Sensor Based Smart Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

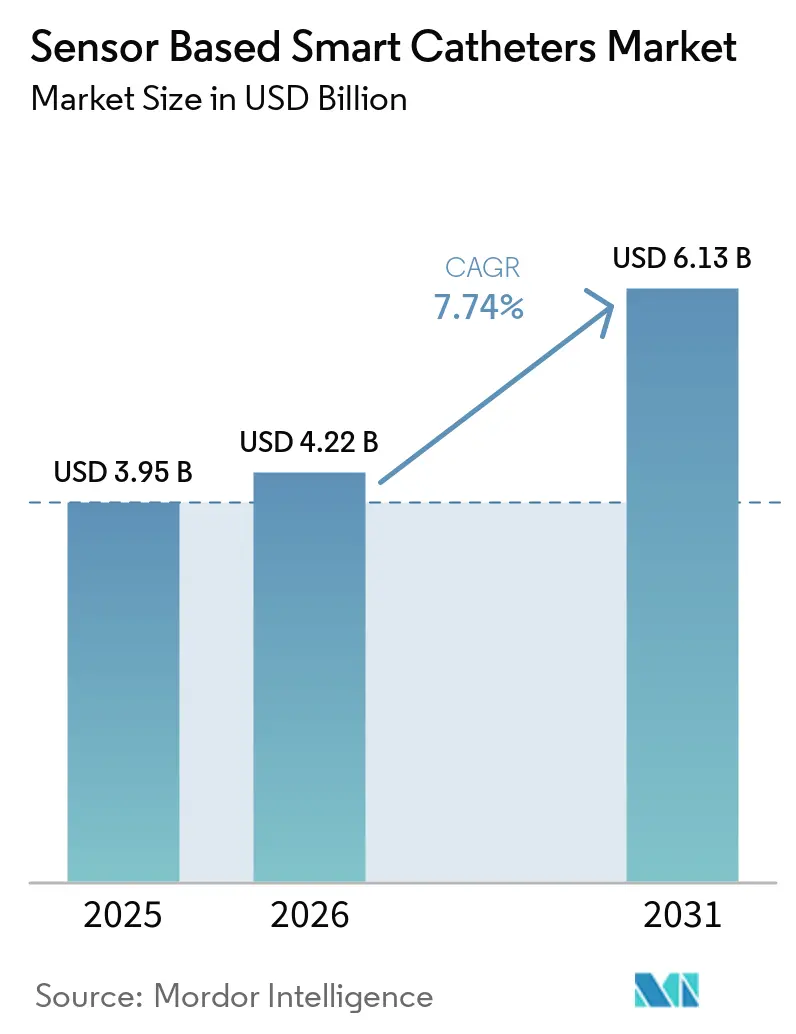

| Market Size (2026) | USD 4.22 Billion |

| Market Size (2031) | USD 6.13 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensor Based Smart Catheters Market Analysis by Mordor Intelligence

The Sensor Based Smart Catheters Market size is expected to increase from USD 3.95 billion in 2025 to USD 4.22 billion in 2026 and reach USD 6.13 billion by 2031, growing at a CAGR of 7.74% over 2026-2031.

The growth outlook reflects a steady transition toward precision-guided procedures that rely on real-time hemodynamic feedback, contact-force awareness, and intravascular imaging to improve outcomes and procedural efficiency. Clinical evidence continues to validate this direction, with focal pulsed field ablation using contact-force catheters showing one-year freedom from atrial arrhythmia, and IVUS-guided PCI demonstrating lower target vessel failure in complex lesions compared with angiography alone. Product ecosystems that integrate mapping, ablation, and imaging are becoming a competitive anchor as they help reduce setup time and improve lesion delivery confidence. Regulatory signals such as Breakthrough Device designations for dual-energy systems and guideline upgrades for intravascular imaging further reinforce adoption in higher-acuity settings. The sensor based smart catheters market also benefits from technology advances that compress procedure times, reduce radiation, and align with outpatient workflows where feasible.

Key Report Takeaways

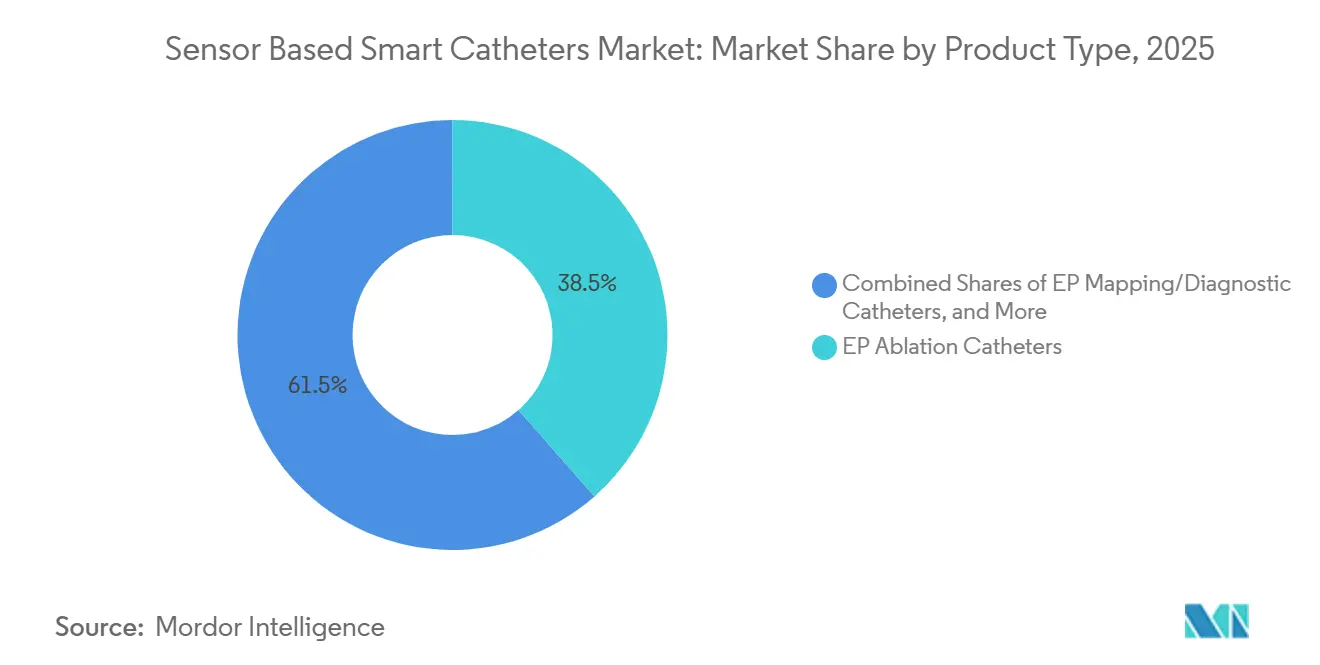

- By product type, electrophysiology ablation catheters led with 38.52% revenue share in 2025 and are projected to grow at an 11.52% CAGR through 2031.

- By sensor modality, ultrasound captured 40.50% in 2025 and contact-force sensors are forecast to grow at 12.23% CAGR to 2031.

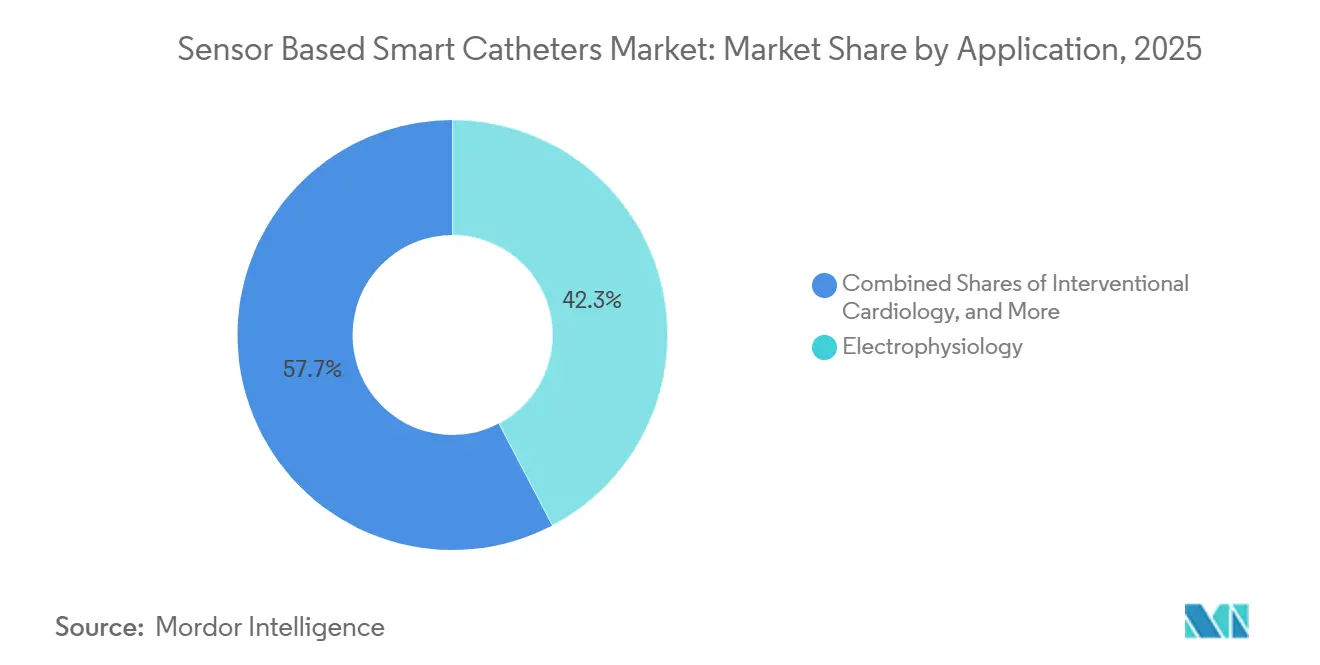

- By application, electrophysiology accounted for a 42.31% share in 2025 and is set to advance at an 11.42% CAGR over 2026-2031.

- By end user, hospitals held 67.50% in 2025 while ambulatory surgical centers are projected to record a 10.98% CAGR through 2031.

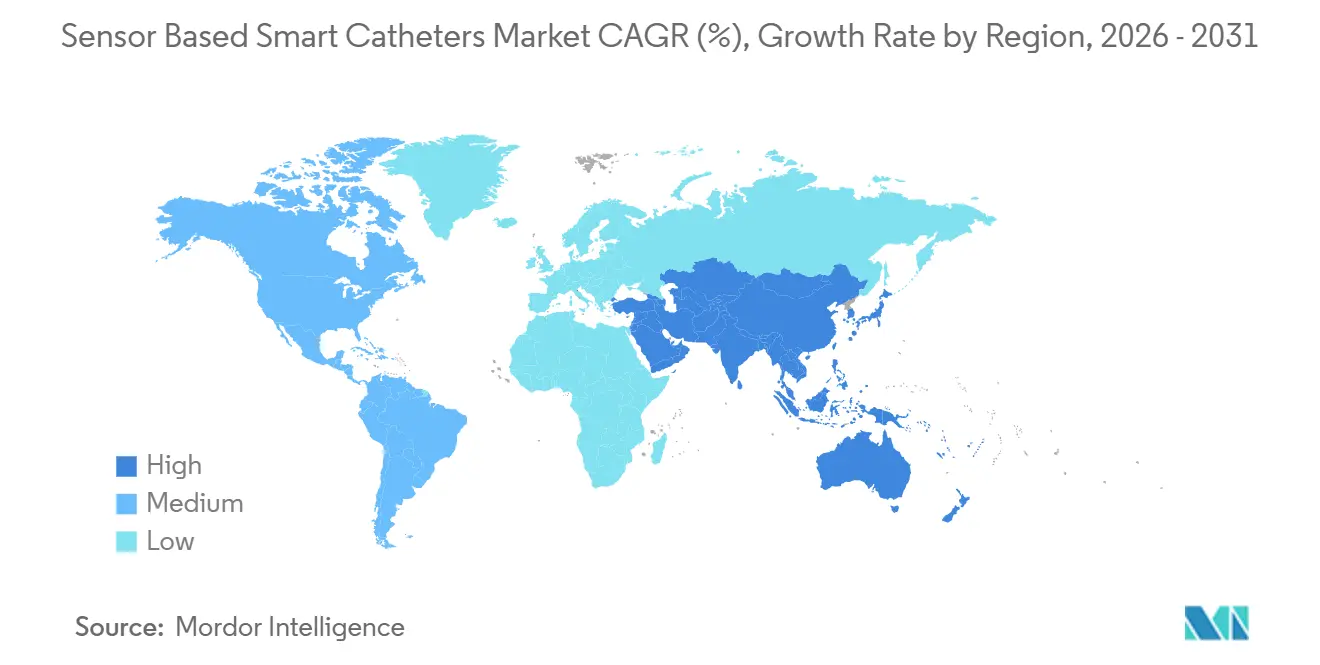

- By geography, North America contributed 41.80% in 2025 and Asia-Pacific is on track to deliver a 10.34% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sensor Based Smart Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EP ablation adoption and AF burden accelerate uptake of force-sensing and high-density mapping catheters | +2.8% | Global, spill-over to APAC via local EP lab expansion | Medium term (2-4 years) |

| IVUS/OCT-guided PCI improves outcomes, driving intravascular imaging catheter adoption | +1.9% | North America & EU core, early gains in China, Japan | Medium term (2-4 years) |

| Hospitals' shift to minimally invasive, image-guided procedures sustains demand for sensor-enabled catheters | +1.4% | Global | Long term (≥ 4 years) |

| MR-guided electrophysiology unlocks radiation-free workflows for sensor-enabled diagnostic and ablation catheters | +0.9% | North America & EU regulatory pilots, niche APAC adoption | Long term (≥ 4 years) |

| Consensus and reimbursement momentum for IVUS in peripheral interventions expands use beyond coronaries | +1.1% | North America & EU core, MEA spill-over in select vascular centers | Medium term (2-4 years) |

| ICE guidance reduces radiation/anesthesia, expanding sensor-enabled catheter use | +1.3% | Global, with early concentration in high-volume structural-heart hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EP Ablation Adoption and AF Burden Accelerate Uptake of Force-Sensing and High-Density Mapping Catheters

The rising global prevalence of atrial fibrillation is increasing the demand for new diagnoses, reinforcing the need for scalable interventional strategies that reduce recurrence and downstream healthcare utilization. The 2025 European Heart Rhythm Association[2]Wolfram Doehner et al., “Atrial fibrillation burden in clinical practice, research, and technology development,” Europace, vbn.aau.dk consensus standardized AF burden as the proportion of time in atrial fibrillation, which supported a care pathway that prioritizes earlier rhythm control and, when suitable, catheter ablation. Burden-based treatment logic is further supported by data showing that patients who maintain very low residual burden after ablation require fewer follow-up interventions, which improves care continuity and capacity management for high-volume centers. Force-sensing ablation catheters such as TactiFlex illustrate how device design contributes to procedural efficiency by improving stability during lesion delivery and supporting higher-power, shorter-duration workflows for pulmonary vein isolation. In parallel, focal pulsed field ablation with contact-force catheters delivered 80.2% one-year freedom from atrial arrhythmia and a favorable safety profile in the ECLIPSE AF study, which helped validate contact-awareness in energy delivery. Regulatory momentum, including Breakthrough Device designations for dual-energy systems, points to accelerated evidence generation and potential speed-to-approval advantages in priority indications.

IVUS/OCT-Guided PCI Improves Outcomes, Driving Intravascular Imaging Catheter Adoption

In complex bifurcation lesions, IVUS-guided PCI reduced target vessel failure by 60% versus angiography-alone guidance in the DKCRUSH VIII trial, with the effect concentrated among patients who achieved optimal IVUS criteria. In a separate meta-analysis of randomized trials for complex lesions, OCT guidance reduced major adverse cardiovascular events, cardiac death, myocardial infarction, and stent thrombosis compared with angiography-only protocols, reframing the clinical question from whether to image to which modality to use. Guideline bodies in Europe and North America elevated intravascular imaging to top-tier recommendations for complex anatomy, reinforcing a standard-of-care trajectory for IVUS and OCT in higher-risk subsets. Hybrid IVUS-OCT platforms can alleviate modality trade-offs by combining deep penetration with high resolution, with early clinical work showing improved visualization performance for certain stent assessments. Industry consolidation is coalescing around integrated imaging and physiology ecosystems, as seen in acquisitions that combine anatomy, plaque composition, and functional indices within single workflows.

MR-Guided Electrophysiology Unlocks Radiation-Free Workflows for Sensor-Enabled Diagnostic and Ablation Catheters

In November 2025, a first ischemic ventricular tachycardia ablation under real-time MRI guidance with a trans-septal approach demonstrated feasibility for MR-guided lesion delivery and chamber access, a key milestone for radiation-free electrophysiology. The platform advanced in early 2026 with clearances that position real-time MR navigation and compatible diagnostic catheters for U.S. commercialization, enabling direct scar visualization and lesion assessment in workflows that historically relied on fluoroscopy. Experimental evidence indicates that MRI can map ablation lesions with strong correspondence to electroanatomic annotations, which supports a model where imaging confirms lesion patterns within short time frames after delivery. The approach also offers an alternative pathway for patients who are poor candidates for higher-radiation procedures, which broadens clinical access where fluoroscopy may be restrictive. Infrastructure outlays for MR-compatible labs and associated device costs remain considerable, and training requirements span both electrophysiology and imaging expertise. Early reimbursement frameworks are still forming in most markets, so activity remains concentrated in academic pilots and early adopter centers.

ICE Guidance Reduces Radiation/Anesthesia, Expanding Sensor-Enabled Catheter Use

Intracardiac echocardiography has expanded from an adjunctive role to routine use in structural heart and electrophysiology procedures, in part because it reduces or avoids general anesthesia dependencies and lowers fluoroscopy exposure. A multicenter evaluation of a 3D ICE catheter reported high technical and clinical success, strong imaging acceptability compared with transesophageal echocardiography or 2D ICE, and favorable workflow characteristics in a range of interventional procedures[1]Mohamad Adnan Alkhouli et al., “Multicenter Experience With a Novel Real-Time 3D ICE Catheter,” Journal of the American Heart Association, ahajournals.org. Recent software advances now transform ICE images into procedural maps with automated anatomical labeling, integrating with established mapping systems and both 2D and 4D ICE probes to streamline setup and interpretation. These integrations support common electrophysiology workflows such as AF or VT ablation and facilitate concomitant tasks through real-time chamber modeling. Early first-in-human studies for newer ICE catheters have reported acceptable safety and image quality compared with incumbent devices, with operators describing a manageable learning curve as proficiency builds. As more centers adopt ICE-driven navigation and guidance, the sensor based smart catheters market gains use cases where radiation minimization and streamlined discharge pathways are core goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device/procedure costs and specialized training needs slow broader adoption | -1.6% | Global, acute in cost-sensitive APAC and MEA markets | Short term (≤ 2 years) |

| Evidence gaps and standardization needs (e.g., IVUS sizing, local impedance metrics) hinder uniform uptake | -0.9% | Global, particularly EU MDR jurisdictions and emerging Asian economies | Medium term (2-4 years) |

| Regulatory timelines and MDR complexity elongate approvals for novel sensor catheters | -1.2% | EU core; EMA centralized reviews span 6 months to >2 years | Medium term (2-4 years) |

| Specialist and lab capacity constraints limit procedure throughput and adoption | -0.8% | Global; acute in rural North America, UK, and developing APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device/Procedure Costs and Specialized Training Needs Slow Broader Adoption

Advanced ablation, imaging, and hemodynamic platforms often require significant upfront capital and specialized consumables, which slows uptake in price-sensitive health systems where budget cycles are tight. For many providers, limited reimbursements and competing capital priorities compress the pace of replacement and refresh decisions, which delays the migration to newer sensor-enabled catheters. Multi-modality ecosystems can reduce procedure time and standardize lesion delivery, but they require new training to achieve repeatable performance across case types and staff experience levels. Training curves for complex mapping, PFA, and integrated imaging workflows can be steep, which places pressure on staffing and case scheduling until competency stabilizes. This dynamic is more pronounced at facilities that lack experienced preceptors and formalized proctoring programs. As a result, the sensor based smart catheters market sometimes sees staggered adoption where early uptake concentrates at reference centers before spreading to community settings.

Evidence Gaps and Standardization Needs (e.g., IVUS Sizing, Local Impedance Metrics) Hinder Uniform Uptake

A multi-society review of EU device regulation experience highlighted that randomized evidence remains limited for a large share of high-risk devices at the time of CE-marking, which complicates uniform adoption of newer platforms. In peripheral interventions, operators still face ambiguity on IVUS-derived vessel sizing thresholds for stent selection, which creates variability in clinical practice and limits consistent guideline-grade pathways outside coronaries. Retrospective analyses associate IVUS use with improved limb outcomes in Medicare populations, but prospective randomized data remain scarce and cost-effectiveness conclusions are sensitive to modeling assumptions. In atrial fibrillation workflows, contact-force sensing can improve acute safety by lowering excessive force during linear ablation, yet durable lesion formation on late gadolinium enhancement MRI did not consistently improve at one year in a randomized trial, underscoring a gap between acute markers and chronic lesion permanence. The sensor based smart catheters market therefore contends with the need for standardized indices that correlate with durable outcomes, which will help align procedural targets across imaging, impedance, and electrogram cues. Greater harmonization and more prospective datasets should reduce practice variability and encourage payers to support expanded use in well-defined indications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fleets Propel EP Ablation Catheter Uptake

EP ablation catheters captured 38.52% sensor based smart catheters market share in 2025 and are poised to expand at 11.52% CAGR over 2026-2031, positioning the category as both current leader and fastest grower. The traction reflects the rising global burden of AF, growing preference for earlier rhythm control and ablation, and the maturation of dual-energy systems that give operators flexibility near sensitive structures while maintaining durable isolation. Abbott’s TactiFlex Duo earned a CE Mark in early 2026 with trial evidence showing one-year freedom from rhythm recurrence in paroxysmal AF[3]Abbott, “TactiFlex Duo Breakthrough Device Designation,” Company Media Room, abbott.mediaroom.com, which highlights how contact-force awareness and dual-energy delivery can work together in streamlined protocols. Single-shot and all-in-one PFA concepts are also progressing, as exemplified by systems that combine mapping and therapy in a single platform to reduce catheter exchanges and shorten case times[4]Medtronic, “Sphere-360 PFA Catheter CE Mark and U.S. IDE First Cases,” Company Press Release via PR Newswire, prnewswire.com. Mapping and diagnostic catheters remain foundational for substrate characterization and for confirming gap closure after ablation, with high-density arrays improving efficiency in large chambers. Intravascular imaging catheters used in interventional cardiology benefit from guideline endorsements in complex coronary anatomies, while peripheral applications gain momentum as clinical data accumulate on stent optimization and patency outcomes.

The sensor based smart catheters market also sees expanding use of ICE catheters, supported by multicenter evidence for 3D imaging that enables high technical success and acceptable image quality compared with transesophageal echocardiography. Hemodynamic and oximetry catheters deliver value in ICU and operating room settings through continuous monitoring, predictive analytics, and decision support that help mitigate hypotension and support fluid management. Temperature-sensing catheters maintain relevance for perioperative care pathways and targeted temperature management protocols, although growth remains more measured than in higher-acuity electrophysiology and coronary imaging lines. Across product types, platform ecosystems that knit together mapping, imaging, and therapy are differentiating on speed, reproducibility, and ease of use in both inpatient and outpatient venues. The net result is a favorable backdrop for systems that compress procedure time and reduce radiation exposure while maintaining or improving safety outcomes in core indications.

By Sensor Modality: Contact Force Sensors Surge as Ablation Workflows Automate

Ultrasound modalities, including IVUS and ICE, commanded 40.50% of revenue in 2025, while contact-force sensors are forecast to post the fastest growth at 12.23% CAGR, as electrophysiology teams intensify their focus on real-time lesion-quality feedback and first-pass isolation. The sensor based smart catheters market size increasingly concentrates on modality combinations that allow operators to balance resolution, penetration, and contact assurance within standardized workflows that translate across lab teams. Fiber-optic force sensing has become a leading approach for stable contact and for consistent lesion indices under high-power, short-duration strategies, which favor durable outcomes with fewer energy deliveries. Clinical experience with focal PFA has shown encouraging one-year arrhythmia freedom and high acute isolation rates in contact-aware workflows, which supports faster adoption of force-sensing designs in electrophysiology. Regulatory momentum in China for pressure-sensing PFA catheters affirmed demand for sensor-fusion platforms in large domestic markets that prioritize safety near vulnerable structures. The sensor based smart catheters market continues to see innovation in physiologic sensing as well, with multimodal systems transitioning between noninvasive and invasive monitoring to sustain continuous hemodynamic visibility without additional disposables.

Optical OCT sensing offers very high resolution, which contributes to precise stent expansion and apposition assessments in complex anatomy when contrast and image acquisition conditions are favorable. Spectroscopy combined with IVUS or DeepOCT helps characterize lipid-rich plaques and may inform treatment strategy through plaque composition insights, a direction reinforced by acquisitions that combine imaging and AI-driven physiologic indices. Temperature sensing remains embedded in pulmonary artery catheters and selected urology catheters for perioperative management and targeted temperature control in critical-care pathways. As the sensor based smart catheters industry refines data capture and processing, the value shifts toward integrated measures that correlate with durable lesion creation, optimal stent deployment, and hemodynamic stability, which gives multi-sensor fusion a clear role in next-generation designs. These contrasts between contact, imaging, and physiologic sensing are likely to narrow as platforms interoperate more tightly across mapping, therapy, and monitoring.

By Application: Electrophysiology Procedures Command Lead and Growth

Electrophysiology accounted for 42.31% of revenue in 2025 and is projected to expand at an 11.42% CAGR between 2026 and 2031, extending its lead through continuous adoption of ablation-first pathways in suitable AF cohorts. Randomized and prospective experiences with pulsed field ablation continue to report strong one-year rhythm outcomes, low collateral injury, and growing evidence on burden reduction, which together encourage physicians to accelerate conversion from RF-only strategies. Sub-analysis of post-ablation AF burden shows that very low residual burden correlates with fewer clinical interventions, supporting continuous rhythm monitoring as a sensitive tool for post-procedural management. The sensor based smart catheters market also benefits from ICE-enabled mapping and AI-assisted anatomical labeling that streamline set-up and increase operator confidence in chamber reconstructions. As focal and single-shot PFA ecosystems mature, dual-energy systems are becoming central to complex anatomies where operators weigh lesion depth and safety needs in real time. These shifts favor sites with strong procedural volumes and standardized post-ablation monitoring protocols.

Interventional cardiology remains a large application with guideline-backed expansion of intravascular imaging in complex lesions, where randomized and pooled analyses show outcome advantages for IVUS and OCT guidance compared with angiography alone. Structural heart procedures rely on fusion imaging and real-time guidance, with FDA-cleared solutions that assist in device tracking and placement while maintaining visualization fidelity. Critical-care hemodynamics continues to use pulmonary artery catheters, arterial-line sensors, and analytics suites that inform anesthesia and ICU decision-making. Urology maintains steady demand for temperature-sensing catheters in perioperative care, and specialty niches in neurovascular and GI manometry represent targeted use cases where reimbursement and evidence depth continue to evolve. Collectively, these clinical domains reinforce a broad base for the sensor based smart catheters market as platforms emphasize precision, safety, and throughput.

By End User: ASCs Ascend as CMS Greenlights EP Ablations

Hospitals accounted for 67.50% of revenue in 2025, reflecting their dominant position in high-acuity structural heart and complex electrophysiology procedures and their installed base of EP and cath lab infrastructure. Ambulatory surgical centers are projected to grow at 10.98% CAGR through 2031, helped by procedure standardization, expanding technology familiarity, and physician preference for settings that combine flexibility with consistent equipment access. As mapping and ablation platforms consolidate steps and reduce exchanges, outpatient feasibility improves for selected arrhythmia cases that meet safety and follow-up criteria. ICE-enabled workflows can facilitate same-day pathways in appropriate patients, since imaging and navigation occur without transesophageal dependencies in many scenarios. Specialty clinics and dedicated EP labs operate as throughput-oriented environments that coordinate schedules and standardize protocols, which supports replication across multiple operators. The sensor based smart catheters market is therefore positioned to add incremental volume across outpatient-capable procedures while hospitals retain complex cases that require surgical backup or higher resource intensity.

Geography Analysis

North America held 41.80% of revenue in 2025, supported by higher healthcare spending, a dense EP and cath lab footprint, and rapid activation of new technologies that pass regulatory review. The region’s adoption is further reinforced by Class I recommendations for intravascular imaging in complex coronary anatomy, which codifies higher-standard practice pathways in acute and elective cases. Evidence in coronary bifurcations and complex lesions, including randomized and pooled analyses, continues to validate the clinical value of IVUS and OCT guidance compared with angiography-only protocols. Regulatory designations such as Breakthrough status and clearances for novel systems further accelerate market entry for dual-energy ablation platforms and AI-enabled imaging suites, which benefits technology diffusion in early-adopter centers. Access and capacity vary by locality, so the sensor based smart catheters market grows fastest where training, reimbursement clarity, and equipment readiness align.

Europe is the second-largest region, benefiting from Class IA recommendations for IVUS and OCT in complex lesions and macro-level support for image-guided procedures across leading health systems. Manufacturers continue to bring forward sensor-enabled mapping and ablation systems and to expand integrated imaging platforms despite longer and more complex regulatory processes under EU. A cross-society review indicated that randomized evidence levels remain uneven across high-risk devices at the time of CE-marking, which raises the bar for post-market evidence generation to sustain broad adoption. Training pipeline constraints and procedure backlogs can cap growth in some markets, so consistent mentorship and proctoring programs are helpful to extend access outside tertiary hubs. Select Middle Eastern countries prioritize medical infrastructure build-outs and technology importation for tertiary-care centers, which supports uptake of ICE, ablation, and intravascular imaging in referral networks that serve regional demand. Elsewhere in the wider region, variations in reimbursement readiness and localized expertise shape the speed of adoption without changing the underlying demand curve for precision-guided interventions.

Asia-Pacific is projected to be the fastest-growing region at 10.34% CAGR between 2026 and 2031, driven by rising cardiovascular disease prevalence, urbanization-linked risk factors, and policy emphasis on expanding advanced cardiac care. Regulatory progress is notable, with approval of the first pressure-sensing PFA catheter in China that reflects receptivity to sensor-fusion platforms and localized manufacturing scale-up. Clinical leadership in complex bifurcation PCI, including multi-center randomized work, strengthens the case for intravascular imaging in large Asian health systems. Japan remains a bellwether for coronary imaging practices and training culture, while Australia and South Korea maintain infrastructure and standards comparable to Western Europe. In South America, leading centers adopt contact-force ablation and ICE within private networks, while public-sector pathways evolve with growing AF prevalence that supports interventional capacity investments over time. These dynamics together set a supportive context for the sensor based smart catheters market as regional ecosystems align training, reimbursement, and supply chains.

Competitive Landscape

The sensor-based smart catheters market shows moderate-to-high consolidation, with integrated portfolios that span ablation, mapping, imaging, and hemodynamics. Product ecosystems create switching costs through workflow familiarity, integrated software, and disposables standardization, which helps incumbents sustain share across inpatient and outpatient settings. Dual-energy ablation systems, high-density mapping arrays, and ICE-enabled anatomy reconstruction are core differentiators because they compress case times and support reproducible lesion sets across operators. In coronary imaging, integrated anatomy and physiology platforms are a focus area for feature expansion, which strengthens competitive positioning in complex PCI workflows.

Emerging players have targeted pricing, local manufacturing, and sensor fusion to accelerate competitive entry in large markets, as seen with pressure-sensing PFA catheters approved for use in China. In MR-guided electrophysiology, recent clearances position a specialist platform as an early mover in radiation-free ablation, although infrastructure and reimbursement constraints concentrate near-term activity in academic centers. The hemodynamic monitoring space remains anchored by continuous monitoring suites that provide predictive analytics tied to anesthesia and critical-care objectives, with noninvasive-to-invasive interoperability emerging in arterial-line interfaces. Overall, the sensor based smart catheters market is shaped by systems that boost throughput, minimize radiation, and standardize outcomes across diverse operator experience levels.

Sensor Based Smart Catheters Industry Leaders

Johnson & Johnson

Abbott

Boston Scientific Corporation

Koninklijke Philips N.V.

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Abbott received CE Mark approval for the TactiFlex Duo Ablation Catheter, Sensor Enabled, a dual-energy device delivering both radiofrequency and pulsed field ablation energy, supported by FOCALFLEX trial data showing 81% one-year freedom from documented rhythm recurrence in paroxysmal AF patients.

- January 2026: Medtronic announced CE Mark approval in Europe and completion of first U.S. IDE cases for the Sphere-360 PFA catheter, the first all-in-one mapping and single-shot pulsed field ablation catheter for paroxysmal atrial fibrillation.

Global Sensor Based Smart Catheters Market Report Scope

The sensor based smart catheters market refers to the global market for advanced catheter systems embedded with one or more sensing technologies that enable real‑time measurement, visualization, and feedback of physiological parameters such as force, pressure, impedance, temperature, flow, and imaging signals during diagnostic and therapeutic procedures, with the objective of improving procedural accuracy, safety, clinical outcomes, and workflow efficiency across cardiovascular, critical care, and urology applications.

The sensor based smart catheters market is segmented by product type into EP ablation catheters, EP mapping and diagnostic catheters, intravascular imaging catheters, intracardiac echocardiography catheters, hemodynamic and oximetry catheters, temperature‑sensing urinary and intravascular temperature‑management catheters, and other related products; by sensor modality including contact force, local impedance, pressure and fractional flow reserve with oximetry, ultrasound, optical, spectroscopy, temperature, and other sensing technologies; by application covering electrophysiology, interventional cardiology, structural heart procedures, critical care hemodynamics, urology, and other uses; by end user comprising hospitals, ambulatory surgical centers, specialty clinics, and cardiac catheterization and electrophysiology laboratories. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| EP Ablation Catheters |

| EP Mapping/Diagnostic Catheters |

| Intravascular Imaging Catheters |

| Intracardiac Echocardiography (ICE) Catheters |

| Hemodynamic & Oximetry Catheters |

| Temperature-sensing Urinary & Intravascular Temp-management Catheters |

| Others (Image-guided Atherectomy Catheters, etc) |

| Contact Force |

| Local impedance |

| Pressure/FFR and oximetry (SvO2/ScvO2) |

| Ultrasound (IVUS/ICE) |

| Optical (OCT) |

| Spectroscopy (NIRS/combined IVUS+NIRS) |

| Temperature |

| Others (Electromagnetic (EM), Flow sensors, etc) |

| Electrophysiology |

| Interventional Cardiology |

| Structural Heart |

| Critical Care Hemodynamics (ICU/OR) |

| Urology |

| Others (Neurovascular and GI manometry niches) |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty clinics |

| Cardiac Cath and Electrophysiology (EP) Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | EP Ablation Catheters | |

| EP Mapping/Diagnostic Catheters | ||

| Intravascular Imaging Catheters | ||

| Intracardiac Echocardiography (ICE) Catheters | ||

| Hemodynamic & Oximetry Catheters | ||

| Temperature-sensing Urinary & Intravascular Temp-management Catheters | ||

| Others (Image-guided Atherectomy Catheters, etc) | ||

| By Sensor Modality | Contact Force | |

| Local impedance | ||

| Pressure/FFR and oximetry (SvO2/ScvO2) | ||

| Ultrasound (IVUS/ICE) | ||

| Optical (OCT) | ||

| Spectroscopy (NIRS/combined IVUS+NIRS) | ||

| Temperature | ||

| Others (Electromagnetic (EM), Flow sensors, etc) | ||

| By Application | Electrophysiology | |

| Interventional Cardiology | ||

| Structural Heart | ||

| Critical Care Hemodynamics (ICU/OR) | ||

| Urology | ||

| Others (Neurovascular and GI manometry niches) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty clinics | ||

| Cardiac Cath and Electrophysiology (EP) Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the sensor based smart catheters market growth outlook to 2031?

The sensor based smart catheters market size is forecast to reach USD 6.13 billion by 2031 at a 7.74% CAGR over 2026-2031, extending a steady shift toward precision-guided workflows.

Which applications currently lead adoption in the sensor based smart catheters market?

Electrophysiology leads with 42.31% of 2025 revenue and is projected to grow at 11.42% CAGR through 2031 on earlier ablation pathways and improving safety profiles in newer energy modalities.

Which product categories are growing fastest in the sensor based smart catheters market?

EP ablation catheters both lead and grow fastest with 38.52% share in 2025 and an 11.52% projected CAGR through 2031, supported by dual-energy designs and high-density mapping.

What sensor modalities are gaining traction in the sensor based smart catheters market?

Ultrasound modalities held 40.50% in 2025, while contact-force sensors are the fastest growing at 12.23% CAGR through 2031 as teams standardize on real-time lesion-quality feedback.

Which region is poised to grow fastest in the sensor based smart catheters market?

Asia-Pacific is projected to expand at a 10.34% CAGR over 2026-2031 on rising cardiovascular disease prevalence, regulatory momentum, and increasing capacity in advanced cardiac care.

Page last updated on: