Singapore Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

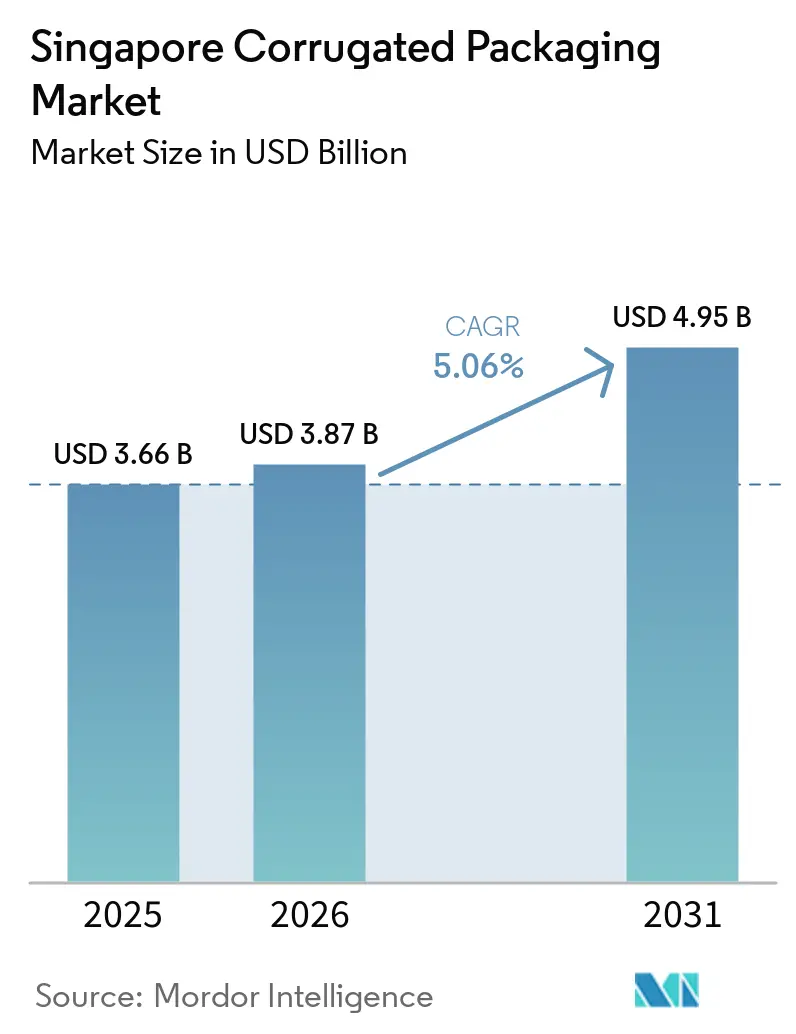

| Base Year Market Size (2025) | USD 3.66 Billion |

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 4.95 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Corrugated Packaging Market Analysis by Mordor Intelligence

The Singapore corrugated packaging market size was valued at USD 3.66 billion in 2025 and is expected to rise from USD 3.87 billion in 2026 to USD 4.95 billion by 2031, recording a 5.06% CAGR between 2026 and 2031. Expansion flows from Singapore’s role as a logistics and e-commerce gateway serving ASEAN, Middle Eastern, and Oceanic destinations that require automation-ready fiber formats. Rising parcel density, premium export positioning, and aggressive circular-economy rules combine to tilt procurement away from single-use plastics toward corrugated substrates that can be certified recyclable. Local converters therefore invest in solar power, digital printing, and robotics to offset the nation’s persistent real-estate and utility premiums while meeting demanding just-in-time cycles. Material innovation, such as lighter F flute and triple-wall structures, lets suppliers balance cost, performance, and sustainability without sacrificing the graphic quality global brands expect.

Key Report Takeaways

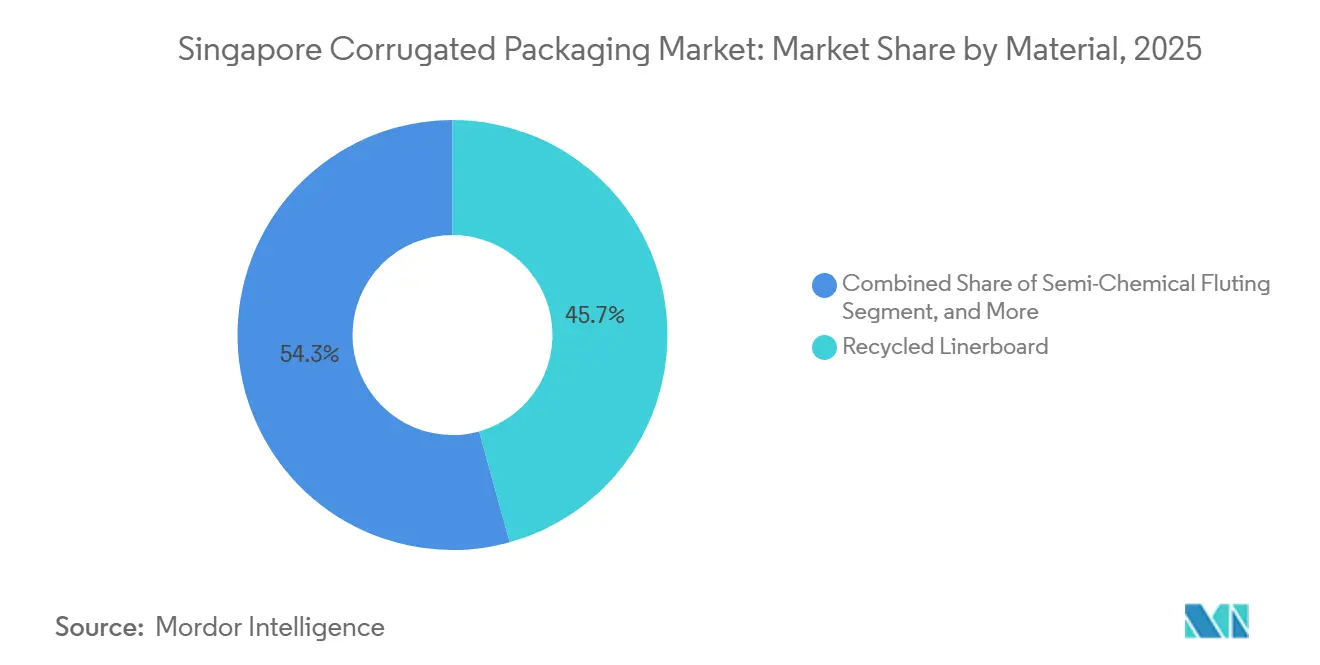

- By material, recycled linerboard captured 45.71% of the Singapore corrugated packaging market share in 2025.

- By flute type, the Singapore corrugated packaging market size for the F flute segment is forecast to advance at a 6.91% CAGR through 2031.

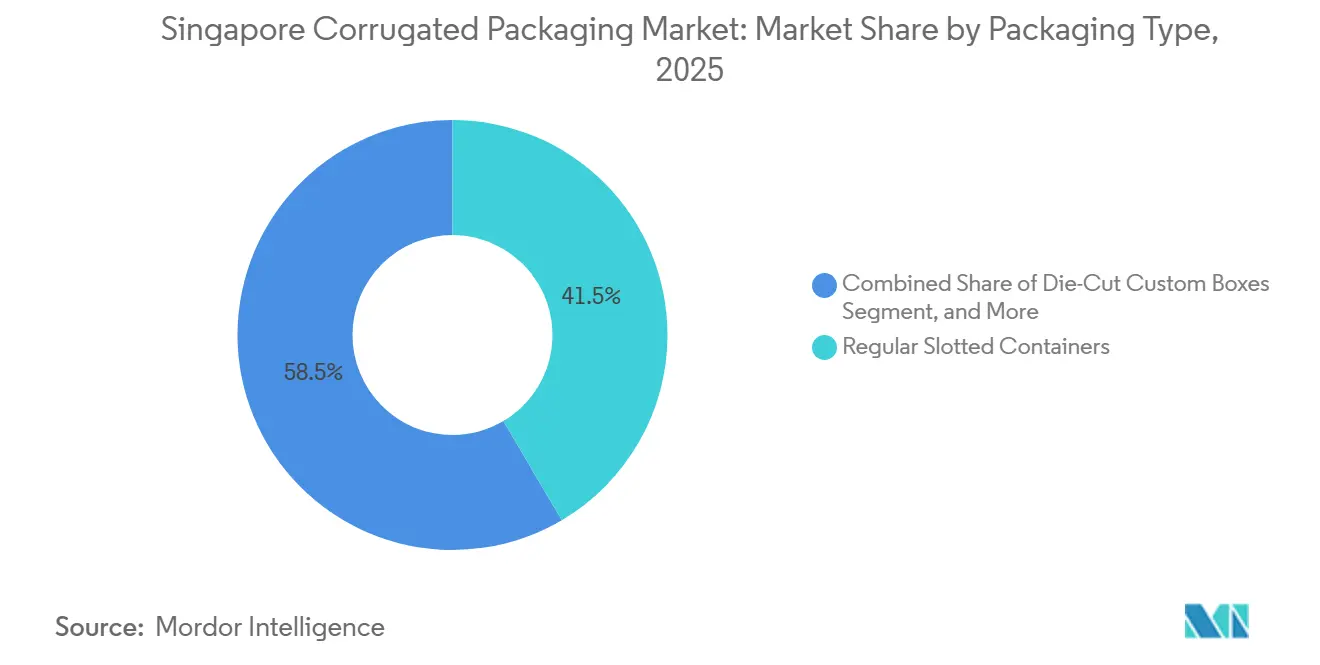

- By packaging type, regular slotted containers captured 41.51% of the Singapore corrugated packaging market share in 2025.

- By wall type, the Singapore corrugated packaging market size for the triple-wall segment is forecast to advance at a 6.81% CAGR through 2031.

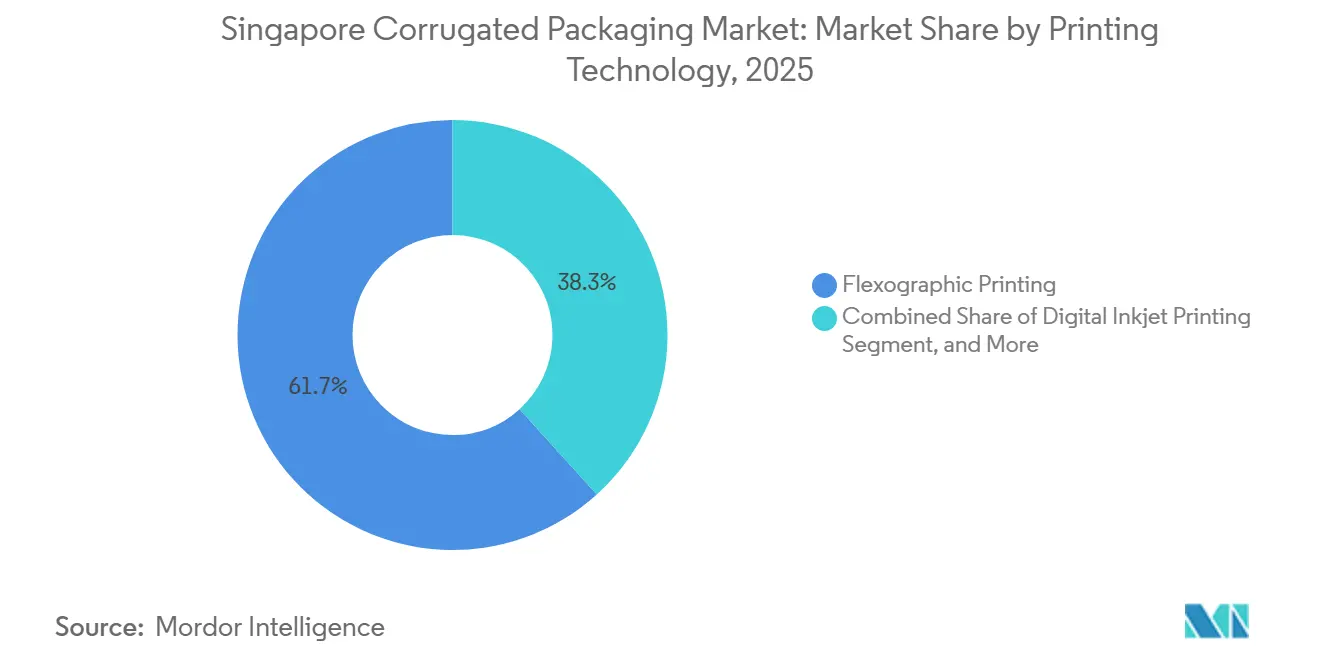

- By printing technology, flexography captured 61.71% of the Singapore corrugated packaging market share in 2025.

- By end-user industry, the Singapore corrugated packaging market size for the personal care and cosmetics segment is forecast to advance at a 7.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Boom Driving Corrugated Box Demand | +1.50% | National logistics hubs | Short term (≤ 2 years) |

| Government Push Toward a Circular Economy | +1.20% | National regulatory domain | Medium term (2-4 years) |

| Growth in Singapore’s Food Processing Exports | +0.90% | Outbound to ASEAN and MEA | Medium term (2-4 years) |

| Accelerating Adoption of Shelf-Ready Packaging by Retailers | +0.70% | Supermarket chains island-wide | Short term (≤ 2 years) |

| Automation Investments by Local Converters | +0.50% | Mid- to large-scale plants | Medium term (2-4 years) |

| Rising Demand for Sustainable Secondary Packaging | +0.40% | Multinational brand owners | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Driving Corrugated Box Demand

Daily parcel volumes now exceed prior decade highs, and leading marketplaces insist on fiber mailers that signal recyclability to urban consumers. New automated hubs, including SingPost’s SGD 182 million (USD 139 million) facility and Maersk’s 1.1 million ft² World Gateway II, each sort 100,000 parcels daily, entrenching demand for dimensionally stable cartons. Corrugated therefore becomes the default for high-speed conveyor systems that cannot risk film tears or dimensional variance. Converters capable of producing narrow flute boxes at tight tolerances win the largest e-commerce contracts. Robust order visibility lets them schedule multi-grade runs efficiently despite Singapore’s high energy tariffs.[1]National Environment Agency, “Alliance for Action on E-Commerce Packaging Guidelines,” nea.gov.sg

Government Push Toward a Circular Economy

Mandatory Packaging Reporting requires companies with a turnover above SGD 10 million (USD 7.65 million) to detail their material footprints, effectively penalizing excessive plastic use. The Beverage Container Return Scheme extends the payback logic, encouraging brands to adopt packaging that is easily recyclable. Technical Reference 109 provides common recyclability metrics, enabling procurement teams to benchmark suppliers on fiber content. Integrating such guidelines, converters secure price premiums for certified corrugated that earn downstream recycling credits. As regulators target a 20% cut in waste sent to landfill by 2026, demand shifts decisively toward paper-based formats that already enjoy strong collection rates.[2]Ministry of Sustainability and the Environment, “Singapore Green Plan 2030,” greenplan.gov.sg

Growth in Singapore’s Food Processing Exports

Processed-food exporters leverage Singapore’s free-trade network to move shelf-stable noodles, sauces, and snacks across ASEAN and the Middle East. Corrugated cases now double as shelf-ready displays, meeting retailer requests to slash labor by eliminating manual unpacking. The Singapore Food Agency’s hygiene codes impel converters to supply grease-resistant liners that meet direct-contact rules. Die-cutting innovations align lids, tear strips, and display windows without compromising compression strength. Consequently, customized cartons carve an outsized share of incremental tonnage moving through refrigerated and ambient supply chains.

Accelerating Adoption of Shelf-Ready Packaging by Retailers

Grocery operators battle chronic staffing shortages and focus on throughput per labor hour. Corrugated cases engineered with perforated fronts allow clerks to place entire units on shelves in seconds, trimming restocking time by nearly half. Digital inkjet printing adds campaign graphics without the cost of plates, making short-run promotions commercially viable. As brand managers test limited editions, converters pivot designs in days, satisfying both marketing teams and store managers. The virtuous cycle reinforces corrugated’s position as both a display medium and a shipping container.[3]HP Inc., “PageWide Technology for Corrugated Packaging,” hp.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Real-Estate and Utility Costs for Converters | -0.80% | Central and western estates | Short term (≤ 2 years) |

| Volatility in Recycled Fiber Import Regulations | -0.60% | Import-dependent operations | Medium term (2-4 years) |

| Competition From Flexible Plastic Formats in Fresh Produce | -0.30% | Wet markets and produce aisles | Short term (≤ 2 years) |

| Limited Domestic Wood Pulp Resources | -0.20% | Reliant on foreign pulp | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Real-Estate and Utility Costs for Converters

JTC lease renewals keep industrial rents elevated, compressing margins for mid-sized corrugators clustered around Tuas and Changi. SP Group’s 2.1% tariff increase in Q2 2026 further magnifies input costs, already elevated by Singapore’s reliance on imported natural gas. Larger players hedge with rooftop solar arrays and multiyear energy contracts, securing a structural cost advantage. Smaller plants that are unable to amortize automation costs struggle to compete on high-volume tenders. These pressures catalyze mergers, exemplified by Tat Seng’s recent USD 5.87 million acquisition of United Packaging Industries.[4]SP Group, “Electricity Tariff Revision for the Period 1 April-30 June 2026,” spgroup.com.sg

Volatility in Recycled Fiber Import Regulations

Basel Convention paperwork imposes four-day disposal receipt deadlines, delaying inbound wastepaper consignments whenever documentation lapses. Source-country export caps can suddenly divert shipments, forcing converters to buy pricier virgin fiber and tie up cash in safety stock. Tight vessel schedules at Singapore’s port leave little tolerance for clearance errors, amplifying inventory swings. Brands evaluating sustainability footprints may also penalize mills linked to contested waste flows, raising reputational risk. Together these factors undermine converters’ ability to lock in predictable margin spreads over containerboard input costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Dominates Yet Virgin Kraft Lifts Premium Applications

Recycled linerboard secured 45.71% of Singapore's corrugated packaging market share in 2025 because it aligns with strict circular‐economy goals and offers a clear unit-cost edge for mass-volume shippers. Virgin Kraft linerboard, however, is projected to grow at a 6.13% CAGR through 2031 as pharmaceutical, electronics, and luxury-food exporters demand superior burst strength and pristine print surfaces that elevate brand perception at the shelf. This surge in premium substrate adoption steadily enlarges the Singapore corrugated packaging market size within value-added grades, giving converters opportunities to command higher margins while meeting overseas regulatory requirements for food contact and medical traceability. Converters that can hot-swap between recovered and virgin fibers during the same production run, therefore capture mixed portfolios without increasing changeover downtime, reinforcing their appeal to multinational buyers.

Virgin Kraft uptake also dovetails with Singapore’s ambition to serve as a regional design lab for sustainable, high-performance packaging that still aligns with downstream deposit-return logistics. Mills serving the city-state have responded by introducing lightweight yet high-stiffness formulations that trim container weight by double-digit percentages, which subsequently reduces freight emissions on air and sea lanes. Enhanced surface smoothness supports high-definition inkjet graphics, allowing brand managers to shift decorative folding-carton programs onto corrugated without visual compromise. Ultimately, sustained virgin kraft gains lift revenue even when tonnage growth moderates, buffering converters against recycled-fiber cost volatility and underpinning long-term stability in the Singapore corrugated packaging market.

By Flute Type: B Flute Retains Reach While F Flute Captures Lightweight Momentum

B flute remained the workhorse with 37.74% share of Singapore corrugated packaging market shipments in 2025 because its 3-millimeter profile balances cushioning, stacking, and economics for fulfillment-center cartons. Retailers and parcel carriers, however, increasingly specify 0.8-millimeter F flute to lower dimensional-weight charges and to nest retail cases tightly on shelf, which accelerates its 6.91% CAGR outlook through 2031. As graphics expectations climb, F flute’s fine surface accepts single-pass inkjet printing without washboarding, enhancing shelf appeal for personal-care and consumer-electronics packages. Converters investing in servo-controlled corrugators can now switch flute profiles in under ten minutes, preserving machine utilization while satisfying diverse customer specifications.

Rising F flute penetration simultaneously expands the Singapore corrugated packaging market size for digital printing inks and inspection systems that guarantee color consistency across SKU variants. Brands gain agility to test seasonal artwork or influencer co-branding because small production lots avoid plate-making costs inherent to flexography. Meanwhile, B flute maintains dominance in food and beverage logistics where pallet stability outweighs shelf aesthetics, preserving volume critical mass for linerboard suppliers. The coexistence of both flute styles lets converters segment price architecture, charging premiums for high-graphic micro flute runs while protecting scale on commodity boxes destined for regional re-export.

By Packaging Type: Custom Die-Cut Solutions Outpace Commodity Containers

Regular slotted containers commanded 41.51% share of the Singapore corrugated packaging market size in 2025 because they remain indispensable for standardized distribution and warehouse automation. Nevertheless, die-cut custom boxes are projected to record a 6.45% CAGR as e-commerce brands differentiate through memorable unboxing experiences that cultivate social-media buzz and repeat purchases. These tailor-made formats incorporate tear-away lids, internal dividers, and printed thank-you notes, all executed economically via digital presses that eliminate tooling delays. As Singapore positions itself as an Asia-Pacific fulfillment hub, quick-turn die-cut capability becomes a competitive necessity rather than a design luxury.

Personal-care founders and electronics start-ups headquartered in the city routinely request pilot runs as small as 500 pieces, which traditional flexographic setups cannot supply profitably. Digital workflows therefore unlock incremental revenue and reinforce converter relevance among venture-backed companies scaling product lines rapidly. Meanwhile, grocers adopting shelf-ready cases that convert from shipper to display unit in one motion reinforce demand for precision die-cutting across fast-moving consumer goods. Together these trends lift average selling prices, sustaining topline expansion even as raw board costs fluctuate, and deepen customer reliance on local converters proficient in rapid artwork iteration.

By Wall Type: Triple-Wall Broadens Beyond Industrial Niches

Single-wall cartons still accounted for 53.85% of Singapore corrugated packaging market shipments in 2025 because they satisfy the protective needs of most parcel networks at the lowest material weight. Triple-wall, however, is projected to grow 6.81% annually to 2031 as semiconductor equipment, precision machinery, and photovoltaic modules demand extra crush resistance across multiple transshipment points. Enhanced rigidity mitigates vibration damage during airfreight legs and temperature cycling in unconditioned containers, protecting cargoes worth millions of dollars.

Automation upgrades inside regional converter plants shorten setup times, making lower-volume triple-wall production economically viable and thereby extending its reach from niche to mainstream high-value exports. Retail automation facilities also prefer triple-wall pallets that resist deflection under robotic arm loads, minimizing downtime caused by collapsed skids. Consequently, premium wall configurations expand their contribution to the Singapore corrugated packaging market size, lifting material revenue even as board grammage per box stabilizes through lightweighting initiatives in single-wall formats.

By Printing Technology: Digital Inkjet Builds Strategic Edge Over Flexography

Flexographic presses maintained 61.71% share in 2025 because long-run commodity cartons still dominate outbound volume, benefiting from proven plate durability and high feet-per-minute speeds. Digital inkjet presses, however, will grow at a 7.18% CAGR as converters chase short-run profitability, variable data compliance, and serialized QR-code programs needed for cross-border traceability. Removing plates slashes lead time from weeks to days, enabling marketing teams to pivot graphics in near real time when campaign analytics signal content fatigue.

Inkjet’s water-based chemistries also support food-contact safety credentials and align with Singapore’s TR109:2023 sustainability metrics, further encouraging brand adoption. Press manufacturers have doubled resolution while raising running widths beyond 1.6 meters, allowing large-format display wraps previously confined to litho-lamination to migrate into one-pass digital workflows. Combined, these improvements raise price realization and diversify revenue streams, preserving converter margins even under rising labor and electricity costs that pressure legacy flexographic economics.

By End-User Industry: Personal Care Surges While Processed Foods Supply Scale

Processed foods retained 31.17% of Singapore corrugated packaging market share in 2025, anchored by regional noodle, condiment, and snack players that export to Middle Eastern and ASEAN supermarkets. Stringent hygiene and shelf-ready display demands keep volume steady, ensuring baseline mill offtake for recycled linerboard. Personal-care and cosmetics shipments, however, are forecast to expand 7.17% annually because premium brands exploit Singapore’s logistics efficiencies to launch Asia-wide SKUs featuring luxurious unboxing rituals. Virgin kraft linerboard paired with micro flute substrates provides tactile quality commensurate with retail price points, lifting value per ton sold.

Pharmaceutical exporters further reinforce high-specification demand by ordering temperature-stable triple-wall cartons that satisfy Good Distribution Practice audits into tropical destinations. E-commerce fulfillment centers add another growth layer by driving single-unit shipments that multiply box counts relative to bulk retail replenishment, thereby enlarging the Singapore corrugated packaging market size without proportional increases in board grammage. Each end-user vertical therefore contributes distinct performance parameters, collectively stimulating continued innovation and equipment investment across the converter landscape.

Geography Analysis

Corrugated production clusters within JTC estates at Tampines, Tuas, and Changi, where direct highway and port links condense transit time to airport cargo zones and container terminals. Co-location with third-party logistics hubs lets converters deliver fresh boards within tight fulfillment windows, a critical advantage for flash-sale e-commerce events that spike order volumes overnight. Close physical proximity also minimizes backhaul inefficiencies, lowering carbon footprints and strengthening compliance with deposit-return and recycling mandates that dominate local sustainability discourse.

Regional fiber supply networks materially affect domestic input prices because Singapore itself lacks natural wood resources. Malaysian and Indonesian mills ship containerboard by short sea, providing recycled linerboard at competitive landed costs, while premium virgin kraft still arrives from Scandinavia and North America. Smurfit Westrock’s shuttering of high-cost EMEA capacity and its bid to lift APAC EBITDA margins signal constrained regional supply, which in turn incentivizes Singapore converters to adopt yield-boosting corrugator control systems that trim waste without sacrificing throughput.

Singapore’s regulatory environment, led by the National Environment Agency and the Ministry of Sustainability and the Environment, sets higher circular-economy benchmarks than many ASEAN neighbors, making the city a showcase for pilot programs. Mandatory Packaging Reporting compliance software developed for domestic operations often becomes the template for rollouts across Thailand, Vietnam, and Indonesia, reinforcing Singapore’s role as a regional knowledge exporter. Foreign brands therefore use local market launches to fine-tune recyclable designs under strict auditing, further entrenching the influence of Singapore corrugated packaging market practices on wider Southeast Asian supply chains.

Competitive Landscape

The market exhibits moderate consolidation because multinational containerboard groups, regional integrated players, and nimble local converters each hold material footholds. Global suppliers such as Smurfit Westrock and Mondi leverage regional kraftliner mills to lock contractual tonnage with leading Singapore converters, ensuring preferential feedstock during seasonal demand spikes. ASEAN champions like SCG Packaging and Oji Holdings integrate mill output with downstream box plants, capturing synergies across logistics, procurement, and sustainability reporting, and passing part of those savings to pan-regional brand accounts.

Local specialists, including Tat Seng Packaging and Greatprint, differentiate via rapid structural design services, 24-hour artwork turnarounds, and door-to-door delivery commitments that align with Singapore’s time-starved retail ecosystem. Their smaller plant footprints enable fast changeovers, letting them chase high-mix personal-care, electronics, and gifting orders that larger plants may overlook due to scheduling complexity. However, persistent rent hikes and electricity tariffs push independents toward mergers or strategic alliances, as evidenced by Tat Seng’s March 2026 acquisition of United Packaging Industries, which lifted scale and bargaining leverage with containerboard suppliers.

Technology spend now separates winners from laggards because brand owners require QR-code serialization, carbon-footprint reporting, and color-managed graphics on even mid-volume programs. Early adopters of single-pass inkjet and autonomous material-handling robots report double-digit labor savings and error-rate reductions, improving bid competitiveness under fixed-price contracts. Converters lagging in digitization face shrinking order books as e-commerce fulfillment centers codify packaging-line compatibility criteria that legacy facilities cannot meet. Consequently, the competitive narrative is shifting from raw tonnage capacity toward data throughput and sustainability traceability, a trend likely to intensify over the forecast horizon.

Singapore Corrugated Packaging Industry Leaders

Smurfit Westrock plc

Mondi Plc

Oji Holdings Corporation

SCG Packaging Public Company Limited

Rengo Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Tat Seng Packaging completed the business transfer of United Packaging Industries for SGD 7.93 million (USD 5.87 million).

- March 2026: Maersk opened World Gateway II, a fully automated 1.1 million square-foot distribution center in Singapore.

- March 2026: SingPost inaugurated a SGD 182 million (USD 135 million) regional e-commerce logistics hub at Tampines Logistics Park.

- February 2026: Smurfit Westrock reported FY 2025 results and set a USD 7 billion EBITDA ambition for 2030.

Singapore Corrugated Packaging Market Report Scope

The Singapore Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Singapore Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-Commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-Commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected 2026 value of Singapore's corrugated packaging market?

The market is expected to reach USD 3.87 billion in 2026.

Why are die-cut custom boxes gaining popularity among Singapore brands?

They enhance unboxing experiences, enable shelf-ready displays, and are economical through digital printing workflows.

How is Singapore's circular-economy policy influencing material choices?

Mandatory reporting and deposit schemes raise plastic costs, steering procurement toward certified recyclable corrugated cartons.

Which printing technology is growing fastest in local corrugating plants?

Digital inkjet is advancing at a 7.18% CAGR due to plate-free setup and variable data capabilities.

What challenges do converters face with recycled fiber imports?

Basel Convention paperwork and export-country caps create lead-time uncertainty, sometimes forcing substitution with pricier virgin pulp.

Which end-use segment offers the highest growth potential through 2031?

Personal-care and cosmetics shipments show the fastest 7.17% CAGR, driven by premium branding and e-commerce expansion.

Page last updated on: