Singapore Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

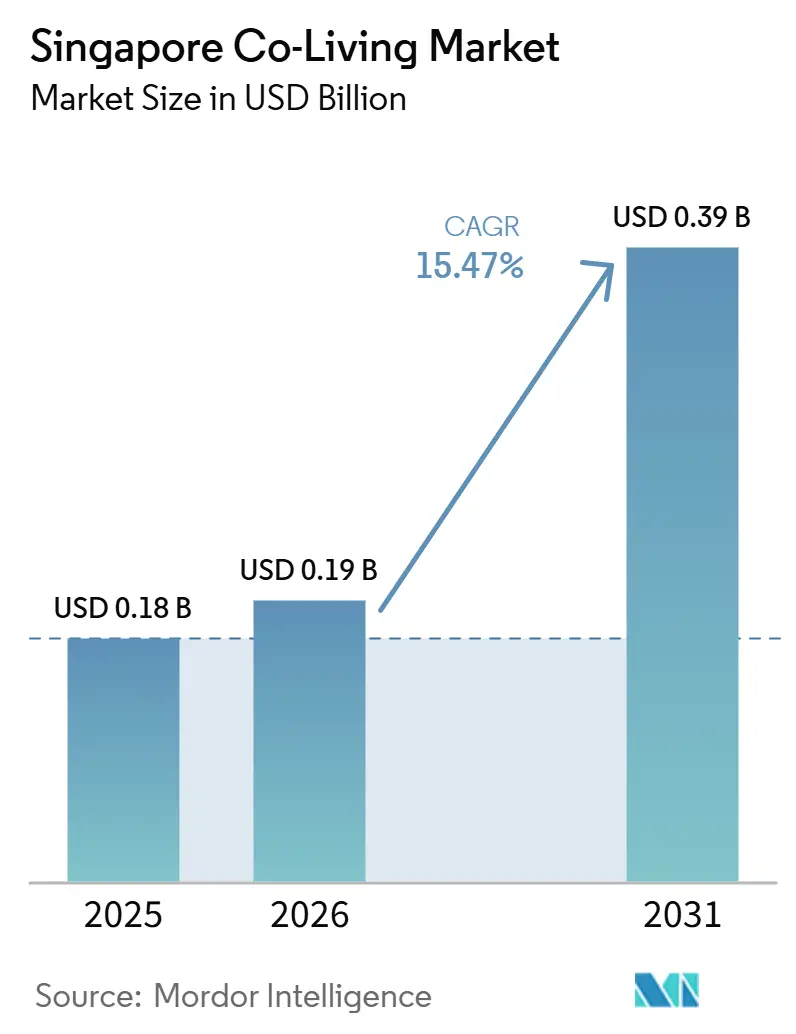

| Base Year Market Size (2025) | USD 0.18 Billion |

| Market Size (2026) | USD 0.19 Billion |

| Market Size (2031) | USD 0.39 Billion |

| Growth Rate (2026 - 2031) | 15.47% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Co-Living Market Analysis by Mordor Intelligence

The Singapore Co-Living Market size is projected to be USD 0.18 billion in 2025, USD 0.19 billion in 2026, and reach USD 0.39 billion by 2031, growing at a CAGR of 15.47% from 2026 to 2031.

The Singapore co-living market has moved beyond its earlier role as a short-term housing option. It now attracts larger pools of capital, with more than SGD 1.4 billion (USD 1.05 billion) committed between 2022 and 2025. Singapore’s limited land area of 734 square kilometers and total population of 6.11 million, including 1.91 million non-residents as of June 2025, continue to create housing demand that standard rental stock does not absorb well for students and mobile professionals. In 2026, private residential supply is up 33% year on year, which has eased headline rent pressure but has not removed the affordability gap that keeps the Singapore co-living market relevant for mid-term occupants. Market-wide occupancy remained 85% to 95% through 2025, above the 70% to 75% breakeven range, while room inventory expanded 17% between 2023 and 2025 without weakening occupancy, suggesting real unmet demand in the Singapore co-living market rather than a temporary demand spike. Competition is active, the top 5 operators controlled 65.3% of room inventory in Q2 2025, and recent listings by Coliwoo and The Assembly Place have widened the funding gap between scaled operators and smaller players, even as staffing, utility, and acquisition costs place more pressure on margins.

Key Report Takeaways

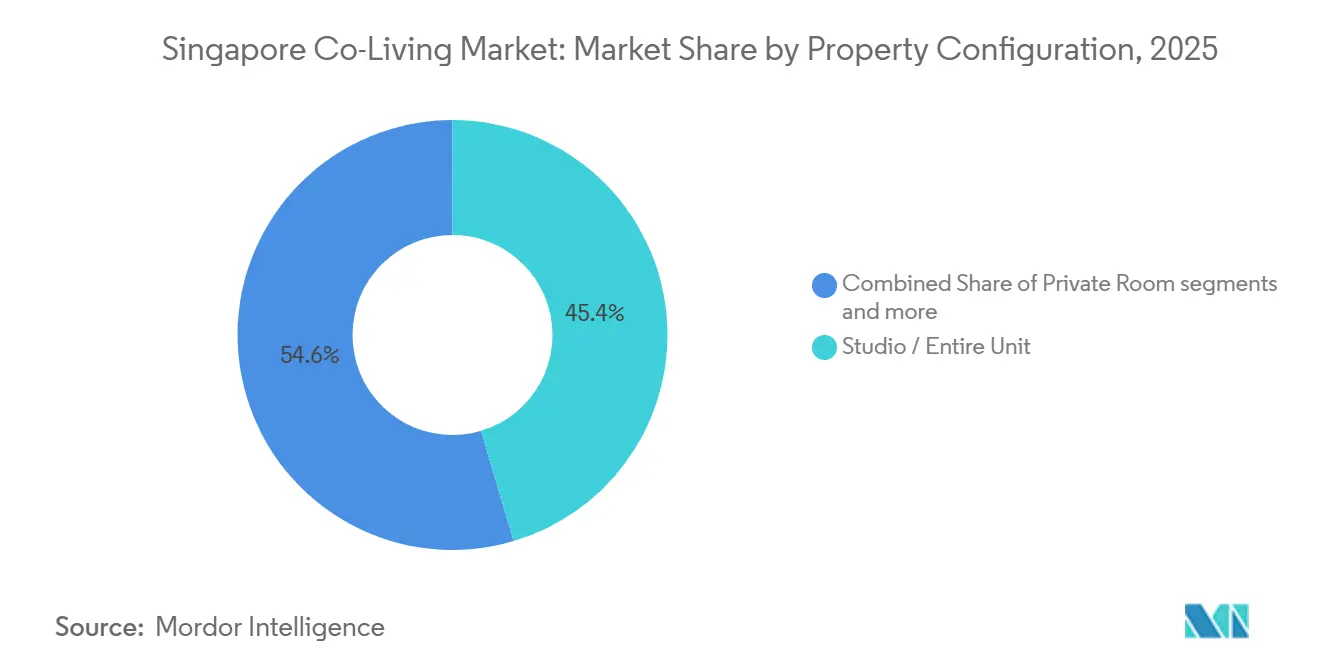

- By property configuration, studio / entire-unit formats held 45.4% of the Singapore co-living market share in 2025 and also recorded the fastest projected CAGR of 16.90% through 2031.

- By business model, asset-light master-lease and lease-arbitrage structures accounted for 42% of revenue in 2025, while asset-light management agreements posted the highest projected CAGR at 16.5% through 2031.

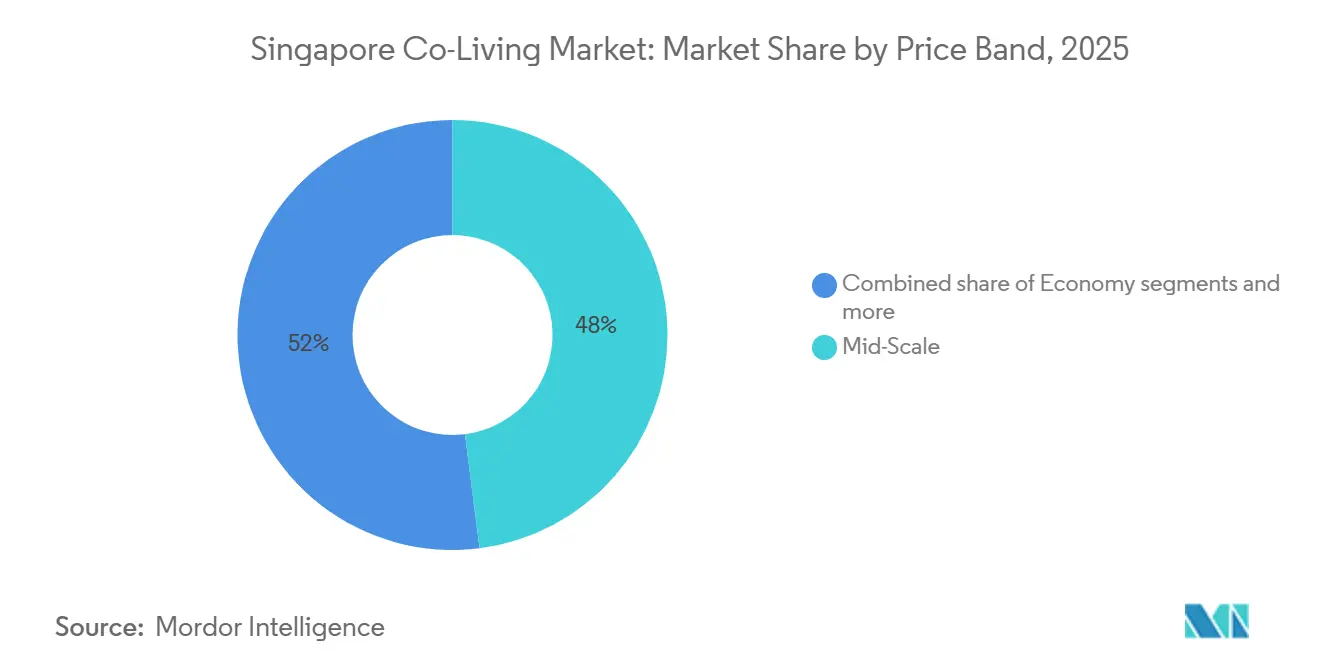

- By price band, mid-scale properties accounted for 48% share of the Singapore co-living market size in 2025 and are forecast to expand at 17.20% CAGR through 2031.

- By end user, students held 54.7% of the Singapore co-living market size in 2025, while working professionals are forecast to grow at 17.00% CAGR through 2031.

- By geography, the Central Area held 34% share of the Singapore co-living market size in 2025 and is also expected to record the fastest CAGR at 17.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Expatriate and Foreign Professional Population Drives Co-Living Demand | +3.8% | Global, with concentration in Central Area and East Region of Singapore | Long term (≥ 4 years) |

| Growing Young Professional and International Student Population Expands Occupancy | +3.1% | National, with concentration near NUS and NTU corridors and the Central Area | Long term (≥ 4 years) |

| Preference for Flexible Lease Terms Boosts Co-Living Adoption | +2.6% | National, with early gains in Central Area, Novena, and Queenstown | Medium term (2-4 years) |

| Rising Institutional Investment Supports Co-Living Market Growth | +2.4% | Central Area, River Valley, Balestier, and city-fringe precincts | Medium term (2-4 years) |

| Urbanization and Limited Land Availability Increases Shared Housing Demand | +1.8% | National | Long term (≥ 4 years) |

| High Residential Rental Costs Encourage Co-Living Adoption | +1.8% | National, particularly Central and city-fringe regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Expatriate and Foreign Professional Population Drives Co-Living Demand

Singapore’s non-resident population rose 2.7% to 1.91 million in June 2025, and this group remains one of the clearest demand pools for the Singapore co-living market[1]National Population and Talent Division, “Population in Brief 2025,” Singapore Government, channelnewsasia.com . Skilled foreign professionals under the Employment Pass and S Pass schemes represent a high-value tenant segment, supporting premium occupancy and stable rental income for operators. As Singapore continues to strengthen its position as a regional financial, technology, and business hub, incoming professionals on project-based and multi-year assignments increasingly prefer fully furnished accommodation with flexible lease terms over conventional long-term rentals. This structural shift toward greater workforce mobility continues to strengthen demand for professionally managed co-living properties.

Growing Young Professional and International Student Population Expands Occupancy

The Singapore co-living market also benefits from rising demand among young professionals and international students seeking flexible, well-connected accommodation near universities and employment hubs. Industry data indicates that Singapore's skilled foreign workforce has grown by 13% since 2018, while the international student population has increased by 47% over the same period, outpacing the expansion of co-living supply. Students accounted for 54.7% of end-user revenue in 2025. Supported by this dual demand base, co-living occupancy remained between 85% and 95% throughout 2025, demonstrating sustained absorption despite continued additions to room supply.

Preference for Flexible Lease Terms Boosts Co-Living Adoption

Traditional residential leases in Singapore usually run for 12 to 24 months, which does not suit many project-based workers, relocating staff, or students. Operators in the Singapore co-living market have leveraged that gap by offering 3- to 6-month leases with furnishings and utilities included, reducing moving friction and upfront setup costs. A 2025 investor survey found that 77% of investors preferred 3-year to 5-year holding periods for co-living assets, supporting the case for a product built around medium-term stays rather than nightly or annual occupancy cycles. The model is especially well aligned with Chinese international students, because academic calendars create strong seasonal housing needs that do not fit well with full-year leases. Corporate relocation policies have also begun to support co-living allowances for international hires, narrowing the divide between serviced apartments and co-living in the Singapore co-living market.

Rising Institutional Investment Supports Co-Living Market Growth

Institutional investors increasingly view the Singapore co-living market as a more defensive allocation within the living sector rather than a niche growth bet. A 2025 investor survey showed that 65% of investors were targeting internal rates of return below 15%, up from 27% in 2023, suggesting lower return thresholds and a more mainstream risk view. One common route has been buying hotels, offices, or hostels for conversion, such as CapitaLand Ascott Trust’s January 2024 purchase of the former Hotel G Singapore for SGD 240 million (USD 180 million), which it reopened as lyf Bugis in August 2024. Warburg Pincus deepened its position in Weave Living in 2024 and later co-invested with BlackRock in a Singapore joint venture valued at SGD 188 million (USD 141 million), demonstrating how larger capital pools are now moving into this format. Singapore is one of the major Asia-Pacific living markets where co-living serves as the primary institutional entry route, so competition for eligible conversion assets in the Singapore co-living market is likely to remain strong.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Property Acquisition and Development Costs Constrain New Supply | -1.8% | National, most acute in Central Area and city-fringe precincts | Long term (≥ 4 years) |

| Limited Availability of Suitable Properties Restricts Market Expansion | -1.2% | National, particularly Central Area, Novena, and Orchard | Medium term (2-4 years) |

| Stringent Regulatory Framework Increases Compliance Burden | -1.1% | National, with regulatory influence from URA zoning and HDB occupancy rules | Short term (≤ 2 years), Medium term (2-4 years) |

| Limited Land Availability Constrains Large-Scale Co-Living Developments | -0.9% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Property Acquisition and Development Costs Constrain New Supply

Acquisition and development costs remain among the clearest constraints on new supply in the Singapore co-living market. Government Land Sale sites with a residential component recorded average land rate growth of nearly 13% in 2025, and land values in the central region reached SGD 1,820 (USD 1,365) per square foot per plot ratio in recent tenders. Those higher entry costs weaken conversion economics because operators need assets priced below condominium benchmarks to preserve acceptable yields. Suitable conversion properties remain limited, even as acquisition costs rise, making expansion more challenging for both existing platforms and new entrants. The response from larger operators has shifted toward capital recycling, and Coliwoo’s March 2026 sale process for 7 freehold assets at SGD 218.5 million (USD 163.9 million) showed that growth can depend as much on asset rotation as on simple portfolio expansion.

Stringent Regulatory Framework Increases Compliance Burden

The regulatory framework in the Singapore co-living market is clear, but it raises compliance costs and limits operating flexibility. The Urban Redevelopment Authority (URA) rules require a minimum stay of 90 days for residential-zoned properties and cap occupancy at 6 unrelated persons per private residential unit, which narrows the range of operating models that can work at scale. The SA2 long-stay serviced apartment pilot, introduced in November 2023, requires a 3-month minimum stay in approved buildings but adds another approval layer that smaller operators may find harder to manage. Operators that breach occupancy or minimum-stay rules face fines of up to SGD 200,000 (USD 150,000), and repeated violations can lead to prosecution, so compliance failure carries real financial risk. As a result, the Singapore co-living market offers less product freedom and lower revenue per unit than some less-regulated regional markets, even though demand remains healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Studio / Entire Units Lead as Privacy Preference Reshapes Product Mix

Studio / entire-unit configurations held 45.4% of Singapore co-living market share in 2025, and they are projected to grow at 16.90% CAGR through 2031. That lead reflects a clear shift in preference toward layouts that offer privacy, self-contained living, and a stronger sense of home than shared-room formats. The format also fits the dominant 3-month to 12-month stay pattern, because tenants on temporary work or study cycles often want a private base without committing to a full apartment lease. In the Singapore co-living market, this makes studios attractive to both operators and tenants, as they can command higher pricing while still below the cost of many conventional rentals.

The student mix has helped reinforce this pattern, especially as Chinese international students have become a stronger source of demand and often value personal study space over larger shared living areas. Private rooms still matter as an entry product for newly arrived professionals who want to learn the rental market before stepping up to a larger commitment. Shared rooms remain relevant for price-sensitive users, but their role is narrowing as operators convert some of that stock into private-room layouts in response to a higher willingness to pay. Studio formats also expand the potential demand pool because a single unit can serve an individual tenant or a couple on assignment, improving the use of available inventory without changing the basic footprint.

By Business Model: Asset-Light: Master Lease / Lease Arbitrage Models Scale While Asset-Light Management Agreement Gain Traction

Asset-light master-lease / lease-arbitrage structures accounted for 42% of segment revenue in 2025, making them the largest operating model in the Singapore co-living market. This model has gained scale because it lets operators expand room count without tying up large amounts of capital in asset ownership. The approach is practical in a market where acquisition costs are high and operators still need sufficient flexibility to add supply quickly in strong-demand pockets. It also suits owners who want steady lease income without building their own operating platform.

Asset-light management agreements are the fastest-growing model, with forecast growth of 16.50% through 2031, as property owners increasingly open to hiring specialist operators while retaining ownership and asset upside. This structure transfers much of the day-to-day operating responsibility to the co-living brand and lowers balance sheet risk for the operator. Own-develop-operate models remain more selective because they require a large upfront investment, but they still appeal to groups that want long-term asset value and future monetization options. Industry Association’s 2025 survey finding that 77% of investors favored 3-year to 5-year holding periods suggests that owned assets will stay strategically important even if asset-light structures continue to dominate new scaling activity.

By Price Band: Mid-Scale Segment Commands Majority as Value Positioning Matures

Mid-scale properties accounted for 48% of segment revenue in 2025 and are forecast to record the fastest CAGR of 17.20% through 2031. This position shows that the Singapore co-living market is centered on value rather than on the cheapest or most premium offer. Mid-scale formats appeal to salaried foreign professionals and self-funded international students who want quality, location, and service but still need cost control. They also sit in the broadest demand band, which supports occupancy stability across different tenant groups.

That balance helps the segment during uncertain business conditions, because employees who might once have been placed in serviced apartments can move into well-managed mid-scale stock without giving up location or convenience. Economy properties still draw budget-sensitive students and entry-level workers, but that tenant base responds more quickly when the wider rental market softens. Premium and luxury co-living cater to a smaller pool of senior expatriates and high-income users. While they can achieve higher margins per unit, growth is naturally capped by a narrower addressable base. Operators across tiers are using tenant-matching tools and smart-building systems to maintain service standards without matching cost growth one-for-one. This trend is becoming increasingly important as the Singapore co-living market matures.

By End User: Student Demand Anchors Occupancy While Professionals Lift Growth Depth

Students accounted for 54.7% of end-user revenue in 2025, which makes them the largest demand base in the Singapore co-living market. Singapore’s role as an education hub continues to support that position, and the draw of leading universities such as NUS and NTU keeps a regular flow of international students entering the city each year. Co-living is well aligned with academic calendars, because students often need medium-term housing with utilities, furnishings, and internet already in place. Operators have adjusted product designs accordingly, with study-friendly layouts, faster connectivity, and community formats that suit peer living.

A shortage of campus housing at major institutions has also put pressure on the private rental market, which sustains student occupancy and revenue. International students provide this segment with a dependable demand tailwind even as broader economic conditions fluctuate. Working professionals are projected to expand at a 17.0% CAGR through 2031, indicating that professional demand is deepening even as students remain the core revenue anchor. A newer layer within the Singapore co-living market is the rise of specialist subgroups, such as foreign healthcare workers, for whom operators have started tailoring offerings to institutional demand and supporting the reuse of state properties.

Geography Analysis

The Central Area accounted for 34% of Singapore's co-living market share in 2025 and is forecast to expand at a 17.45% CAGR through 2031, keeping it the clear center of demand and supply in this market. The area works for both Central Business District (CBD)-based professionals and students because it combines office access, campus reach, and strong public transport connectivity. New stock has largely come from reused shophouses and former hospitality assets rather than new construction, allowing operators to add rooms without bearing the full cost of new residential development. The SA2 long-stay serviced apartment pilot has helped support that reuse path by providing an approved route for longer-stay formats in selected buildings. The planned redevelopment of the 5.7-hectare Phoenix Park site into a 700-unit co-living community also shows that larger projects are starting to enter the pipeline where the right asset and planning conditions exist.

The East Region remains a smaller part of the Singapore co-living market, but it has become more distinct, serving a different tenant profile than the central core. Its appeal comes from the overlap between Changi Business Park employment, airport-linked mobility, and the lifestyle value of the East Coast corridor. That has encouraged operators to test different product formats, including corporate-oriented long stays and more leisure-led offers for longer-duration tenants. The overlap with healthcare demand around Novena adds another layer of support, especially for mobile professionals who need furnished housing outside the CBD.

The West, North-East, and North regions together still represent a smaller revenue base, yet each one is gaining relevance as Singapore pushes activity into newer employment nodes. One-North in the West draws life sciences, media, and technology workers whose housing choices are often shaped by travel time rather than central prestige. The North-East gains from the Digital District at Punggol, where a co-living hospitality project is being developed to meet future technology-related demand in that corridor. The North remains at an earlier stage of co-living development because it has a lower concentration of international workers today. Even so, growth in Woodlands Regional Center could gradually widen the tenant base there over the 2026 to 2031 period if commercial activity deepens as planned[2] Urban Redevelopment Authority and Housing Development Board, “Draft Master Plan 2025 Housing Demand and Supply,” Government of Singapore, channelnewsasia.com.

Competitive Landscape

The Singapore co-living market is concentrated, with Coliwoo, Cove, lyf by Ascott, Hmlet, and The Assembly Place controlling 65.3% of total room supply as of Q2 2025. The leading operators benefit from stronger capital access, broader property sourcing, and more advanced operating platforms, enabling them to scale faster than smaller competitors. The listings of Coliwoo in November 2025 and The Assembly Place in January 2026 further strengthened the competitive position of larger operators by providing more transparent access to capital for portfolio expansion, fit-outs, and asset acquisitions. While boutique and specialist operators continue to serve niche tenant segments, the market is increasingly influenced by a relatively small group of established platforms.

Leading companies are strengthening their market positions through asset-light expansion and portfolio optimization. Management agreements and master leases have become preferred growth models because they enable faster room additions with lower capital intensity. At the same time, Coliwoo's March 2026 sale process for seven freehold assets valued at SGD 218.5 million (USD 163.9 million) demonstrated how established operators are recycling capital to fund future expansion. Cove's acquisition of Casa Mia Coliving in November 2025 added nearly 500 furnished rooms in prime central locations and increased annualized rental income to more than USD 50 million[3]Cove, “Cove Acquires Casa Mia Coliving, Strengthening Its Leadership in APAC Flexible-Stay,” Cove, blog.cove.sg.

Market concentration has continued to increase through strategic acquisitions and institutional investment. Mitsubishi Estate's acquisition of Habyt's operations brought 829 units in Singapore and 232 units in Hong Kong under the relaunched Hmlet brand, creating a combined portfolio of 2,915 units across Singapore, Hong Kong, and Japan. Larger operators are also investing in digital leasing, tenant matching, and facility management to improve operating efficiency and resident experience. Although niche opportunities remain for specialist providers serving healthcare workers, higher-income single professionals, and other mobile tenant groups, the Singapore co-living market is expected to remain concentrated, with the leading platforms continuing to strengthen their competitive positions through scale, capital access, and operational capabilities.

Singapore Co-Living Industry Leaders

Coliwoo

The Assembly Place

Cove

Habyt

lyf by The Ascott

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The Assembly Place and TS Home established TSTAPPRH Private Limited (39% TAP equity), a joint venture to convert the 5.7-hectare Phoenix Park heritage site on Tanglin Road into a 700-unit co-living community with health, sports, and dining facilities, the largest single-site co-living project in Singapore. The project deepens The Assembly Place's light-asset co-investment strategy and diversifies its portfolio into landmark mixed-use formats.

- April 2026: FL Japan Holdings, a subsidiary of Mitsubishi Estate, acquired Habyt Pte. Ltd., which owns 829 units in Singapore and 232 in Hong Kong. The acquisition reunified the platform under the revived Hmlet brand, with co-founder Yoan Kamalski returning as Chief Executive Officer (CEO). The combined group's total managed units reached 2,915 across Singapore, Hong Kong, and Japan.

- March 2026: Coliwoo launched a portfolio sale of seven freehold living-sector assets in River Valley, Balestier, and Rangoon Road, with a combined guide price of approximately USD 168.9 million. The sale signals a capital-recycling strategy to redeploy proceeds into pipeline acquisitions in higher-growth locations.

- March 2026: Coliwoo completed the acquisition of 2 Changi Business Park Avenue 1, the former Park Avenue Changi Hotel, for approximately USD 78.1 million, targeting 368 operational rooms by Q1 FY2027 following asset enhancement works.

Singapore Co-Living Market Report Scope

The Singapore Co-Living Market Report is Segmented by Property Configuration (Studio / Entire Unit, Private Room, and Shared Room), Business Model (Asset-Light Master Lease / Lease Arbitrage and More), Price Band (Economy, Mid-Scale, and Premium / Luxury), End User (Students, and Working Professionals), and Region (Central Area, East Region, West Region, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement |

| Asset-Heavy Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium/Luxury |

| Students |

| Working Professionals |

| Central Area |

| East Region |

| West Region |

| North-East Region |

| North Region |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement | |

| Asset-Heavy Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium/Luxury | |

| By End User | Students |

| Working Professionals | |

| By Region | Central Area |

| East Region | |

| West Region | |

| North-East Region | |

| North Region |

Key Questions Answered in the Report

What is the current size of Singapore co-living in 2026?

The Singapore co-living market stands at USD 0.19 billion in 2026 and is projected to reach USD 0.39 billion by 2031 at a 15.47% CAGR.

Which tenant group contributes the most revenue in Singapore?

Students are the largest end-user group, accounting for 54.7% of revenue in 2025, supported by strong international student inflows and limited campus housing.

Why is the Central Area the strongest location for operators?

The Central Area held 34% of 2025 revenue and is forecast to grow at 17.5% CAGR because it combines CBD access, campus proximity, and strong public transport links.

Which property format performs best in Singapore?

Studio and entire-unit configurations lead with 45.4% share in 2025 and are also the fastest-growing format at 16.9% CAGR through 2031.

Page last updated on: