Sensor-Based Sorting Machine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

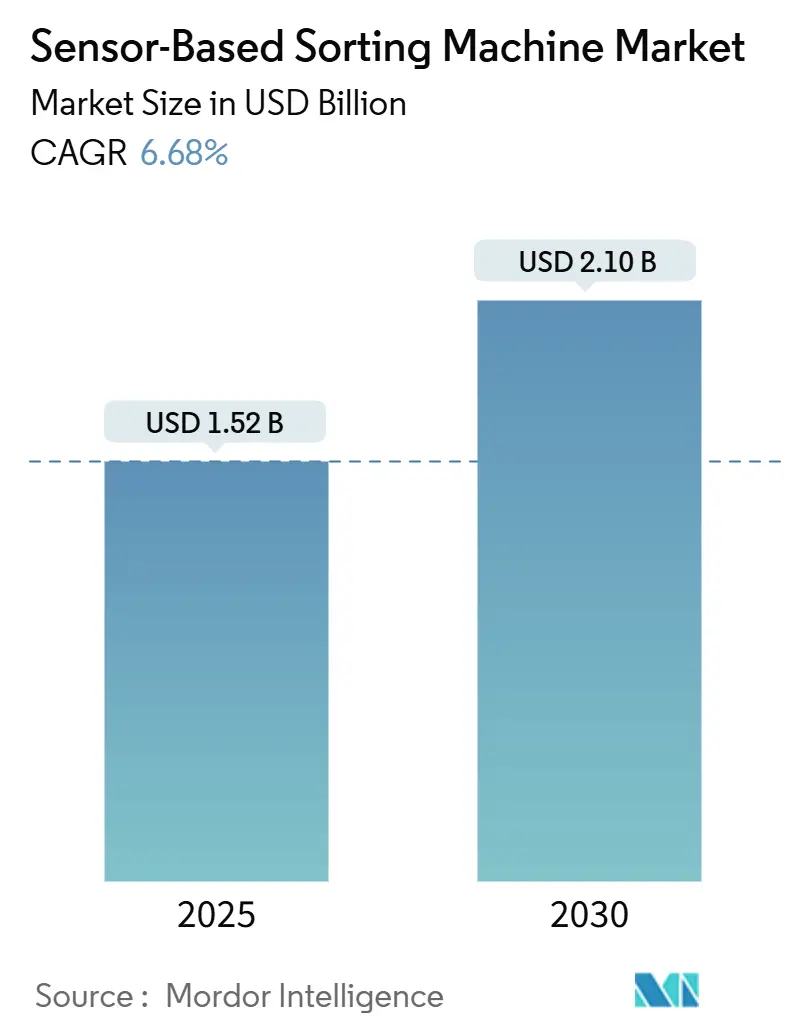

| Market Size (2025) | USD 1.52 Billion |

| Market Size (2030) | USD 2.10 Billion |

| Growth Rate (2025 - 2030) | 6.68% CAGR |

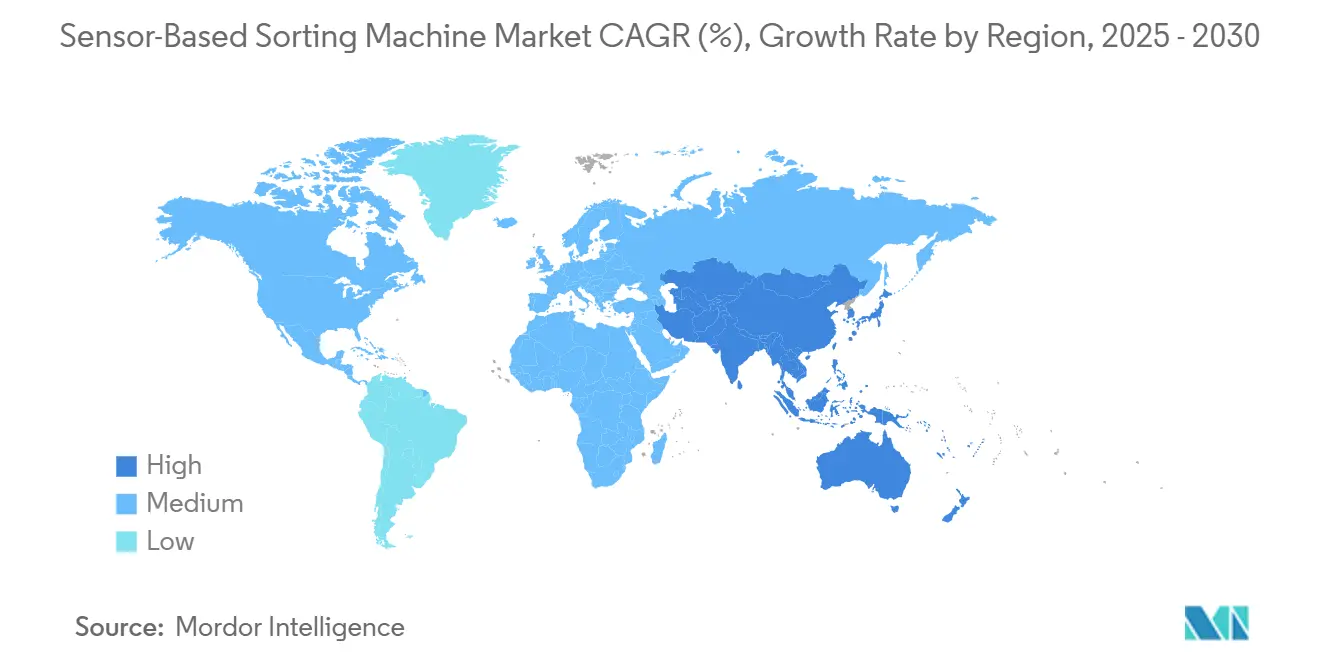

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

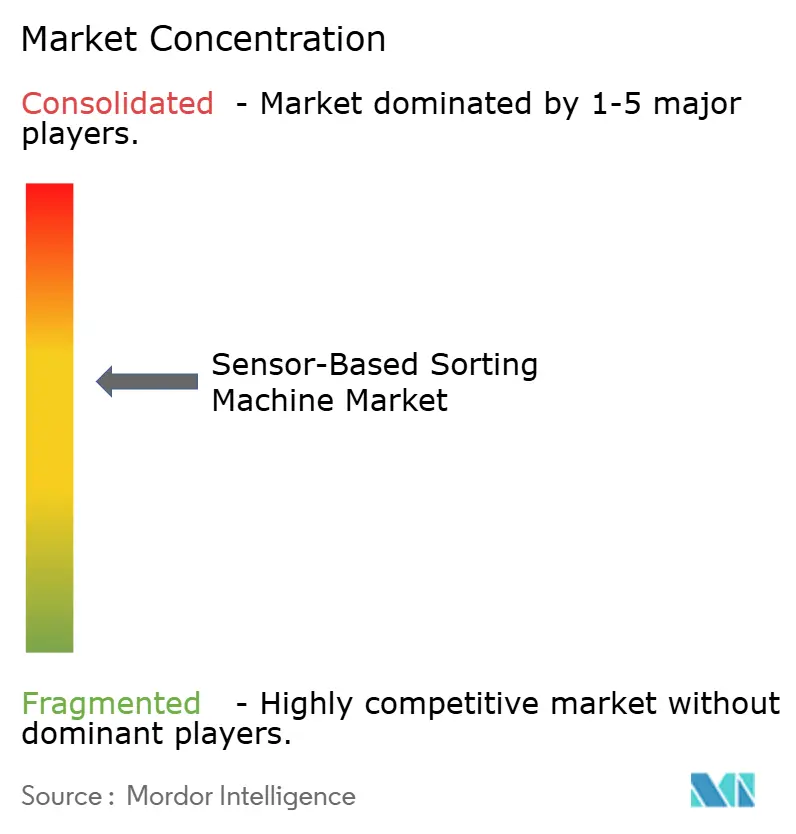

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensor-Based Sorting Machine Market Analysis by Mordor Intelligence

The sensor-based sorting machine market size is valued at USD 1.52 billion in 2025 and is forecast to reach USD 2.10 billion by 2030, reflecting a 6.68% CAGR across the period. This steady expansion stems from tighter contamination limits in mining, recycling, and food processing, where automated precision sorting mitigates material loss and boosts yield. Rising global emphasis on resource efficiency, coupled with labour shortages in high-risk manual sorting jobs, intensifies adoption of advanced detection platforms. Strategically, suppliers are embedding edge-based AI and multi-sensor fusion to deliver real-time optimization, while buyers demand flexible architectures that accommodate shifting feedstocks. Supply-chain fragility in imaging components and X-ray tubes presents near-term cost pressure, yet medium-term investment commitments signal resilience for the broader sensor-based sorting machine market.[1]European Investment Bank, “Circular Economy Investment Report 2024,” EIB.ORG

Key Report Takeaways

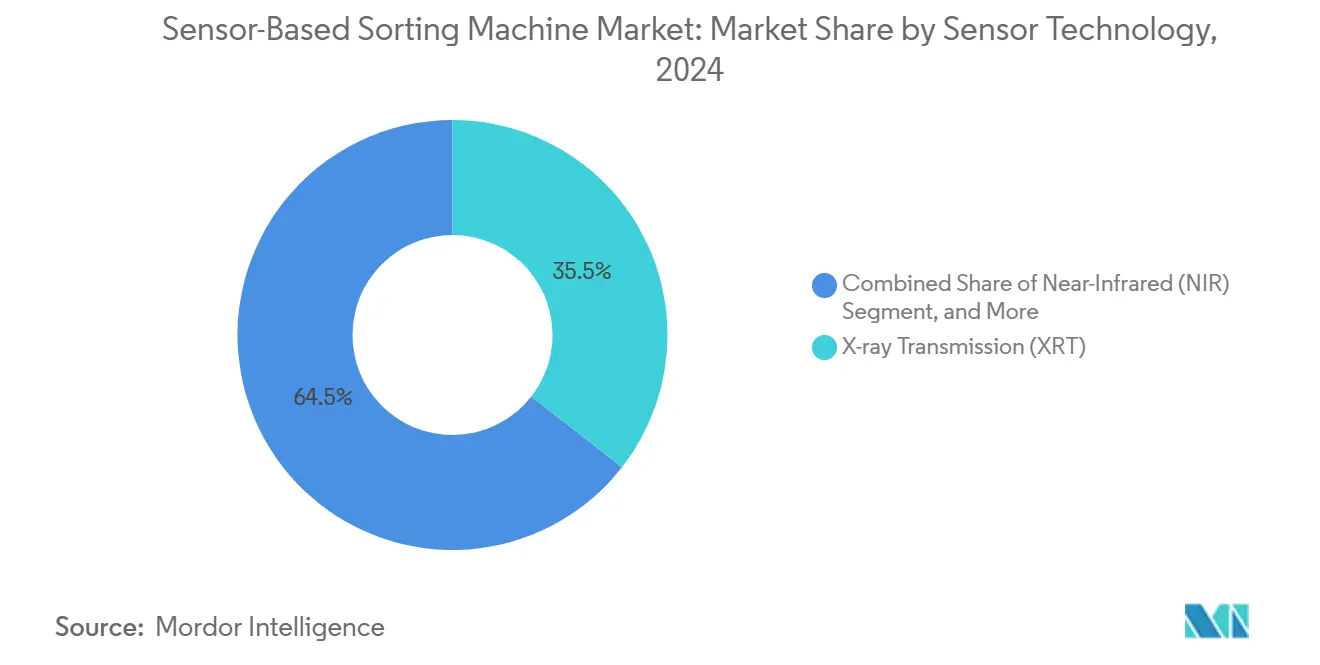

- By sensor technology, X-ray transmission captured 34.83% of sensor-based sorting machine market share in 2024, while hyperspectral imaging is projected to expand at a 7.11% CAGR through 2030.

- By sorting configuration, belt sorters led with 38.74% revenue share in 2024 in the sensor-based sorting machine market; robotic pick-and-place units are advancing at a 7.33% CAGR to 2030.

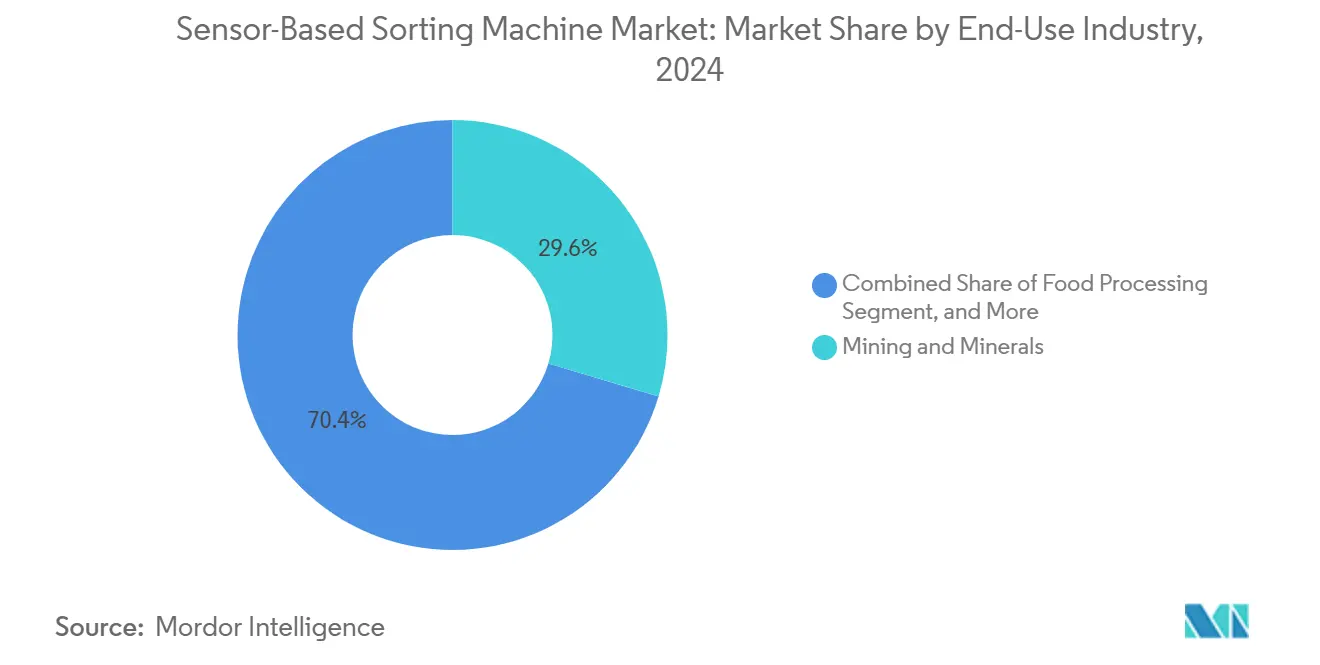

- By end-use industry, mining and minerals accounted for 29.61% of the sensor-based sorting machine market size in 2024, whereas recycling-plastics exhibits the highest forecast CAGR at 6.99% to 2030.

- By throughput capacity, systems above 200 TPH held 41.83% of sensor-based sorting machine market size in 2024, yet installations below 50 TPH are growing fastest at 7.55% CAGR.

- By geography, North America maintained 38.74% market share in 2024 in the sensor-based sorting machine market; Asia-Pacific represents the fastest-growing regional opportunity with a 7.66% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sensor-Based Sorting Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-purity recycled materials | +1.8% | Global, with concentration in EU and North America | Medium term (2-4 years) |

| Increasing labour shortages and wage inflation in sorting operations | +1.5% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Stricter global regulations on waste and mineral recovery rates | +1.2% | Global, led by EU regulatory frameworks | Long term (≥ 4 years) |

| Growing adoption of Industry 4.0 and AI-enabled inline analytics | +1.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Surge in lithium-bearing ore processing for battery supply chains | +0.9% | Global, concentrated in Australia, Chile, Argentina | Short term (≤ 2 years) |

| ESG-driven investment into closed-loop resource cycles | +0.7% | North America and EU, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Purity Recycled Materials

Demand for near-virgin quality recycled inputs is reshaping procurement specifications, pushing contamination thresholds below 0.1% for food-grade resins and elevating lithium-ion battery feed requirements.[2]European Commission, “Circular Economy Action Plan Implementation Report,” EC.EUROPA.EU Sorting plants now standardize multi-sensor systems that pair near-infrared, hyperspectral, and optical detectors to isolate polymers and critical metals with 99.5% accuracy. Municipal mandates under the EU Circular Economy Action Plan accelerate infrastructure upgrades, while premium buyers agree to long-term offtake contracts, improving capital recovery prospects for automated lines. In metals, cathode-to-cathode recycling depends on precise spectral separation to maintain electrochemical profiles, enhancing the investment narrative for the sensor-based sorting machine market. Forward-looking operators integrate cloud-linked analytics that document purity proof points for downstream auditors, creating data-driven differentiation.

Increasing Labour Shortages and Wage Inflation in Sorting Operations

Annual wage inflation above 8% in North American and European sorting facilities intensifies substitution of human pickers with robotic or automated classifiers.[3]International Labour Organization, “Future of Work in Industrial Automation,” ILO.ORG Recruitment shortfalls, compounded by heightened safety regulations for hazardous e-waste streams, lengthen vacancy periods and raise training costs. Robotic pick-and-place platforms offset these gaps, posting a 7.33% CAGR as users replace multiple manual sorters per shift. AI-guided vision systems outperform fatigued workers during extended shifts, maintaining steady throughput and purity targets. For operators, labour cost certainty outweighs the capital burden, shortening payback horizons despite high initial outlays. Policy incentives such as tax credits for automation and workforce retraining grants further de-risk adoption across the sensor-based sorting machine market.

Stricter Global Regulations on Waste and Mineral Recovery Rates

Legislators now tie operating permits to audited recovery metrics: the EU Waste Framework Directive imposes a 70% material reclamation target for construction waste by 2025, and China’s National Sword policy bans low-grade recyclables, compelling domestic processors to upgrade. Mining authorities intensify tailings controls, requiring demonstrable mineral recovery improvements to reduce environmental footprints. Parallel food-safety statutes from the FDA and EFSA push processors to detect invisible contaminants, raising standards for optical and hyperspectral detectors. Collectively, these rules build a compliance-driven moat around advanced separation solutions, bolstering equipment orders among mid-tier players that previously relied on manual inspection. Over the forecast horizon, regulatory harmonization will tighten global baselines, locking in expansion for the sensor-based sorting machine market.

Growing Adoption of Industry 4.0 and AI-Enabled Inline Analytics

Processing plants now couple edge-based compute modules with cloud dashboards to enable real-time feedback loops.[4]TOMRA Systems ASA, “Annual Report 2024,” TOMRA.COM Machine-learning models ingest spectral and particle-size data to adjust air jets or robotic trajectories within milliseconds, boosting yield and reducing false rejects. Operators leverage predictive maintenance alerts derived from vibration and temperature sensors, curbing unplanned downtime. In APAC, leapfrogging investments embed smart-factory architectures from the outset, illustrating how emerging markets may drive the next wave of growth in the sensor-based sorting machine industry. Suppliers respond with subscription models bundling analytics updates and remote calibration, creating recurring revenue streams that smooth equipment replacement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure and long pay-back periods | -0.9% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

| Limited sensor performance on moist or dusty feed material | -0.6% | Mining-heavy regions, tropical climates | Medium term (2-4 years) |

| Scarcity of skilled technicians for calibration and maintenance | -0.5% | Global, acute in developing markets | Medium term (2-4 years) |

| Trade restrictions on critical imaging chips and X-ray tubes | -0.4% | Global, particularly US-China trade corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Long Pay-Back Periods

Acquiring state-of-the-art systems demands USD 500,000–2 million per line, an entry hurdle that deters smaller recyclers and quarry operators. Payback stretches beyond 3 years if throughput is seasonal or commodity prices dip. Rapid sensor obsolescence causes hesitation, as operators fear stranded assets when next-generation AI models arrive. To bridge the gap, vendors pilot equipment-as-a-service contracts that transform capex into opex, yet subscription fees may clash with cyclical cash flows. Development banks channel concessional loans to circular-economy projects, but uptake remains uneven, limiting the short-term penetration ceiling for the sensor-based sorting machine market.

Limited Sensor Performance on Moist or Dusty Feed Material

Moisture above 15% skews near-infrared readings, while airborne dust dulls optical clarity, forcing recalibration or shielding that disrupts uptime. Mines in equatorial regions grapple with humidity-induced detector drift, and composting facilities combat steam plumes that fog lenses. Though X-ray transmission tolerates challenging feeds, higher energy costs curb adoption outside high-value ore. Engineers add automated wipers and pressurized air curtains, but maintenance overhead escalates for small plants. As a result, operators either delay new purchases or overspecify protective enclosures, tempering growth momentum in certain geographies within the sensor-based sorting machine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Technology: AI Integration Drives Hyperspectral Growth

Hyperspectral imaging lines posted a 7.11% CAGR forecast, reflecting surging uptake in plastics, battery metals, and food applications where spectral fingerprints differentiate materials invisible to standard optics. X-ray transmission retained a 34.83% sensor-based sorting machine market share in 2024 thanks to durability in dense ore separation. Near-infrared systems stay dominant for polymer ID in post-consumer packaging streams, while RGB vision suits bulk commodity plants that prioritize speed over granularity.

Edge computing now compresses hyperspectral data into one-click classification rules, shrinking model training times and unlocking pharmaceutical use cases that demand API verification to parts-per-million precision. Laser-induced breakdown spectroscopy gains attention in scrap metals, identifying alloy composition within milliseconds. VTT’s real-time spectral-processing breakthrough positions hyperspectral to challenge X-ray lines in high-tonnage mines, hinting at further redistribution of sensor-based sorting machine market size between modalities. As multi-modal platforms combine X-ray, NIR, and hyperspectral arrays, suppliers tout 99.5% purity across mixed waste, raising the innovation bar for lagging competitors.

By Sorting Configuration: Robotics Challenge Belt Dominance

Belt-based machines secured 38.74% revenue in 2024 owing to proven reliability at more than 200 TPH, anchoring the high-capacity segment of the sensor-based sorting machine market. Robotic pick-and-place units, though slower in bulk terms, outpace peers at 7.33% CAGR because they flexibly target irregular items like lithium battery cells or electronics components. Free-fall chutes serve gravity-fed glass and aggregate lines, and drum sorters maintain niche relevance in mineral beneficiation where abrasive particles shorten belt life.

ABB’s AI-guided grippers exemplify convergence between industrial robotics and spectral imaging, reducing human contact with hazardous e-waste. Modular conveyors add plug-and-play sensor mounts to narrow the versatility gap with robots. Hybrid layouts place a vision-equipped robot at the end of a belt line to correct mis-ejections, blending throughput with selectivity. As aftermarket retrofits proliferate, incumbents defend installed bases by launching firmware upgrades that double detection points without mechanical overhaul, preserving share in the sensor-based sorting machine market.

By End-Use Industry: Recycling Plastics Surge Past Traditional Mining

Mining maintained 29.61% of 2024 revenues, yet resin reclaimers clock a 6.99% CAGR on the back of circular-economy legislation. Municipal solid waste streams deliver mixed polymers requiring sophisticated spectroscopy, and bottle-to-bottle mandates raise purity targets to 0.1% contaminant levels. Metal scrap yards invest steadily, especially for aluminum and copper delineation that protects smelter economics.

Food processors deploy optical sorters to comply with FDA foreign-material rules, while pharmaceutical firms adopt hyperspectral units for color-independent tablet authentication. Niche sectors such as nutraceuticals and seed grading underscore demand for compact, low-volume devices that fit constrained footprints. Industrial minerals players apply sensor-based ore upgrading to sidestep water-intensive flotation, advancing ESG goals. Consequently, the sensor-based sorting machine market size continues to diversify beyond its historic mining core, balancing cyclic commodity exposure with defensible regulatory-driven niches.

By Throughput Capacity: Small-Scale Operations Drive Growth

Systems above 200 TPH controlled 41.83% share in 2024, particularly in large mines and regional material recovery facilities. However, sub-50 TPH lines are projected to grow at 7.55% CAGR as distributed recycling hubs and specialty processors seek agile equipment that scales with feed availability. Medium-capacity solutions (50–200 TPH) cater to county-level waste plants balancing capex and redundancy.

Declining component costs let suppliers offer modular frames where operators stack identical lanes as volumes rise, lowering initial investment and smoothing cash-flow. AI-enabled predictive maintenance equalizes uptime across scales, mitigating the perception that small machines are inherently less robust. Financiers now bundle micro-loans with performance guarantees, catalyzing penetration of the sensor-based sorting machine industry in emerging regions where processing volumes remain modest.

Geography Analysis

North America held 38.74% market share in 2024, underpinned by stringent landfill diversion rules, mature curbside collection infrastructure, and a robust mining sector that values high-capacity equipment. The U.S. further tightens PFAS and microplastic limits in food-grade packaging, stimulating new polymer sorting projects. Canada’s potash and copper producers deploy X-ray systems to maximize recovery rates from lower-grade ore, while Mexico’s automotive supply chain opts for mid-capacity lines to manage metal scrap generated in stamping operations. Wage inflation sustains interest in automation, and federal subsidies targeting domestic recycling capacity buttress the sensor-based sorting machine market.

Asia-Pacific is forecast to grow at 7.66% CAGR through 2030, driven by China’s ban on imported low-grade recyclables and the rollout of local feedstock processing projects. India’s national clean-city initiative unlocks municipal investment in optical sorters to replace manual picking, and Japan combats labour shortages with AI-enabled vision lines. South Korea’s electronics sector pioneers robotic pickers that recover high-value circuit boards from shredding lines. Southeast Asian economies invest in plastic reprocessing hubs to capture export opportunities, collectively propelling the regional sensor-based sorting machine market.

Europe commands steady demand on the strength of the EU Circular Economy Action Plan, which mandates 65% recycling of municipal waste by 2030 and imposes extended producer responsibility fees on packaging. Germany leads Industry 4.0 retrofits, incorporating cloud-linked analytics across legacy belt sorters, and France extends eco-modulation fees, incentivizing high-purity outputs. Italy’s large agri-food sector upgrades optical lines to comply with stricter shell-fragment thresholds, while post-Brexit Britain adapts sourcing strategies yet retains alignment with EU purity metrics. Compliance-driven replacements rather than capacity expansions dominate spending, reflecting the mature nature of the sensor-based sorting machine market in Europe.

Competitive Landscape

The market exhibits moderate concentration: the top five vendors collectively control near-60% of global revenues, balancing technology moats with healthy challenger activity. TOMRA, Bühler, and Steinert differentiate through proprietary AI libraries and scalable service contracts that guarantee uptime. Each invests in modular frames compatible with software upgrades, locking in customers via digital ecosystems rather than hardware alone.

Emerging players focus on hyperspectral analytics, cloud-native dashboards, and subscription pricing, challenging equipment-centric incumbents. Patent race intensity is evident, with WIPO reporting triple-digit growth in filings related to AI-driven material recognition. Strategic alliances between sensor specialists and robot manufacturers accelerate time-to-market for integrated cells that merge detection and manipulation, further evolving the competitive structure of the sensor-based sorting machine market.

Geographically, localized assembly hubs mitigate tariff exposure and shorten lead times. Steinert’s Singapore NIR center caters to Asian customization requests, while Key Technology’s U.S. plant emphasizes quick-turn modifications for produce sorters. Vendor consolidation through M&A, such as Sesotec’s Safeline purchase, signals a pivot toward regulated niches such as pharmaceuticals, where certification hurdles defend margins. Collectively, these moves illustrate a shift from commodity machinery sales to lifecycle-value platforms anchored in data and domain expertise.

Sensor-Based Sorting Machine Industry Leaders

TOMRA Systems ASA

Bühler AG

Steinert GmbH

Sesotec GmbH

Key Technology LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: TOMRA Systems launched GAINnext, an AI platform that autonomously adjusts ore-sorting parameters in real time to boost copper and lithium recovery.

- September 2024: Bühler partnered with Microsoft to integrate Azure AI services, aiming for 25% downtime reduction through cloud-based predictive maintenance.

- August 2024: Sesotec acquired Safeline for USD 45 million, widening its pharmaceutical contamination-detection portfolio.

- July 2024: Steinert opened a USD 12 million NIR competence center in Singapore to localize support for APAC recyclers.

Global Sensor-Based Sorting Machine Market Report Scope

| X-ray Transmission (XRT) |

| Near-Infrared (NIR) |

| Color / Optical RGB Cameras |

| Laser-Induced Breakdown Spectroscopy (LIBS) |

| Induction/EM Sensors |

| Hyperspectral Imaging |

| Belt Sorters |

| Free-Fall / Chute Sorters |

| Conveyor-Based Sorters |

| Drum Sorters |

| Robotic Pick-and-Place Sorters |

| Mining and Minerals |

| Recycling – Metals |

| Recycling – Plastics |

| Recycling – Paper |

| Food Processing |

| Waste Management (MSW) |

| Pharmaceuticals and Nutraceuticals |

| Agriculture (Grains and Seeds) |

| Industrial Minerals |

| Low Capacity (below 50 TPH) |

| Medium Capacity (50-200 TPH) |

| High Capacity (above 200 TPH) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Sensor Technology | X-ray Transmission (XRT) | ||

| Near-Infrared (NIR) | |||

| Color / Optical RGB Cameras | |||

| Laser-Induced Breakdown Spectroscopy (LIBS) | |||

| Induction/EM Sensors | |||

| Hyperspectral Imaging | |||

| By Sorting Configuration / System Type | Belt Sorters | ||

| Free-Fall / Chute Sorters | |||

| Conveyor-Based Sorters | |||

| Drum Sorters | |||

| Robotic Pick-and-Place Sorters | |||

| By End-Use Industry | Mining and Minerals | ||

| Recycling – Metals | |||

| Recycling – Plastics | |||

| Recycling – Paper | |||

| Food Processing | |||

| Waste Management (MSW) | |||

| Pharmaceuticals and Nutraceuticals | |||

| Agriculture (Grains and Seeds) | |||

| Industrial Minerals | |||

| By Throughput Capacity | Low Capacity (below 50 TPH) | ||

| Medium Capacity (50-200 TPH) | |||

| High Capacity (above 200 TPH) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the global value of the sensor-based sorting machine market in 2025?

The market stands at USD 1.52 billion in 2025, with a forecast to reach USD 2.10 billion by 2030.

Which sensor technology is growing fastest?

Hyperspectral imaging is projected to expand at a 7.11% CAGR through 2030 as AI models unlock new identification use cases.

Why are robotics gaining share in sorting configurations?

Labor shortages, safety regulations, and demand for flexible handling of irregular items drive a 7.33% CAGR for robotic pick-and-place systems.

Which region offers the highest growth potential?

Asia-Pacific leads with a 7.66% CAGR, propelled by regulatory tightening, infrastructure investment, and Industry 4.0 adoption.

How do high capital costs impact smaller operators?

Up-front investments of USD 500,000–2 million extend payback to 3–5 years, prompting SMEs to explore leasing or equipment-as-a-service models.

Page last updated on: