SiC Ingots Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

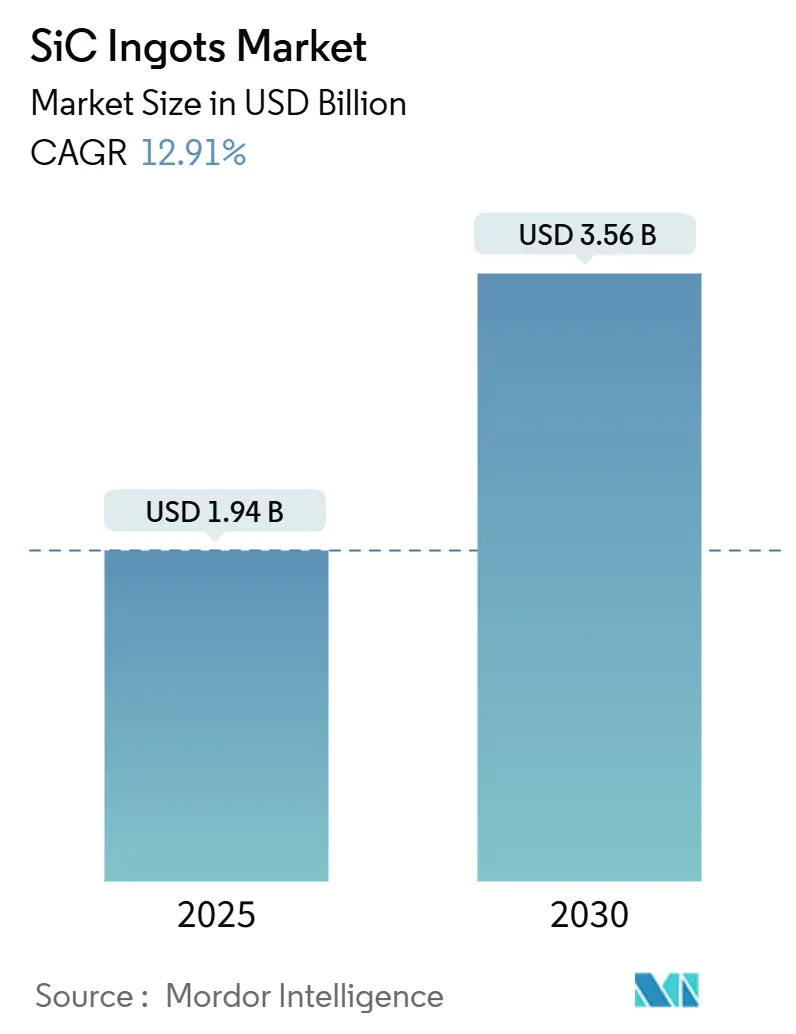

| Market Size (2025) | USD 1.94 Billion |

| Market Size (2030) | USD 3.56 Billion |

| Growth Rate (2025 - 2030) | 12.91% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

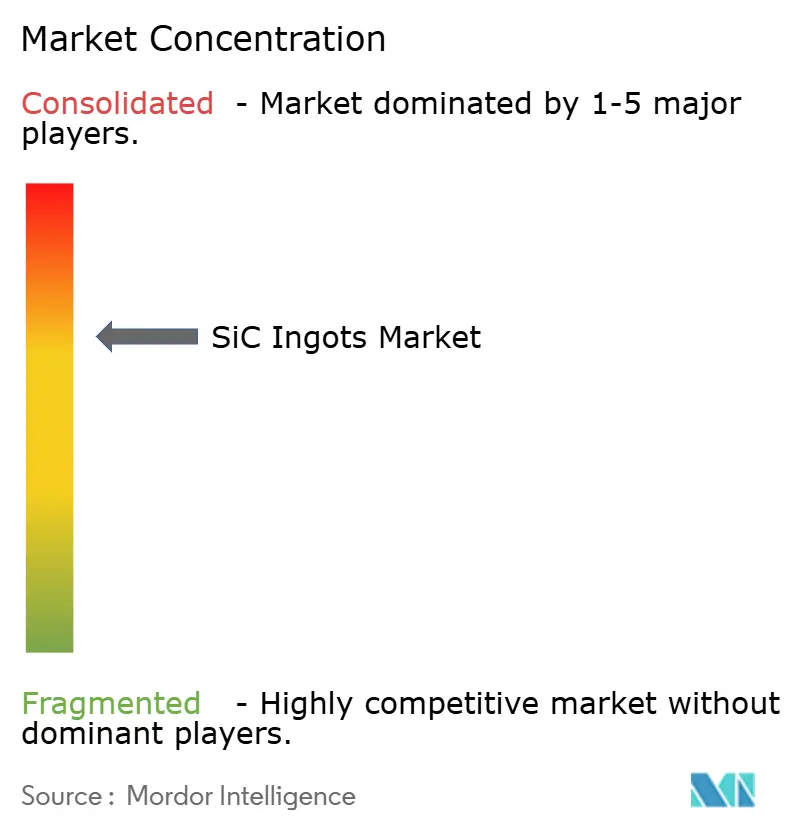

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SiC Ingots Market Analysis by Mordor Intelligence

The SiC ingots market size is valued at USD 1.94 billion in 2025 and is projected to reach USD 3.56 billion by 2030, translating into a CAGR of 12.91% across the forecast window. Throughout the period, the silicon ingot market is being reshaped by intersecting forces: automotive OEMs are moving to 800 V battery platforms, governments are subsidizing onshore wide-bandgap supply chains, and producers are shifting from 6-inch to 8-inch boules to curb per-die costs by nearly 30%. Export-control frictions on crystal-growth furnaces are forcing regional buildouts instead of globally integrated plants, thereby tightening supply in the short term while raising long-term localization opportunities. Equipment makers are accelerating tool roadmaps for 8-inch throughput, and capital flows from strategic investors are underwriting riskier furnace upgrades that shorten the yield-learning curve. Against this backdrop, the sic ingots market is entering a volume expansion phase that favors vendors able to combine scale economics with advanced defect-mapping metrology.

Key Report Takeaways

- By ingot diameter, 6-inch substrates led with a 79.12% SiC ingots market share in 2024, while 8-inch ingots are projected to track a 13.83% CAGR to 2030.

- By polytype, 4H-SiC accounted for 82.14% of the output in 2024 and is expected to expand at a 13.49% CAGR through 2030.

- By conductivity type, N-type substrates accounted for 66.73% of demand in 2024, whereas semi-insulating material is projected to grow at a 13.21% CAGR to 2030.

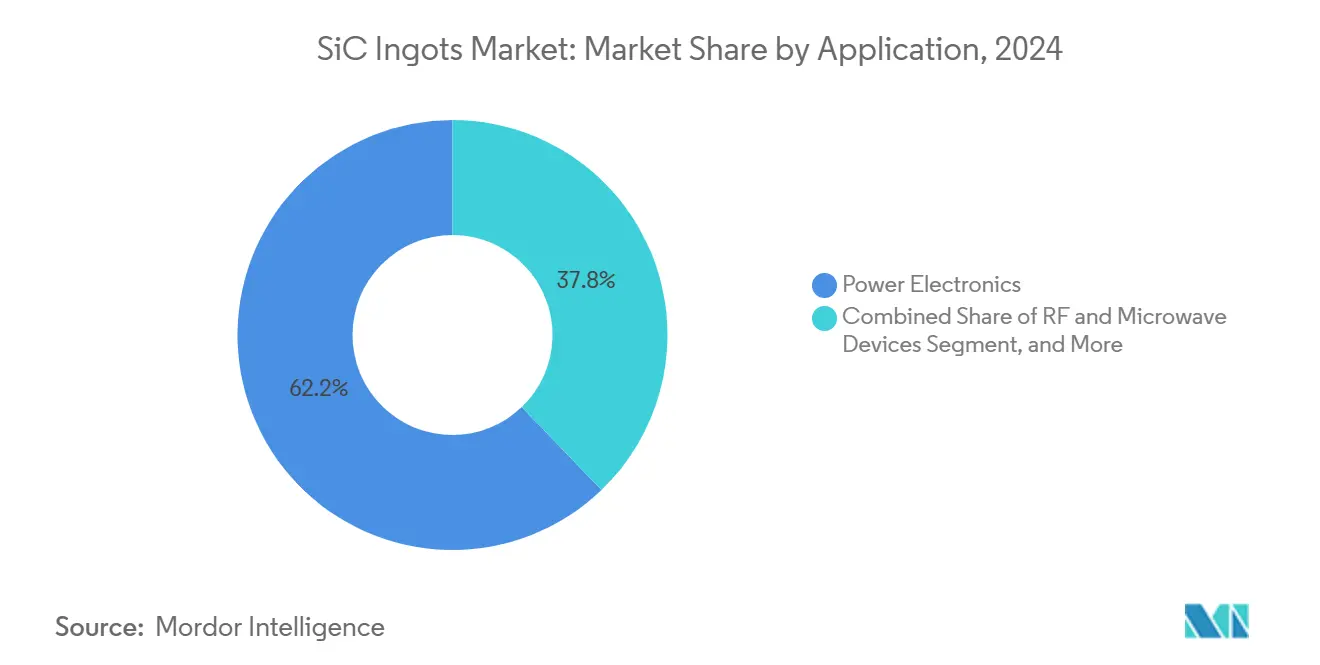

- By application, power electronics represented 62.19% of usage in 2024, and RF and microwave devices constitute the fastest-growing slot at a 13.77% CAGR to 2030..

- By growth method, physical vapor transport retained an 87.23% share in 2024; high-temperature CVD is projected to grow at 13.54% through 2030.

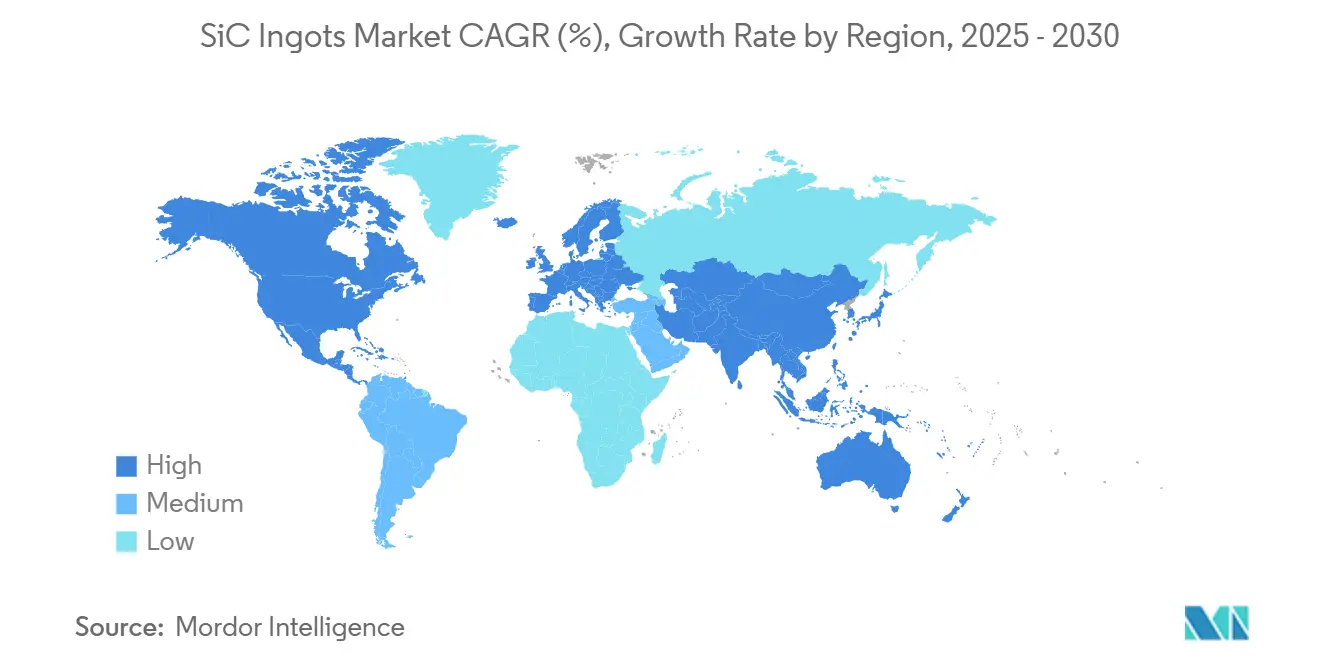

- By geography, the Asia-Pacific region captured 54.78% of sales in 2024, but Europe is forecast to rise at a 13.89% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SiC Ingots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift to 800V Electric Vehicle Architectures | +3.2% | Global, with early concentration in Europe and China | Medium term (2-4 years) |

| Government Incentives for Onshore Wide-Bandgap Supply Chains | +2.8% | North America, Europe, China | Long term (≥ 4 years) |

| Rapid Scale-Up of 8-Inch Wafer Lines | +2.5% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Emergence of European Domestic SiC Substrate Producers | +1.9% | Europe, with indirect effects on North America | Long term (≥ 4 years) |

| Advancements in High-Purity 6N SiC Powder Synthesis | +1.4% | Global | Long term (≥ 4 years) |

| Data Center AI Compute Power Density Surge | +1.1% | North America and Asia-Pacific, early adoption in hyperscale facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to 800V Electric Vehicle Architectures

Automakers are standardizing on 800V traction inverters to achieve sub-20-minute fast charging and smaller wiring harnesses, conditions that silicon devices cannot meet without incurring heavy conduction losses. Porsche, Hyundai, Kia, and General Motors have secured SiC MOSFETs for their next-generation platforms, effectively tripling SiC die demand per vehicle.[1]Roland Berger, “E-Mobility Index Q1/2024,” rolandberger.com As design cycles in the automotive sector run for 5-7 years, substrate suppliers gain multi-year volume visibility, accelerating furnace capital payback and anchoring the SiC ingots market in long-term contracts.

Government Incentives for Onshore Wide-Bandgap Supply Chains

Subsidy programs are shifting capacity placement decisions from lowest-cost to sovereign-priority logic. The United States CHIPS and Science Act allocates USD 52.7 billion, with Wolfspeed originally awarded USD 2.5 billion for domestic SiC lines.[2]U.S. Department of Commerce, “CHIPS and Science Act,” commerce.gov Europe’s Chips Act commits EUR 43 billion (USD 46.9 billion) in support, allowing STMicroelectronics to invest EUR 5 billion (USD 5.5 billion) in vertically integrated SiC plants. China has earmarked CNY 344 billion (USD 47 billion) for the same purpose. These interventions mute early-stage financial risk and fast-track local champions, pushing the sic ingots market toward regionally balanced capacity.

Rapid Scale-Up of 8-Inch Wafer Lines

Six-inch lines remain dominant, yet 8-inch boules deliver 1.8 times die surface area at roughly 25% lower epi cost per square centimeter, a critical lever as EV and renewable energy converters chase cost parity. TrendForce counts 14 greenfield or retrofit fabs scheduled to start 8-inch output between 2025 and 2027, which is expected to exceed 1.2 million wafers per year by 2028. Early movers include SiCrystal’s EUR 500 million (USD 545 million) Nuremberg build-out and Wolfspeed’s Mohawk Valley site, albeit now delayed. The Shift is compressing equipment lead times and redistributing pricing power toward furnace vendors with qualified 8-inch tool sets.

Data Center AI Compute Power Density Surge

Hyperscale operators are confronting 100 kW-plus racks as AI accelerators drive higher current draw, making traditional silicon power supplies untenable. Google’s 2024 sustainability filing cited a transition to 48 V direct-to-chip distribution, and Microsoft has secured a multi-year SiC substrate deal for 98% conversion efficiency modules.[3]Microsoft Corporation, “Annual Report 2024,” microsoft.com Although the volume is smaller than that of the automotive sector, premium pricing and tight micropipe specifications below 1 cm² create an outsized revenue stream that rewards suppliers with best-in-class defect control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Crystal Growth Yield Bottlenecks | -2.1% | Global, with acute effects in 8-inch production | Medium term (2-4 years) |

| Shortfall of Ultra-High-Temperature Graphite Consumables | -1.6% | Asia-Pacific, indirect pressure on North America and Europe | Short term (≤ 2 years) |

| Export Controls on Critical Furnace Technology | -1.3% | China, with secondary effects on global equipment lead times | Long term (≥ 4 years) |

| Volatile Pricing of Specialty Power Electronics Grade Graphite | -0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Crystal Growth Yield Bottlenecks

Physical vapor transport yields only 60-70% usable boule mass at 6 inches and drops below 50% at 8 inches, primarily due to micropipe formation at growth temperatures of 2,200-2,400 °C. The stochastic defect landscape forces overproduction, elevates working capital, and extends cash-conversion cycles across the sic ingots market. Vanadium-doped semi-insulating runs amplify the challenge because the resistivity target above 10⁵ Ω-cm shrinks the acceptable process window.

Shortfall of Ultra-High-Temperature Graphite Consumables

Japan’s 2024 export-control extension added semiconductor-grade graphite to its restricted list, lengthening crucible replacement lead times from 8 to 12 weeks to 20 to 26 weeks for Chinese buyers. Toyo Tanso and Tokai Carbon account for roughly 60% of global supply and have not announced expansions sized for the 8-inch wave, causing furnace operators throughout the sic ingots market to carry larger inventories and tie up more cash in spares.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingot Diameter: 8-Inch Formats Capture Cost-Sensitive Tiers

The sic ingots market registered a 79.12% share for 6-inch material in 2024, reflecting the legacy install base in automotive power modules. Between 2025 and 2030, 8-inch ingots are projected to grow at 13.83%, underpinned by a 30% per-die cost advantage that offsets the requalification expense for epitaxy lines. Industry announcements of 14 dedicated 8-inch fabs through 2027 reinforce a supply-led pivot that typically precedes rapid share migration.

Four-inch and 2-inch diameters remain confined to RF prototypes and photonics labs, while exploratory 12-inch boules have yet to clear proof-of-concept hurdles. Vendors are allocating capital toward 8-inch yield breakthroughs instead of leap-frogging to 12-inch, mirroring silicon’s staircase but on a compressed timetable. As utilization rates climb, the sic ingots market size attributable to 8-inch formats is poised to surpass USD 1 billion by 2030, providing additional volume breathing room for downstream device lines.

By Polytype: 4H-SiC’s Dual-Use Advantage

4H-SiC accounted for 82.14% of 2024 shipments and is growing faster than the market at 13.49%, driven by its power-device and RF versatility. Its 3.26 eV bandgap and high electron mobility support both traction inverters and GaN-on-SiC radar amplifiers, giving OEMs a one-substrate roadmap. Investment in design libraries, tool recipes, and process kits has locked in switching costs that insulate 4H-SiC from share erosion.

6H-SiC occupies niche industrial heating roles, while 3C-SiC remains academic. Without a defect-free 3C growth breakthrough, the SiC ingots market will remain anchored to 4H-SiC for the forecast horizon, ensuring that scale economies keep wafer pricing on a steady downward glide path.

By Conductivity Type: Semi-Insulating Substrates Ride Defense Budgets

N-type conductive boules held 66.73% share in 2024, driven by automotive and industrial demand for low on-resistance MOSFETs. Semi-insulating inventory, however, is pacing a 13.21% CAGR as defense-funded phased-array radar and satellite programs specify GaN-on-SiC amplifiers. Qorvo logged a 40% jump in semi-insulating substrate consumption in 2024, validating the pull from secure-supply buyers.

Vanadium doping increases semi-insulating costs by 20-25%, but defense customers accept the premium in exchange for lattice isolation and improved thermal management. The split positions suppliers with dual doping lines to capture volume and margin simultaneously, broadening the sic ingots market size opportunities on both price bands.

By Application: Power Electronics’ Automotive Anchor

Power electronics generated 62.19% of ingot demand in 2024 and will remain the gravitational center of the SiC ingots market as 800V penetration widens. RF and microwave devices, advancing at 13.77%, absorb semi-insulating output for 5G mid-band and Ka-band satellites. Industrial heating elements exhibit stable, low-single-digit growth, while photonics remains a niche market.

Research and prototyping volumes are small yet strategically vital, providing early cash flow for new polytypes and diameters. Quantum-computing explorations could eventually open a third pillar of demand, but commercialization lies beyond the forecast window.

By Growth Method: PVT’s Incumbency Versus HTCVD’s Precision

Physical vapor transport owned 87.23% of 2024 shipments, aligning with furnace fleet economics and doping flexibility. HTCVD, advancing at 13.54%, wins contracts where micropipe guarantees below 0.1 cm⁻² justify a 40-50% cost premium. Solution growth remains at the lab scale; GT Advanced Technologies has demonstrated 6-inch boules with a 0.5 cm² micropipe density, but has not yet announced a firm release date.

Yield learning on PVT 8-inch runs remains the primary cost lever for the sic ingots market, and vendors deploying in-situ X-ray feedback loops expect a 10-15 percentage-point utilization lift by 2027.

Geography Analysis

The Asia-Pacific dominated the sic ingots market with a 54.78% share in 2024, driven by China’s capacity surge and Japan’s mature supply chain. Chinese firms TanKeBlue, SICC, and Shanxi Semisic collectively announced 600,000 additional 6-inch and 8-inch wafers by 2027, targeting the domestic EV and solar segments. Japan retains strong vertical integration, although export-control frictions on graphite are nudging automotive tier ones to qualify non-Japanese sources.

Europe is forecast to log the highest regional CAGR at 13.89% as the EUR 5 billion (USD 5.5 billion) STMicroelectronics complex in Catania and Crolles comes online by late 2025. Soitec’s 6-inch license deal aims for 50,000 wafers by 2027, cushioning its dependency on imports. EU designations of SiC as a strategic raw material streamline permitting and financing, giving European entrants a regulatory tailwind.

North America sits mid-pack after Wolfspeed’s October 2024 Chapter 11 filing stalled 8-inch ramp plans, pushing some automotive programs to seek European or Asian alternatives. Canada and Mexico remain peripheral, and the Middle East and South America only register exploratory joint-venture talks. Regional diversification is therefore deepening, but absolute capacity growth still centers on the Asia-Pacific region.

Competitive Landscape

The top five suppliers controlled an estimated 65-70% of the capacity in 2024, placing the overall concentration in the mid-to-high range. Wolfspeed’s restructuring has fractured historic single-source deals, enabling SiCrystal, SICC, and TanKeBlue to secure European automotive slots. Western incumbents double down on yield and metrology to defend premium pricing, while Chinese entrants prioritize volume even at higher defect levels.

Technology leadership is migrating toward real-time defect-mapping furnaces. SiCrystal’s EP4012345 patent describes a closed-loop PVT reactor that adapts to temperature gradients mid-run, thereby reducing micropipe rates. Equipment disruptors like Jingsheng are marketing PVT tools at 40-50% lower sticker prices than Japanese peers, slashing capex hurdles for emerging makers. Concurrently, device manufacturers such as STMicroelectronics and ROHM are internalizing substrate lines to secure supply and capture market share, thereby shrinking the merchant addressable pool and intensifying competition for independent vendors.

The market’s white space lies in semi-insulating substrates for defense and satellite payloads, where domestic sourcing mandates override cost considerations. European niche producers partner with GaN epi specialists to carve out this premium segment, distancing themselves from volume-driven Asian competitors. Overall, strategic differentiation rests on defect control, furnace innovation, and vertical integration agility across the sic ingots market.

SiC Ingots Industry Leaders

Wolfspeed, Inc.

SiCrystal GmbH

SICC Co., Ltd.

Beijing TanKeBlue Semiconductor Co., Ltd.

EEMCO GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The European Investment Bank and STMicroelectronics closed a EUR 1 billion (USD 1.13 billion) financing deal that backs the company’s SiC substrate and power device expansion in Italy and France. An initial EUR 500 million (USD 565 million) tranche was released the same month, fast-tracking 200 mm wafer production in Catania by Q4 2025 and establishing the largest domestic SiC substrate capacity in Europe for automotive power modules.

- October 2025: Mitsubishi Electric finished building its new Kumamoto, Japan facility after a JPY 100 billion (USD 660 million) outlay. The site started pilot runs on 8-inch lines geared for 60,000 wafers a year by 2027, bolstering Japan’s SiC supply base for electric-vehicle and industrial customers.

- April 2025: STMicroelectronics confirmed that 200 mm SiC wafer output at its Catania plant remains on track for Q4 2025 under the company’s EUR 5 billion vertical-integration program. The facility is slated to reach 50,000 wafers a year by 2028 and will supply Stellantis, Volkswagen and Renault under long-term contracts.

- March 2025: Wolfspeed emerged from Chapter 11 after a court-approved restructuring that cut debt by USD 3.2 billion and pushed the Mohawk Valley and Siler City ramps to 2027-2028. The company kept its USD 2.5 billion CHIPS Act grant contingent on meeting performance milestones, and automakers such as General Motors and Mercedes-Benz resumed substrate qualification even as some tier-ones diversified sourcing during the bankruptcy period.

Global SiC Ingots Market Report Scope

The SiC Ingots Market Report is Segmented by Ingot Diameter (2-Inch, 4-Inch, 6-Inch, 8-Inch, 12-Inch), Polytype (3C-SiC, 4H-SiC, 6H-SiC), Conductivity Type (N-Type Conductive, and Semi-Insulating), Application (Power Electronics, RF and Microwave Devices, Industrial Heating Components, Photonics and Optoelectronics, Research and Prototyping), Growth Method (Physical Vapor Transport, High-Temperature Chemical Vapor Deposition, Solution Growth), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| 2-Inch |

| 4-Inch |

| 6-Inch |

| 8-Inch |

| 12-Inch |

| 3C-SiC |

| 4H-SiC |

| 6H-SiC |

| N-Type Conductive |

| Semi-Insulating |

| Power Electronics |

| RF and Microwave Devices |

| Industrial Heating Components |

| Photonics and Optoelectronics |

| Research and Prototyping |

| Physical Vapor Transport (PVT) |

| High-Temperature Chemical Vapor Deposition (HTCVD) |

| Solution Growth |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Ingot Diameter | 2-Inch | ||

| 4-Inch | |||

| 6-Inch | |||

| 8-Inch | |||

| 12-Inch | |||

| By Polytype | 3C-SiC | ||

| 4H-SiC | |||

| 6H-SiC | |||

| By Conductivity Type | N-Type Conductive | ||

| Semi-Insulating | |||

| By Application | Power Electronics | ||

| RF and Microwave Devices | |||

| Industrial Heating Components | |||

| Photonics and Optoelectronics | |||

| Research and Prototyping | |||

| By Growth Method | Physical Vapor Transport (PVT) | ||

| High-Temperature Chemical Vapor Deposition (HTCVD) | |||

| Solution Growth | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current dollar value of the sic ingots market?

The sic ingots market size stands at USD 1.94 billion in 2025.

How fast is global demand expected to grow?

Between 2025 and 2030, the market is forecast to register a 12.91% CAGR.

Which ingot diameter is gaining momentum fastest?

8-inch boules are forecast to expand at a 13.83% CAGR thanks to lower per-die costs and higher die counts.

Why are semi-insulating substrates becoming more important?

Defense radar and satellite programs need GaN-on-SiC amplifiers, lifting semi-insulating demand at a 13.21% CAGR.

Which region will post the strongest growth?

Europe is projected to log the highest regional CAGR at 13.89% through 2030, aided by Chips Act subsidies.

Which growth method dominates commercial supply?

Physical vapor transport accounts for 87.23% of production, remaining the backbone of the sic ingots market.

Page last updated on: