Secure Multiparty Computation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

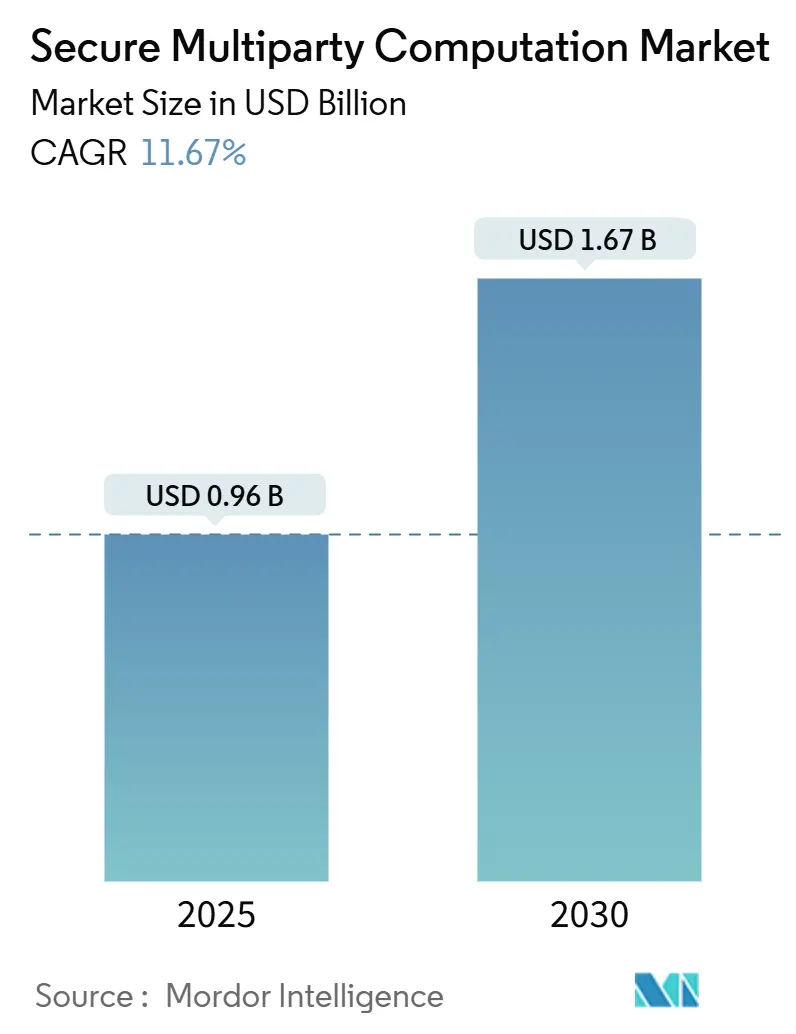

| Market Size (2025) | USD 0.96 Billion |

| Market Size (2030) | USD 1.67 Billion |

| Growth Rate (2025 - 2030) | 11.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Multiparty Computation Market Analysis by Mordor Intelligence

The secure multiparty computation market size is valued at USD 0.96 billion in 2025 and is projected to reach USD 1.67 billion by 2030, advancing at an 11.67% CAGR. Robust compliance mandates under the European Union’s Financial Data Access regulation, the Bank for International Settlements’ cross-border payments guidance, and similar rules in major jurisdictions set a structural foundation for privacy-preserving technologies. The increasing deployment of artificial-intelligence workloads that require multi-institutional training without data exposure boosts the secure multiparty computation market, while hardware accelerators, such as Intel Software Guard Extensions, lower latency barriers. Venture funding exceeding USD 300 million in 2024 underpins rapid product innovation, and blockchain-driven custody solutions create new protocol demand. Competition remains fragmented as specialized cryptography vendors refine their algorithms, integrate confidential computing hardware, and pursue vertical solutions.

Key Report Takeaways

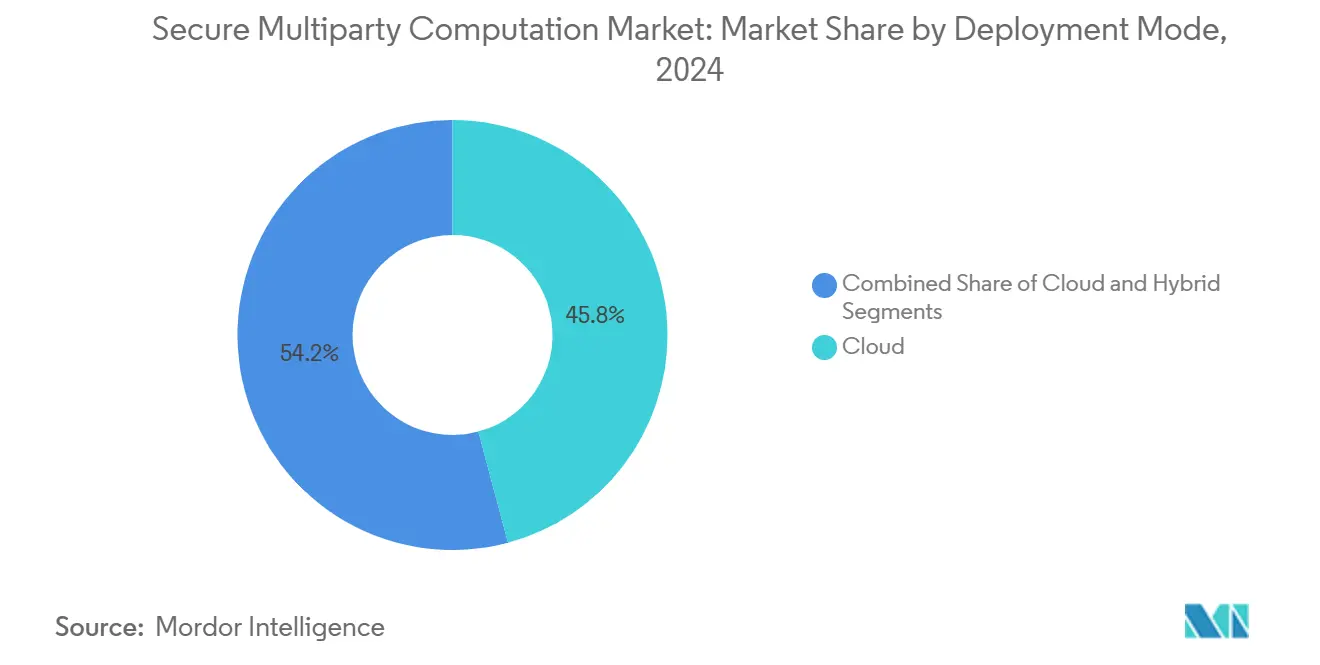

- By deployment mode, cloud captured 45.84% of the secure multiparty computation market share in 2024; hybrid architectures are forecast to expand at an 11.93% CAGR through 2030.

- By application, privacy-preserving analytics accounted for a 37.51% share of the secure multiparty computation market size in 2024, while secure AI and ML are projected to advance at a 12.57% CAGR through 2030.

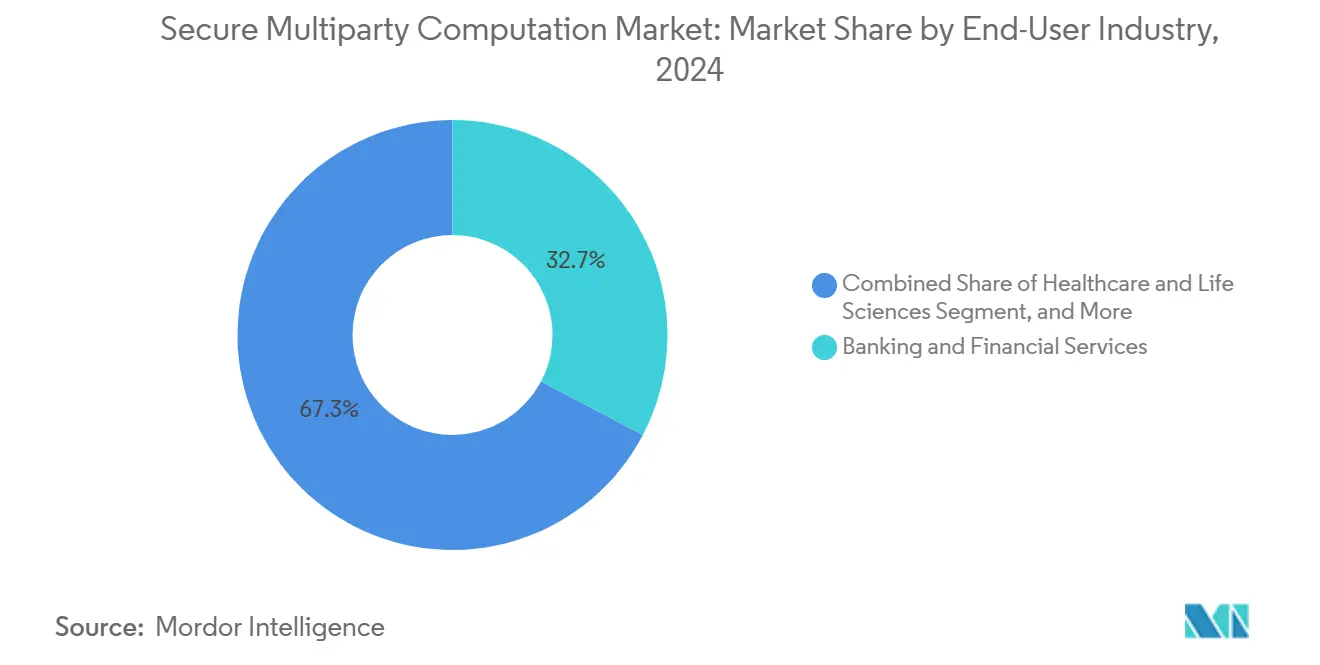

- By end-user industry, banking and financial services led with a 32.69% share of the secure multiparty computation market size in 2024; the healthcare and life sciences sector is projected to grow fastest at a 12.63% CAGR to 2030.

- By protocol type, secret-sharing maintained 45.91% of the secure multiparty computation market share in 2024, whereas zero-knowledge proofs are set to rise at a 12.51% CAGR through 2030.

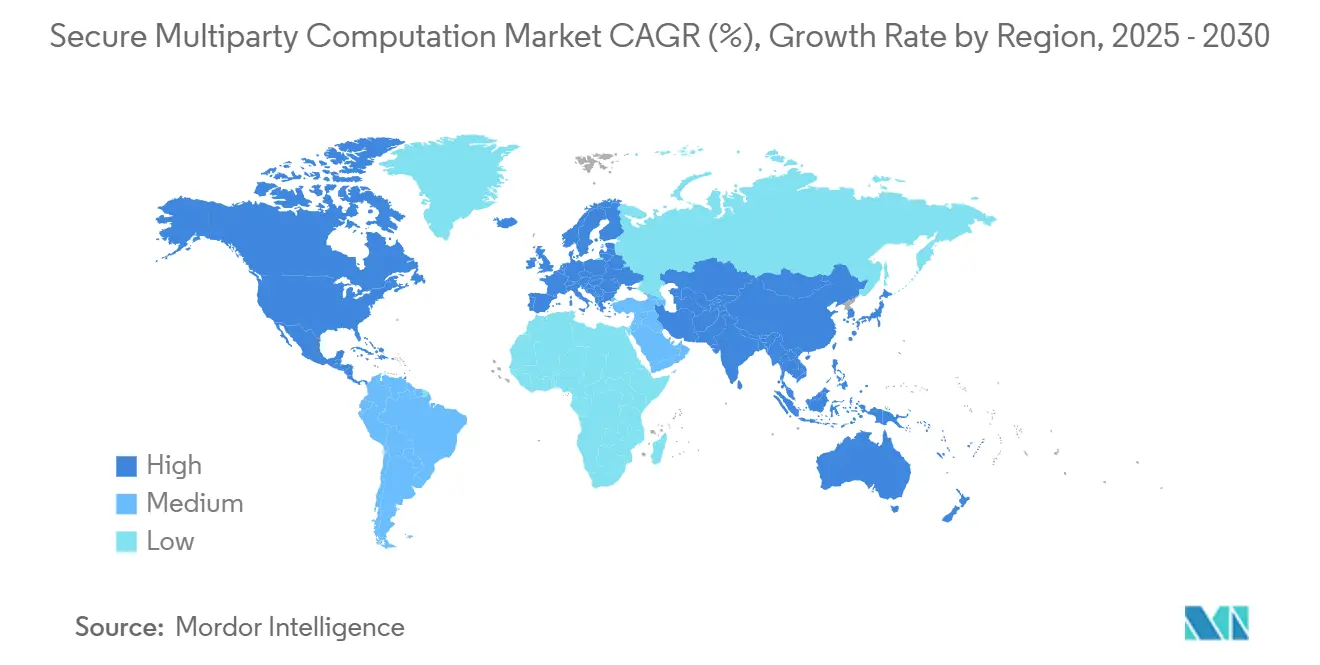

- By geography, North America held a 38.19% share of the secure multiparty computation market in 2024, and the Asia Pacific is poised to record a 12.44% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Secure Multiparty Computation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Regulatory Demand for Privacy-Preserving Data Collaboration | +3.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| Proliferation of AI and ML Workloads Requiring Secure Training | +2.8% | Global, concentrated in North America and Asia Pacific | Long term (≥ 4 years) |

| Surge in Cross-Border Data Sharing Across Financial Institutions | +2.4% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Integration of MPC with Confidential-Computing Hardware | +1.9% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Emergence of Blockchain-Based MPC Protocols for DeFi Custody | +1.1% | Global, with concentration in North America | Medium term (2-4 years) |

| Venture Capital Momentum in Cryptographic Startups | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Regulatory Demand for Privacy-Preserving Data Collaboration

Data-sharing mandates under the EU’s Financial Data Access regulation require banks to grant third-party analytics while protecting customer confidentiality, making MPC an attractive option for compliance teams.[1]European Banking Authority, “Guidelines on ICT and Security Risk Management,” eba.europa.eu Similar obligations arise from the Bank for International Settlements’ cross-border payment guidance, which highlights the use of privacy-preserving analytics for anti-money laundering monitoring. United States healthcare providers comply with HIPAA by shifting from data masking to cryptographic computation. Asia-Pacific regulators follow suit, embedding secure multiparty computation market requirements into emerging personal information protection statutes. As rules tighten, enterprises view MPC as essential infrastructure rather than an optional enhancement.

Proliferation of AI and ML Workloads Requiring Secure Training

Pharmaceutical firms run MPC-enabled federated learning to train drug-discovery models without exposing patient records.[2]Nature Biotechnology, “Privacy-Preserving Federated Learning for Drug Discovery,” nature.com Banks utilize secure machine-learning ensembles for consortium-level fraud detection, maintaining confidentiality while enhancing precision. Advances shrink computational overhead from 1000× to near 10× relative to plaintext, helping the secure multiparty computation market penetrate mainstream ML pipelines. Large-language-model developers adopt MPC to fine-tune proprietary datasets without compromising intellectual property. Together, these innovations create long-run demand across sectors.

Surge in Cross-Border Data Sharing Across Financial Institutions

Networks such as SWIFT deploy privacy-preserving screening that discovers sanctions-evading patterns without disclosing transaction fields.[3]SWIFT, “Sanctions Screening Solutions,” swift.com BIS wholesale-CBDC pilots rely on MPC to enable multi-central-bank settlement while preserving sovereignty. Trade-finance platforms utilize technology for supply-chain verification, thereby curbing fraud and enhancing trust among counterparties. Resulting network effects are reinforcing the expansion of the secure multiparty computation market in global finance hubs.

Integration of MPC with Confidential-Computing Hardware

Intel Software Guard Extensions v3.0 reduces MPC overhead by 40%, making real-time risk analytics within reach. AMD Secure Encrypted Virtualization strengthens cloud memory isolation, broadening deployment in regulated environments. Microsoft Azure combines hardware enclaves with turnkey MPC orchestration, letting enterprises use familiar cloud interfaces for privacy-preserving analytics. Hardware-software synergy differentiates vendors and accelerates adoption across corporate IT stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Computational Overhead Limiting Real-Time Applications | -1.8% | Global, particularly affecting latency-sensitive sectors | Long term (≥ 4 years) |

| Scarcity of Skilled Cryptographers and Developers | -1.2% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Fragmented and Evolving Global Privacy Regulations | -0.9% | Global, with complexity concentrated in cross-border operations | Medium term (2-4 years) |

| Limited Interoperability Among Different MPC Protocols | -0.7% | Global, particularly affecting multi-vendor enterprise deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Computational Overhead Limiting Real-Time Applications

Even optimized protocols can require 10-1000× more cycles than plaintext, impeding high-frequency trading, interactive web services, and edge analytics. Round-trip communication between parties further increases latency, and memory footprints scale poorly with the number of participants. While GPU acceleration, algorithmic pruning, and enclave support trim delays, fundamental cryptographic constraints keep fully real-time MPC out of reach for certain workloads. Enterprises must weigh the security benefits against the performance costs.

Scarcity of Skilled Cryptographers and Developers

Universities in North America and Europe graduated fewer than 500 PhD-level cryptographers in 2024. Enterprise demand outstrips supply, driving salary premiums of over 40% compared to standard software roles. Implementation projects often stall as firms retrain staff, elongating rollouts. Vendor-provided toolkits and low-code interfaces help mitigate the gap, yet human expertise remains a key factor in complex deployments within the secure multiparty computation industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Solutions Bridge Compliance and Performance

Hybrid architectures reached an 11.93% CAGR, outpacing other modes as enterprises combine on-premises data control with cloud scalability. Financial institutions process sensitive identifiers locally but offload compute-intensive analytics to secure cloud enclaves, meeting residency mandates while optimizing cost. Healthcare providers retain patient records on-premises while joining research consortia using cloud-based MPC, thereby satisfying both HIPAA and GDPR requirements simultaneously. The cloud segment still holds a 45.84% share of the secure multiparty computation market size, driven by turnkey managed services. On-premises remains critical for defense agencies that require full hardware custody.

Organizations are gravitating toward hybrid models as confidential-computing chips in public clouds close security gaps that were formerly addressed only by private deployments. This convergence shortens procurement cycles, lowers capex, and future-proofs infrastructure against changing regulations. Vendors are increasingly packaging orchestration layers that direct workloads to the optimal environment in real-time, further enhancing hybrid adoption across the secure multiparty computation market.

By Application: Secure AI and ML Emerges as Growth Catalyst

Secure AI and ML applications are projected to expand at a 12.57% CAGR, propelled by federated-learning frameworks that train across siloed datasets. Pharmaceutical alliances use MPC to cross-analyze genomic repositories while safeguarding individual privacy. Banks embed MPC within fraud-detection pipelines to fuse transaction streams across institutions, enhancing detection rates without violating secrecy laws. Privacy-preserving analytics, which holds 37.51% of the secure multiparty computation market share, remains the largest slice, thanks to established business intelligence use cases.

Emerging implementations apply MPC to large language model fine-tuning, supply chain provenance, and digital identity verification. Reduced compute overhead, improved developer toolkits, and hardware integration drive broader AI uptake, cementing the segment’s role as a core growth driver for the secure multiparty computation market.

By End-User Industry: Healthcare Drives Fastest Expansion

The healthcare and life sciences sector is forecast to grow at a 12.63% CAGR, benefiting from genomic and clinical-trial collaborations that demand cryptographic privacy. Drug innovators utilize MPC to aggregate trial data across global sites, thereby accelerating molecule selection while respecting patient consent. Banking and financial services maintain leadership with 32.69% secure multiparty computation market share, leveraging MPC for risk modeling and cross-border compliance. Governments deploy protocols for the exchange of classified information, and telecom firms safeguard network telemetry within joint cyber-defense initiatives.

Precision-medicine agendas and the expansion of genetic databases amplify data-sharing needs, making MPC indispensable in life-science workflows. Meanwhile, central-bank digital currency pilots and anti-money-laundering mandates ensure sustained investment from financial institutions, anchoring demand diversity across the secure multiparty computation market.

By Protocol Type: Zero-Knowledge Proofs Gain Institutional Traction

Secret-sharing protocols currently command 45.91% secure multiparty computation market share, valued for computational efficiency and maturity. Zero-knowledge proofs, however, are expected to log a 12.51% CAGR as blockchain custody providers seek verifiable yet private compliance reporting. Advances in zk-SNARKs and zk-STARKs enhance scalability, enabling institutions to audit computations without revealing their inputs. Homomorphic encryption appeals to sectors that require computation on fully encrypted data, although its heavier overhead confines its usage to regulated environments.

Hybrid schemes that blend protocol types are emerging, enabling organizations to tailor security and performance trade-offs according to their workloads. Such flexibility supports broader penetration into high-value sectors, reinforcing long-run expansion prospects for the secure multiparty computation market.

Geography Analysis

North America generated 38.19% of 2024 revenue, buoyed by more than USD 200 million in venture backing for cryptographic startups such as Zama and Nexus. Federal privacy regulations, such as the California Consumer Privacy Act, provide clarity, while hyperscale cloud providers integrate confidential computing features that embed MPC capabilities. Financial-services innovation clusters in New York, Toronto, and San Francisco drive early adoption.

The Asia Pacific is the fastest-growing region, with a 12.44% CAGR, as Japan’s Society 5.0 funds privacy-preserving computation for smart-city services, and China’s data-security law necessitates local processing. South Korea tightens personal information regulations, and India finalizes digital privacy legislation, each catalyzing demand. Regional cloud vendors partner with cryptography specialists to offer compliant services, thereby further accelerating the uptake of secure multiparty computation.

Europe sustains momentum through the GDPR and the forthcoming Data Act, which prioritize privacy by design. The European Medicines Agency pilots MPC for pharmacovigilance, while the Digital Finance Strategy spurs banking deployment. The Middle East and Africa are witnessing the nascent adoption of financial-inclusion projects and government modernization, whereas South America’s cross-border trade frameworks are gradually incorporating privacy-preserving analytics. Geographic heterogeneity ensures both short-term revenue concentration in mature markets and long-term upside in emerging jurisdictions.

Competitive Landscape

The secure multiparty computation market remains fragmented, as specialized vendors compete with large technology providers that integrate MPC into cloud and analytics stacks. Duality Technologies, Partisia, and Inpher secure strategic alliances with multinational banks and healthcare networks, leveraging niche protocol expertise. Microsoft and IBM embed MPC within broader confidential-computing platforms, attracting enterprises that favor one-stop solutions.

Differentiation pivots on protocol efficiency, hardware acceleration, and vertical customization. Intel’s SGX v3.0 launch triggered partnerships focused on latency-sensitive workloads, while startup MPCH Labs targets decentralized-finance custody. Patent filings in homomorphic encryption and zero-knowledge proofs create intellectual-property moats.

Venture funding, exceeding USD 300 million in 2024, intensifies competition as new entrants iterate rapidly. End-user purchasing increasingly values implementation support and compliance tooling over pure cryptographic novelty, steering market share to providers that combine technical depth with operational maturity.

Secure Multiparty Computation Industry Leaders

Duality Technologies Inc.

Partisia ApS

Inpher Inc.

Cosmian SAS

Enveil Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Banks across Japan, Singapore, and Australia expanded their use of secure computation for cross-border payment analytics in response to tighter data-localization mandates. These projects illustrate how Asia Pacific regulations are driving steady uptake of privacy-preserving collaboration tools that keep international transactions compliant with sovereignty requirements.

- June 2025: A consortium of healthcare researchers launched federated-learning systems powered by secure multiparty computation to support multi-site clinical trials. The deployment enables joint drug-discovery work while staying within HIPAA and GDPR rules, showing that MPC has matured for regulated healthcare use.

- March 2025: Major cloud providers upgraded their confidential-computing offerings with new hardware accelerators and optimized protocols, cutting MPC processing overhead by about 35%. The boost lets organizations run real-time, privacy-preserving analytics that were previously too slow for production.

- January 2025: The European Union brought the Markets in Crypto-Assets Regulation into full force, pushing cryptocurrency platforms to use privacy-preserving tools for transaction monitoring and compliance. Exchanges and custodians are now turning to zero-knowledge proofs and secure multiparty computation so they can prove adherence without exposing trading details, creating lasting demand in financial services.

Global Secure Multiparty Computation Market Report Scope

The Secure Multiparty Computation Market Report is Segmented by Deployment Mode (On-Premises, Cloud, Hybrid), Application (Privacy-Preserving Analytics, Fraud Detection, Secure AI/ML, Genomic Data Analysis, Other Application), End User Industry (Banking and Financial Services, Healthcare and Life Sciences, Government and Defense, IT and Telecom, Other End User Industry), Protocol Type (Secret Sharing, Homomorphic Encryption, Zero-Knowledge Proofs, Hybrid Protocols, Other Protocol Type), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud |

| Hybrid |

| Privacy-Preserving Analytics |

| Fraud Detection |

| Secure AI/ML |

| Genomic Data Analysis |

| Other Application |

| Banking and Financial Services |

| Healthcare and Life Sciences |

| Government and Defense |

| IT and Telecom |

| Other End User Industry |

| Secret Sharing |

| Homomorphic Encryption |

| Zero-Knowledge Proofs |

| Hybrid Protocols |

| Other Protocol Type |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| Hybrid | |||

| By Application | Privacy-Preserving Analytics | ||

| Fraud Detection | |||

| Secure AI/ML | |||

| Genomic Data Analysis | |||

| Other Application | |||

| By End User Industry | Banking and Financial Services | ||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| IT and Telecom | |||

| Other End User Industry | |||

| By Protocol Type | Secret Sharing | ||

| Homomorphic Encryption | |||

| Zero-Knowledge Proofs | |||

| Hybrid Protocols | |||

| Other Protocol Type | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How fast is the secure multiparty computation market expected to grow through 2030?

The secure multiparty computation market is projected to record an 11.67% CAGR between 2025 and 2030, moving from USD 0.96 billion to USD 1.67 billion.

Which deployment model is gaining popularity for privacy-preserving computing?

Hybrid architectures are expanding at an 11.93% CAGR because they balance on-premises data control with the scalability of cloud resources.

What industry segment is the fastest-growing adopter of secure multiparty computation?

Healthcare and life sciences lead growth with a forecast 12.63% CAGR, driven by genomic collaborations and clinical-trial privacy requirements.

Why are zero-knowledge proofs important in this market?

Zero-knowledge proofs allow institutions to verify transactions or analytics without exposing underlying data, fueling a 12.51% CAGR in protocol adoption.

Which region offers the highest growth potential?

Asia Pacific shows the strongest outlook at a 12.44% CAGR as regulatory frameworks in Japan, China, and India emphasize privacy-preserving data collaboration.

What limits real-time use of secure multiparty computation today?

High computational and communication overheads still create latency barriers, making it challenging for time-critical applications to meet performance targets.

Page last updated on: