Secure Flash Drive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

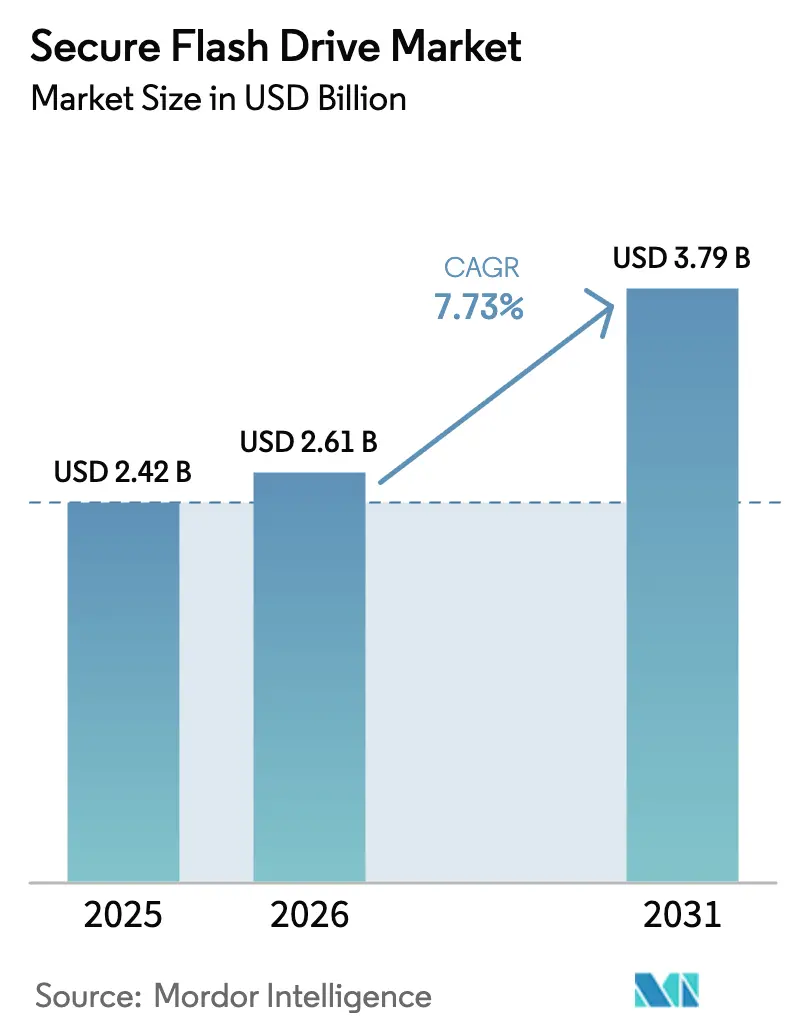

| Market Size (2026) | USD 2.61 Billion |

| Market Size (2031) | USD 3.79 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

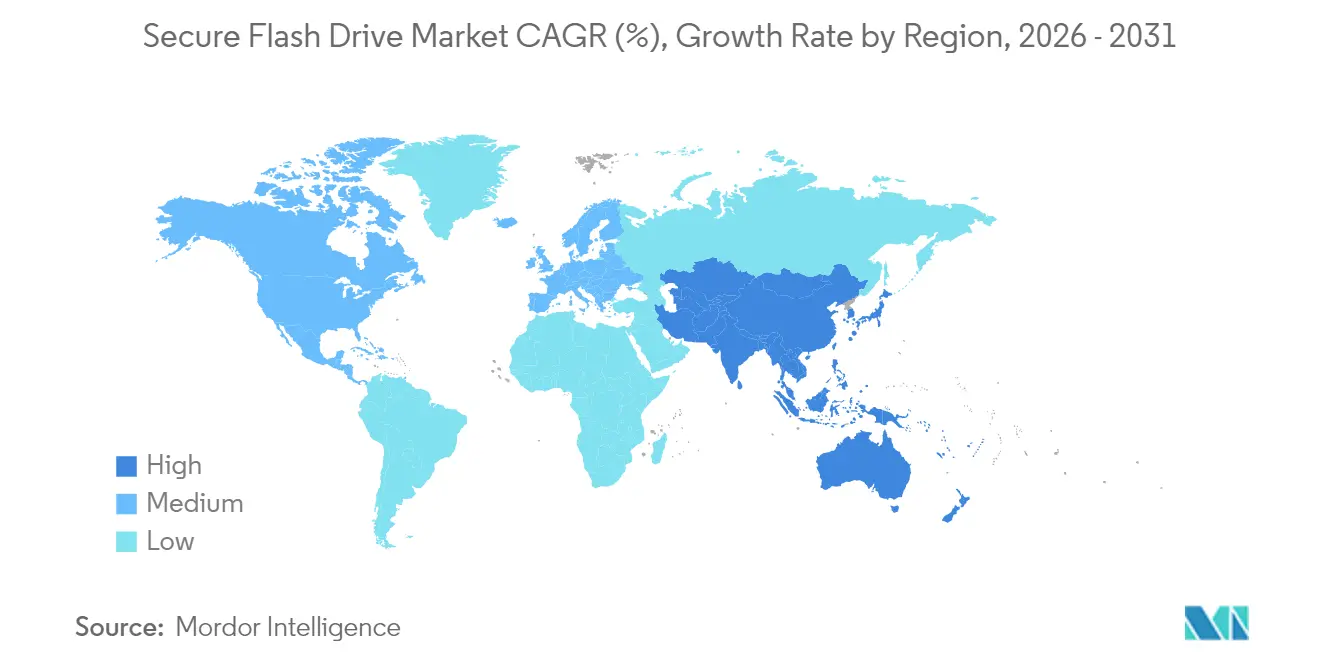

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Flash Drive Market Analysis by Mordor Intelligence

Secure flash drive market size in 2026 is estimated at USD 2.61 billion, growing from 2025 value of USD 2.42 billion with 2031 projections showing USD 3.79 billion, growing at 7.73% CAGR over 2026-2031. This pace reflects escalating encryption mandates, the arrival of post-quantum-ready controllers, and the security gaps opened by bring-your-own-device (BYOD) policies. Procurement cycles in the United States and the European Union have shortened as agencies and regulated enterprises replace legacy USB sticks with FIPS 140-3 Level 3 hardware, while laptop makers’ wholesale shift to USB Type-C ports accelerates refresh spending. Healthcare breach costs, quantum-safe readiness, and cloud-linked remote-wipe consoles are additional demand catalysts that differentiate vendor roadmaps and open premium pricing tiers. Competitive rivalry centers on certification velocity, high-capacity NVMe drives, and miniature cryptographic modules that can be firmware-upgraded to FIPS 203/204/205 algorithms without increasing power consumption.

Key Report Takeaways

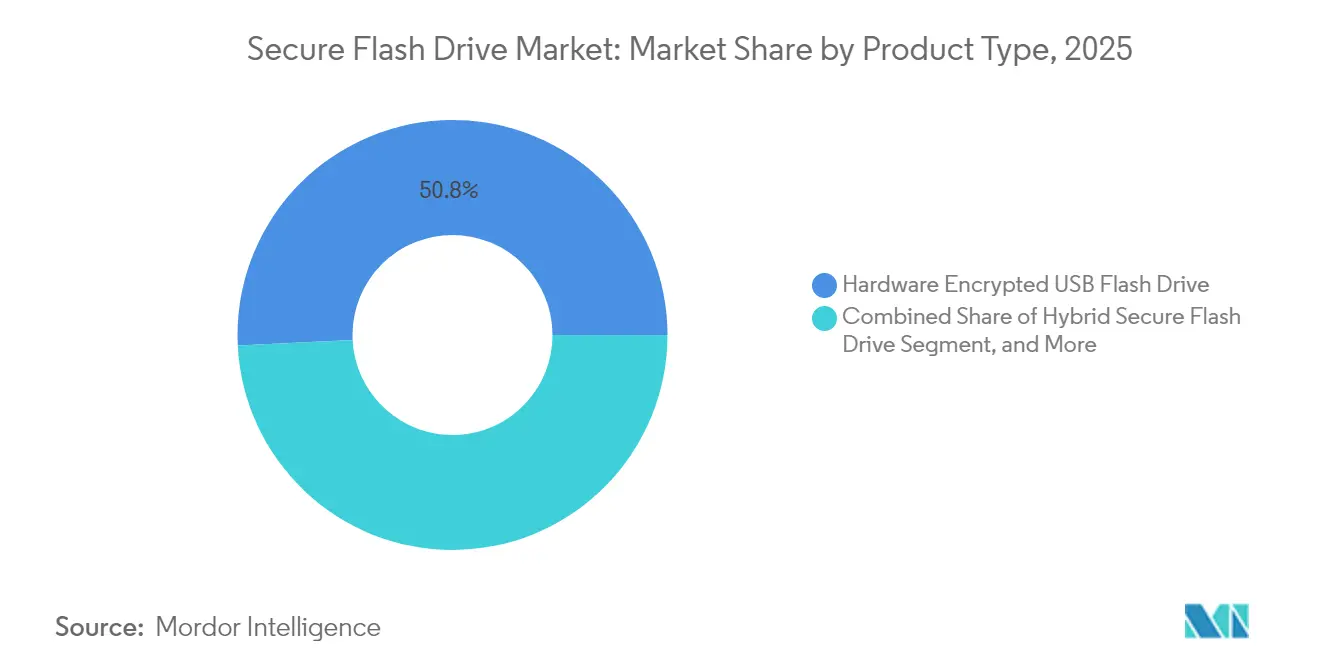

- By product type, hardware-encrypted USB flash drives led with a 50.78% share of the secure flash drive market in 2025, while hybrid models are forecasted to expand at a 9.66% CAGR through 2031.

- By connectivity interface, USB 3.x commanded a 53.05% revenue share of the secure flash drive market in 2025; USB Type-C is set to grow at a 10.29% CAGR to 2031.

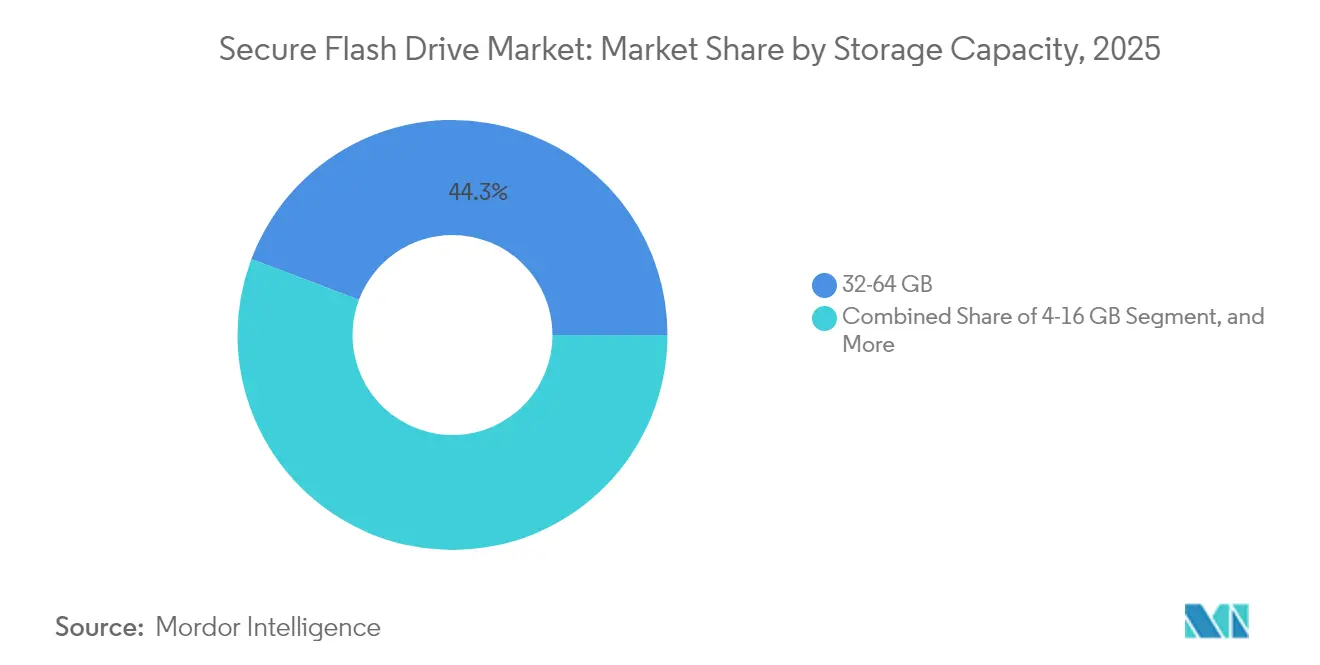

- By storage capacity, devices with 32-64 GB accounted for 44.25% of the secure flash drive market size in 2025; devices with 512 GB and above are expected to advance at an 10.92% CAGR between 2026 and 2031.

- By end-user industry, the government and defense sector generated 39.31% of the secure flash drive market's revenue in 2025, while the healthcare sector is poised to grow at a 12.13% CAGR from 2025 to 2031.

- By geography, North America dominated the secure flash drive market, accounting for a 36.35% share in 2025. In contrast, the Asia Pacific is projected to post the highest CAGR of 10.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Secure Flash Drive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Hardware-Encrypted Portable Storage in Government Agencies | +1.8% | North America, Europe, Middle East | Medium term (2-4 years) |

| Proliferation of BYOD Policies Elevating Endpoint Security Concerns | +1.5% | Global, concentration in North America and Asia Pacific | Short term (≤2 years) |

| Regulatory Mandates on Data Protection such as GDPR and CCPA | +1.4% | Europe, North America, spillover to Asia Pacific | Medium term (2-4 years) |

| Growth of Edge Computing Requiring Secure Offline Data Transfer | +1.2% | Global, early adoption in Asia Pacific manufacturing hubs and European industry | Long term (≥4 years) |

| Surge in Cyber-Insurance Premium Discounts for Encrypted Storage Usage | +0.9% | North America, Europe | Short term (≤2 years) |

| Miniaturization of Post-Quantum Ready Cryptographic Controllers | +1.4% | Global, R&D concentration in North America and Asia Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Hardware-Encrypted Portable Storage in Government Agencies

Federal contracting rules are driving wholesale upgrades. The U.S. Department of Defense now obliges contractors handling controlled unclassified information to deploy FIPS 140-3 Level 3 devices by September 2026.[1]U.S. Department of Defense, “DFARS Clause 252.204-7012,” acquisition.gov Kanguru Solutions secured early certification for its Defender Elite 300 in 2025, thereby unlocking contract opportunities ahead of incumbents who were waiting for NIST validation. European civil agencies are following suit under the NIS2 Directive, which extends encrypted-storage duties to 160,000 operators of essential services.[2]European Union Agency for Cybersecurity, “NIS2 Directive,” enisa.europa.eu Hardware buyers favor tamper-evident casings, dual-factor keypads, and epoxy-sealed chips that zeroize keys if intrusion is detected. These specifications elevate average selling prices and shift vendor engineering toward rugged housings and kinetic sabotage sensors.

Proliferation of BYOD Policies Elevating Endpoint Security Concerns

Remote work practices have turned personal USB sticks into covert exfiltration channels. The Australian Cyber Security Centre identifies removable media as a high-risk vector, advising enterprises to adopt hardware-encrypted drives with centralized wipe capabilities. Hybrid secure flash drives marry onboard AES-256 encryption with cloud dashboards that log every file event, supporting HR off-boarding and lost-device kill switches. Banks embed drive serial numbers into acceptable-use policies, and healthcare CIOs whitelist only FIPS-validated models for imaging transfers between clinics. The result is a double-digit expansion of hybrid SKUs even as pure software encryption loses relevance.

Regulatory Mandates on Data Protection such as GDPR and CCPA

Fines have intensified. European regulators levied EUR 1.6 billion in GDPR penalties in 2024, the bulk of which was linked to breaches involving unencrypted portable data. California’s amended CCPA similarly triggers statutory damages when unencrypted consumer information is exposed. Payment processors must comply with PCI DSS v4.0, which now requires encryption of cardholder data stored on USB devices. Audit fatigue prompts compliance officers to adopt turnkey hardware encryption, as software keys can be stolen from system RAM. Vendors promoting FIPS-validated SKUs experience a reduction in procurement cycles from 16 to 9 months in the finance and retail segments.

Miniaturization of Post-Quantum Ready Cryptographic Controllers

NIST finalized FIPS 203-205 algorithms in August 2024, prompting drive makers to harden future-proof hardware. Kingston’s IronKey Vault Privacy 80 ships with controller microcode that can load ML-KEM and ML-DSA via signed firmware updates. R&D teams are shrinking lattice-based cipher blocks to fit existing board real estate while maintaining steady power budgets. Government tenders now cite “quantum-resistant readiness” as a weighted scoring factor, nudging buyers to over-specify drives that will remain compliant for a decade. Early movers gain pricing latitude and are more likely to receive multi-year renewals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Premiums Over Standard USB Drives | -1.2% | Global, acute in South America and Africa | Short term (≤2 years) |

| Performance Trade-offs Due to On-Device Encryption | -0.8% | Global, heavy in media production and research | Medium term (2-4 years) |

| Limited Standardization Across Interface Protocols | -0.6% | Global | Medium term (2-4 years) |

| Rising Threat of Firmware-Level Supply-Chain Attacks | -0.7% | Global, defense and critical infrastructure | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Price Premiums Over Standard USB Drives

Hardware encryption multiplies the bill-of-materials cost. A 64 GB secure flash retails for USD 129-217, while commodity equivalents cost USD 8-15.[3]Kingston Technology, “IronKey Vault Privacy Pricing,” kingston.com Certification fees, tamper-proof enclosures, and dedicated crypto chips keep margins high, deterring adoption among small businesses in South America and Africa. Vendors are pooling silicon across SKUs and migrating to 3D NAND to reduce the cost per gigabyte, but FIPS labs and destructive testing still limit price reductions. Many enterprises defer purchases until regulators or cyber-insurers make the use of encrypted drives non-negotiable.

Performance Trade-offs Due to On-Device Encryption

Real-time ciphering reduces throughput to 145-310 MB/s read and 115-250 MB/s write, far below the 1,000 MB/s read speeds of unencrypted NVMe sticks. Video editors, genomics labs, and HPC researchers balk at queue delays. Apricorn’s Aegis NVX pushes encrypted NVMe to 1,000 MB/s yet costs more than USD 400 per TB. Until controller clock speeds and thermal budgets improve, performance-sensitive verticals will adopt them selectively or maintain dual inventories of fast, unencrypted units and slower, secure units.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Models Gain Enterprise Traction

Hybrid secure flash drives are projected to post a 9.66% CAGR, surpassing pure hardware, despite hardware accounting for 50.78% of the secure flash drive market share in 2025. The model combines on-device AES-256 engines with SaaS consoles that geo-fence usage, push firmware updates, and remotely wipe lost units. Enterprises under BYOD pressure value centralized oversight more than absolute ruggedness. Government and defense still favor keypad-equipped hardware units that operate independently of host systems, insulating keys from malware.

The secure flash drive market size attributable to hybrid devices is expected to double by 2031 as banking and healthcare audits endorse remote-management evidence logs. Software-only encryption persists in cost-sensitive SMB niches, but its revenue share is shrinking as regulators question the security of host-based key storage. Vendors are integrating biometric sensors and post-quantum firmware pipelines to future-proof both hardware and hybrid lines.

By Connectivity Interface: Type-C Ascends on Laptop Design Shifts

USB 3.x maintained a 53.05% revenue share in 2025, yet USB Type-C is forecasted to outpace it with a 10.29% CAGR. Thin-and-light laptops now ship almost exclusively with Type-C ports, compelling IT buyers to procure reversible secure flash models. The resulting refresh fuels the secure flash drive market, enabling drive makers to achieve read speeds of up to 310 MB/s while maintaining encryption overhead limits.

Government desktops and ruggedized workstations still rely on Type-A; therefore, vendors bundle dual-headed cables to hedge against mixed fleets. Thunderbolt remains a niche enthusiast option among forensic labs seeking 40 Gbps bandwidth. As the installed base of Type-C hosts grows, the secure flash drive market size tied to legacy interfaces will contract, concentrating R&D on Type-C and USB 4 support.

By Storage Capacity: High-Capacity Drives Serve Data-Intensive Workflows

The 512 GB and above tier is projected to achieve an 10.92% CAGR, the fastest among capacities, while the 32-64 GB tier held a 44.25% share in 2025. Field engineers capturing sensor data and radiology departments exchanging 2 GB DICOM studies need portable petabytes, not megabytes. Apricorn’s 24 TB launch marks the pinnacle of current scaling and signals the roadmap toward mainstream 1 TB by 2028.

Cost curves also tilt demand upward: USD 0.41 per GB at 512 GB bests USD 2.00 per GB at 64 GB. Government agencies continue to procure lower tiers for document transport, yet audit findings increasingly recommend that there is surplus headroom. Consequently, higher-density SKUs now anchor vendor gross margins and spur NAND suppliers to bundle more layers per die, thereby reinforcing the momentum in the secure flash drive market for premium capacities.

By End-user Industry: Healthcare Breach Costs Accelerate Adoption

Government and defense generated 39.31% of 2025 revenue, but healthcare’s 12.13% CAGR makes it the fastest-climbing vertical. The average breach remediation cost reached USD 9.77 million in 2024, and 725 healthcare incidents were reported to U.S. regulators. Hospitals now include FIPS-validated USB drives in every imaging transfer SOP.

Banks embed encrypted drives in PCI DSS v4.0 playbooks to secure transaction logs, while energy utilities adhere to IEC 62443 guidelines that demand air-gapped portable media for SCADA updates. Manufacturing plants load CNC programs via sealed USB drives to avoid exposure to Ethernet. Across industries, breach fines and cyber-insurance deductibles are directly translating into increased demand for secure flash drives, even in verticals once thought to be price-averse.

Geography Analysis

North America held a 36.35% share in 2025, driven by DFARS compliance and a dense defense-contractor ecosystem. Canada mirrors U.S. encryption norms through the Canadian Centre for Cyber Security's guidance, and Mexico’s banks follow the Banco de México's encryption rules. Despite strong top-line spend, SMB penetration is uneven because price premiums exceed IT budgets outside regulated verticals.

The Asia Pacific is expected to post a 10.21% CAGR, the fastest regional growth rate. Japan, India, and China are embedding data-sovereignty clauses in AI procurement that demand on-premises encrypted storage. [4]Dell Technologies, “Sovereign AI Whitepaper,” dell.com China’s Cybersecurity Law additionally earmarks domestic suppliers, spurring local champions. India’s Digital Personal Data Protection Act widens breach-notification liability, pushing enterprises to standardize on secure flash devices. Manufacturing dominance means that Asia both produces and consumes the lion’s share of global USB output, completing a virtuous cycle for regional vendors within the secure flash drive market.

The enforcement of NIS2 defines Europe’s outlook. Penalties of up to EUR 10 million or 2% of global turnover are prompting mid-sized firms to fast-track hardware-encrypted procurement. Germany’s BSI technical guides and the U.K.’s NCSC advisories align closely with FIPS benchmarks, making U.S.-certified drives acceptable across borders. South America and Africa trail behind due to budget constraints, although Brazil’s LGPD and South Africa’s POPIA are laying the legal groundwork. The Middle East is emerging as a hub for petrochemicals, utilities, and sovereign wealth, with a focus on embedding encrypted portable media in zero-trust network architectures.

Competitive Landscape

The secure flash drive market is moderately fragmented. Kingston Technology, iStorage, Apricorn, and Kanguru Solutions captured the largest slices of 2024 revenue, especially in public-sector bids. Their moat is rapid FIPS 140-3 validation; early certification grants incumbency advantages in multi-year frameworks. Kingston’s IronKey Vault Privacy 80, announced in May 2024, blends 2 TB capacity with pending Level 3 clearance and firmware hooks for post-quantum patches. Apricorn responded with a 24TB hardware-encrypted drive designed for forensic imaging workflows.

Strategic pivots center on hybrid management stacks. DataLocker and Kanguru are layering SaaS consoles over hardware, courting BFSI and healthcare auditors that demand asset-level audit trails. Biometric authentication is maturing as a differentiator; fingerprint-enabled enclosures obviate PIN fatigue and thwart shoulder-surfing. Performance race lines are redrawn around NVMe, where Apricorn’s Aegis NVX crosses 1 GB/s while retaining hardware encryption. Competitors are re-architecting controller pipelines to close that gap without breaching thermal envelopes.

White-space opportunities persist in offering sub-USD 100 price points at 256 GB with Level 3 validation, a feat that requires silicon cost-downs and shared crypto cores. Vendors that compress BOM costs first will unlock price-sensitive geographies and broaden the addressable market for secure flash drives.

Secure Flash Drive Industry Leaders

Kingston Technology Company, Inc.

iStorage Limited

Apricorn, Inc.

Kanguru Solutions LLC

DataLocker Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Apricorn has expanded its Aegis Secure Key 3NX family to 512 GB, providing forensic units and field engineers with a FIPS 140-2 Level 3 drive that securely stores high-resolution images and raw sensor files while maintaining chain-of-custody integrity in the field.

- August 2024: NIST released the first trio of post-quantum algorithms, FIPS 203 (ML-KEM), FIPS 204 (ML-DSA), and FIPS 205 (SLH-DSA), compelling secure flash-drive manufacturers to incorporate quantum-safe code into their controllers as future government bids begin to require it.

- May 2024: Kingston unveiled the IronKey Vault Privacy 80 external SSD, offering up to 2 TB, FIPS 140-3 Level 3 pending status, and firmware hooks for post-quantum updates, positioning the drive for agencies racing to meet the September 2026 DFARS deadline.

- May 2024: Kingston also introduced the IronKey Keypad 200 Series, a PIN-pad device that supports up to 512 GB and carries FIPS 140-3 Level 3 pending validation, addressing defense contractor demand for tamper-evident, brute-force-proof portable storage.

Global Secure Flash Drive Market Report Scope

| Hardware Encrypted USB Flash Drive |

| Software Encrypted USB Flash Drive |

| Hybrid Secure Flash Drive |

| USB 2.0 |

| USB 3.x |

| USB Type-C |

| Thunderbolt |

| 4–16 GB |

| 32–64 GB |

| 128–256 GB |

| 512 GB and Above |

| Government and Defense |

| Banking, Financial Services and Insurance |

| Healthcare |

| Energy and Utilities |

| IT and Telecom |

| Manufacturing |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Hardware Encrypted USB Flash Drive | ||

| Software Encrypted USB Flash Drive | |||

| Hybrid Secure Flash Drive | |||

| By Connectivity Interface | USB 2.0 | ||

| USB 3.x | |||

| USB Type-C | |||

| Thunderbolt | |||

| By Storage Capacity | 4–16 GB | ||

| 32–64 GB | |||

| 128–256 GB | |||

| 512 GB and Above | |||

| By End-user Industry | Government and Defense | ||

| Banking, Financial Services and Insurance | |||

| Healthcare | |||

| Energy and Utilities | |||

| IT and Telecom | |||

| Manufacturing | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the secure flash drive market?

The market is valued at USD 2.61 billion in 2026 and is forecast to reach USD 3.79 billion by 2031.

Which product type is growing fastest?

Hybrid models that pair hardware encryption with cloud management are projected to expand at a 9.66% CAGR through 2031.

Why is healthcare demand accelerating?

Breach remediation averages USD 9.77 million, so hospitals are adopting FIPS-validated drives to meet HIPAA and data-breach-notification rules.

How will post-quantum standards affect purchasing?

Drives that can load FIPS 203-205 algorithms via firmware will be favored, especially in government bids that specify quantum-safe readiness.

Which region shows the highest growth rate?

Asia Pacific is forecast to advance at 10.21% CAGR, driven by data-sovereignty mandates in Japan, India, and China.

What interface will dominate new laptop deployments?

USB Type-C is gaining ground rapidly as OEMs drop Type-A ports, pushing enterprises to standardize on reversible connectors.

Page last updated on: