Secure and Quantum-Safe Fiber Backbone Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 11.52 Billion |

| Growth Rate (2026 - 2031) | 29.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

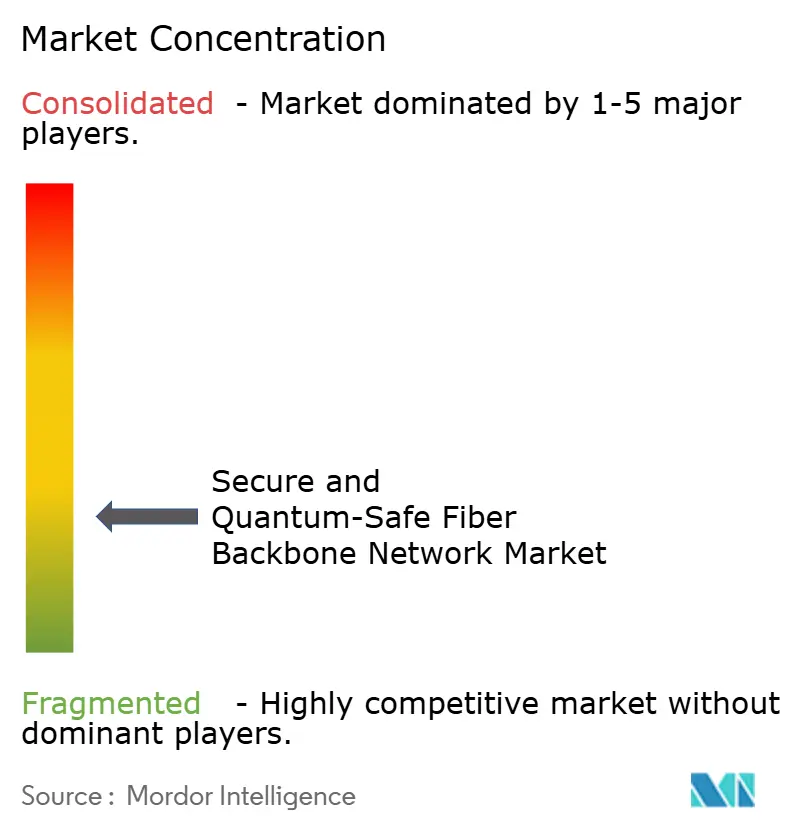

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure and Quantum-Safe Fiber Backbone Network Market Analysis by Mordor Intelligence

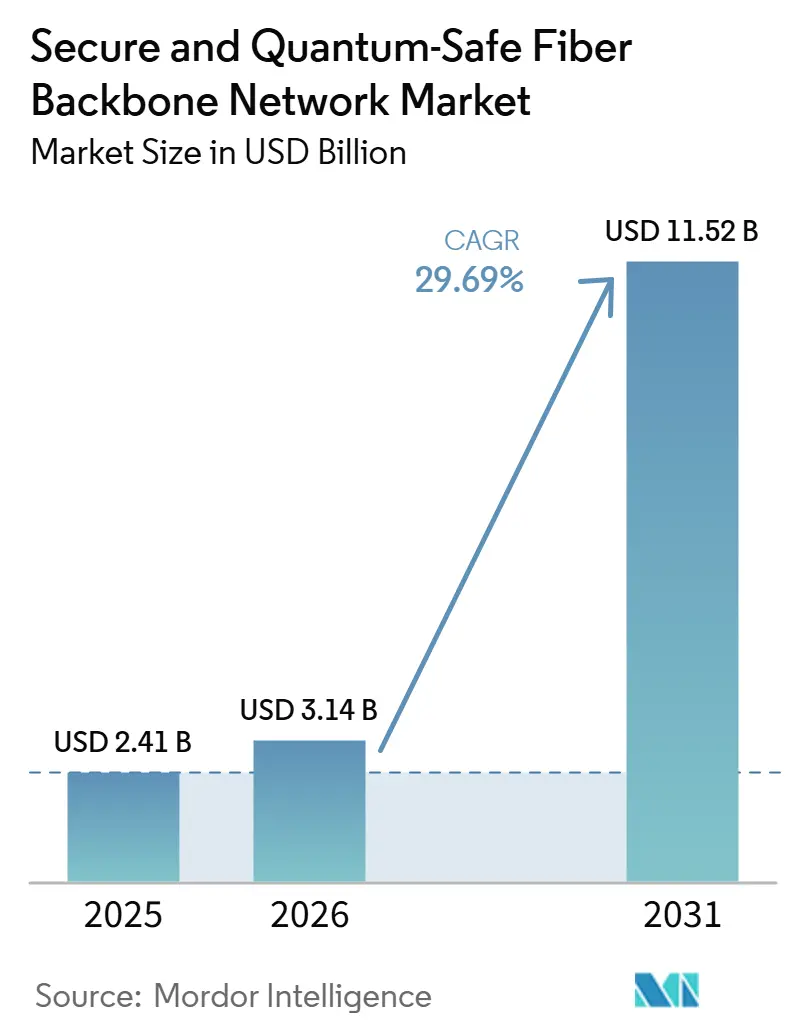

The Secure And Quantum-Safe Fiber Backbone Network Market size is projected to expand from USD 2.41 billion in 2025 and USD 3.14 billion in 2026 to USD 11.52 billion by 2031, registering a CAGR of 29.69% from 2026 to 2031. The pace of growth reflects a direct response to the harvest-now, decrypt-later risk that has moved from a theoretical issue to an active concern for long-haul communications networks. Government migration deadlines for post-quantum cryptography are also pushing carriers, defense suppliers, and critical network operators to move earlier than many had originally planned. At the same time, 5G backbone upgrades and early 6G design work are making quantum-safe controls part of broader network modernization budgets rather than a separate future initiative. The supply side remains tight because several core photonic and detector components still come from a narrow manufacturing base, and multi-vendor interoperability is not yet fully mature across trusted-node environments. Even with those limits, the secure and quantum-safe fiber backbone network market is attracting stronger participation from telecom incumbents, cloud providers, optical transport vendors, and quantum security specialists, thereby widening the opportunity for managed services, software-led migration programs, and backbone security overlays.

Key Report Takeaways

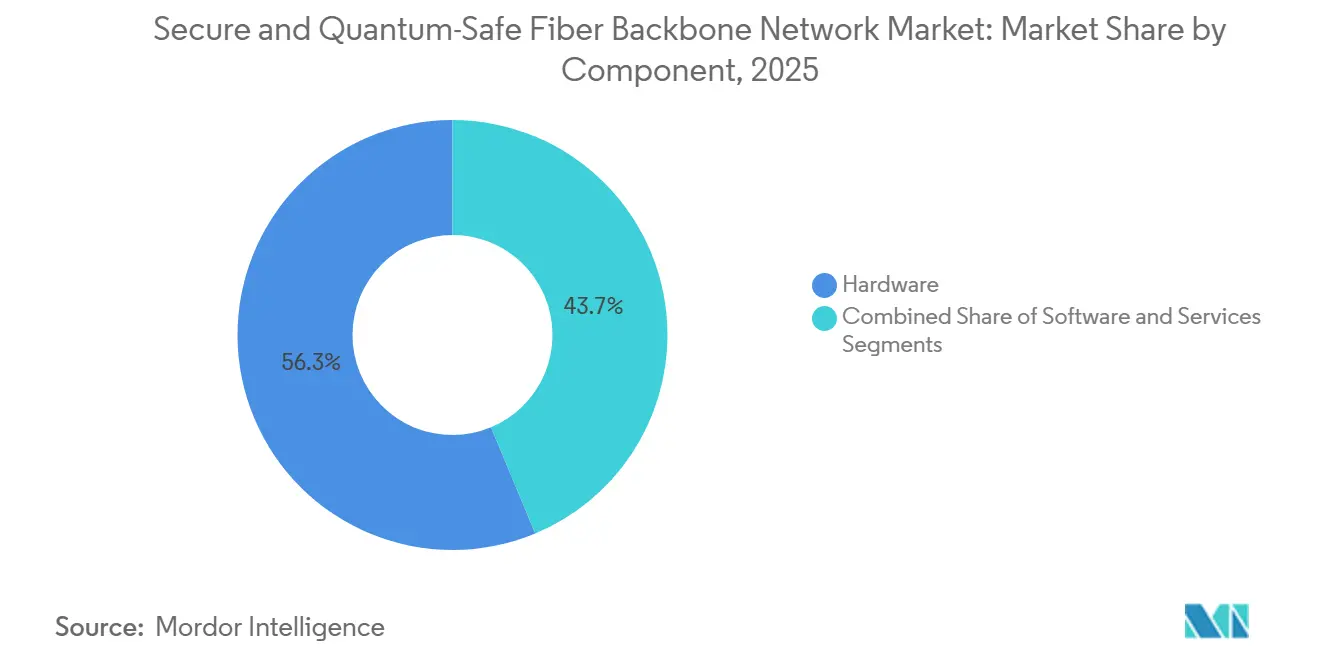

- By component, hardware held a 56.29% revenue share in the secure and quantum-safe fiber backbone network market in 2025, while software is projected to expand at a 34.33% CAGR through 2031.

- By technology, post-quantum cryptography accounted for 51.10% revenue share in the secure and quantum-safe fiber backbone network market in 2025, while quantum key distribution is projected to grow at a 33.61% CAGR through 2031.

- By application, telecommunications captured 33.23% revenue share in the secure and quantum-safe fiber backbone network market in 2025, while BFSI is projected to expand at a 31.99% CAGR through 2031.

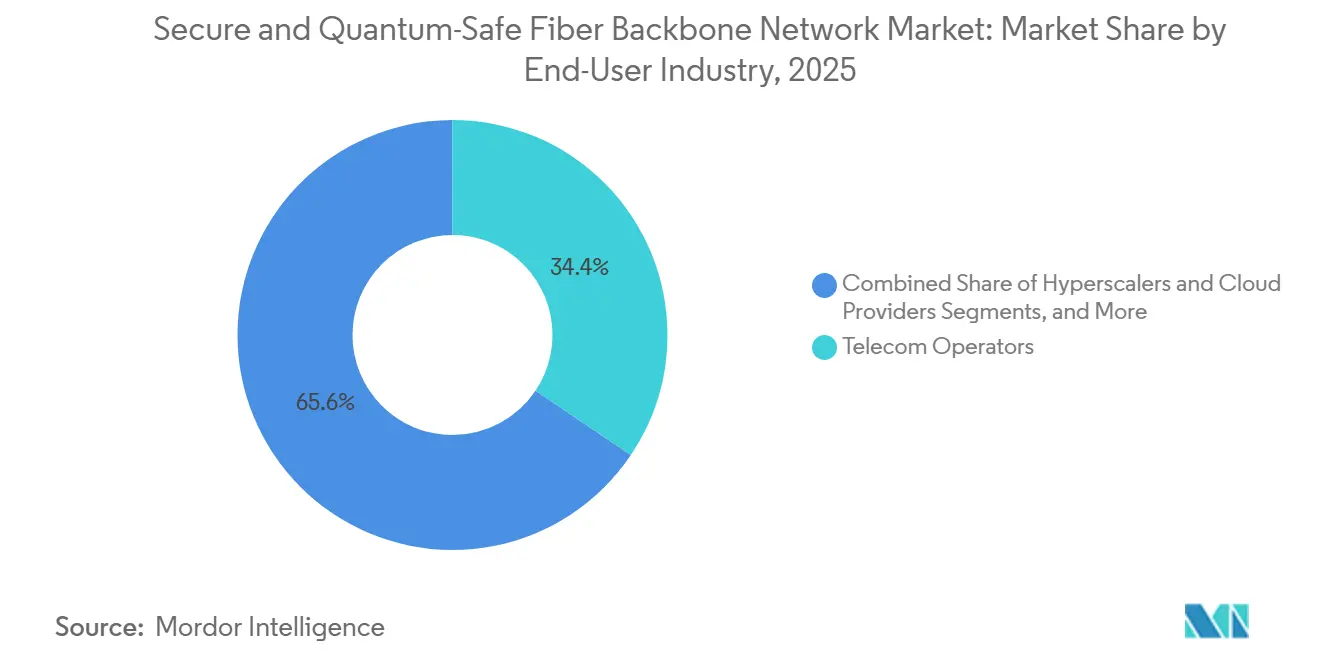

- By end-user industry, telecom operators held 34.43% revenue share in the secure and quantum-safe fiber backbone network market in 2025, while hyperscalers and cloud providers are projected to advance at a 35.42% CAGR through 2031.

- By network type, long-haul fiber networks accounted for 39.13% revenue share in the secure and quantum-safe fiber backbone network market in 2025, while subsea and cross-border fiber links are projected to grow at a 41.00% CAGR through 2031.

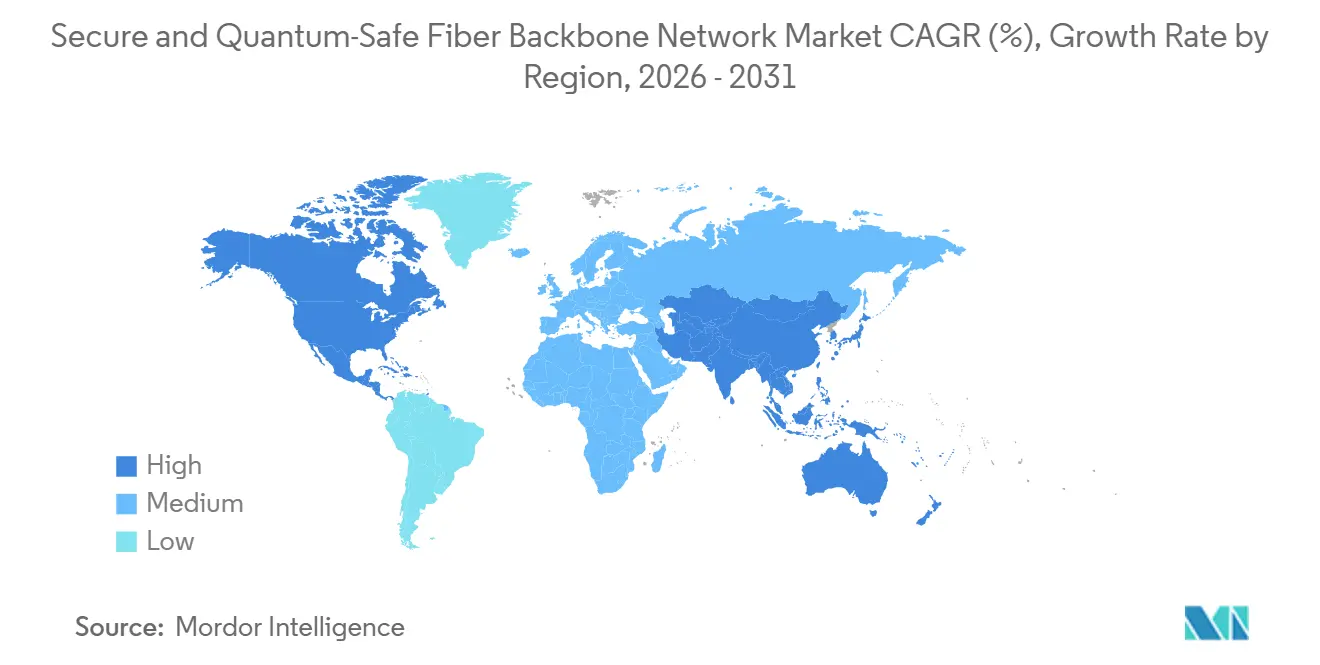

- By geography, North America held 32.12% revenue share in the secure and quantum-safe fiber backbone network market in 2025, while Asia-Pacific is projected to expand at a 32.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Secure and Quantum-Safe Fiber Backbone Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Harvest-Now, Decrypt-Later Exposure | +8.2% | Global | Short term (≤ 2 years) |

| NIST Post-Quantum Migration Deadlines | +6.8% | North America and EU, spillover to APAC and Middle East and Africa | Short term (≤ 2 years) |

| Telecom Backbone Modernization for 5G and 6G | +5.4% | APAC core, North America, EU | Medium term (2-4 years) |

| Sovereign Quantum Network Programs | +3.9% | China, EU, India, UK, Middle East | Medium term (2-4 years) |

| Quantum-Safe Data Retention for Critical Infrastructure | +2.6% | Global | Medium term (2-4 years) |

| Hybrid QKD and PQC Deployment Economics | +1.8% | Global, early gains in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Harvest-Now, Decrypt-Later Exposure

The harvest-now, decrypt-later model has moved beyond theory and now shapes how carriers and critical infrastructure operators view backbone security risk in the secure and quantum-safe fiber backbone network market. Research published in 2026 found that storing even 1% of intercepted global encrypted traffic could cost nation-state actors around USD 1 billion per year under conservative commercial cloud pricing, which is a manageable level for high-value intelligence collection. Long-haul fiber routes are especially vulnerable because they carry heavy traffic along predictable physical paths, making bulk interception more practical through fiber taps or collection mandates. Archived 5G and future 6G control-plane records create a lasting vulnerability because they preserve session and authentication data that could be decrypted later if cryptographically relevant quantum systems emerge. This cost imbalance, where interception is cheap today and decryption can wait, is shortening procurement cycles across the secure and quantum-safe fiber backbone network market even in countries without formal migration laws.

NIST Post-Quantum Migration Deadlines

The NIST standardization effort has shifted the secure and quantum-safe fiber backbone network market from early evaluation into deadline-driven procurement. NIST finalized FIPS 203, FIPS 204, and FIPS 205 in August 2024, and then selected HQC in March 2025 to widen key-establishment options for future deployments.[1]National Institute of Standards and Technology, “NIST Selects HQC as Fifth Algorithm for Post-Quantum Encryption,” National Institute of Standards and Technology, nist.gov The White House then accelerated the pace in June 2026 through Executive Order 14412, which required federal agencies to migrate high-value assets to PQC key establishment by December 31, 2030, and digital signatures by December 31, 2031. OMB Memorandum M-26-15 also required agency migration plans within 120 days and placed total federal transition costs at USD 7.1 billion over a decade, providing suppliers and network operators with a clear budget signal. Because federal contractors and defense communications vendors must align with these rules, the secure and quantum-safe fiber backbone network market is seeing demand spread well beyond government agencies into the broader backbone supply chain.

Telecom Backbone Modernization For 5G And 6G

Post-quantum security is becoming part of mainstream transport planning as operators modernize core networks across the secure and quantum-safe fiber backbone network market. Research released in 2025 showed that ML-KEM and ML-DSA could be introduced into 5G core functions with only limited latency and bandwidth overhead, which reduced a major barrier to full-network adoption. Operators are also paying closer attention to timing data because archived 5G Precision Timing Protocol records pose a future decryption risk that older security models cannot easily address. In June 2025, Juniper Networks, ID Quantique, and Turkcell validated a QKD-over-5G-backhaul approach that protected Precision Timing Protocol channels without introducing a latency penalty. By MWC Barcelona 2026, vendors were already demonstrating end-to-end 5G stacks with embedded PQC in hybrid mode, which signaled that the secure and quantum-safe fiber backbone network market was moving toward production-ready deployment rather than isolated trials.[2]Canonical, “Building Quantum-Safe Telecom Infrastructure for 5G and Beyond,” Canonical, canonical.com

Sovereign Quantum Network Programs

Government-backed backbone programs are acting as anchor demand in the secure and quantum-safe fiber backbone network market. China’s national quantum communication network operated 145 fiber backbone nodes and 20 metropolitan networks across 80 cities and 17 provinces, while the combined network length of CN-QCN and the earlier Beijing-Shanghai backbone exceeded 12,000 km. India reached a 1,000 km QKD network milestone in April 2026 through its National Quantum Mission and is working toward a 2,000 km national backbone with satellite integration by 2031. The United Kingdom also committed GBP 125 million (USD 159 million) to quantum networking within its wider GBP 2 billion (USD 2.66 billion) quantum program for 2026-2030, naming BT Group as the delivery partner for quantum-secure infrastructure.[3]UK Government, “UK’s Quantum Leap to Help Beat Disease, Deliver High-Paid Jobs, and Strengthen National Security,” UK Government, gov.uk These sovereign programs matter beyond direct public spending because they justify larger component production volumes, thereby improving supply availability and lowering unit costs for private operators entering the secure and quantum-safe fiber backbone network market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Trusted-Node and QKD Rollouts | -4.5% | Global, most acute in Middle East and Africa and South America | Short term (≤ 2 years) |

| Limited Fiber Reach Without Trusted Nodes | -3.1% | Rural regions, long-haul routes, developing markets | Medium term (2-4 years) |

| Interoperability Gaps Across Vendor Stacks | -2.2% | Global | Medium term (2-4 years) |

| Quantum Hardware Supply Chain and Testbed Scarcity | -1.4% | Global, most acute in markets outside China, Japan, and Switzerland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX For Trusted-Node And QKD Rollouts

Capital intensity remains one of the clearest constraints on near-term expansion in the secure and quantum-safe fiber backbone network market. QKD devices currently cost EUR 200,000 (USD 228,000) per unit, and point-to-point deployments usually require USD 250,000 to USD 500,000 in initial spending before operating costs are added. That pricing keeps early adoption concentrated among sovereign programs, Tier-1 carriers, and regulated financial institutions that can justify dedicated security budgets. In many emerging markets, QKD spending competes directly with existing optical security and backbone modernization budgets, slowing deployment in parts of the Middle East, Africa, and South America. The cost curve should improve as photonic integration advances, but the relief is still medium-term rather than immediate for much of the secure and quantum-safe fiber backbone network market.

Limited Fiber Reach Without Trusted Nodes

Distance remains a technical and economic challenge for the secure and quantum-safe fiber backbone network market. Standard fiber attenuation typically limits QKD to 100 km to 200 km before a trusted node is needed, and each relay introduces a gap because keys are decrypted and re-encrypted at the intermediate point. Extending coverage across continental or transoceanic routes, therefore, requires dense trusted-node infrastructure or satellite QKD, both of which materially increase deployment costs. This burden is particularly heavy on subsea corridors, border-crossing routes, and dispersed national networks where metropolitan density cannot offset the economics of relay placement. Technical progress is evident, but trustless long-distance operation at a broad commercial scale is still several years away, which keeps this restraint active across the secure and quantum-safe fiber backbone network market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Anchored Revenue While Software Closed The Gap

Hardware held 56.29% of the secure and quantum-safe fiber backbone network market share in 2025, making it the largest revenue contributor across current deployments. That lead came from direct procurement of DWDM systems, optical transport platforms, QKD terminals, and trusted-node equipment across backbone programs in China, Europe, the United States, South Korea, and the Middle East. The hardware position is structural because physical quantum links and secure optical nodes must be installed before higher software layers can operate at scale on those routes. Confirmed public and carrier programs, therefore, converted more quickly into hardware bookings than into any other component category. Within the secure and quantum-safe fiber backbone network market, software is projected to expand at a 34.33% CAGR through 2031 as operators adopt crypto-agile key management, FIPS-compliant libraries, and quantum-readiness tools ahead of full hardware migration.

Software is gaining traction because it lowers the first spending threshold while preserving room for later hardware integration. That makes the software layer attractive for carriers and enterprises that want to map cryptographic exposure now and phase capital deployment over time. Services are also expanding as operators seek outside support for migration planning, architecture design, and system integration, especially where in-house quantum cryptography talent is limited. The broader direction of the secure and quantum-safe fiber backbone network market still points toward tighter hardware and software integration, with smaller photonic designs and more flexible control platforms expected to narrow the cost gap over the forecast period.

By Technology: Post-Quantum Cryptography Led Adoption Volume While QKD Expanded On Sovereign Demand

Post-quantum cryptography accounted for a 51.10% share in 2025, making it the leading technology path by current adoption volume. Its position came from immediate deployability enabled by NIST-standardized algorithms and a cost structure that does not depend on dedicated QKD hardware or special-purpose fiber routes. That software-led approach also fits well with hyperscale cloud environments, where large providers have already begun embedding PQC into broader infrastructure security stacks. For buyers who needed faster action against long-retention exposure, PQC offered a practical migration step while physical quantum networking matured. This kept PQC at the center of early procurement across the secure and quantum-safe fiber backbone network market.

QKD is projected to grow at a 33.61% CAGR through 2031 as sovereign and carrier programs move from pilot stages into live backbone deployments. The strongest QKD demand is tied to national infrastructure, defense communications, and high-value financial corridors where information-theoretic protection has strategic appeal. Hybrid quantum-safe solutions are becoming more common because they combine QKD on dedicated or high-priority fiber paths with PQC on wider network segments, thereby reducing the risk of relying entirely on a single approach during an active standards cycle. The pace of government-backed rollouts in 2025 and 2026 showed that the secure and quantum-safe fiber backbone network market is no longer choosing between PQC and QKD in absolute terms, and is increasingly using both where network economics permit.

By Application: Telecommunications Anchored Volume While BFSI Drove Value Growth

Telecommunications led with a 33.23% share in 2025, reflecting the central role of carrier backbones in 5G transport and national network hardening. Operators are now treating quantum-safe controls as part of standard transport design, with PQC protecting broader traffic layers and QKD increasingly used for timing-sensitive or high-assurance links. This made telecommunications the clearest base-load segment for current demand in the secure and quantum-safe fiber backbone network market. Existing carrier assets also lowered deployment friction because operators already owned the fiber, transport systems, and network operations frameworks needed for overlay security upgrades. That combination helped telecommunications remain the largest application even as new use cases expanded.

BFSI is projected to expand at a 31.99% CAGR through 2031 because long-retention transaction records, central bank communications, and cross-border clearing data are especially exposed to delayed decryption risk. The Eurofiber and Colt initiative announced in March 2026, which targeted a quantum-secured corridor linking Amsterdam, London, and Brussels, directly reflected that urgency in major financial centers. Data centers remained another major application as hyperscalers sought quantum-safe interconnects to protect the movement of AI workloads and high-value data across sites. Government and defense, along with healthcare and energy and utilities, are also playing a meaningful role in the secure and quantum-safe fiber backbone network market as security mandates, retention obligations, and operational risk concerns continue to grow.

By End-User Industry: Telecom Operators Held The Largest Share While Hyperscalers Led Growth

Telecom operators held 34.43% share in 2025, supported by dark fiber ownership, carrier-grade operations, and their ability to place QKD equipment at a lower incremental cost than most enterprise buyers. That asset base gave operators a durable advantage in the first wave of deployment across the secure and quantum-safe fiber backbone network market. It also lets carriers package transport, security overlays, and managed operations together, which makes procurement easier for public-sector and enterprise customers. The operator role remains strong because many national programs still rely on incumbent telecom infrastructure for physical deployment and network management. This kept telecom operators at the center of current revenue even as the buyer base broadened.

Hyperscalers and cloud providers are projected to grow at a 35.42% CAGR through 2031 as AI-related traffic, sovereign compliance requirements, and native PQC integration reshape data center interconnect demand. Microsoft moved its own PQC migration target to 2029 and placed quantum-safe readiness within its Secure Future Initiative in June 2026, which showed how quickly large cloud providers are moving ahead of public deadlines. Financial institutions remain a major end-user group because they hold sensitive records for long periods and face clear obligations around transaction integrity and settlement security. Public agencies and critical infrastructure operators are also creating structured procurement pipelines, which means the secure and quantum-safe fiber backbone network market is expanding through program-based adoption rather than short-term reactive spending.

By Network Type: Long-Haul Backbones Dominated Revenue While Subsea Links Set The Pace

Long-haul fiber networks commanded a 39.13% share in 2025 and remained the largest network type, as national backbone programs initially focused on the highest-capacity terrestrial routes. That pattern reflected where traffic density, strategic sensitivity, and public funding overlapped most clearly. The 923 km DemoQuanDT link between Berlin and Bonn demonstrated that carrier-grade QKD could operate over live, long-distance infrastructure and offered a practical model for backbone operators evaluating similar upgrades. Long-haul routes, therefore, stayed at the core of present deployment economics in the secure and quantum-safe fiber backbone network market. Their installed base also made them the first target for overlays that combined optical transport upgrades with post-quantum controls.

Subsea and cross-border fiber links are projected to grow at a 41.00% CAGR through 2031, as these routes carry a significant share of international financial, diplomatic, and intelligence traffic. Colt Technology Services and Ciena demonstrated 800 GbE quantum-safe transmission over 6,900 km between New York and London in June 2026, setting a new commercial benchmark for secure transatlantic performance. Metro fiber networks are also expanding through urban data-center interconnects, including BT Group’s 2024 QKD link between Equinix sites in Canary Wharf and Slough. At the same time, terrestrial networks are improving their ability to carry classical and quantum signals on shared fiber via wavelength-division multiplexing, reducing the need for dedicated dark fiber in selected deployments and broadening the addressable market for the secure and quantum-safe fiber backbone network.

Geography Analysis

North America held a 32.12% share in 2025, making it the largest region in the secure and quantum-safe fiber backbone network market. That lead came from the strongest regulatory framework for PQC migration, especially in the United States, where Executive Order 14412 mandated a defined procurement schedule for planning. The order required high-value federal assets to move to PQC key establishment by December 31, 2030, and to use digital signatures by December 31, 2031, while OMB also framed the transition around USD 7.1 billion in spending over 10 years. That regulatory clarity pulled defense contractors, federal network operators, and regulated financial institutions into active buying cycles across the region. Canada also advanced quantum-safe infrastructure work through critical network initiatives and long-distance communication planning, while Mexico remained at an earlier stage but stood to benefit from North American standards alignment over time.

Europe continued to build one of the most coordinated regional ecosystems in the secure and quantum-safe fiber backbone network market through EuroQCI and related national programs. Germany’s 923 km DemoQuanDT deployment between Berlin and Bonn provided European operators with a live, carrier-grade model for long-distance QKD implementation. Deutsche Telekom T-Labs and Qunnect then achieved quantum teleportation over 30 km of commercial fiber in Berlin in January 2026, which showed that entanglement-based capabilities were moving into real operator environments. The United Kingdom added further weight by committing GBP 125 million (USD 159 million) to quantum networking and by launching a National Quantum Standards Network in June 2026, supported by GBP 10 million (USD 13.22 million) in government funding. Cross-border programs in broader Europe also showed that deployment was no longer limited to the region’s largest western economies.

Asia-Pacific is projected to grow at a 32.89% CAGR through 2031, which makes it the fastest-expanding regional block in the secure and quantum-safe fiber backbone network market. China anchors that trajectory with a national QKD backbone of more than 12,000 km, 145 fiber backbone nodes, and 20 metropolitan networks across 17 provinces and 80 cities. India’s 1,000 km QKD milestone in April 2026 confirmed that national-scale deployment had moved beyond the earliest research stage, while South Korean carriers also pushed quantum security closer to future 6G planning. Middle Eastern markets are emerging through live commercial dark-fiber deployments for sovereign and financial communications, while South America and Africa remain earlier-stage adopters, starting with software overlays before broader hardware rollout.

Competitive Landscape

The secure and quantum-safe fiber backbone network market brings together quantum-native specialists, telecom incumbents, optical transport vendors, and cloud-oriented security providers, creating a broad, still unsettled competitive field. Companies such as ID Quantique SA, LuxQuanta Technologies S.L., QuintessenceLabs Pty Ltd., and Quantum Xchange, Inc. compete alongside larger operator-led and infrastructure-led players, including BT Group plc, Deutsche Telekom AG, SK Telecom Co., Ltd., Colt Technology Services Group Limited, Ciena Corporation, Nokia Corporation, Toshiba Corporation, and Huawei Technologies Co., Ltd. The result is a market where technology depth alone is not enough, because delivery scale, installed fiber access, and compliance readiness also shape contract outcomes. Hardware segments are more concentrated than the broader field, but the commercial model for software overlays and managed services remains open to a broader set of participants. This keeps the secure and quantum-safe fiber backbone network market competitive even as procurement filters become stricter.

Several leading players are using interoperability and deployment partnerships to strengthen their position. Colt Technology Services and Ciena set a high-profile benchmark in June 2026 with 800 GbE quantum-safe transmission across 6,900 km between New York and London, which showed that secure transatlantic performance could be delivered at commercial bandwidth. Eurofiber and Colt then extended the strategic logic in Europe by announcing a cross-carrier QKD corridor for Amsterdam, London, and Brussels, with a clear focus on financial network demand. Juniper Networks has also embedded quantum-safe functionality into existing MACsec and IPsec environments, giving enterprise buyers a lower-friction migration path than a standalone hardware transition.

Another clear pattern is the growing value of certification and alignment with standards in the secure and quantum-safe fiber backbone network market. Vendors with FIPS-compliant implementations or strong alignment with ETSI-style interoperability frameworks are better positioned to win regulated contracts, as buyers increasingly seek auditable migration paths. This favors platform approaches that combine software control, transport compatibility, and security hardware rather than isolated point products. White-space opportunities still exist in Middle Eastern subsea links, Southeast Asian backbone upgrades, and healthcare data center interconnects where demand is forming faster than vendor concentration. At the same time, the secure and quantum-safe fiber backbone network market remains fragmented enough that no single provider or small vendor group appears to control the broader value chain end to end, which leaves room for both specialist innovation and operator-led service expansion.

Secure and Quantum-Safe Fiber Backbone Network Industry Leaders

Toshiba Corporation

ID Quantique SA

Thales S.A.

Huawei Technologies Co., Ltd.

QuintessenceLabs Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The White House signed Executive Order 14412, Securing the Nation Against Advanced Cryptographic Attacks, mandating that US federal agencies migrate high-value assets to PQC key establishment by December 31, 2030, and to digital signatures by December 31, 2031. The companion OMB Memorandum M-26-15 required agency-level PQC Migration Plans within 120 days and required the FAR Council to publish rules requiring covered contractors to comply by December 31, 2030.

- June 2026: Colt Technology Services and Ciena completed an 800 GbE quantum-safe data transmission across 6,900 km of Colt’s transatlantic subsea and terrestrial network between New York and London. The demonstration used Ciena’s WaveLogic 6 Extreme 1.6T encryption solution with NIST-compliant ML-KEM, FIPS 203, PQC algorithms and confirmed that quantum-safe encryption was commercially viable at data-center-scale bandwidths across transoceanic distances.

- May 2026: Terra Quantum and Melita Business successfully deployed a commercial QKD link connecting Melita’s 2 main data centers in Malta across live telecom carrier fiber, the first QKD deployment demonstrated on an existing operational carrier fiber network in Malta, and a validation of QKD viability on inherited infrastructure.

- March 2026: Eurofiber and Colt Technology Services announced at Mobile World Congress 2026 a cross-carrier QKD initiative to deploy a quantum-secured fiber corridor linking the financial districts of Amsterdam, London, and Brussels, creating a multi-operator quantum-safe infrastructure layer specifically designed for banks, trading platforms, and market infrastructure operators.

Global Secure and Quantum-Safe Fiber Backbone Network Market Report Scope

The secure and quantum-safe fiber backbone network market covers fiber backbone networks integrated with post-quantum cryptography (PQC), quantum key distribution (QKD), and hybrid quantum-safe solutions to protect high-capacity optical communications from cyber threats. The market's revenue is generated from secure optical networking hardware, quantum-safe security software, and services such as consulting, quantum-readiness assessments, deployment, integration, and lifecycle support for telecom operators, hyperscalers, financial institutions, public sector agencies, and critical infrastructure operators across terrestrial, metro, long-haul, and subsea fiber networks. The secure and quantum-safe fiber backbone network market report is segmented by component (hardware, software, and services), technology (quantum key distribution, post-quantum cryptography, hybrid quantum-safe solutions), application (telecommunications, data centers, government and defense, BFSI, healthcare, and energy and utilities), end-user industry (telecom operators, hyperscalers and cloud providers, financial institutions, public sector agencies, and critical infrastructure operators), network type (terrestrial fiber networks, metro fiber networks, long-haul fiber networks, and subsea and cross-border fiber links), and geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in value (USD).

| Hardware (Includes Optical Transport Equipment (DWDM/CWDM Systems), Optical Transponders and Muxponders, ROADM (Reconfigurable Optical Add-Drop Multiplexer) Systems, Optical Line Systems (OLS), Coherent Optical Modules, Optical Amplifiers (EDFA/Raman)) |

| Software (Includes Post-Quantum Cryptography (PQC) Software, Quantum-Safe Key Management Systems (KMS), Network Encryption Management Platforms, SDN Controllers with Security Orchestration, Network Management Systems (NMS)) |

| Services (Includes Security Consulting, Quantum-Readiness Assessments, Cryptographic Risk Assessments, Network Security Architecture Design, Deployment and Integration of Quantum-Safe Solutions) |

| Quantum Key Distribution |

| Post-Quantum Cryptography |

| Hybrid Quantum-Safe Solutions |

| Telecommunications |

| Data Centers |

| Government and Defense |

| BFSI |

| Healthcare |

| Energy and Utilities |

| Telecom Operators |

| Hyperscalers and Cloud Providers |

| Financial Institutions |

| Public Sector Agencies |

| Critical Infrastructure Operators |

| Terrestrial Fiber Networks |

| Metro Fiber Networks |

| Long-Haul Fiber Networks |

| Subsea and Cross-Border Fiber Links |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of the Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware (Includes Optical Transport Equipment (DWDM/CWDM Systems), Optical Transponders and Muxponders, ROADM (Reconfigurable Optical Add-Drop Multiplexer) Systems, Optical Line Systems (OLS), Coherent Optical Modules, Optical Amplifiers (EDFA/Raman)) | |

| Software (Includes Post-Quantum Cryptography (PQC) Software, Quantum-Safe Key Management Systems (KMS), Network Encryption Management Platforms, SDN Controllers with Security Orchestration, Network Management Systems (NMS)) | ||

| Services (Includes Security Consulting, Quantum-Readiness Assessments, Cryptographic Risk Assessments, Network Security Architecture Design, Deployment and Integration of Quantum-Safe Solutions) | ||

| By Technology | Quantum Key Distribution | |

| Post-Quantum Cryptography | ||

| Hybrid Quantum-Safe Solutions | ||

| By Application | Telecommunications | |

| Data Centers | ||

| Government and Defense | ||

| BFSI | ||

| Healthcare | ||

| Energy and Utilities | ||

| By End-User Industry | Telecom Operators | |

| Hyperscalers and Cloud Providers | ||

| Financial Institutions | ||

| Public Sector Agencies | ||

| Critical Infrastructure Operators | ||

| By Network Type | Terrestrial Fiber Networks | |

| Metro Fiber Networks | ||

| Long-Haul Fiber Networks | ||

| Subsea and Cross-Border Fiber Links | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the secure and quantum-safe fiber backbone network space?

The secure and quantum-safe fiber backbone network market stood at USD 3.14 billion in 2026 and is projected to reach USD 11.52 billion by 2031, growing at a 29.69% CAGR over 2026-2031.

Which component category currently generates the most revenue?

Hardware led in 2025 with a 56.29% share because backbone deployments still require upfront spending on transport systems, QKD terminals, and trusted-node equipment.

Which technology path is gaining adoption fastest?

QKD is projected to grow fastest at a 33.61% CAGR through 2031, while PQC held the larger 2025 share at 51.10% because it can be deployed immediately through software.

Why are telecom operators still leading demand?

Telecom operators held 34.43% share in 2025 because they already own dark fiber, operate carrier-grade infrastructure, and can deploy quantum-safe overlays at lower incremental cost.

Which network routes are attracting the strongest future investment?

Subsea and cross-border fiber links are projected to grow at a 41.00% CAGR through 2031 because they carry concentrated international financial, diplomatic, and intelligence traffic.

Which region is expanding the fastest?

Asia-Pacific is projected to grow at a 32.89% CAGR through 2031, supported by China's large operational backbone, India's national mission, and broader regional work tied to future 6G readiness.

Page last updated on: