Slovakia Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

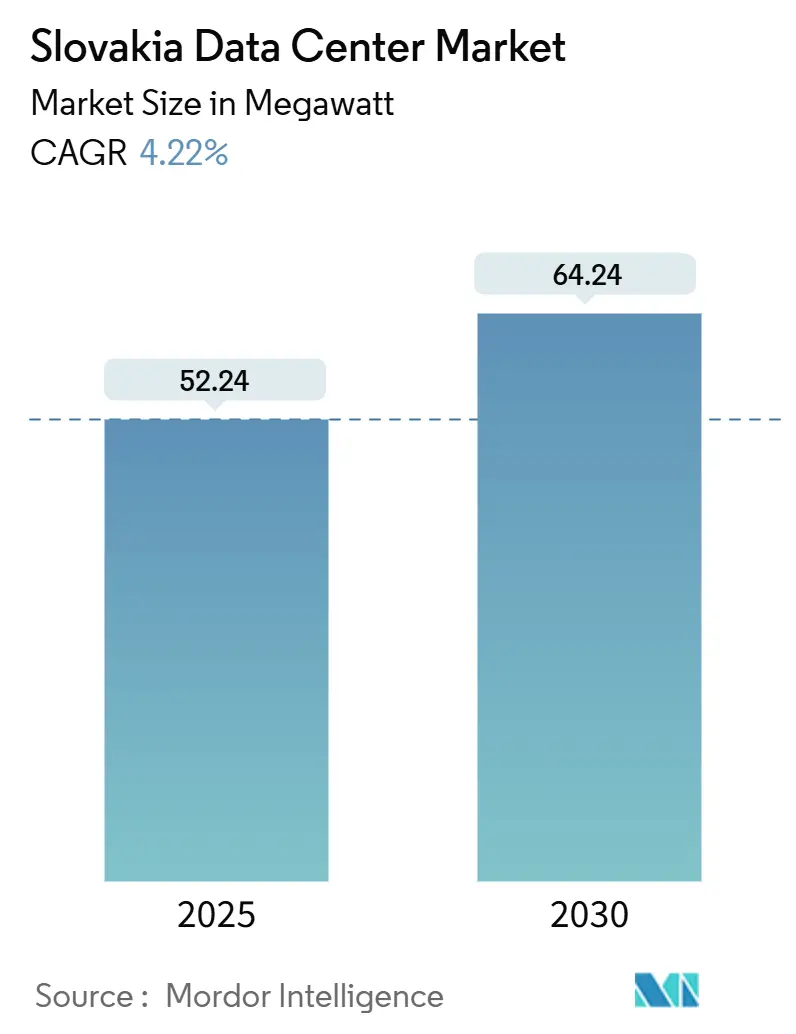

| Market Volume (2025) | 52.24 megawatt |

| Market Volume (2030) | 64.24 megawatt |

| Growth Rate (2025 - 2030) | 4.22% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Slovakia Data Center Market Analysis by Mordor Intelligence

The Slovakia data center market size stands at 52.24 MW in 2025 and is projected to reach 64.24 MW by 2030, expanding at a 4.22% CAGR over the forecast period. Demand is driven by Tier III–compliant legislation, EU-backed fiber rollouts, and the strategic Vienna–Bratislava latency corridor, which positions facilities within 2 ms of one of Europe’s largest Internet hubs. Growing local cloud adoption, automotive e-mobility investments, and solar-PPA incentives further bolster construction pipelines, while energy price volatility and skilled labor shortages temper short-term growth. Operators are shifting capital toward medium-sized and mega campuses to meet hyperscale requirements while maintaining efficiency targets of less than 1.4 PUE.

Key Report Takeaways

- By data center size, medium facilities (2–5 MW) led with 40% revenue share of the Slovakia data center market in 2024; the mega segment (greater than 25 MW) is projected to expand at a 6.5% CAGR through 2030.

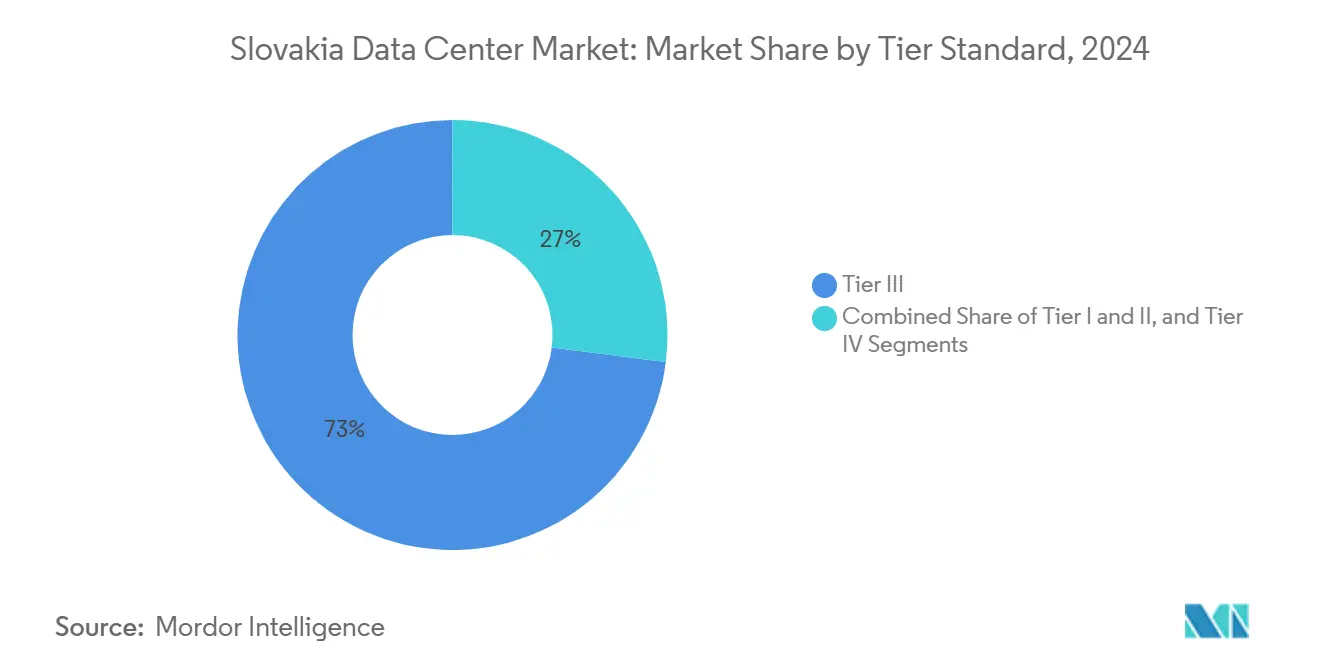

- By tier standard, Tier III captured 73% of the Slovakia data center market share in 2024, while Tier IV records the highest projected CAGR at 6.6% through 2030.

- By absorption, utilised capacity accounted for 77% of the Slovakia data center market size in 2024 and is advancing at a 4.9% CAGR through 2030.

- By geography, Bratislava commanded 72% of the Slovakia data center market in 2024; Eastern Slovakia is forecast to post a 5.5% CAGR to 2030.

Slovakia Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cloud-first adoption by Slovak corporates | +1.2% | National, concentrated in Bratislava and Košice | Medium term (2-4 years) |

| EU-funded fibre backhaul roll-outs to Tier-III cities | +0.8% | National, emphasis on Central and Eastern Slovakia | Long term (≥ 4 years) |

| Edge-AI demand from automotive e-mobility cluster | +0.9% | Western Slovakia, spillover to Central regions | Medium term (2-4 years) |

| Mandatory Critical-Infrastructure Act 367/2024 for uptime ≥Tier III | +0.7% | National, immediate impact in major urban centers | Short term (≤ 2 years) |

| Solar-PPA incentives cutting PUE-linked opex | +0.4% | National, concentrated in high-solar regions | Long term (≥ 4 years) |

| Vienna-Bratislava <2 ms latency attracting hyperscalers | +0.6% | Bratislava region, extending to Western Slovakia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cloud-First Adoption by Slovak Corporates

Enterprises are accelerating digital modernization as Slovakia channels EUR 6.408 billion (USD 6.92 billion) of recovery funds into broadband and e-government projects.[1]European Commission, “Slovakia’s Recovery and Resilience Plan,” commission.europa.eu Banks, such as UniCredit, finalized the full deployment of ARBES TOPAS in August 2024 to automate payment matching and analytics, thereby boosting secure colocation demand. Retailers operate 15,630 e-shops that generated EUR 2 billion (USD 2.32 billion) in 2024, necessitating low-latency hosting and content delivery. Mandatory e-invoicing slated for 2027 expands compliance workloads that enterprises prefer to run in Tier III environments. Together, these factors sustain double-digit bookings across Bratislava facilities, reinforcing medium-sized build strategies.

Edge-AI Demand from Automotive E-Mobility Cluster

The automotive sector secured EUR 1.2 billion (USD 1.30 billion) from Gotion–InoBat for battery plants at Šurany and USD 256.7 million from Hyundai Mobis for an EV power-system plant in Novaky, each integrating digital twin and real-time analytics at the edge. Volkswagen Slovakia partners with Asseco CEIT on data-driven logistics that need sub-10 ms latency, pushing workloads from Germany into Western-Slovak edge nodes. Twinzo’s digital-twin platform achieves 20% fleet reduction in pilot factories, proving ROI for on-premise micro-data centers. These use cases spur suppliers to colocate near manufacturing clusters, driving demand for 2–5 MW facilities.

Mandatory Critical-Infrastructure Act 367/2024 for Uptime ≥ Tier III

Effective January 2025, Act 367/2024 compels critical operators to meet concurrent-maintainability standards and robust cyber-resilience practices. Existing Tier I/II sites must retrofit dual power feeds and independent cooling loops or migrate workloads to compliant facilities, triggering a retrofit rush across public-sector IT rooms. Certification backlogs already exceed nine months, favoring established Tier III operators, and raising the Slovakia data center market entry barrier for small entrants. Insurers have started to demand proof of compliance, bolstering premium pricing for certified capacity.

EU-Funded Fibre Backhaul Roll-Outs to Tier-III Cities

Slovakia’s broadband coverage of 62.1% trails the EU mean, prompting deployment of very-high-capacity networks backed by Connecting-Europe Facility grants.[2]European Data Journalism Network, “Gigabit Society,” europeandatajournalism.eu Projects extend 10 Gbps XG-PON fiber to cities like Košice and Bardejov through operators such as ANTIK, unlocking edge-colocation demand for regional enterprises. Cross-border interconnect plans in the Continental Central East Region improve redundancy at Slovak–Czech and Slovak–Hungarian nodes. Enhanced backhaul reduces total cost of ownership for distributed workloads, stimulating investor interest in Central and Eastern Slovakia, where land costs remain 30% below Bratislava averages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity spot-price volatility post-2023 cap removal | -0.8% | National, acute impact in Western Slovakia | Short term (≤ 2 years) |

| Talent deficit in mission-critical facility engineering | -0.6% | National, concentrated in major urban centers | Medium term (2-4 years) |

| Grid-connection queue >24 months in Western Slovakia | -0.4% | Western Slovakia, spillover effects nationally | Long term (≥ 4 years) |

| Limited brownfield sites with dual 110 kV feeders | -0.3% | National, critical in high-demand regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Electricity Spot-Price Volatility Post-2023 Cap Removal

Commercial tariffs are exposed to wholesale price fluctuations, despite the government capping household prices at EUR 61/MWh (USD 65.88) until 2025.[3] Enerdata, “Electricity Price Cap,” enerdata.net Slovakia exports surplus nuclear-hydro power, yet geopolitical pressures can widen the SK-AT day-ahead spread, raising opex for data halls. The Mochovce-3 reactor, which has been online since 2023, helps mitigate baseload risk but will not fully stabilize prices until all turbines reach their design output in 2026. Operators hedge through long-term solar PPAs that shave PUE by up to 0.1 and lock in rates below 70 EUR/MWh (USD 81.22), but small colocation players struggle to secure volume discounts.

Talent Deficit in Mission-Critical Facility Engineering

Eurostat reports 51.4% of Slovak firms struggle to hire ICT specialists, mirroring a 62.8% EU average skills gap. Certified electrical and mechanical engineers command 20% wage premiums, prompting operators to recruit abroad or establish graduate academies in Košice and Žilina. Deutsche Telekom IT Solutions invests in upskilling 3,900 local staff through edge-computing labs, yet churn remains high as hyperscale builders lure talent with global rotations. Persistent shortages slow fit-out schedules by up to twelve weeks, delaying revenue recognition for new halls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hotspot: Bratislava Dominance Drives Regional Expansion

Bratislava commands a dominant 72% market share in 2024, leveraging its strategic position as Slovakia's capital and primary economic hub with direct connectivity to Vienna's financial and technology ecosystems. The region's competitive advantage stems from its sub-2 millisecond latency connection to Vienna, enabling data centers to serve up to 100 million users across Central Europe with optimal performance characteristics. Bratislava's concentration of multinational corporations, government agencies, and financial institutions creates dense demand for colocation and cloud services, while the city's membership in multiple internet exchange points, including SIX-SK at Perpetuus DC, ensures robust connectivity options. However, the region faces infrastructure constraints including grid connection delays exceeding 24 months and limited availability of brownfield sites with dual 110 kV power feeders, creating supply bottlenecks that may limit future expansion capacity.

Eastern Slovakia emerges as the fastest-growing hotspot with a 5.5% CAGR through 2030, driven by government initiatives to develop the Košice IT Valley and EU-funded infrastructure improvements extending high-capacity connectivity to secondary cities. The region employs approximately 11,000 IT professionals contributing 16% to local GDP, creating a skilled workforce foundation supporting data center operations and related technology services. Deutsche Telekom IT Solutions Slovakia's significant presence in Košice, where it operates as the second-largest regional employer with over 3,900 staff, demonstrates the area's capacity to support large-scale technology operations. Western Slovakia and Central Slovakia represent emerging opportunities as enterprises seek alternatives to Bratislava's capacity constraints, benefiting from lower real estate costs while maintaining access to improving digital infrastructure through EU connectivity programs targeting Tier-III cities. The World Bank's assessment across five Slovak cities highlights varying regulatory implementation quality, with improvements needed in building permits and utility services to create more conducive environments for data center development.

By Data Center Size: Medium Facilities Drive Market Expansion

Medium facilities held 40% of the Slovakia data center market share in 2024, reflecting enterprise demand for scalable yet cost-efficient capacity. The segment’s resilient take-up keeps utilisation above 80%, allowing operators to fund incremental 1 MW phases from cash flow. Mega facilities, though currently niche, are set to post a 6.5% CAGR as hyperscalers exploit the Vienna–Bratislava corridor. Datacube’s NATO-certified campus, located 2 km from the Austrian border, exemplifies the mega model’s appeal among US cloud providers seeking low-latency reach to 100 million Central European users.

The Slovakia data center market size for mega facilities is projected to add 8 MW between 2025 and 2030, supported by land-bank acquisitions in Senec and Malacky. Operators plan to incorporate on-site solar plus fuel-cell peaking plants to maintain sub-1.3 PUE, aligning with EU taxonomy thresholds. Small and large bands are expected to grow below the market average as enterprise tenants consolidate legacy server rooms into modern colocation suites.

By Tier Standard: Compliance Requirements Elevate Infrastructure Standards

Tier III sites captured 73% of 2024 capacity after Act 367/2024 catalyzed upgrades across BFSI, healthcare, and e-government estates. Migrating to concurrent-maintainable designs improved SLA adherence, reducing unplanned outage minutes by 28% year-on-year. Tier IV, though only 5 MW today, shows strongest pipeline activity with two greenfield builds in Trnava and Žilina targeting financial-services tenants. The Slovakia data center market size for Tier IV is forecast to triple by 2030 as regulators tighten cyber-resilience audits in critical sectors.

Tier I and II footprints continue shrinking, repurposed into disaster-recovery nodes or edge POPs. Operators redeploy redundant generators into rural solar-diesel hybrids servicing 5G towers, aligning with EU circular-economy mandates.

By Absorption: Utilisation Rates Signal Market Health

Utilised racks accounted for 77% of installed power in 2024, indicating healthy equilibrium between supply additions and tenant demand. High usage stems from cloud repatriation workloads and digital-twin pilots that run hottest during daytime production cycles. The Slovakia data center market size for utilised capacity is set to reach 50 MW by 2030, while non-utilised capacity grows moderately as operators provision ahead of demand.

Hyperscale colocation, within utilised capacity, posts the fastest trajectory as AWS, Azure, and Google Cloud scout land near the D4 highway loop. Retail colocation maintains steady bookings from SMEs migrating to Odoo-based ERP and Shopify storefronts.

Geography Analysis

Bratislava dominates with 72% of installed power, benefiting from dense carrier hotels, a multilingual workforce, and electricity tariffs 38% below the EU average. Its data centers peer at SIX-SK and NIX.SK, ensuring sub-2 ms round-trip to Vienna and Frankfurt. Land scarcity and 24-month grid-connection queues, however, push new entrants toward nearby Senec and Pezinok, where industrial-zoned plots remain available.

Eastern Slovakia records the fastest 5.5% CAGR through 2030 as Košice IT Valley nurtures 11,000 software professionals contributing 16% of regional GDP. Deutsche Telekom’s 3,900-strong campus anchors demand, while municipal grants subsidize brownfield conversions for Tier III halls. EU backhaul projects cut latency to Bratislava by 25%, enhancing disaster-recovery attractiveness.

Western and Central Slovakia form emerging clusters. Novaky and Žilina leverage proximity to Czech data routes and automotive suppliers. Grid upgrades adding dual 110 kV feeders unlock parcels once deemed unsuitable. Balanced regional incentives reduce over-reliance on Bratislava, stabilizing real-estate costs and broadening the Slovakia data center market.

Competitive Landscape

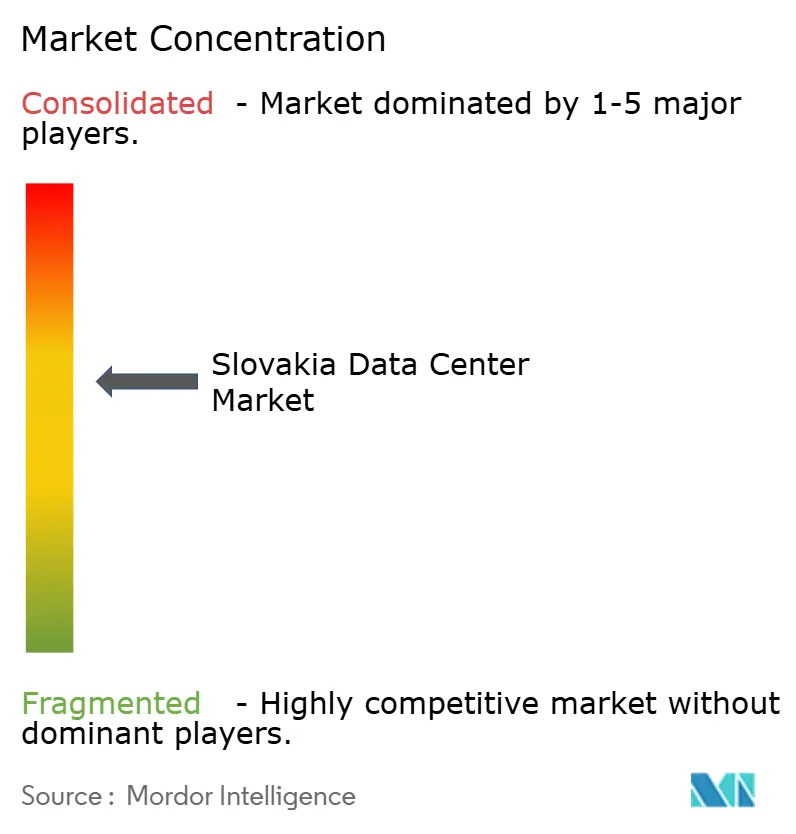

The market is moderately fragmented, with the top five players accounting for 46% of the capacity. Deutsche Telekom IT Solutions leads by combining colocation, hybrid cloud, and managed security, serving 500+ global clients. Datacube differentiates through NATO clearance and direct fiber to Vienna’s Digital Realty campus, attracting US and Japanese gaming studios. Aliter Technologies scales through the 2025 acquisition of Canadian network-engineering firm 3CIS, extending its expertise in secure communications for defense customers.

New entrants like Vantage Data Centers inject fresh capital, leveraging a EUR 1.4 billion (USD 1.62 billion) regional war chest to design 16 MW blocks pre-wired for liquid cooling. Local ISP NIX.SK modernized its peering fabric to VXLAN-EVPN leaf–spine, offering ready cross-connects for wholesale tenants. Competitive focus now centers on energy sourcing; operators with a renewable mix of more than 50% obtain green-bond financing at 20 basis points below conventional debt, widening their cost advantages.

Consolidation pressures will intensify as compliance costs for Act 367/2024 raise barriers for sub-2 MW independents. Expect M&A activity targeting Tier II sites for portfolio roll-ups into region-wide edge grids.

Slovakia Data Center Industry Leaders

-

Deutsche Telekom

-

Vnet a.s.

-

Computer and Network consulting

-

Axians

-

SITEL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Vantage Data Centers pledged EUR 1.4 billion (USD 1.51 billion) for EMEA expansion, earmarking Bratislava land options.

- January 2025: DigitalBridge and Silver Lake closed a USD 9.2 billion equity round into Vantage, accelerating Slovak builds

- January 2025: Critical-Infrastructure Act 367/2024 took effect, mandating Tier III minimum uptime

- October 2024: Hyundai Mobis confirmed a USD 256.7 million power-system plant at Novaky, raising edge-AI demand.

Slovakia Data Center Market Report Scope

| Bratislava |

| Western Slovakia |

| Central Slovakia |

| Eastern Slovakia |

| Small |

| Medium |

| Large |

| Massive |

| Mega |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| By Hotspot | Bratislava | ||

| Western Slovakia | |||

| Central Slovakia | |||

| Eastern Slovakia | |||

| By Data Centet Size | Small | ||

| Medium | |||

| Large | |||

| Massive | |||

| Mega | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

Key Questions Answered in the Report

How large is the Slovakia data center market in 2025?

Nstalled IT power totals 52.24 MW, with a forecast to reach 64.24 MW by 2030 at a 4.22% CAGR.

Which Slovak region leads data center capacity?

Bratislava hosts 72% of national capacity thanks to dense fiber routes and sub-2 ms connectivity to Vienna.

Why is Tier III so dominant in Slovak facilities?

Critical-Infrastructure Act 367/2024 requires Tier III-level uptime for key sectors, prompting upgrades and new builds.

What end-user sector drives demand most?

Financial-services firms anchor over one-third of live whitespace by modernizing core banking and regulatory systems.

How do energy prices affect operators?

Spot-price volatility raises opex, but long-term solar PPAs and nuclear baseload help stabilize costs for compliant sites.

Which segment will grow fastest by 2030?

Mega facilities (>25 MW) are projected to expand at 6.5% CAGR as hyperscalers capitalize on the Vienna-Bratislava corridor.

Page last updated on: