2030.

Slovenia Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud and hyperscale-adoption boom | +1.8% | National-Ljubljana, Maribor clusters | Medium term (2-4 years) |

| 5G-enabled edge-computing demand | +1.2% | National-early rollout in Ljubljana, Kranj | Short term (≤ 2 years) |

| EU Digital-Decade and national incentives | +1.5% | Nationwide, backed by RRF grants | Long term (≥ 4 years) |

| Data-sovereignty needs under GDPR | +0.9% | Nationwide with cross-border spillover | Medium term (2-4 years) |

| Cross-border Adriatic-DACH low-latency link | +0.7% | Nova Gorica and Koper corridors | Long term (≥ 4 years) |

| Surplus renewable energy for green DCs | +0.6% | Hydro-rich Alpine regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud and Hyperscale-Adoption Boom

Enterprise workloads continue their flight from legacy on-premises hardware toward scalable x-as-a-service models. Public-sector spending supports momentum; the Ministry of Public Administration ring-fenced EUR 38 million (USD 44.03 million) for cloud programs in the current budget.[1]Red Hat, “T-2 Builds As-a-Service Infrastructure for Slovenian Businesses,” redhat.com Slovenia’s location enables sub-20 ms round-trip latency to Vienna, Milan, and Munich, prompting international hyperscalers to evaluate Maribor as a potential location for regional PoPs. Local operator T-2 demonstrated the model’s viability by building a Red Hat-based IaaS stack that lets ministries and banks run containerized workloads within national borders. As more tenants offload procurement, colocation halls built for 3-5 MW blocks are filling rapidly, lifting the Slovenia data center market’s average rack density above 6 kW in 2025.

5G-Enabled Edge-Computing Demand

Fifth-generation mobile coverage reached 70% of population by late-2024, and the nation’s first private 5G SA network went live at Cinkarna Celje in February 2025.[2]5G.hr, “Kontron and Telekom Slovenije Introduce Slovenia’s First Private 5G SA Network,” 5g.hr Manufacturers now push time-sensitive control loops to local micro-data centers; proof-of-concept trials at an Iskratel smart-factory campus registered sub-10 ms latencies for machine-vision analytics. Edge nodes in Maribor and Nova Gorica shorten backhaul distances and relieve congestion in Ljubljana metro. These deployments favor modular 300-500 kW designs that can be commissioned inside 20 weeks, adding incremental power into the Slovenia data center market without straining grid head-room.

EU Digital-Decade and National Incentives

Slovenia aligns with the European Union’s Digital Decade agenda, targeting universal gigabit access by 2030. RRF outlays allocate EUR 256 million (USD 296.65 million) to public administration cloud migration and EUR 225 million (USD 260.73 million) to digital skills programs, providing operators with visibility into long-dated workload pipelines. The Treasury showcased its intent by issuing a EUR 30 million (USD 34.76 million) blockchain-settled sovereign bond in July 2024, underscoring the need for high-availability, onshore computing. Feed-in tariffs and green tax rebates further incentivize designs using hydro and solar inputs, advancing the sustainability credentials of the Slovenian data center market.

Data-Sovereignty Needs Under GDPR

The 2023 customer-data leak at NLB Bank reignited governance debates and spurred new procurement policies stipulating local data residency.[3]24ur, “NLB Accidentally Discloses Customer Account Information,” 24ur.com Financial regulators now mandate that core banking data remain inside the European Economic Area; for Slovenian institutions, in-country nodes minimize cross-border risk. Participation in Gaia-X through the national hub cements architectural blueprints for federated yet sovereign clouds. Demand is strongest among finance and healthcare tenants that treat Tier IV or Tier III+ redundancy as non-negotiable, lifting the segment’s share of the Slovenia data center market toward 31% by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power bottlenecks in Ljubljana metro | −0.8% | Capital region distribution substations | Short term (≤ 2 years) |

| Escalating construction and financing costs | −1.2% | National-costlier urban brownfields | Medium term (2-4 years) |

| Shortage of certified data-center engineers | −0.9% | Ljubljana and Maribor | Medium term (2-4 years) |

| Seismic- and water-permit delays on new builds | −0.5% | Karst and river-adjacent zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Power Bottlenecks in Ljubljana Metro

Distribution operator Elektro Ljubljana has secured a EUR 50 million (USD 57.94 million) EIB loan for capacity upgrades, although the projects are not expected to conclude until 2026. Until then, megawatt-scale requests face protracted interconnection queues. One hyperscaler divided a planned 12 MW hall into three 4 MW sites, located along the A1 corridor, to mitigate exposure. The bottleneck nudges investors toward Maribor and Nova Gorica plots, where the reserve margin exceeds 30 MVA, altering spatial demand patterns across the Slovenian data center market.

Escalating Construction and Financing Costs

Tighter European Central Bank rates lifted debt spreads through 2024, raising weighted-average cost of capital on speculative builds. Government statistics show building-permit volumes up 18%, stretching contractor capacity and inflating specialized labor premiums. Data-center fit-outs, already reliant on imported switchgear, face longer procurement lead-times, forcing developers to front-load cash outlays. Smaller domestic operators without multinational balance sheets risk postponing capacity-addition cycles, tempering near-term supply growth within the Slovenia data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Medium Footprints Dominate, Mega Builds Gain Pace

Facilities between 1-5 MW owned 40% of the Slovenia data center market share in 2024 because they align with SME-heavy enterprise demand and balanced capex envelopes. Large halls above 5 MW accounted for 34%, serving banking, telecom, and public-sector clouds. The mega-tier single sites above 15 MW logged a 7.7% CAGR and are expected to reach 18 MW installed by 2030, as hyperscale tenants increasingly demand contiguous blocks. Clients lease CPU-hour bundles rather than racks, sidestepping capital budgets while hosting data locally.

In Ljubljana, a new multi-tenant project is being phased in four 4 MW data halls, allowing the builder to cash-flow each stage from signed pre-lets. Elsewhere, a proposed 24 MW mega-campus near Maribor’s Tezno industrial zone leverages dual sub-stations and recycled-water cooling loops. Modular medium-sized sites for agile enterprise colocation, and purpose-built mega clusters for cloud giants, collectively enrich the choice across the Slovenian data center market.

By Tier Standard: Tier III Prevalent, Tier IV Rises for Mission-Critical Loads

Tier III assurances, with 99.982% availability, dominate 69% of capacity because they strike a balance between redundancy and cost. Tier I-II supply supports dev-test, back-up, and edge nodes where price sensitivity trumps uptime. Tier IV’s 7.1% CAGR reflects compliance-centric verticals such as banking and medicines manufacturing. ARNES relies on Tier III+ attributes, dual utility feeds, and concurrently maintainable paths to support academic supercomputing workloads.

Financial services procurement guidelines now rank MTTR and demonstrated Tier certification among the top evaluation criteria following the 2023 breach incident. Accordingly, two Ljubljana projects are upgrading to Tier IV double-string architecture with concurrently active paths and fault-tolerant switchgear. This mix secures risk-aligned options for stakeholders across the Slovenia data center market.

By Absorption: Utilization at 59% Signals Healthy Maturity

Total fitted power reached 50.78 MW in 2025, of which 30 MW is actively drawn, translating to a 59% utilization rate. Hyperscale colocation is the fastest-growing slice with a 9.2% CAGR as U.S. and regional SaaS firms adopt “Slovenia-plus-one” strategies for Balkan coverage. Wholesale deals capture 10-15 rack pods leased over five-year terms, while retail cages serve engineering consultancies and MSPs.

The non-utilized reserve, which accounts for 41% of the standing power, acts as a buffer for step-wise tenant ramp-ups, underpinning investor confidence. Developers schedule transformer and generator installments in modular 2 MW blocks so capex parallels customer uptake. This supply discipline limits stranded capacity and sustains pricing integrity across the Slovenia data center market.

By Hotspot: Ljubljana Leads, Maribor Accelerates

Ljubljana contributed 48% of installed power in 2024, reflecting its concentration of ministries, banks, and headquarters. The Slovenia data center market size for the capital is forecast to advance at a steady 5.5% CAGR, yet land scarcity and a stretched grid restrain single-parcel expansions. Operators respond with multi-story designs that stack white space vertically while maximizing power-usage effectiveness. Maribor’s lower land costs and access to redundant 110 kV feeds drive a faster 6.9% CAGR. Nova Gorica leverages bilateral fiber routes into Trieste, while Koper positions for submarine-cable landing opportunities. Smaller municipalities capture disaster-recovery nodes, improving geographic risk diversification inside the Slovenia data center market.

Ljubljana’s colocation halls sit within 15 km of the main Internet exchange, ensuring sub-2 ms latency to national carriers. Maribor’s Creative Park Drava technology hub, backed by the Regional Development Agency, packages incentives such as expedited permitting and tax offsets. These factors shift 28 MW of the 2025-2030 capacity pipeline northward. Within the five-city cluster, edge facilities under 1 MW meet industrial 5G workloads, whereas hyperscalers cluster capacity at two planned 8 MW campuses, collectively reshaping the Slovenia data center market’s heat map.

Geography Analysis

Ljubljana dominates the current footprint but faces immediate infrastructure constraints. The 2024 EUR 50 million (USD 57.94 million) EIB-backed reinforcement program will retrofit 460 km of lines and deploy 400,000 smart meters; however, until its completion, large requests continue to reroute north or west. The capital nonetheless enjoys the densest fiber mesh, direct access to Slovenia Internet Exchange, and a concentration of certified engineers, keeping average sales cycles under six months.

Maribor, located 130 km northeast, attracts industrial and logistics tenants aligned with the A1/A4 highway axis. Creative Park Drava’s incentive packages accelerate permit issuance within 90 days, encouraging brownfield conversions of former textile plants into data halls. Nova Gorica leverages dual-border fiber to Italy and a low earthquake risk; one operator pipes chilled water from Soča River tributaries to reduce the PUE below 1.25. Koper’s coastal plots attract Mediterranean cable back-haul projects, positioning it as a potential inter-tie node between Balkan terrestrial networks and submarine systems.

Beyond urban centers, municipalities such as Celje and Novo Mesto pilot micro-edge units of 250 kW to support smart-city traffic analytics. National fiber-to-the-premises already covers 78.5% of households, allowing even rural sites to guarantee <5 ms latency to carrier PoPs. Government plans to channel EUR 17 billion (USD 19.70 billion) into logistics corridors by 2030 will further equalize infrastructure, enhancing the Slovenia data center market’s geographic resilience.

Competitive Landscape

Market structure is moderately fragmented. ARNES connects 1,400+ research bodies and anchors academic cloud growth. Telekom Slovenije blends carrier-neutral colocation with last-mile fiber, giving enterprises single-invoice contracts. International consultancies rent cages for managed SAP and IBM mainframe clients, while Arctur differentiates via high-performance computing and ISO 27001 accreditations. DHH-owned Webtasy captures SME cloud hosting through localized language support and flat-rate packages.

Strategic behavior tilts toward hybrid solutions. Telekom Slovenije offers ExpressRoute and Direct Connect gateways, allowing customers to burst into Azure or AWS while meeting residency rules. T-2 bundles managed Kubernetes with 10 Gbps city-ring connectivity, highlighting value in integrated networks. United Group pledges to achieve 100% renewable energy by 2027 across its regional data-center assets. Operators note that green power offsets help clinch multinational procurement, especially as Scope 2 reporting becomes mandatory under CSRD.

Consolidation prospects increase following Telemach’s 2024 purchase of T-2, which delivered a 55% fixed-broadband share under one umbrella. Scale economies unlock pooled dark-fiber rights and common spare-parts stock, pressuring smaller independents. Still, regulatory safeguards limit excessive concentration, preserving multiple gateway options for hyperscalers considering entry into the Slovenia data center market.

Slovenia Data Center Industry Leaders

PERFTECH

SoftNET

RvO d.o.o (Datacenter.si)

Arctur d.o.o.

IBM (CSP)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kontron and Telekom Slovenije debuted the country’s first private 5G standalone network at Cinkarna Celje, enabling ultra-low-latency process automation

- December 2024: Novartis inaugurated a EUR 40 million (USD 46.35 million) viral-vector plant in Mengeš, heightening local demand for GMP-compliant compute.

- September 2024: The EIB extended a EUR 50 million (USD 57.94 million) loan to Elektro Ljubljana for grid upgrades, targeting a 2026 completion date.

- August 2024: United Group’s Telemach acquired 98.06% of T-2, reshaping telecom and data-center capacity pools.

Slovenia Data Center Market Report Scope

Slovenia Data Center Market Report is Segmented by Data-Center Size (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, and Tier IV), Absorption (Non-Utilized, Utilized (Colocation Type (Hyperscale, Retail, Wholesale), End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users)), and Hotspot (Ljubljana, Maribor, Nova Gorica and Goriška, and Koper and Coastal-Karst). The Market Forecasts are Provided in Terms of Volume (MW Capacity).

| Small |

| Medium |

| Large |

| Mega |

| Tier I-II |

| Tier III |

| Tier IV |

| Utilized Capacity | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud and IT Services | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Non-Utilized Reserve | ||

| Ljubljana (Central Slovenia) |

| Maribor (Stajerska) |

| Nova Gorica and Goriška |

| Koper and Coastal-Karst |

| Rest of Slovenia |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| By Tier Standard | Tier I-II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Utilized Capacity | By Colocation Type | Hyperscale |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud and IT Services | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| Non-Utilized Reserve | |||

| By Hotspot | Ljubljana (Central Slovenia) | ||

| Maribor (Stajerska) | |||

| Nova Gorica and Goriška | |||

| Koper and Coastal-Karst | |||

| Rest of Slovenia | |||

Key Questions Answered in the Report

How much power capacity is installed in Slovenia’s current data-center fleet?

Installed capacity totals 50.78 MW in 2025 and is projected at 70.78 MW by 2030.

Which city is adding capacity the fastest?

Maribor leads expansion with a forecast 6.9% CAGR through 2030, outpacing Ljubljana.

What renewable-energy share supports Slovenian data halls?

Renewable sources supplied 25.07% of national final energy use in 2023, and 41.89% of electricity generation.

What tier standard dominates facility design?

Tier III accounts for 69% of active white space, balancing uptime and cost.

How are hyperscalers influencing local development?

Demand for contiguous 15 MW blocks is spurring mega-campus projects near Maribor and distributed micro-edge nodes near 5G-enabled factories.

Are government incentives available for new builds?

Yes, the Recovery and Resilience Plan allocates dedicated digital-infrastructure grants and tax offsets for green-powered facilities.

Page last updated on: