Slit Lamps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 315.45 Million |

| Market Size (2031) | USD 405.49 Million |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

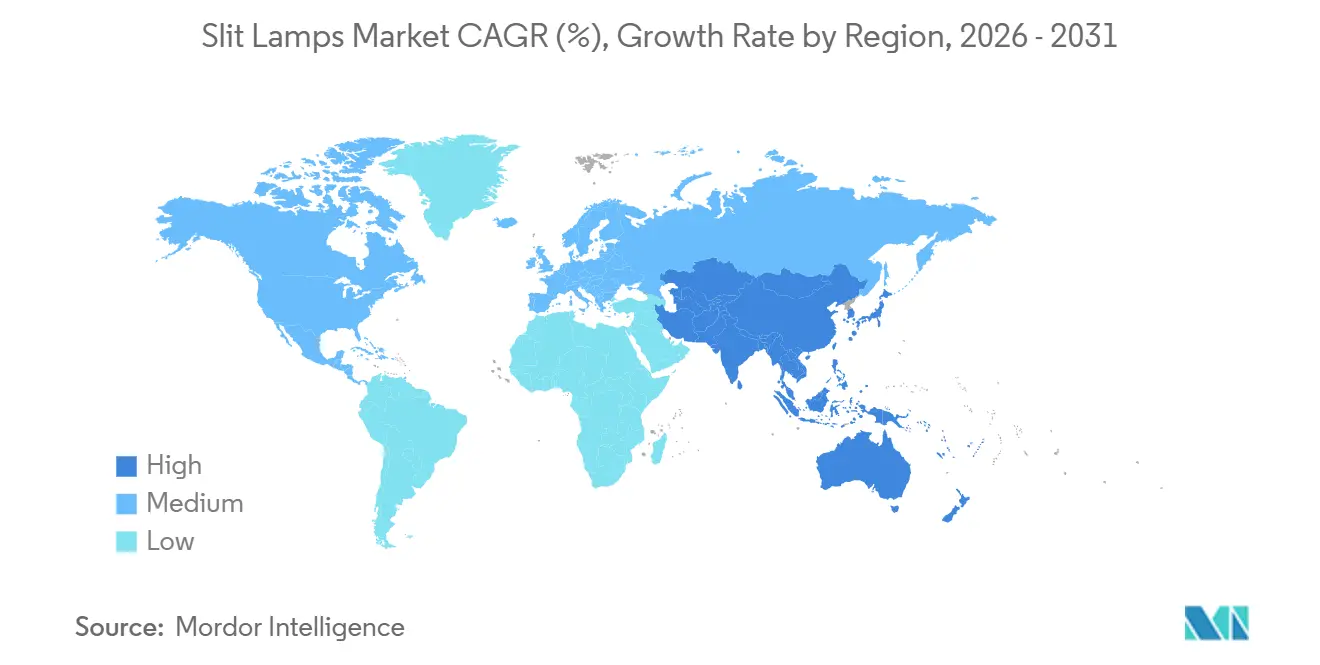

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slit Lamps Market Analysis by Mordor Intelligence

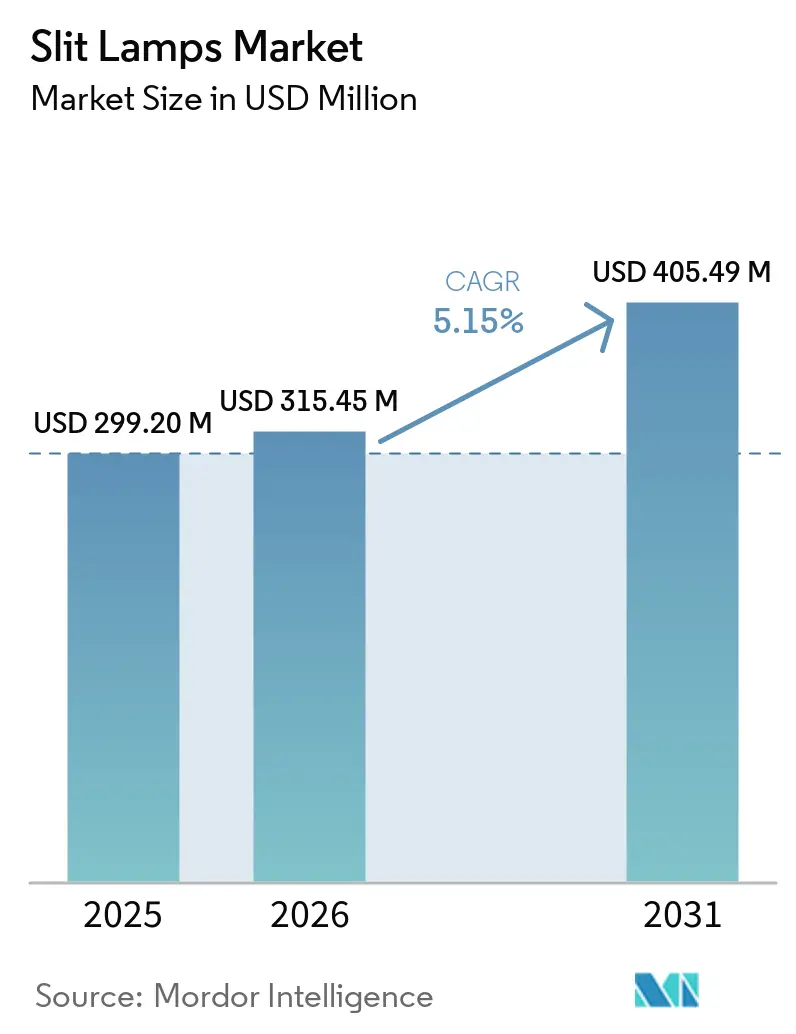

The Slit Lamps Market size is expected to grow from USD 299.20 million in 2025 to USD 315.45 million in 2026 and is forecast to reach USD 405.49 million by 2031 at 5.15% CAGR over 2026-2031.

Strong growth reflects rising cataract and glaucoma screening volumes, a pivot from analog to AI-enabled imaging platforms, and payer pressure for evidence-linked reimbursement that favors devices able to archive images directly into electronic records. Ambulatory surgical centers and tertiary eye hospitals adopt premium digital units because faster diagnostic throughput offsets higher capital cost. Portable models gain traction in rural clinics and veterinary practices where mobility and space constraints dominate purchasing criteria. Across regions, LED illumination outperforms halogen on energy use, heat output, and bulb life, accelerating replacement demand.

Key Report Takeaways

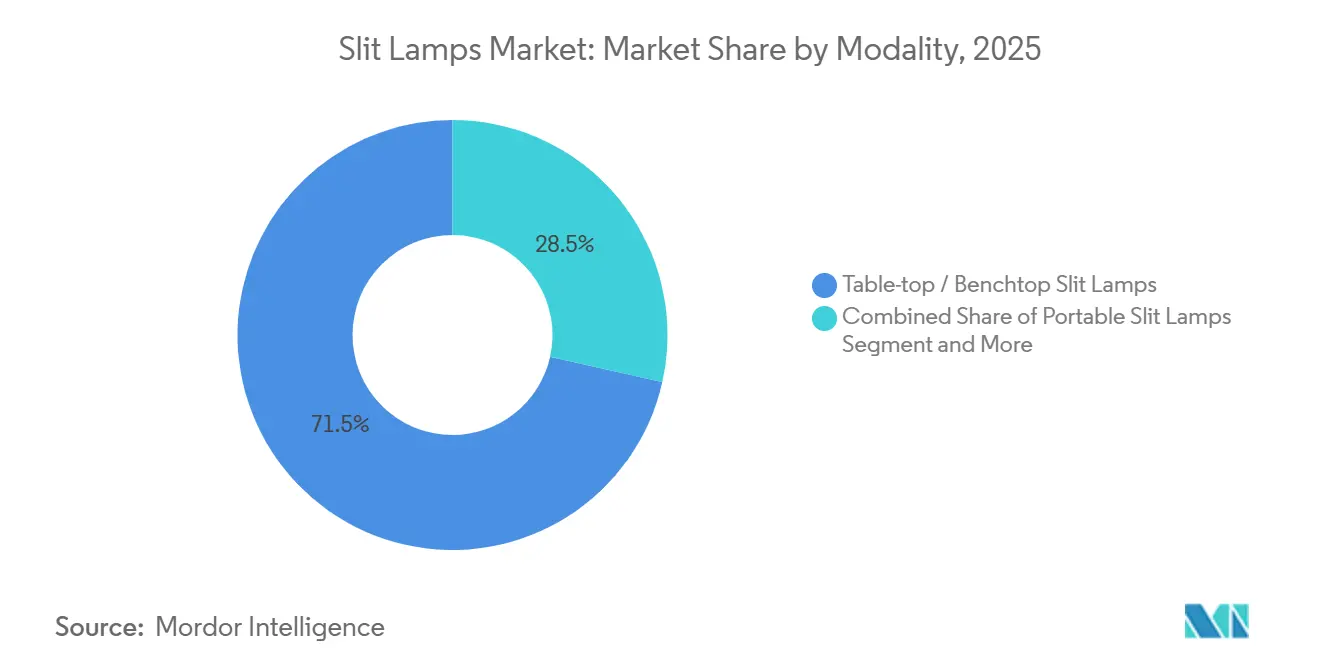

- By modality, benchtop systems held 71.55% of the slit lamps market share in 2025 while portable units are forecast to climb at an 8.25% CAGR through 2031.

- By light source, LED captured 59.53% revenue in 2025 and is projected to expand at a 7.55% CAGR to 2031.

- By technology, conventional analog models represented 54.23% of 2025 sales, whereas AI-enabled digital platforms will grow at a 9.15% CAGR over the forecast horizon.

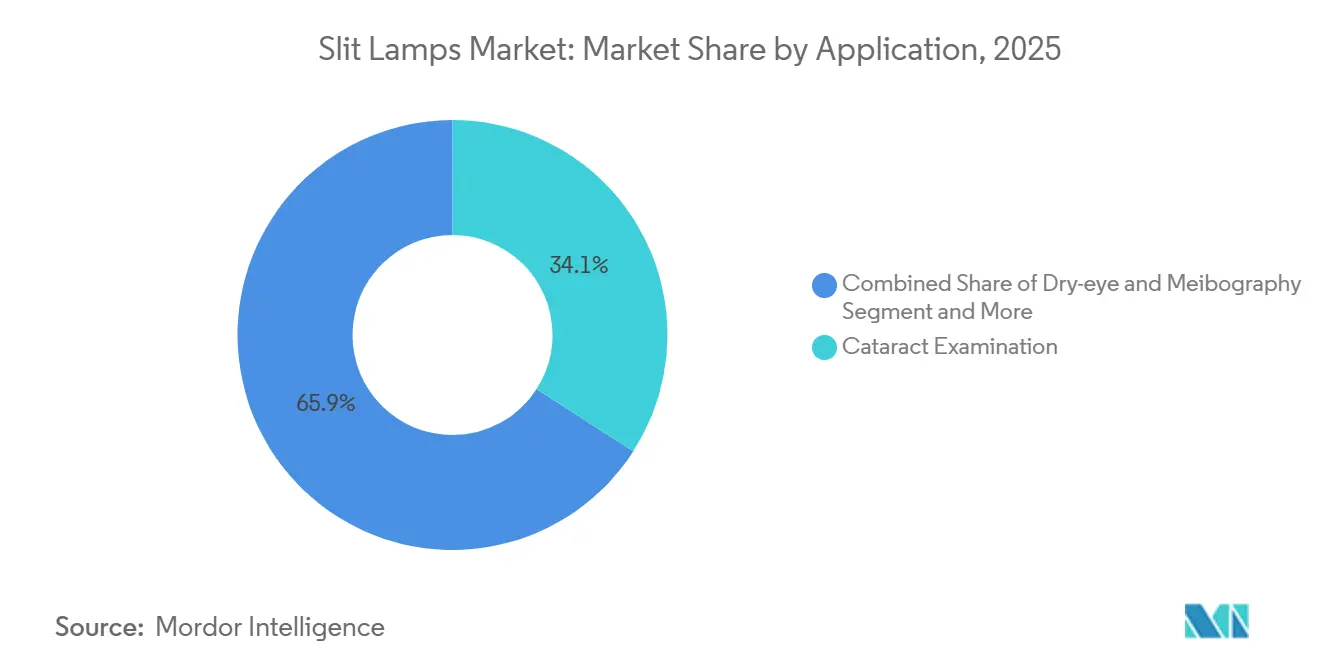

- By application, cataract examination led with 34.15% share in 2025; dry-eye and meibography imaging is expected to advance at a 9.45% CAGR through 2031.

- By end user, hospitals and tertiary eye centers accounted for 61.25% of demand in 2025, while ambulatory surgical centers demonstrate the highest projected CAGR at 9.21% to 2031.

- By geography, North America commanded 34.55% of 2025 revenue; Asia-Pacific is positioned to register a 7.51% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Slit Lamps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in age-related ocular diseases | +1.2% | Global, with concentration in North America, Europe, and aging Asia-Pacific markets (Japan, South Korea) | Long term (≥ 4 years) |

| Global shift toward LED-illuminated systems | +0.9% | Global, led by North America and Europe; accelerating in Asia-Pacific | Medium term (2-4 years) |

| Accelerating demand for portable point-of-care units | +0.7% | Asia-Pacific core, spillover to Middle East and Africa; rural North America | Medium term (2-4 years) |

| Digitally integrated imaging and EHR connectivity | +0.8% | North America and Europe; emerging in urban Asia-Pacific tertiary centers | Short term (≤ 2 years) |

| AI-assisted anterior-segment screening in primary care | +0.6% | North America, Europe; pilot deployments in India, China | Medium term (2-4 years) |

| Growing uptake in veterinary ophthalmology | +0.3% | North America, Europe; niche expansion in Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Age-Related Ocular Diseases

Global vision-impairment now affects 2.2 billion people, and the U.S. population aged 65 plus will reach 73.1 million by 2030. Greater longevity inflates cataract and glaucoma caseloads, obliging clinics to expand diagnostic capacity without adding real estate. Slit lamp utilization per patient has increased because annual intraocular pressure checks and optic nerve exams require biomicroscopy. India illustrates scale effects: 7 million cataract surgeries in 2024 each demanded pre-operative slit lamp imaging across more than 1,000 district hospitals[1]National Programme for Control of Blindness and Visual Impairment, “Annual Report 2023-2024,” npcbvi.mohfw.gov.in. Practices that delay upgrading risk throughput losses when reimbursement depends on documented imaging.

Global Shift Toward LED-Illuminated Systems

LED modules deliver 450,000 lux while consuming 40% less power than halogen and lasting 50,000 hours instead of 500. Stable 5,500 K color temperature ensures diagnostic consistency, and lower heat output improves patient comfort. Top vendors no longer offer halogen models, while Chinese manufacturers supply cost-competitive LED devices that meet ISO 15004-2 safety rules. Remaining halogen units cluster in cash-constrained public hospitals where upfront cost still prevails.

Accelerating Demand for Portable Point-of-Care Units

Urban specialist concentration leaves rural populations underserved, prompting India’s mobile screening camps to adopt battery-powered devices under 2 kg that pair with tablets for image capture. Smartphone-based optics validated at 96% diagnostic accuracy show how low-cost imaging can substitute for benchtop units during field screening. Veterinary clinics also favor handheld instruments sized for companion animals, adding another portable demand stream. As a result, the segment advances faster than any other modality.

Digitally Integrated Imaging and EHR Connectivity

U.S. and European record-keeping mandates reward devices capable of pushing images directly into patient files. A five-megapixel camera mounted on Topcon’s SL-D series uploads images via Ethernet or Wi-Fi, cutting transcription errors and billing audits. Keeler shortened integration time by shipping slit lamps pre-configured for Epic and Cerner systems. Connectivity also enables longitudinal comparison of optic-nerve images, essential for glaucoma management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs of digital models | -0.8% | Global, most acute in price-sensitive Asia-Pacific and Latin America markets | Short term (≤ 2 years) |

| Regulatory approval complexity across regions | -0.5% | Global, with highest friction in Europe (MDR) and China (NMPA) | Medium term (2-4 years) |

| Cybersecurity risk for networked slit lamps | -0.3% | North America and Europe; emerging concern in connected Asia-Pacific hospitals | Medium term (2-4 years) |

| Smartphone-based imaging cannibalization | -0.4% | Asia-Pacific, Middle East, and Africa; limited impact in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Digital Models

Digital units with imaging and AI functions exceed USD 15,000, while service contracts add 10-15% per year[2]Haag-Streit AG, “BM 900 LED and BQ 900 LED,” haag-streit.com. Practices in price-sensitive markets turn to USD 6,950 analog LED devices that forgo imaging. Leasing eases budgets in Japan and Western Europe yet remains rare elsewhere.

Regulatory Approval Complexity Across Regions

Class II status in the United States requires 510(k) clearance in roughly nine months, but Europe’s Medical Device Regulation stretches approval to 18 months and higher cost. China’s streamlined domestic rule accelerates legacy models but leaves AI platforms waiting for extra clinical data. Sequential rather than parallel filings delay global launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Benchtop Precision Versus Portable Growth

Benchtop units represented 71.55% of 2025 revenue, anchoring examination lanes that integrate tonometry and fundus imaging. This share reflects durable optics and stereoscopic depth that surgeons need for cataract planning. Portable devices, however, are forecast to post an 8.25% CAGR to 2031, driven by rural screening programs and veterinary clinics where mobility is essential. Hybrid mobile-cart solutions offer benchtop optics on wheels yet remain expensive, limiting adoption. Handheld models serve pediatric and emergency settings but lack the magnification for detailed mapping. The split shows how differing workflow priorities keep both modalities relevant.

Portable gains demonstrate that throughput advantages alone cannot offset all use cases. Rural health workers prefer battery operation and tablet pairing, while hospital networks rely on fixed lanes for high patient volume. Maintenance standards also diverge; benchtop optics need precise alignment each year, whereas portable devices are designed for field robustness. Leasing options, mainly in Europe, help smaller clinics afford premium benchtops, yet most emerging-market buyers still choose base-spec analog LED models. Over time, AI modules may bridge the capability gap, letting portable units deliver triage accuracy closer to fixed systems, yet surgeons will still require the stability of bench equipment when planning high-risk cases.

By Light Source: LED Economics Drive Adoption

LED commanded 59.53% of 2025 sales and is growing at a 7.55% CAGR because one long-life module replaces a hundred halogen bulbs over the device lifespan. Clinics avoid downtime tied to bulb swaps and enjoy consistent 5,500 K illumination that enhances visualization of subtle corneal edema. Halogen’s remaining share centers on low-budget hospitals and locations with unreliable power where users value simplicity over performance. Xenon survives only in research scenarios needing ultra-high intensity.

Lifecycle economics give LED units a clear payback inside three years, particularly as energy prices rise. China’s domestic suppliers leverage lower production cost to undercut imports by 30–40% while still meeting safety norms, speeding LED penetration in community hospitals. Government tenders increasingly specify LED to minimize operating expense across public programs. If laser-based illumination matures post-2031, the slit lamps market may see another technology leap, yet current lab prototypes remain years from commercialization.

By Technology: AI Platforms Earn Premium Pricing

Analog systems still dominate with 54.23% share because a USD 4,000–8,000 price bracket fits many small practices. Digital imaging-ready units fill the mid-tier at USD 12,000–18,000 and satisfy EHR mandates in developed markets. AI-enabled platforms, forecast to grow at 9.15% CAGR, embed neural networks that flag keratitis or shallow anterior chambers in real time. Confocal and laser variants attract academic centers yet remain cost-prohibitive for general clinics.

Reimbursement trends reinforce the shift toward digital. Payers increasingly require image proof for cataract pre-authorizations, effectively penalizing analog workflows. AI analytics reduce false negatives in primary care, improving referral quality when specialist capacity is scarce. Vendors pair hardware sales with subscription software, creating recurring revenue and raising switching costs. Nevertheless, analog remains entrenched in emerging economies where cash purchase dominates and network connectivity is unreliable. Dual product lines are therefore likely to persist beyond 2031.

By Application: Dry-Eye Imaging Gains Momentum

Cataract assessment accounted for 34.15% of 2025 use, reflecting 28 million global surgeries that each need slit-lamp clearance of lens and cornea. Dry-eye and meibography imaging is projected to rise at 9.45% CAGR as infrared modules quantify gland dropout, turning a once subjective test into a reimbursable procedure. Glaucoma screening remains critical because gonioscopy and optic-nerve exams require the slit lamp’s stereoscopic view of the anterior chamber.

Integrating meibography inside existing platforms lets clinics add a new billable code without extra floor space. Successful adoption hinges on patient education; visualizing gland loss motivates adherence to treatment. For posterior-segment disease, slit lamps play a supportive role only when combined with ancillary lenses, so growth potential centers on anterior-segment conditions. If AI algorithms gain clearance for tear-film analytics, dry-eye imaging may accelerate further.

By End User: Outpatient Migration to ASCs

Hospitals and tertiary eye centers held 61.25% share in 2025 because they manage complex surgeries and postgraduate teaching. Ambulatory surgical centers are set to grow at 9.21% CAGR as payers steer routine cataract extraction to lower-cost outpatient settings where equipment utilization is higher. Ophthalmology clinics serve as gatekeepers, referring surgical cases while managing chronic care with mid-tier digital models.

ASC procurement favors LED digital slit lamps with plug-and-play EHR modules to sustain rapid patient flow. Hospital buyers still seek top-end optics for corneal transplants and ocular trauma triage. Optometry chains and mobile screening programs collectively form a small but innovative buyer group, often piloting portable AI-ready devices before mainstream users adopt them. Veterinary clinics round out demand with specialized models adjusted for animal anatomy.

Geography Analysis

North America led revenue with a 34.55% share in 2025 due to early LED uptake, dense ASC networks, and reimbursement incentives that reward documented imaging. Growth is steady rather than spectacular because the installed base is mature; most purchases replace aging analog systems with digital equivalents. Cybersecurity rules and payer audits further accelerate digital upgrades.

Asia-Pacific is forecast to post a 7.51% CAGR through 2031, the fastest regional pace, propelled by India’s 7 million annual cataract surgeries and China’s streamlined NMPA pathway that helps local vendors compete on price. Japan’s rapidly aging society deepens screening demand, while Australia and South Korea adopt portable AI devices for outreach in remote areas. Price sensitivity keeps analog sales alive, yet bulk government tenders now specify LED modules to minimize running costs.

Europe shows moderate expansion as Medical Device Regulation compliance lengthens approval cycles, favoring incumbents with robust quality systems. Germany and the United Kingdom buy premium digital units to integrate with nationwide EHR platforms, but southern and eastern member states still prioritize upfront savings. Middle East and Africa plus South America collectively add meaningful volume, especially where charitable eye-care missions deploy portable units in rural clinics. Overall, regional divergence reflects income levels and regulatory stringency: developed markets seek digital integration, while emerging markets prioritize broad access using lower-price LED or analog devices.

Competitive Landscape

The slit lamps market is moderately concentrated. Japanese firms Topcon, NIDEK, and Kowa combine optical heritage with wide distribution, while European specialists Haag-Streit and Carl Zeiss Meditec leverage precision engineering and bundled surgical packages to maintain premium positioning[3]Carl Zeiss Meditec AG, “Q3 FY2024 Results,” zeiss.com. Chinese entrants such as Suzhou KangJie Medical Instruments exploit the 2025 NMPA rule that eases domestic production of imported designs, enabling 30–40% price discounts in Asia-Pacific.

Competitive emphasis shifts from optics to software. Keeler’s 2025 launch of a digital slit lamp pre-configured for leading EHR platforms illustrates the move toward workflow integration. IBEXeye targets primary-care networks with AI-enabled devices, bypassing traditional specialist channels. Incumbents respond by acquiring algorithm developers or embedding cloud archives that lock customers into service contracts.

Regulation acts as a moat. FDA and MDR compliance demands extensive documentation, favoring companies with established quality teams. In China, local brands grow quickly at home but face hurdles abroad without CE or FDA approvals. Veterinary ophthalmology and mobile screening form attractive niches where smaller innovators can gain footholds before incumbents adjust portfolios. Overall rivalry intensifies as imaging, AI, and connectivity become mandatory rather than optional.

Slit Lamps Industry Leaders

Haag-Streit AG

Topcon Corporation

Carl Zeiss Meditec AG

NIDEK Co., Ltd.

Keeler Ltd. (Halma plc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Haag-Streit introduced the Elara 900 slit lamp and the Refractor 900 digital phoropter at the ESCRS 2025 Congress in Copenhagen.

- February 2025: DigitalOptometrics unveiled SlitLED, the first autonomous, remotely controlled slit lamp designed for tele-optometry.

Global Slit Lamps Market Report Scope

As per the scope of the report, a slit lamp is a specialized microscope with a bright light used by ophthalmologists and optometrists to examine the anterior segment of the eye, including the eyelids, cornea, conjunctiva, iris, and lens. It provides a magnified, three-dimensional view, allowing detailed assessment of eye structures for diagnosis and treatment.

The slit lamps market is segmented by modality into table-top/benchtop slit lamps, portable slit lamps, hand-held slit lamps, and hybrid/mobile-cart systems; by light source into LED, halogen, xenon, and other emerging sources; by technology into conventional/analog, digital imaging-ready, AI-enabled digital, and confocal/laser slit lamps; by application into cataract examination, glaucoma screening, dry-eye & meibography, macular degeneration & retinal pathology, and other applications; by end user into hospitals & tertiary eye centers, ophthalmology clinics, ambulatory surgical centers, and other end users; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Table-top / Benchtop Slit Lamps |

| Portable Slit Lamps |

| Hand-held Slit Lamps |

| Hybrid / Mobile-cart Systems |

| LED |

| Halogen |

| Xenon |

| Other Emerging Sources |

| Conventional / Analog |

| Digital Imaging-ready |

| AI-enabled Digital |

| Confocal / Laser Slit Lamps |

| Cataract Examination |

| Glaucoma Screening |

| Dry-eye & Meibography |

| Macular Degeneration & Retinal Pathology |

| Other Applications |

| Hospitals & Tertiary Eye Centres |

| Ophthalmology Clinics |

| Ambulatory Surgical Centres |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | Table-top / Benchtop Slit Lamps | |

| Portable Slit Lamps | ||

| Hand-held Slit Lamps | ||

| Hybrid / Mobile-cart Systems | ||

| By Light Source | LED | |

| Halogen | ||

| Xenon | ||

| Other Emerging Sources | ||

| By Technology | Conventional / Analog | |

| Digital Imaging-ready | ||

| AI-enabled Digital | ||

| Confocal / Laser Slit Lamps | ||

| By Application | Cataract Examination | |

| Glaucoma Screening | ||

| Dry-eye & Meibography | ||

| Macular Degeneration & Retinal Pathology | ||

| Other Applications | ||

| By End User | Hospitals & Tertiary Eye Centres | |

| Ophthalmology Clinics | ||

| Ambulatory Surgical Centres | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the slit lamps market in 2031?

The market is expected to reach USD 405.49 million by 2031.

Which modality is growing fastest through 2031?

Portable slit lamps lead growth with an 8.25% CAGR through 2031.

Why are LED slit lamps replacing halogen models?

LEDs cut energy use, eliminate frequent bulb changes, and deliver consistent color temperature for more reliable diagnosis.

How will AI influence purchasing decisions for slit lamps?

AI-enabled units provide automated pathology flags that improve triage accuracy, making them attractive despite higher price.

Which region offers the highest growth opportunity?

Asia-Pacific shows the fastest regional expansion with a 7.51% CAGR through 2031, supported by large cataract surgery volumes and favorable local regulations.

What limits adoption of digital slit lamps in emerging markets?

High upfront cost and complex regulatory approvals slow uptake where reimbursement does not reward imaging records.

Page last updated on: