Silica Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

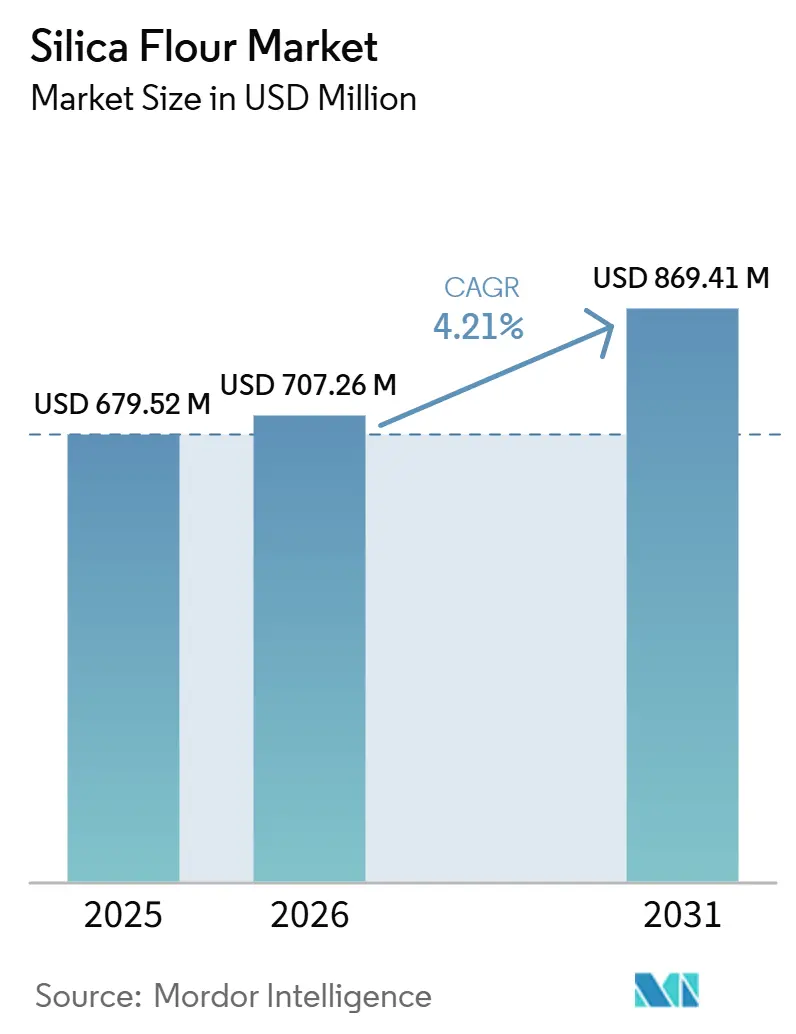

| Market Size (2026) | USD 707.26 Million |

| Market Size (2031) | USD 869.41 Million |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silica Flour Market Analysis by Mordor Intelligence

The Silica Flour Market size is projected to expand from USD 679.52 million in 2025 and USD 707.26 million in 2026 to USD 869.41 million by 2031, and is expected to register a CAGR of 4.21% between 2026 and 2031. The silica flour market is shifting toward tighter quality specifications, particularly in applications that require narrower particle size distributions and lower iron oxide content. This is increasing contract values even when volume growth remains moderate. The shift is creating a clear gap between specialty grades and commodity material, which explains why pricing has remained more stable in differentiated product lines than in standard industrial grades. The market also faces a two-speed supply dynamic, as premium-grade material faces tighter availability while upstream infrastructure linked to industrial sand continues to deal with oversupply pressure in more commoditized channels. Competitive behavior in the market reflects this divide, with producers focusing on pricing pass-through, product upgrading, and selective capacity discipline, while private capital and strategic buyers continue to treat silica assets as durable industrial platforms. The market faces downside risk from any slowdown in Chinese glass and ceramics output and from disruption in high-purity quartz supply chains, both of which can affect availability, lead times, and pricing across premium applications.

Key Report Takeaways

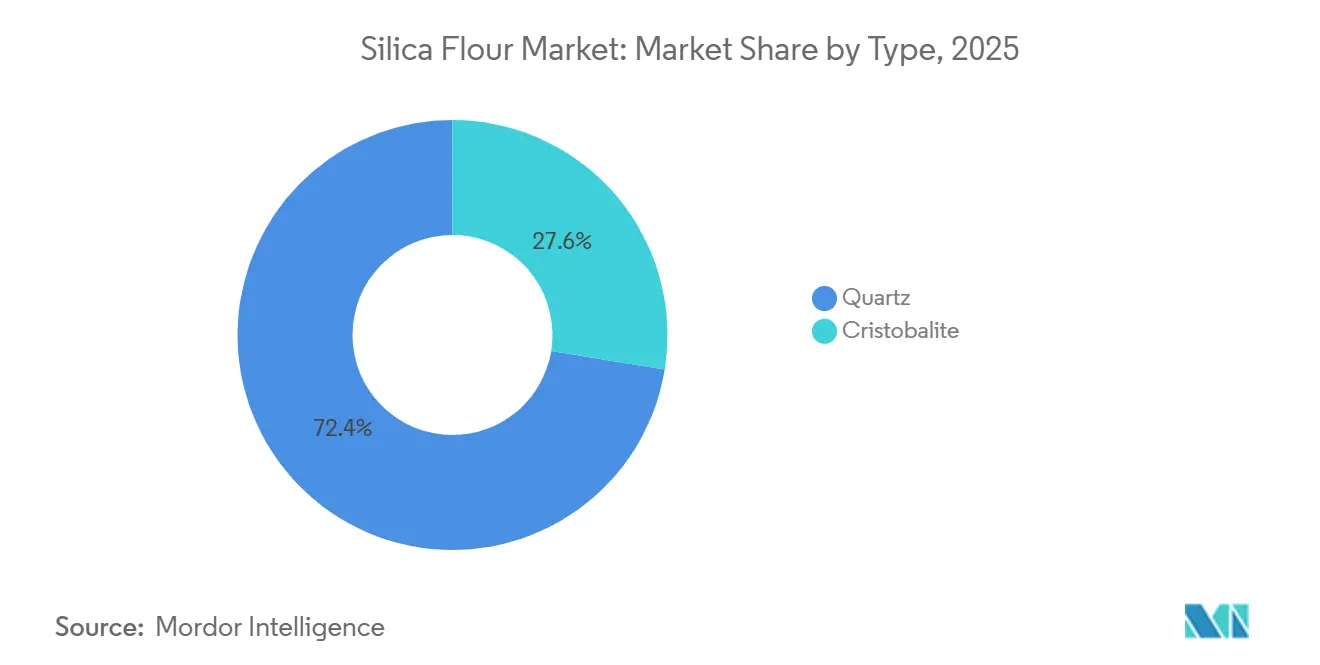

- By type, quartz held 72.44% of revenue in 2025, while cristobalite is projected to record the fastest CAGR of 5.18% through 2031.

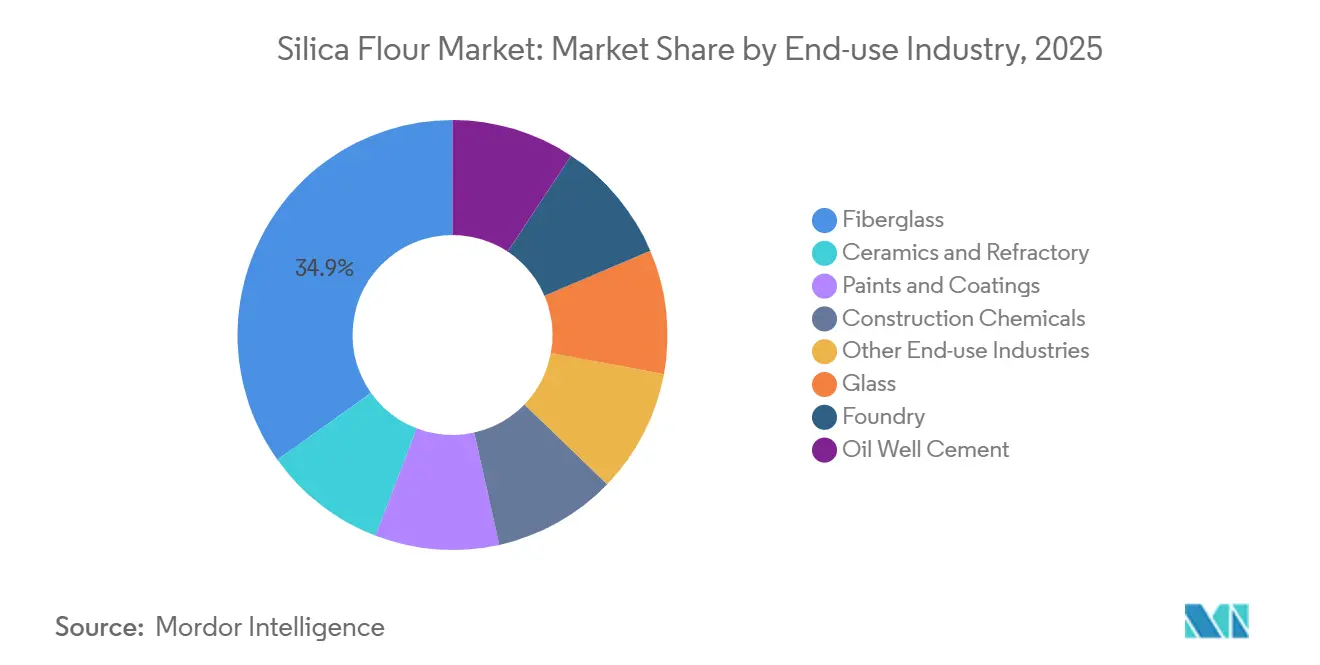

- By end-use industry, fiberglass accounted for 34.86% of revenue in 2025, while construction chemicals are forecast to expand at a 5.34% CAGR through 2031.

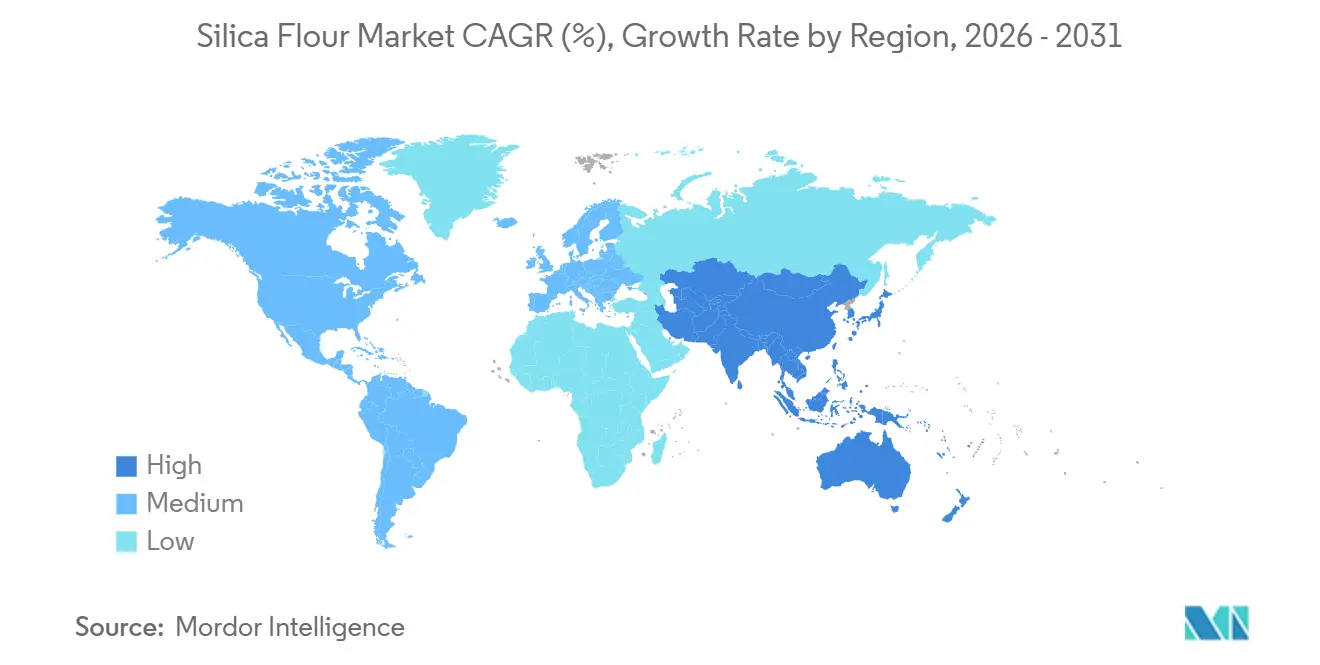

- By geography, Asia-Pacific held 45.27% of revenue in 2025 and is also projected to record the highest CAGR of 6.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silica Flour Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand from the Glass Industry | +0.9% | Global, concentrated in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Expansion of Foundry Applications | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growth in Fiberglass Production | +1.1% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Increasing Demand for Oil Well Cement | +0.8% | North America, the Middle East, and South America | Medium term (2-4 years) |

| Expansion of Ceramics and Refractories | +0.7% | Asia-Pacific, Europe, the Middle East, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from the Glass Industry

Glass is one of the key demand drivers for the silica flour market, spanning flat glass, container glass, specialty glass, and solar photovoltaic glass. Buyers are requesting tighter particle-size control and lower iron content to support higher-performance glass products. This is particularly relevant in solar-related applications, where quality thresholds and qualification standards are more stringent. As a result, the silica flour market is growing in volume and shifting toward higher-purity product lines with stronger pricing. Producers that can upgrade through acid leaching and fine classification are positioned to secure longer contracts and more stable returns. Producers without that capability remain more closely tied to cyclical glass demand and face greater price pressure in standard grades.

Growth in Fiberglass Production

Fiberglass production is driving demand for silica flour across insulation, composites, and wind energy manufacturing. Fiberglass customers place a high value on consistency, cleanliness, and controlled particle distribution. Longer wind turbine blades and more demanding composite applications are increasing the need for qualified silica inputs that perform reliably during resin wet-out and downstream processing. This requirement narrows the pool of approved suppliers and supports a price premium for consistent material. The silica flour market is therefore gaining from fiberglass through both tonnage demand and a stricter supplier selection process. This makes fiberglass a stabilizing factor for the silica flour market when commodity-driven applications weaken.

Expansion of Foundry Applications

Foundry demand supports the silica flour market through molding, binding, refractory use, and precision casting applications. Demand is tied to industrial production trends, particularly in automotive, aerospace, and machinery manufacturing, where casting quality and dimensional accuracy are important. Lightweight casting programs are also increasing demand for finer material, as surface finish and defect control are more critical in advanced parts. Higher-grade flour can improve consistency in specialty foundry processes. Ceramics and refractories also move in parallel with foundry activity, giving producers a wider industrial customer base and reducing dependence on construction cycles alone.

Increasing Demand for Oil Well Cement

Oil well cement is a technically demanding application for silica flour, used to prevent compressive strength retrogression in high-temperature wells. Demand from this application is driven by deepwater and high-pressure, high-temperature drilling programs, which require specialized cement systems. Qualification standards are stricter in this channel, resulting in a narrower approved supply base and firmer pricing compared to basic industrial grades. Performance failures in well cement result in significantly higher operational costs for the end user, reinforcing the value of certified, reliable supply. Some vertically integrated oilfield service companies are moving toward captive supply, which can limit third-party sales in certain regions. Oil well cement nonetheless remains a valuable outlet for the silica flour market, as it rewards technical reliability and product certification.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crystalline Silica Exposure Health and Regulatory Risks | -0.5% | Global, most acute in North America, Europe, and China | Short term (≤ 2 years) |

| Volatility in Mining Costs and Raw Material Supply | -0.4% | Global, especially North America and Southeast Asia | Medium term (2-4 years) |

| Environmental Restrictions on Mining and Processing | -0.3% | Asia-Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crystalline Silica Exposure and Regulatory Compliance Costs

Health and workplace regulations constrain the silica flour market, as processing and handling create direct exposure risks requiring permanent control systems. The Occupational Safety and Health Administration (OSHA) mandates a permissible exposure limit of 50 μg/m³ as an 8-hour time-weighted average, along with written exposure control plans, engineering controls, medical surveillance at the action level of 25 μg/m³, and long-term recordkeeping obligations[1]Occupational Safety and Health Administration, “Silica, Crystalline, Occupational Exposure to Respirable Crystalline Silica 29 C.F.R. § 1910.1053, General Industry and Maritime,” U.S. Department of Labor, osha.gov. These requirements raise both upfront and recurring costs for producers, making compliance a core operating issue. The silica flour market also faces a structural margin constraint, as these costs are harder to absorb in lower-value grades than in premium material. The U.S. Geological Survey (USGS) identifies crystalline silica exposure regulation as an ongoing concern for industrial sand and gravel operations, indicating that this issue will persist across the silica value chain. Consequently, the silica flour market is likely to favor operators with strong engineering controls and compliance systems.

Volatility in Mining Costs and Raw Material Supply

Cost volatility restrains the silica flour market, as the production chain includes crushing, milling, air classification, and, in premium grades, additional processing steps such as acid leaching and thermal treatment. The market is sensitive to swings in energy, labor, logistics, and raw material availability, as these factors directly affect operating margins. USGS reported that the average unit value of U.S. industrial sand and gravel fell to USD 36 per metric ton in 2025 from USD 40.9 in 2024, reflecting oversupply in the frac sand segment, which shares upstream infrastructure with industrial silica products. USGS also reported that U.S. ground high-purity quartz production fell to 100,000 tons in 2025 from 200,000 tons in 2024, showing how concentrated premium-grade supply can be disrupted by weather events and trade uncertainty. Covia raised industrial product prices by as much as 20%, effective June 1, 2026, indicating that cost pressure required direct pass-through rather than margin absorption. This creates a divide in the silica flour market between customers willing to pay for reliable specialty supply and those pushing back on pricing for standardized material.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Quartz Holds the Largest Base While Cristobalite Advances in Specialty Uses

Quartz accounted for 72.44% of revenue in 2025, the largest market share by type in the silica flour market. This reflects quartz's broad applicability across glass, foundry, fiberglass, and other established applications where cost efficiency and reliable availability remain priorities. The silica flour market continues to rely on quartz as its primary source, supporting both legacy demand and many upgraded product lines. However, the quartz segment is facing increasing specification requirements, as customers tighten impurity limits and demand more controlled particle distributions. The market is not moving away from quartz, but is requiring greater processing sophistication within the quartz category itself.

Producers that have invested in dry classification, flotation, and acid leaching are gaining access to higher-value contracts and longer supply arrangements. This operational gap is gradually creating a divide between standard quartz flour and upgraded grades that serve more demanding industrial applications. Cristobalite is the fastest-growing type, with its silica flour market size projected to expand at a 5.18% CAGR through 2031. Demand for cristobalite is rising as customers in architectural coatings, construction chemicals, and selected casting applications value its lower bulk density, whiteness profile, and reduced equipment abrasion characteristics. Cristobalite is gaining ground in specialty applications, while quartz remains the core revenue foundation across the broader silica flour market.

By End-Use Industry: Fiberglass Leads Current Revenue While Construction Chemicals Record the Fastest Growth

Fiberglass accounted for 34.86% of end-use revenue in 2025, the largest application segment in the silica flour market. This position relies on fiberglass in insulation, marine products, reinforced piping, composites, and wind energy components, all of which require consistent silica input quality. Advanced fiberglass production favors suppliers that can deliver consistent particle-size distributions and low contamination levels. As blade sizes and composite performance requirements increase, purchasing decisions are concentrating among approved suppliers with proven technical reliability. This strengthens contract quality for producers that can meet repeatable specifications, keeping fiberglass central to the silica flour market.

Construction chemicals are the fastest-growing end-use segment, with their silica flour market size projected to expand at a 5.34% CAGR through 2031. Growth in this category is tied to the use of silica flour in high-performance concrete, repair mortars, specialty grouts, and polymer-modified formulations where performance and finish quality are prioritized over simple filler volume. Infrastructure and urban development projects continue to favor materials with greater durability, workability, and crack resistance, benefiting the silica flour market. Other major applications, including glass, foundry, ceramics and refractories, paints and coatings, and oil well cement, provide a broad demand base, reducing the silica flour industry's dependence on any single end market. This combination of stable applications and faster-growing technical uses gives the silica flour market a balanced demand structure, with fiberglass anchoring current revenue and construction chemicals driving forward growth.

Geography Analysis

Asia-Pacific held 45.27% of the silica flour market share in 2025 and is forecast to register the fastest CAGR of 6.18% through 2031. The region leads due to demand for glass, ceramics, fiberglass, and construction chemicals across China, India, Japan, South Korea, and Southeast Asia. The silica flour market is concentrated in this region because downstream industries are clustered, export-oriented, and focused on product quality and scale. China remains the primary regional hub, though its market role is shifting from volume absorption toward tighter specification-setting for purity and product consistency. India is growing in importance to the silica flour market, as buyers seek alternative supply platforms and local downstream demand continues to expand.

North America and Europe form the premium-value core of the silica flour market, as regional demand is driven by specialized glass, filtration, semiconductor-related, and high-performance construction applications. U.S. Silica expanded its specialty focus by opening the Rochelle Innovation Center in Illinois in September 2025, which supports product development for filtration, renewable diesel, and industrial oil applications. Sibelco reported first half (H1) 2025 revenue of EUR 1,153 million (equivalent to USD 1.3 billion), attributing growth to performance in core European markets and Asia-Pacific[2]Sibelco, “Sibelco Delivers 7% Revenue Growth Despite Challenges,” Sibelco, sibelco.com. These regions remain significant to the silica flour market for volume, higher revenue per ton, and a mix of differentiated grades.

South America, the Middle East and Africa, and the rest of Europe account for smaller shares of the silica flour market, with each region having a distinct demand profile. Brazil is notable because construction activity and deepwater oil well cementing support specialized silica use within a single national market. The Middle East and Africa are driven by glass, ceramics, and construction demand, with regional suppliers benefiting from shorter delivery routes and local customer relationships. The rest of Europe remains relevant as sourcing patterns shift and buyers seek dependable supply outside disrupted trade corridors.

Competitive Landscape

The silica flour market is moderately fragmented globally, with Sibelco, U.S. Silica, Covia Holdings, and Quarzwerke GmbH operating as key competitors within their respective regional strongholds. The market also includes a broad base of regional specialists that remain relevant, as freight costs, local availability, and application support often outweigh global scale in customer decisions. This combination of large integrated suppliers and numerous local operators keeps the market competitive without full fragmentation. Market leadership tends to be stronger within regional cores than at the global level. The silica flour market shows notable concentration in select geographies while still offering room for smaller players in localized industrial clusters.

Recent strategies in the silica flour market have centered on ownership changes, pricing discipline, portfolio upgrades, and investment in higher-value products. Apollo agreed to acquire U.S. Silica for USD 1.85 billion in 2023, reflecting the view of silica assets as cash-generative industrial platforms with room for operational improvement. Sibelco repositioned its platform through its Build 2030 framework and its 2024 acquisition of Strategic Materials Inc., which added recycled glass capability and strengthened its circular-material offering. U.S. Silica's Rochelle Innovation Center signals that technical development is becoming a more visible component of competition in the silica flour market. These moves indicate that major companies are working to increase specialty exposure relative to commodity exposure rather than competing solely on extraction scale.

Pricing behavior in 2025 and 2026 reflected that cost recovery and grade differentiation are central to the silica flour market. U.S. Silica announced price increases of up to 20% across its industrial product range, effective January 1, 2026, and Covia announced a comparable increase effective June 1, 2026, both in response to rising energy, labor, logistics, and materials costs. Regulatory pressure around crystalline silica handling is making compliance quality a stronger competitive differentiator, as customers increasingly value suppliers with sound operating controls and lower exposure risk profiles. Contract strength is increasingly tied to product quality, processing discipline, and operational credibility rather than mine ownership alone.

Silica Flour Industry Leaders

Sibelco

U.S. Silica

Covia Holdings LLC

Adwan Chemical Industries Co. Ltd.

AGSCO Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: U.S. Silica announced price increases of up to 20% across its Industrial and Specialty Products segment, effective January 1, 2026, covering glass, filtration, foundry, paints, coatings, elastomers, and other industrial applications. This marked the second consecutive year of double-digit price adjustments, driven by input cost pressures faced by North American silica processors.

- September 2025: U.S. Silica inaugurated its Rochelle Innovation Center in Rochelle, Illinois, a 10,000-square-foot R&D laboratory and pilot plant facility adjacent to its Ottawa mining operations. The center focuses on specialty-grade product development for filtration, renewable diesel, and industrial oil applications, supporting a strategic shift toward higher-margin, differentiated silica product lines.

Global Silica Flour Market Report Scope

Silica flour is a finely ground, high-purity crystalline silica (silicon dioxide, SiO₂) produced by milling high-grade quartz. It is characterized by hardness, thermal stability, chemical inertness, and abrasion resistance.

The Silica flour market is segmented by type, end-use industry, and geography. By type, the market is segmented into quartz and cristobalite. By end-use industry, the market is segmented into glass, foundry, fiberglass, oil well cement, ceramics and refractory, paints & coatings, construction chemicals, and other end-use industries. The report also covers market size and forecasts for silica flour across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Quartz |

| Cristobalite |

| Glass |

| Foundry |

| Fiberglass |

| Oil Well Cement |

| Ceramics and Refractory |

| Paints & Coatings |

| Construction Chemicals |

| Other End-use Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Quartz | |

| Cristobalite | ||

| By End-Use Industry | Glass | |

| Foundry | ||

| Fiberglass | ||

| Oil Well Cement | ||

| Ceramics and Refractory | ||

| Paints & Coatings | ||

| Construction Chemicals | ||

| Other End-use Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Silica Flour Market?

The Silica Flour Market size is projected to expand from USD 679.52 million in 2025 and USD 707.26 million in 2026 to USD 869.41 million by 2031, and is expected to register a CAGR of 4.21% between 2026 and 2031.

Which type leads silica flour demand today?

Quartz led the market in 2025 with a 72.44% revenue share because it remains cost-effective and widely used across glass, foundry, and fiberglass applications.

Which end-use application is the largest for silica flour?

Fiberglass was the largest end-use segment in 2025 with a 34.86% revenue share, reflecting its broad use in insulation, composites, piping, and wind energy components.

Which region is growing the fastest in silica flour?

Asia-Pacific was the largest regional market in 2025 with a 45.27% share and is also the fastest-growing region, with a projected 6.18% CAGR through 2031.

Page last updated on: