Slide Stainer Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

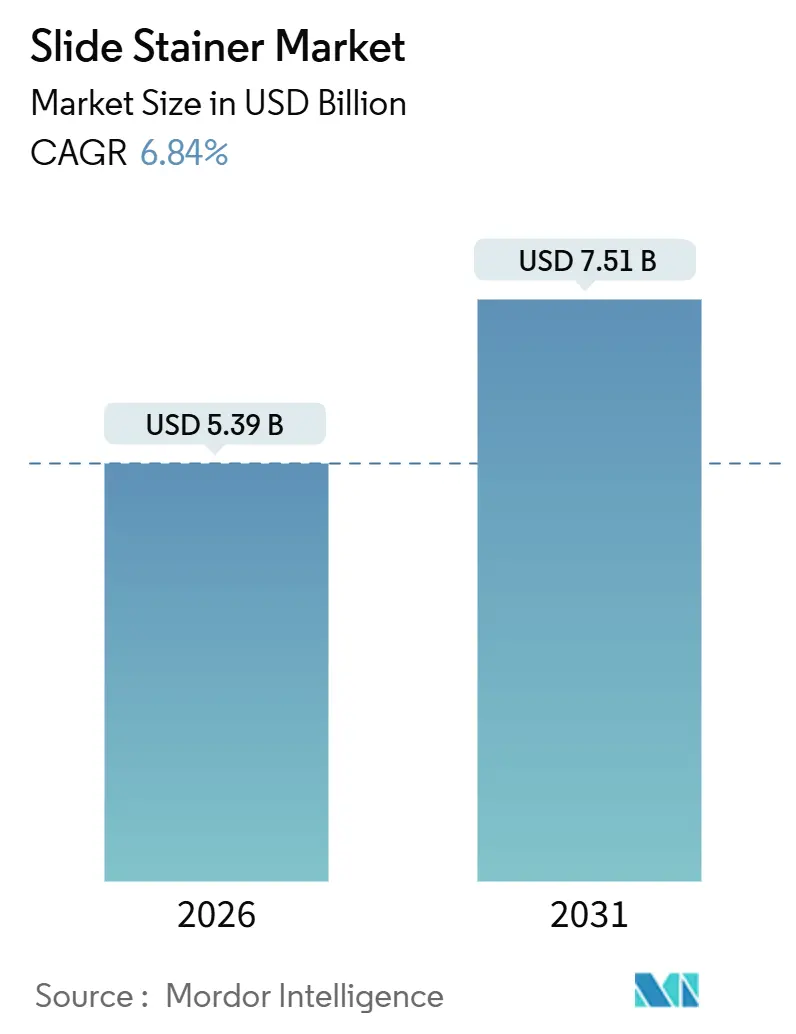

| Market Size (2026) | USD 5.39 Billion |

| Market Size (2031) | USD 7.51 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

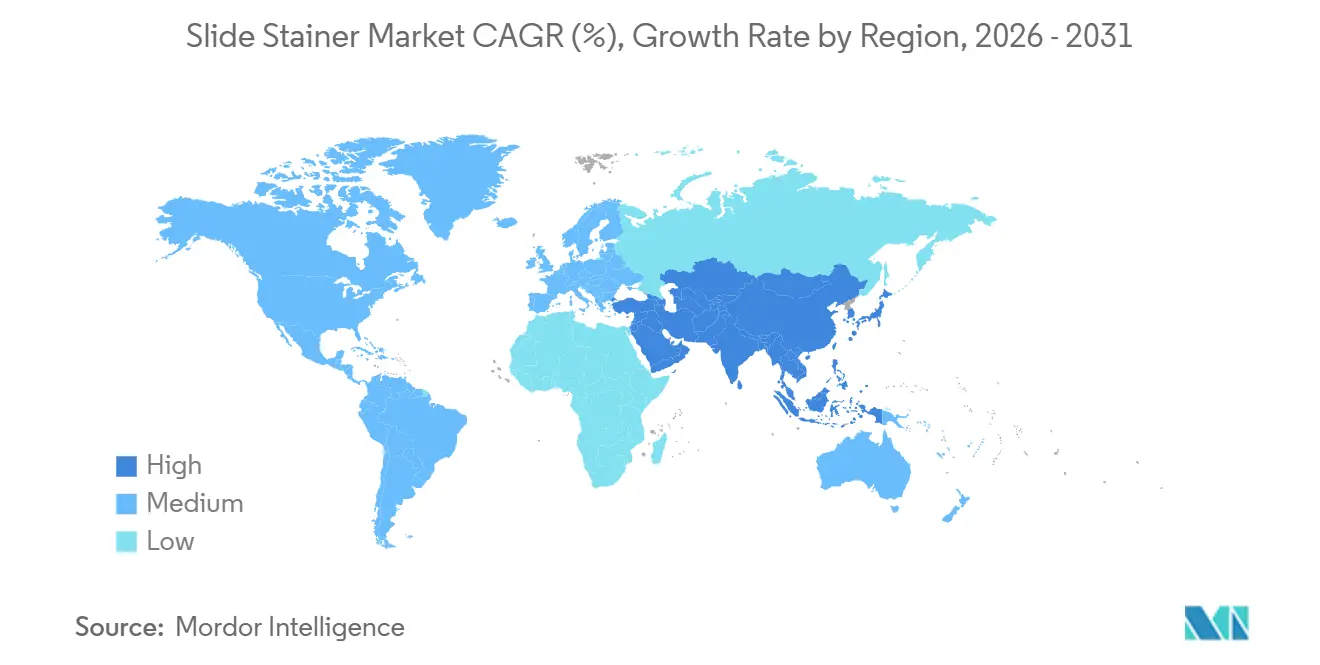

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

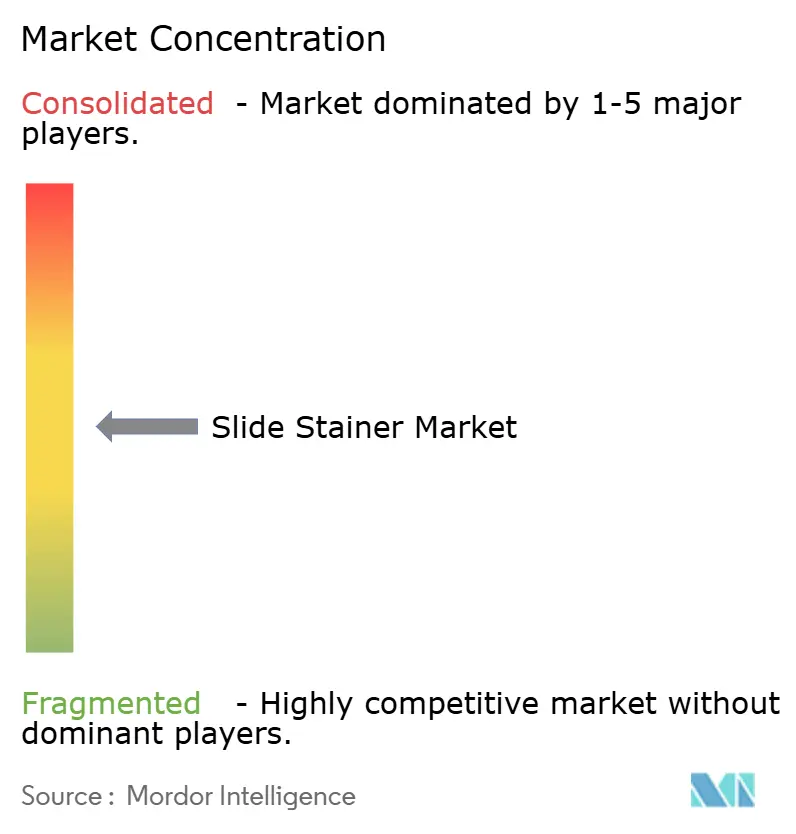

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slide Stainer Market Analysis by Mordor Intelligence

The Slide Stainer Market size is estimated at USD 5.39 billion in 2026, and is expected to reach USD 7.51 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031).

Rising cancer biopsy volumes, expanding outpatient surgery numbers, and the need to automate labor-intensive staining workflows underpin this expansion. North American hospitals continue to refresh aging fleets, while Asia-Pacific laboratories draw investment from multinational vendors that localize production to avoid tariff exposure. Centralized reference laboratories demand high-volume systems that process more than 350 slides per hour, whereas community hospitals gravitate toward reagent-funded leases that convert capital purchase outlays into predictable operating expenses. Competitive intensity centers on reagent ecosystem control, FDA-cleared companion diagnostics, and pay-per-use service models that lock laboratories into multi-year consumable contracts.

Key Report Takeaways

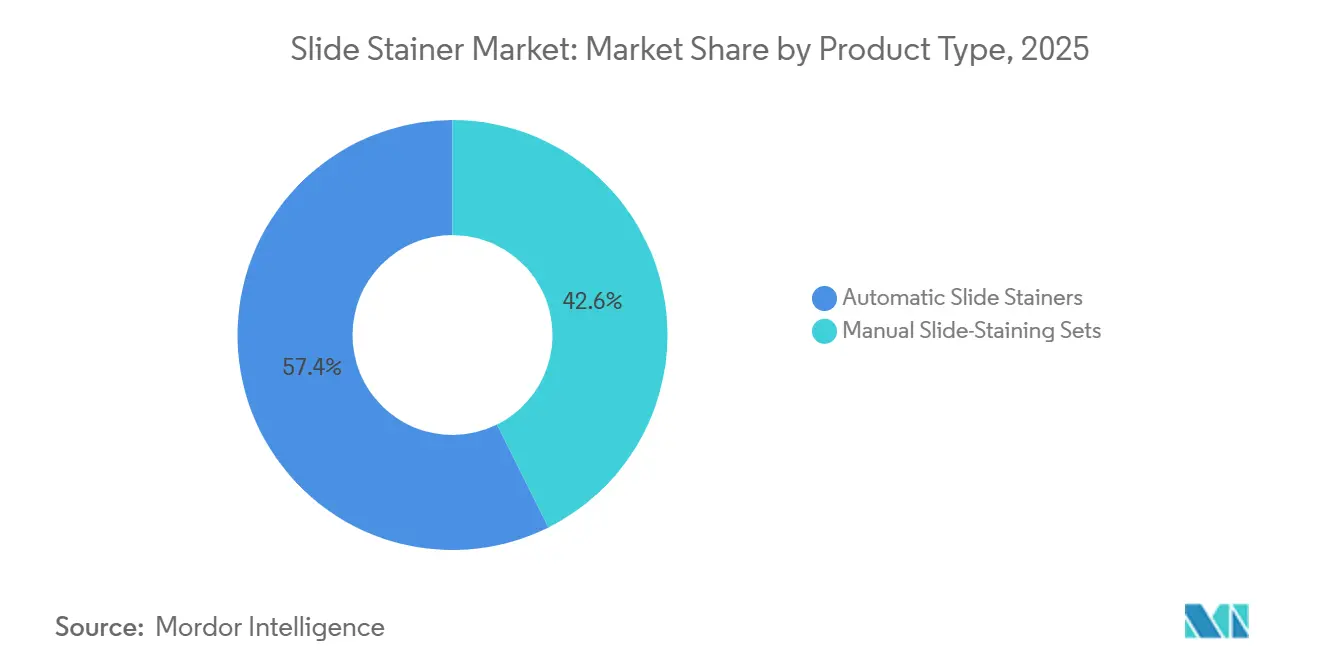

- By product type, automated slide stainers commanded 57.36% of revenue in 2025 and are advancing at a 9.35% CAGR through 2031, far outpacing manual sets.

- By throughput capacity, mid-volume systems (120–350 slides per hour) held 43.52% of the slide stainer market share in 2025, while high-volume platforms above 350 slides per hour exhibit the fastest growth at 8.73% through 2031.

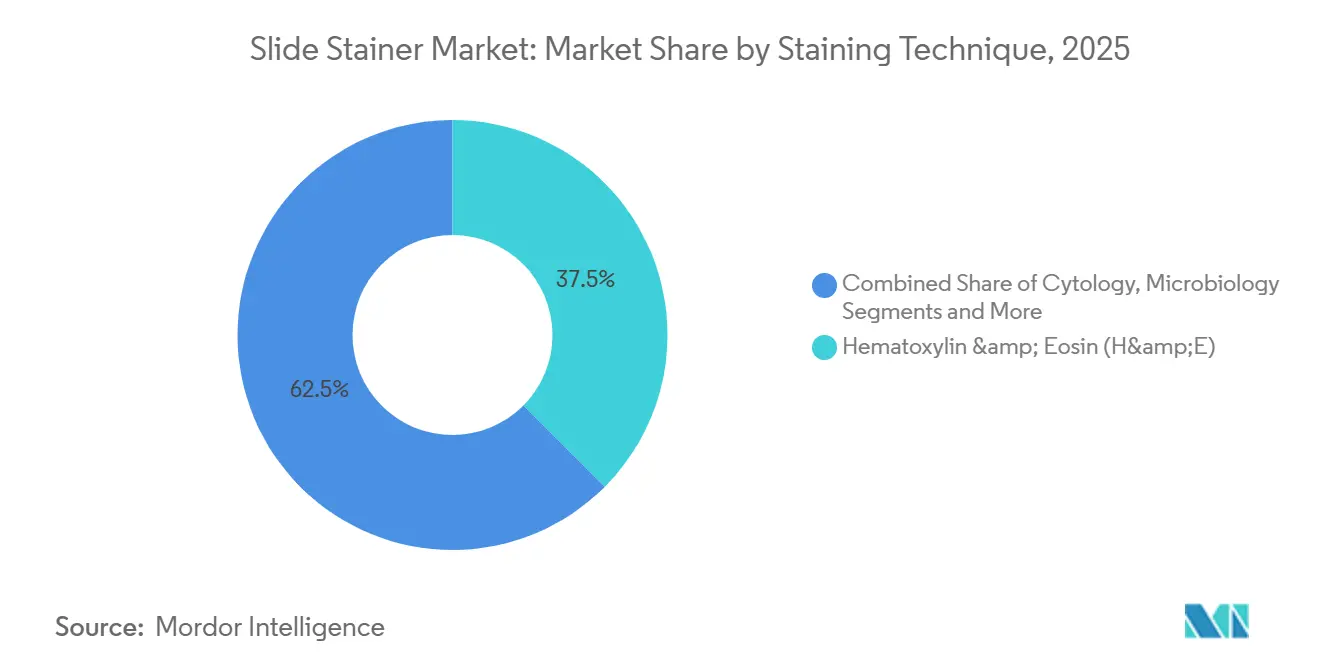

- By staining technique, hematoxylin and eosin staining retained 37.46% of the slide stainer market size in 2025, yet immunohistochemistry grows at 9.25% on the back of new FDA-cleared companion diagnostics.

- By end user, hospitals and diagnostic centers accounted for 53.53% of demand in 2025, although pharmaceutical and biotechnology companies post the highest CAGR at 10.34% through 2031.

- By Geography, North America generated 39.11% of 2025 global revenue, whereas Asia-Pacific is the fastest expanding region, forecast to grow at 8.24% until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Slide Stainer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cancer incidence driving biopsy volumes | +1.5% | Global, highest growth in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Automation demand to offset lab-staff shortages | +1.3% | North America and Europe core, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Digitization and LIS/AI integration | +1.2% | Early adoption in North America and Europe, Asia-Pacific following | Medium term (2-4 years) |

| Surge in ambulatory and outpatient surgeries | +0.9% | Dominant in North America, moderate in Europe, nascent in Asia-Pacific | Medium term (2-4 years) |

| Emerging pay-per-use service models | +0.8% | North America and Europe, selective Asia-Pacific metros | Short term (≤ 2 years) |

| Regional localization to avoid tariff shocks | +0.7% | India, Vietnam, Mexico manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Cancer Incidence Driving Biopsy Volumes

The International Agency for Research on Cancer logged 20 million new cancer cases in 2022 and expects 35 million by 2050, a 77% increase that directly enlarges histopathology workloads.[1]Christopher Wild, “Cancer Today,” International Agency for Research on Cancer, who.int Multi-marker immunohistochemistry panels now accompany most surgical resections, multiplying slide counts per case. New FDA-approved assays such as Roche’s VENTANA CLDN18, cleared in October 2024 for gastric cancers, further expand mandatory testing panels.[2]U.S. Food and Drug Administration, “FDA Approves Roche VENTANA CLDN18 for Gastric Cancer,” fda.gov Laboratories unable to automate face mounting two-day reporting expectations that contrast sharply with manual staining cycles spanning up to five days.

Automation Demand to Offset Lab-Staff Shortages

Vacancy rates of 13%–18% across U.S. histology and cytology departments, coupled with 7- to 12-month hiring timelines, compel hospitals to adopt walk-away stainers that cut hands-on time from 90 minutes to 15 minutes per batch.[3]Allison Bettini, “2024 Vacancy Survey of Medical Laboratories in the United States,” American Society for Clinical Pathology, ascp.orgRoche’s VENTANA HE 600, cleared in 2025, processes 200 slides per hour and allows one technologist to supervise multiple instruments. Rural hospitals and secondary European centers view automation not only as a productivity tool but also as a workforce-continuity safeguard.

Digitization and LIS/AI Integration

FDA clearance of the VENTANA DP 600 scanner in January 2025 catalyzed adoption of closed-loop ecosystems where stainers, scanners, and laboratory information systems exchange barcoded metadata. Agilent’s Dako Omnis family embeds RFID-tagged reagent tracking, shrinking specimen misidentification rates from 1 in 1,000 to 1 in 10,000. Artificial-intelligence algorithms now detect uneven staining and trigger instant re-runs, trimming pathologist turnaround times and redefining vendors as software partners rather than pure hardware suppliers.

Surge in Ambulatory and Outpatient Surgeries

Medicare-certified ambulatory surgery centers performed 28.4 million procedures in 2023, sending specimen volumes to centralized reference laboratories that rely on stainers capable of 350–500 slides per hour. High-throughput demand underpins the high CAGR forecast for the high-volume subsegment. Random-access designs, such as Sakura’s Tissue-Tek Genie, accommodate diverse batches from dozens of centers while ensuring same-day diagnoses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of fully automated systems | -0.9% | Emerging markets and rural North America/Europe | Medium term (2-4 years) |

| Chronic shortage of trained biomedical engineers and histotechnologists | -0.7% | Asia-Pacific, Middle East & Africa, South America | Long term (≥ 4 years) |

| Stringent FDA / CE regulatory timelines | -0.6% | North America and Europe | Long term (≥ 4 years) |

| Supply-chain fragility for critical reagents | -0.5% | Global, acute where single-source suppliers dominate | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Fully Automated Systems

Fully automatic stainers list at USD 150,000–USD 300,000, while mandatory service contracts add 10%–15% annually, limiting adoption in cash-constrained hospitals. Currency swings of up to 20% during procurement amplify affordability challenges in India, Indonesia, and parts of Africa. Pay-per-use programs partly offset hurdles but remain concentrated in credit-rich markets.

Chronic Shortage of Trained Biomedical Engineers and Histotechnologists

India graduates fewer than 2,000 histotechnologists a year against demand exceeding 10,000, extending equipment downtime to five days when spare parts or expertise are unavailable. Similar gaps in Southeast Asia drive service-contract premiums and limit take-up of advanced AI-driven quality-control modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automation Accelerates Pharma Adoption

Automated systems captured 57.36% of 2025 revenue, driven by pharmaceutical and biotechnology companies that require standardized, auditable workflows for companion diagnostics. The subsegment will expand at 9.35% through 2031, well above the slide stainer market average. Semi-automatic platforms attract mid-tier hospitals balancing budget caution with protocol consistency, especially in Europe. Manual sets persist in low-volume veterinary and forensic settings, retaining flexibility at the cost of labor. Automated configurations that integrate slide handling, reagent dispensing, and waste collection dominate upgrades as contract research organizations chase walk-away operation.

Manual kits still serve exploratory research and irregular workload environments, yet their share declines as reagent-funded leases lower financial barriers. Agilent’s Dako Omnis line illustrates the migration path from entry automation to high-capacity configurations. This maturity curve aligns adoption stages with capital availability and throughput needs, reflecting an orderly progression across the slide stainer industry.

By Throughput Capacity: Centralization Favors High-Volume Platforms

High-volume platforms able to process more than 350 slides per hour are forecast to grow at 8.73% through 2031, supported by the consolidation of specimens from 6,110 U.S. ambulatory surgery centers that executed 28.4 million procedures in 2023. Mid-volume units, which held 43.52% of the 2025 slide stainer market share, remain staples in hospital labs processing 200–500 specimens daily. Low-volume machines now address niche intraoperative and point-of-care use. Modular high-throughput architectures minimize footprint while maximizing capacity, fitting the hub-and-spoke logistics model of large reference laboratories.

Mid-volume designs will continue in tertiary hospitals where batch variability demands flexibility. Integrated printers such as Leica’s HistoCore Lightning S cut pre-analytical errors, tightening loops with laboratory information systems. Low-volume equipment sustains translational research and veterinary diagnostics that value protocol agility over speed. Throughput capacity trends mirror broader health-care centralization, with hubs consuming the lion’s share of new investment while spokes depend on mid-scale versatility.

By Staining Technique: IHC Gains on Precision Oncology

Hematoxylin and eosin remains foundational, representing 37.46% of 2025 revenue, yet immunohistochemistry advances at 9.25% as HER2-ultralow and MAGE-A4 assays widen precision-oncology panels. In situ hybridization grows in tandem as reflex testing follows equivocal IHC outcomes. Cytology staining faces volume shifts from HPV molecular screening but expands in low-income regions where Pap tests remain standard. Microbiology and hematology stains stay niche and largely manual. Special stains retain importance for renal, liver, and connective-tissue evaluation, driving laboratories to favor mid-volume platforms with open reagent compatibilities.

Regulatory clearances for new biomarkers reinforce IHC expansion, embedding stainers within closed-loop platforms that collect metadata for digital pathology review. Vendors position software analytics as differentiators, ensuring staining techniques evolve beyond chemistry into data-rich diagnostic workflows across the slide stainer market size spectrum.

By End User: Pharma and Biotech Outpace Hospitals

Hospitals and diagnostic centers delivered 53.53% of 2025 orders, yet pharma and biotech firms lead growth at 10.34% through 2031. Contract research organizations aggregate trial specimens, favoring high-volume throughput and 21 CFR Part 11 compliant audit trails. Academic institutes balance flexibility and compliance, adopting scalable systems suited to exploratory research destined for clinical transition. Forensic and environmental labs continue using small-batch solutions geared toward non-standard slides.

Vendor partnerships, such as Danaher’s precision-medicine alliance with Leica Biosystems, illustrate the pivot from equipment sales to integrated tissue-processing ecosystems. End-user segmentation therefore reflects a widening gap between volume-driven commercial demand and resource-constrained institutional settings, shaping future product road maps within the slide stainer industry.

Geography Analysis

North America generated 39.11% of 2025 revenue, driven by Medicare reimbursement stability and high installed bases. Replacement cycles and digital pathology integration sustain a region-wide 6.84% CAGR. Pay-per-use leasing lets community hospitals deploy automation while preserving capital. Canada and Mexico contribute incremental gains, with Mexican demand boosted by USMCA-aligned local manufacturing.

Asia-Pacific shows the fastest trajectory at 8.24% through 2031. Roche’s USD 100 million Hyderabad plant, Siemens Healthineers’ USD 250 million Bengaluru expansion, and Danaher’s USD 80 million Suzhou center shorten lead times and sidestep tariff exposures. India’s National Health Mission and China’s Healthy China 2030 funnel funding to county laboratories, spurring mid-volume stainer uptake. Japan and South Korea emphasize telepathology to serve aging populations; Southeast Asian markets battle technician shortages that elongate downtime.

Europe retains a mid-20s percentage share, constrained by Medical Device Regulation compliance costs that push hospitals toward incremental rather than wholesale upgrades. Eastern European nations benefit from EU structural funds, while Western Europe focuses on digital integration. The Middle East invests in tertiary centers for medical tourism, whereas much of Africa relies on donor programs and manual staining. South America, led by Brazil and Argentina, faces tariff-inflated pricing yet tracks the global average CAGR as currency stabilizes post-2024. Abbott’s USD 40 million Indian diagnostic expansion underlines vendor strategies that localize production to serve emergent growth corridors.

Competitive Landscape

Market concentration is moderate. Danaher’s USD 5.7 billion Abcam acquisition secures monoclonal antibody supply, reinforcing entry barriers. Thermo Fisher’s USD 912.5 million CorEvitas purchase extends real-world evidence offerings, creating bundled propositions for pharma clients. Smaller players like Sakura Finetek, Biocare Medical, and Epredia differentiate via random-access architectures and rapid service commitments in secondary cities.

Artificial-intelligence quality control and closed-loop scanner integration represent emerging battlefields, shifting competition from hardware to software value. Cardinal Health and Excedr disrupt legacy capital sales through reagent-funded leases that turn equipment into a service, recasting revenue streams around consumables and maintenance. Asian challengers Dakewe Biotech and Fuzhou Maixin undercut pricing by up to 40%, appealing to budget-sensitive markets but must overcome lengthy U.S. and EU regulatory pathways.

Regulatory compliance remains a strong moat. Six-month to one-year 510(k) cycles and USD 1 million-plus validation costs favor incumbents that maintain clinical trial networks and regulatory affairs teams. As reliance on digital pathology deepens, vendors able to deliver cybersecurity-ready, fully validated platforms stand to fortify their leadership within the slide stainer market.

Slide Stainer Industry Leaders

Sakura Finetek Japan Co., Ltd.

F. Hoffmann–La Roche Ltd

Danaher Corporation

Thermo Fisher Scientific Inc.

Agilent Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Agilent Technologies launched the Dako Omnis family of automated stainers, adding barcode and RFID tracking that cut misidentification rates tenfold.

- April 2025: Dartmon introduced the AS100, a compact benchtop IHC/ISH stainer that automates 10 slides per cycle for small laboratories.

- January 2025: Roche secured FDA clearance for the VENTANA DP 600 scanner with 240-slide capacity and 40-fold throughput improvement over the prior model, enabling same-day imaging.

Global Slide Stainer Market Report Scope

A slide stainer is a laboratory device that automates the application of biological stains, such as H&E and IHC, to microscope slides containing tissue or cell samples. It ensures precise and timed dye application and rinsing, highlighting structures for microscopic analysis while providing consistency, speed, and reduced manual errors compared to traditional staining methods.

The Slide Stainer Market Report is Segmented by Product Type, throughput capacity, staining technique, end user and geography. By product type, the market is segmented into Automated Slide Stainers and Manual Slide-Staining Sets. The automated Slide Stainer is further subsegmented into Fully Automatic and Semi-automatic. By Throughput Capacity, the market is segmented into Low-Volume, Mid-Volume, and High-Volume. By Staining Technique, the market is segmented into H&E, IHC, ISH, Cytology, Microbiology, Hematology, and Special Stains. By End User, the market is segmented into Hospitals & Diagnostic Centers, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, CROs, Forensic & Environmental Labs. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Automated Slide Stainers | Fully Automatic |

| Semi-automatic | |

| Manual Slide-Staining Sets |

| Low-Volume (<120 slides/hour) |

| Mid-Volume (120–350 slides/hour) |

| High-Volume (>350 slides/hour) |

| Hematoxylin & Eosin (H&E) |

| Immunohistochemistry (IHC) |

| In Situ Hybridisation (ISH) |

| Cytology |

| Microbiology |

| Hematology |

| Special Stains |

| Hospitals & Diagnostic Centers |

| Academic & Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organisations |

| Forensic & Environmental Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Automated Slide Stainers | Fully Automatic |

| Semi-automatic | ||

| Manual Slide-Staining Sets | ||

| by Throughput Capacity | Low-Volume (<120 slides/hour) | |

| Mid-Volume (120–350 slides/hour) | ||

| High-Volume (>350 slides/hour) | ||

| By Staining Technique | Hematoxylin & Eosin (H&E) | |

| Immunohistochemistry (IHC) | ||

| In Situ Hybridisation (ISH) | ||

| Cytology | ||

| Microbiology | ||

| Hematology | ||

| Special Stains | ||

| By End User | Hospitals & Diagnostic Centers | |

| Academic & Research Institutes | ||

| Pharmaceutical & Biotechnology Companies | ||

| Contract Research Organisations | ||

| Forensic & Environmental Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the slide stainer market in 2026?

It stands at USD 5.39 billion and is forecast to reach USD 7.51 billion by 2031, yielding a 6.84% CAGR.

Which segment grows fastest within slide stainers?

Automated, fully automatic systems post a 9.35% CAGR as laboratories replace manual workflows.

Why is immunohistochemistry gaining share?

Companion diagnostics cleared between 2024 and 2025 expand multi-marker testing, boosting IHC volumes at a 9.25% rate.

What drives Asia-Pacific demand?

Local manufacturing investments by Roche, Siemens Healthineers, and Danaher shorten lead times and align pricing with India’s National Health Mission and China’s Healthy China 2030 projects.

How do pay-per-use leases benefit laboratories?

Reagent-funded models convert USD 150,000–USD 300,000 capital costs into monthly fees, cutting five-year ownership costs by up to 30%.

Page last updated on: