Sintered Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 30.65 Billion |

| Market Size (2031) | USD 40.89 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sintered Steel Market Analysis by Mordor Intelligence

The Sintered Steel Market size is expected to increase from USD 29.11 billion in 2025 to USD 30.65 billion in 2026 and reach USD 40.89 billion by 2031, and is expected to grow at a CAGR of 5.93% over 2026-2031. The sintered steel market draws demand from automotive powertrain manufacturing, industrial machinery, and electrified drivetrain applications, including e-axle reduction gearboxes, soft magnetic composite motor cores, and electric power steering assemblies. The shift toward energy-efficient mobility is expanding the role of sintered steel beyond conventional engine parts, as press-and-sinter methods can produce complex shapes at scale with less material waste than many machined alternatives. Asia-Pacific remained the largest regional market, supported by China's large vehicle production base and India's policy-backed push for auto component manufacturing. The market also reflects rising competitive overlap among integrated powder producers, automotive powder metallurgy (PM) suppliers, and specialist metal injection molding (MIM) manufacturers as end-use boundaries become less rigid. Raw material volatility remains a structural pressure point, but long original equipment manufacturer (OEM) relationships, process familiarity, and the economics of near-net-shape production continue to support the cost position of sintered steel in high-volume programs.

Key Report Takeaways

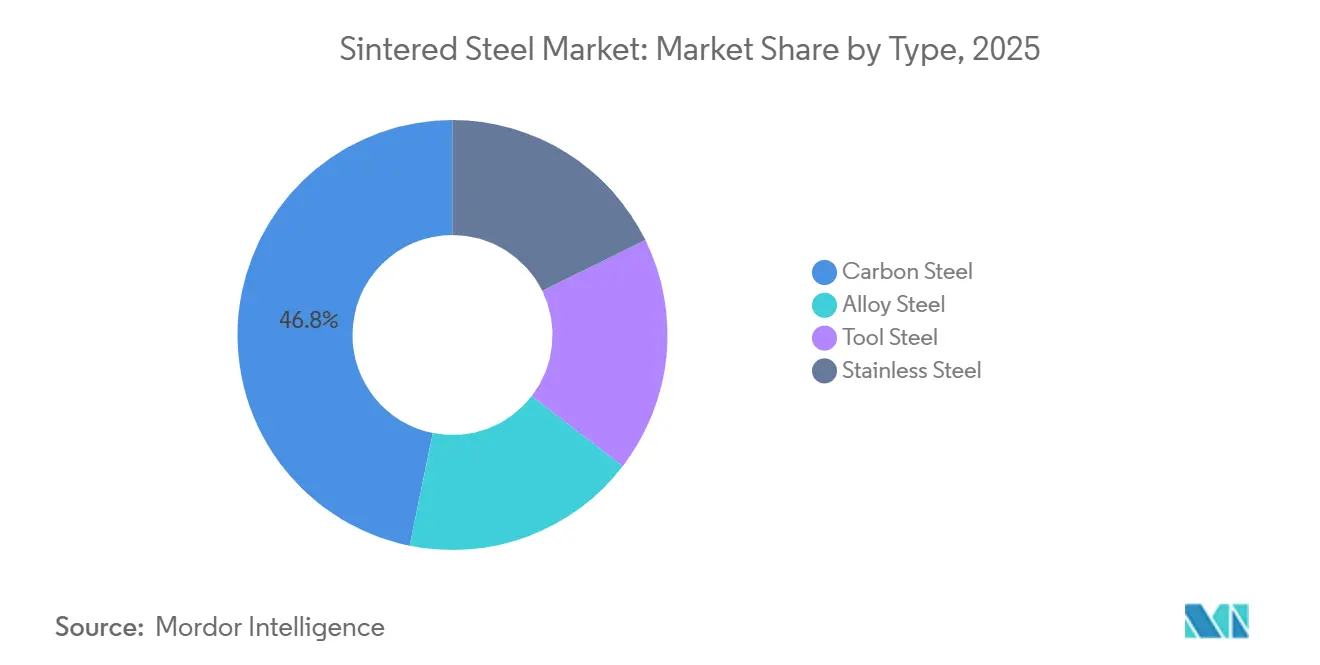

- By type, carbon steel led with 46.82% share in 2025, while stainless steel is projected to expand at 6.84% CAGR through 2031.

- By process, conventional powder metallurgy held 50.89% share in 2025, while additive manufacturing is projected to grow at 7.36% CAGR through 2031.

- By application, gears and transmission components accounted for 29.84% share in 2025, while electrical and magnetic components are forecast to advance at 7.21% CAGR through 2031.

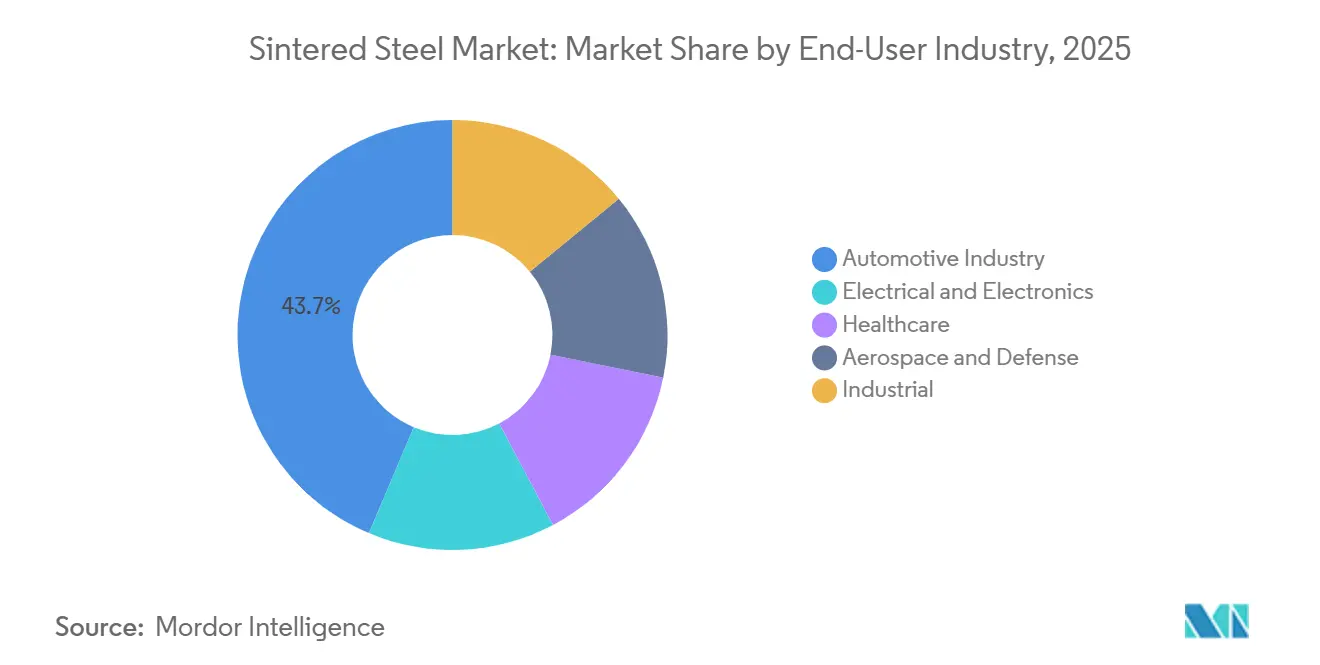

- By end-user industry, automotive held 43.65% share in 2025, while electrical and electronics is projected to expand at 7.43% CAGR through 2031.

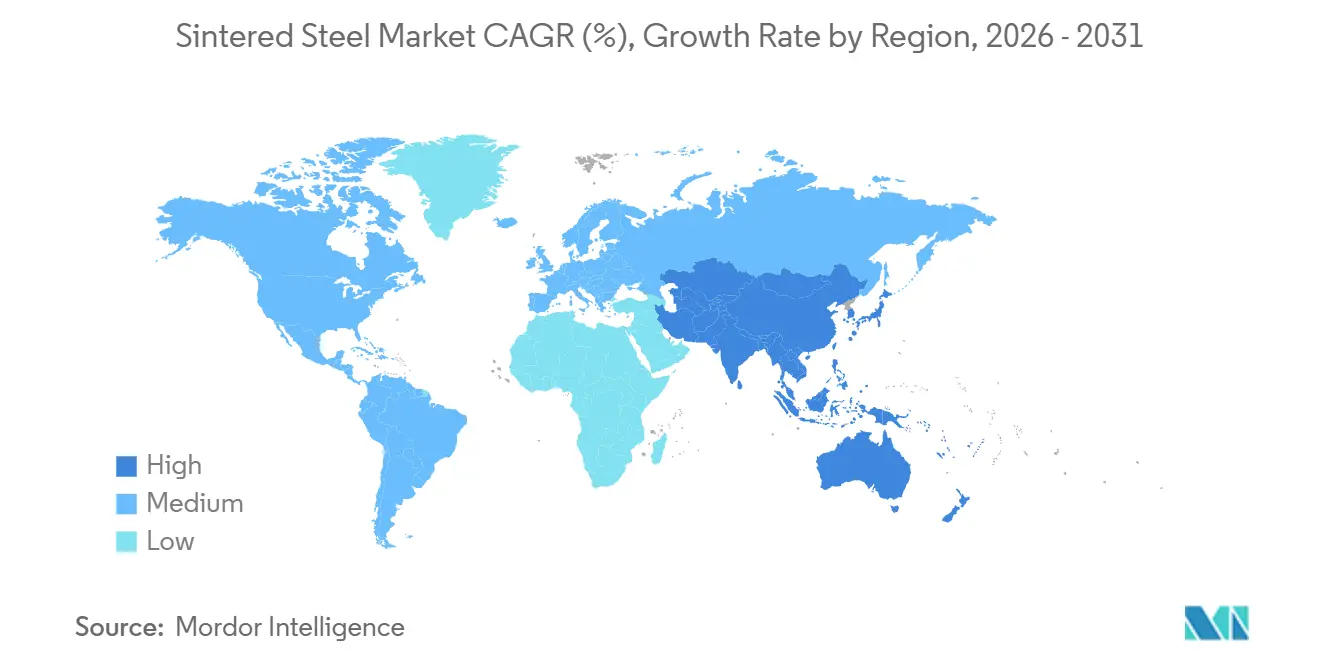

- By geography, Asia-Pacific captured 48.32% of global revenue in 2025 and is also expected to post the fastest regional CAGR of 6.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sintered Steel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Sintered Steel in Automotive Applications | +2.1% | Global, the highest in Asia-Pacific, North America, and Europe | Medium term (2-4 years) |

| Rising Demand for Sintered Components in Electric Vehicles | +1.2% | Global, strongest in China, Germany, and South Korea | Long term (≥ 4 years) |

| Expansion of the Industrial Manufacturing Sector | +0.8% | Asia-Pacific core, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Increasing Preference for Near-Net-Shape Manufacturing | +0.5% | Global | Short term (≤ 2 years) |

| Growing Adoption of Metal Injection Molding | +0.4% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Sintered Steel in Automotive Applications

Automotive manufacturing remains the largest end market for sintered steel, as drivetrain and chassis programs continue to absorb high volumes of powder metal parts. The automotive sector accounted for more than 70% of iron powder shipments in North America in 2024, highlighting how closely vehicle output shapes order flow in the sintered steel market. North American new-vehicle sales reached 15.9 million units in 2024, and hybrid sales rose by nearly 37%, keeping powder metal demand firm even as OEM powertrain mixes began to shift. Gears, connecting rods, bearing caps, and synchronizer hubs remain core volume products, as they offer repeatable tolerances and strong throughput economics at scale. Research published in 2026 found that two-speed EV gearboxes can improve highway-cycle motor efficiency by 5% to 7% compared to single-speed hardware, supporting further use of sintered planet carriers and differential components in future vehicle architectures[1]“Electric Drive Axle Systems In New Energy Vehicles,” Frontiers in Mechanical Engineering, frontiersin.org. This shift helps the sintered steel market remain relevant even as demand for Internal Combustion Engine (ICE)-only parts eases over time.

Rising Demand for Sintered Components in Electric Vehicles

Electric vehicle (EV) adoption is expanding the addressable market for sintered steel, as new EV platforms require motor, gearbox, and steering components that support compact, efficient designs. Global electric car sales exceeded 17 million units in 2024, up 25% from 2023, lifting demand for soft magnetic composite (SMC) motor cores, e-axle planetary carriers, and electric power steering pump rotors. A 2024 study published in Metals reported that SMC materials for EV motors can reduce core losses by more than 20%, strengthening the case for their use in compact motor layouts where efficiency gains are critical. Another 2024 paper showed that sintered SMC motor cores can deliver efficiency comparable to 0.35 mm non-oriented silicon steel laminations while enabling three-dimensional flux paths that are difficult to achieve with stacked laminations. India's Production Linked Incentive Scheme allocated INR 10,000 crore (USD 1.2 billion) for automobile and auto component manufacturing, including technologies relevant to powder metallurgy adoption. These developments give the sintered steel market a larger role in the vehicle transition, rather than limiting it to legacy engine content.

Expansion of the Industrial Manufacturing Sector

The expanding industrial manufacturing base is broadening demand for sintered steel beyond automotive applications, as many machine builders require bearings, bushings, actuator gears, and valve components with repeatable dimensions and controlled porosity. Rising industrial demand was evident in North America during 2024, when demand for molybdenum, a key alloying element in high-performance sintered grades, climbed by nearly 17% across aerospace, automotive, electronics, defense, and medical applications. Defense demand is also contributing to growth, as increased military spending in 2024 and 2025 boosted tungsten carbide powder demand for armor-piercing applications and encouraged secondary recovery and mine development in North America. This broader industrial spread reduces the sintered steel market's historical dependence on a single end-user cycle. It also benefits suppliers that can serve multiple verticals using the same base materials, tooling knowledge, and finishing capabilities. As more factories in Asia-Pacific expand local production, the sintered steel market stands to gain from both direct component demand and deeper regional supply chains.

Growing Adoption of Metal Injection Molding

Metal injection molding (MIM) is becoming an important growth route in the sintered steel market, as it enables the production of small and complex parts that standard press-and-sinter lines cannot produce within the same dimensional envelope. The process is particularly relevant in medical devices, defense hardware, electronics, and precision consumer goods, where part geometry, surface finish, and tight tolerances are simultaneously required. Indo-MIM filed a Draft Red Herring Prospectus with the Securities and Exchange Board of India (SEBI) in September 2025 to raise INR 1,000 crore (USD 113 million) for capacity expansion and advanced binder jetting systems at its Bengaluru facility. This filing indicates that producers continue to direct capital toward higher-value sintering routes rather than relying solely on conventional automotive volumes. Stainless grades such as 316L and 17-4PH remain central to MIM programs for medical and defense parts, as they combine corrosion resistance with dimensional consistency in miniaturized designs. This process trend broadens the demand base for the sintered steel market and supports stronger pricing in segments where precision is prioritized over tonnage.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Requirements | -0.6% | Global, with a disproportionate effect on Small and Medium-sized Enterprises (SMEs) in emerging markets | Medium term (2-4 years) |

| Volatility in Raw Material Prices | -0.5% | Global, most acute in Europe and the Asia-Pacific | Short term (≤ 2 years) |

| Competition for Alternative Manufacturing Processes | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements

High capital requirements continue to restrain the sintered steel market, as advanced furnaces, compaction systems, and tooling demand substantial upfront investment before stable program volumes are secured. Vacuum sintering furnaces range from USD 55,000 to more than USD 200,000 per unit, while complete press-and-sinter lines often require multi-million-dollar expenditure. The financial burden increases further when part designs require complex multi-level dies, as those tools must be amortized across large production runs to justify the investment. This challenge is more pronounced in newer Powder Metallurgy (PM) geographies, where low-cost financing, skilled furnace operators, and stable, long-term Original Equipment Manufacturer (OEM) contracts remain limited. The burden grows further when producers add industrial binder jetting or powder bed systems, as these technologies create a second capital layer on top of the standard sintering line. As a result, the sintered steel market in emerging regions continues to expand through licensed capacity or supplier partnerships rather than independent greenfield plants.

Volatility In Raw Material Prices

Raw material price volatility constrains the sintered steel market because iron powder, nickel, chromium, and molybdenum prices can shift faster than component contracts are reset with OEM buyers. Standard water-atomized iron powder traded in the USD 800 to USD 1,200 per metric ton range during 2025 and 2026, while premium highly compressible grades carried a 15% to 25% price premium. Supply uncertainty is more severe for alloy-rich grades, and the North American molybdenum outlook was affected by mine closures and changing Chinese export rules during the study period. Höganäs is responding with a biochar substitution program that targets 20% replacement of fossil coal in sponge iron production, which can reduce carbon-related exposure and sensitivity to energy price fluctuations[2]Höganäs AB, “Sustainability Report 2025,” Höganäs AB, hoganas.com. Vertically integrated producers, therefore, retain an advantage in the sintered steel market, as they can manage feedstock risk more effectively than component makers that purchase powder on the spot market. This cost gap can widen when OEM pricing remains fixed while alloy prices rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carbon Steel Anchors Volume While Stainless Steel Gains In Performance-Driven Niches

Carbon steel held 46.82% of the sintered steel market share in 2025, maintaining its lead among material types. Its position is based on low input costs, broad compatibility with conventional tooling, and a long track record of performance in high-volume automotive and industrial applications. Alloy steel sits above it in the value chain because nickel, molybdenum, and copper additions support higher tensile strength and better fatigue resistance in demanding components. Tool steel remains smaller in volume, but it serves precision insert applications and specialized machinery where wear performance matters more than tons. Stainless steel is the fastest-growing type, with a 6.84% CAGR through 2031, because medical devices, corrosion-sensitive electrical assemblies, and food processing equipment require material properties that carbon grades cannot provide.

This shift indicates that the sintered steel market is no longer shaped only by the lowest-cost material route, as qualification standards in newer end uses are changing what buyers accept. Stainless grades also lend themselves well to metal injection molding (MIM) production when miniaturization and clean-surface requirements are priorities. That combination gives suppliers room to move into higher-value programs even when total volume remains lower than carbon steel. Material decisions are also increasingly tied to customer sustainability goals, as original equipment manufacturer (OEM) buyers are paying closer attention to Scope 3 emissions in the upstream supply chain. Höganäs reported continued investment in lower-carbon powder production and disclosed a 55% reduction in Scope 1 and 2 emissions versus 2018, demonstrating how material suppliers are differentiating beyond mechanical performance alone. In this context, the sintered steel market is likely to reward producers that can pair reliable metallurgy with stronger sustainability credentials.

By Process: Conventional Powder Metallurgy Sustains Leadership While Additive Routes Expand Design Flexibility

Conventional powder metallurgy accounted for 50.89% of the market in 2025, making it the leading process route in the sintered steel market. That position reflects strong economics in large automotive and industrial programs where fixed tooling costs can be spread over high production volumes. The process also benefits from high material utilization, estimated at near 95%, compared with much lower yields for fully machined equivalents. Metal injection molding is the next tier, serving medical, defense, electronics, and precision consumer goods applications with tighter tolerances than standard press-and-sinter operations typically provide. Powder forging remains important for high-density structural parts such as connecting rods and synchronizer rings, where near-full density is required. Additive manufacturing is the fastest-growing process, with a 7.36% CAGR through 2031, indicating that design complexity and low-volume flexibility are becoming increasingly important in the sintered steel market.

This does not mean additive routes will displace conventional powder metallurgy (PM) in bulk programs, as the cost logic still favors traditional tooling once volumes scale. It does mean that the process mix within the sintered steel market is broadening as aerospace, defense, and medical buyers move from prototyping toward production qualification. Metal injection molding (MIM) also benefits from this shift because it sits between scale manufacturing and precision machining, making it attractive for parts that are too intricate for conventional pressing but too costly for pure machining. Indo-MIM's September 2025 filing for INR 1,000 crore (USD 113 million) to fund capacity expansion and advanced binder jetting systems indicates that manufacturers still see room for strategic investment in these routes. As more suppliers combine design validation, advanced powders, and repeatable sintering, the sintered steel market is expected to add applications previously out of reach for older process chains.

By Application: Gears and Transmission Lead Current Volume While Electrical and Magnetic Components Shape the Next Demand Wave

Gears and transmission components accounted for 29.84% of the sintered steel market in 2025, making them the largest application segment. Their position reflects the long-standing use of powder metal parts in automotive and industrial driveline systems that require repeatable strength, dimensional control, and scale efficiency. Bearings and bushings followed as another strong volume base because controlled porosity gives sintered parts self-lubricating behavior that many machined alternatives cannot match without additional systems. Engine, structural, and brake components remain important mid-tier applications because their program economics still favor near-net-shape PM within the right production ranges. Electrical and magnetic components are projected to post the fastest growth at a 7.21% CAGR through 2031, indicating where the sintered steel market is finding its next demand cycle.

That shift is already visible in commercial production. Sumitomo Electric began mass production of ultra-thin, insulation-coated, high-blocking-voltage magnetic cores in December 2024, confirming the transition from concept to scaled production in axial-flux motor applications. The application mix is also changing within the largest segment, as EV e-axle planet carriers and reduction gearboxes are replacing some legacy ICE transmission content. Sensors and precision components remain smaller in share but carry better pricing because automotive safety systems, medical diagnostics, and industrial automation require tight tolerances and consistent performance. A 2024 study in Metals found that sintered SMC stator cores in axial-flux motors can achieve efficiency levels comparable to those of thin non-oriented silicon steel laminations while enabling three-dimensional flux paths. That performance result strengthens the long-run position of the sintered steel market in motor designs where packaging and magnetic path flexibility matter.

By End-User Industry: Automotive Retains the Volume Base, While Electrical and Electronics Accelerates

Automotive accounted for 43.65% of end-user demand in 2025, making it the single largest vertical in the sintered steel market. The sector retains large installed design positions in ICE vehicles and is also adding new content in BEV e-axles, motor cores, and electric power steering systems. PM content averaged 14.8 kg per passenger vehicle in North America in 2024, reflecting the technology's continued integration into the vehicle bill of materials. Industrial end users form the next broad demand layer, as robotics, HVAC, agricultural machinery, power tools, and fluid control systems all use components that benefit from wear resistance and dimensional repeatability. Healthcare, aerospace, and defense remain smaller in volume but carry higher value because miniaturization, biocompatibility, and specialized performance standards support premium pricing. The automotive base, therefore, keeps the sintered steel market stable even as newer verticals grow faster.

The electrical and electronics end-user segment is projected to grow at a 7.43% CAGR, making it the fastest-growing outlet in the sintered steel market. Growth in this segment is tied to EV motor systems, miniaturized electromagnetic parts, and precision components used in compact electronic assemblies. Global EV sales growth in 2024 and the efficiency gains linked to soft magnetic composites both support this shift by increasing demand for magnetic parts that can be manufactured with repeatable geometry at scale.

Geography Analysis

Asia-Pacific held 48.32% of the sintered steel market share in 2025 and is projected to register the fastest regional CAGR of 6.78% through 2031. This position reflects the region's scale in vehicle assembly, growing EV supply chains, and manufacturing cost competitiveness. China remains the largest country-level demand center in the region due to its broad automotive and precision manufacturing base. India is an active policy-driven growth market, supported by the Ministry of Heavy Industries' allocation of INR 10,000 crore (USD 1.2 billion) under the Production Linked Incentive (PLI) scheme for auto components, which includes relevant powder metallurgy technologies. Japan holds an important technology role in high-precision Metal Injection Molding (MIM) and advanced sintered components through companies such as Sumitomo Electric Industries and Porite Corporation, while South Korea adds depth through its automotive and electronics manufacturing base. The Asia-Pacific sintered steel market combines present scale with future product diversification.

North America remained the second-largest regional market for sintered steel, supported by its automotive supply chain and an established powder metallurgy (PM) vendor base. More than 70% of regional iron powder shipments went to the automotive sector in 2024, confirming that regional demand closely follows vehicle production trends. New-vehicle sales of 15.9 million units in 2024 and hybrid sales growth of nearly 37% helped sustain near-term demand, even as OEMs balanced ICE, hybrid, and EV strategies. Europe ranked as the third-largest regional market, led by Germany and Sweden, where close ties between material suppliers and automotive OEMs support the co-development of newer PM specifications. European procurement is also being increasingly shaped by expectations for low-carbon inputs, and Höganäs reported a 55% reduction in Scope 1 and 2 emissions versus 2018 as it advanced its lower-carbon powder strategy.

South America remained a smaller but expanding part of the sintered steel market, with Brazil as the primary regional anchor due to its vehicle assembly base and industrial machinery demand. Argentina and neighboring countries contributed lower volumes and remained more dependent on imported components than on local PM production. The Middle East and Africa represented the smallest regional segment, with Saudi Arabia linked to downstream industrial demand and South Africa supported by established vehicle assembly activity. Growth potential exists in both areas, but the sintered steel market in these regions remains dependent on imports from Asia-Pacific and Europe, while domestic PM capacity remains limited.

Competitive Landscape

The sintered steel market is moderately consolidated, with producers such as GKN Powder Metallurgy (under Dauch Corporation), Höganäs AB, Miba AG, Sumitomo Electric Industries, PMG Holding, and AMES Group accounting for an estimated 40% to 48% of global PM component capacity. This structure creates a visible leadership tier, but leaves a large base of regional specialists, country-level suppliers, and niche MIM producers. Scale is an advantage because large players can distribute R&D, powder sourcing, tooling expertise, and customer qualification costs across a broader portfolio. Smaller firms, however, remain competitive where custom design, local OEM access, or highly specialized tolerances are more important than a global footprint. The result is a market where consolidation is meaningful, but not strong enough to eliminate regional competition.

The most notable strategic development in the recent period was Dauch Corporation's acquisition of Dowlais Group in February 2026, which brought GKN Powder Metallurgy's 27 manufacturing facilities across 9 countries into the group and created one of the largest powertrain and metal-forming platforms in the market. This deal is likely to drive portfolio reviews and supplier rationalization, as competitors now face a larger, integrated rival with global customer reach. Höganäs is pursuing a different strategy, focused on lower-carbon powder production; its biochar program aims to replace 20% of fossil coal in sponge iron production while reducing exposure to carbon and energy cost pressures. Indo-MIM's September 2025 filing for INR 1,000 crore (USD 113 million) for capacity expansion and advanced binder jetting systems demonstrates how specialist producers are building scale in higher-value precision routes rather than competing directly in every mass-volume PM segment. These developments indicate that the sintered steel market is being shaped by both consolidation at the top and selective specialization in faster-growing niches.

Competition is also shifting toward application readiness in EV motors, e-axle systems, medical parts, and electronics, rather than remaining focused solely on legacy engine programs. Sumitomo Electric's start of mass production for ultra-thin powder magnetic cores in December 2024 illustrates how product launches can secure a position in newer magnetic and electrification applications. Suppliers that can demonstrate repeatable quality in soft magnetic composites, corrosion-resistant miniaturized parts, and advanced surface finishes are likely to gain share in the next phase of the sintered steel market. Large integrated companies retain an advantage in raw material security and customer qualification, while niche firms can defend their position by offering faster development cycles or a tighter process focus. The competitive landscape therefore remains active, with room for both broad platform players and focused specialists within the sintered steel market.

Sintered Steel Industry Leaders

GKN Powder Metallurgy

Miba AG

Höganäs AB

Sumitomo Electric Industries, Ltd.

Schunk Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Dauch Corporation completed the acquisition of Dowlais Group plc, incorporating GKN Powder Metallurgy's 27 manufacturing facilities across 9 countries into its group structure.

- September 2025: Indo-MIM Limited filed its Draft Red Herring Prospectus with SEBI to raise INR 1,000 crore (USD 113 million), with proceeds earmarked for capacity expansion and binder jetting systems at its Bengaluru headquarters.

Global Sintered Steel Market Report Scope

Sintered steel is a material manufactured by compacting steel powder under extreme pressure and heating it to near-melting temperatures. This powder compaction process fuses the particles into a solid, precise component with controlled porosity and durability.

The sintered steel market is segmented by type, process, application, end-use industry, and geography. By type, the market is segmented into stainless steel, carbon steel, alloy steel, and tool steel. By process, the market is segmented into conventional powder metallurgy, metal injection molding (MIM), powder forging, and additive manufacturing. By application, the market is segmented into gears & transmission components, bearings & bushings, engine components, structural components, brake components, electrical & magnetic components, sensors & precision components, and other applications. By end-use industry, the market is segmented into automotive industry, industrial, electrical and electronics, healthcare, and aerospace and defense. The report also covers market size and forecasts for sintered steel across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Stainless Steel |

| Carbon Steel |

| Alloy Steel |

| Tool Steel |

| Conventional Powder Metallurgy |

| Metal Injection Molding (MIM) |

| Powder Forging |

| Additive Manufacturing |

| Gears & Transmission Components |

| Bearings & Bushings |

| Engine Components |

| Structural Components |

| Brake Components |

| Electrical & Magnetic Components |

| Sensors & Precision Components |

| Other Applications |

| Automotive Industry |

| Industrial |

| Electrical and Electronics |

| Healthcare |

| Aerospace and Defense |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Stainless Steel | |

| Carbon Steel | ||

| Alloy Steel | ||

| Tool Steel | ||

| By Process | Conventional Powder Metallurgy | |

| Metal Injection Molding (MIM) | ||

| Powder Forging | ||

| Additive Manufacturing | ||

| By Application | Gears & Transmission Components | |

| Bearings & Bushings | ||

| Engine Components | ||

| Structural Components | ||

| Brake Components | ||

| Electrical & Magnetic Components | ||

| Sensors & Precision Components | ||

| Other Applications | ||

| By End-User Industry | Automotive Industry | |

| Industrial | ||

| Electrical and Electronics | ||

| Healthcare | ||

| Aerospace and Defense | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Sintered Steel Market?

The Sintered Steel Market size is expected to increase from USD 29.11 billion in 2025 to USD 30.65 billion in 2026 and reach USD 40.89 billion by 2031, growing at a CAGR of 5.93% over 2026-2031.

Which region leads to global demand for sintered steel components?

Asia-Pacific led with a 48.32% share in 2025 and is also the fastest-growing region, with a projected 6.78% CAGR through 2031.

Why is the automotive industry still the largest market for sintered parts?

Automotive accounted for 43.65% of end-user demand in 2025 because vehicle programs still use high volumes of gears, bearings, structural parts, and newer EV-related components.

Which application area is growing the fastest in this space?

Electrical and magnetic components are projected to grow at 7.21% CAGR through 2031, supported by the rising use of soft magnetic composite motor cores and related EV components.

Page last updated on: