Self-Adhesive Waterproof Wallpaper Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 4.86 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Adhesive Waterproof Wallpaper Market Analysis by Mordor Intelligence

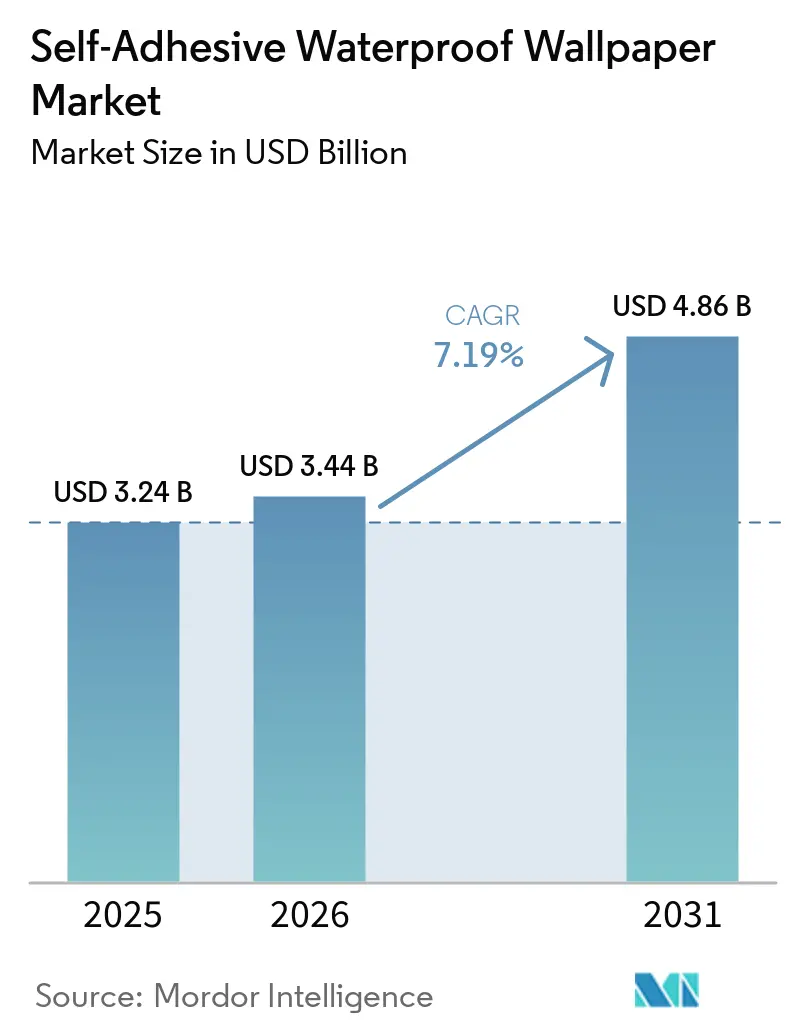

The self-adhesive waterproof wallpaper market is expected to grow from USD 3.24 billion in 2025 to USD 3.44 billion in 2026 and is forecast to reach USD 4.86 billion by 2031 at a 7.19% CAGR over 2026–2031. Growth in the self-adhesive waterproof wallpaper market continues to rest on demand for simple interior upgrades that do not require wet trades, long downtime, or permanent wall changes. The category is also gaining wider acceptance, driven by decorative finishes in kitchens, bathrooms, rental units, serviced apartments, and light commercial spaces where fast turnaround matters. Compliance is becoming more important as low-emission adhesive systems and safer ink chemistry improve access to regulated institutional and premium residential channels, especially in Europe and North America[1]European Commission, “REACH Regulation (EC) No. 1907/2006,” European Commission, europa.eu. At the same time, digital printing is expanding design options and making small custom runs more practical, helping brands defend value in the self-adhesive waterproof wallpaper market against low-cost imports and private-label products. Competition remains broad rather than concentrated, with established wallpaper makers, regional specialists, and digital-first brands all using design refreshes, trade tools, and product claims to differentiate their offers in the self-adhesive waterproof wallpaper market.

Key Report Takeaways

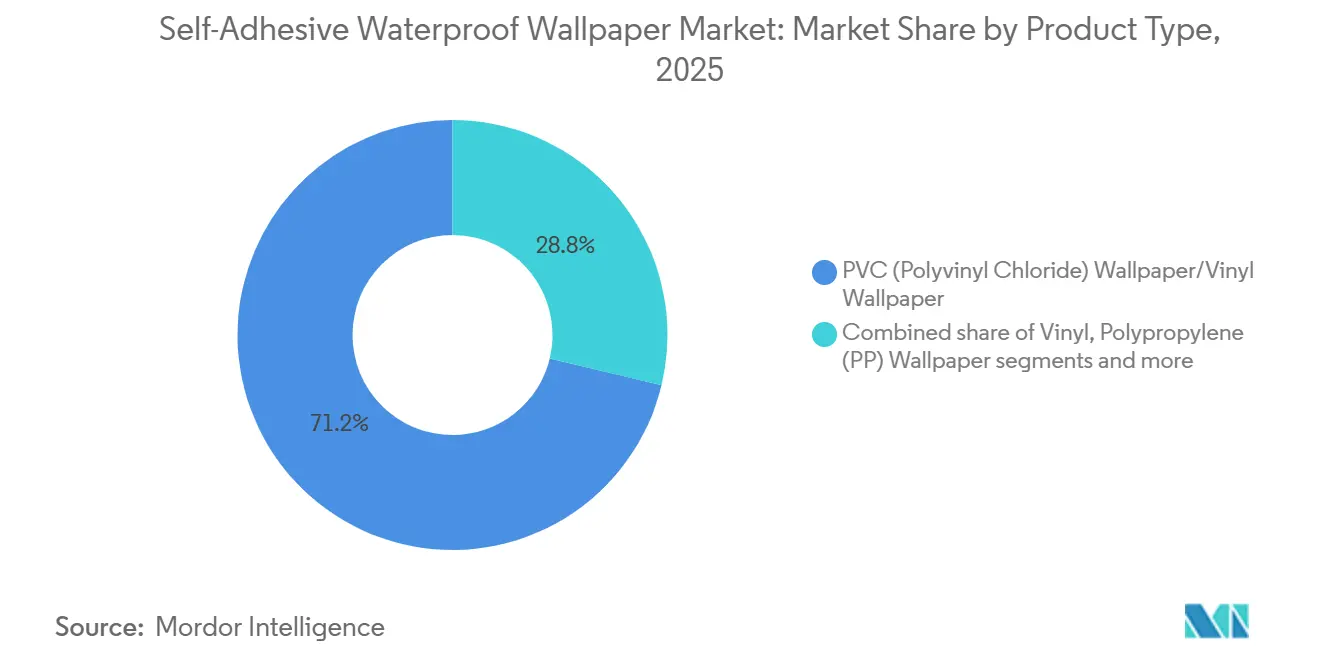

- By material type, PVC (Polyvinyl Chloride) wallpaper/vinyl wallpaper led with 71.24% of the self-adhesive waterproof wallpaper market share in 2025, while PET (Polyethylene Terephthalate) wallpaper is projected to expand at an 8.14% CAGR through 2031.

- By application, renovation and remodeling held 65.16% of the self-adhesive waterproof wallpaper market share in 2025, whereas new construction is forecast to grow at a 7.47% CAGR through 2031.

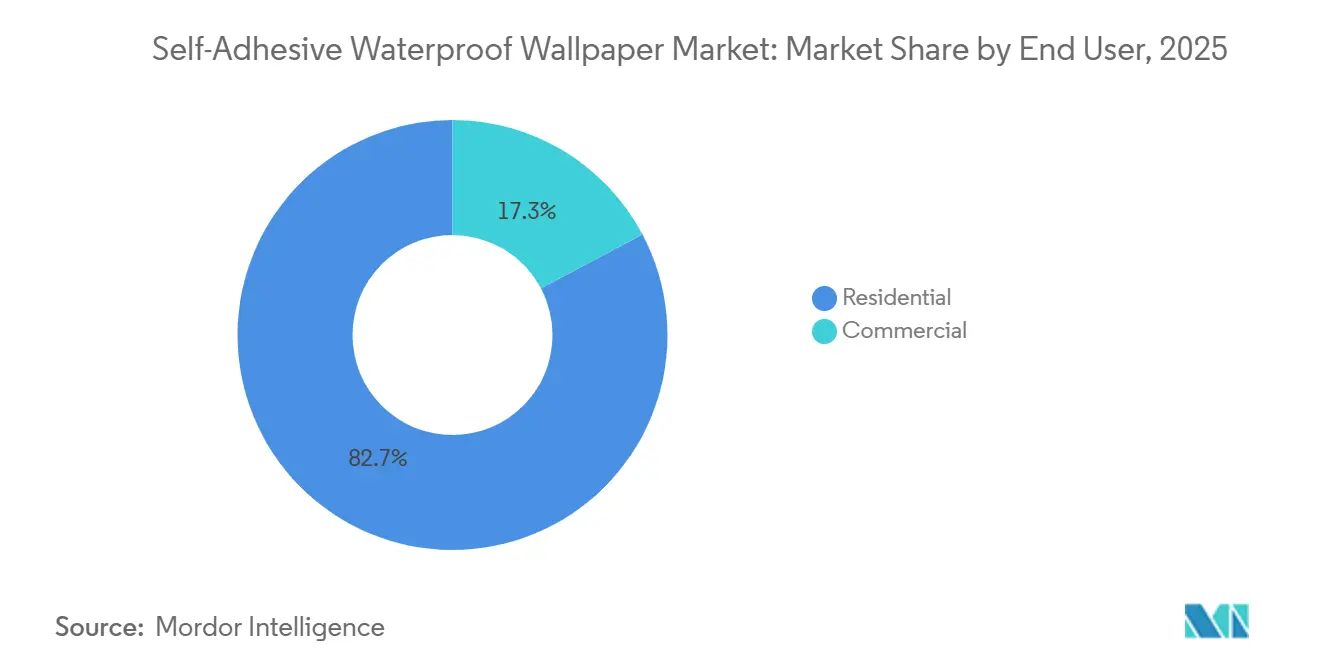

- By end user, residential held 82.74% of the self-adhesive waterproof wallpaper market share in 2025, whereas commercial is forecast to grow at an 8.35% CAGR through 2031.

- By distribution channel, B2C channels held 88.65% of the self-adhesive waterproof wallpaper market share in 2025, whereas B2B channels are forecast to grow at a 7.62% CAGR through 2031.

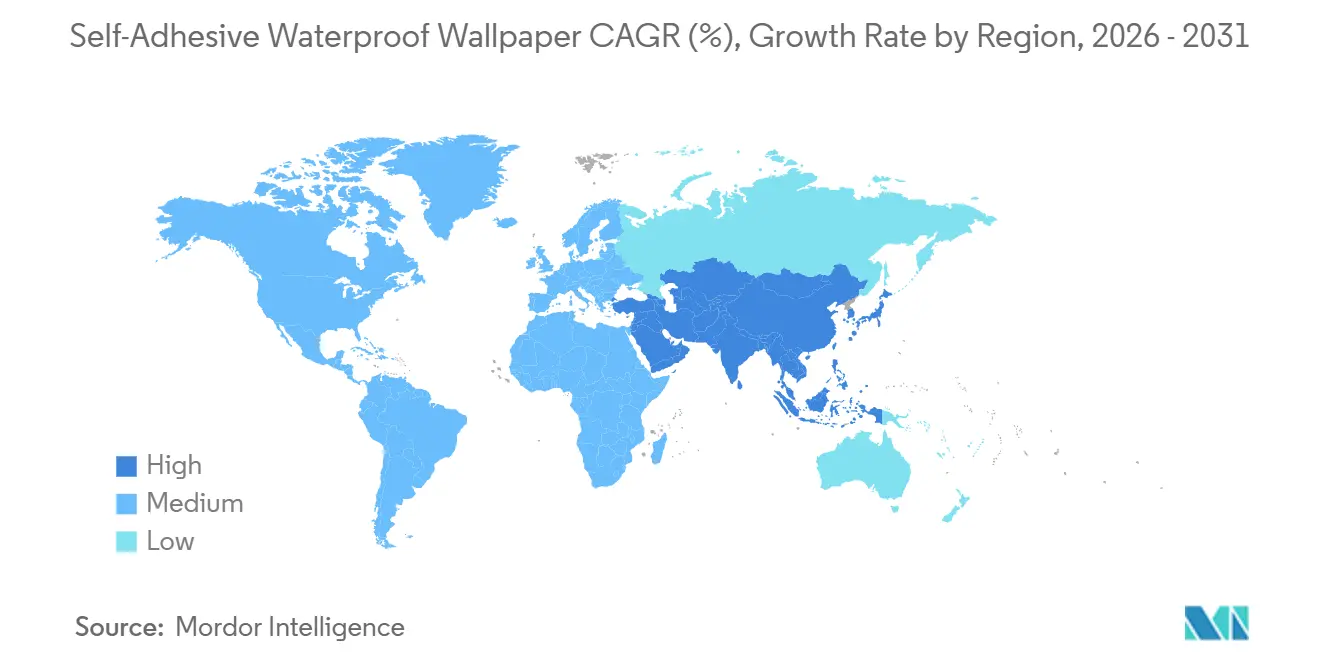

- By geography, Asia-Pacific held 40.31% of the self-adhesive waterproof wallpaper market share in 2025, and the region is also forecast to be the fastest-growing market at a 7.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Self-Adhesive Waterproof Wallpaper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DIY-Friendly Renovation Demand in Rental Housing | +1.60% | North America and Europe core, with spillover into urban Asia-Pacific markets | Long term (≥ 4 years) |

| Moisture-Resistant Decorative Finishes for Kitchens and Bathrooms | +1.40% | Global, with strong relevance in Europe and North America | Medium term (2-4 years) |

| Social Commerce and Interior Inspiration Content | +0.90% | Global, with stronger conversion in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Low-VOC Repositionable Adhesives in Regulated Markets | +0.70% | Europe, North America, and Australia | Medium term (2-4 years) |

| Digital Print Customization for Short-Run Designs | +0.60% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| Hygienic Washable Surfaces in Hospitality and Healthcare Refits | +0.50% | Global, with visible pull in the Middle East, Africa, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DIY-Friendly Renovation Demand in Rental Housing

Demand in the self-adhesive waterproof wallpaper market remains closely tied to spaces where occupants want visual change without drilling, tiling, or permanent surface treatment. Rental housing keeps this need visible because lease restrictions and deposit concerns make reversible decoration more practical than paste wallpaper or many other finish types. The same logic extends to furnished apartments and short-stay properties where owners need a fresh look without long installation cycles. This makes the self-adhesive waterproof wallpaper market less dependent on large renovation budgets and more closely tied to frequent, low-disruption refreshes. Products that remove cleanly, reposition easily, and cover dated surfaces well are likely to stay central to demand as consumers continue to favor flexible home improvement formats.

Moisture-Resistant Decorative Finishes for Kitchens and Bathrooms

Kitchens and bathrooms are among the highest-traffic, highest-humidity areas in any dwelling, yet decorative wall coverings have historically underserved them. The growing availability of PVC- and PET-backed self-adhesive formats with verified moisture-resistance is beginning to change that equation. Wall&decèo's patented AQUABOUT WET SYSTEM™, deployed in more than 24,000 showers across 81 countries, demonstrates that technical waterproofing credentials can drive commercial-grade adoption of wallpaper in direct-water-contact zones that were previously exclusive to tile[2]Wall&decò, “AQUABOUT WET SYSTEM Waterproof Wallcovering,” Wall&decò, wallanddeco.com . This matters because it expands the number of surfaces that can be treated with a fast, design-led product rather than a labor-heavy finish. It also raises confidence around backsplash-style and accent-wall use cases, where visual effect and easier installation both matter. As more consumers and specifiers accept wallpaper in moisture-prone rooms, the self-adhesive waterproof wallpaper market gains broader surface opportunities in each project.

Low-VOC Repositionable Adhesives in Regulated Markets

The self-adhesive waterproof wallpaper market is also benefiting from tighter expectations around indoor emissions and chemical safety. European chemical rules and formaldehyde-related restrictions are pushing buyers toward products that can document cleaner adhesive and material performance, especially in institutional and premium channels. Brands that already use certified low-emission components are better placed to meet these requirements and avoid procurement barriers. Spoonflower’s use of GREENGUARD Gold-certified inks shows how compliance-related claims can support commercial credibility beyond design appeal[3]Spoonflower, “Welcome to Spoonflower, The Print-on-Demand Difference,” Spoonflower Help Center, spoonflower.com . Over time, this should help the self-adhesive waterproof wallpaper market shift part of its value mix toward higher-grade products rather than purely price-led offerings.

Digital Print Customization for Short-Run Designs

Digital print technology is improving how the self-adhesive waterproof wallpaper market handles customization, design turnover, and smaller production runs. Roland DG noted in 2025 that only a small share of wallpaper printing had shifted to digital systems, suggesting a large remaining runway for change[4]Roland DG Corporation, “Roland DG Adds New Materials and Paints to DIMENSE Interior Decoration Solution,” Roland DG, rolanddga.com. This matters because short-run economics improve when brands can print more designs in lower volumes without the same inventory burden. It also supports faster response to color trends, mural requests, and room-specific graphics that are difficult to serve with older production models. In the self-adhesive waterproof wallpaper market, companies that match digital printing with dependable waterproof substrates are likely to hold a stronger position in higher-value custom and replacement demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Installation Failure Risk In Humid or Poorly Prepared Surfaces | -0.50% | Global, with stronger exposure in humid climates and older housing stock | Medium term (2-4 years) |

| Price Compression from Commodity Imports and Private Labels | -0.60% | Global, strongest in North America and European mass retail | Long term (≥ 4 years) |

| Limited Recyclability of Multi-Layer Film Structures | -0.40% | Europe and North America, where sustainability rules are advancing faster | Long term (≥ 4 years) |

| Substitution From Paint Panels And Tile-Look Films | -0.50% | Global, especially in DIY and contractor-led renovation channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Compression from Commodity Imports and Private Labels

Pricing pressure remains one of the clearest restraints on the self-adhesive waterproof wallpaper market. Large-scale producers and retailer-owned lines can mirror popular looks at lower price points, which narrows margins for mid-tier branded suppliers. A.S. Création reported weaker sales in 2025 and directly linked part of the pressure to difficult consumer conditions and stronger competition in its core European markets. That kind of pressure makes design depth, licensed collections, digital flexibility, and verified product performance more important than ever. Without clearer differentiation, brands in the self-adhesive waterproof wallpaper market can be drawn into a competition driven mainly by discounting.

Limited Recyclability of Multi-Layer Film Structures

End-of-life handling remains a structural challenge for the self-adhesive waterproof wallpaper market because many products rely on layered constructions that are harder to recycle than simpler mono-material formats. Sustainability discussions around plastics continue to favor materials and systems that fit more easily into existing recovery streams. This does not remove demand for waterproof vinyl-based products, but it does increase scrutiny from institutional buyers and regulated regions. Suppliers that can improve material traceability, lower-emission chemistry, or more recyclable constructions should face less resistance in formal specifications. The issue is unlikely to disappear quickly, so it remains a longer-term constraint on how the self-adhesive waterproof wallpaper market evolves by material mix.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: PVC Holds Scale While PET Gains on Sustainability Positioning

PVC wallpaper or vinyl wallpaper held 71.24% of the self-adhesive, waterproof wallpaper market share in 2025, reflecting its strong fit with moisture resistance, print clarity, texture replication, and repositionable adhesive systems. In practical terms, vinyl remains the mainstream base for peel-and-stick décor because it can imitate tile, stone, fabric, and patterned surfaces at a lower installation cost. Foam-based wallpaper continues to serve feature walls that need depth and a softer visual profile, while polypropylene and fabric-based waterproof products stay more selective in their use. Composite and multi-layer constructions remain relevant where better dimensional stability or cleaner stripping performance matters in residential and light commercial settings.

PET wallpaper is projected to grow at an 8.14% CAGR through 2031, which makes it the fastest-growing material type in the self-adhesive waterproof wallpaper market. A key reason is that PET aligns better with recycling discussions than many multi-layer vinyl structures. This factor is becoming more relevant as buyers pay closer attention to sustainability claims. Even within PVC, suppliers are starting to respond to procurement expectations, as evidenced by Sangetsu’s launch of Japan’s first FSC-certified PVC wallpaper in 2025. That move suggests the leading material in the self-adhesive waterproof wallpaper market is adapting rather than standing still. Over the forecast period, the balance is likely to remain in favor of PVC for scale, while PET gains faster in projects where sustainability screening carries more weight.

By Application: Renovation Provides the Base While New Construction Builds Momentum

Renovation and remodeling accounted for 65.16% of the self-adhesive waterproof wallpaper market in 2025, making it the category's core application base. That position is logical because existing homes, rentals, and hospitality spaces often need a visual refresh without invasive work, extended room shutdown, or skilled installation. The product also fits short replacement cycles well because style updates can be made more often than with many traditional wall finishes. In mature housing markets, this gives the self-adhesive waterproof wallpaper market a steady stream of repeat use tied to aesthetic refresh rather than full structural renovation.

New construction is forecast to expand at a 7.47% CAGR through 2031, indicating the category is moving beyond its original renovation-led identity. Developers are paying more attention to finishes that install faster, reduce labor dependency, and still provide visible differentiation in apartment interiors and shared spaces. Digital printing supports this shift because room-specific graphics and coordinated design packages can be supplied in smaller runs without the same setup burden as older production systems. The result is a wider role for the self-adhesive waterproof wallpaper market in entry-level and mid-tier developments where cost control and visual impact both matter. This application should remain smaller than renovation in absolute scale, but it is becoming a more important source of forward growth.

By End User: Residential Leads Volume While Commercial Adds Higher-Momentum Demand

Residential end users accounted for 82.74% of 2025 demand, confirming that the self-adhesive waterproof wallpaper market remains mainly consumer-led in volume terms. Households use the product because it allows quick room updates, low-disruption installation, and easier replacement when tastes change. It also works well in kitchens, accent walls, children’s rooms, and smaller wet-adjacent areas where people want a visible result without a full build-out. This broad household relevance keeps residential demand central to the self-adhesive waterproof wallpaper market even as new commercial uses expand.

Commercial demand is projected to grow at an 8.35% CAGR through 2031, making it the fastest-growing end-user category. Hospitality, healthcare, and flexible office settings value surfaces that refresh easily, wipe clean, and reduce labor intensity during fit-outs or refurbishments. Grandeco’s Pure & Protect wallpaper illustrates how functional claims, such as antimicrobial performance, can help wallpaper move into more specification-driven environments. At the same time, cleaner chemistry and documented emissions performance improve suitability for institutional procurement in regulated markets. This means the self-adhesive waterproof wallpaper market is slowly shifting from a purely consumer décor category to a broader set of wall-finish solutions.

By Distribution Channel: B2C Delivers Scale While B2B Improves Channel Quality

B2C channels accounted for 88.65% of revenue in 2025, keeping them firmly in the lead across the self-adhesive waterproof wallpaper market. Hypermarkets, specialty décor stores, home centers, brand websites, online marketplaces, and local retailers remain the main route because the product is easy to ship and easy to demonstrate visually. That visual quality matters because consumers often buy based on patterns, colors, room inspiration, and before-and-after presentations rather than deep technical specifications. As a result, the self-adhesive waterproof wallpaper market continues to benefit from retail formats that combine design discovery with quick purchase decisions.

B2B channels are forecast to grow at 7.62% through 2031, suggesting a gradual improvement in channel depth rather than immediate channel dominance. Contractors, interior designers, architects, and project procurement teams become more relevant when the product moves into hotels, clinics, care settings, and developer-led interior packages. Trade buyers also value precision tools, made-to-measure capabilities, faster sample handling, and product documentation that reduces approval time. That is why several brands are building tools and catalogs specifically for professional users rather than relying only on consumer storefronts. Over time, the self-adhesive waterproof wallpaper market should see B2B capture a larger share of value, even as B2C retains most of the unit volume.

Geography Analysis

Asia-Pacific held 40.31% of the global self-adhesive waterproof wallpaper market share in 2025 and simultaneously leads the growth ranking with a projected 7.84% CAGR through 2031, giving the region both scale and momentum. China remains central because it combines great domestic demand with a strong manufacturing base for coated films, printing, and wallcovering exports. India, Southeast Asia, Japan, and South Korea add to regional demand through a mix of residential build-out, urban apartment living, and hospitality refurbishment. Sangetsu’s ongoing catalog expansion shows how major regional suppliers continue to refresh both residential and non-residential offers in response to changing specification needs. Asia-Pacific’s cost position also affects pricing in the wider self-adhesive waterproof wallpaper market, as export-oriented supply from the region influences pricing across the entry and mid-tier price bands globally.

North America and Europe form the next major demand block and remain important for value realization, brand building, and product compliance. In North America, demand is supported by interior refresh activity, rental housing use cases, and acceptance of reversible decorative solutions for kitchens, bathrooms, and multipurpose living spaces. Europe remains important because design-driven demand is paired with tighter material scrutiny, especially where indoor emissions and product safety are part of procurement review. That makes the self-adhesive waterproof wallpaper market in these regions more selective, but it also allows compliant and better-documented products to defend premium positioning. European suppliers, therefore, compete not only on pattern libraries and retailer access but also on chemistry, sustainability messaging, and digital production readiness.

South America, the Middle East, and Africa remain smaller in current scale, but all three regions matter for the future expansion of the self-adhesive waterproof wallpaper market. In South America, renovation-led demand is rising as urban households continue to invest in lower-disruption interior improvement. In the Middle East, hospitality construction, serviced living formats, and frequent room refresh cycles create a practical opening for washable, quick-install wall finishes. Parts of Africa remain at an earlier stage, and modern retail penetration still shapes how quickly branded peel-and-stick formats can scale. These regions are unlikely to lead global volume in the near term, but they provide useful growth pockets for suppliers that can balance design appeal with project-oriented selling.

Competitive Landscape

The self-adhesive waterproof wallpaper market remains moderately fragmented, with no single company controlling the category across all regions, price tiers, and channels. European groups such as A.S. Création, Rasch, and Grandeco compete with broad pattern libraries, established retailer relationships, and production scale. Grandeco’s broader Wallfashion platform shows how consolidation and portfolio expansion remain active levers, especially when companies want to cover both wallpaper and adjacent wall system formats. In Asia-Pacific, Sangetsu continues to anchor the upper competitive tier through its catalog breadth and a model that supports rapid product refreshes across residential and non-residential interiors. This spread of suppliers keeps the self-adhesive waterproof wallpaper market competitive without structurally concentrating it.

A.S. Création’s continuing Create 2030 strategy is one clear example of how legacy suppliers are responding. The company is pushing further into digital printing, e-commerce, and higher-margin design collections while navigating soft demand and stronger pricing pressure in Europe. Sangetsu provides another example through its catalog cycle and adjacent wall solutions, which support closer engagement with non-residential specification and project business. Tempaper illustrates a different route, using design collaborations and award-backed branded collections to maintain premium consumer attention in a crowded field. Together, these moves show that the self-adhesive waterproof wallpaper market rewards both operational capability and brand-led design relevance.

Digital-native players such as Tempaper, WallPops, Spoonflower, and Chasing Paper continue to shape the United States side of the self-adhesive, waterproof wallpaper market through social-first demand capture and rapid design rotation. Spoonflower’s print-on-demand model adds another layer of differentiation by supporting low minimums and a wide design tail, while also carrying recognized indoor air quality credentials for its inks. Technical standards are also becoming a stronger filter, as antimicrobial claims, emissions compliance, and digital throughput increasingly matter alongside style. Companies that can combine documented performance with design agility are likely to hold a stronger position than firms that compete only on low price. That balance should keep the self-adhesive waterproof wallpaper market active, design-led, and fragmented over the forecast period.

Self-Adhesive Waterproof Wallpaper Industry Leaders

A.S. Création Tapeten AG

Asian Paints Limited

Brewster Home Fashions LLC

Chasing Paper, LLC

F. Schumacher and Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Tempaper & Co. announced the launch of its new Back-to-School Collection, which will be available exclusively at Target stores and on Target.com from June 14 through September 19, 2026.

- December 2025: WallPops® launched the Brownstone Boys × WallPops Wallpaper Collection, comprising 11 peel-and-stick wallpaper designs across 5 patterns inspired by New York City's architectural heritage. The collection is available directly through wallpops.com.

Global Self-Adhesive Waterproof Wallpaper Market Report Scope

Self-adhesive waterproof wallpaper is a pressure-sensitive decorative wall covering built for tool-free installation and clean removal from suitable painted surfaces. Unlike paste-applied wallpaper, these products use a repositionable adhesive backing that allows users to install, adjust, and remove panels with minimal surface disruption, making them relevant for rental housing, hospitality refreshes, light commercial interiors, and DIY renovation. The self-adhesive waterproof wallpaper industry in this report is segmented by material type, application, end user, distribution channel, and geography. Material coverage includes PVC or vinyl wallpaper, PET wallpaper, polypropylene wallpaper, fabric-based waterproof wallpaper, foam-based wallpaper, and composite or multi-layer wallpaper. Application coverage includes new construction, renovation, and remodeling. End-user coverage includes residential and commercial demand. Distribution includes B2C routes such as home centers, specialty stores, online retail, and local shops, and B2B routes such as contractors, designers, architects, project procurement, and institutional sales. Geographic coverage includes North America, South America, Europe, Asia-Pacific, and the Middle East and Africa, with market value presented in USD across the covered segments.

| PVC (Polyvinyl Chloride) Wallpaper/Vinyl Wallpaper |

| Vinyl Wallpaper |

| PET (Polyethylene Terephthalate) Wallpaper |

| Polypropylene (PP) Wallpaper |

| Fabric-Based Waterproof Wallpaper |

| Foam-Based Wallpaper |

| Composite / Multi-Layer Wallpaper |

| New Construction |

| Renovation and Remodeling |

| Residential |

| Commercial |

| B2C Channels | Hypermarkets and Supermarkets |

| Specialty Stores | |

| Home Centers | |

| Online | |

| Local Shops | |

| Other Distribution Channels | |

| B2B Channels (Contractors and Installers, Interior Designers and Architects, Project Procurement and Institutional Sales) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Material Type | PVC (Polyvinyl Chloride) Wallpaper/Vinyl Wallpaper | |

| Vinyl Wallpaper | ||

| PET (Polyethylene Terephthalate) Wallpaper | ||

| Polypropylene (PP) Wallpaper | ||

| Fabric-Based Waterproof Wallpaper | ||

| Foam-Based Wallpaper | ||

| Composite / Multi-Layer Wallpaper | ||

| By Application | New Construction | |

| Renovation and Remodeling | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C Channels | Hypermarkets and Supermarkets |

| Specialty Stores | ||

| Home Centers | ||

| Online | ||

| Local Shops | ||

| Other Distribution Channels | ||

| B2B Channels (Contractors and Installers, Interior Designers and Architects, Project Procurement and Institutional Sales) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the projected value of self-adhesive waterproof wallpaper by 2031?

The self-adhesive waterproof wallpaper market is forecast to reach USD 4.86 billion by 2031, up from USD 3.44 billion in 2026, with a 7.19% CAGR.

Which material type currently leads demand?

PVC or vinyl wallpaper leads demand with a 71.24% share in 2025, due to its moisture resistance, high print quality, and broad design flexibility.

Which application is growing faster, renovation or new construction?

Renovation and remodeling remain larger, with a 65.16% share in 2025, while new construction is growing faster at a 7.47% CAGR through 2031.

Why is commercial demand increasing in this category?

Commercial demand is rising because hotels, healthcare sites, and workspaces value washable surfaces, lower installation disruption, and faster refresh cycles.

Which region is most important for future expansion?

Asia-Pacific is the most important region, accounting for 40.31% in 2025 and projected to post the fastest CAGR of 7.84% through 2031.

What is the biggest competitive challenge for suppliers?

The biggest challenge is price compression from low-cost imports and private-label products, which pushes brands to compete through design, compliance, and product performance rather than price alone.

Page last updated on: