Singapore Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

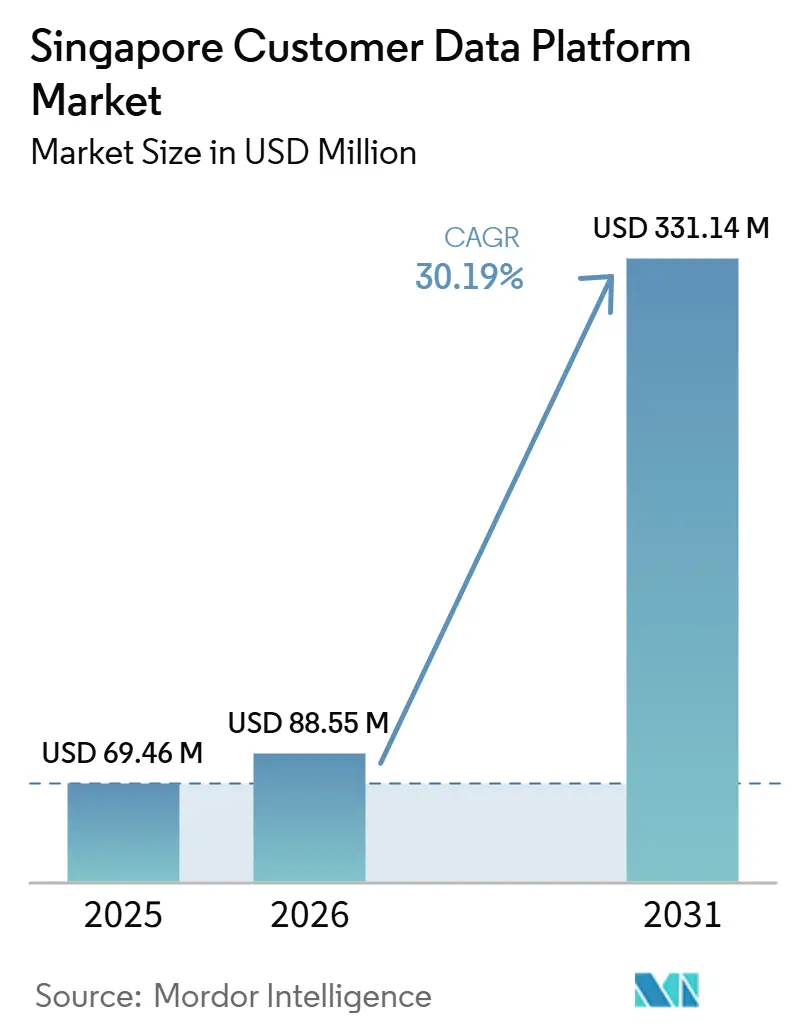

| Base Year Market Size (2025) | USD 69.46 Million |

| Market Size (2026) | USD 88.55 Million |

| Market Size (2031) | USD 331.14 Million |

| Growth Rate (2026 - 2031) | 30.19% CAGR |

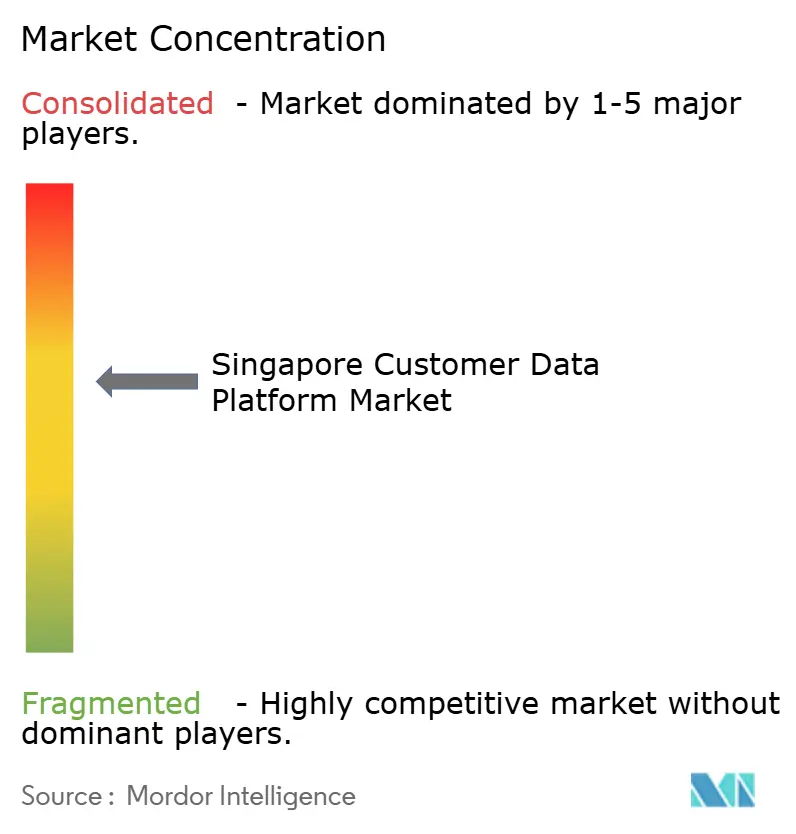

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Customer Data Platform Market Analysis by Mordor Intelligence

The Singapore customer data platform market size was valued at USD 69.46 million in 2025 and estimated to grow from USD 88.55 million in 2026 to reach USD 331.14 million by 2031, at a CAGR of 30.19% during the forecast period (2026-2031). The Singapore customer data platform market is expanding as enterprises move away from fragmented marketing and customer systems that no longer support unified engagement across channels. National support for AI adoption is also reinforcing demand, as firms need governed, centralized customer data before they can scale personalization, automation, and analytics. Singapore’s role as a regional headquarters base drives demand beyond local consumer activity, as many deployments support ASEAN-wide customer operations from a single hub. The Singapore customer data platform market is also shaped by a clear contrast between strong growth potential and operational friction, with privacy obligations, integration complexity, and talent shortages slowing implementation even as enterprise interest remains high. Competitive activity remains intense as global platform vendors, APAC-focused specialists, and warehouse-native architectures vie to define the preferred model for customer data management in Singapore.

Key Report Takeaways

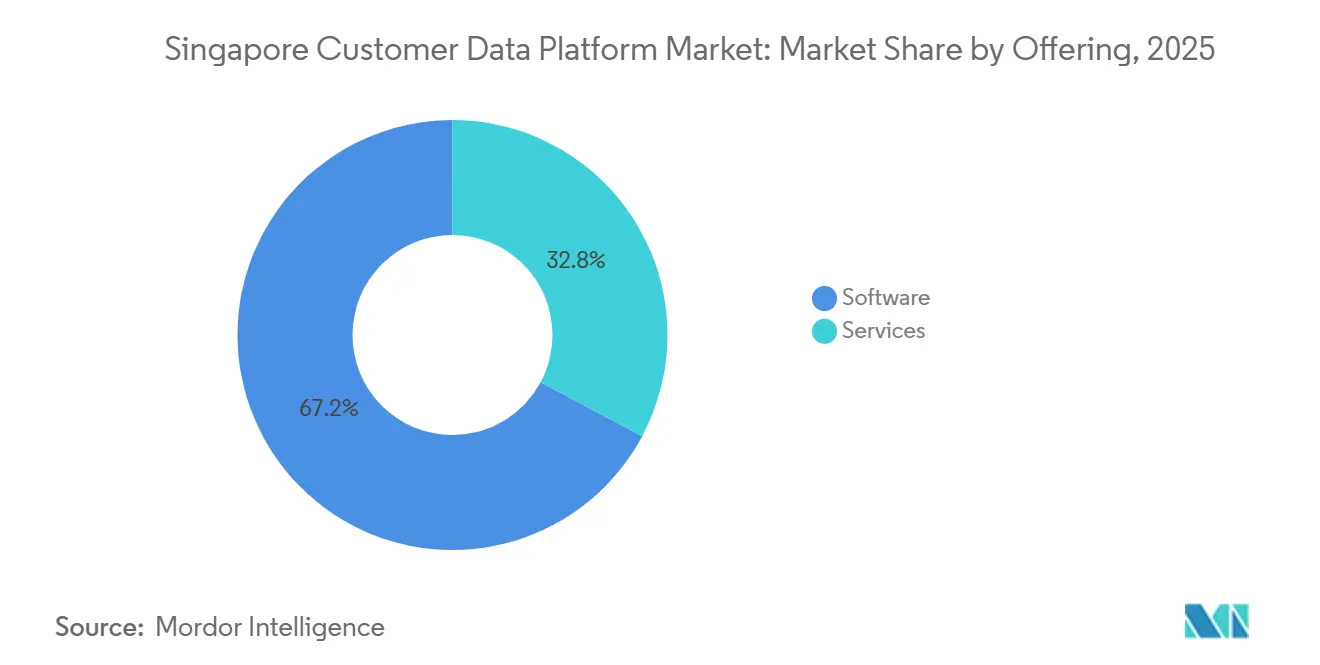

- By offering, software held 67.19% of the Singapore customer data platform market share in 2025, while services are projected to expand at a 32.91% CAGR through 2031.

- By deployment mode, cloud accounted for 65.23% of the Singapore customer data platform market in 2025 and is projected to record the highest CAGR of 32.12% through 2031.

- By organization size, large enterprises held 71.23% of the Singapore customer data platform market in 2025, while SMEs are projected to grow at a 32.56% CAGR through 2031.

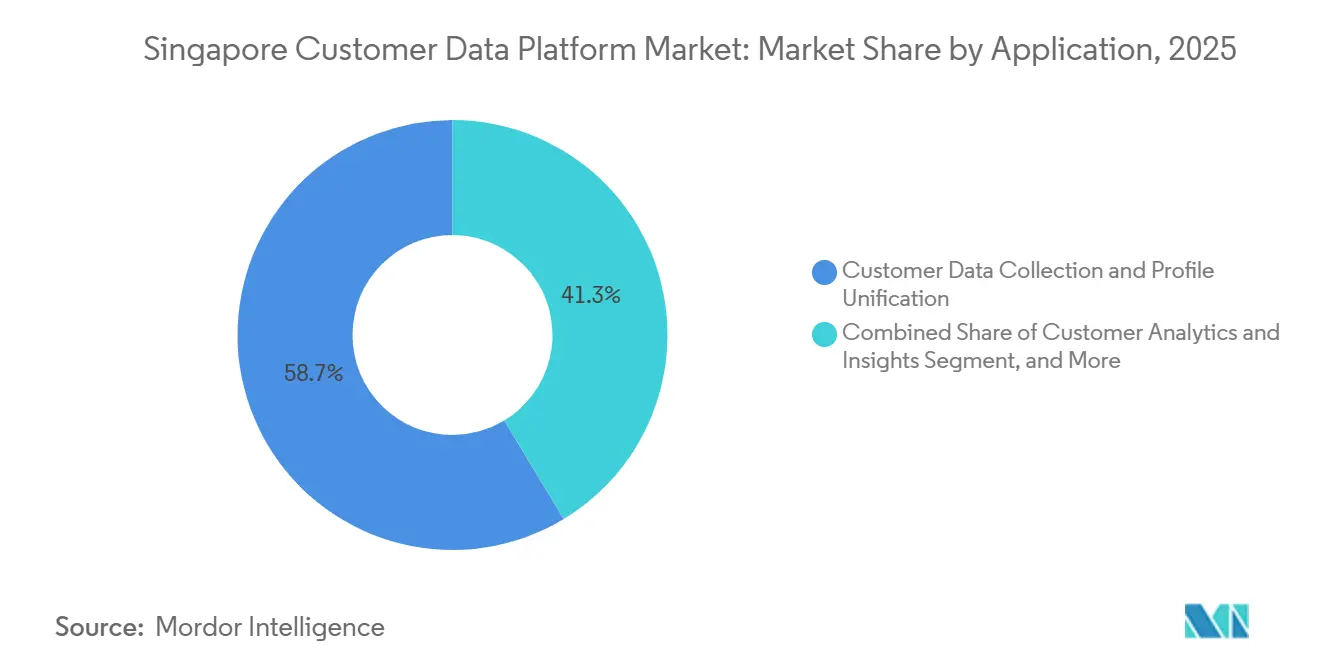

- By application, customer data collection and profile unification accounted for 58.66% of the Singapore customer data platform market in 2025, while audience segmentation and personalization are projected to grow at a 31.77% CAGR through 2031.

- By end-user industry, retail and e-commerce held 29.14% of the Singapore customer data platform market in 2025, while BFSI is projected to expand at a 31.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising First-Party Data Dependency after Cookie Deprecation | +6.2% | Global, with concentrated relevance in Singapore and ASEAN digital advertising ecosystems | Medium term (2-4 years) |

| AI-Driven Personalization Requiring Unified Customer Graphs | +5.8% | Global, intensive in Singapore, Japan, and Australia as digitally mature APAC markets | Medium term (2-4 years) |

| Real-Time Identity Resolution Needs across Fragmented Customer Journeys | +4.5% | APAC core, particularly acute in Singapore’s omnichannel retail and BFSI sectors | Short term (≤ 2 years) |

| Cloud-Native CDP Adoption to Reduce Integration Friction | +4.1% | Global, accelerated in Singapore through hyperscaler data center presence enabling PDPA-compliant residency | Short term (≤ 2 years) |

| Singapore as a Regional Hub for MarTech Consolidation | +2.9% | Singapore and Southeast Asia spillover markets | Medium term (2-4 years) |

| Data Activation Demands From Retail, BFSI, and Travel Brands | +2.4% | Singapore domestic and APAC regional hub operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Dependency after Cookie Deprecation

The Singapore customer data platform market is benefiting from a lasting shift toward first-party data ownership as brands lose confidence in third-party identifiers and campaign models built around them. Privacy changes across browsers, mobile ecosystems, and ad environments have made audience reach less predictable, pushing customer data collection and consent-based profiling closer to the center of digital strategy. In Singapore, this shift matters more because many brands operate across premium digital channels and regional customer programs that depend on stable identity and measurement. The result is a stronger demand for platforms that can connect website behavior, app activity, email response, transaction history, and loyalty participation into profiles that firms directly control. This has strengthened the role of the Singapore customer data platform market at the ingestion and identity layers, where enterprises are replacing older data-handling approaches with governed customer records built for activation and compliance.

AI-Driven Personalization Requiring Unified Customer Graphs

The Singapore customer data platform market is drawing direct support from AI-led personalization programs that cannot work well with fragmented customer data. Salesforce reported in June 2026 that 87% of Singapore marketers ran generic campaigns and 100% faced barriers to personalization due to siloed systems and poor data quality, even though AI was already widespread in their workflows. Adobe also found in 2025 that fragmented data remained the main obstacle to effective personalization across Asia, which aligns with the operational bottleneck seen in Singapore. This means AI budgets increasingly pull CDP spending along with them, because organizations need a unified customer graph before predictive models, recommendation engines, and real-time decision tools can perform as expected. The Singapore customer data platform market, therefore, benefits not only from demand for better marketing execution but also from the broader push to make enterprise AI spending more usable and accountable.

Real-Time Identity Resolution Needs Across Fragmented Customer Journeys

The Singapore customer data platform market is also being boosted by the need to consistently recognize customers across multiple active touchpoints. Retailers, banks, insurers, and service providers increasingly serve users through apps, websites, loyalty systems, service portals, and physical channels, and each interaction can create a separate identifier if records are not linked. This weakens analytics, suppresses relevant outreach, and makes real-time engagement less accurate because teams cannot see a single, reliable profile. PDPC guidance has also reinforced the need for organizations using personal data in automated decision systems to maintain strong accountability, data quality, and governance, which increases the value of systems that can coordinate identity and consent across processes.[1]Personal Data Protection Commission, “Advisory Guidelines on the Use of Personal Data in AI Recommendation and Decision Systems,” PDPC, pdpc.gov.sg In the Singapore customer data platform market, this creates a dual business case where identity resolution supports both commercial activation and defensible data handling across customer journeys.

Cloud-Native CDP Adoption to Reduce Integration Friction

The Singapore customer data platform market continues to favor cloud-native deployment because local hyperscaler infrastructure reduces residency and performance concerns that often delay customer data projects in other Southeast Asian countries. AWS, Microsoft Azure, and Google Cloud all maintain data center capacity in Singapore, making it easier for enterprises to keep customer records within a compliant local framework while still using modern activation tools. Tealium’s March 2026 launch in the AWS Singapore Region directly addressed this need and emphasized low-latency engagement, alongside support for Singapore's PDPA and broader ASEAN data protection requirements. This has strengthened demand for architectures that run on top of cloud warehouses rather than forcing full duplication across separate environments, thereby shortening implementation cycles and reducing friction for data teams. The Singapore customer data platform market is therefore seeing cloud deployment act as both a technology choice and a procurement accelerator, especially for organizations that already run core workloads in established cloud environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Data Governance Burden under Singapore PDPA and Cross-Border Rules | -3.4% | Singapore domestic, with cross-border implications for ASEAN-wide operations routed through Singapore | Long term (≥ 4 years) |

| Complex Integration with Legacy CRM, ERP, and Loyalty Stacks | -2.8% | Global, amplified in Singapore’s enterprise base with deep CRM and ERP incumbency | Medium term (2-4 years) |

| Talent Shortage in Identity Resolution, Reverse ETL, and MarTech Ops | -2.0% | Singapore domestic, compounded by regional talent competition | Medium term (2-4 years) |

| High Switching Costs for Enterprises Already Locked into Suites | -1.5% | Global, particularly relevant in Singapore’s enterprise segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Data Governance Burden under Singapore PDPA and Cross-Border Rules

The Singapore customer data platform market faces a real constraint due to the governance requirements for running centralized customer records in a tightly regulated environment. PDPC guidance places clear emphasis on accountability, explainability, data quality, and proper handling of personal information used in recommendation and decision systems, which increases the operational burden on firms that want to unify and activate customer data at scale. The burden increases further when Singapore-based operations manage customer records across ASEAN markets, as consent, storage, transfers, and usage must remain aligned across multiple regulatory settings. This slows deployment, raises compliance review requirements, and makes consent propagation a core technical feature rather than a secondary workflow. Even so, the same pressure is also pushing buyers toward better-governed platforms, which means the restraint slows execution speed more than it weakens long-term demand.

Complex Integration with Legacy CRM, ERP, and Loyalty Stacks

The Singapore customer data platform market also faces slower adoption because many enterprises already have deep, long-standing investments in CRM, ERP, service, loyalty, and analytics systems. These environments often contain partial customer records in different formats, making deduplication and activation difficult without careful mapping, reverse ETL, and ongoing schema management. The challenge is especially visible in large organizations where older systems still anchor daily workflows and cannot be replaced quickly. This is one reason services are growing faster than software in the Singapore customer data platform market, because deployment success depends heavily on integration design, identity logic, and operational tuning after the license is purchased. The effect is not a lack of interest, but a longer path to value, which is why buyers increasingly weigh implementation support and architectural flexibility as heavily as product features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Narrows the Gap with Software’s Market Lead

Software held a 67.19% share in 2025, which confirms that packaged platforms remained the main entry point into the Singapore customer data platform market. Early adoption favored software because enterprises first needed a formal system of record for customer data before they could improve orchestration, analytics, or consent management. That pattern still supports the larger installed base of software across enterprise buyers in retail, BFSI, telecom, and other data-heavy sectors. It also reflects the preference for established vendors that can bundle CDP functions into broader customer experience, service, and enterprise software suites.

Services are projected to grow at a 32.91% CAGR through 2031, indicating that value creation is shifting after the initial software purchase. As platform features become more similar, differentiation is moving toward implementation quality, identity resolution accuracy, audience logic, and post-deployment optimization in the Singapore customer data platform market. Twilio reported in 2025 that predictive trait usage among CDP users had surged, which supports the view that analytics tuning and activation support are becoming standard workstreams after implementation. This also fits the local talent gap in customer data operations, where many enterprises still need outside expertise to build and maintain useful workflows. The customer data platform industry in Singapore, therefore, remains software-led in revenue today, but service intensity is rising because outcomes now depend more on execution than on simple platform ownership.

By Deployment Mode: Cloud Extends its Lead Across Scale and Use Cases

Cloud accounted for 65.23% of the market in 2025, giving it the largest share of the Singapore customer data platform market by deployment model. That lead reflects a practical fit with local infrastructure because large cloud providers already support Singapore-based residency requirements and enterprise workloads. Buyers also favor cloud because it reduces hardware dependency, enables faster updates, supports easier integration, and enables more flexible activation across customer channels. This has made the cloud the default path for many organizations seeking faster rollouts without compromising access to advanced analytics and AI tooling.

Cloud is also projected to record the highest CAGR of 32.12% through 2031, which shows that leadership is strengthening rather than plateauing. Tealium’s move into the AWS Singapore Region in 2026 reflected how vendors are aligning product delivery with local data residency and low-latency performance needs. On-premises deployments remain relevant in more tightly controlled settings, especially where outsourcing and risk oversight remain sensitive. Hybrid models also remain useful for enterprises moving from older databases toward modern activation stacks without a full system replacement. In the Singapore customer data platform market, cloud is steadily gaining ground because it aligns with both compliance expectations and the operating models already used by major enterprises.

By Organization Size: SME Growth Quickens as Large Enterprise Adoption Matures

Large enterprises held 71.23% of the market in 2025, indicating that the Singapore customer data platform market was initially built around larger organizations with complex customer journeys and stronger budgets. These buyers were able to absorb early implementation costs and had enough data scale to justify a dedicated investment in unified customer infrastructure. They also had stronger reasons to centralize records because they often ran multiple business units, service functions, and digital channels simultaneously. This keeps large enterprises central to revenue generation even as growth begins to spread into smaller accounts.

SMEs are projected to grow at a 32.56% CAGR through 2031, indicating broader expansion of the Singapore customer data platform market beyond its original enterprise base. IMDA launched the National AI Impact Program in March 2026 to support 10,000 enterprises with structured AI adoption, thereby broadening the pathway for smaller firms to adopt customer data and marketing systems that were once out of reach.[2]Infocomm Media Development Authority, “National AI Impact Programme, Empowering Enterprises and Workers to Transform with AI,” IMDA, imda.gov.sg Budget 2026 also expanded support for qualifying AI expenditure through existing business support channels, which lowers adoption friction for smaller firms. SaaS delivery, usage-based pricing, and quicker setup have narrowed the operating gap between small firms and larger adopters. The customer data platform industry is therefore entering a more inclusive phase where enterprise dominance remains intact, but SME participation is becoming a more visible source of incremental growth.

By Application: Profile Unification Remains the Entry Point While Personalization Scales Faster

Customer data collection and profile unification held 58.66% of the market in 2025, making it the largest application in the Singapore customer data platform market. This confirms that most buyers still begin with the foundational task of creating a single usable customer record from multiple disconnected systems. Without that first step, downstream use cases such as activation, analytics, and journey design remain inconsistent because teams are working from incomplete or duplicate information. The application, therefore, continues to anchor buying decisions, especially among firms that are still early in their customer data modernization programs.

Audience segmentation and personalization are projected to grow at a 31.77% CAGR through 2031, indicating that buyers are moving toward higher-value activation once the data foundation is in place. Adobe announced the general availability of Real-Time CDP Collaboration in February 2025, which expanded privacy-conscious first-party audience creation and measurement for brands and publishers. PDPC guidance also underscores the importance of governing data use in recommendation and decision systems, which has led to greater interest in centralized consent and preference workflows. Campaign orchestration, analytics, and consent management remain closely linked layers that build on identity and profile quality rather than replacing them. In the Singapore customer data platform market, this means foundational unification still holds the largest share, while personalization is expanding faster as firms aim to turn cleaner data into measurable engagement results.

By End-User Industry: BFSI Gains Speed While Retail and E-Commerce Keep the Largest Base

Retail and e-commerce accounted for 29.14% of the market in 2025, giving the segment the largest share of the Singapore customer data platform market by end-user industry. The sector reached this position early because it manages broad customer interaction across stores, websites, apps, loyalty programs, and social commerce touchpoints. That operating model creates the kind of fragmented data environment that CDPs are designed to resolve. It also makes unified profiles valuable for promotion timing, retention activity, abandoned cart recovery, and channel coordination.

BFSI is projected to grow at a 31.48% CAGR through 2031, making it the fastest-growing vertical in the Singapore customer data platform market. MAS published its Safeguards for Agentic Finance at Runtime framework in 2026, and this sharpened attention on governance, authorization, and auditable data use in financial services. The result is that CDPs are increasingly viewed not only as marketing systems, but also as support infrastructure for governed AI and data handling in regulated institutions. Healthcare, telecom, media, manufacturing, and government remain relevant demand pools, but their adoption path is less mature and more selective. The Singapore customer data platform market, therefore, still relies on retail for scale today, while BFSI is growing faster because compliance and AI readiness are driving deeper customer data investment into financial institutions.

Geography Analysis

The Singapore customer data platform market position as a regional headquarters base makes that footprint more significant operationally than its domestic population alone would suggest. Many multinational firms run Southeast Asian customer data operations through Singapore, which increases platform demand beyond what local end-user volume alone would imply. This role is supported by strong digital infrastructure, with major hyperscalers maintaining local capacity that aligns with enterprise residency and latency requirements. IMDA’s 2025 digital economy reporting continued to place Singapore among the world’s most competitive digital environments, reinforcing why customer data deployments are often anchored there first. The Singapore customer data platform market also benefits from national AI policy support, because finance, healthcare, manufacturing, and connectivity have been prioritized in the refreshed national agenda.

Domestic demand is strongest where customer records are both numerous and heavily regulated. Retail and e-commerce continue to generate large volumes of cross-channel activity, while BFSI adds a stronger governance layer, turning customer data control into an operational requirement rather than a discretionary upgrade. MAS proposed amendments to its Technology Risk Management Notices in June 2026, which increased attention on asset control, monitoring, incident management, and related governance for technology environments used by financial institutions.[3]Monetary Authority of Singapore, “Consultation Paper on Proposed Amendments to Notices on Technology Risk Management,” MAS, mas.gov.sg At the same time, PDPC enforcement attention has made smaller firms more aware that customer data handling cannot remain loosely managed as their digital engagement grows. This supports the strong SME growth outlook already visible in the Singapore customer data platform market.

Singapore’s gateway role has a compounding effect because vendors that win local deals often use those deployments as templates for wider ASEAN expansion. Tealium’s March 2026 AWS Singapore launch explicitly linked local deployment to support for both Singapore PDPA and broader ASEAN data protection needs. That gives the Singapore customer data platform market a regional multiplier, where domestic adoption supports future product investment, stronger support ecosystems, and higher reference value across Southeast Asia. The result is a geography story in which Singapore is not only a national market but also a strategic operating base for broader customer data deployment in the region.

Competitive Landscape

The Singapore customer data platform market remains moderately concentrated in large enterprise accounts and more fragmented in mid-market demand. Adobe, Salesforce, Oracle, SAP, and Tealium continue to hold strong positions because they combine CDP functionality with broader software relationships already in place within large organizations. Those relationships matter because buyers often prefer one vendor that can connect customer data, service workflows, marketing execution, and analytics under a shared operating model. This gives established players an advantage in procurement, especially where switching costs and integration risk are already high. The Singapore customer data platform market, therefore, rewards scale, ecosystem depth, and trust as much as product capability.

Competition is also shifting because warehouse-native and composable approaches are challenging the older model of moving customer records into another managed platform. This model is gaining attention in Singapore because many enterprises already maintain mature cloud warehouse environments and want to activate data without duplication. SAP and Google Cloud expanded their partnership in April 2026 to support multi-agent AI and bidirectional zero-copy data access, reflecting this broader move toward a more composable data architecture. That change does not remove the incumbent's position, but it does pressure them to offer more flexible deployment and data access options. In the Singapore customer data platform market, architecture is becoming a more visible competitive variable alongside pricing, service support, and governance capability.

Recent strategic moves show how leading vendors are trying to strengthen their position before the market matures further. Salesforce announced a USD 1 billion investment in Singapore in March 2025 and expanded local data residency support for Data Cloud and Agentforce, reinforcing its long-term commitment to the country as its APAC base. Adobe expanded its partner ecosystem in April 2026 across AI platforms, technology providers, agencies, and integrators to support customer experience orchestration built on Adobe Real-Time CDP.[4]Adobe, “Adobe Expands Partner Ecosystem to Deliver Frictionless Workflows for Customer Experience Orchestration,” Adobe News, news.adobe.com Tealium strengthened its local operating case by launching in the AWS Singapore Region in March 2026, directly addressing compliance and low-latency engagement needs. These moves suggest that vendors are not competing only on features but also on local infrastructure, partner reach, deployment flexibility, and confidence in the governance of AI use. The Singapore customer data platform market still has room for specialists, but success is likely to depend on solving enterprise integration and usability problems better than the large suites do.

Singapore Customer Data Platform Industry Leaders

Adobe Inc.

SAP SE

Salesforce, Inc.

Oracle Corporation

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Salesforce launched its AI Innovation Hub in its Singapore office, enabling customers and partners to co-innovate, test, and deploy Agentforce solutions. Data and AI Centers of Excellence established with Accenture, PwC Singapore, and Huron will go live later in 2026, deepening the partner ecosystem needed to implement Data Cloud and CDP-driven customer engagement at scale in the region.

- April 2026: Treasure Data rebranded as Treasure AI and introduced Treasure AI Studio, a conversational AI workspace converging its intelligent CDP, AI agent foundry, and AI marketing cloud into a single agentic experience platform available across web, mobile, desktop, and command-line interfaces, directly embedding CDP activation into AI agent workflows.

- April 2026: SAP and Google Cloud expanded their partnership to deploy multi-agent AI, introducing SAP Business Data Cloud (BDC) Connect for Google and BigQuery, enabling bidirectional, zero-copy data access between the two platforms with enterprise-grade security and governance, advancing cross-platform CDP integration for joint enterprise customers.

- April 2026: Adobe expanded its partner ecosystem across more than 30 AI platforms, technology companies, agencies, and system integrators, including Amazon, Anthropic, Google, NVIDIA, Accenture, Deloitte Digital, EY, and PwC, to support agent-based workflows for customer experience orchestration built on Adobe Real-Time CDP.

Singapore Customer Data Platform Market Report Scope

The Singapore Customer Data Platform Market comprises software solutions and associated services that aggregate, unify, and activate customer data across multiple channels to enable data-driven marketing, personalization, customer analytics, and engagement strategies. These platforms help organizations create unified customer views, improve audience targeting, automate customer journeys, and comply with data privacy requirements. Singapore's highly developed digital economy, strong adoption of cloud technologies, and growing focus on customer experience transformation support the market. Customer data platforms enable businesses to leverage customer intelligence to improve marketing efficiency, strengthen customer retention, and drive business growth.

The Singapore Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 size of the Singapore customer data platform space?

The Singapore customer data platform market was estimated at USD 88.55 million in 2026 and is projected to reach USD 331.14 million by 2031 at a 30.19% CAGR.

What is driving adoption in Singapore?

The biggest forces are the shift toward first-party data, rising AI personalization needs, stronger demand for unified customer profiles, and continued investment in compliant cloud-based data infrastructure.

Which deployment model is leading in Singapore?

Cloud led with 65.23% share in 2025 and is also projected to record the fastest growth at a 32.12% CAGR through 2031.

Which buyer group is expanding the fastest?

SMEs are projected to grow at a 32.56% CAGR through 2031, supported by easier SaaS delivery and government-backed AI adoption pathways.

Which application area is still the largest?

Customer data collection and profile unification remained the largest application with 58.66% share in 2025 because most firms still begin with identity and data foundation work.

Which end-user segment is showing the strongest momentum?

Retail and e-commerce held the largest 2025 share at 29.14%, while BFSI is projected to grow the fastest at a 31.48% CAGR because governance and AI readiness are becoming more important in financial services.

Page last updated on: